3D Concrete Printing Market Size, Share, Trends and Forecast by Product Type, Concrete Type, Printing Type, End Use, and Region 2026-2034

Global 3D Concrete Printing Market Size, Share, Trends & Forecast (2026-2034)

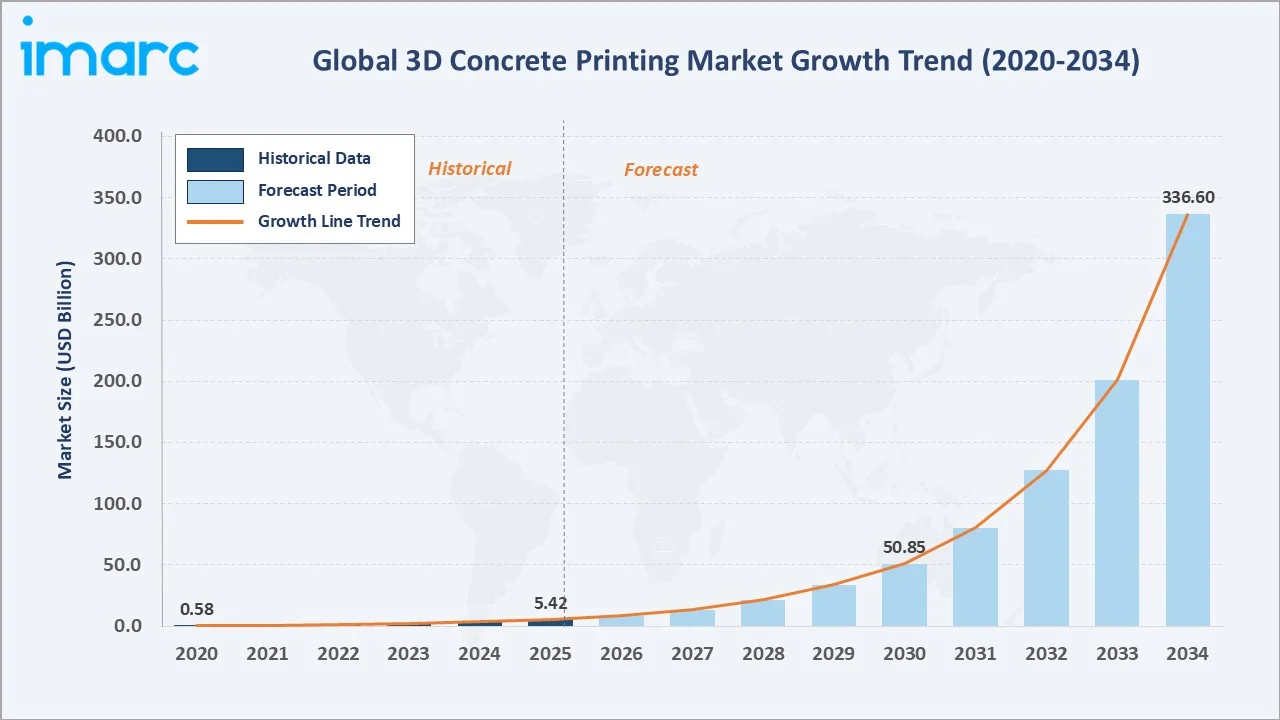

The global 3D concrete printing market size reached USD 5.42 Billion in 2025 and is projected to reach USD 336.60 Billion by 2034, exhibiting a CAGR of 56.45% during 2026-2034. Rising demand for sustainable, cost-effective construction, labour shortages, and accelerating urbanisation are the primary forces driving market growth.

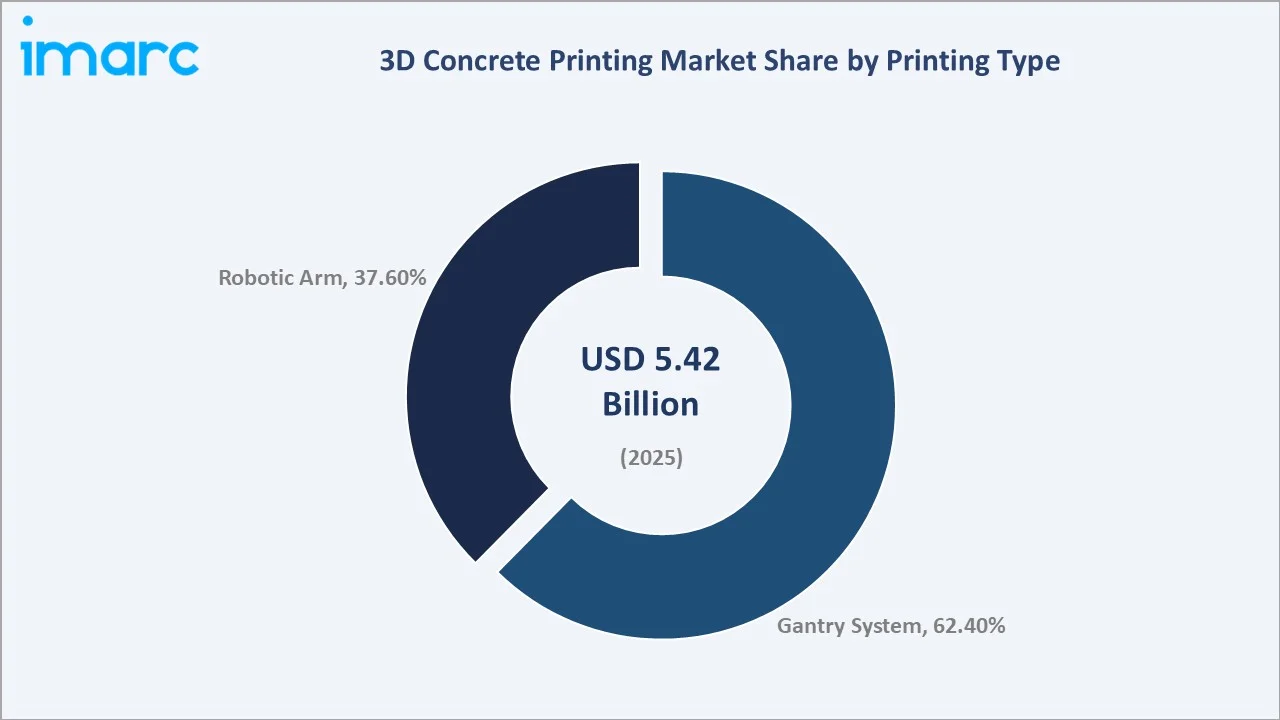

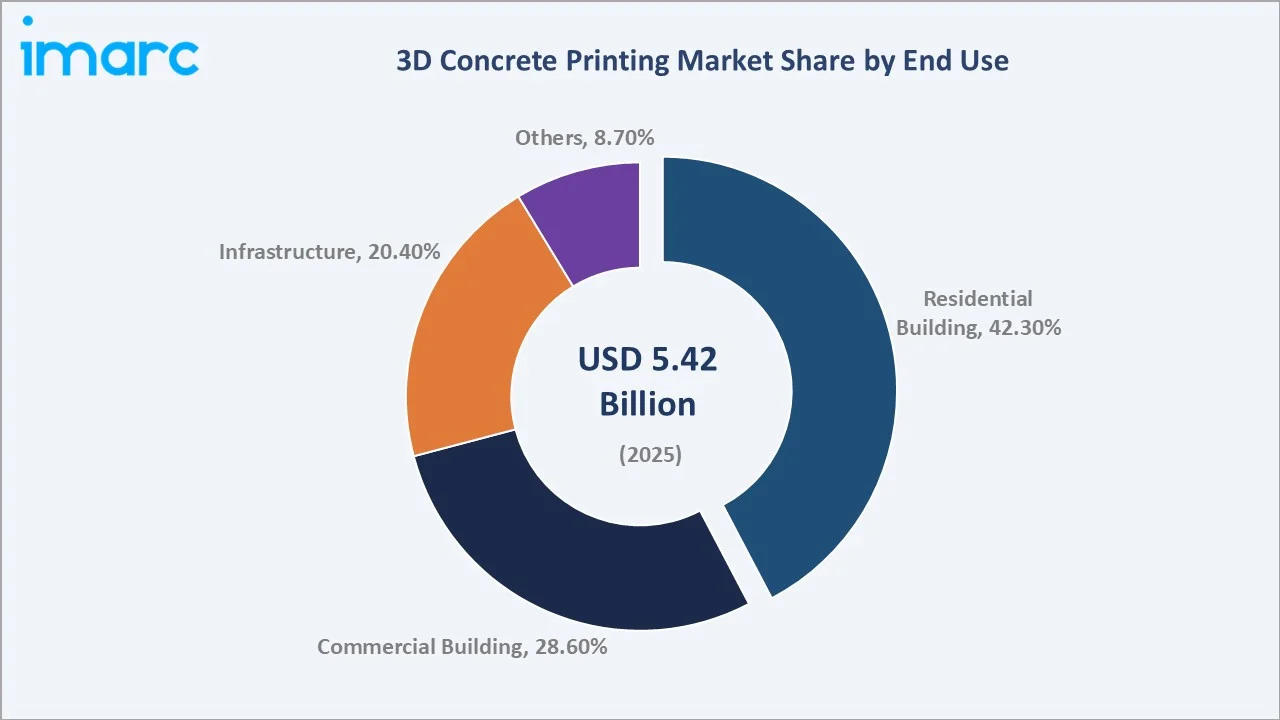

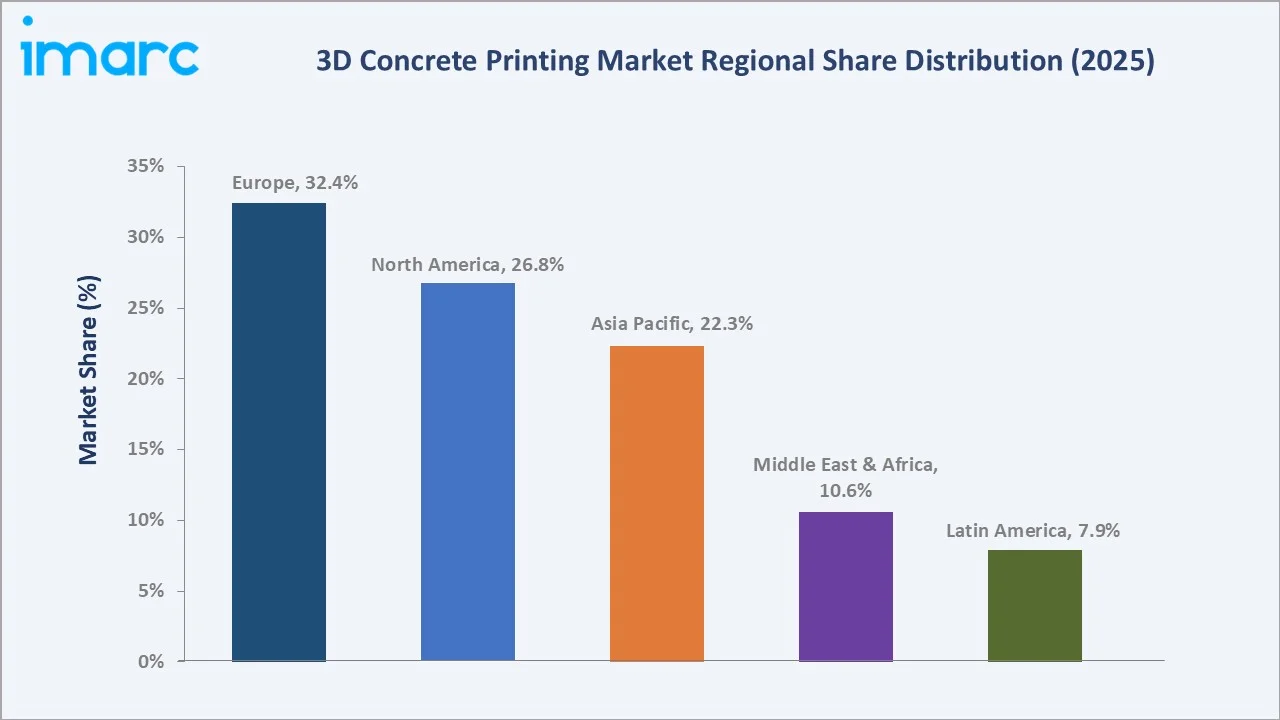

Gantry system dominates printing type at 62.4% in 2025, while residential building leads end use at 42.3%. Europe commands a dominant 32.4% regional share in 2025, reflecting strong regulatory support and early technology adoption.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.42 Billion |

|

Forecast Market Size (2034) |

USD 336.60 Billion |

|

CAGR (2026-2034) |

56.45% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Region |

Europe (32.4% share, 2025) |

|

Second Region |

North America (26.8% share, 2025) |

|

Leading Printing Type |

Gantry System (62.4%, 2025) |

|

Leading End Use |

Residential Building (42.3%, 2025) |

The growth trajectory from 2020 through 2034, with the historical expansion to USD 5.42 Billion in 2025 and the forecast to USD 336.60 Billion in 2034, reflects accelerating construction technology adoption, government-backed affordable housing programmes, and rapid digitalisation of the built environment across both developed and developing economies.

To get more information on this market, Request Sample

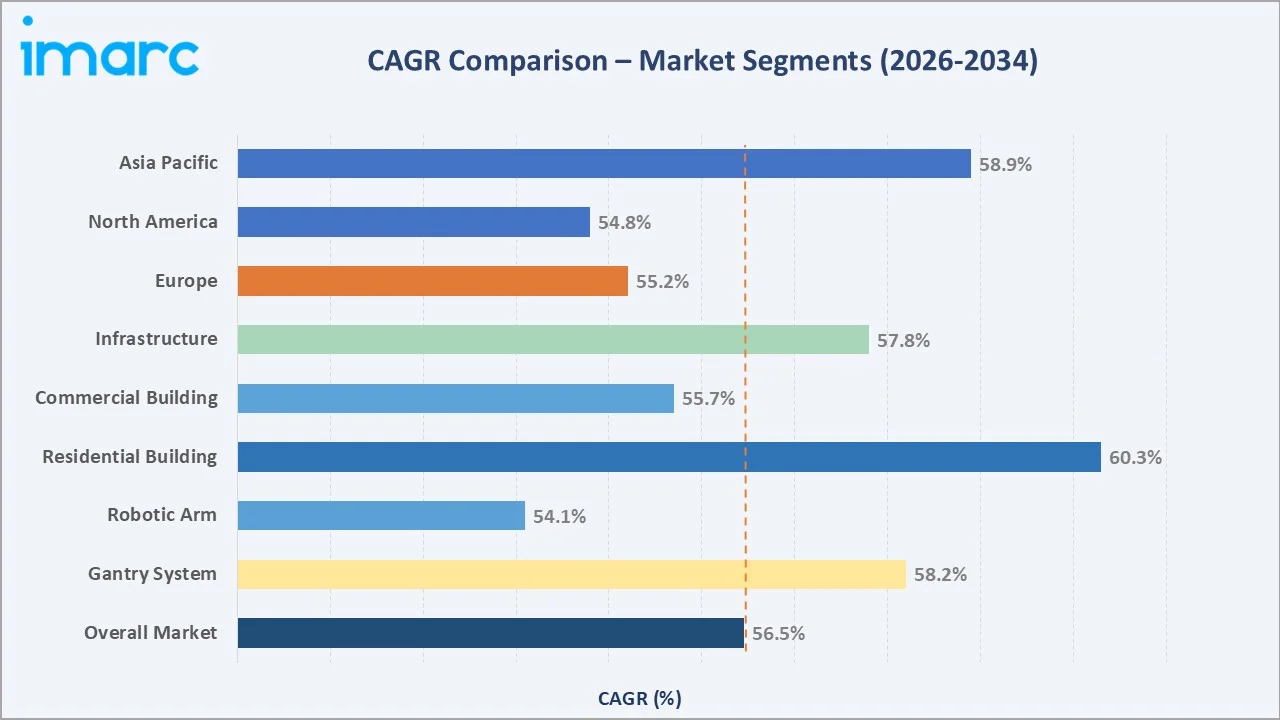

The CAGR trajectories across key printing type, end use, and regional sub-segments reveal that Residential Building applications (~60.3% CAGR) and Gantry System technology (~58.2% CAGR) are the fastest-growing categories within the global 3D concrete printing industry through 2034.

Executive Summary

The global 3D concrete printing market is on an exceptional growth trajectory from USD 5.42 Billion in 2025 to USD 336.60 Billion by 2034. This construction technology, which uses computer-controlled extrusion of specialised concrete mixtures to build structures layer by layer, is transforming the construction sector through speed, design freedom, and waste minimisation.

Gantry System printing dominates at 62.4% in 2025 owing to its large-format printing capability and established use in residential and infrastructure projects. The precision and cost efficiency of gantry systems make them the preferred choice for mass housing and public works globally.

Residential Building commands the largest end-use share at 42.3% in 2025, reflecting acute global housing shortages and the technology's ability to build affordable homes in a fraction of conventional timelines. Europe leads regionally at 32.4% driven by strong R&D investment and progressive building code reforms.

Key Market Insights

| Insight | Data |

|

Largest Printing Type |

Gantry System – 62.4% share (2025) |

|

Fastest-Growing Type |

Robotic Arm – higher architectural flexibility |

|

Leading End Use |

Residential Building – 42.3% revenue share (2025) |

|

Leading Region |

Europe – 32.4% revenue share (2025) |

|

Second Region |

North America – 26.8% revenue share (2025) |

|

Top Companies |

COBOD International A/S, ICON Technology, Inc., Apis Cor, CyBe Construction, XtreeE, Sika AG, Contour Crafting, WASP S.r.l. |

Key Analytical Observations Expanding On The Above Data:

- Gantry System, with 62.4% in 2025, dominates because of its scalability for large structural printing projects including full building facades and infrastructure components. Gantry systems satisfy the broadest range of project specifications for residential and commercial applications globally.

- Residential Building, with 42.3% in 2025, leads end use driven by critical global housing deficits. The UN estimates a need for 96,000 new affordable housing units daily through 2030, creating an enormous structural demand driver for low-cost, rapid 3D printing construction.

- Europe's 32.4% dominance in 2025reflects multiple structural advantages: a dense concentration of 3D printing technology innovators, progressive regulatory frameworks for printed construction, and high labour costs that strongly incentivise automation.

- North America, with 26.8% in 2025, benefits from ICON Technology's large-scale deployment of printed housing communities in Texas and the US Department of Defense investment in military housing and forward-operating base construction using 3D printing.

Global 3D Concrete Printing Market Overview

3D concrete printing is an additive manufacturing process that deposits specially formulated cementitious mixtures through a computer-controlled nozzle, building structures layer by layer without traditional formwork. Systems are configured as either large-frame gantry printers or robotic arm systems, each suited to different structural scales and geometric complexities.

The global ecosystem integrates cement and admixture manufacturers, equipment producers, software and BIM platform providers, construction firms, government housing agencies, and a diverse set of end-use sectors spanning residential, commercial, and civil infrastructure applications across all major global regions.

Market Dynamics

To evaluate market opportunities, Request Sample

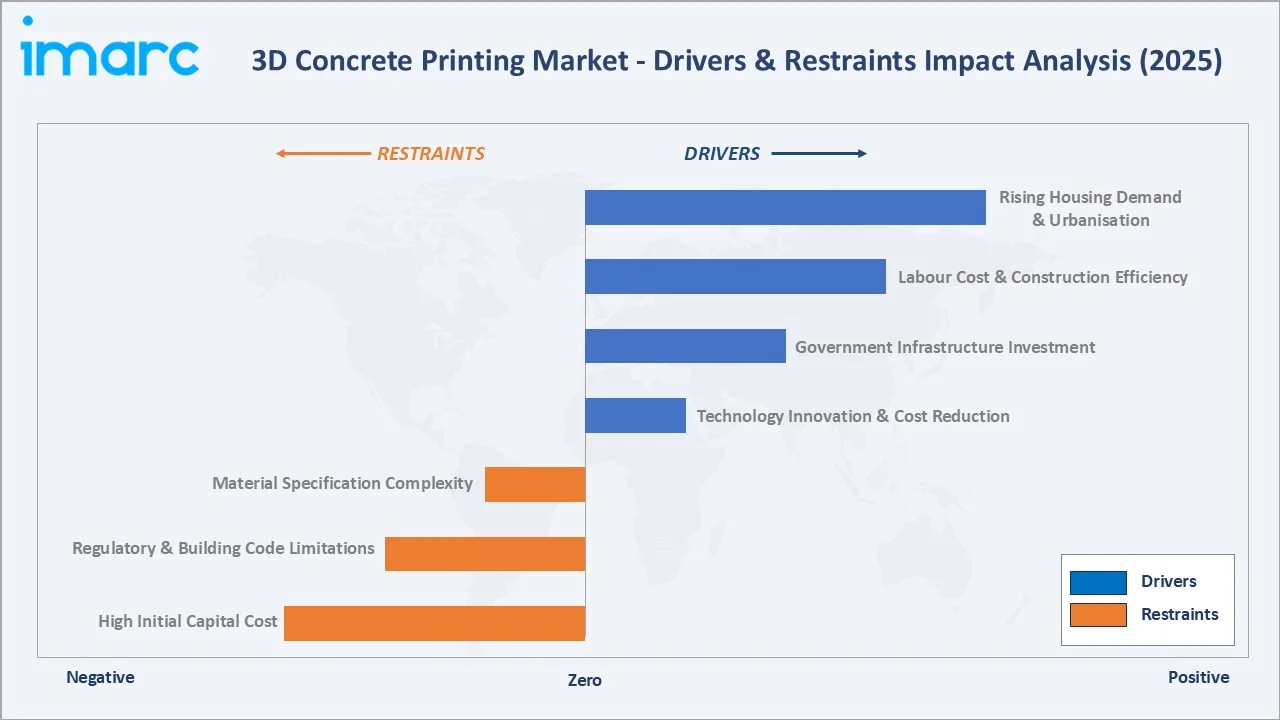

Market Drivers

- Global Housing Shortage and Urbanisation: The UN estimates a need for 96,000 affordable housing units daily globally through 2030. 3D concrete printing reduces construction time by up to 70% and material costs by 30–40%, positioning it as a critical enabler of affordable housing.

- Labour Cost Pressures and Skilled Labour Shortage: The global construction industry faces a structurally skilled labour deficit. In the US alone, the Associated Builders and Contractors report a need for 500,000+ additional workers annually. 3D printing reduces on-site labour requirements significantly.

- Government Infrastructure Investment: Global infrastructure spending is projected to reach USD 94 Trillion by 2040. Government-backed smart city and public housing programmes are directly funding 3D concrete printing pilots and large-scale deployments.

Market Restraints

- High Initial Capital Cost: Industrial-grade 3D concrete printing systems range from USD 300,000 to over USD 2 million per unit, creating significant barriers for small construction firms and limiting adoption in cost-sensitive emerging markets.

- Regulatory and Building Code Limitations: Most national building codes were not designed for additively manufactured structures. Obtaining structural certification and insurance coverage for 3D printed buildings remains complex and market specific.

Market Opportunities

- Disaster Relief and Emergency Housing: Rapid-deployment 3D printing systems can construct emergency shelters within 24 hours, offering immense humanitarian potential. UNHCR and FEMA programmes are actively exploring 3D printed shelter deployment for disaster-affected populations.

- Military and Defence Applications: US Army Corps of Engineers and NATO programmes have funded multiple 3D printed forward-operating base projects. Defence budgets represent a high-value procurement channel with strong appetite for rapid field-deployable construction capability.

Market Challenges

- Material Specification Complexity: Printable concrete mixes must balance workability, open time, and buildability with final structural strength. Standard off-the-shelf concrete mixes are not suitable, requiring specialised mix design and quality control per project.

- Scalability for High-Rise Construction: Current gantry and robotic arm systems are primarily suited for low-rise structures up to 3–5 storeys. Adapting the technology for high-rise and complex multi-use buildings remains a significant engineering and commercial challenge.

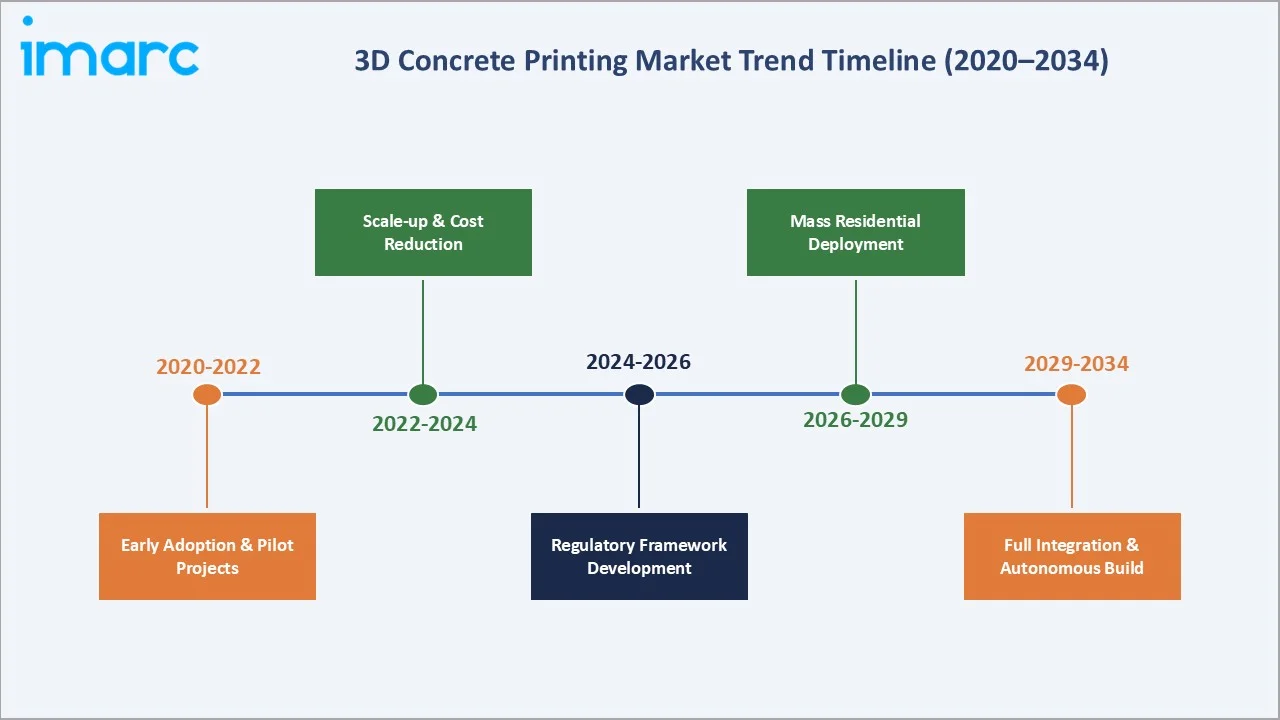

Emerging Market Trend

1. Autonomous Multi-Arm Robotic Printing Systems

Next-generation systems combine multiple coordinated robotic arms to print different structural elements simultaneously, reducing project timelines by an additional 40–60% over single-arm configurations. Companies including COBOD and ICON are actively developing autonomous swarm-printing capabilities.

2. Geopolymer and Low-Carbon Concrete Mix Innovation

Environmental regulations are driving development of geopolymer and slag-based printable mixes that reduce embodied carbon by up to 80% compared to Portland cement. These mixes are increasingly specified in government-funded affordable housing and green infrastructure projects globally.

3. Integration with BIM and Digital Twin Platforms

End-to-end digital workflows connecting BIM design tools, robotic path planning, and live structural monitoring are transforming project delivery accuracy. Autodesk, Trimble, and specialist software providers are developing BIM plug-ins specifically for 3D concrete printing workflows.

4. Mobile and On-Site Printing Systems for Remote Locations

Containerised, mobile printing systems capable of operating in remote and austere environments are expanding the addressable market for 3D concrete printing to rural housing, mining camp infrastructure, and military forward-operating bases where traditional construction logistics are prohibitive.

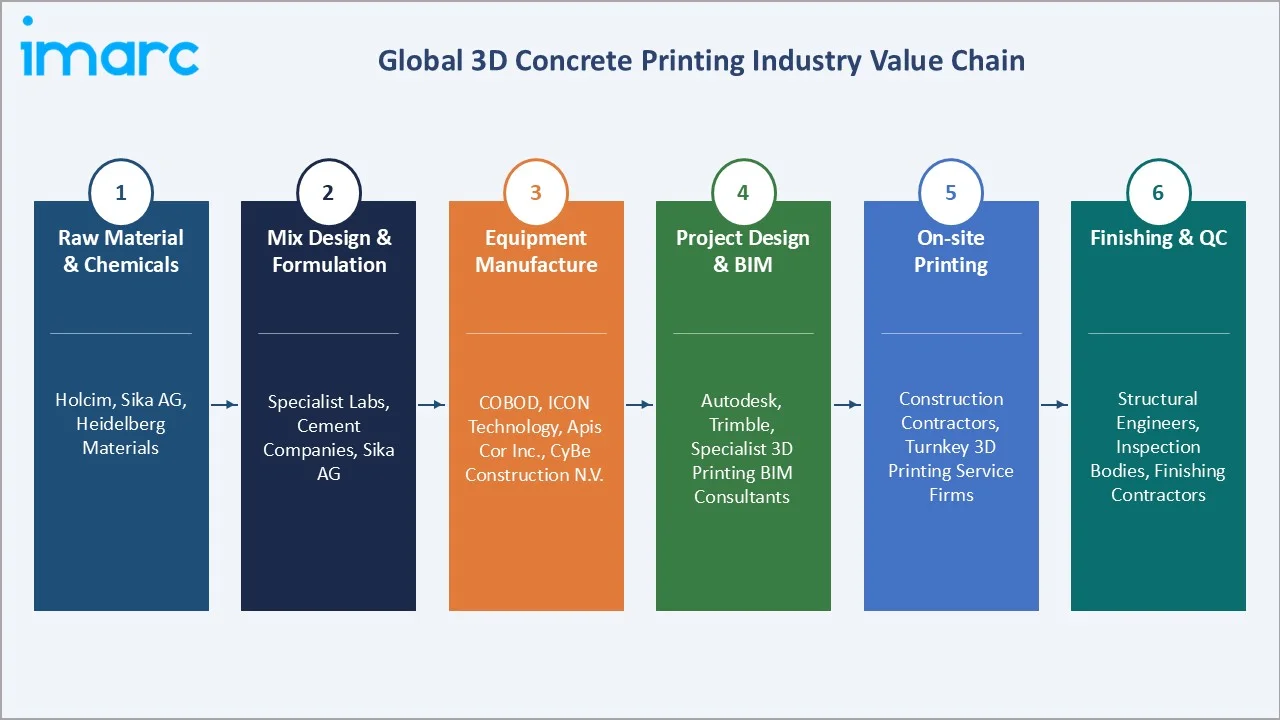

Industry Value Chain Analysis

The 3D concrete printing value chain spans six stages from raw material supply through post-printing finishing. Technology providers and equipment manufacturers capture the highest value-add margins, while specialised mix design and on-site printing generate significant project-specific value.

|

Stage |

Key Players / Examples |

|

Raw Material & Chemicals |

Holcim, Sika AG, HeidelbergMaterials |

|

Mix Design & Formulation |

Specialist labs, cement companies, Sika AG |

|

Equipment Manufacture |

COBOD, ICON Technology, Apis Cor Inc., CyBe Construction N.V. |

|

Project Design & BIM |

Autodesk, Trimble, specialist 3D printing BIM consultants |

|

On-site Printing |

Construction contractors, turnkey 3D printing service firms |

|

Finishing & QC |

Structural engineers, inspection bodies, finishing contractors |

Vertically integrated players such as ICON Technology, which controls mix design, gantry system manufacturing, and project delivery, achieve superior project economics versus standalone equipment vendors. Vertical integration is a key competitive advantage as the market matures and price competition intensifies.

Technology Landscape in the 3D Concrete Printing Industry

Gantry System Technology

Gantry-based printing systems use a frame-mounted extrusion head that traverses X-Y-Z axes to deposit concrete in precise layers. Systems can be configured at building-scale (up to 12m x 12m x 8m) and are well-suited to repetitive residential and modular construction with high printing speed and positional accuracy.

Robotic Arm Systems

6-axis industrial robotic arms adapted for concrete extrusion offer greater freedom of movement and are preferred for complex architectural geometries, curved surfaces, and custom design applications. Their compact footprint makes them suitable for retrofits and constrained urban sites.

Printable Concrete Mix Technology

Advanced admixture systems (retarders, accelerators, viscosity modifiers) enable precise control of concrete open time, pump-ability, and layer bonding strength. Fibre-reinforced printable mixes, incorporating steel, glass, or polypropylene fibres, address structural tensile requirements without traditional rebar in low-rise applications.

Digital Design and Path Planning Software

Slicing software translates BIM architectural models into machine-readable print paths, optimising material deposition efficiency, structural layer sequencing, and real-time monitoring integration. AI-assisted path planning is emerging as a next-generation capability for automated design optimisation.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | 🔒 | 🔒 | 2025 |

| Concrete Type | 🔒 | 🔒 | 2025 |

| Printing Type | Gantry System | 62.4% | 2025 |

| End Use | Residential Building | 42.3% | 2025 |

| Region | Europe | 32.4% | 2025 |

By Printing Type

To access detailed market analysis, Request Sample

Gantry system commands a 62.4% majority share in 2025owing to its structural scalability, established supply chains, and cost efficiency at high print volumes. Gantry systems are the default technology for mass residential construction, public infrastructure, and large commercial building applications globally.

Robotic arm at 37.6% in 2025, and growing fastest, is preferred for complex architectural geometries, renovation and infill projects in constrained sites, and applications requiring curved and non-rectilinear designs. Leading architects and design firms are increasingly specifying robotic arm printing for signature commercial and cultural building projects.

By End Use

Residential building commands a 42.3% majority share in 2025 owing to the acute global housing deficit and the technology's proven ability to deliver habitable structures at dramatically reduced cost and timeline versus conventional methods. Low-rise residential construction is the proven core use case for 3D concrete printing at commercial scale.

Commercial building at 28.6% in 2025 captures growing demand from retail, hospitality, and office developers seeking construction speed advantages and architectural differentiation. Infrastructure at 20.4% encompasses bridges, retaining walls, noise barriers, and utility structures where 3D printing offers time and formwork cost advantages.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe |

32.4% |

Technology leadership; regulatory support; high labour costs driving automation |

|

North America |

26.8% |

ICON deployments; DoD programmes; housing crisis response; CHIPS Act spill-over |

|

Asia Pacific |

22.3% |

India affordable housing; Southeast Asian construction boom |

|

Middle East & Africa |

10.6% |

NEOM & Vision 2030 mega-projects; desert construction challenges favour 3D printing |

|

Latin America |

7.9% |

Social housing programmes; Brazil, Mexico pilot projects; infrastructure deficit |

Europe's 32.4% market dominance in 2025 is driven by a unique combination of technology innovation concentration, high construction labour costs creating strong automation incentives, and proactive regulatory frameworks. The Netherlands, Denmark, France, and Germany collectively host the largest cluster of 3D concrete printing technology companies in the world.

North America, with 26.8% in 2025, is defined by large-scale commercial deployment. ICON Technology has printed over 100 homes in the US and secured a USD 57.2 million contract from NASA for lunar surface construction research. The US faces a structural housing deficit exceeding 3.8 million units, creating an enormous addressable market for 3D printing construction technology.

Competitive Landscape

The global 3D concrete printing market is highly fragmented and innovation-driven, with regional leaders holding strong positions in their home markets while several global technology companies compete across multiple geographies. Europe and North America host the majority of technology-leading companies.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

COBOD International A/S |

BOD2, BOD3 |

Leader |

Europe leader; modular system; global projects |

|

ICON Technology, Inc. |

TITAN |

Leader |

US leader; largest deployment base; NASA partner |

|

Apis Cor |

Frank |

Challenger |

US & global; fastest single-house print record |

|

CyBe Construction |

CyBe RC, CyBe RT, CyBe R, CyBe GR |

Challenger |

Netherlands; infrastructure focus; mortar specialist |

|

XtreeE |

xHead |

Challenger |

France; architectural; complex geometry specialist |

|

Sika AG |

Sikacrete 3D |

Challenger |

Materials global leader; OEM supply to all printers |

|

Contour Crafting |

D-Crafter, CrafTrans, Gantry Crafter |

Emerging |

Pioneering patent portfolio; NASA partnership |

|

WASP S.r.l. |

Crane WASP, Stand-Alone Crane WASP |

Emerging |

Italy; sustainable earth printing; social housing |

Key Company Profiles

COBOD International A/S

COBOD International, headquartered in Copenhagen, Denmark, is Europe's leading 3D construction printing company and one of the most globally deployed large-format concrete printer manufacturers. COBOD's modular BOD2 system is scalable to any building footprint and has been deployed across 30+ countries.

- Product Portfolio: BOD2 and BOD3, among others.

- Recent Developments: In October 2025, Europe’s largest 3D-printed housing project was on an active stage of completion in Denmark, where 36 student apartments were constructed using COBOD’s BOD3 3D construction printer. Developed by 3DCP Group for the housing organization NordVestBO, the project is in Holstebro and spans a total printed area of about 1,654 square meters across six buildings.

- Strategic Focus: COBOD's strategy leverages its modular system architecture to penetrate emerging markets with scalable, lower-cost configurations while maintaining premium technical positioning in European infrastructure and energy transition applications.

ICON Technology, Inc.

ICON Technology, headquartered in Austin, Texas, is the dominant US 3D construction printing company and has achieved the largest commercial housing deployment of any global 3D printing firm. ICON's printer proprietary concrete mix are purpose-engineered as an integrated printing ecosystem.

- Product Portfolio: TITAN

- Recent Developments: In March 2026, ICON introduced its new Titan 3D concrete printer, a large-scale system specifically designed to construct two-storey buildings, marking a major step forward in 3D-printed construction technology. The machine features a massive robotic arm with an extended reach, enabling it to print large structures efficiently. It uses a specialized material, which is designed to reduce carbon emissions compared to traditional concrete, supporting more sustainable construction practices.

- Strategic Focus: ICON's strategy focuses on achieving commercial-scale residential deployment in the US housing market while simultaneously developing next-generation autonomous printing systems for off-planet and extreme-environment construction.

CyBe Construction B.V.

CyBe Construction, headquartered in the Netherlands, is a specialist 3D concrete printing company focused on infrastructure, civil engineering, and custom architectural applications. CyBe manufactures its own robotic arm printing systems and proprietary CyBe Mortar fast-curing printable concrete mix.

- Product Portfolio: CyBe RC, CyBe RT, CyBe R, CyBe GR

- Recent Developments: In October 2022, CyBe announced plans to construct what is expected to be the world’s first four-storey 3D-printed apartment building in Eindhoven, in collaboration with housing developer Lab040. The project aims to push the boundaries of 3D concrete printing by moving beyond low-rise structures into multi-storey residential construction.

- Strategic Focus: CyBe's strategy differentiates through infrastructure and civil engineering specialisation, targeting bridge, tunnel lining, and water management structure applications where its reinforced concrete printing capability provides structural certification advantages.

Sika AG

Sika AG, headquartered in Baar, Switzerland, is a global specialty chemicals company and the dominant supplier of printable concrete admixtures and mix systems to 3D printing equipment manufacturers globally.

- Product Portfolio: Sikacrete 3D

- Recent Developments: In June 2025, Sika expanded its global footprint through a series of strategic investments across multiple regions, reinforcing its “local-for-local” approach to production and innovation. The company has launched advanced manufacturing developments in China, Brazil, and Morocco to better serve regional markets with localized production capabilities.

- Strategic Focus: Sika's strategy positions it as the materials infrastructure provider to the entire 3D concrete printing ecosystem, generating recurring consumables revenue as the installed base of printing systems scales rapidly through 2034.

Market Concentration Analysis

The global 3D concrete printing market is highly fragmented at the global level, with no single company holding more than 8–10% of total global market revenue in 2025. The market is characterised by a large number of specialised regional players, startup technology companies, and large material suppliers who serve the printing equipment market as OEM partners.

Consolidation is accelerating through venture capital and strategic investment. M&A activity is expected to accelerate as the market scales, with major construction material and equipment companies likely to acquire leading technology platforms.

Investment & Growth Opportunities

Fastest-Growing Segments

Residential Building applications at ~60.3% CAGR through 2034 represent the highest-growth end-use segment, driven by global housing deficits and government-funded affordable housing programmes. Gantry System technology at ~58.2% CAGR captures the dominant share of volume growth as large-scale residential projects scale internationally.

Emerging Markets

Middle East and Africa, at ~10.6% share in 2025 and growing rapidly, is the highest-potential emerging region. Saudi Arabia's Vision 2030 programme, which includes the NEOM USD 500 Billion mega-city project, and UAE Smart City initiatives are creating the largest government-funded 3D printing deployment opportunities in any global region.

Venture & Investment Trends

Venture capital investment in 3D construction printing exceeded USD 500 million globally between 2020 and 2025. Key investment themes include software-hardware integrated platforms, autonomous multi-printer systems, and sustainable low-carbon printable concrete materials. Construction technology venture investors view 3D printing as the most transformative single technology in construction since steel frame.

Future Market Outlook (2026-2034)

The global 3D concrete printing market is forecast to expand from USD 5.42 Billion in 2025 to USD 336.60 Billion by 2034 at a CAGR of 56.45%. This extraordinary growth reflects a technology moving from pilot-scale to global commercial deployment across residential, commercial, and infrastructure applications simultaneously.

Three forces will most significantly shape the industry through 2034: the automation imperative driven by global construction labour shortages; government housing mandates in response to urban population growth; and material innovation delivering low-carbon printable concrete that aligns the technology with global net-zero construction commitments.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews in 2024–2025 with 3D concrete printing industry stakeholders, including senior engineers at printer manufacturers, construction project managers, government housing agency officials, and specialty concrete materials scientists. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include IMARC Group market databases, World Bank infrastructure investment data, UN-Habitat global housing reports, IEA construction energy efficiency reports, ASTM and ISO concrete printing standards documentation, company annual reports, and specialist trade publications including Construction Robotics Journal and Concrete Plant International.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanisation indices, construction activity data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative) was performed to account for technology adoption pace uncertainty.

3D Concrete Printing Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Walls, Floors and Roofs, Panels and Lintels, Staircases, Others |

| Concrete Types Covered | Ready-mix, High-density, Precast, Shotcrete, Others |

| Printing Types Covered | Gantry System, Robotic Arm |

| End Uses Covered | Residential Building, Commercial Building, Infrastructure, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | COBOD International A/S, ICON Technology Inc., Apis Cor, CyBe Construction, XtreeE, Sika AG, Contour Crafting, WASP S.r.l., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the 3D concrete printing market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global 3D concrete printing market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the 3D concrete printing industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the 3D Concrete Printing Market Report

The global 3D concrete printing market reached USD 5.42 Billion in 2025, reflecting accelerating adoption of automated construction technology driven by housing shortages and construction labour cost pressures.

The market is projected to reach USD 336.60 Billion by 2034, growing at a CAGR of 56.45% during 2026-2034, driven by residential construction demand, government infrastructure investment, and rapid technology cost reduction.

Gantry System leads with a 62.4% printing type share in 2025, valued for its scalability, structural precision, and cost efficiency at high print volumes across residential and infrastructure applications.

Residential Building leads at 42.3% in 2025, representing the core commercial use case for 3D concrete printing, driven by global housing deficits and the technology's proven ability to reduce build time and cost.

Europe commands a dominant 32.4% market share in 2025, driven by technology innovation concentration, high labour costs incentivising automation, and progressive building code frameworks enabling printed construction.

Leading companies include COBOD International A/S, ICON Technology, Inc., Apis Cor, CyBe Construction, XtreeE, Sika AG, Contour Crafting, WASP S.r.l., and others.

Key applications include affordable residential housing, commercial buildings, road and bridge infrastructure, military and emergency shelter construction, and specialist architectural feature elements.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)