Brazil Diabetes Market Size, Share, Trends and Forecast by Segment and Distribution Channel, 2026-2034

Brazil Diabetes Market Size, Share, Trends & Forecast (2026-2034)

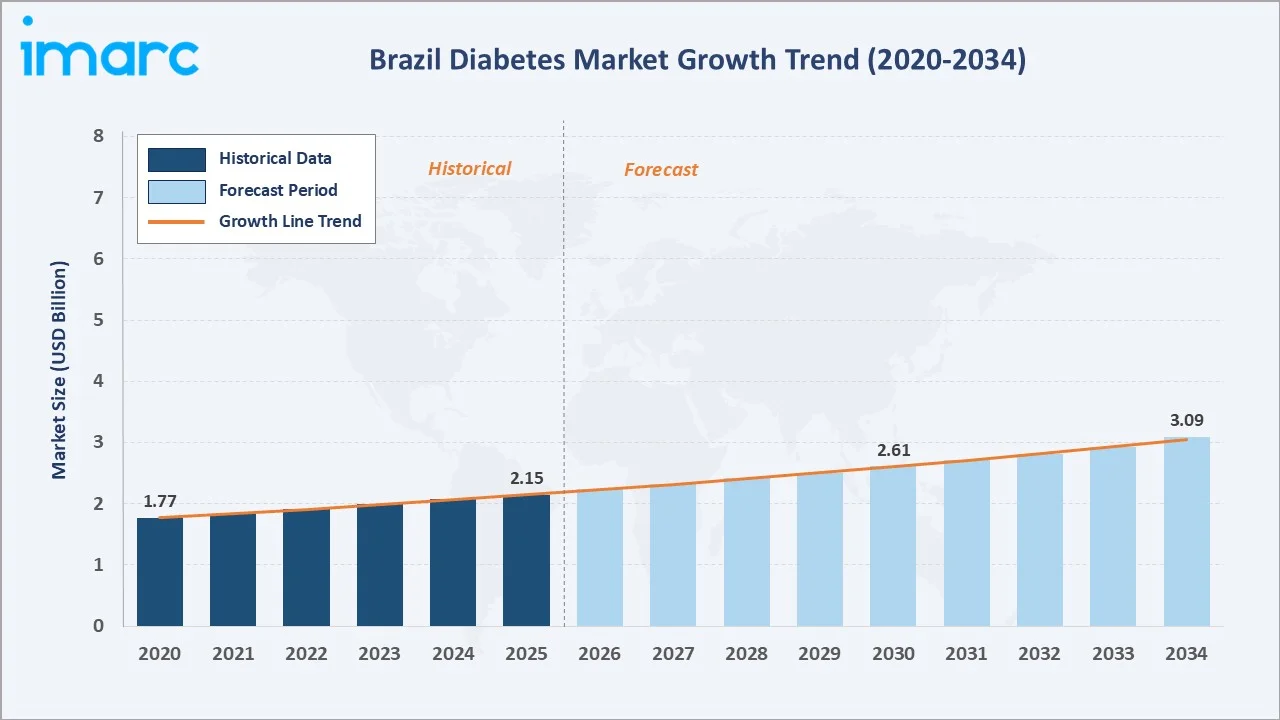

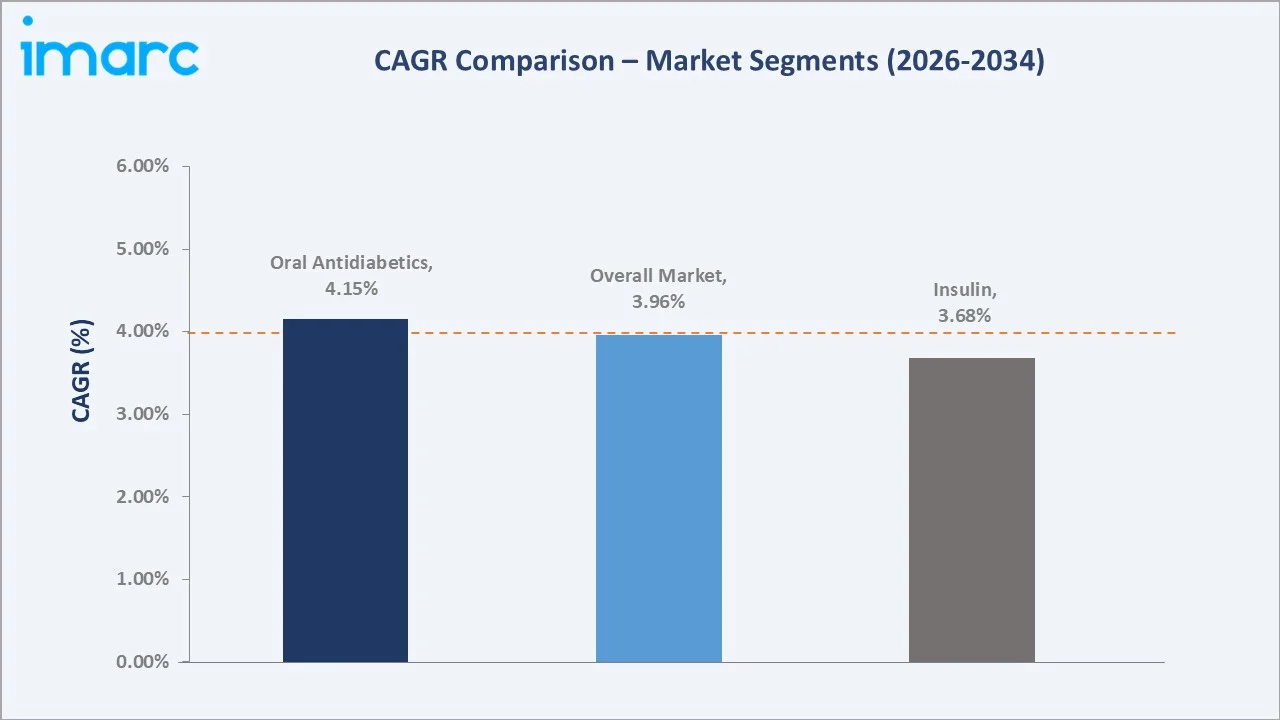

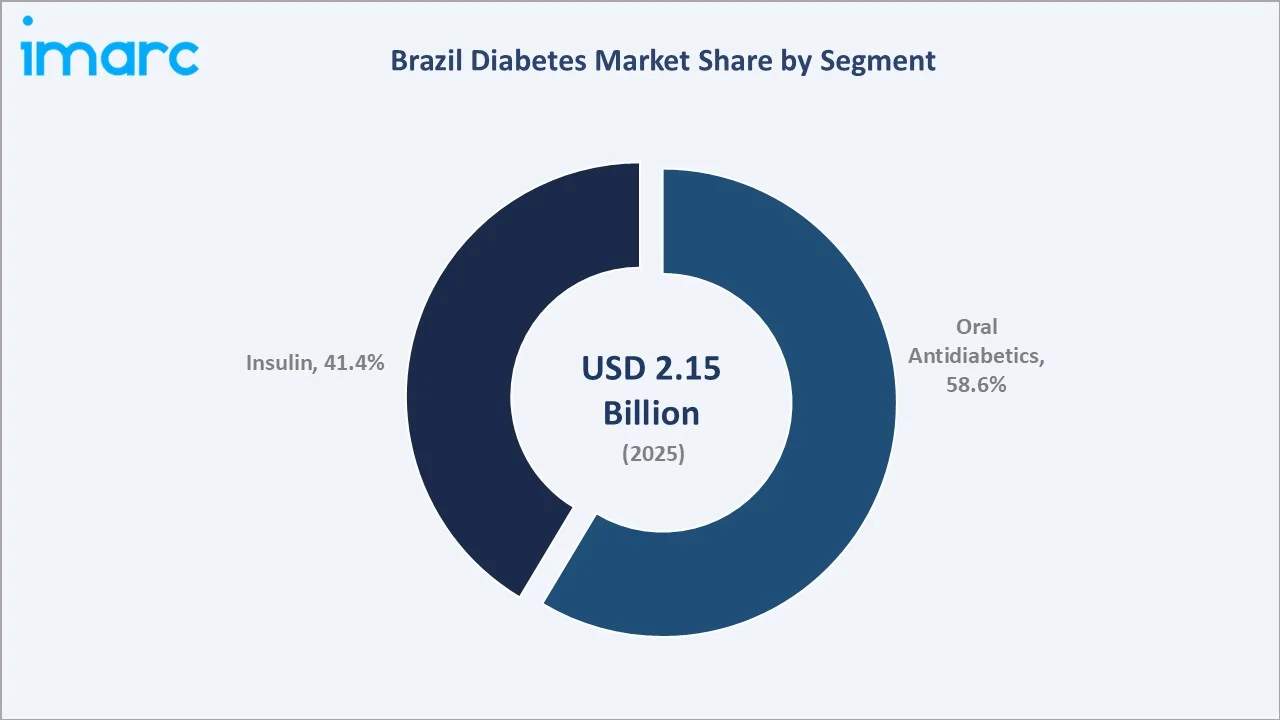

The Brazil diabetes market reached USD 2.15 Billion in 2025 and is projected to reach USD 3.09 Billion by 2034, growing at a CAGR of 3.96% during 2026 to 2034. Rising diabetes prevalence driven by urbanization, sedentary lifestyles, and an ageing population are the primary market catalysts. Brazil hosts one of the largest diabetic populations in Latin America, creating sustained demand for both oral antidiabetics and insulin therapies.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.15 Billion |

|

Forecast Market Size (2034) |

USD 3.09 Billion |

|

CAGR (2026-2034) |

3.96% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Segment |

Oral Antidiabetics – 58.6% share (2025) |

|

Leading Distribution Channel |

Retail Pharmacies – 38.5% share (2025) |

The Brazil diabetes market demonstrated a steady CAGR of approximately 3.96% during 2026–2034. This growth trajectory was shaped by a confluence of rising Type-2 diabetes incidence, broader SUS Farmacia Popular coverage of oral antidiabetic medications, and post-pandemic recovery in pharmaceutical consumption across all Brazilian regions.

To get more information on this market, Request Sample

Looking ahead, the forecast period (2026–2034) is driven by the progressive entry of biosimilar insulin products reducing cost barriers, the rapid commercialization of GLP-1 receptor agonists (semaglutide, dulaglutide) capturing premium market spend, and the acceleration of e-commerce and tele-pharmacy distribution expanding patient reach across Brazil's underserved North and Northeast regions.

Executive Summary

The Brazil diabetes market is on a sustained upward trajectory, underpinned by an escalating burden of Type-2 diabetes, growing public health investments under the Sistema Unico de Saude (SUS), and the increasing adoption of digital health and tele-pharmacy platforms. The market reached USD 2.15 Billion in 2025 and is forecast to surpass USD 3.09 Billion by 2034, reflecting a CAGR of 3.96% across the forecast period.

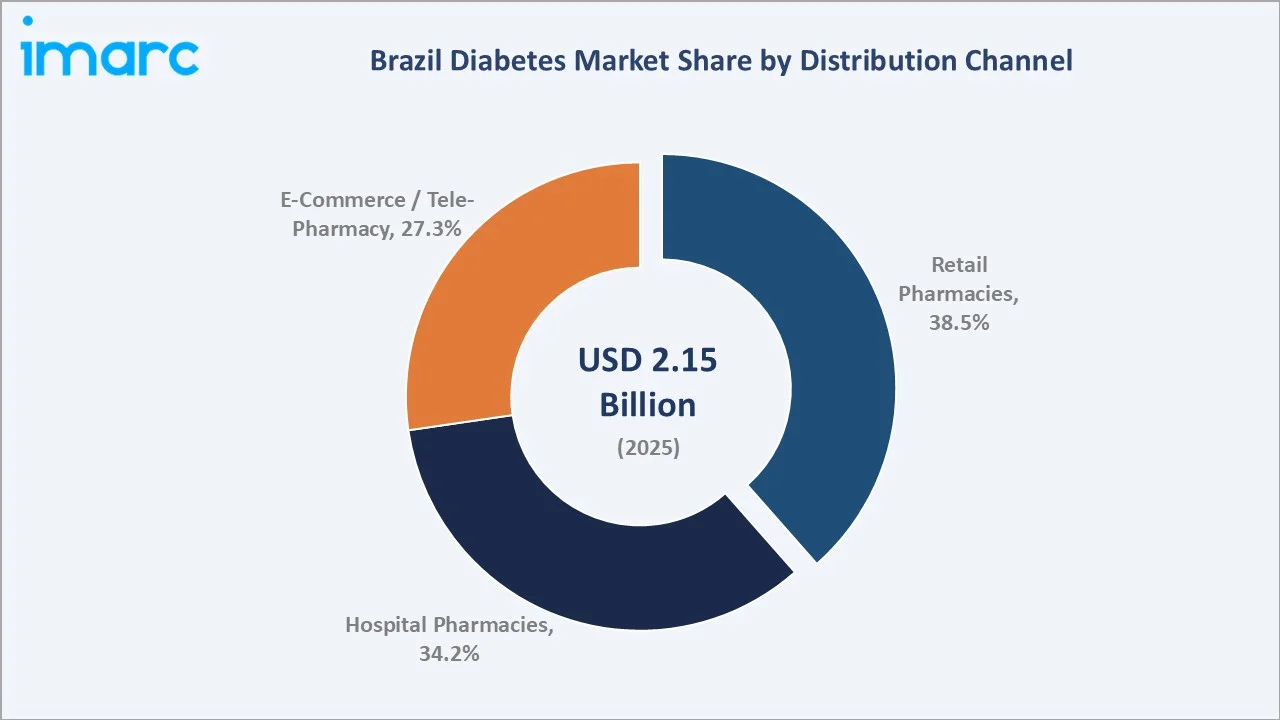

Oral antidiabetics command the largest segment share at 58.6% in 2025, driven by widespread prescription of metformin, SGLT-2 inhibitors, and DPP-4 inhibitors. The insulin segment accounts for 41.4% and is growing steadily as biosimilar insulin options expand affordability and access. Retail pharmacies remain the dominant distribution channel at 38.5%, though e-commerce and tele-pharmacy platforms are rapidly gaining ground with a 27.3% share as digital adoption accelerates across Brazil.

The Southeast region accounts for approximately 48% of the national diabetes drug market in 2025, reflecting its higher urbanization, healthcare infrastructure density, and larger diabetic patient pool. Key players include Novo Nordisk A/S, Sanofi, Lilly USA, LLC, AstraZeneca, and Merck & Co. Inc., all investing in product localization and portfolio expansion strategies tailored to the Brazilian healthcare environment.

Key Market Insights

|

Insight |

Data |

|

Largest Segment |

Oral Antidiabetics – 58.6% share (2025) |

|

2nd Largest Segment |

Insulin – 41.4% share (2025) |

|

Leading Channel |

Retail Pharmacies – 38.5% share (2025) |

|

Fastest Growing Channel |

E-Commerce/Tele-Pharmacy – 27.3% share (2025) |

|

Dominant Region |

Southeast – ~42.6% revenue share (2025) |

|

Top Companies |

Novo Nordisk A/S, Sanofi, Lilly USA, LLC, AstraZeneca, and Merck & Co. Inc. |

|

Market Opportunity |

GLP-1 & biosimilar insulin segment projected at USD 650 Million by 2034 |

Key Analytical Observations Supporting the Above Data:

- Oral antidiabetics account for 58.6% of the Brazil diabetes market in 2025, anchored by metformin as first-line treatment and the rapidly growing SGLT-2 inhibitor class, driven by cardiovascular and renal protective benefits certified in Brazilian cardiology guidelines.

- Insulin holds a 41.4% share in 2025; growth is fueled by biosimilar market entry, SUS procurement programs, and rising insulin-dependent patient cohorts in the Northeast and Southeast regions.

- Retail pharmacies remain the leading distribution channel at 38.5% in 2025, supported by a dense network of over 90,000 pharmacies across Brazil and increasing generic drug availability at competitive price points.

- E-commerce and tele-pharmacy channels have reached 27.3% share in 2025 as patients embrace subscription-based medication delivery and digital health applications across urban centers.

- The Brazilian GLP-1 receptor agonist and biosimilar insulin opportunity is estimated to reach USD 650 Million by 2034, growing at a CAGR exceeding 9% and representing the highest-growth investment vector in the market.

Brazil Diabetes Market Overview

Diabetes mellitus is one of the fastest-growing non-communicable diseases in Brazil. According to the International Diabetes Federation (IDF), Brazil ranks 6th globally in total number of diabetic adults, with prevalence particularly concentrated in urban centers and among the elderly population. The market encompasses two principal therapeutic classes, oral antidiabetics (OADs) and insulin, distributed through retail pharmacies, hospital pharmacies, and rapidly expanding e-commerce and tele-pharmacy platforms.

Macroeconomic and structural factors shaping the market include the Sistema Unico de Saude (SUS), which provides universal healthcare coverage and procures insulin and select oral agents at zero cost to eligible patients, creating a dual-track market structure. The private sector, comprising insurance-covered and out-of-pocket segments, drives premium OAD adoption. ANVISA regulates pharmaceutical market access with biosimilar pathways governed by the RDC 55/2010 framework, and new molecular entity review processes extending 18–24 months.

Market Dynamics

To evaluate market opportunities, Request Sample

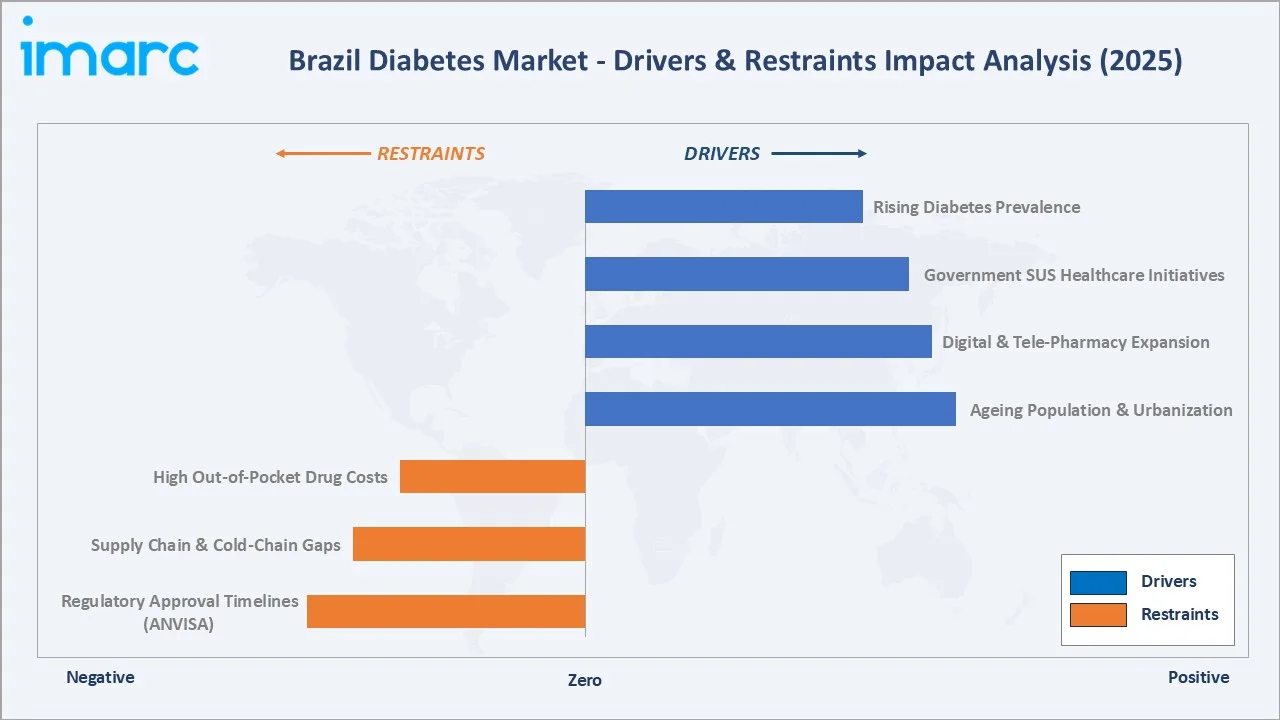

Market Drivers

- Rising Diabetes Prevalence: Brazil's diabetic adult population exceeded 16 million in 2024, growing in line with obesity and sedentary lifestyle trends. The Northeast and Southeast regions account for the majority of new diagnoses, creating sustained drug demand across both private and SUS distribution channels.

- Government SUS Healthcare Initiatives: The SUS Farmacia Popular program subsidizes metformin, glibenclamide, and insulin, expanding access to lower-income strata. Brazil had announced a 6.2% increase in funding for the Unified Health System (SUS) in 2025 compared to 2024. The primary focus for growth will be on enhancing primary health care and expanding specialized care services.

- Digital & Tele-Pharmacy Expansion: Post-pandemic regulatory relaxations enabled remote prescription dispensing, fueling e-commerce channel growth from 11% in 2020 to 27.3% in 2025. Platforms such as iClinic, Consulta Remedios, and Drogasil online saw combined active user growth exceeding 28% in 2024.

- Ageing Population & Urbanization: Brazil's population aged 60+ will exceed 14.7% by 2030, and urban caloric-dense diets are accelerating Type-2 diabetes onset across age cohorts, creating a structurally expanding patient base for all therapeutic segments.

Market Restraints

- High Out-of-Pocket Drug Costs: Newer drug classes such as GLP-1 receptor agonists and SGLT-2 inhibitors remain largely unavailable through SUS, placing a significant financial burden on patients and limiting access in lower-income segments where the majority of diabetes cases are concentrated.

- Supply Chain & Cold-Chain Gaps: Northern and Central-Western regions face logistical challenges in cold-chain insulin distribution, leading to gaps in medication adherence and sub-optimal care outcomes in underserved communities.

- Regulatory Approval Timelines (ANVISA): ANVISA's review processes for new molecular entities and biosimilars can extend to 18–24 months, delaying access to innovative therapies relative to the USA, EU, and other major markets.

Market Opportunities

- Biosimilar Insulin Expansion: With multiple international biosimilar manufacturers receiving ANVISA approval, insulin prices are projected to decline through 2030, expanding the addressable patient population and driving volume-based revenue growth.

- GLP-1 Receptor Agonist Market Entry: Semaglutide and liraglutide are experiencing strong uptake in Brazil's private market. The GLP-1 receptor agonist segment is estimated to grow at a CAGR exceeding 9% through 2034, representing the premium innovation frontier for the Brazil market.

- Digital Disease Management Platforms: CGM-integrated mobile health solutions and AI-powered diabetes management platforms are creating new revenue streams for pharmaceutical and medtech companies while improving adherence and driving prescription continuity across the patient base.

Market Challenges

- Counterfeit & Substandard Medications: In Brazil, the sale of counterfeit medicines has risen over the past decade, accompanied by a notable increase in arrests made by the Brazilian Federal Police (BFP), undermining patient safety and siphoning revenue from legitimate market participants.

- Fragmented Healthcare Access: Significant disparities exist between Brazil's Southeast and Northern/Northeast regions in specialist availability, diagnostic infrastructure, and adherence monitoring, creating unequal market penetration and disproportionate disease burden.

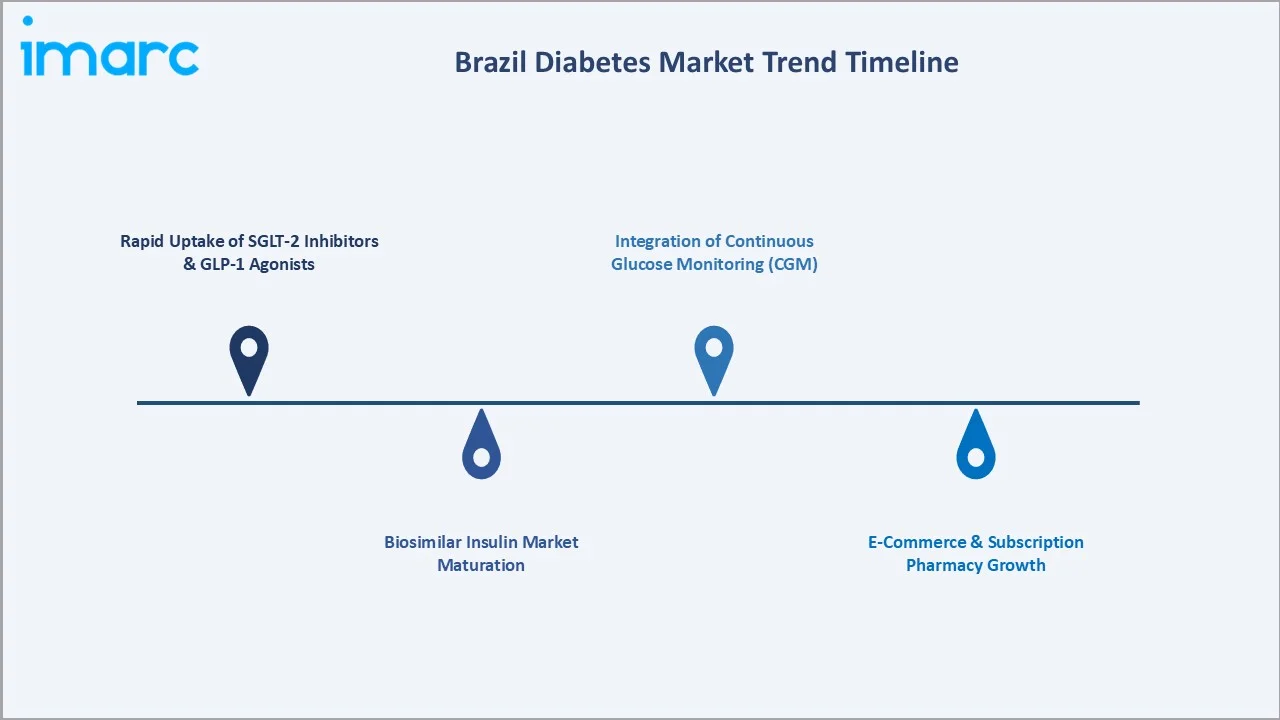

Emerging Market Trends

1. Rapid Uptake of SGLT-2 Inhibitors and GLP-1 Agonists

Brazil's cardiologists and endocrinologists are increasingly prescribing empagliflozin, dapagliflozin, and semaglutide not only for glycaemic control but for their proven cardiovascular and renal protective properties. SGLT-2 inhibitor prescription volume in Brazil grew at approximately 22% annually between 2022 and 2025, making it the fastest-growing OAD subclass in the private market.

2. Biosimilar Insulin Market Maturation

Between 2023 and 2025, ANVISA approved four new biosimilar insulin products, intensifying price competition and enabling SUS to expand procurement volumes. Brazil's biosimilar market accounts for an estimated USD 572.95 Million in 2024 and is expected to reach USD 3,991.36 by 2033 as manufacturing capacity scales nationally.

3. E-Commerce and Subscription Pharmacy Growth

Digital pharmacy platforms grew from approximately 11% of Brazil's diabetes drug distribution in 2020 to 27.3% by 2025. Monthly subscription medication services offering home delivery and integrated adherence tracking are disrupting the traditional retail pharmacy model, particularly among working-age urban patients in São Paulo and Rio de Janeiro.

4. Integration of Continuous Glucose Monitoring (CGM)

CGM device adoption among Brazilian diabetics grew 34% in 2024, spurred by falling sensor prices and emerging SUS coverage pilots in selected states. CGM adoption is driving increased medication adherence and more frequent drug therapy adjustments, indirectly boosting injectable and oral diabetes drug utilization.

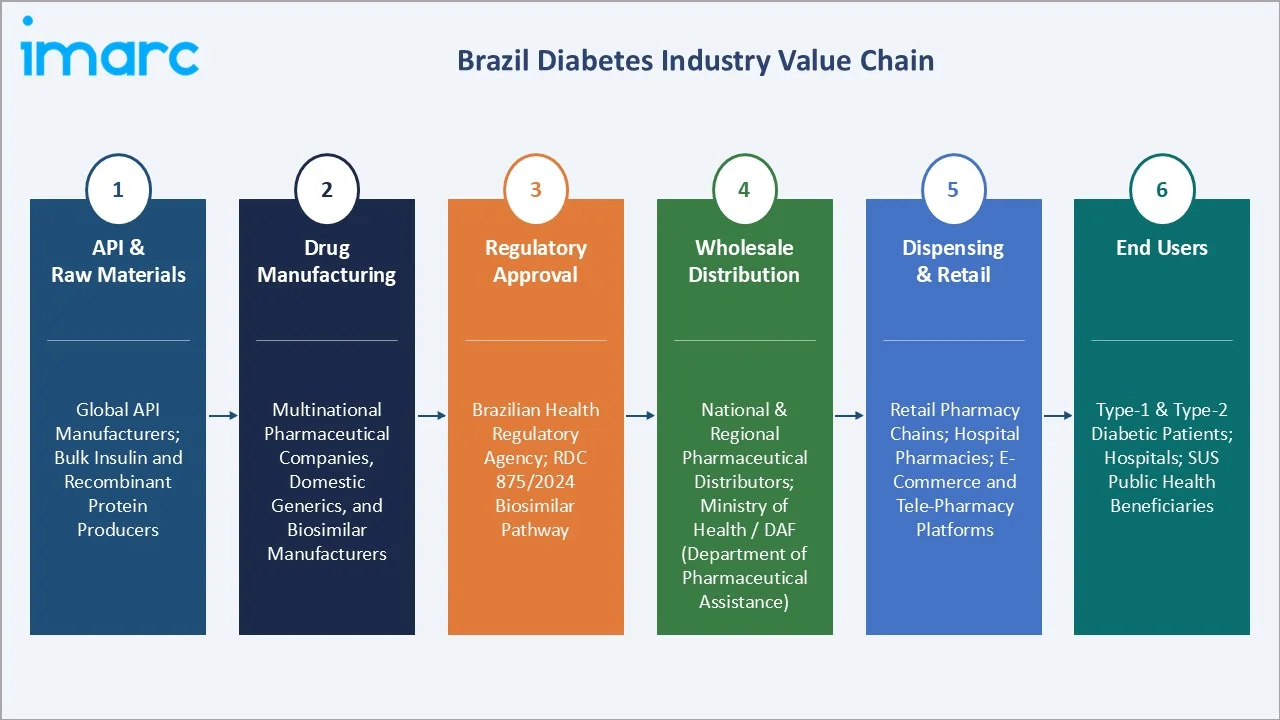

Industry Value Chain Analysis

The Brazil diabetes drug market value chain spans bulk active pharmaceutical ingredient (API) production through to end-patient dispensing, with each stage populated by specialized operators whose performance directly influences product quality, accessibility, pricing, and patient outcomes across the country's complex dual public-private healthcare structure.

|

Stage |

Key Players / Examples |

|

API & Raw Materials |

Global API manufacturers; bulk insulin and recombinant protein producers |

|

Drug Manufacturing |

Multinational pharmaceutical companies, domestic generics, and biosimilar manufacturers |

|

Regulatory Approval |

Brazilian Health Regulatory Agency; RDC 875/2024 biosimilar pathway |

|

Wholesale Distribution |

National & regional pharmaceutical distributors; Ministry of Health / DAF (Department of Pharmaceutical Assistance) |

|

Dispensing & Retail |

Retail pharmacy chains; hospital pharmacies; e-commerce and tele-pharmacy platforms |

|

End Users |

Type-1 & Type-2 diabetic patients; hospitals; SUS public health beneficiaries |

Technology Landscape in the Brazil Diabetes Market

Advanced Insulin Delivery Systems

Smart insulin pens with Bluetooth connectivity, enabling dose tracking and integration with digital diabetes management applications, are being introduced to the Brazilian private market by Novo Nordisk and Sanofi. These devices improve adherence tracking and support remote endocrinologist consultations, enhancing patient outcomes and prescription continuity.

AI-Powered Diabetes Management Platforms

Brazilian healthtech companies such as Nilo Saude provide an intelligent, automated platform that consolidates patient information and integrates it with property attribution models. This approach enhances patient engagement, generates actionable insights, and boosts financial performance. These platforms are forging commercial partnerships with pharmaceutical distributors and pharmacy chains, creating new hybrid digital-pharmaceutical business models.

Biosimilar & Generic Drug Manufacturing Technology

India‑based Biocon Biologics has signed an exclusive licensing and supply agreement with Brazil’s Biomm S.A. to commercialize semaglutide, a drug for type‑2 diabetes treatment, in the Brazilian market. These investments are expected to halve the cost differential between originator and biosimilar products by 2030, materially expanding SUS procurement volumes and patient access in lower-income segments.

Telemedicine & Remote Prescribing Infrastructure

ANVISA's 2022 regulatory resolution enabling permanent telemedicine services in Brazil has created a robust infrastructure for remote diabetes consultations and e-prescribing. This is directly driving tele-pharmacy channel adoption and enabling pharmaceutical companies to reach patients in underserved Northeast and Northern regions via digital engagement models.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Segment | Oral Antidiabetics | 58.6% | 2025 |

| Distribution Channel | Retail Pharmacies | 38.5% | 2025 |

By Segment

Oral antidiabetics dominate the Brazil diabetes market with a 58.6% share in 2025 (equivalent to approximately USD 1,261 Million), reflecting the entrenched role of metformin as the universal first-line Type-2 diabetes treatment, as well as the growing penetration of premium OAD classes including DPP-4 inhibitors and SGLT-2 inhibitors across Brazil's private healthcare segment.

To access detailed market analysis, Request Sample

Insulin accounts for 41.4% of the market. The segment is sustained by a large insulin-dependent Type-1 patient cohort, by Type-2 patients transitioning to insulin therapy as disease progresses, and by SUS's comprehensive insulin procurement program. Biosimilar insulins, including glargine analogues, are driving steady volume growth while moderating average selling prices across both public and private channels.

By Distribution Channel

Retail pharmacies represent the leading channel at 38.5% share in 2025, supported by Brazil's dense pharmacy network exceeding 90,000 outlets and the widespread availability of both branded and generic oral antidiabetic medications. Hospital pharmacies follow at 34.2%, driven by SUS inpatient dispensing of insulin and injectable agents.

E-commerce and tele-pharmacy platforms have reached 27.3% of the market in 2025, emerging as the fastest-growing channel as urban patients increasingly opt for subscription-based home delivery and integrated digital prescribing services

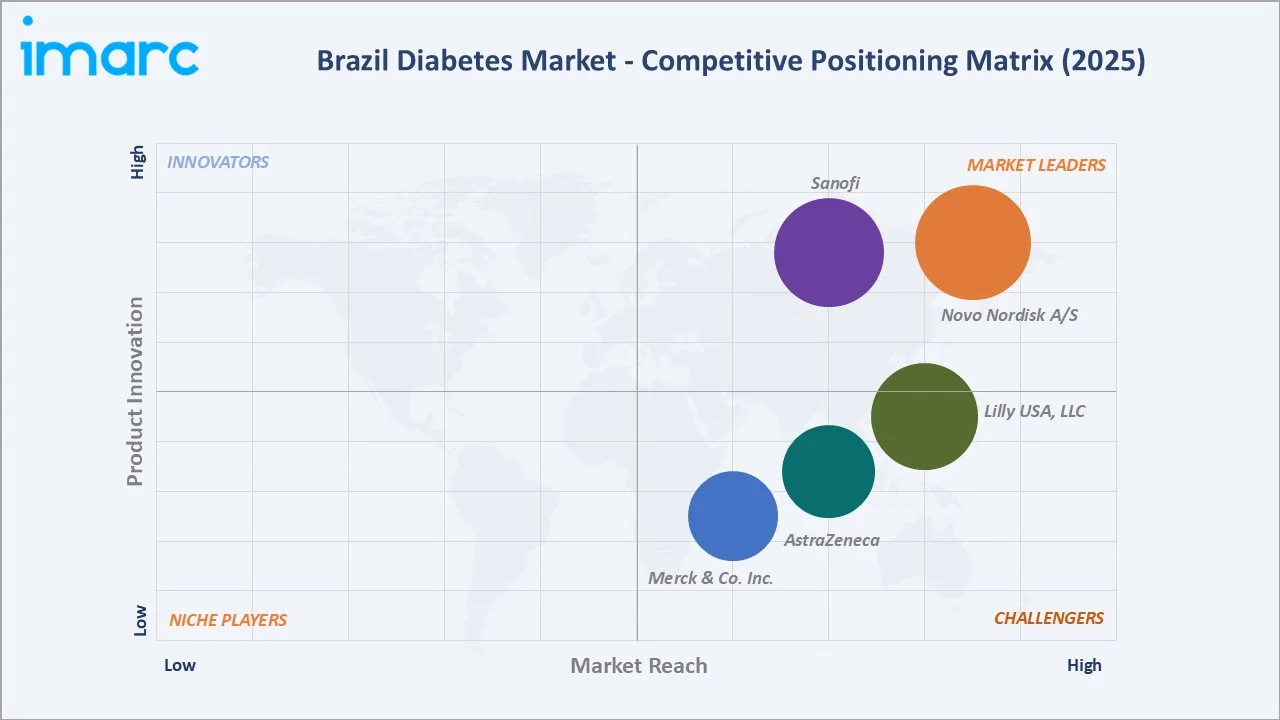

Competitive Landscape

The Brazil diabetes market exhibits a moderately concentrated structure at the innovative pharmaceutical level. The top five companies, Novo Nordisk A/S, Sanofi, Lilly USA, LLC, AstraZeneca, and Merck & Co. Inc., collectively account for approximately 58–62% of market revenue in 2025.

|

Company Name |

Core Segment |

Market Position |

Core Strength |

|

Novo Nordisk A/S |

Insulin & GLP-1 |

Market Leader |

Global insulin leader; Ozempic/Victoza driving GLP-1 growth in Brazil |

|

Sanofi |

Insulin |

Market Leader |

Lantus is dominant in basal insulin |

|

Lilly USA, LLC |

Mounjaro |

Strong Challenger |

Humalog/Trulicity portfolio; strong hospital pharmacy presence |

|

AstraZeneca |

Oral Antidiabetics |

Strong Challenger |

Forxiga (dapagliflozin) is leading the SGLT-2 segment in Brazil |

|

Merck & Co. Inc. |

Oral Antidiabetics |

Challenger |

Januvia (sitagliptin); strong DPP-4 inhibitor franchise across Brazil |

Brazilian local manufacturers, including EMS Farmaceutica and Biolab Farmaceutica, compete strongly in the generic and biosimilar segments, particularly through SUS procurement channels.

Key Company Profiles

Novo Nordisk A/S

Novo Nordisk A/S, headquartered in Bagsvaerd, Denmark, is the global insulin market leader and holds the largest single-company revenue share in the Brazilian diabetes market, with operations spanning all insulin classes, GLP-1 receptor agonists, and digital health solutions.

- Product Portfolio: Tresiba (degludec), Ozempic (semaglutide), Victoza (liraglutide), NovoRapid, NovoMix 30.

- Recent Developments: In October 2025, Eurofarma and Novo Nordisk A/S formed a strategic partnership to introduce two new weekly injectable semaglutide brands in Brazil, expanding access to treatments for type 2 diabetes and obesity.

- Strategic Focus: GLP-1 growth leadership in Brazil's premium private market; biosimilar defense strategy via Tresiba differentiation; digital insulin pen ecosystem expansion.

Lilly USA, LLC

Lilly USA, LLC, operating in Brazil as Eli Lilly do Brasil Ltda, is a key participant in both the insulin and oral antidiabetic segments, with a strong hospital pharmacy presence and a growing GLP-1 franchise through Trulicity and co-promoted Jardiance.

- Product Portfolio: Humalog (lispro), Basaglar (biosimilar glargine), Jardiance (empagliflozin, co-promoted with Boehringer Ingelheim), Mounjaro (tirzepatide).

- Recent Developments: In April 2026, Lilly’s Phase 3 ACHIEVE‑4 trial of its oral GLP‑1 candidate Foundayo (orforglipron) showed the drug met key cardiovascular safety goals and delivered consistent improvements in blood sugar control and body weight for adults with type 2 diabetes.

- Strategic Focus: Biosimilar insulin volume growth; Trulicity and tirzepatide GLP-1 market development; Jardiance co-promotion in the cardiometabolic segment.

AstraZeneca

AstraZeneca, headquartered in Cambridge, UK, has rapidly emerged as a leading oral antidiabetic player in Brazil through Forxiga (dapagliflozin), which benefits from strong cardiovascular and renal outcome data recognized in Brazilian cardiology guidelines.

- Product Portfolio: Forxiga

- Recent Developments: In February 2026, AstraZeneca is advancing its in‑licensed oral GLP‑1 receptor agonist elecoglipron into Phase III pivotal trials after positive mid‑stage results, aiming to expand oral treatment options for type 2 diabetes beyond injectables.

- Strategic Focus: SGLT-2 market leadership; cardiometabolic indication expansion; multi-specialty physician education programs across cardiology, nephrology, and endocrinology.

Market Concentration Analysis

The Brazil diabetes market displays moderate-to-high concentration at the innovative pharmaceutical level, with the top five originator companies holding approximately 58–62% of total market revenue in 2025. However, the generic and biosimilar segments, supplied predominantly by local manufacturers such as EMS Farmaceutica, Biolab Farmaceutica, and Hypera Pharma, account for a significant share of volume dispensed through SUS channels, ensuring overall market accessibility from a public health perspective.

Consolidation pressures are building as patent expirations create biosimilar entry opportunities and as ANVISA's streamlined biosimilar approval pathway continues to reduce barriers for local manufacturers. The market is expected to see incremental genericization of key DPP-4 and SGLT-2 molecules through 2030, compressing average selling prices while expanding volume-driven revenues for distribution channel participants.

Investment & Growth Opportunities

Fastest Growing Segments

GLP-1 receptor agonists (estimated CAGR ~9.2%), biosimilar insulin (volume CAGR ~8.5%), and digital/e-pharmacy distribution platforms (CAGR ~11%) represent the three highest-growth investment vectors through 2034. Together, these niches address an incremental addressable market of approximately USD 650 Million by 2034 within the broader Brazil diabetes market.

Emerging Market Expansion

Brazil's Northeast region represents the most underserved high-growth diabetes market, with diabetes prevalence above the national average but pharmaceutical distribution infrastructure significantly below Southeast levels. Investment in last-mile cold-chain logistics, tele-pharmacy platform partnerships, and SUS procurement alignment in Bahia, Ceará, and Pernambuco can unlock significant incremental revenue through 2034.

Venture and Institutional Investment Trends

- Key investment themes include biosimilar insulin manufacturing scale-up, CGM-integrated diabetes management platforms, AI-powered patient adherence solutions, and tele-pharmacy infrastructure targeting Brazil's North and Northeast regions.

- Private equity interest is elevated in Brazil's pharmacy retail consolidation space, with digital-physical pharmacy hybrids attracting significant growth capital from both Brazilian and international investors.

- International pharmaceutical companies are investing in local ANVISA registration programs for newer GLP-1 and dual GIP/GLP-1 receptor agonists (e.g., tirzepatide) targeting Brazil's premium private market, the fastest-growing therapeutic sub-segment.

Future Market Outlook (2026-2034)

The Brazil diabetes market is positioned for sustained, broad-based growth through 2034. From a base of USD 2.15 Billion in 2025, the market is projected to reach USD 3.09 Billion by 2034, representing total incremental value creation of approximately USD 940 Million over the forecast decade at a CAGR of 3.96%.

Regulatory evolution – particularly ANVISA's expanding biosimilar approval framework, SUS's ongoing Farmacia Popular expansion, and Brazil's National Chronic Disease Prevention Plan – will drive both volume growth and pricing pressures across segments. Companies that build robust SUS public tender capabilities alongside premium private market positioning will capture a disproportionate share of Brazil's structurally growing diabetes market.

Long-term, the market trajectory is tied to three structural macro-themes: the rising incidence of obesity-driven Type-2 diabetes creating a structurally expanding patient base; innovation in drug classes offering cardiovascular and renal co-benefits driving prescription premiumization; and digital health integration reshaping how medications are prescribed, dispensed, and monitored across Brazil's vast geography and unequal healthcare infrastructure.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 120 industry participants in 2024–2025, including pharmaceutical company representatives, hospital pharmacists, retail pharmacy managers, endocrinologists, SUS procurement officers, and patient advocacy groups across Brazil's five major regions.

Secondary Research

Secondary research encompassed a systematic review of ANVISA regulatory filings, SUS DATASUS procurement databases, IDF Diabetes Atlas (10th Edition, 2024), WHO non-communicable disease surveillance reports, company annual reports, IQVIA Brazil pharmaceutical market intelligence data, and clinical trial registries. Over 200 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating epidemiological prevalence data, drug treatment penetration rates, average therapy costs by class, and SUS vs. private market split dynamics. A base-case CAGR of 3.96% reflects consensus analyst estimates validated against reported pharmaceutical company Brazil segment revenues and SUS procurement trend data.

Brazil Diabetes Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Segments Covered | Oral Antidiabetics, Insulin |

| Distribution Channels Covered | E-commerce and Tele-pharmacy, Hospital Pharmacies, Retail Pharmacies |

| Companies Covered | Novo Nordisk A/S, Sanofi, Lilly USA, LLC, AstraZeneca, Merck & Co. Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Brazil Diabetes Market Report

The Brazil diabetes market reached USD 2.15 Billion in 2025, making it the largest diabetes pharmaceutical market in Latin America.

The market is projected to reach USD 3.09 Billion by 2034, growing at a CAGR of 3.96% during 2026-2034, driven by rising diabetes prevalence, biosimilar insulin expansion, and GLP-1 receptor agonist uptake.

Oral antidiabetics lead with a 58.6% market share in 2025. The segment is anchored by metformin as the universal first-line therapy and the rapidly growing SGLT-2 inhibitor class, whose prescription volume grew at ~22% annually between 2022 and 2025.

Insulin accounts for 41.4% of the Brazil diabetes market in 2025. Biosimilar glargine products represent 18% of the insulin segment in 2025, a share expected to grow to 35% by 2034 as local manufacturing scales up.

Retail pharmacies lead with 38.5% share in 2025, supported by a network of over 90,000 outlets across Brazil. Hospital pharmacies follow at 34.2%, driven by SUS inpatient insulin dispensing. E-commerce and tele-pharmacy platforms represent 27.3% share in 2025 and are the fastest-growing channel.

Leading companies include Novo Nordisk A/S, Sanofi, Lilly USA, LLC, AstraZeneca, and Merck & Co. Inc., collectively holding approximately 58–62% of market revenue in 2025. Local players EMS Farmaceutica and Biolab Farmaceutica lead the biosimilar and generic segments through SUS procurement channels.

Key growth drivers include rising diabetes prevalence, government SUS healthcare initiatives (BRL 3.5 Billion procurement budget in 2024), rapid expansion of digital and tele-pharmacy channels, and ageing population trends accelerating Type-2 diabetes onset across urban Brazil.

Key challenges include high out-of-pocket costs for newer drug classes not covered by SUS, supply chain and cold-chain distribution gaps in the North and Northeast, ANVISA regulatory approval timelines of 18–24 months for new therapies, and counterfeit drug circulation in informal markets estimated at 3–5% of units.

Biosimilar insulin entry is a significant structural driver, projected to reduce insulin prices by up to 20% by 2030. This is expanding SUS procurement volumes and improving access for lower-income diabetic patients across Brazil's underserved regions, particularly the Northeast and North.

Key investment opportunities include GLP-1 receptor agonist commercialization (CAGR ~9.2%), biosimilar insulin scale-up (volume CAGR ~8.5%), e-pharmacy/tele-pharmacy infrastructure (CAGR ~11%), and last-mile cold-chain logistics targeting the Northeast and North regions, collectively representing an incremental USD 650 Million opportunity by 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)