Seed Industry in India Size, Share, Trends and Forecast by Crop Type and Region, 2026-2034

Seed Industry in India Size, Share, Trends & Forecast (2026-2034)

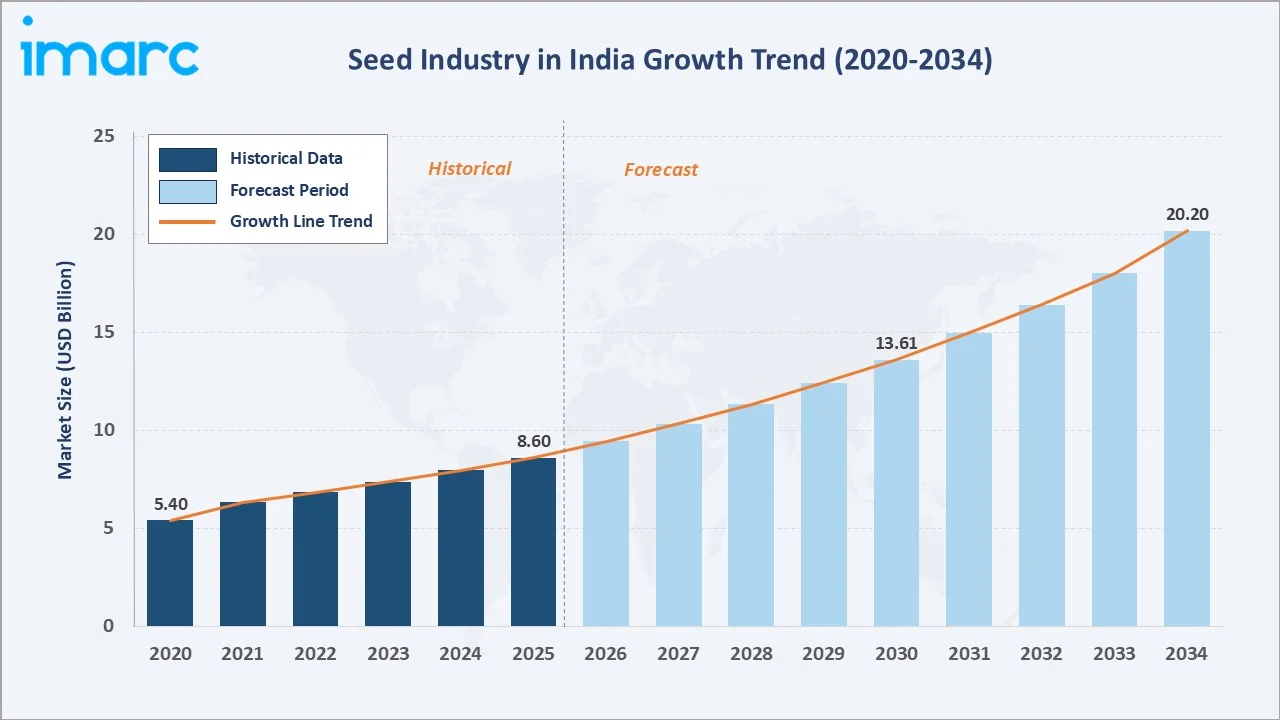

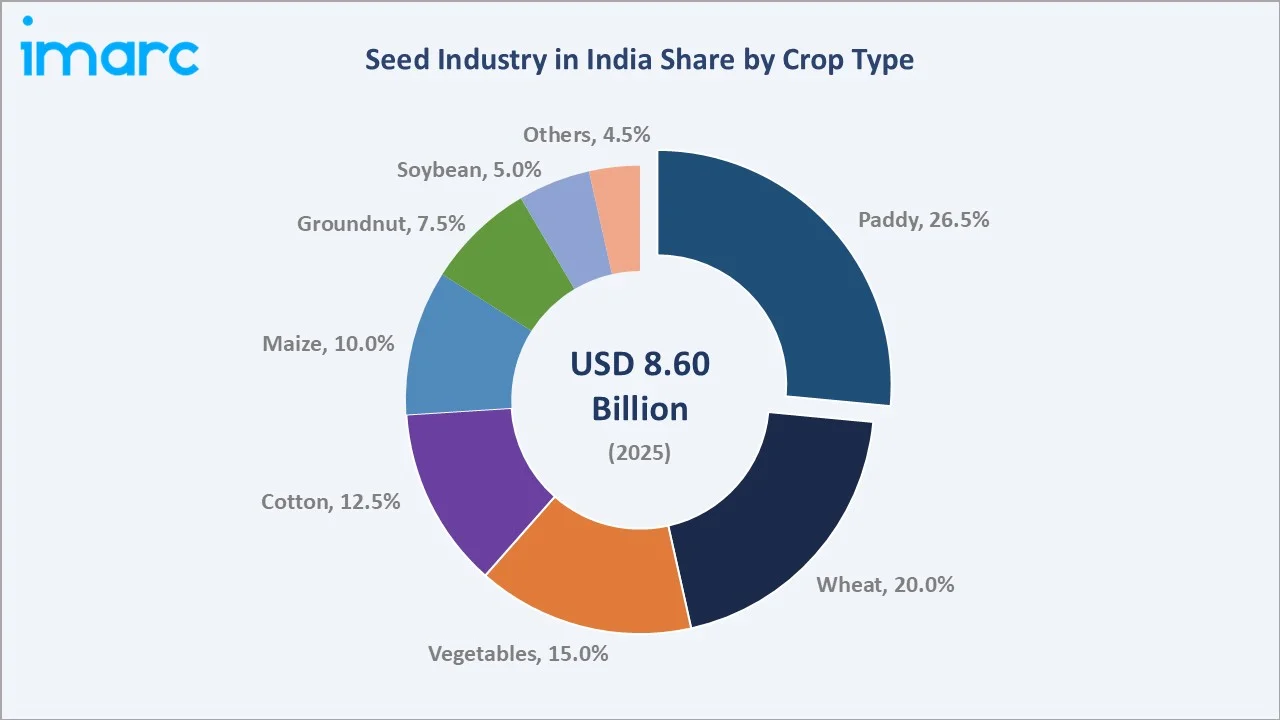

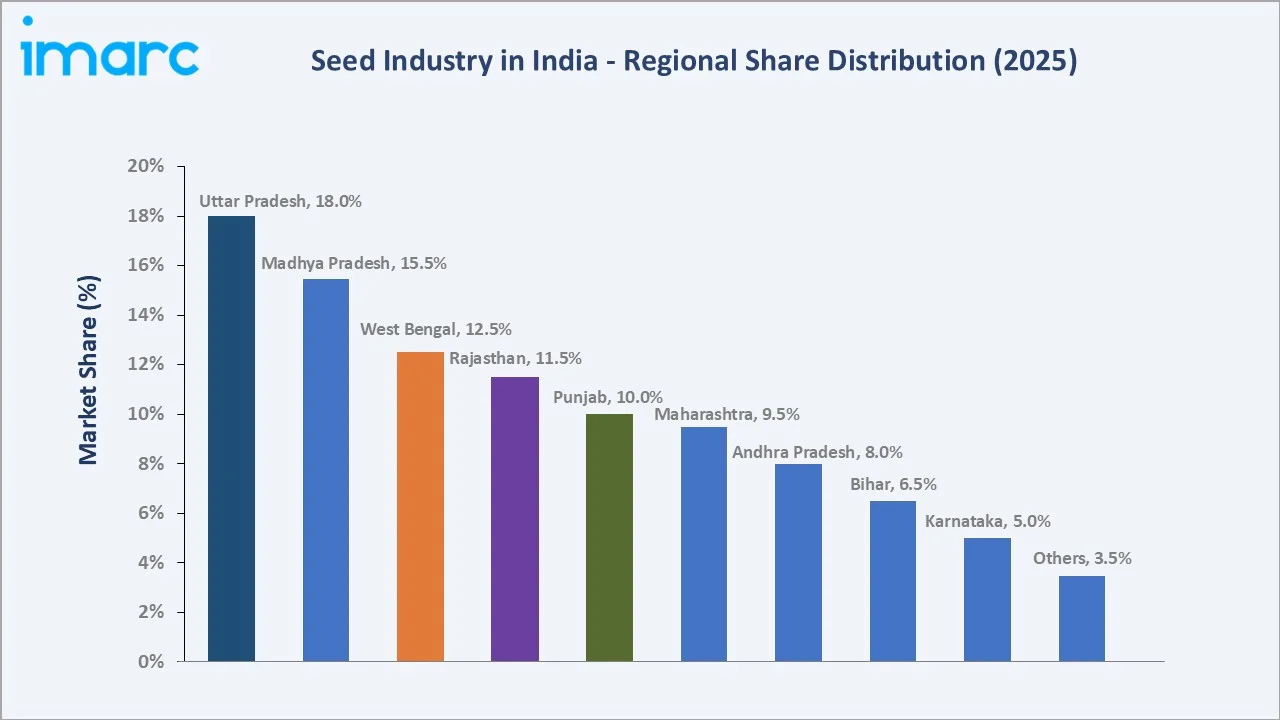

The seed industry in India was valued at USD 8.6 Billion in 2025 and is projected to reach USD 20.2 Billion by 2034, exhibiting a compound annual growth rate of 9.68% during the forecast period 2026-2034. Surging demand for high-yielding hybrid and climate-resilient seed varieties, active public-private collaboration in agricultural R&D, growing commercialization of Indian agriculture, and robust government support through initiatives such as the National Mission on High Yielding Seeds are driving the seed industry in India market growth. Paddy leads crop type segmentation at 26.5% share in 2025, while Uttar Pradesh accounts for 18.0% of regional revenue in 2025, the largest state market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.6 Billion |

|

Forecast Market Size (2034) |

USD 20.2 Billion |

|

CAGR (2026-2034) |

9.68% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Billion |

|

Largest Crop Type |

Paddy (26.5% share, 2025) |

|

Largest Region |

Uttar Pradesh (18.0% share, 2025) |

To get more information on this market, Request Sample

Executive Summary

The seed industry in India is undergoing a structural transformation driven by the convergence of agricultural modernization, biotechnology innovation, and food security imperatives. Valued at USD 8.6 Billion in 2025, the industry is forecast to reach USD 20.2 Billion by 2034 at a CAGR of 9.68%. In February 2025, the Indian government announced the National Mission on High Yielding Seeds with a budget allocation of INR 100 Crore (USD 12.1 Million) for the National Mission on Hybrid Seeds, aiming to strengthen the research ecosystem and ensure the commercial availability of over 100 new seed varieties released since July 2024.

Paddy commands the dominant crop type share at 26.5% in 2025, driven by its role as India's staple food crop, government minimum support price mechanisms, and the growing adoption of hybrid rice varieties that deliver 20-30% higher productivity. Wheat at 20.0% is the second-largest segment, supported by extensive cultivation across the Indo-Gangetic plains and rising demand for climate-resilient wheat varieties.

Uttar Pradesh dominates with an 18.0% share in 2025, led by its vast agricultural base, particularly in paddy and wheat cultivation, alongside strong government seed subsidies and a large farming population. Madhya Pradesh holds 15.5% in 2025, anchored by its position as a major soybean and wheat belt, and West Bengal contributes 12.5%, driven by significant rice production volumes and expanding vegetable seed markets.

Key Market Insights

|

Insight |

Data |

|

Largest Crop Type |

Paddy - 26.5% share (2025) |

|

Leading Region |

Uttar Pradesh - 18.0% share (2025) |

|

Second Largest Region |

Madhya Pradesh - 15.5% share (2025) |

|

Leading Crop Segment (2nd) |

Wheat - 20.0% share (2025) |

|

Top Companies |

Advanta, Kaveri Seeds, Syngenta, Bayer, J K Seeds, Rallis India |

Key Analytical Observations Supporting the Above Data:

- Paddy's 26.5% dominance in 2025 reflects India's position as the world's second-largest rice producer and the government's sustained focus on rice self-sufficiency through seed subsidies and minimum support prices.

- Wheat holds a 20.0% share in 2025, supported by extensive cultivation across Uttar Pradesh, Punjab, and Madhya Pradesh, and the growing introduction of heat-tolerant and rust-resistant wheat varieties.

- Uttar Pradesh's 18.0% dominance in 2025 reflects its dual role as India's largest agricultural state by cultivated area and a major consumer of paddy and wheat seeds across multiple cropping seasons.

- Hybrid seeds commanded approximately 70% of India's commercial seed market revenue in 2024, reflecting farmers' increasing preference for varieties that deliver superior yields and pest resistance.

- The competitive landscape features a blend of multinational corporations such as Bayer and Syngenta alongside domestic leaders like Kaveri Seeds and Nuziveedu Seeds, driving innovation through global partnerships and localized R&D.

Seed Industry in India Overview

Seeds are embryonic plants enclosed in a protective cover with a food reserve, forming the foundational input for India's agricultural sector. The Indian seed industry supports the cultivation of approximately 200 million hectares of cropland across multiple agro-climatic zones, with less than 1% of seeds imported, showcasing India's impressive self-sufficiency in seed production. Hybrid seeds are cultivated on approximately 35 million hectares, while the remainder is dedicated to open-pollinated varieties.

Applications span the entire agricultural spectrum: food grains including rice, wheat, and maize; cash crops such as cotton and sugarcane; oilseeds including soybean and groundnut; and horticultural crops comprising vegetables and fruits. The seed value chain encompasses germplasm research, seed breeding, production, processing, quality certification, and distribution through extensive dealer networks and government outlets.

Macroeconomic enablers include India's growing population exceeding 1.4 billion, declining per capita arable land availability from 0.12 hectares in 2016 to 0.11 hectares in 2020, rising agricultural mechanization, and the government's sustained push toward food security and agricultural export competitiveness.

Market Dynamics

To evaluate market opportunities, Request Sample

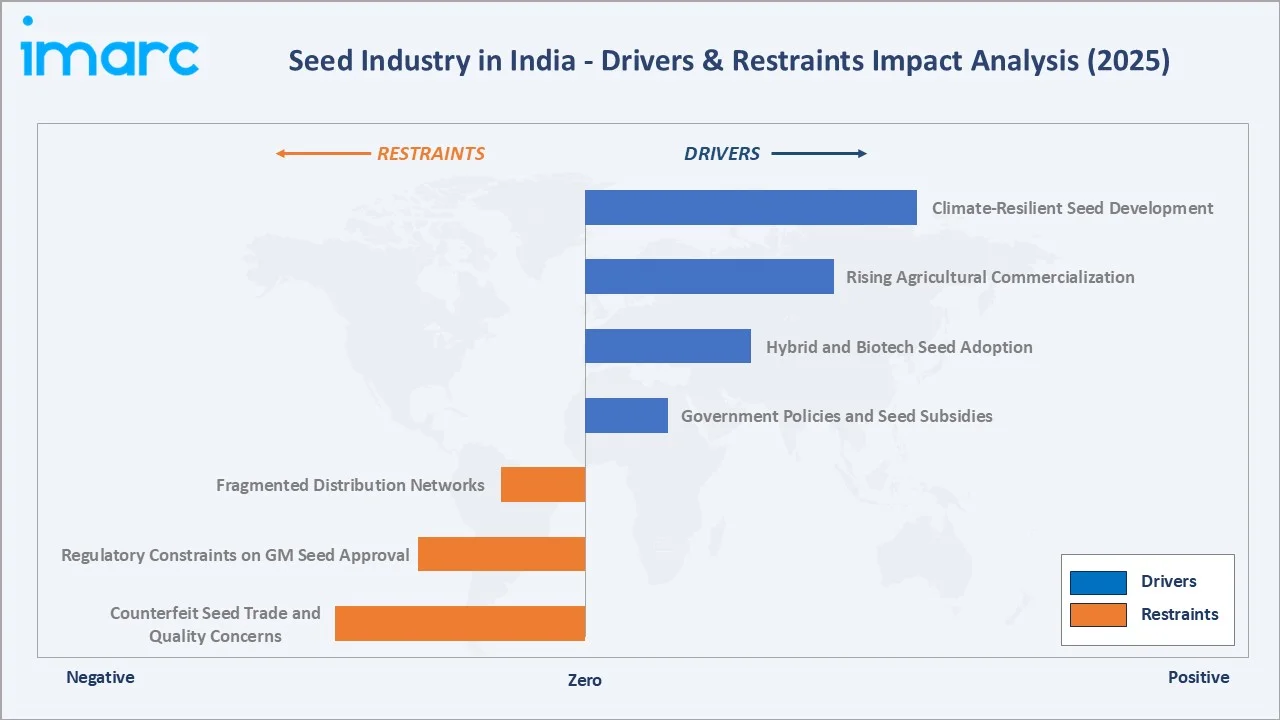

Market Drivers

- Government Policies and Seed Subsidies: The Indian government is the most influential structural driver for the seed industry. In May 2025, the Cabinet Committee on Economic Affairs approved an increase in Minimum Support Prices (MSP) for 14 Kharif crops for the Marketing Season 2025-26. In October 2025, the PM Dhan-Dhaanya Krishi Yojana was launched to enhance agricultural development in 100 districts with low productivity through improvements in seed quality, irrigation, and credit accessibility.

- Hybrid and Biotech Seed Adoption: Hybrid seeds deliver yield increases of 25-40% compared to traditional varieties, driving a sustained shift toward genetically improved cultivars. Bt cotton remains the only commercially approved GM crop in India, yet the introduction of hybrid varieties in rice, maize, and vegetables has significantly boosted farm productivity. In September 2024, PowerPollen and VNR Seeds initiated a pollination-technology pilot in Indian corn-seed production, targeting superior hybrid yields through advanced pollen-capture technology.

- Rising Agricultural Commercialization: India's agricultural sector is rapidly transitioning from subsistence to commercial farming, driven by rising rural incomes, expanding market linkages, and the government's push for crop diversification. The ethanol blending mandate is channeling incremental demand for high-starch maize hybrids suited to industrial processing, while export-oriented rice and cotton cultivation is expanding certified seed adoption.

Market Restraints

- Counterfeit Seed Trade and Quality Concerns: The proliferation of counterfeit and sub-standard seeds in India's fragmented distribution network undermines farmer confidence and reduces productivity. Limited traceability infrastructure in rural markets makes it difficult to verify seed authenticity, particularly for small and marginal farmers.

- Regulatory Constraints on GM Seed Approval: Ongoing regulatory and legal uncertainties around genetically modified food crops have restricted new GM releases beyond Bt cotton, limiting commercial seed innovation in key cereal and oilseed categories.

Market Opportunities

- Climate-Resilient Seed Development: Climate variability is accelerating demand for seeds engineered to withstand drought, flooding, and heat stress, pushing companies and research institutions to invest heavily in advanced breeding and biotechnology. This trend is expanding R&D pipelines, enabling the development of high-yield, climate-resilient varieties that ensure stable agricultural productivity under extreme weather conditions.

- Digital Agriculture and Precision Farming: Integration of AI, IoT, and blockchain technologies is transforming seed quality tracking, supply chain transparency, and farmer advisory services, opening new avenues for seed companies to enhance distribution efficiency and customer engagement.

Market Challenges

- Fragmented Distribution Networks: India's seed supply chain involves multiple intermediaries between production and end-farmer delivery, increasing costs and complicating last-mile distribution in remote rural areas.

- Low Seed Replacement Rates: Many farmers continue to rely on farm-saved seeds rather than certified commercial varieties, limiting market penetration for improved seed products and reducing overall crop productivity.

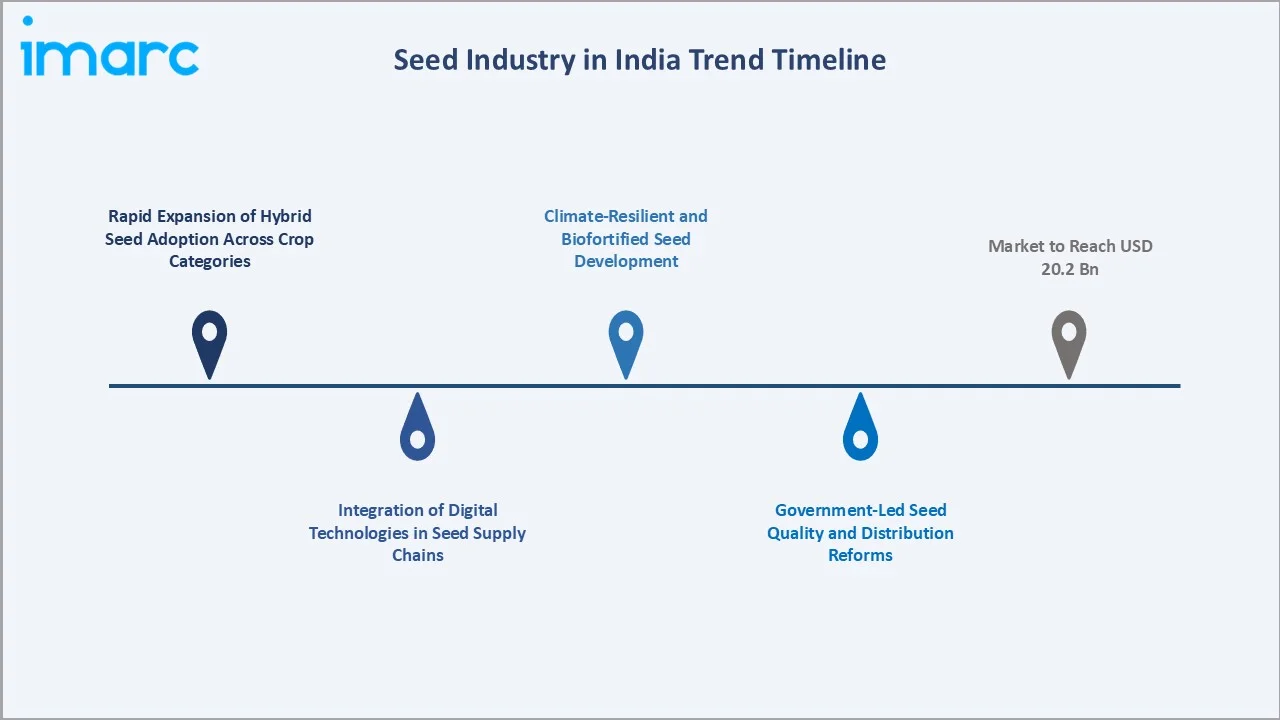

Emerging Market Trends

1. Rapid Expansion of Hybrid Seed Adoption Across Crop Categories

The Indian agricultural sector is witnessing a pronounced shift from open-pollinated varieties toward hybrid seeds across cereals, oilseeds, and vegetables. Hybrids commanded approximately 70.1% of India's seed market revenue in 2024, delivering 25-40% higher yields compared to traditional varieties. This adoption is being driven by rising farmer awareness, improved seed distribution networks, and government programs that subsidize hybrid seed purchases for smallholder farmers.

2. Integration of Digital Technologies in Seed Supply Chains

Seed companies are investing in tamper-proof holograms and QR codes linked to blockchain registries to safeguard brand equity and combat counterfeiting. Digital platforms are providing real-time advisory services to farmers, enabling data-driven seed selection based on soil conditions, climate forecasts, and crop performance analytics. This digitalization is improving supply chain transparency and reducing intermediary leakages in rural distribution.

3. Government-Led Seed Quality and Distribution Reforms

In February 2025, the Indian government launched the National Mission on High Yielding Seeds to strengthen research ecosystems and ensure the availability of over 100 new seed varieties. The PM Dhan-Dhaanya Krishi Yojana, launched in October 2025, targets 100 low-productivity districts with improvements in seed quality, irrigation, and credit accessibility, directly supporting the industry's expansion into underserved regions.

4. Climate-Resilient and Biofortified Seed Development

With climate change posing mounting challenges to Indian agriculture, seed companies and public research institutions are focusing on developing drought-tolerant, flood-resistant, and heat-adapted varieties. The Clean Plant Programme, approved in August 2024 with funding of INR 1,765.67 Crore (USD 211.2 Million), focuses on hybrid seed multiplication, quality assurance, and molecular breeding to enhance climate resilience across key crop categories.

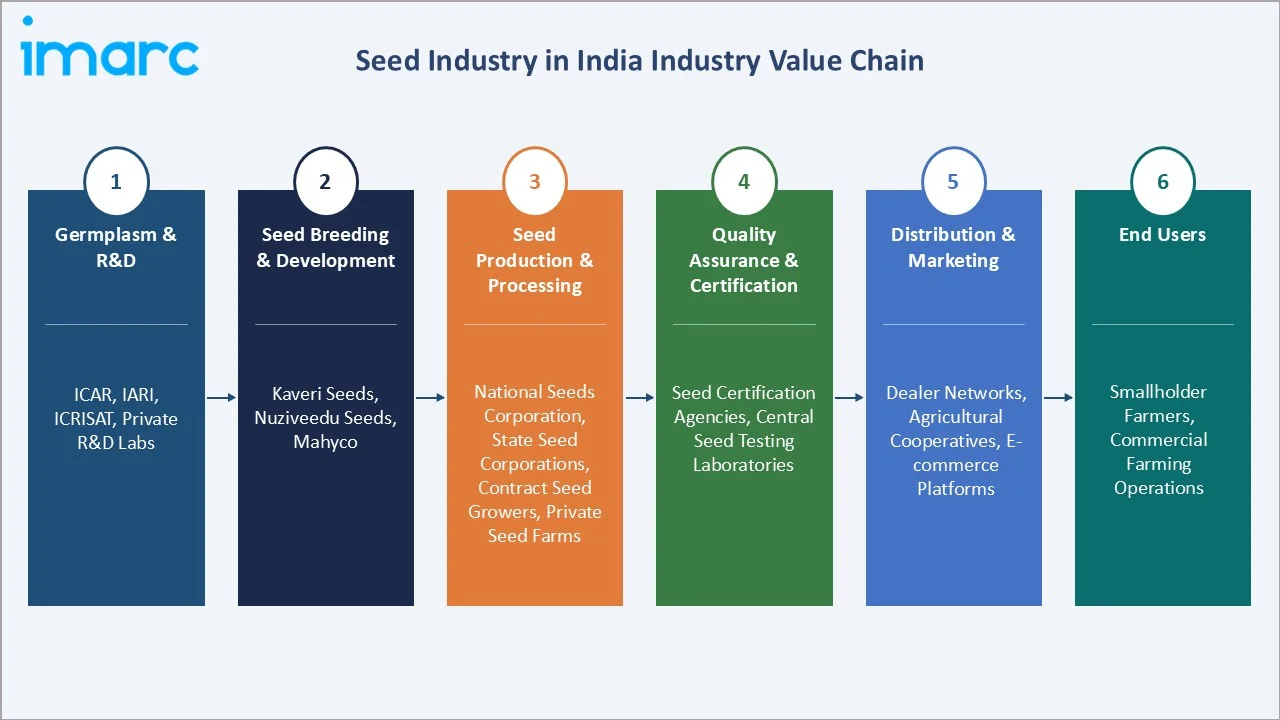

Industry Value Chain Analysis

The Indian seed industry value chain spans six integrated stages from germplasm research through end-farmer delivery. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements.

|

Stage |

Key Players / Examples |

|

Germplasm & R&D |

ICAR, IARI, State Agricultural Universities, ICRISAT, IRRI, Private R&D Labs |

|

Seed Breeding & Development |

Kaveri Seeds, Nuziveedu Seeds, Mahyco, Advanta Seeds, Syngenta, Bayer CropScience |

|

Seed Production & Processing |

National Seeds Corporation, State Seed Corporations, Contract Seed Growers, Private Seed Farms |

|

Quality Assurance & Certification |

Seed Certification Agencies, Central Seed Testing Laboratories |

|

Distribution & Marketing |

Dealer Networks, Agricultural Cooperatives, E-commerce Platforms, Government Seed Outlets |

|

End Users |

Smallholder Farmers, Commercial Farming Operations, Export-Oriented Producers |

Private seed companies occupy the highest strategic value position in the Indian seed value chain, integrating germplasm access, breeding expertise, and extensive dealer networks into comprehensive seed solutions. However, public institutions including ICAR, IARI, and State Agricultural Universities remain critical for foundational research and pre-breeder material that underpins private-sector hybrid development programs.

Technology Landscape in the Indian Seed Industry

Genomics and Biotechnology: Marker-Assisted Selection and Genome Editing

India’s seed breeding programs are undergoing a genomics-driven shift. Marker-Assisted Selection (MAS) is now standard at Kaveri Seeds and Mahyco, reducing trait introgression from ten seasons to three. CRISPR-Cas9 genome editing, enabled by India’s 2022 SDN-1 and SDN-2 exemptions, is accelerating drought-tolerant and disease-resistant variety development across rice, wheat, and vegetable crops.

Artificial Intelligence and Predictive Breeding

AI-powered genomic prediction models and UAV-based phenotyping platforms enable Indian breeders to evaluate thousands of plots simultaneously, compressing trial cycles and improving yield trait selection accuracy. Advanta Seeds and Syngenta India represent the vanguard.

Digital Distribution and AgriTech Platforms

India’s seed distribution stack is layered: agri-commerce platforms including DeHaat, AgroStar, and BigHaat for direct-to-farmer fulfilment, the National Seed Portal for certified lot traceability, and the Government’s Agri Stack for verified farmer identity and targeted product delivery.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Crop Type |

Paddy |

26.50% |

2025 |

|

Region |

Uttar Pradesh |

18.00% |

2025 |

By Crop Type

To access detailed market analysis, Request Sample

Paddy commands a 26.5% majority share in 2025, reflecting its critical role as India's staple food crop and the extensive government support for rice production through minimum support prices, seed subsidies, and the National Food Security Mission. India is the world's second-largest rice producer, cultivating paddy across multiple states, and the growing adoption of hybrid rice varieties that deliver shorter maturity periods and mechanization compatibility is further strengthening paddy seed demand.

Wheat at 20.0% in 2025 is the second-largest crop segment, driven by extensive cultivation across the Indo-Gangetic plains covering Uttar Pradesh, Punjab, Madhya Pradesh, and Rajasthan. Advancements in heat-tolerant and rust-resistant wheat varieties are helping farmers maintain yields despite rising temperatures during the critical grain-filling stage. Vegetables hold a 15.0% share, emerging as one of the fastest-growing segments driven by hybrid seed adoption, rising urban food demand, and protected cultivation growth. Cotton at 12.5% remains significant, with Bt cotton hybrids dominating this segment. Maize at 10.0% is growing steadily, fuelled by poultry feed sector expansion and the ethanol blending mandate. Groundnut (7.5%), soybean (5.0%), and others (4.5%) represent the remaining market segments.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Uttar Pradesh |

18.0% |

Paddy & wheat cultivation hub, strong government seed subsidies, large farming population |

|

Madhya Pradesh |

15.5% |

Soybean and wheat belt, expanding hybrid seed adoption, National Food Security Mission focus |

|

West Bengal |

12.5% |

Major rice-producing state, jute seed demand, growing vegetable seed market |

|

Rajasthan |

11.5% |

Groundnut and mustard cultivation, arid-zone seed R&D, dryland farming innovation |

|

Punjab |

10.0% |

Wheat and paddy heartland, high seed replacement rate, advanced farm mechanization |

|

Maharashtra |

9.5% |

Cotton seed hub, soybean and sugarcane, dense seed processing infrastructure |

|

Andhra Pradesh |

8.0% |

Paddy and cotton cultivation, strong hybrid seed adoption, seed export activity |

|

Bihar |

6.5% |

Maize and wheat production, growing certified seed adoption, government extension programs |

|

Karnataka |

5.0% |

Maize, cotton, and vegetables, emerging biotech seed R&D, Syngenta production facility |

|

Others |

3.5% |

Emerging seed demand from northeastern states and Union territories |

Uttar Pradesh commands an 18.0% share in 2025, the most dominant regional position in India's seed industry. The state's vast and diverse agricultural activities, particularly paddy and wheat cultivation, contribute significantly to the demand for quality seeds. With a large farming population relying on agricultural income, the adoption of high-yielding seed varieties is critical for improving productivity. UP also benefits from robust government initiatives, including subsidies and loans for seeds, alongside a strong infrastructure for agricultural marketing and distribution.

Madhya Pradesh, with 15.5% in 2025, is anchored by its position as India's leading soybean-producing state and a major wheat belt, with expanding hybrid seed adoption driven by the National Food Security Mission and state-level agricultural programs. West Bengal at 12.5% is a significant rice-producing state where jute seed demand and growing vegetable seed markets add further diversity. Rajasthan at 11.5% leverages groundnut and mustard cultivation, with arid-zone seed R&D innovations supporting dryland farming productivity. Punjab at 10.0% represents one of India's most mechanized agricultural regions, with high seed replacement rates in wheat and paddy driving premium seed demand.

Competitive Landscape

|

Company |

Brand/Parent |

Position |

Core Strength |

|

Advanta Seeds |

UPL Limited |

Leader |

Hybrid seeds across corn, rice, sorghum, vegetables |

|

Kaveri Seeds |

Kaveri Seeds |

Leader |

Cotton, rice, maize hybrids; strong R&D pipeline |

|

Syngenta India |

Syngenta Group |

Leader |

Hybrid corn, rice, vegetables; crop protection integration |

|

Bayer CropScience |

Bayer AG |

Leader |

Bt cotton, corn hybrids; digital farming solutions |

|

Nuziveedu Seeds LTD |

Nuziveedu |

Challenger |

Cotton, rice, maize; extensive dealer network |

|

Rallis India Limited |

Tata Group |

Challenger |

Crop care and seeds; rural distribution strength |

|

J K Seeds |

J K Agri Genetics |

Emerging |

Cotton, maize, vegetables; regional market focus |

|

Pioneer |

Corteva Agriscience |

Emerging |

Advanced corn and soybean hybrids; biotech traits |

The seed industry in India competitive landscape is characterized by a fragmented market structure where the top five companies hold approximately 29% of revenue, creating space for regional breeders that specialize in niche agro-climatic zones. Multinational corporations leverage deep R&D pipelines and proprietary trait technologies, while domestic leaders like Kaveri Seeds and Nuziveedu Seeds capitalize on intimate agro-ecological knowledge and extensive dealer networks across rural India.

Competition is intensifying through investments in hybrid seed development, digital farming platforms, and strategic partnerships with public research institutions. Companies are focusing on expanding product portfolios across climate-resilient, biofortified, and high-yielding varieties to capture growing farmer demand for premium seed solutions.

Key Company Profiles

Advanta Seeds (UPL Limited)

Advanta Seeds is one of India’s leading hybrid seed companies, operating as a subsidiary of UPL Limited with a diverse portfolio spanning corn, rice, sorghum, sunflower, and vegetable seeds. With a presence across India and multiple emerging markets, Advanta leverages UPL’s extensive agri-input distribution infrastructure to deliver hybrid seed products to smallholder and commercial farmers across a wide range of agro-climatic zones.

- Product & Platform Portfolio: Hybrid corn seeds, hybrid rice varieties, sorghum hybrids, sunflower hybrids, vegetable seed range (okra, hot pepper, watermelon).

- Recent Developments: In July 2025, Advanta Seeds secured Plant Variety Protection (PVP) for its widely popular hybrid okra variety, Raadhika, reinforcing its innovation credentials and ensuring continued farmer access to superior okra genetics with enhanced disease resistance and higher yields.

Kaveri Seed Company

Kaveri Seed Company is one of India’s largest domestic hybrid seed companies, with established strengths in cotton, rice, and maize hybrids. The company operates an extensive R&D pipeline supported by multiple breeding stations across key agricultural states, enabling the rapid development and commercialization of regionally adapted hybrid varieties for India’s diverse farming landscape.

- Product & Platform Portfolio: Hybrid cotton seeds (ATM brand), hybrid rice, hybrid maize, hybrid sunflower, vegetable seeds including tomato, chilli, and brinjal.

- Recent Developments: In 2025, Kaveri Seed Company announced a strategic shift in its business model, aiming to strengthen its non-cotton seed portfolio. The move comes as part of the company's efforts to reduce its dependence on cotton seeds and target double-digit growth along with margin recovery.

Syngenta India

Syngenta India, a subsidiary of the global Syngenta Group (ChemChina), combines crop protection and seed businesses to offer integrated agricultural solutions. With a strong hybrid corn, rice, and vegetable seed portfolio, Syngenta targets both commercial farming operations and smallholder segments, leveraging its global R&D pipeline and proprietary seed treatment technologies to deliver differentiated seed products.

- Product & Platform Portfolio: NK brand hybrid corn and sunflower, hybrid rice, vegetable seeds (CLAUSE brand – tomato, pepper, cucurbits), fungicide-treated seeds, integrated crop protection solutions.

- Recent Developments: In March 2024, Syngenta Vegetable Seeds inaugurated a new Seed Health Lab in Hyderabad, India on Thursday, strengthening the company’s continued investment in quality control capabilities. The lab is one of the most advanced seed testing facilities in the world and is India’s first dedicated seed health lab which will serve growers in India, Asia Pacific region and beyond.

Market Concentration Analysis

The seed industry in India exhibits low-to-moderate market concentration, with the top five companies collectively holding approximately 29% of total revenue in 2025, reflecting the industry’s highly fragmented structure. This fragmentation is characteristic of India’s agricultural input market, where agro-climatic diversity across more than 15 major zones creates demand for locally adapted varieties that regional breeders are well-positioned to supply. National-level seed companies must compete alongside hundreds of state-level and regional seed producers who possess deep agronomic knowledge and established farmer relationships in their respective geographies.

The Indian seed market is undergoing gradual consolidation driven by escalating hybrid seed R&D costs, digital platform investment requirements, and increasingly complex regulatory compliance for new variety registration under the Seeds Act. Multinational corporations including Syngenta and Bayer leverage global R&D pipelines and proprietary trait technologies to maintain premium positioning, while domestic leaders like Kaveri Seeds and Nuziveedu Seeds compete through intimate agro-ecological knowledge and extensive rural dealer networks.

Investment & Growth Opportunities

Fastest-Growing Segments

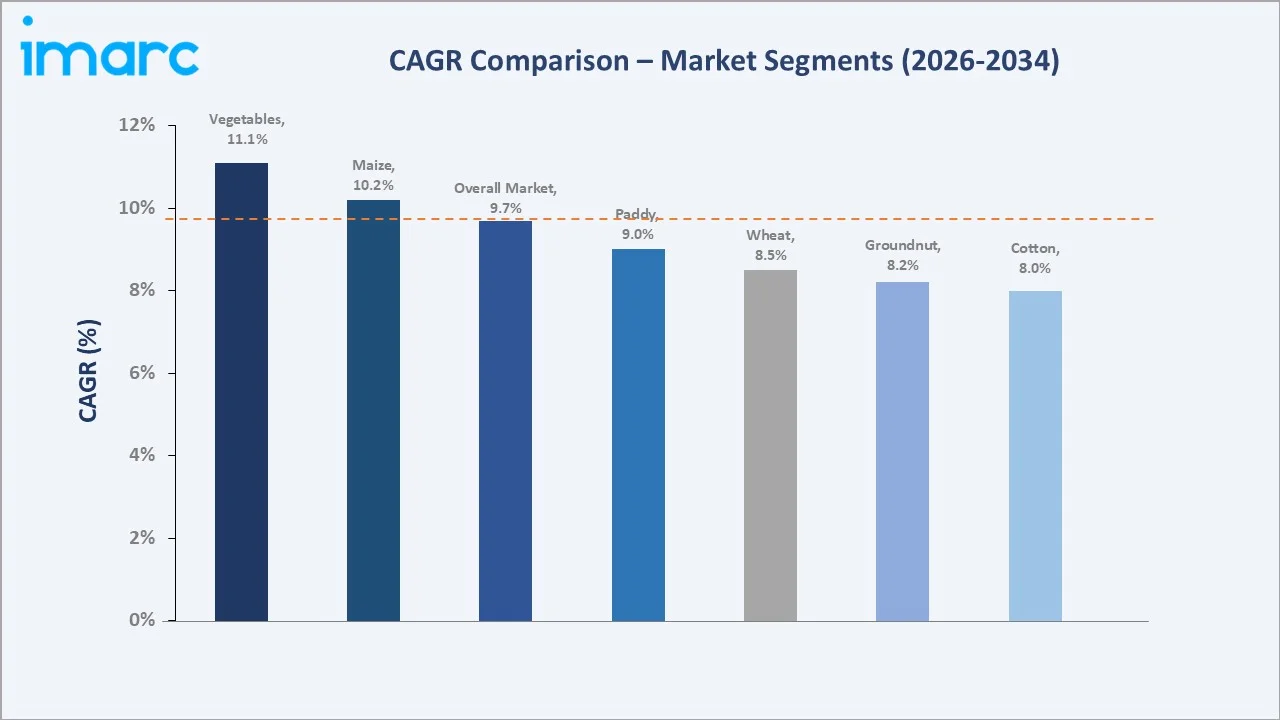

Vegetable seeds represent the fastest-growing crop category at approximately 11.1% CAGR through 2034, driven by hybrid seed adoption in protected cultivation, rising urban food demand, and increasing export-oriented horticulture activity. Climate-resilient seed varieties – drought-tolerant, flood-resistant, and heat-adapted cultivars – are the highest-priority R&D investment category for both public institutions and private seed companies, commanding premium pricing that elevates segment revenue growth well above volume trends. Maize hybrid seeds are growing steadily at approximately 10.2% CAGR, fuelled by the ethanol blending mandate, poultry feed sector expansion, and growing industrial starch demand, making corn hybrids one of the most strategically attractive investment segments in the Indian seed industry through 2034.

Emerging Market Expansion

Gene editing technologies, particularly CRISPR-Cas9 applications for developing non-GM improved varieties, represent an emerging regulatory-friendly innovation pathway that bypasses India’s stringent GM crop approval constraints, opening new avenues for precision trait development in key cereals and oilseeds. Digital agriculture integration – AI-powered seed recommendation platforms, blockchain-enabled seed traceability systems, and direct-to-farmer e-commerce channels – is creating new routes to market that reduce intermediary dependency and enhance farmer engagement.

Venture & Private Investment Trends

Venture capital activity in India’s agri-tech ecosystem is increasingly targeting seed-tech platforms, precision breeding start-ups, and digital seed distribution models, with agri-tech venture investment in India growing significantly through 2024-2025. Domestic private equity funds are increasing exposure to organized seed distribution platforms and input retail networks as consolidation opportunities emerge in India’s fragmented seed distribution landscape.

Future Market Outlook (2026-2034)

The seed industry in India is forecast to expand from USD 8.6 Billion in 2025 to USD 20.2 Billion by 2034 at a compound annual growth rate of 9.68%, a near-doubling of market value driven by hybrid seed penetration expansion, government-led quality reform programs, and the structural shift toward climate-resilient agriculture. Three transformative forces will reshape the seed industry through 2034: digital traceability platforms that combat counterfeiting and enhance supply chain efficiency; gene-editing technologies that bypass traditional GM regulatory constraints; and the expansion of protected cultivation systems that drive premium vegetable seed demand.

By 2034, the Indian seed industry is expected to have completed its transition from a primarily volume-driven commodity market to a technology-intensive, quality-differentiated industry. The competitive landscape will be shaped by companies that successfully integrate biotechnology innovation, digital distribution platforms, and farmer-centric advisory services to deliver measurable productivity gains across India's diverse agro-climatic zones.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted with seed industry stakeholders including product directors at seed companies, agricultural researchers, government policy officials, seed distribution network managers, and institutional investors in agricultural technology. Primary insights validated market sizing, segmentation estimates, technology adoption timelines, and competitive positioning assessments.

Secondary Research

Secondary sources include ICAR and IARI research publications, Ministry of Agriculture and Farmers' Welfare policy documents, Press Information Bureau announcements, National Seeds Corporation data, State Seed Certification agency reports, company annual reports, and trade publications including the Indian Journal of Agricultural Sciences and Agriculture Today.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, agricultural output data, seed replacement rates, and historical market evolution patterns. Scenario analysis was performed to account for macroeconomic uncertainty and policy variability.

Seed Industry in India Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Billion |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Crop Types Covered |

Paddy, Wheat, Vegetables, Cotton, Maize, Groundnut, Soybean, Others |

|

Regions Covered |

Uttar Pradesh, Madhya Pradesh, West Bengal, Rajasthan, Punjab, Maharashtra, Andhra Pradesh, Bihar, Karnataka, Others |

|

Companies Covered |

Advanta Seeds, Kaveri Seeds, Syngenta India, Bayer CropScience, Nuziveedu Seeds LTD, Rallis India Limited, J K Seeds, Pioneer, etc. |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (editable PPT/Word on special request) |

Frequently Asked Questions About the Seed Industry in India Market Report

The seed industry in India was valued at USD 8.6 Billion in 2025, driven by hybrid seed adoption, government subsidies, and agricultural commercialization.

The industry is projected to reach USD 20.2 Billion by 2034, growing at a compound annual growth rate of 9.68% during 2026-2034, driven by technology-led seed innovation, climate-resilient variety development, and expanding government support programs.

Paddy leads with a 26.5% share in 2025, driven by India's position as the world's second-largest rice producer, extensive government support through minimum support prices, and the growing adoption of high-yielding hybrid rice varieties across multiple states.

Uttar Pradesh leads with an 18.0% share in 2025, anchored by its vast agricultural base, major paddy and wheat cultivation, large farming population, and robust government seed subsidy programs.

Key drivers include government policies and seed subsidies, growing hybrid and biotech seed adoption, agricultural commercialization, rising food security imperatives, digital technology integration, and increasing public-private collaboration in seed research and development.

Major challenges include counterfeit seed trade, regulatory constraints on GM crop approval, climate vulnerability, fragmented distribution networks, and low seed replacement rates among smallholder farmers in several regions.

Leading companies include Advanta Seeds (UPL), Kaveri Seed Company, Syngenta India, Bayer CropScience, Nuziveedu Seeds, Rallis India Limited, J K Seeds, and Pioneer.

Vegetables is among the fastest-growing crop segments, driven by hybrid seed adoption, rising urban food demand, and the expansion of protected cultivation systems. The protected cultivation seed segment is forecast to expand at approximately 11.08% CAGR through 2030.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)