Automotive Ignition Coil Market Size, Share, Trends and Forecast by Type, Product Type, Vehicle Type, Distribution Channel, and Region, 2026-2034

Automotive Ignition Coil Market Size, Share, Trends & Forecast (2026-2034)

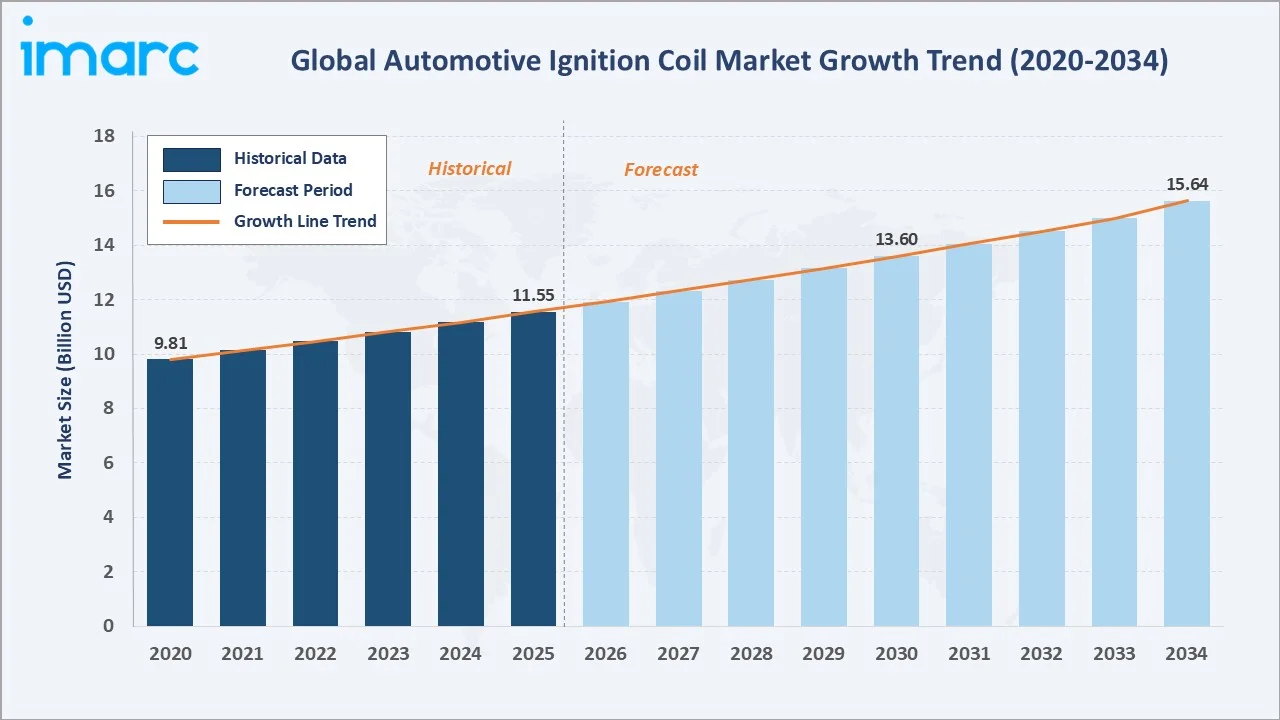

The automotive ignition coil market was valued at USD 11.55 Billion in 2025 and is projected to reach USD 15.64 Billion by 2026-2034, exhibiting a CAGR of 3.32% during 2026-2034. According to the International Organization of Motor Vehicle Manufacturers (OICA), worldwide vehicle production increased from 92.7 Million units in 2024 to 96.4 Million units in 2025 (+3.9%), sustaining strong structural demand for ignition coil components across both OEM and aftermarket channels. Rising aftermarket replacement requirements and expanding internal combustion engine (ICE) vehicle production in emerging economies are the primary drivers shaping market growth.

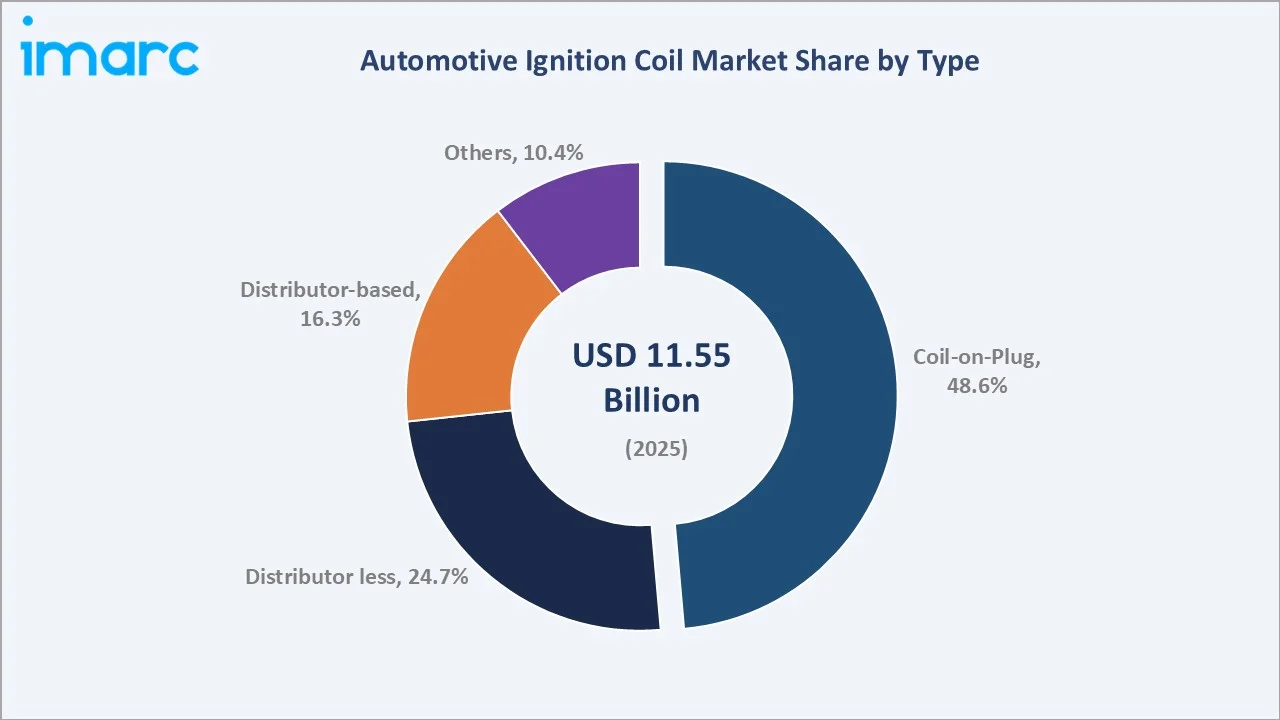

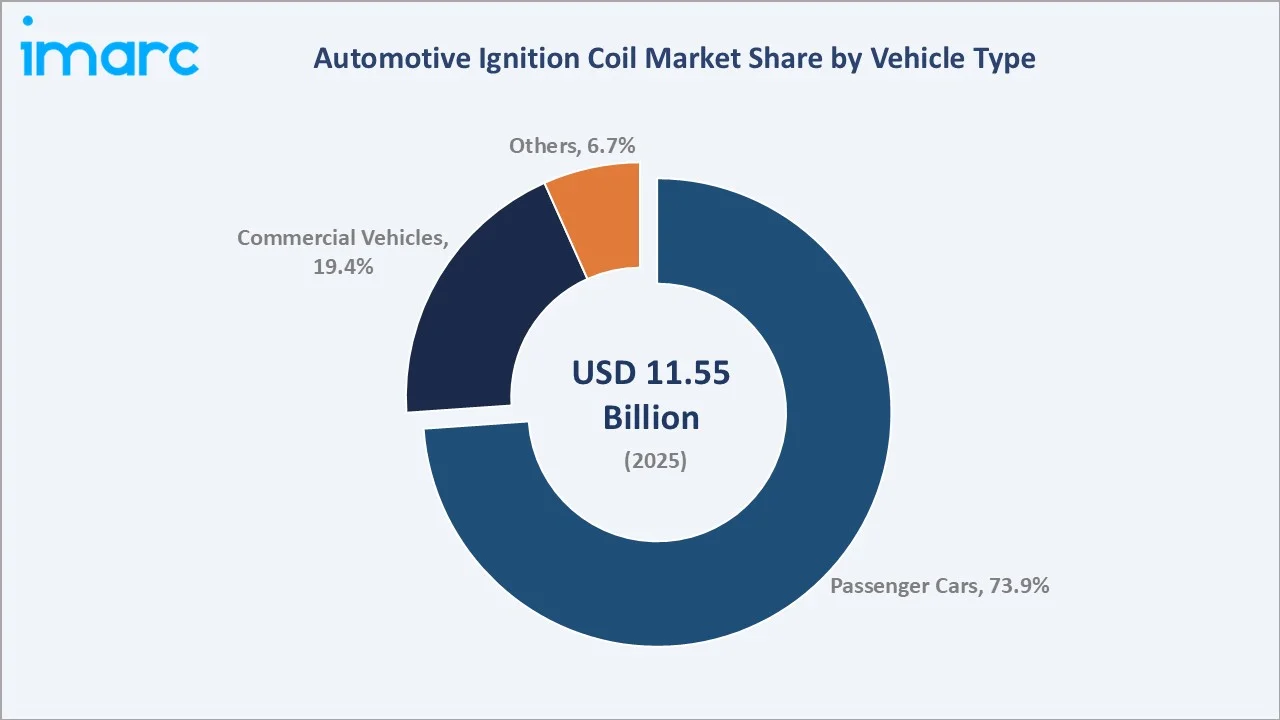

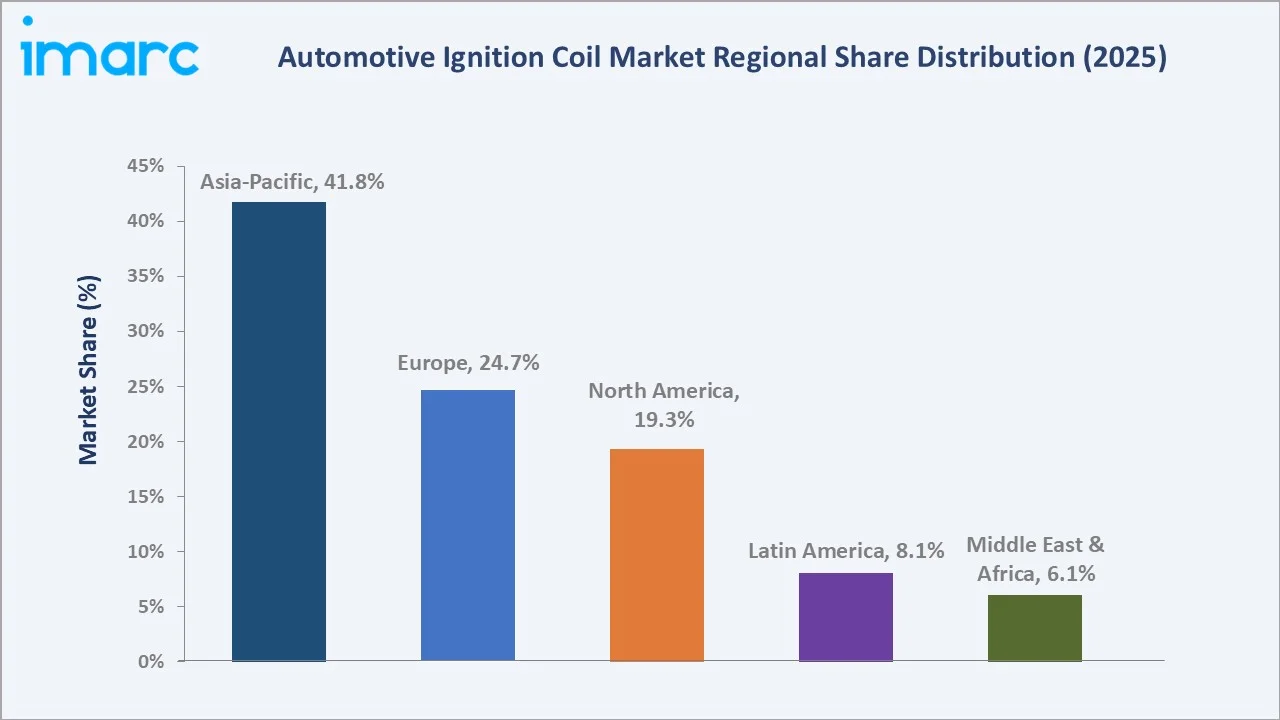

Coil-on-plug leads the type segment at 48.6%, passenger cars dominate vehicle type at 73.9%, and Asia-Pacific commands 41.8% regional share.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 11.55 Billion |

| Forecast Market Size (2026-2034) | USD 15.64 Billion |

| CAGR (2026-2034) | 3.32% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Largest Region | Asia-Pacific (41.8%, 2025) |

| Fastest Growing Region | Latin America (8.1%, 2025) |

| Leading Type | Coil-on-Plug (48.6%, 2025) |

| Leading Vehicle Type | Passenger Cars (73.9%, 2025) |

The automotive ignition coil market expanded from USD 9.81 Billion in 2020 to USD 11.55 Billion in 2025, underpinned by a large and growing global vehicle fleet, steady aftermarket demand, and continued ICE vehicle production in Asia and Latin America. Anchored at USD 13.60 Billion in 2030, the forecast to USD 15.64 Billion by 2034 reflects sustained replacement demand, hybrid vehicle growth, and aftermarket channel expansion.

To get more information on this market, Request Sample

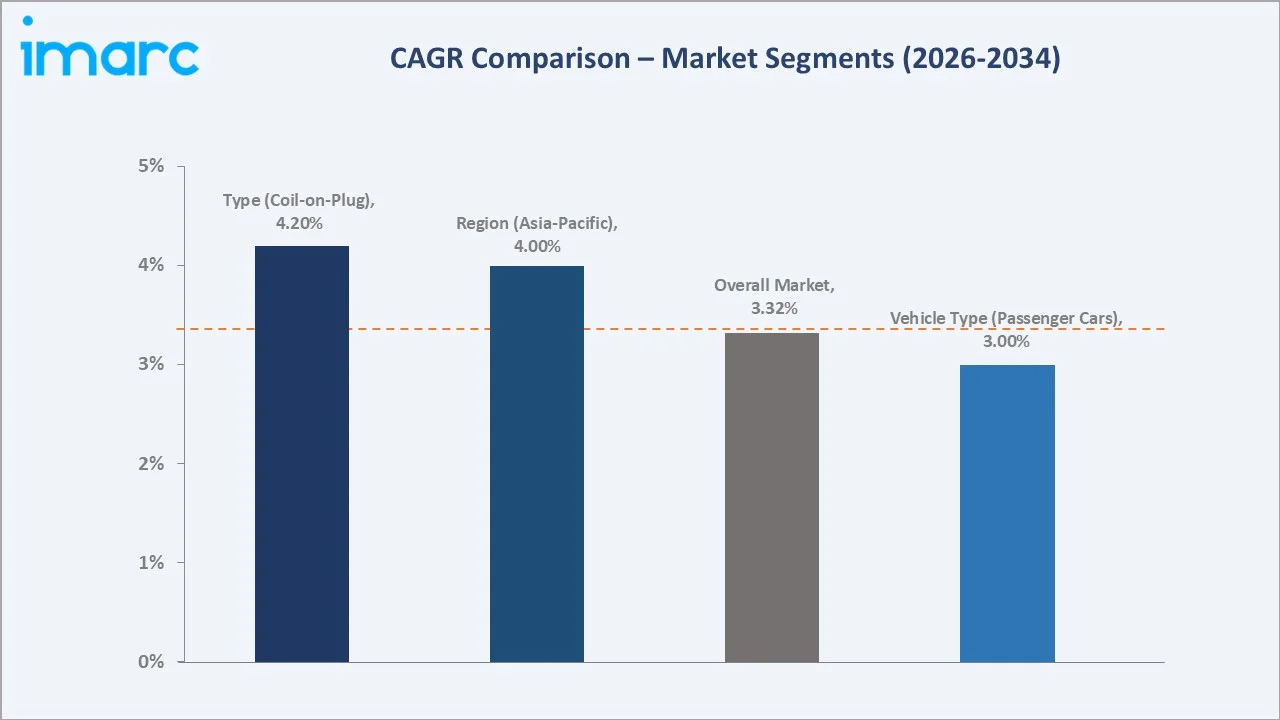

CAGR trajectories across type and vehicle type sub-segments show coil-on-plug and commercial vehicles expanding faster than the overall 3.32% market CAGR, driven by OEM technology upgrades and rising freight logistics demand across emerging economies.

Executive Summary

The automotive ignition coil market is on a steady growth trajectory from USD 9.81 Billion in 2020 to USD 15.64 Billion by 2034. Ignition coils have remained indispensable components in gasoline-powered ICE and hybrid drivetrains, directly influencing fuel efficiency, emissions compliance, and engine reliability. Increasing vehicle parc longevity and the growing replacement demand for high-performance ignition systems are further supporting sustained market expansion across passenger and commercial vehicle segments.

Coil-on-plug leads with 48.6% type share, reflecting OEM preference for precise cylinder-level ignition control. Passenger cars represent 73.9% of demand, anchoring the market firmly to the mass-market automotive segment. Asia-Pacific commands 41.8% share in 2025, driven by high vehicle production volumes in China, Japan, South Korea, and India. As per IBEF, the overall production of passenger vehicles, three wheelers, two wheelers, and quadricycles in January 2026 reached 2.9 Million units.

Key Market Insights

| Insight | Data |

|---|---|

| Leading Type | Coil-on-Plug – 48.6% share (2025) |

| Leading Vehicle Type | Passenger Cars – 73.9% share (2025) |

| Leading Region | Asia-Pacific – 41.8% share (2025) |

| Fastest Growing Region | Latin America – 8.1% share (2025) |

| Top Companies | Robert Bosch GmbH, BorgWarner Inc., Niterra Co., Ltd., Standard Motor Products, Inc., Mitsubishi Electric Corporation |

Key Analytical Observations Expanding On The Data Above:

- Coil-on-plug dominance at 48.6% is driven by OEM adoption in modern ICE engine designs requiring individual coil units per cylinder for improved ignition timing, reduced emissions, and enhanced fuel economy.

- Distributor less share at 24.7% reflects OEM preference for electronically controlled ignition without mechanical distribution components. Modern electronic engine management systems have driven widespread distributor less ignition integration in vehicle platforms across leading global automakers.

- Passenger cars leadership at 73.9% is supported by high global passenger vehicle production volumes and continued reliance on internal combustion engine platforms, where ignition coils remain essential for efficient engine operation, combustion stability, and emissions control.

- Commercial vehicles at 19.4% maintain stable demand due to the continued use of gasoline-powered light commercial fleets, delivery vans, and medium-duty vehicles requiring durable ignition systems capable of supporting high-mileage operating conditions and long service intervals.

- Asia-Pacific at 41.8%: leads the market. In 2024, China manufactured 31.3 Million vehicles (+3.7%), while the overall new vehicle market rose by 4.5% to 31.44 Million vehicles, as reported by CAAM, cementing the region's dominant position in the automotive ignition coil market.

Automotive Ignition Coil Market Overview

Automotive ignition coils are electromagnetic devices that convert low-voltage battery current into the high-voltage electrical pulses required to fire spark plugs in ICEs. They are critical components in gasoline-powered passenger cars, light commercial vehicles, and hybrid electric vehicles (EVs), directly influencing fuel efficiency, emissions compliance, and engine performance across duty cycles.

The industry ecosystem encompasses upstream raw material suppliers, core and winding component manufacturers, coil assembly and testing units, Tier-1 OEM suppliers, aftermarket distributors and retailers, vehicle service centers, and end use vehicle owners. Electrification trends are reshaping the long-term demand profile, while near-to-medium-term growth is supported by an expanding global vehicle parc, aging fleet replacement needs, and ongoing ICE vehicle production in Asia, Latin America, and other emerging regions.

Market Dynamics

To evaluate market opportunities, Request Sample

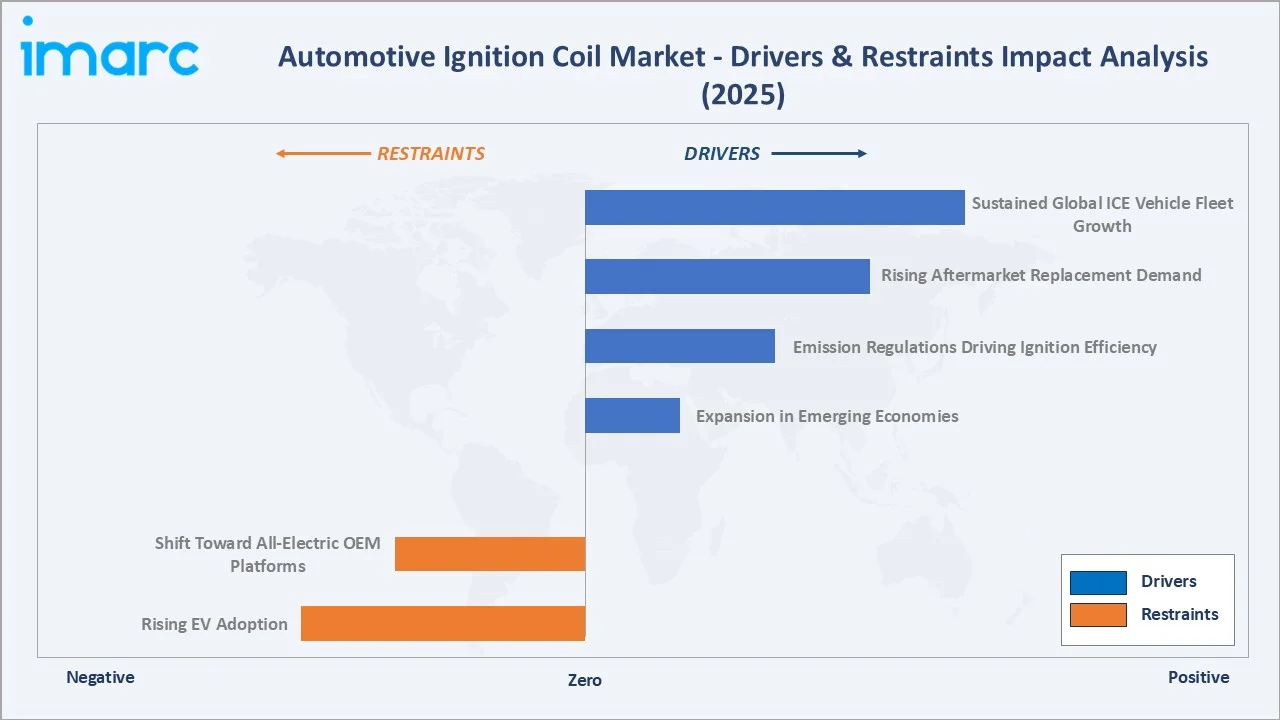

Market Drivers

- Sustained Global ICE Vehicle Fleet Growth: The global vehicle fleet continues to expand, with hundreds of millions of ICE and hybrid vehicles on roads worldwide requiring periodic ignition coil maintenance and replacement. This expanding fleet base provides a durable and predictable demand foundation for both OEM supply and the aftermarket channel.

- Rising Aftermarket Replacement Demand: As per the 2023 edition of ACEA’s ‘Vehicles in use’ report, the average age of passenger cars in the European Union stood at 12.5 years in 2023, driving significant aftermarket demand for engine components, including ignition coils. Aging vehicle populations in North America, Europe, and Asia-Pacific are key drivers.

- Expansion in Emerging Economies: Rising middle-class vehicle ownership in India, Southeast Asia, Latin America, and Africa is driving both new vehicle production and growing aftermarket parts demand. These markets represent a substantial incremental growth opportunity for ignition coil manufacturers seeking to expand beyond mature saturated markets.

- Emission Regulations Driving Ignition Efficiency: Increasingly stringent emission norms in Europe, China, India, and North America are pushing OEMs toward advanced coil-on-plug designs offering more precise ignition timing control. This regulatory pressure is driving continuous product upgrades and supporting premium ignition coil adoption in new vehicle platforms.

Market Restraints

- Rising EV Adoption: The accelerating transition toward battery EVs presents a long-term challenge for the automotive ignition coil market, as fully electric powertrains do not require ignition systems, reducing component demand in new vehicle production.

- Shift Toward All-Electric OEM Platforms: The increasing focus of automakers on all-EV platforms is gradually reducing long-term dependence on internal combustion engine components, creating potential demand pressure for ignition coils in future vehicle production cycles.

Market Opportunities

- Hybrid Vehicle Segment Growth: Mild hybrid and full hybrid EVs retain conventional ignition coil systems for their ICE components. The rapid global adoption of hybrid platforms, particularly across Europe and Asia-Pacific, is expanding the application base for high-performance and advanced ignition coil technologies beyond conventional ICE vehicles.

- Aftermarket Channel Expansion in Emerging Markets: Growing vehicle penetration in India, Brazil, Indonesia, and sub-Saharan Africa is creating a rapidly expanding aftermarket base. Established brands and new entrants with cost-competitive product portfolios are well-positioned to capture this high-growth opportunity through strengthened distribution networks.

Market Challenges

- Raw Material Price Volatility: Copper, silicon steel, and specialty insulation materials are key input commodities for ignition coil manufacturing. Global commodity price fluctuations and supply chain disruptions create margin pressure for manufacturers, particularly those without vertically integrated supply chains or long-term materials contracts.

- Increasing Competition from Low-Cost Manufacturers: The growing presence of low-cost aftermarket ignition coil producers, particularly from China, is intensifying price competition in the global replacement parts segment. Established manufacturers must invest in quality differentiation and brand positioning to protect margin and market share against cost-driven alternatives.

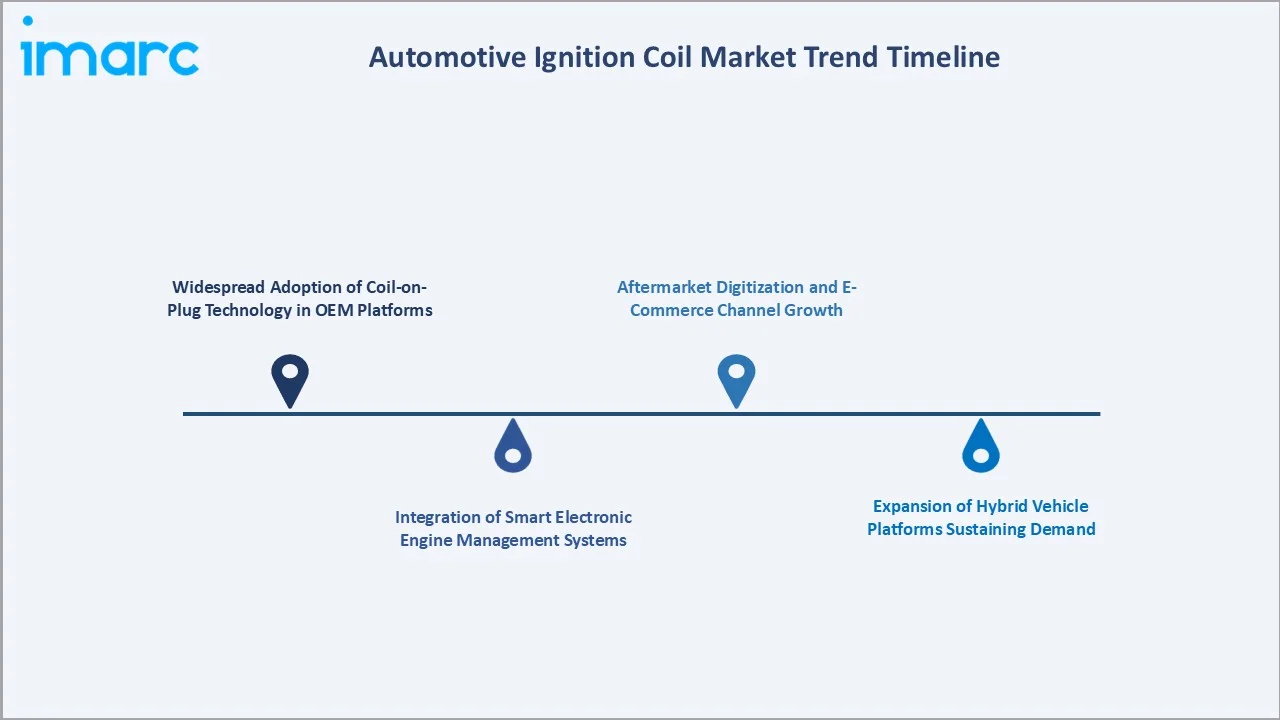

Emerging Market Trends

1. Widespread Adoption of Coil-on-Plug Technology in OEM Platforms

Coil-on-plug designs have become the dominant ignition architecture in modern gasoline engine platforms, replacing older rail and distributor-based systems. Each cylinder receives an individual coil unit, enabling more precise ignition timing control, improved combustion efficiency, and reduced emissions compliance complexity for OEM engineers.

2. Integration of Smart Electronic Engine Management Systems

Advanced ignition coils are increasingly integrated with electronic control unit (ECU) platforms capable of real-time combustion monitoring and adaptive ignition adjustment. The integration with smart engine management systems is elevating the technical requirements for ignition coil products, favoring manufacturers capable of supplying precision-engineered components meeting OEM-grade quality and reliability specifications.

3. Aftermarket Digitization and E-Commerce Channel Growth

The automotive aftermarket is undergoing significant digitization, with e-commerce platforms, digital parts catalogs, and direct-to-consumer channels reshaping how ignition coils reach end users. This shift is lowering barriers to entry for new suppliers while also enabling established brands to expand geographic reach beyond traditional brick-and-mortar distribution networks.

4. Expansion of Hybrid Vehicle Platforms Sustaining Demand

The rapid global proliferation of mild hybrid, full hybrid, and plug-in hybrid vehicle platforms is creating a durable application base for ignition coil systems. Hybrid vehicles retain ICE components requiring ignition coils, and their growing production volumes are partially offsetting demand displacement from pure battery EVs in new vehicle OEM supply channels.

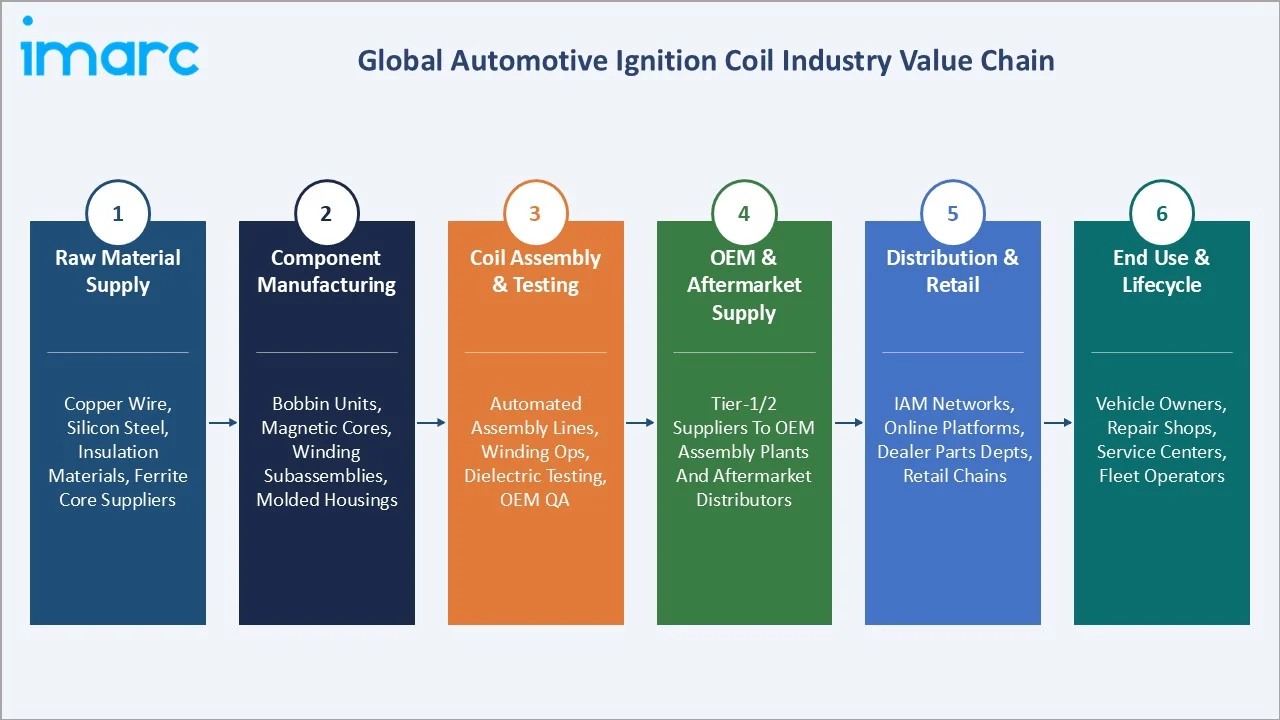

Industry Value Chain Analysis

The automotive ignition coil value chain spans six stages from raw material sourcing through end-of-life vehicle maintenance. Coil assembly and Tier-1 OEM supply stages capture the highest value-add, while aftermarket distribution and installer relationships generate downstream competitive differentiation in this quality-sensitive category.

| Stage | Key Players / Examples |

|---|---|

| Raw Material Supply | Suppliers of copper wire, silicon steel laminations, high-voltage insulation materials, and ferrite cores supporting coil manufacturing |

| Component Manufacturing | Producers of bobbin units, magnetic core assemblies, winding subassemblies, and precision molded housings for ignition coil construction |

| Coil Assembly & Testing | Automated assembly lines, precision winding operations, high-voltage dielectric testing, and OEM-grade quality assurance processes |

| OEM & Aftermarket Supply | Tier-1 and Tier-2 suppliers delivering to automotive OEM assembly plants and wholesale aftermarket distributors globally |

| Distribution & Retail | Automotive parts distributors, independent aftermarket (IAM) networks, online platforms, dealership parts departments, and retail chains |

| End Use & Lifecycle | Vehicle owners, independent repair shops, franchise service centers, fleet operators, and end-of-life vehicle dismantlers |

Vertically integrated players, which manufacture core components and complete ignition coil assemblies in-house, achieve superior cost control and supply security compared with assemblers relying on third-party component sourcing for their manufacturing operations.

Technology Landscape in the Automotive Ignition Coil Industry

Coil Design and Architecture Innovation

Modern ignition coil engineering has advanced significantly toward compact pencil coils and plug-top coil architectures optimized for high energy density and thermal performance. Engineers are focusing on increasing secondary voltage output, extending operational life beyond 100,000 miles, and reducing coil weight and footprint to accommodate increasingly compact engine bay designs in modern vehicle platforms.

Materials and Insulation Technology

Advanced epoxy resin systems and thermoplastic molding materials are replacing older insulation compounds, enabling higher operating temperature resistance and improved dielectric strength. These material innovations are critical for meeting OEM durability requirements in turbocharged and high-performance engine applications where thermal stress on ignition coil components is significantly elevated.

Smart Connectivity and Diagnostics Integration

Next-generation ignition coil designs are increasingly incorporating onboard diagnostic capabilities compatible with OBD-II and advanced ECU architectures. These smart ignition systems enable real-time misfire detection, predictive maintenance scheduling, and integration with vehicle telematics platforms. This technology evolution is elevating product complexity and supporting premium pricing in the OEM supply channel.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Coil-on-Plug |

48.6% |

2025 |

|

Product Type |

🔒 |

🔒 |

2025 |

|

Vehicle Type |

Passenger Cars |

73.9% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

Asia-Pacific |

41.8% |

2025 |

By Type

Coil-on-plug commands a 48.6% majority share in 2025, driven by its widespread adoption in modern multi-cylinder gasoline engines requiring dedicated coil units per cylinder. These systems deliver superior ignition energy precision and enable individual cylinder misfire detection, making them the preferred architecture for OEM design engineers focused on emissions compliance and engine efficiency

To access detailed market analysis, Request Sample

Distributor less accounts for 24.7% share, supported by electronically controlled ignition platforms favored in mid-range and performance vehicle segments. Reduced mechanical complexity and improved ignition precision continue to support adoption across modern engine architectures requiring enhanced reliability, lower maintenance, and optimized combustion efficiency.

By Vehicle Type

Passenger cars dominate with a 73.9% share in 2025, reflecting the overwhelming dominance of the passenger vehicle segment in global vehicle production and fleet composition. The mass-market passenger car category drives the largest absolute volume of ignition coil demand across both new vehicle OEM supply and aftermarket replacement channels.

Commercial vehicles account for 19.4% share, with demand anchored by medium- and heavy-duty trucks, vans, and commercial fleet operators. This segment benefits from fleet-driven replacement cycles and sustained freight transport demand across major logistics economies in Asia, North America, and Europe.

Regional Market Insights

| Region | Share (2025) | Key Growth Drivers |

|---|---|---|

| Asia-Pacific | 41.8% | High vehicle production volumes, expanding middle-class vehicle ownership, and growing aftermarket parts demand across major economies |

| Europe | 24.7% | Established OEM supply chains, aging vehicle fleet driving aftermarket demand, and stringent emissions standards supporting premium coil adoption |

| North America | 19.3% | Large and aging vehicle fleet, strong aftermarket infrastructure, and demand for high-quality replacement ignition components |

| Latin America | 8.1% | Rising vehicle penetration, expanding middle-class car ownership, and growing demand for cost-competitive aftermarket ignition products |

| Middle East and Africa | 6.1% | Growing vehicle parc, infrastructure expansion, and increasing demand for automotive parts supporting emerging aftermarket channels |

Asia-Pacific at 41.8% in 2025 leads the global market, anchored by China, Japan, South Korea, and India. China's position as the world's leading vehicle producer generates enormous OEM coil demand, while Japan and South Korea contribute technology-intensive OEM manufacturing. India's rapidly growing middle-class vehicle market is expanding the regional aftermarket opportunity.

Europe at 24.7%, benefits from a mature OEM supply chain ecosystem and one of the world's oldest average vehicle fleet ages, which generates sustained aftermarket replacement demand. Continued production of hybrid and internal combustion engine vehicle platforms across key European automotive manufacturing hubs further supports stable ignition coil consumption in the region.

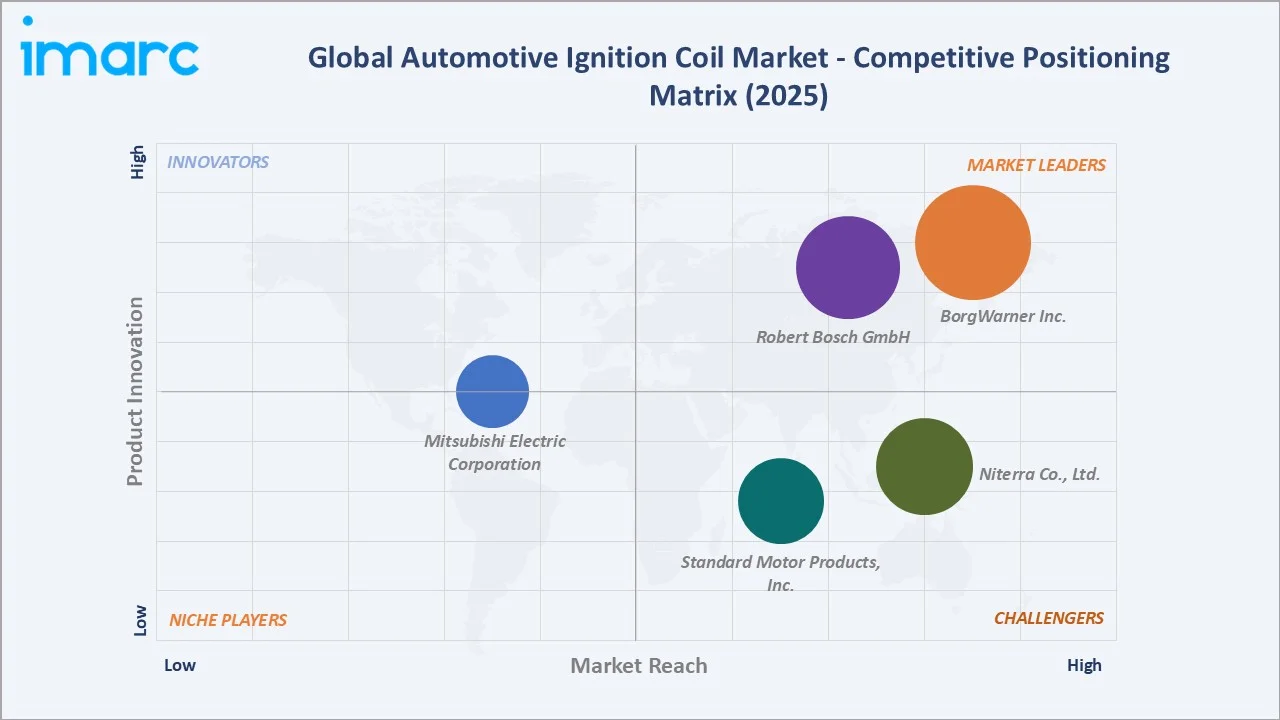

Competitive Landscape

The automotive ignition coil market is moderately concentrated, with global Tier-1 suppliers dominating OEM supply channels while a fragmented aftermarket segment includes dozens of regional and specialty manufacturers. OEM certification, quality consistency, product coverage breadth, and distribution network depth form the key competitive moats in this technically demanding market.

| Company Name | Brand / Key Product | Position | Strategic Focus |

|---|---|---|---|

| Robert Bosch GmbH | Bosch Ignition Coils | Leader | OEM supply leadership and global aftermarket expansion |

| BorgWarner Inc. | BERU | Leader | Propulsion systems integration and aftermarket distribution |

| Niterra Co., Ltd. | NGK Ignition Coils | Challenger | Ignition component quality and balanced OEM and aftermarket channel strategy |

| Standard Motor Products, Inc. | Blue Streak | Challenger | Aftermarket catalog breadth and North American distribution network |

| Mitsubishi Electric Corporation | Ignition Coil | Emerging | Automotive electronics supply and OEM relationships |

Key players include Robert Bosch GmbH, BorgWarner Inc., Niterra Co., Ltd., Standard Motor Products, Inc., and Mitsubishi Electric Corporation, among others.

Key Company Profiles

Robert Bosch GmbH

Robert Bosch GmbH is a leading global automotive supplier and a recognized leader in ignition coil systems, serving OEM vehicle manufacturers and the independent aftermarket across major global regions. The company produces a broad range of ignition coil architectures suited to modern and legacy gasoline engine platforms.

- Product Portfolio: A comprehensive range of ignition coil products, including distributor ignition coils, for passenger cars and commercial vehicles across a wide range of engine configurations and vehicle platforms.

- Recent Developments: Robert Bosch revealed the inclusion of 82 aftermarket automotive part numbers across various product categories in the first quarter of 2025, expanding coverage to almost 63 Million vehicles on the road. Additional part numbers were incorporated into Bosch sensors, brakes, ignition coils, spark plugs, fuel injectors, valves, and A/C compressors.

- Strategic Focus: OEM supply leadership, global aftermarket expansion, and sustained investment in ignition product quality and coverage breadth across key automotive markets.

BorgWarner Inc.

BorgWarner Inc. is a global automotive components supplier with an established presence in ignition coil systems, marketing products under the BERU brand across OEM and aftermarket channels. The company serves a broad range of vehicle manufacturers and independent aftermarket customers globally.

- Product Portfolio: BERU branded ignition coil products for passenger cars and light commercial vehicles, covering a range of coil-on-plug and rail coil configurations for OEM and independent aftermarket distribution channels globally.

- Recent Developments: BorgWarner Inc. continues to maintain and develop its ignition coil product range under the BERU brand, supporting OEM customer programs and expanding aftermarket coverage across key vehicle markets in Europe, North America, and Asia-Pacific.

- Strategic Focus: Propulsion systems integration, aftermarket channel development under the BERU brand, and alignment of ignition product strategy with broader powertrain portfolio objectives.

Market Concentration Analysis

The automotive ignition coil market is moderately concentrated. The top five companies (Robert Bosch GmbH, BorgWarner Inc., Niterra Co., Ltd., Standard Motor Products, Inc., and Mitsubishi Electric Corporation) are estimated to collectively account for approximately 50-60% of global market revenue in 2025.

Barriers to entry include OEM qualification requirements, multi-year Tier-1 supplier certification processes, broad application coverage catalog requirements for aftermarket participation, and the manufacturing capability needed to consistently produce high-voltage ignition components meeting OEM-grade quality and durability standards.

Consolidation is progressing through OEM platform standardization, aftermarket catalog acquisitions, and distribution network partnerships. Scale advantages in manufacturing, application engineering, and after-sales support are reinforcing the competitive position of established Tier-1 suppliers while creating meaningful challenges for smaller aftermarket-only participants.

Investment & Growth Opportunities

Fastest-Growing Segments

Coil-on-plug at 48.6% expands above the overall 3.32% market CAGR, driven by continued OEM platform standardization on this architecture. Commercial vehicles at 19.4% comprise the fastest-growing vehicle type category, supported by expanding freight logistics demand and commercial fleet growth across Asia-Pacific and emerging markets.

Emerging Markets

Latin America at 8.1% share represents the fastest-growing region through 2034, with Brazil, Mexico, and Argentina driving both new vehicle demand and expanding aftermarket channel development. India, Indonesia, and Vietnam represent the largest untapped Asia-Pacific growth opportunities as rising income levels, expanding road infrastructure, and growing vehicle penetration unlock mass-market aftermarket demand.

Venture & Investment Trends

Investment is concentrated in advanced ignition coil manufacturing automation, smart diagnostic ignition technologies compatible with connected vehicle platforms, and aftermarket e-commerce distribution capabilities. Manufacturers are also investing in hybrid vehicle ignition coil designs capable of meeting elevated thermal and electrical performance requirements in next-generation mild hybrid and full hybrid powertrain platforms.

Future Market Outlook (2026-2034)

The automotive ignition coil market is forecast to expand from USD 11.55 Billion in 2025 to USD 15.64 Billion by 2034 at a CAGR of 3.32%, adding approximately USD 4.09 Billion in incremental annual market value over the forecast period.

Four forces will shape the market through 2034: continued growth of the global vehicle parc driving aftermarket replacement demand; hybrid vehicle proliferation expanding the application base for advanced ignition coil systems; emerging market vehicle penetration unlocking new aftermarket opportunities; and OEM platform standardization on coil-on-plug architecture reinforcing segment leadership.

By 2034, coil-on-plug designs are expected to account for an even larger share of both OEM and aftermarket demand as vehicle fleets globally continue aging and legacy distributor-based vehicles phase out. The aftermarket channel will become the primary demand driver as EV penetration gradually reduces new-vehicle OEM ignition coil volumes, with the large installed ICE fleet sustaining replacement demand through the mid-2030s.

Research Methodology

Primary Research

Primary research included interviews with procurement managers at leading automotive OEMs, senior product engineers at ignition coil manufacturers, aftermarket distribution executives, and independent automotive service industry experts. These discussions validated market sizing, segment share estimates, regional demand dynamics, and technology adoption trends.

Secondary Research

Secondary sources included IEA global energy and transport reports, ACEA European automotive fleet data, company annual reports, press releases, investor presentations from listed manufacturers, patent filings, and industry trade association publications from automotive aftermarket organizations.

Forecasting Models

Market forecasts used top-down and bottom-up models combining global vehicle production volumes, regional vehicle parc size and age composition, replacement cycle frequencies, segment share evolution, and pricing trends. Scenario analysis addressed EV penetration rate variation, commodity price sensitivity, and emerging market growth rate assumptions.

Automotive Ignition Coil Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Coil-on-Plug, Distributor-based, Distributor less, and Others |

| Products Types Covered | Can-type Ignition Coil, Electronic Distributor Coil, Double Spark Coil, Pencil Ignition Coil, Ignition Coil Rail, and Others |

| Vehicle Types Covered | Passenger Cars, Commercial Vehicles, and Others |

| Distribution Channels Covered | OEM, Aftermarket |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Robert Bosch GmbH, BorgWarner Inc., Niterra Co., Ltd., Standard Motor Products, Inc., Mitsubishi Electric Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Automotive Ignition Coil Market Report

The market was valued at USD 11.55 Billion in 2025, driven by sustained ICE vehicle production, growing vehicle parc, and rising aftermarket replacement demand globally.

The market is projected to grow at a 3.32% CAGR from 2026-2034, reaching USD 15.64 Billion, supported by aftermarket demand and hybrid vehicle growth.

Coil-on-plug leads at 48.6% in 2025, driven by OEM standardization on individual-coil-per-cylinder architectures for improved emissions and efficiency.

Passenger cars dominate at 73.9% in 2025, reflecting the mass-market dominance of the passenger vehicle segment in global vehicle production and fleet composition.

Asia-Pacific leads with 41.8% share in 2025, anchored by China, Japan, South Korea, and India's combined vehicle production and expanding aftermarket demand.

Leading players include Robert Bosch GmbH, BorgWarner Inc., Niterra Co., Ltd., Standard Motor Products, Inc., and Mitsubishi Electric Corporation.

Rising EV adoption introduces long-term demand displacement risk for new-vehicle OEM supply, while the large existing ICE fleet sustains robust aftermarket demand through the 2030s.

Aging vehicle fleet populations, regular replacement cycles for worn ignition components, and growing vehicle parc in emerging markets are primary drivers of aftermarket demand growth.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)