Africa E-Learning Market Size, Share, Trends and Forecast by Sector, Product Type, Technology, and Region 2026-2034

Africa E-Learning Market Size, Share, Trends & Forecast (2026-2034)

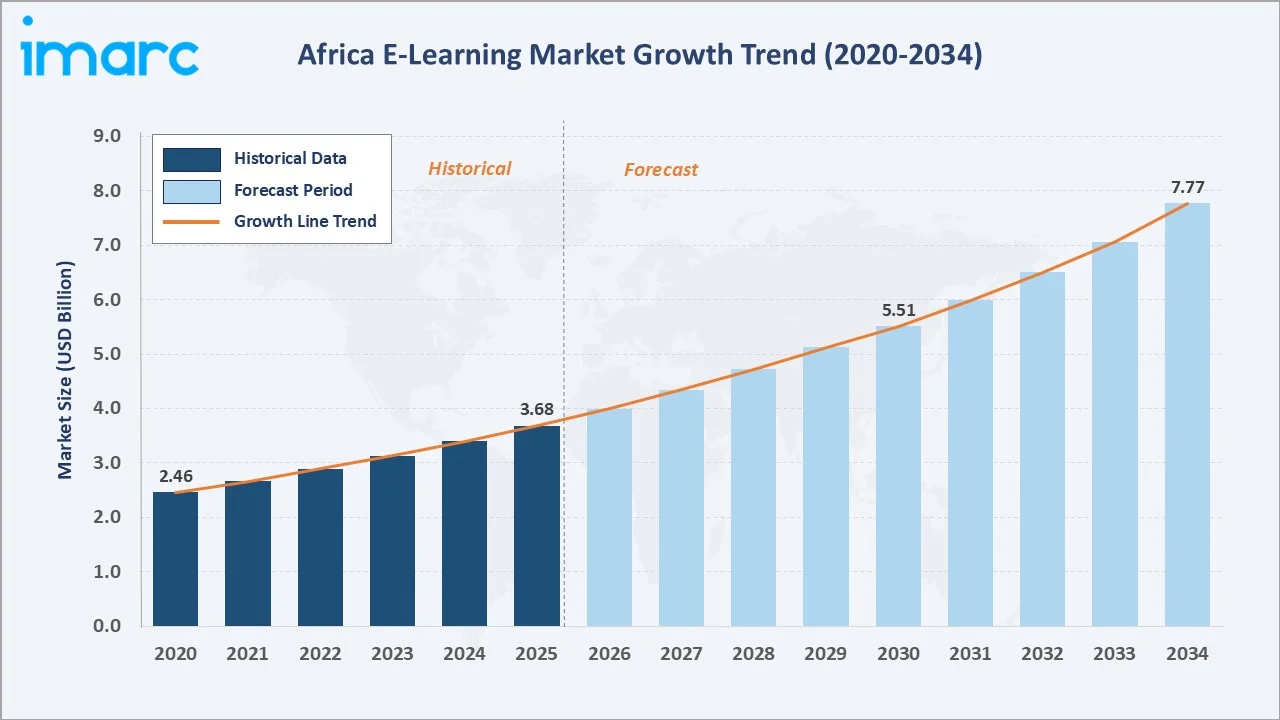

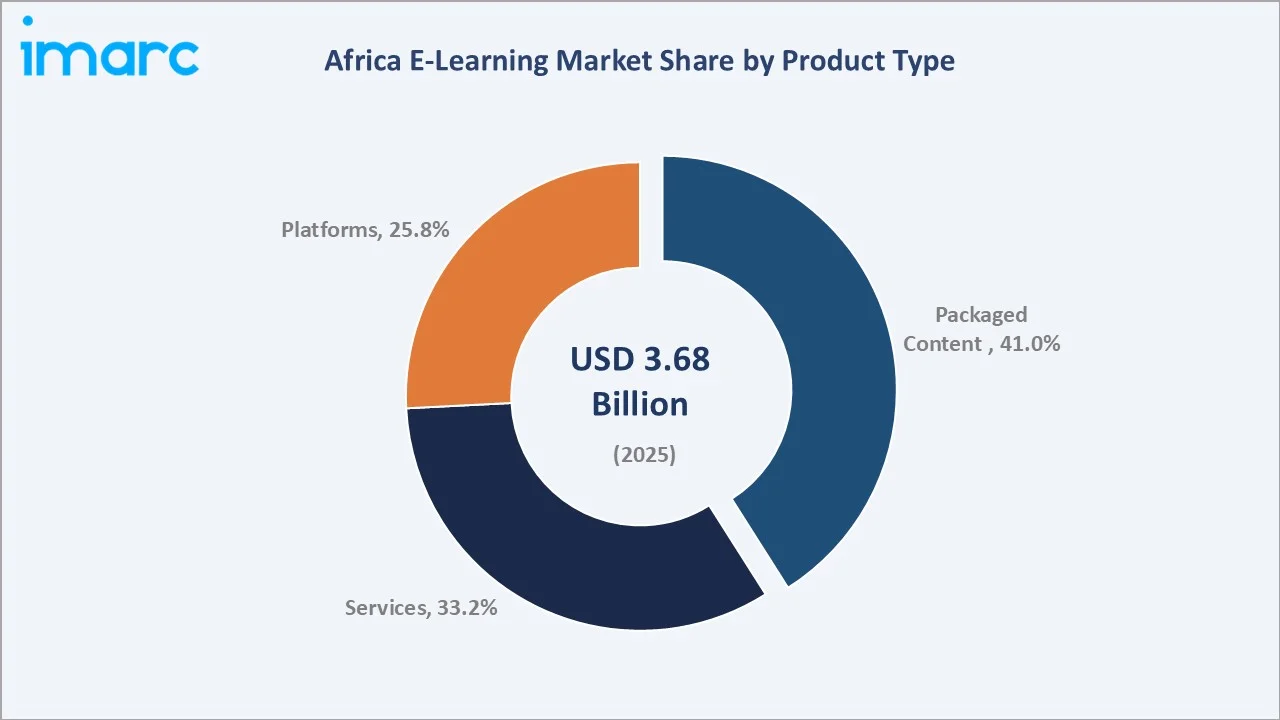

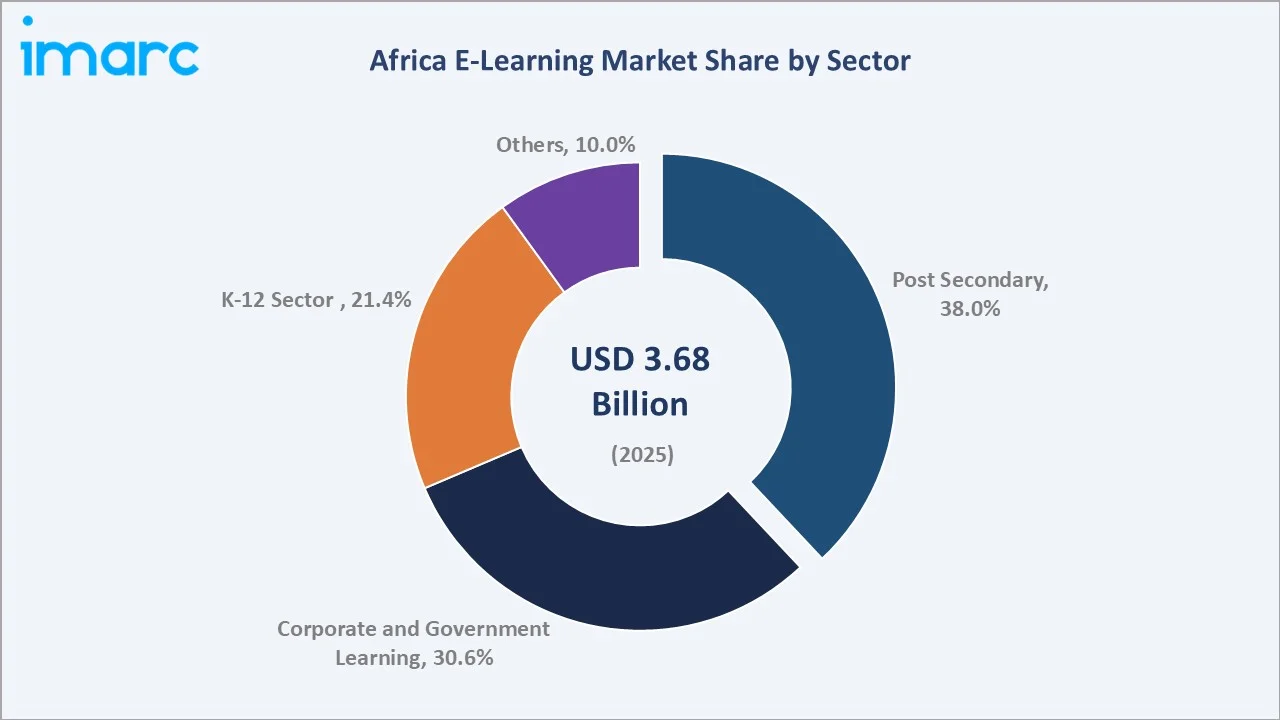

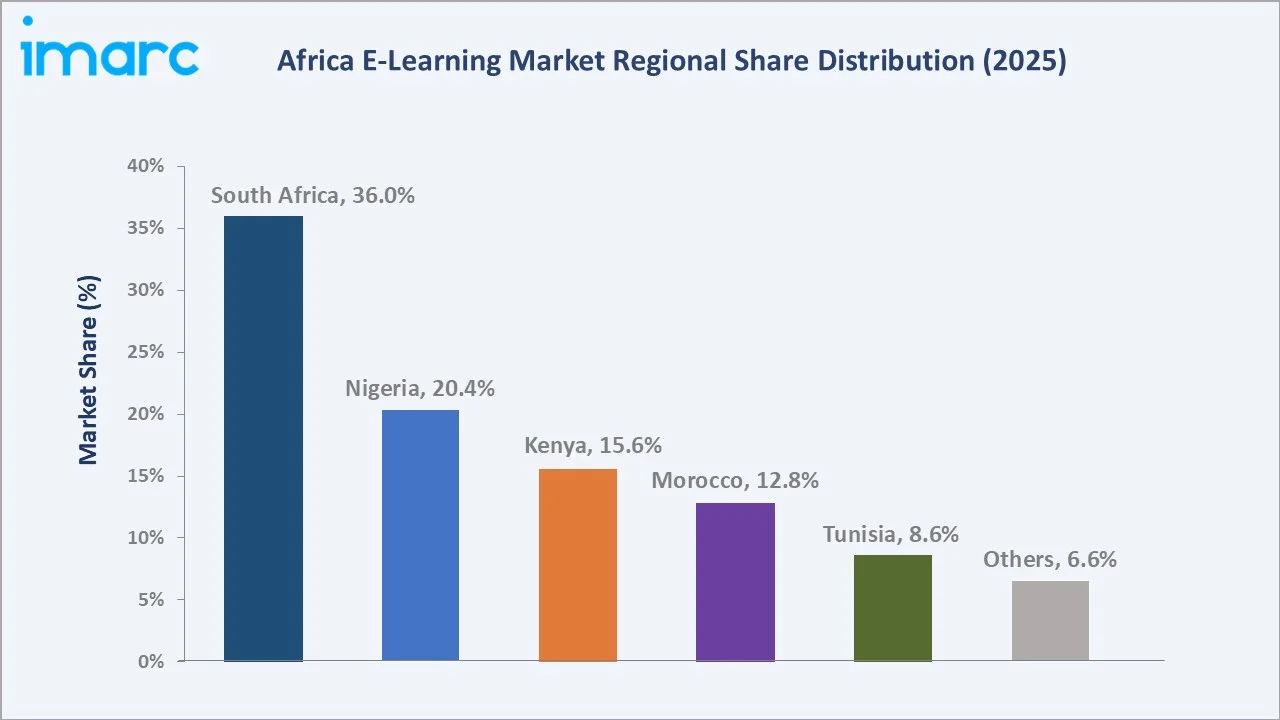

The Africa e-learning market size was valued at USD 3.68 Billion in 2025 and is projected to reach USD 7.77 Billion by 2034, exhibiting a CAGR of 8.41% during the forecast period 2026-2034. The market's strong growth is underpinned by rising mobile internet penetration across Sub-Saharan and North Africa, a rapidly expanding young learner population exceeding 60% of the continent's 1.4 billion people below age 25, and accelerating government-led digital education mandates. Packaged Content leads product type with a 41.0% share in 2025, and Post-Secondary dominates the sector segment at 38.0%. South Africa commands the largest regional share at 36.0% in 2025, followed by Nigeria at 20.4% and Kenya at 15.6%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.68 Billion |

|

Forecast Market Size (2034) |

USD 7.77 Billion |

|

CAGR (2026-2034) |

8.41% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South Africa (36.0% share, 2025) |

|

Fastest Growing Region |

Kenya (mobile-first EdTech adoption) |

|

Leading Product Type |

Packaged Content (41.0%, 2025) |

|

Leading Sector |

Post-Secondary (38.0%, 2025) |

To get more information on this market, Request Sample

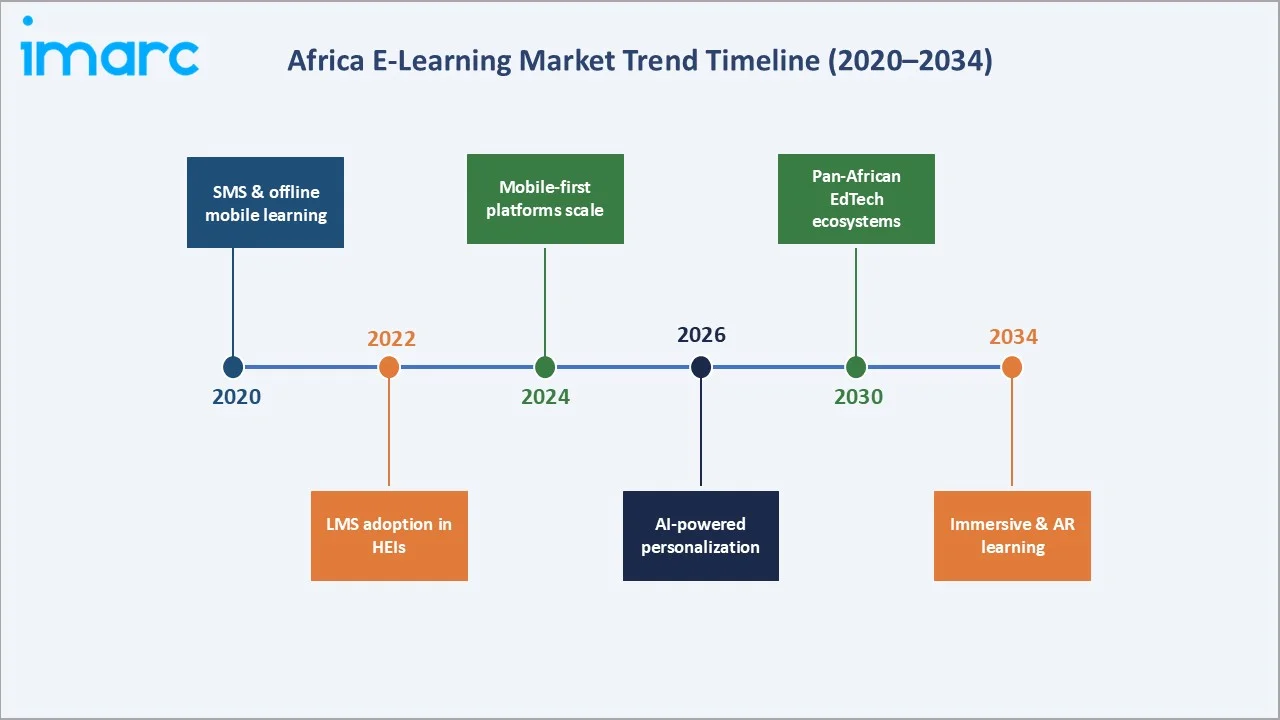

The Africa e-learning market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by mobile internet proliferation, government digital education initiatives, and the rapid rise of indigenous African EdTech ecosystems.

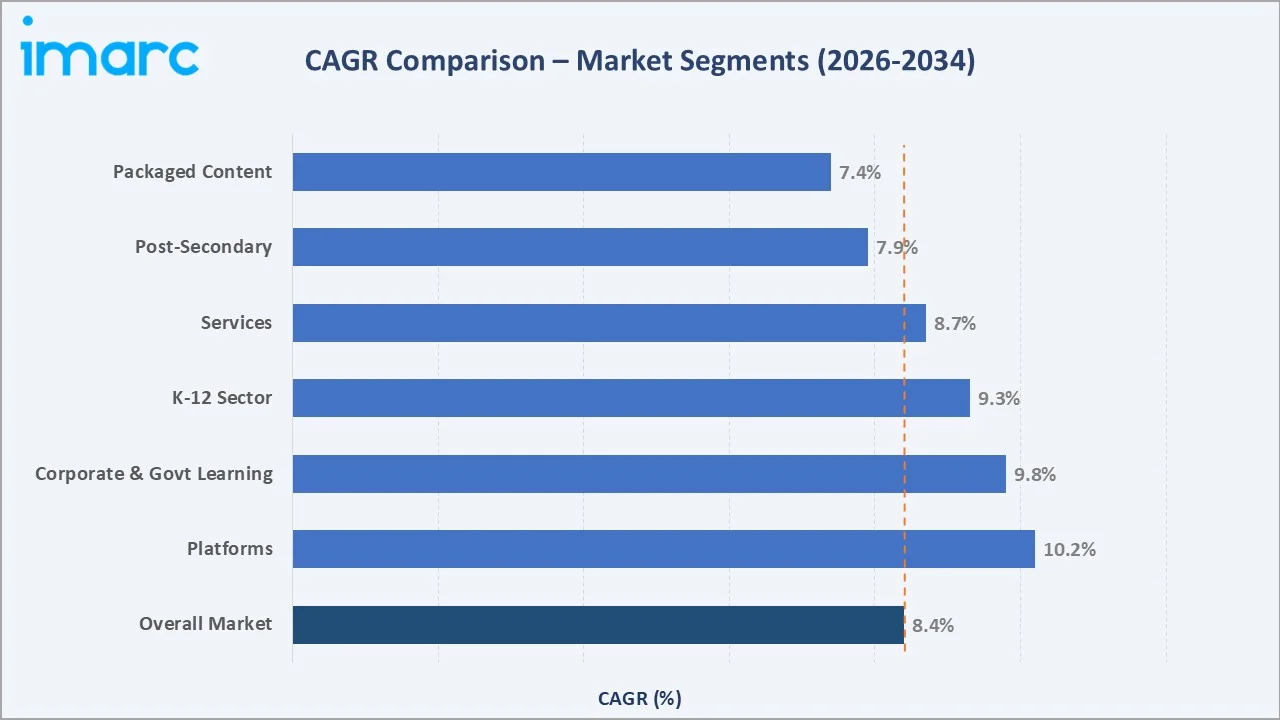

Segment-level CAGR comparisons highlighting Platforms and Corporate & Government Learning as the two fastest-growing sub-categories within the Africa e-learning industry analysis through 2034.

Executive Summary

The Africa e-learning market is undergoing a structural transformation driven by the convergence of mobile technology, demographic dynamics, and public-private investment in digital education infrastructure. Valued at USD 3.68 Billion in 2025, the market is forecast to reach USD 7.77 Billion by 2034 at a CAGR of 8.41%.

Packaged Content commands a 41.0% market share in 2025, underpinned by the scalability advantage of pre-produced digital content across teacher-scarce environments. Services at 33.2% reflect growing institutional LMS implementation demand, while Platforms at 25.8% represent the fastest-growing product type as cloud-hosted SaaS models gain traction. Within sectors, Post-Secondary institutions account for 38.0% of revenue, led by university digitization programs in South Africa, Morocco, Nigeria, and Kenya. Corporate and Government Learning at 30.6% reflects employer investment in workforce reskilling across fintech, healthcare, and telecom verticals.

South Africa retains regional leadership at 36.0% in 2025, supported by advanced ICT infrastructure, a mature EdTech startup ecosystem, and high corporate L&D spending. Nigeria (20.4%) and Kenya (15.6%) represent the highest-growth opportunity markets, driven by population scale and mobile-first learning adoption, respectively. The competitive landscape is bifurcated between global platform giants – Coursera, Udemy, Microsoft, and Google – and agile African-indigenous innovators such as ALX Africa, Andela, eLimu, and Snapplify.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Packaged Content – 41.0% share (2025) |

|

Leading Sector |

Post-Secondary – 38.0% share (2025) |

|

Fastest Growing Sector |

Corporate & Government Learning (digital upskilling surge) |

|

Leading Region |

South Africa – 36.0% revenue share (2025) |

|

Fastest Growing Region |

Kenya – strong mobile-first EdTech adoption |

|

Market Opportunity |

Offline-to-online transition across Sub-Saharan Africa |

|

Top Companies |

Coursera, Udemy, Microsoft, Google, ALX Africa, Andela, eLimu |

Key analytical observations supporting the above data:

- Packaged Content's 41.0% dominance in 2025 reflects Africa's acute teacher shortage and the scalability advantage of pre-produced digital content across rural and urban learner populations, enabling curriculum delivery without physical infrastructure investment.

- Post-Secondary sector's 38.0% leadership is driven by universities across South Africa, Nigeria, Morocco, and Kenya partnering with Coursera, edX, and Microsoft to offer online degree and certificate programs, expanding enrolment beyond physical campus capacity.

- Corporate & Government Learning at 30.6% is growing rapidly due to fintech, healthcare, and telecom sector workforce digitization, with companies like MTN, Safaricom, and Standard Bank investing in LMS-based training ecosystems for distributed workforces.

- South Africa's 36.0% regional dominance in 2025 reflects mature broadband infrastructure, high smartphone penetration, and leadership in EdTech investment, content production, and institutional LMS adoption.

- Kenya's mobile payment ecosystem enables seamless micropayment models for e-learning subscriptions, positioning the country as a digital learning innovation hub for East Africa.

- The Platforms segment at 25.8% represents the highest-growth product type through 2034, as SaaS-based LMS models gain traction among corporate and government clients seeking scalable cloud-hosted training delivery infrastructure across multiple African markets.

Africa E-Learning Market Overview

E‑learning in Africa delivers educational and training content via digital platforms, mobile apps, LMS, and packaged media, spanning K‑12, higher education, corporate training, government capacity building, and lifelong learning. Africa’s mobile-first population, urban-rural infrastructure gaps, and multilingual needs (over 2,000 languages) shape platform design, while a growing EdTech ecosystem attracts significant venture and institutional investment.

Applications cover school learners, university students, corporate employees, civil servants, and adult vocational learners. The AfCFTA, connecting 55 countries and ~1.4 billion people, is driving cross-border learner mobility and credential portability, enabling digital platforms to scale regionally.

Macroeconomic enablers include Africa’s projected 5.2 % GDP growth (IMF 2024), rising household incomes, expanding 4G/5G coverage reaching 1.1 billion subscriptions (GSMA), and development finance support from the World Bank, African Development Bank, and Mastercard Foundation, boosting digital education infrastructure and adoption.

Market Dynamics

To evaluate market opportunities, Request Sample

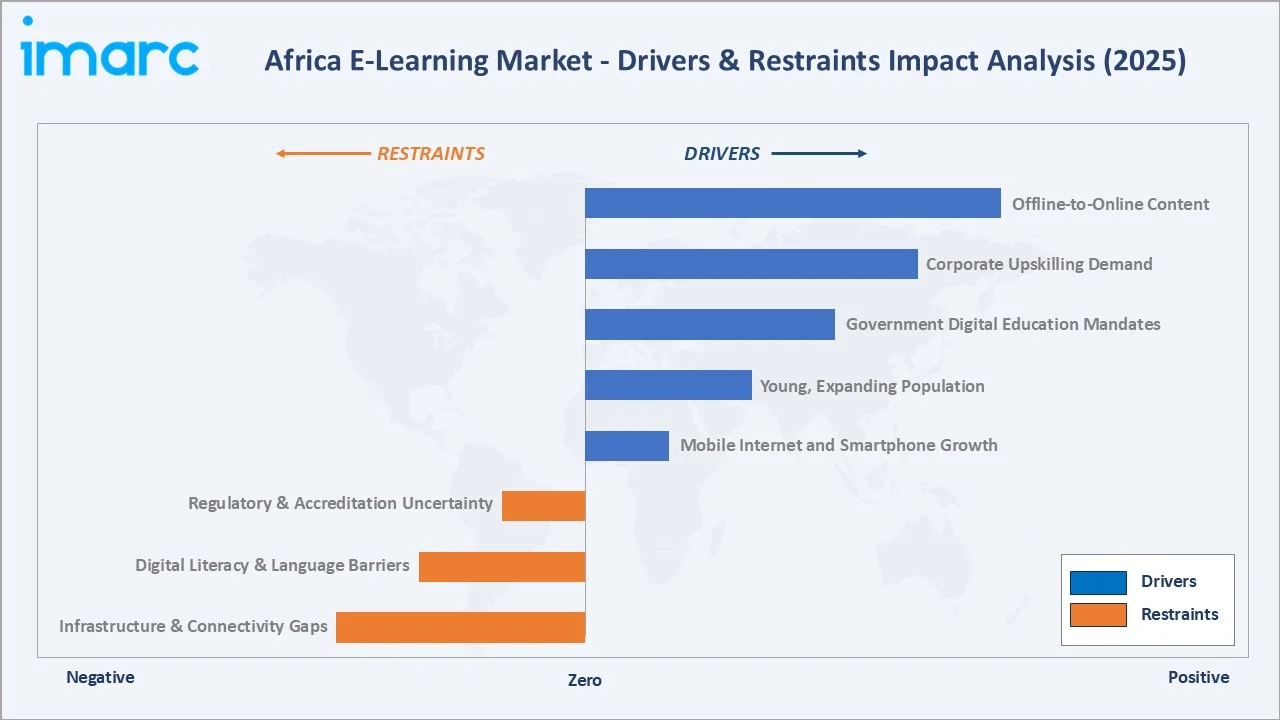

Market Drivers

- Mobile Internet and Smartphone Growth: Sub-Saharan Africa had 560 million mobile broadband subscriptions in 2024 (GSMA), with smartphone adoption growing 8–10 % annually. Mobile-first e-learning platforms in Nigeria, Kenya, and Ghana are reaching learners without PCs and enabling per-lesson micropayments via mobile money.

- Young, Expanding Population: Africa’s median age is 19.7 years, with over 60 % under 25. This creates strong, sustained demand for K‑12, post-secondary, and vocational digital learning.

- Government Digital Education Mandates: National strategies — including South Africa’s National Digital and Future Skills Strategy, Kenya’s Digital Literacy Programme, Morocco’s Education Digitalization Roadmap 2030, and Rwanda’s Smart Rwanda Master Plan — are driving public investment in e-learning infrastructure, devices, and content.

- Corporate Upskilling Demand: Africa’s growing tech, fintech, healthcare, and renewable energy sectors are expanding corporate e-learning. Companies like Jumia, Flutterwave, and M-KOPA are adopting LMS-based training for distributed workforces.

Market Restraints

- Infrastructure & Connectivity Gaps: Despite mobile growth, ~60 % of rural Sub-Saharan Africa lacks reliable high-speed internet in 2024. Unstable power and limited device affordability hinder e-learning adoption, especially in lower-income areas.

- Digital Literacy & Language Barriers: Uneven digital literacy and Africa’s 2,000+ languages challenge scalable e-learning, requiring extensive content localization.

- Regulatory & Accreditation Uncertainty: Inconsistent online degree accreditation frameworks limit recognition of digital credentials, reducing learner willingness to pay in markets where physical certificates dominate.

Market Opportunities

- Offline-to-Online Content: Africa’s vast traditional educational content offers a strong digitization opportunity. Platforms like Snapplify and Siyavula enable schools and universities to transition from physical to digital resources.

- Micro-Credentials & Short Courses: Rising employer demand for verifiable digital skills drives micro-credentials and short courses. ALX Africa enrolled 100,000+ learners across 60+ countries in 2024, showing strong adoption.

- Francophone Africa Opportunity: Côte d’Ivoire, Senegal, Cameroon, and DRC (250M+ population) are underpenetrated by English-language platforms, offering first-mover potential for localized French content.

Market Challenges

- Device Affordability & Digital Divide: Entry-level smartphones cost USD 130–160, equivalent to 2–4 months of income for low-income learners in Sub‑Saharan Africa, limiting access to rich e-learning content.

- Monetization & Payment Gaps: Low credit card adoption constrains subscription models, though mobile money platforms like M-Pesa and MTN Mobile Money are progressively enabling payments across East and West Africa.

Emerging Market Trends

1. Mobile-First and Offline-Capable Learning Platforms

African EdTech companies are leading mobile-first, low-bandwidth learning with offline-capable content. Platforms like eLimu (Kenya) and uLesson (Nigeria) enable e-learning in semi-urban and peri-urban communities, a model now being adopted by global entrants.

2. AI-Powered Personalized Learning and Adaptive Assessment

AI is transforming African e-learning, enabling personalized learning paths. Eneza Education (Kenya) serves 3+ million learners via SMS-based adaptive platforms, while global players like Coursera and Microsoft Learn are rolling out AI tutoring features across Africa from 2024.

3. Rise of Pan-African EdTech Ecosystems

African EdTech attracted over USD 200 million in venture capital in 2023 (Partech Africa), with platforms like ALX Africa, Andela, and Ingressive for Good building continent-wide learner networks, driving demand for curriculum-aligned content, corporate partnerships, and government skills programs, and signalling a maturing, capital-recycling EdTech ecosystem.

4. Gamification and Interactive Content for K-12 Learner Engagement

K-12 African e-learning platforms are using gamification — points, badges, leaderboards, and narratives — to boost engagement and reduce dropouts. Snapplify, Siyavula, and uLesson report higher completion rates with gamified content versus traditional formats.

5. Public-Private Partnerships Driving Large-Scale Deployment

African governments are partnering with tech and EdTech companies for large-scale digital learning. Initiatives like the Google-Kenya MOOC, Microsoft ADC programs, and Mastercard Foundation EdTech Fellows are expanding national-scale e-learning infrastructure and adoption.

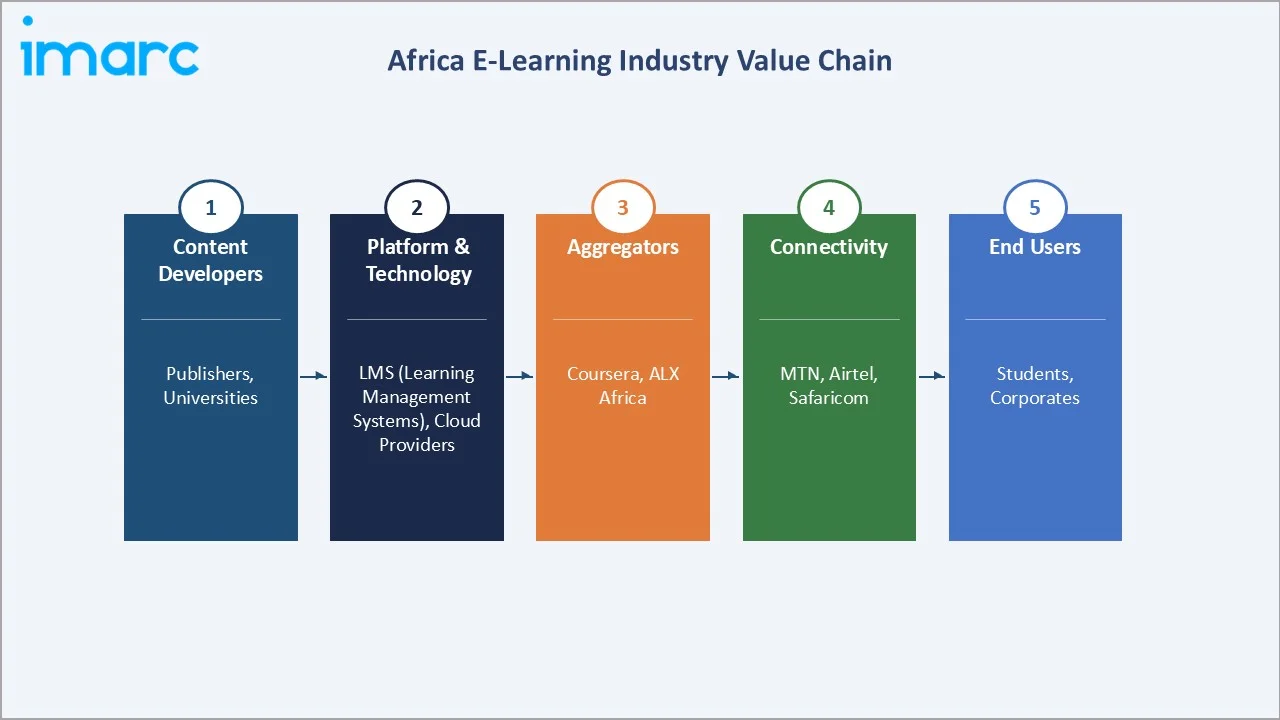

Industry Value Chain Analysis

The Africa e-learning value chain spans five integrated stages from content development through end-user delivery. Each stage presents distinct competitive dynamics, margin profiles, and localization requirements specific to Africa's heterogeneous market environment.

|

Stage |

Key Players / Examples |

|

Content Development |

Publishers, academic institutions, instructional designers, and curriculum boards |

|

Platform & Technology |

LMS vendors (Moodle, Canvas, Blackboard), cloud providers (AWS, Azure, Google Cloud) |

|

Aggregators & Distributors |

Coursera, Udemy, edX, African EdTech startups (eLimu, Snapplify, uLesson, ALX Africa) |

|

Connectivity Infrastructure |

Mobile network operators (MTN, Airtel, Safaricom), ISPs, and government broadband initiatives |

|

End Users |

Students (K-12, post-secondary), corporate employees, government trainees, adult learners |

Content developers and curriculum designers represent the upstream value chain, with African universities, curriculum publishers, and instructional designers increasingly collaborating with global platform operators to produce locally-relevant digital content aligned to national curricula. Platform and technology providers sit at the core of the value chain, providing LMS infrastructure, cloud hosting, and adaptive learning technologies that enable content delivery at scale across heterogeneous device and connectivity environments.

The aggregator and distributor layer – comprising both global platforms and African-indigenous EdTech companies – represents the highest margin and highest competitive intensity segment of the value chain. Connectivity infrastructure is provided by mobile network operators and fixed-line ISPs, increasingly influenced by government universal service obligation programs and DFI-backed connectivity expansion initiatives, progressively reducing the cost of content delivery in underserved markets.

Technology Landscape in the Africa E-Learning Industry

Mobile‑First & Offline Platforms

Mobile‑First & Offline Platforms: Platforms like eLimu (Kenya) and uLesson (Nigeria) provide curriculum-aligned content that works offline after sync, expanding e-learning into semi-urban and peri-urban communities.

AI‑Powered Personalized Learning

Eneza Education serves millions with adaptive, AI-driven content, tailoring difficulty and pace to individual learners. Global players like Coursera are adopting AI features for African learners.

Pan‑African EdTech Ecosystems

VC investment in African EdTech exceeded USD 200M in 2023 (Partech Africa). Regional leaders like ALX Africa, Andela, and Ingressive for Good are building continent-wide learner networks.

Gamification & K‑12 Engagement

Platforms like Snapplify, Siyavula, and uLesson use game-based learning — points, badges, and leaderboards — to improve course completion and engagement.

Public‑Private Partnerships

Initiatives like the Mastercard Foundation EdTech Fellows, Google-Kenya MOOC, and Microsoft Africa Development Centre programs support large-scale digital learning deployments across the continent.

Market Segmentation Analysis

By Product Type

To access detailed market analysis, Request Sample

The Africa e-learning market is segmented into Packaged Content (41.0 %), Services (33.2 %), and Platforms (25.8 %) in 2025. Packaged Content — including video lectures, interactive textbooks, gamified modules, and curriculum-aligned materials — leads the market due to its scalability and cost-effectiveness in teacher-scarce environments, with providers like Snapplify, Siyavula, and Pearson Digital dominating institutional licensing. Services encompass LMS implementation, customization, and managed support, reflecting growing demand from universities, governments, and enterprises. Platforms, particularly cloud-hosted SaaS models, are the fastest-growing segment, expanding at a projected CAGR of 10.2 % through 2034 as they increasingly replace on-premise LMS installations.

By Sector

The Africa e-learning market by sector is led by Post-Secondary at 38.0%, followed by Corporate and Government Learning at 30.6%, K-12 Sector at 21.4%, and Others at 10.0% in 2025. Each sector exhibits distinct technology adoption patterns, content requirements, and growth drivers through the forecast period 2026–2034.

Post-Secondary sector dominates at 38.0% in 2025. South Africa's universities, Egyptian institutions, Moroccan grandees écoles, and Nigerian federal universities are leading LMS adoption, partnering with Coursera, edX, and Microsoft to expand access to degree and certificate programs. Corporate and Government Learning at 30.6% is the fastest-growing sector, driven by enterprise investment in employee upskilling across financial services, technology, healthcare, and telecommunications. The K-12 Sector at 21.4% will grow significantly post-2026 as government-funded device programs and digital curriculum mandates broaden learner access.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South Africa |

36.0% |

Largest economy, advanced broadband infrastructure, strong corporate L&D spending, leading EdTech ecosystem |

|

Nigeria |

20.4% |

Largest population base, rising smartphone penetration, growing startup-driven EdTech sector in Lagos |

|

Kenya |

15.6% |

Mobile-first digital learning culture, Safaricom M-Pesa ecosystem, government digital literacy programs |

|

Morocco |

12.8% |

Strong government digitalization agenda, bilingual content demand, and rising higher education enrolment |

|

Tunisia |

8.6% |

High literacy rates (82.7%), university digitization programs, and the IT sector are driving corporate upskilling. |

|

Others |

6.6% |

Ethiopia, Ghana, Egypt, Côte d'Ivoire, and other emerging markets with growing EdTech investments |

The Africa e-learning market is regionally concentrated, with South Africa, Nigeria, and Kenya accounting for over 72 % of revenue in 2025. South Africa (36 %) leads, supported by advanced ICT infrastructure (93 % 4G coverage), high corporate L&D spending, and a vibrant EdTech ecosystem in Cape Town and Johannesburg. Nigeria (20.4 %) offers the largest growth potential with its 220+ million population, expanding middle class, and Lagos-centered EdTech startups. Kenya (15.6 %) benefits from Safaricom’s 4G network, widespread mobile money adoption, and government initiatives like the Digital Literacy Programme. North Africa contributes 21.4 %, with Morocco (12.8 %) leveraging its Education Digitalization Roadmap and EU/France partnerships, and Tunisia (8.6 %) supported by the region’s highest literacy rate (82.7 %), strong bilingual content, and a tech-engaged graduate population driving e-learning adoption.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Coursera Inc. |

Coursera |

Global Leader |

University partnerships, African institutional tie-ups, Mastercard Foundation-backed access programs |

|

Udemy Inc. |

Udemy |

Global Challenger |

Marketplace model, corporate B2B, Udemy for Business across African enterprises |

|

Microsoft Corporation |

Microsoft Learn |

Leader – Corporate |

LinkedIn Learning, ADC Kenya/Nigeria, 1M annual African upskilling commitment |

|

Google LLC |

Google for Education |

Leader – K-12/HEI |

Chromebook ecosystem, Google Classroom, Google Career Certificates Africa |

|

ALX Africa |

ALX |

Pan-African Leader |

Tech career training, 60+ African countries, Mastercard Foundation-backed |

|

Andela Inc. |

Andela |

Emerging – African |

Developer talent marketplace, tech upskilling, and employer partnerships |

|

eLimu |

eLimu |

Niche – K-12 |

Kenya-focused K-12, curriculum-aligned content, East Africa county government partnerships |

|

Snapplify |

Snapplify |

Niche – Content |

Digital textbook distribution, school-facing platform, South Africa market leader |

The Africa e-learning market features a bifurcated landscape: global platforms like Coursera, Udemy, Microsoft, and Google dominate post-secondary and corporate segments with scale, brand recognition, and institutional partnerships, while African-indigenous EdTechs focus on hyper-localized solutions offering curriculum alignment, local language support, and offline capability. Key dynamics include content localization, mobile-first/offline architecture, and public-private partnership capability for large-scale government deployments. Direct-to-consumer segments face intense price competition, often mitigated by freemium models, while local players hold a competitive edge in K-12 alignment, language content, and government relationships, which are difficult for global entrants to replicate quickly.

Market Concentration Analysis

The Africa e-learning market shows moderate concentration, with the top five platforms — Coursera, Udemy, Microsoft Learn, Google for Education, and ALX Africa — capturing 40–48 % of revenue in 2025, while fragmentation remains high at sub-regional and country levels. K-12 is the most fragmented, dominated by local curriculum-aligned providers, whereas post-secondary and corporate segments are more concentrated due to global platforms’ scale and multinational preference for recognized credentials.

Concentration is expected to rise through 2034 as AI-powered personalization and multilingual content create entry barriers. Emerging Pan-African platforms like ALX Africa and Andela, strategic acquisitions of local content, and MNO-EdTech partnerships for bundled data-inclusive access are further shaping consolidation across the continent.

Key Company Profiles

Coursera Inc.

Coursera is a global online learning platform offering university-accredited courses, specializations, professional certificates, and online degrees in partnership with universities and companies worldwide. In Africa, Coursera partners with the University of Cape Town, University of Pretoria, African Leadership University, and the University of Lagos.

- Product & Platform Portfolio: University-partnered online degrees, Coursera Plus subscription, professional certificate programs (Google, IBM, Meta), and Coursera for Business enterprise LMS platform.

- Recent Developments: In March 2026, The Africa Universities Fund, Inc. (AUF) was officially approved as a Coursera Impact Partner, reinforcing its role as a structured gateway to globally recognized career credentials for underserved learners across Africa.

- Strategic Focus: Coursera’s Africa strategy focuses on university partnerships for co-branded degrees, enterprise sales to multinationals, and subsidized programs with DFIs and foundations to boost employment outcomes for underserved learners.

Udemy Inc.

Udemy operates a marketplace-model e-learning platform with 230,000+ courses across 75 languages and 65+ million learners globally as of 2024. Udemy for Business targets corporate clients across Africa's financial services, technology, and professional services sectors with curated learning path subscriptions.

- Product & Platform Portfolio: Individual course marketplace, Udemy for Business enterprise LMS, instructor-led content creation platform, and mobile learning application with offline download capability.

- Recent Developments: In 2024, Udemy reported continued growth in the EMEA region, with Udemy Business expanding its enterprise customer base and supporting thousands of organisations across Europe, the Middle East, and Africa with flexible, AI‑enhanced learning solutions as part of its broader upskilling strategy.

- Strategic Focus: Udemy’s African strategy focuses on Udemy for Business to capture corporate L&D budgets, while using the consumer platform for brand building and learner acquisition.

Microsoft Corporation

Microsoft’s African strategy combines Microsoft Learn for technical certification and LinkedIn Learning for professional skills, with the Africa Development Centre (Nairobi and Lagos) driving Africa-specific product development and partnerships.

- Product & Platform Portfolio: Microsoft Learn (free technical training and certification pathways), LinkedIn Learning (5,000+ professional development courses), Azure-based LMS integrations for enterprise clients, and Microsoft Teams-integrated education tooling for institutional deployments.

- Recent Developments: In 2025, Microsoft launched an AI skilling initiative in South Africa, aiming to train one million learners in AI and digital skills by 2026, equipping individuals across business, government, and youth sectors with industry‑aligned competencies and recognised credentials to help bridge the digital skills gap.

- Strategic Focus: Microsoft’s Africa education strategy leverages Azure certifications to drive cloud adoption and LinkedIn to monetize professional learning, while its Africa Development Centre (ADC) focuses on co-developing AI-for-education tools tailored to African languages and curricula.

Investment & Growth Opportunities

Fastest-Growing Segments & Emerging Markets

The Platforms segment is Africa’s fastest-growing e-learning product type, driven by the shift from on-premise LMS to cloud-hosted SaaS across universities, enterprises, and governments. Corporate and government learning is expanding rapidly as organisations digitize training and implement upskilling mandates. High-growth country markets include Kenya, Nigeria, and Ethiopia, combining large learner populations, rising EdTech investment, and improving connectivity.

Emerging Market Expansion

Francophone West and Central Africa — Côte d’Ivoire, Senegal, Cameroon, Burkina Faso, and the DRC — represents a major underpenetrated market (250+ million people), while Ethiopia offers the largest single country opportunity under its Digital Ethiopia 2030 strategy. Micro-credentials and short-form vocational programs are growing fastest, with 40–60% higher completion rates than traditional courses and strong employer adoption.

Venture & Private Investment Trends

African EdTech attracted significant funding in recent years, with USD 200+ million in venture capital in 2023 and co-investment from institutions like IFC, AfDB, and USAID, reducing early-stage risk. Notable transactions include uLesson’s Series A, ALX Africa expansion funding from the Mastercard Foundation, and Andela’s growth capital from Generation Investment Management, reflecting growing investor confidence in scalable African EdTech platforms.

Future Market Outlook (2026-2034)

The Africa e-learning market forecast projects sustained value expansion from USD 3.68 Billion in 2025 to USD 7.77 Billion by 2034 at a CAGR of 8.41%, representing a near-doubling of market value driven by mobile connectivity proliferation, demographic-driven learner demand growth, and increasing institutional and corporate investment in digital learning infrastructure across all major African economies.

Three structural dynamics are set to reshape the Africa e-learning market through 2034. First, Pan-African EdTech ecosystems such as ALX Africa, Andela, and regional LMS providers will scale continent-wide, challenging global incumbents on curriculum relevance, language support, and institutional relationships. Second, mobile money-enabled micropayments will unlock the mass-market direct-to-consumer segment, expanding paying learners beyond formal-sector employees. Third, AI-powered content localization will lower costs for African-language content, accelerating penetration in francophone, lusophone, and Arabic-language markets. By 2034, e-learning is expected to transition from an institutional niche to a mass-market consumer service, with a competitive landscape dominated by global platforms (Coursera, Microsoft, Google) in post-secondary and corporate segments, Pan-African indigenous platforms (ALX Africa, Andela) in employment-linked skills, and mobile-first micro-learning providers serving individual learners.

Research Methodology

Primary Research

Primary research encompassed over 45 structured interviews and expert consultations conducted in 2024–2025 with Africa e-learning industry stakeholders, including EdTech platform executives, university LMS administrators, corporate L&D directors, government education ministry officials, mobile network operator digital services leads, EdTech venture capital investors, and development finance institution program managers. Primary insights validated market sizing, segmentation estimates, technology adoption timelines, and competitive positioning assessments across key African markets.

Secondary Research

Secondary sources include UNESCO Education Statistics, GSMA Mobile Economy Sub-Saharan Africa report (2024), Partech Africa VC Report (2023), African Development Bank education sector assessments, IFC EdTech Africa investment reports, World Bank digital skills development program data, national government digital education strategy documents from South Africa, Kenya, Nigeria, Morocco, and Rwanda, EdTech Africa conference proceedings, company annual reports, and trade publications including EdSurge, Africa Tech, and eLearning Industry.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models incorporating GDP growth rates, internet and smartphone penetration trajectories, learner population demographics, historical e-learning adoption curves from comparable emerging markets, and government digital education investment commitments. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty, connectivity infrastructure development pace, and regulatory environment evolution across key African markets.

Africa E-Learning Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sectors Covered | K-12 Sector, Post-Secondary, Corporate and Government Learning, Others |

| Product Types Covered | Packaged Content, Services, Platforms |

| Technologies Covered | Mobile Learning, Simulation Based Learning, Game Based Learning, Learning Management System (LMS), Others |

| Regions Covered | South Africa, Morocco, Nigeria, Tunisia, Kenya, Others |

| Companies Covered | Coursera Inc., Udemy Inc., Microsoft Corporation, Google LLC, ALX Africa, Andela Inc., eLimu, Snapplify |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Africa e-learning market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Africa e-learning market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Africa e-learning industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Africa E-Learning Market Report

The Africa e-learning market was valued at USD 3.68 Billion in 2025, driven by mobile internet expansion, growing youth population demographics, and rising government and corporate investment in digital education infrastructure across Sub-Saharan and North Africa.

The market is projected to reach USD 7.77 Billion by 2034, growing at a CAGR of 8.41% during 2026-2034, driven by mobile-first platform proliferation, AI-powered personalization, and expanding corporate and government sector digital learning adoption.

Packaged Content leads with a 41.0% share in 2025, driven by Africa's teacher shortage and the scalability advantage of pre-produced digital content for curriculum delivery across under-resourced educational institutions at urban and rural scales.

Post-Secondary sector leads at 38.0% share in 2025, driven by African university enrolment growth, institutional LMS adoption, and partnerships between universities and global platforms.

South Africa leads with a 36.0% revenue share in 2025, driven by advanced broadband infrastructure, high corporate L&D spending, and the continent's most mature EdTech startup ecosystem.

Key drivers include mobile internet subscription growth, the continent's 60%+ population below age 25, government digital education mandates across South Africa, Kenya, Nigeria, and Morocco, and corporate workforce upskilling demand across fintech, healthcare, and telecommunications sectors.

Platforms are the fastest-growing product type at approximately 10.2% CAGR through 2034, driven by cloud-hosted SaaS LMS adoption among corporate and government clients.

Leading companies include Coursera Inc., Udemy Inc., Microsoft Corporation, Google LLC, ALX Africa, Andela Inc., eLimu, and Snapplify.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)