Low Voltage Electric Motor Market Size, Share, Trends and Forecast by Efficiency, End-Use Industry, Application, and Region 2026-2034

Global Low Voltage Electric Motor Market Size, Share, Trends & Forecast (2026-2034)

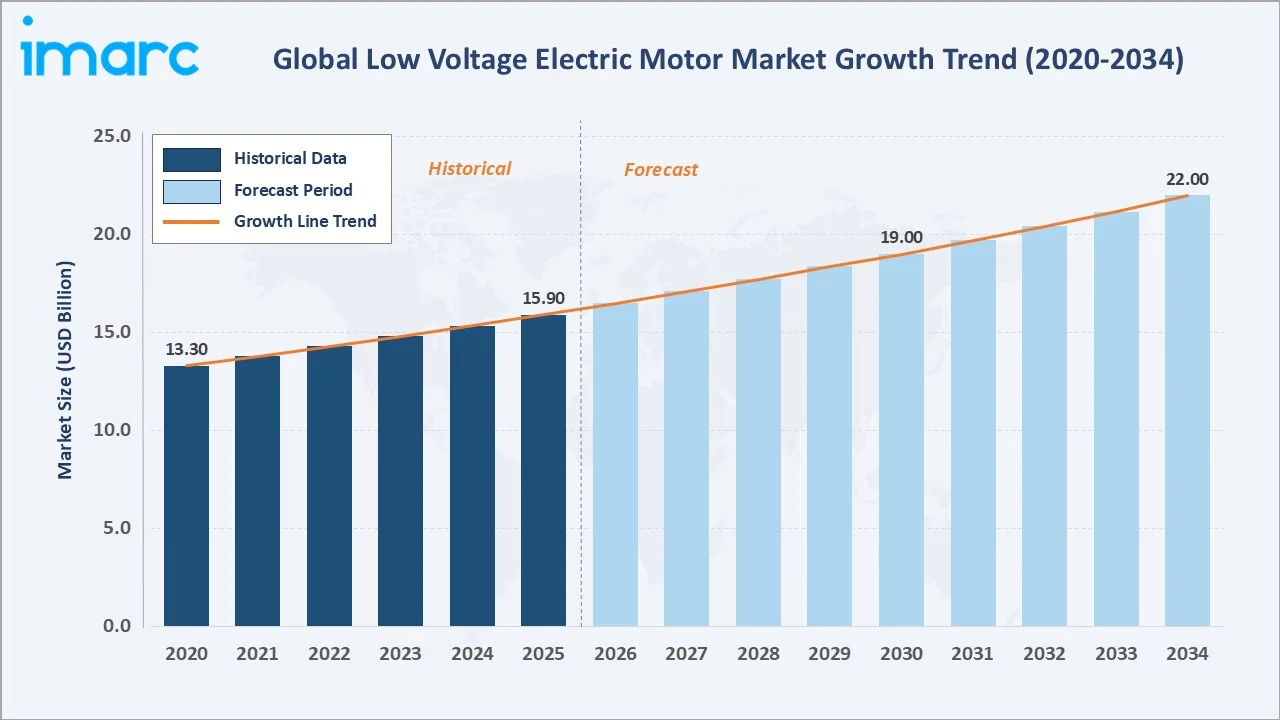

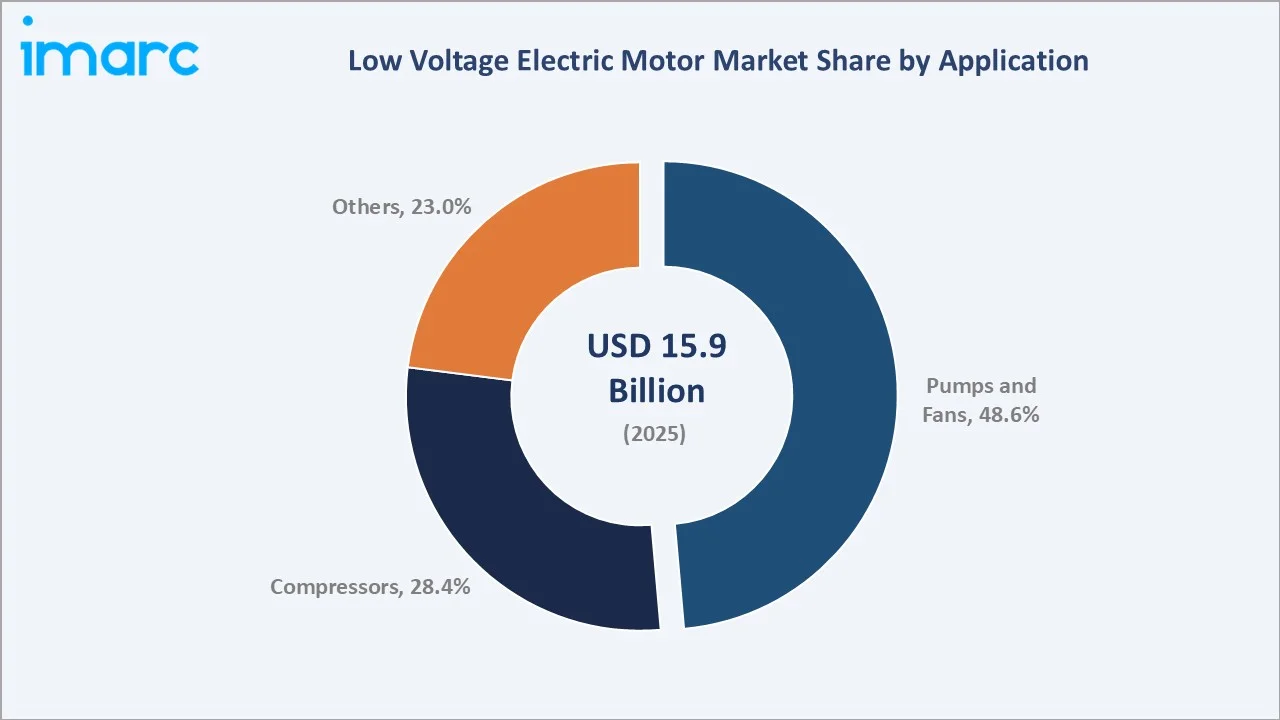

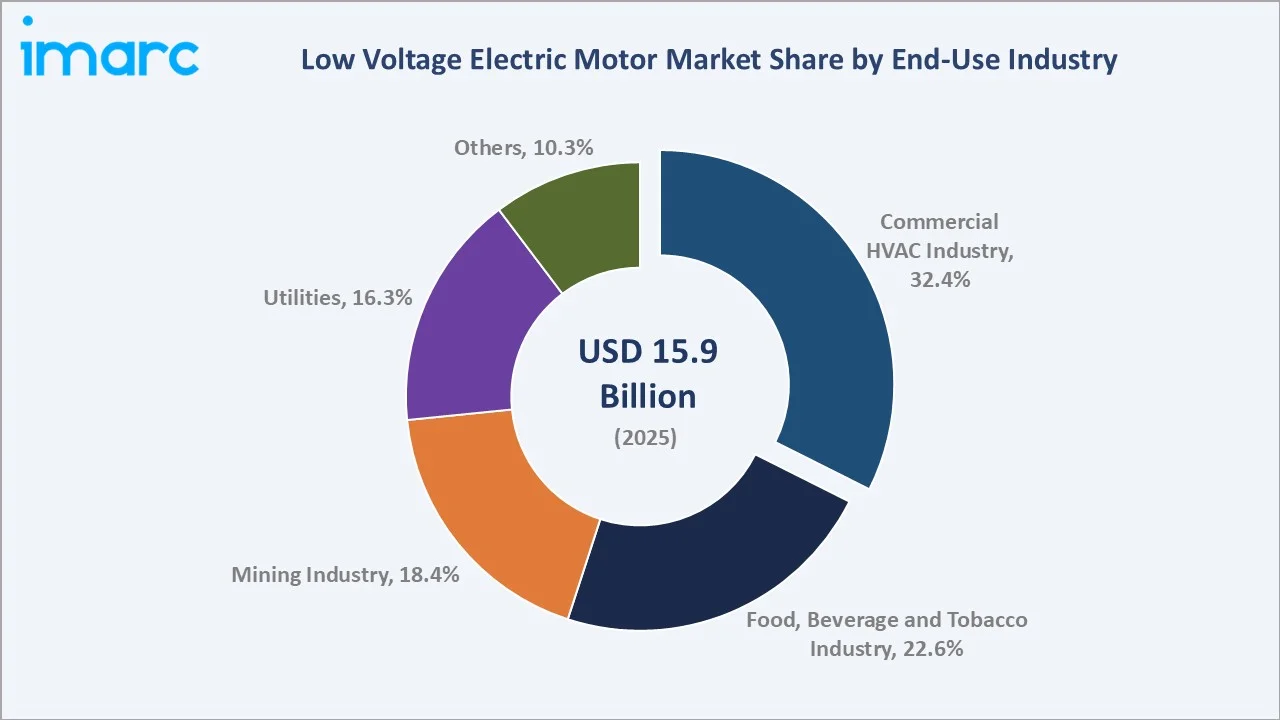

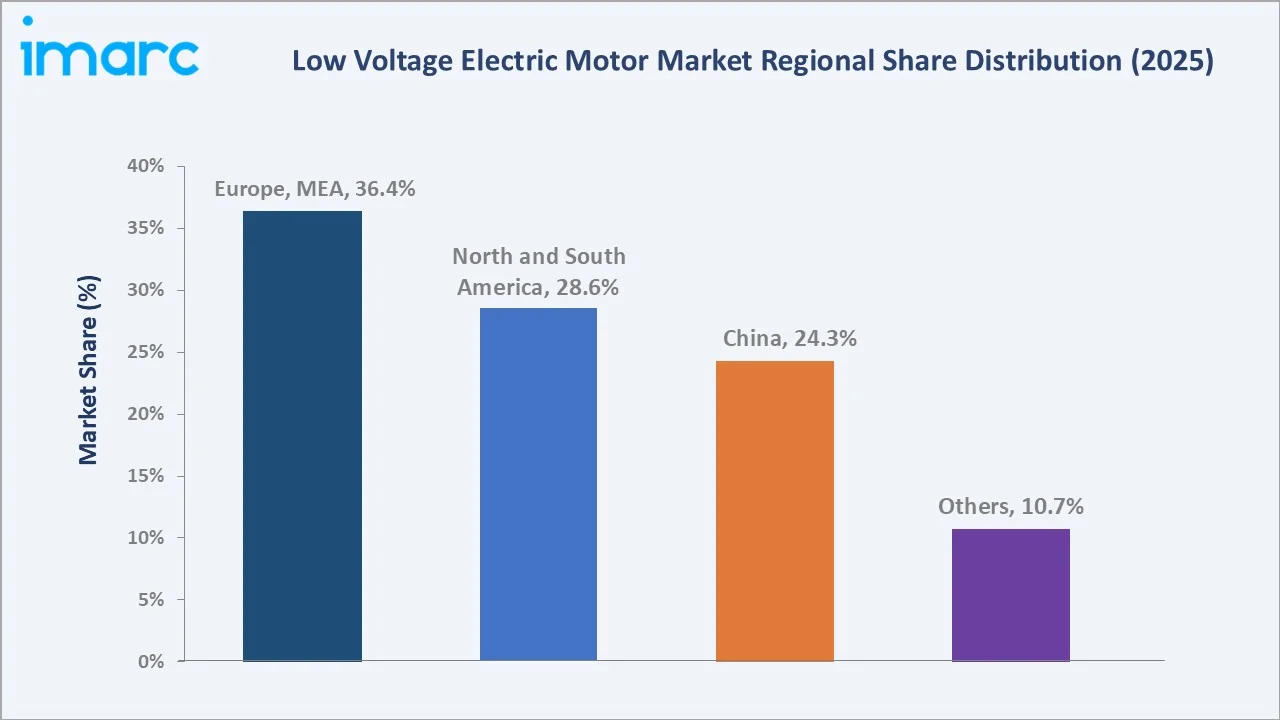

The global low voltage electric motor market size was valued at USD 15.9 Billion in 2025 and is projected to reach USD 22.0 Billion by 2034, exhibiting a CAGR of 3.6% during the forecast period 2026-2034. Rising global demand for energy-efficient industrial equipment, mandatory IE3/IE4 efficiency regulations across the EU, China, and North America, and accelerating industrial automation investment are the primary growth catalysts. Pumps and Fans dominate application demand at 48.6% in 2025, while the Commercial HVAC Industry leads end-use consumption at 32.4%. Europe, Middle East and Africa (EMEA) commands the largest regional share at 36.4%, anchored by the EU Ecodesign Regulation (EU) 2019/1781.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 15.9 Billion |

|

Forecast Market Size (2034) |

USD 22.0 Billion |

|

CAGR (2026-2034) |

3.6% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe, Middle East and Africa – 36.4% share (2025) |

|

Fastest Growing Region |

China – driven by GB18613-2020 IE3 mandate |

|

Leading Application |

Pumps and Fans – 48.6% revenue share (2025) |

|

Leading End-Use Industry |

Commercial HVAC Industry – 32.4% share (2025) |

The global low voltage electric motor market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base driven by industrial demand against a sustained forecast curve powered by energy-efficiency regulations, automation investment, and expanding data centre and renewable energy infrastructure.

To get more information on this market, Request Sample

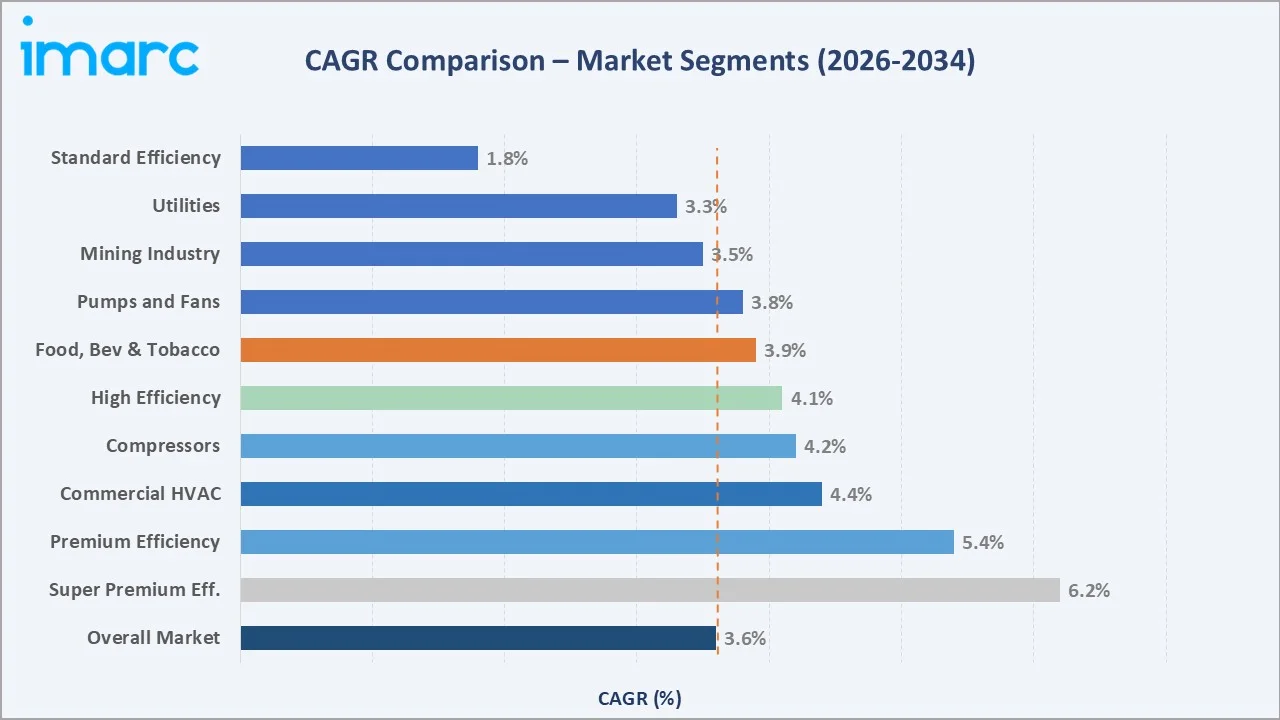

Segment-level CAGR comparisons highlighting Super Premium Efficiency motors and Commercial HVAC applications as the fastest-growing sub-categories within the global low voltage electric motor market analysis through 2034.

Executive Summary

The global low voltage electric motor market is undergoing a regulation-driven transformation as energy efficiency mandates reach new levels of stringency across the world's major industrial economies. Valued at USD 15.9 Billion in 2025, the market is forecast to reach USD 22.0 Billion by 2034 at a CAGR of 3.6%.

Pumps and Fans command the dominant application share at 48.6% in 2025, driven by ubiquitous deployment in building HVAC systems, water utilities, and industrial process cooling. Compressors represent 28.4% of revenue, supported by energy-intensive refrigeration and compressed-air applications across food processing, manufacturing, and data centres. Among end-use industries, the Commercial HVAC Industry holds the largest 32.4% share, benefiting from rapid smart-building adoption and green certification programmes globally. The Food, Beverage and Tobacco Industry (22.6%) and Mining Industry (18.4%) collectively represent over 40% of market demand.

EMEA leads regional demand at 36.4% in 2025, supported by the EU's industry-leading efficiency regulatory framework. North and South America follow with 28.6%, anchored by US industrial automation capex and data centre expansion. China, at 24.3% is the single most impactful near-term growth market, as the GB18613-2020 IE3 mandate continues to drive replacement of an enormous legacy motor fleet.

Key Market Insights

|

Insight |

Data |

|

Largest Application Segment |

Pumps and Fans – 48.6% revenue share (2025) |

|

Second Application Segment |

Compressors – 28.4% revenue share (2025) |

|

Leading End-Use Industry |

Commercial HVAC Industry – 32.4% (2025) |

|

Second End-Use Industry |

Food, Beverage and Tobacco Industry – 22.6% (2025) |

|

Leading Region |

Europe, Middle East and Africa – 36.4% (2025) |

|

Top Companies |

ABB Ltd, Siemens AG, WEG S.A., Nidec Corporation |

Key Analytical Observations Supporting The Above Data:

- Pumps and Fans at 48.6% dominance in 2025 reflects the sector's continuous-duty operating profile and deep penetration of VFD-controlled motor drives in building HVAC and water management, where energy-efficiency regulations have the most direct impact.

- Compressors at 28.4% are driven by industrial compressed-air systems – estimated to account for 10% of industrial electricity use in developed markets – and refrigeration compressors in food cold chains, making motor efficiency a key corporate sustainability priority.

- Commercial HVAC at 32.4% is the largest end-use vertical because motors power every HVAC subsystem: fans, pumps, compressors, and air-handling units. Green-certified real estate (LEED, BREEAM) increasingly specifies IE3 or IE4 motors as a requirement.

- EMEA's 36.4% regional leadership is anchored by the EU Ecodesign Regulation (EU) 2019/1781, which mandates IE3 minimum efficiency for motors from 0.75 kW to 1,000 kW, compelling systematic fleet replacement across European industry.

- China's 24.3% share and strong growth outlook are driven by the GB18613-2020 standard making IE3 the mandatory minimum since July 2021, initiating the world's largest single motor replacement programme.

- IE4 Super Premium and IE5 Ultra-Premium motors are transitioning from niche to mainstream as total-cost-of-ownership analyses consistently demonstrate payback periods of 5-7 years, compelling adoption in energy-intensive continuous-duty applications.

Global Low Voltage Electric Motor Market Overview

Low‑voltage (LV) electric motors operate below 1,000 V, converting electrical energy into mechanical torque, and are classified under IEC 60034‑30‑1 from IE1 (standard) to IE5 (ultra‑premium), by power (0.12–1,000 kW), enclosure (TEFC, ODP, HazLoc), and technology (squirrel-cage induction, PMSM, SynRM). They power a wide range of industrial and commercial applications, including pumps, fans, compressors, conveyors, mixers, and precision drives in automation and robotics.

The LV motor ecosystem spans raw material suppliers, component manufacturers, OEMs, VFD suppliers, system integrators, and end users, with VFD integration enabling 20–50% energy savings in variable-torque applications. Demand is driven by industrial automation, robotics, smart factories, massive data centre expansion (global electricity use projected to double by 2030), grid modernization, and sustainability programs mandating efficiency upgrades. Structurally, the LV motor market is highly correlated with industrial production, building construction, and electricity infrastructure investment, making it a key enabler of energy-efficient industrial and commercial operations.

Market Dynamics

To evaluate market opportunities, Request Sample

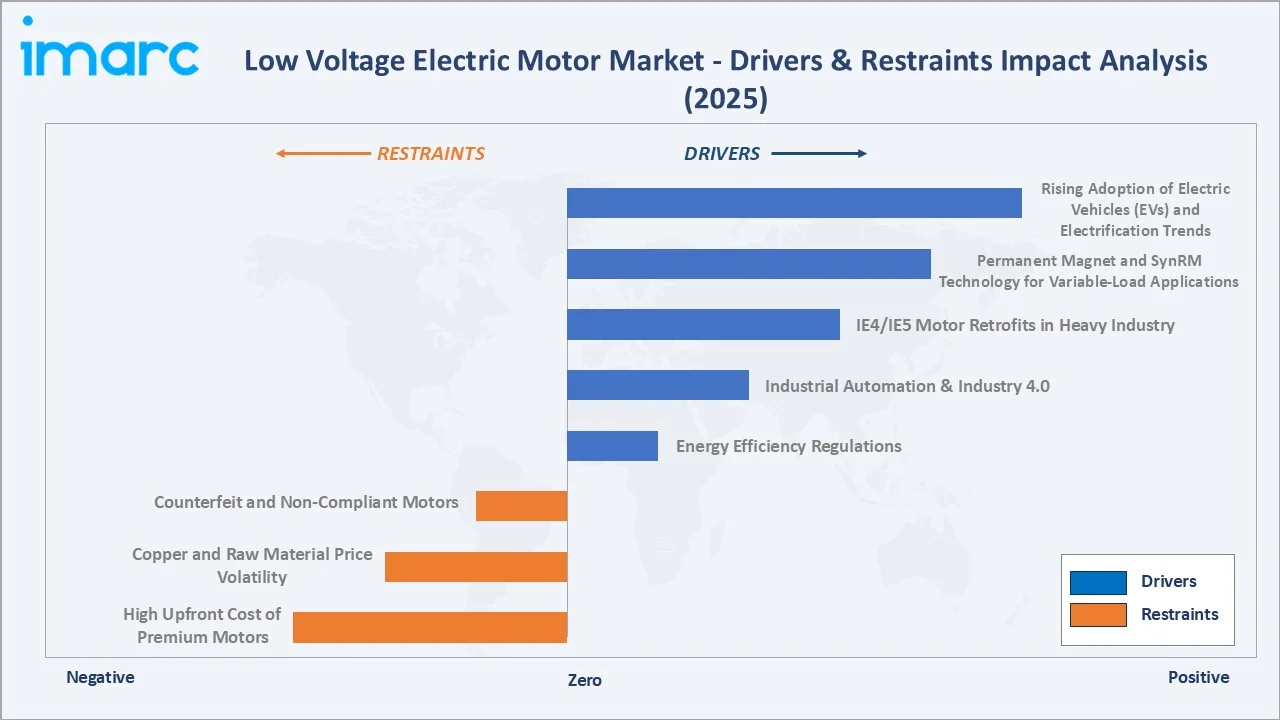

Market Drivers

- Energy Efficiency Regulations: Mandatory standards—EU Ecodesign 2019/1781, China GB 18613‑2020, and US DOE NEMA Premium rules—require replacement of legacy IE1/IE2 motors with IE3/IE4 units, driving a multi‑year, multi‑billion-dollar upgrade cycle.

- Industrial Automation & Industry 4.0: Robotics and smart manufacturing, with over 590,000 industrial robots installed globally in 2023, are increasing demand for precision-controlled LV motors.

Market Restraints

- High Upfront Cost of Premium Motors: Premium‑efficiency motors (IE4/IE5) typically command significant price premiums over standard IE1/IE2 units, which can delay purchases in price‑sensitive markets and among SMEs despite favorable lifecycle economics. Costs of higher efficiency classes rise with more advanced materials and construction compared with lower classes.

- Copper and Raw Material Price Volatility: Copper prices have surged to multi‑year highs and remain volatile due to tight supply and strong demand, pressuring manufacturers’ input costs and compressing margins. Copper is a major cost driver in motors, and elevated prices increase finished motor prices and can slow large capital purchases.

Market Opportunities

- IE4/IE5 Motor Retrofits in Heavy Industry: Large fleets of aged motors in mining, cement, chemicals, and pulp‑and‑paper are being targeted with IE4/IE5 retrofit programs that can yield incremental energy savings over IE3 with short payback periods at current electricity prices. Industrial decarbonisation policies such as the EU Fit for 55 package and the US Inflation Reduction Act bolster the economic case for upgrades.

- Permanent Magnet and SynRM Technology for Variable-Load Applications: Permanent Magnet Synchronous Motors and Synchronous Reluctance Motors achieve IE4–IE5 efficiency in VFD‑driven pump, fan, and compressor applications and deliver measurable gains over induction motors at partial loads. Declining rare‑earth costs and scaling production are supporting wider adoption.

Market Challenges

- Counterfeit and Non‑Compliant Motors: Substandard motors falsely labeled as IE2/IE3 undercut OEMs, slow efficiency gains, and pose reliability risks, especially in markets with weak enforcement.

- VFD Integration Challenges: Integrating VFDs with legacy systems can cause harmonics, insulation stress, and maintenance complexity, limiting adoption and the full efficiency benefits of IE3+ motors.

Emerging Market Trends

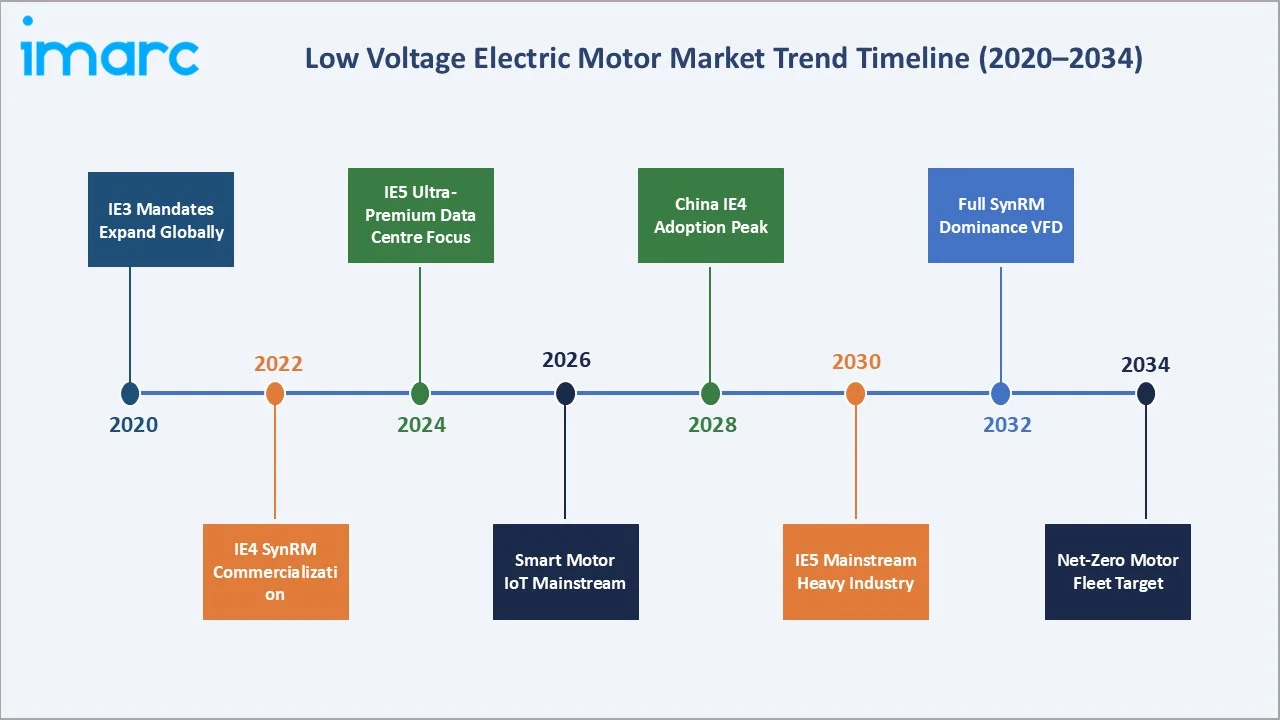

1. IE4 and IE5 Motor Classes Transitioning from Niche to Commercial Baseline

IE4 motors are transitioning from premium niche to the baseline in EU and North America, while IE5 is gaining traction in data centres, large HVAC, and heavy industry. Leading OEMs (ABB, Siemens, WEG) have expanded portfolios.

2. IoT-Enabled Smart Motor Systems and Condition-Based Maintenance

Embedded sensors monitoring temperature, vibration, and current enable predictive maintenance. Solutions like ABB Ability Smart Sensor and Siemens SIRIUS reduce unplanned downtime by 30–50%, expanding OEM value into lifecycle services and recurring revenue.

3. Synchronous Reluctance Motor (SynRM) Disrupting the IE3 to IE4 Transition

Synchronous reluctance motors deliver IE4 efficiency without rare-earth magnets, excelling in VFD-driven pumps, fans, and compressors. Platforms from ABB and Siemens match or exceed IE5 system-level performance, making SynRM a premium option for continuous-duty industrial applications.

4. Industrial Decarbonisation Strategies Accelerating Motor Fleet Turnover

Corporate net-zero targets and policies like the EU Fit for 55 and US Inflation Reduction Act are accelerating motor replacements and efficiency upgrades, particularly in mining, food processing, and utilities.

5. Supply Chain Regionalisation and Local Manufacturing Expansion

Post-pandemic disruptions and geopolitical factors are prompting OEMs to regionalise production. WEG expanded North American capacity, Regal Rexnord is growing in Mexico, and Chinese OEMs are entering Southeast Asia, reducing lead times and meeting local content requirements.

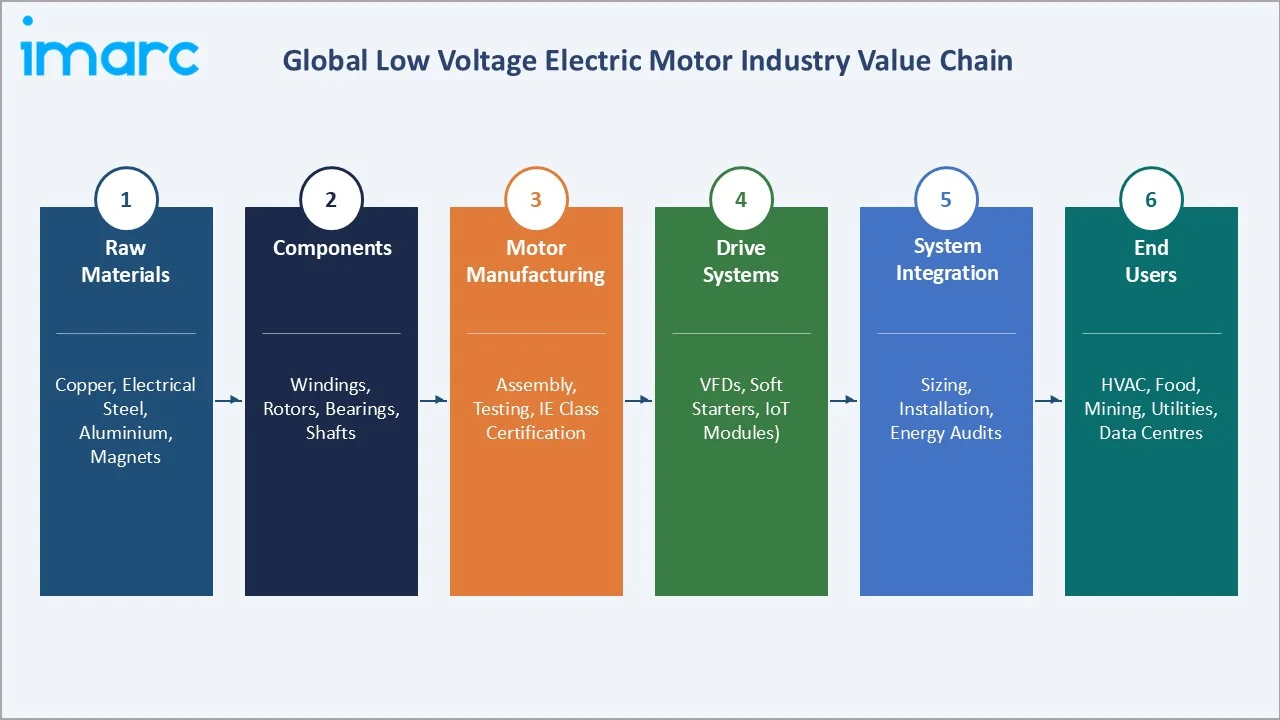

Industry Value Chain Analysis

The low voltage electric motor value chain spans from raw materials to end-user operation, with distinct dynamics across each stage. Motor OEMs sit at the core, integrating components into certified, high-efficiency motors and increasingly offering integrated motor-drive-control systems.

|

Value Chain Stage |

Key Activities / Players |

|

Raw Materials |

Copper wire & rod (Freeport-McMoRan, Codelco); Electrical steel laminations (NLMK, POSCO, Nippon Steel); Aluminium die castings; Rare-earth magnets for PMSM (MP Materials, China Northern RE) |

|

Component Manufacturing |

Motor windings & coil assembly; Rotor/stator lamination stamping & assembly; Precision bearings (SKF, NSK, Schaeffler); Shaft machining; Encoder & sensor modules |

|

Motor Manufacturing |

Full motor assembly & balancing; IE-class efficiency testing & certification (IEC 60034-30); Enclosure fabrication (TEFC, ODP, HazLoc); ABB, Siemens, WEG, Nidec, Wolong Electric |

|

Drive & Control Systems |

Variable-frequency drives (ABB, Danfoss, Yaskawa, Siemens SINAMICS); Soft starters (Schneider Electric, ABB); Motor controllers; IoT interface & condition monitoring modules |

|

System Integration |

Motor-VFD system sizing & specification; Installation & commissioning; Energy audits & retrofit assessments; Regional engineering contractors & OEM service arms |

|

End Users & O&M |

HVAC facility operators (Carrier, Trane, Daikin); Food processors (Nestlé, Tyson, JBS); Mining operators (Freeport, BHP, Glencore); Utilities (Veolia, SUEZ); Data centre operators (Equinix, Digital Realty) |

The shift toward smart, IoT-enabled motors is expanding OEM value capture into services and maintenance, boosting recurring revenues. On the demand side, HVAC, food processing, and mining are the leading adopters of high-efficiency and smart motor solutions.

Technology Landscape in the Low Voltage Electric Motor Industry

Three-Phase Squirrel-Cage Induction Motors: The Dominant Technology

Squirrel-cage induction motors dominate the LV market due to their robustness, low maintenance, cost efficiency, and compatibility with VFDs. Continuous design improvements (optimized windings, low-loss materials) have enabled IE3/IE4 efficiency levels, sustaining their leadership in pumps, fans, and compressors.

Permanent Magnet Synchronous Motors (PMSMs)

PMSMs deliver higher efficiency—especially at partial loads—making them ideal for variable-speed applications such as HVAC, data centre cooling, and automation. While dependent on rare-earth magnets, improving supply dynamics and lifecycle energy savings are driving increased adoption.

Synchronous Reluctance Motors (SynRM): The Emerging Premium Choice

SynRM motors offer IE4-level efficiency without rare-earth materials, using a magnet-free rotor design that reduces losses and operating temperatures. Supported by platforms from ABB, Siemens, and Nidec, they are gaining share in medium-power, variable-torque applications.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Efficiency | High Efficiency | 🔒 | 2025 |

| End-Use Industry | Commercial HVAC Industry | 32.4% | 2025 |

| Application | Pumps and Fans | 48.6% | 2025 |

| Region | Europe, Middle East and Africa | 36.4% | 2025 |

By Application

Pumps and Fans command a 48.6% majority share of the global low voltage electric motor market in 2025, the largest application segment by a substantial margin. This dominance reflects the pervasive deployment of fluid-moving and air-handling systems across every industrial and commercial sector.

To access detailed market analysis, Request Sample

Compressors account for 28.4% of 2025 market revenue. The demand driven by industrial compressed-air systems and refrigeration in HVAC, cold chains, and process cooling. High energy consumption and continuous operation make them a key focus for efficiency upgrades, particularly IE4 motors. The Others category at 23.0% includes conveyors, agitators, mixers, extruders, hoists, and escalators – all driven by industrial automation investment trends.

By End-Use Industry

The Commercial HVAC Industry represents 32.4% of global LV electric motor market revenue in 2025. Growth is driven by smart-building certifications (LEED, BREEAM, ENERGY STAR) mandating high-efficiency systems, with data centre cooling emerging as the fastest-growing sub-segment.

The Food, Beverage and Tobacco Industry (22.6%) is the second-largest segment, with motors used in conveyors, processing, refrigeration, and packaging. Demand is supported by automation trends and stringent hygiene standards, driving adoption of washdown-duty, food-grade motors.

The Mining Industry at 18.4% relies on LV motors for heavy-duty applications such as conveyors, ventilation, dewatering, and processing equipment. Demand is tied to mining capex cycles in energy-transition metals, requiring robust, explosion-proof, and high-durability motor solutions.

Regional Market Insights

EMEA commands the largest regional revenue share of 36.4% in 2025, driven by the EU's world-leading motor-efficiency regulatory framework. North and South America hold 28.6%, anchored by the US industrial economy and rapidly growing data centre infrastructure. China at 24.3% is the most impactful near-term growth catalyst globally, as the GB18613-2020 IE3 mandate progresses through the world's largest motor installed base. The Others grouping at 10.7% represents the high-growth potential of South and Southeast Asia, India, Australia, and the broader Rest of World.

EMEA is the most regulation-driven, high-specification market, led by the EU Ecodesign Regulation (EU) 2019/1781 mandating IE3 minimum efficiency with ongoing IE4 phase-in. Germany, Italy, and France dominate demand, driven by industrial automation and HVAC retrofits, while the Middle East (Saudi Arabia, UAE) is emerging as a high-growth pocket due to industrial expansion and data centre investments.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe, Middle East & Africa |

36.4% |

EU Ecodesign Regulation (EU) 2019/1781 IE3/IE4 fleet replacement; Germany, Italy, France HVAC and industrial automation; Middle East Vision 2030 infrastructure; UK net-zero industrial policy |

|

North and South America |

28.6% |

US NEMA Premium / DOE 2016 motor efficiency rule; reshoring manufacturing investment; data centre expansion (Equinix, Digital Realty, AWS); Brazil ANEEL motor programme; Mexico industrial growth |

|

China |

24.3% |

GB18613-2020 mandatory IE3 standard (July 2021); State Grid efficiency infrastructure investment; Made in China 2025 industrial upgrade; massive legacy IE1/IE2 fleet replacement cycle |

|

Others |

10.7% |

India IS 12615:2018 IE2/IE3 adoption; Australia MEPS 2021 (IE3 minimum); SE Asia manufacturing expansion; Japan/Korea advanced motor technology ecosystems |

North and South America are led by the US, where NEMA Premium (IE3-equivalent) adoption is well established, and data centre growth is accelerating demand. Policy support, including energy-efficiency incentives under the Inflation Reduction Act, is encouraging motor upgrades. Latin America (Brazil, Mexico, Chile) is a developing growth region, supported by mining, food processing, and grid modernization, with regulatory programs such as Brazil’s ANEEL initiatives driving efficiency adoption.

Competitive Landscape

The global low voltage electric motor competitive landscape is characterised by a small number of global OEMs commanding broad product portfolios and geographic reach, alongside a large number of regional and domestic manufacturers competing primarily on price, particularly in China and Southeast Asia.

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

ABB Ltd |

ABB SynRM+ |

Global Leader |

Broadest IE4/IE5 portfolio; SynRM technology; ABB Ability IoT platform; global service network |

|

Siemens AG |

SIMOTICS GP/SD/M Platform |

Global Leader |

Full IE2-IE4 range; deep EMEA and Asia presence; integrated motor-drive-control solutions |

|

WEG S.A. |

W22/W50 IE3/IE4 Series |

Strong Challenger |

Americas market leader; cost-competitive; expanding EMEA and US presence; IE4 data centre focus |

|

Nidec Corporation |

Nidec / Leroy-Somer |

Strong Challenger |

Acquisitive growth; EMEA presence via Leroy-Somer; broad industrial motor range |

|

Wolong Electric Group |

Wolong IE3 Series |

Regional Leader |

China market leader; growing export footprint; highly competitive cost structure |

|

Toshiba International |

Toshiba IHM Series |

Established Player |

Mining and utility specialist; Asia-Pacific installed base; IE3 TEFC range |

The top four players – ABB, Siemens, WEG, and Nidec– collectively account for 45-50% of global market revenue in 2025, with the balance distributed across over 100 regional and local manufacturers worldwide.

Key Company Profiles

ABB Ltd

ABB leads the global LV motor market with a full IE3–IE5 portfolio across induction, PMSM, and SynRM technologies, while its ABB Ability Smart Sensor digitizes legacy motors for predictive maintenance, expanding value from hardware to lifecycle services.

- Product & Platform Portfolio: IE2 to IE5 motors (0.12 kW – 1,000 kW+), SynRM+, PMSM, HazLoc motors, marine motors, food-grade motors, integrated motor-VFD systems, ABB Ability Smart Sensor.

- Recent Developments: In September 2025, ABB expands its IE5 synchronous reluctance motor (SynRM) portfolio with smaller frame sizes, offering the broadest range of magnet- and rare earth-free motors.

- Strategic Focus: ABB targets energy transition leadership through IE4/IE5 premium motor expansion, IIoT-enabled smart motor systems, and growing its service and retrofit business to capture installed base revenue over the motor lifecycle.

Siemens AG

Siemens’ SIMOTICS LV motors cover IE2–IE4 efficiency and general-purpose, severe-duty, HazLoc, and servo applications, leveraging strong EMEA OEM ties and integrated motor-drive solutions through its automation division.

- Product & Platform Portfolio: SIMOTICS GP (General Purpose), SIMOTICS SD (Severe Duty), SIMOTICS M compact motors, explosion-proof motors, fire-rated motors, SynRM variants.

- Recent Developments: In March 2023, Siemens carved out its motors and large drives activities — including low‑ to high‑voltage motors, geared motors and converters — into a separate company called Innomotics, a wholly‑owned subsidiary aimed at strengthening focus and market potential.

- Strategic Focus: Siemens focuses on integrated automation with SIMOTICS motors, SINAMICS drives, and SIRIUS controls, digital lifecycle management via Xcelerator, and expanding its IE4/IE5 portfolio to meet stricter EU Ecodesign standards.

WEG S.A.

WEG, the Americas’ largest LV motor producer, is cost-competitive globally and expanding rapidly in EMEA and Asia-Pacific, dominating Latin American mining, food, and utility sectors while growing in North America through reshoring-driven investments.

- Product & Platform Portfolio: W22 and W50 IE3/IE4 motors; synchronous motors; explosion-proof motors; washdown-rated motors; mining heavy-frame motors; integrated motor-drive-starter packages.

- Recent Developments: In September 2023, WEG S.A. agreed to buy the industrial electric motors and generators business of Regal Rexnord Corporation — including the Marathon, Cemp, and Rotor brands — for about US $400 million.

- Strategic Focus: WEG is extending beyond Latin America into EMEA and North America with an IE4 portfolio, offering integrated motor-drive-starter packages and targeting data centre cooling as a premium growth segment.

Market Concentration Analysis

The global low voltage electric motor market exhibits moderate concentration. The top four players (ABB, Siemens, WEG, Nidec) collectively hold an estimated 45-50% combined revenue share in 2025, with the remaining balance distributed across more than 100 regional and domestic manufacturers, particularly concentrated in China (50+ domestic OEMs), India, and Southeast Asia.

The LV motor market is evolving along a bifurcated path. In developed regions (EMEA, North America), rising regulatory complexity, IE4/IE5 R&D requirements, and the need for global service capabilities are driving consolidation, favoring large OEMs and full-system providers offering integrated motor, VFD, and IoT solutions—evidenced by deals like Nidec and Regal Rexnord’s formation. In contrast, Asian markets, particularly China, remain fragmented and price-driven in the IE3 segment, though leading players like Wolong are expanding globally. Further consolidation is expected as efficiency standards tighten and digital capabilities become critical.

Investment & Growth Opportunities

Fastest-Growing Segments

IE4 (super premium efficiency) motors are the fastest-growing segment, driven by tightening EU efficiency regulations and rising corporate sustainability mandates. IE5 motors, while still niche, are gaining traction in high-duty applications such as data centre cooling and large HVAC systems. At the application level, compressors and commercial HVAC are key growth areas, supported by cold-chain expansion, industrial energy-efficiency programs, and increasing demand from data centres and smart buildings.

Emerging Market Expansion

China represents the largest upgrade opportunity, with its GB18613-2020 standards accelerating the replacement of legacy, inefficient motors. India is witnessing strong growth supported by IS 12615:2018 standards and industrial expansion initiatives such as the PLI scheme. Southeast Asia (Indonesia, Vietnam, Thailand) is emerging as a key demand hub, driven by rapid industrialization across electronics, food processing, and automotive manufacturing.

Venture & Investment Trends

Investment in the LV motor ecosystem is concentrating in three key areas: smart motor systems and IIoT platforms enabling predictive maintenance and performance optimization, integrated motor-drive and energy service models offering retrofit programs with guaranteed savings, and rare-earth-free motor technologies such as SynRM and ferrite-based designs to reduce supply chain risks.

Future Market Outlook (2026-2034)

The global low voltage electric motor market is forecast to grow from USD 15.9 Billion in 2025 to USD 22.0 Billion by 2034 at a CAGR of 3.6%, representing a total incremental revenue addition of USD 6.1 Billion over the nine-year forecast period. Growth is structurally assured by the convergence of mandatory efficiency regulations covering most of the global motor consumption, rising industrial automation investment, and the energy transition, creating new demand vectors in renewable energy infrastructure and data centres.

Three technology shifts will redefine the LV electric motor market through 2034. IE4 will become the effective global baseline as regulations tighten and lifecycle energy savings outweigh upfront costs, with IE5 gaining traction in high-duty applications. PMSM and SynRM motors will increasingly replace induction motors in VFD-driven systems, improving efficiency and OEM revenue per unit. Smart, IoT-enabled motor systems will expand OEM value pools beyond hardware into software, services, and performance-based models.

By 2034, the industry will undergo a structural shift driven by energy transition policies. IE4 will be standard across major markets, while IE5 will dominate high-utilization segments. OEMs with strong high-efficiency portfolios, integrated motor-drive capabilities, and digital platforms will capture disproportionate market share, while laggards risk structural erosion.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with LV electric motor industry stakeholders, including product directors at major OEMs (ABB, Siemens, WEG, Nidec), procurement managers at large industrial end users in HVAC, mining, and food processing, regulatory specialists in the EU and China, energy efficiency consultants, and system integrators. Primary research informed bottom-up unit shipment and revenue estimates by efficiency class, application, end-use industry, and region, and provided qualitative context on adoption barriers and competitive dynamics.

Secondary Research

Secondary sources include IEC 60034-30-1 and IEC 60034-30-2 efficiency standard documentation, EU Ecodesign Regulation (EU) 2019/1781 regulatory text and impact assessments, Chinese National Standard GB18613-2020, CEMEP (European Committee of Manufacturers of Electrical Machines) annual statistics, US DOE motor efficiency rulemaking documents, IEA World Energy Outlook data, company annual reports and investor presentations, trade publications including Drives & Controls and Electric Motor Technology, and industry association data from NEMA and GAMBICA.

Forecasting Models

Market size estimations and growth projections use a combination of bottom-up and top-down forecasting methodologies. Bottom-up estimates aggregate unit shipments by power class, efficiency tier, and application, cross-validated with a top-down analysis from OEM revenue data. Regulatory adoption curves for each major market (EU, US, China) are modelled against historically observed compliance patterns from prior efficiency standard transitions (e.g., EU IE2-to-IE3 transition). Scenario analysis incorporates base, accelerated, and decelerated regulatory compliance cases, with the base case reflecting IMARC's consensus view.

Low Voltage Electric Motor Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Efficiencies Covered | Standard Efficiency, High Efficiency, Premium Efficiency, Super Premium Efficiency |

| End-Use Industries Covered | Commercial HVAC Industry, Food, Beverage and Tobacco Industry, Mining Industry, Utilities, Others |

| Applications Covered | Pumps and Fans, Compressors, Others |

| Region Covered | North and South America, Europe, Middle East and Africa, China, Others |

| Companies Covered | ABB Ltd, Siemens AG, WEG S.A., Nidec Corporation, Wolong Electric Group, Toshiba International, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Low Voltage Electric Motor Market Report

The global low voltage electric motor market was valued at USD 15.9 Billion in 2025, driven by energy efficiency mandates and industrial automation demand.

The market is projected to reach USD 22.0 Billion by 2034, growing at a CAGR of 3.6% during 2026-2034, driven by IE3/IE4 regulatory mandates, data centre expansion, and industrial electrification.

Pumps and Fans lead with a 48.6% share in 2025, driven by widespread deployment in building HVAC, water utilities, and industrial process cooling applications globally.

The Commercial HVAC Industry leads with 32.4% of market revenue in 2025, driven by smart-building programmes, green certifications, and data centre cooling infrastructure expansion.

Europe, Middle East, and Africa lead with a 36.4% share in 2025, driven by the EU Ecodesign Regulation (EU) 2019/1781, which mandates IE3 minimum efficiency across a broad motor range.

Key drivers include mandatory IE3/IE4 efficiency standards (EU, China, US), industrial automation investment, data centre construction, and renewable energy infrastructure expansion.

GB18613-2020 mandated IE3 as the minimum efficiency for LV motors in China from July 2021, triggering the world's largest single motor replacement cycle and adding substantial forecast-period demand.

Leading companies include ABB Ltd, Siemens AG, WEG S.A., Nidec Corporation, Wolong Electric Group, Nidec Corporation, Toshiba International and other.

Super Premium Efficiency (IE4) motors are the fastest-growing efficiency class at ~6.2% CAGR, driven by EU regulatory phase-in and corporate sustainability procurement requirements.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)