Brazil Logistics Market Size, Share, Trends and Forecast by Model Type, Transportation Mode, End Use, and Region, 2026-2034

Brazil Logistics Market Size, Share, Trends & Forecast (2026-2034)

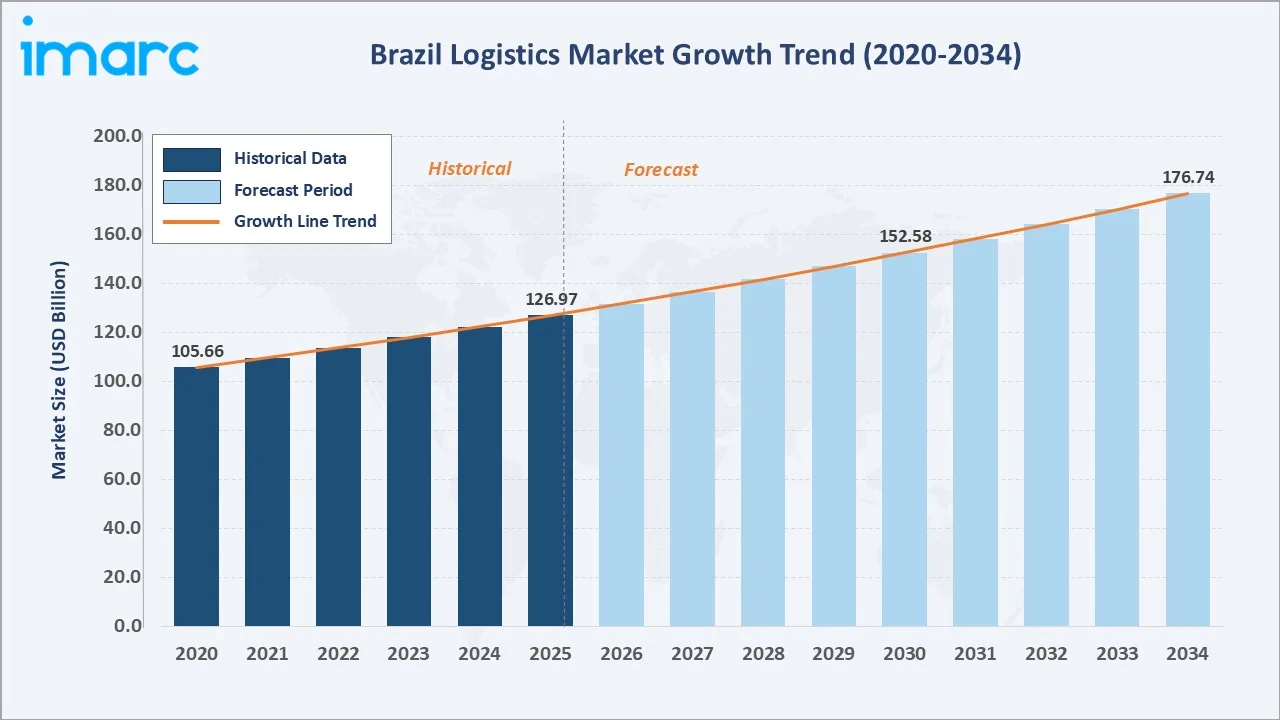

The Brazil logistics market size reached USD 126.97 Billion in 2025 and is projected to reach USD 176.74 Billion by 2034, exhibiting a CAGR of 3.74% during 2026-2034. Rapid e-commerce expansion, government infrastructure investment under the Novo PAC initiative, and rising industrial activity are the primary forces driving market growth.

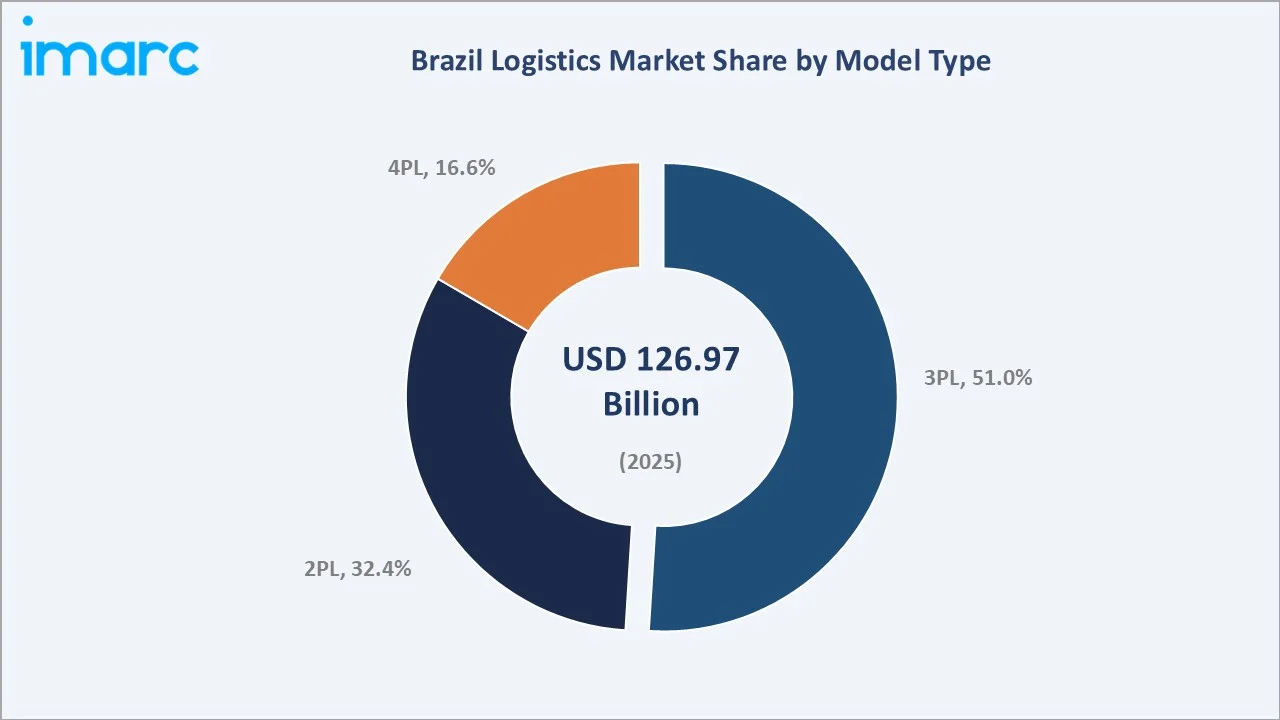

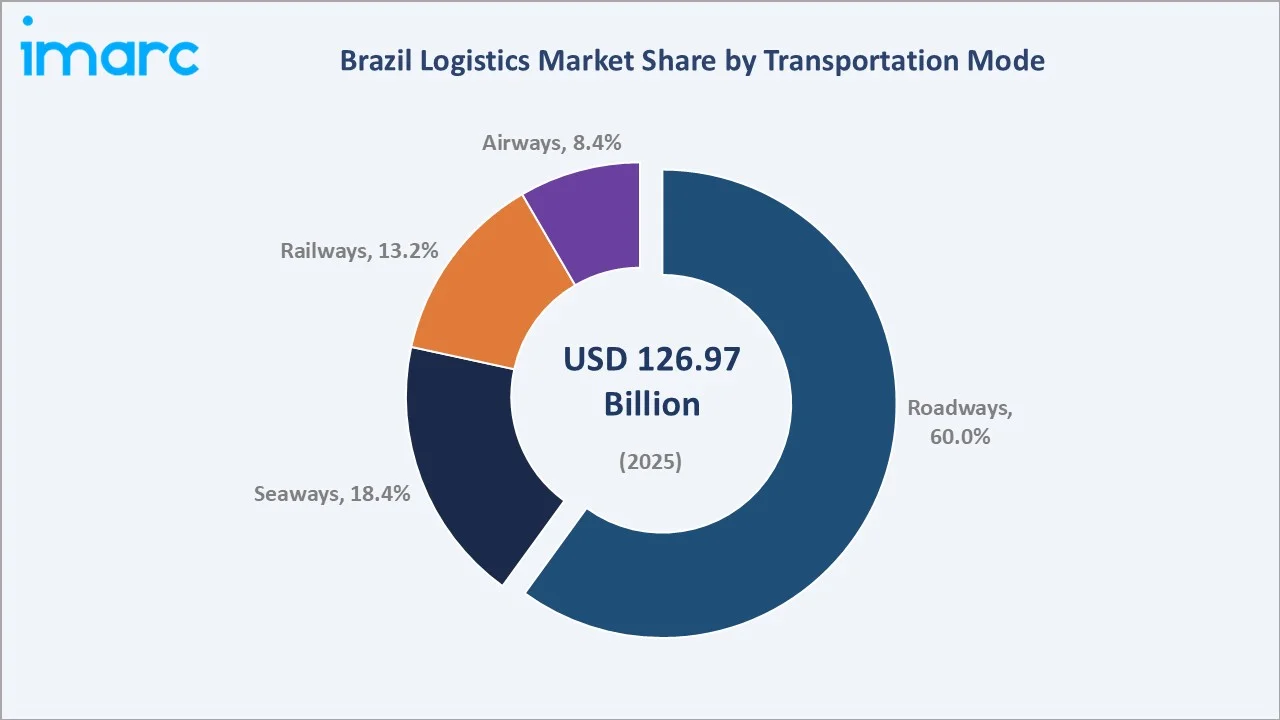

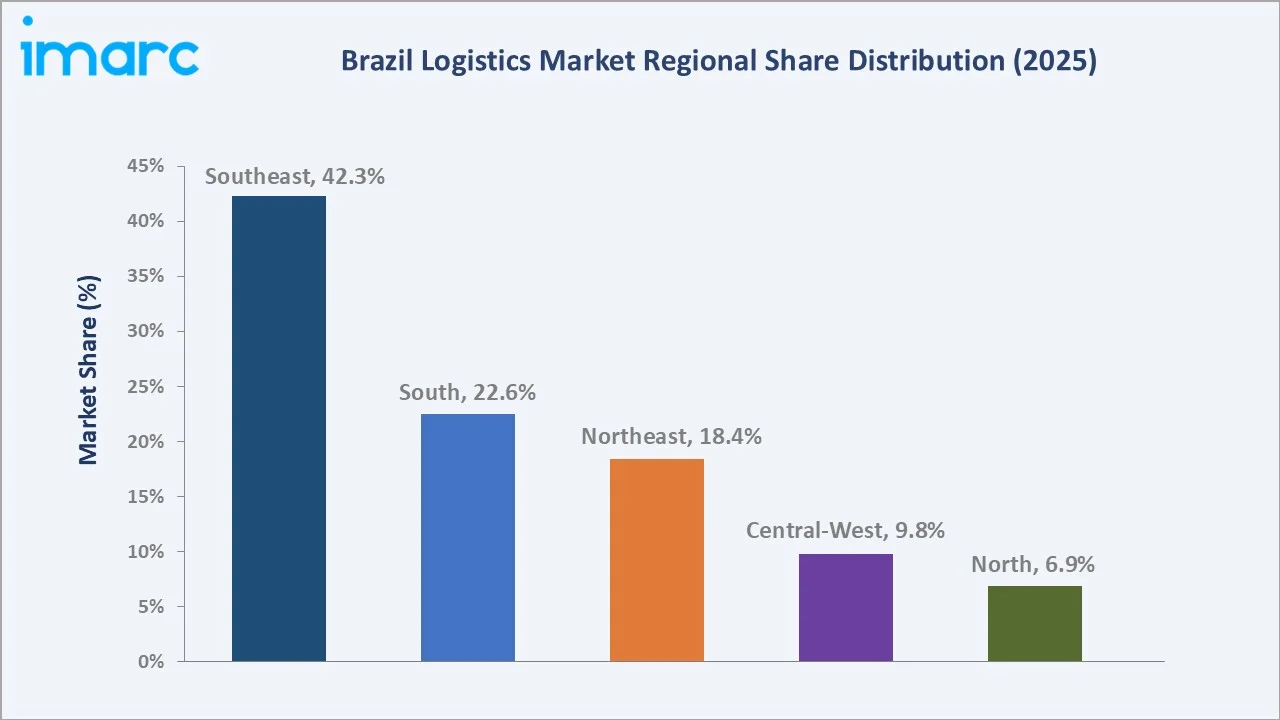

3 PL dominates model type at 51.0% in 2025, while Roadways leads transportation at 60.0%. The Southeast region commands 42.3% regional share, anchored by the Port of Santos and the São Paulo industrial corridor.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 126.97 Billion |

|

Forecast Market Size (2034) |

USD 176.74 Billion |

|

CAGR (2026-2034) |

3.74% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Southeast (42.3% share, 2025) |

|

Second Region |

South (22.6% share, 2025) |

|

Leading Model Type |

3 PL (51.0%, 2025) |

|

Leading Transport Mode |

Roadways (60.0%, 2025) |

To get more information on this market, Request Sample

The Brazil logistics market growth trajectory from 2020 through 2034, with historical expansion to USD 126.97 Billion in 2025, reflects consistent infrastructure-driven demand. The forecast to USD 176.74 Billion captures accelerating e-commerce adoption, industrial investment, and multimodal corridor development across Brazil's five economic regions.

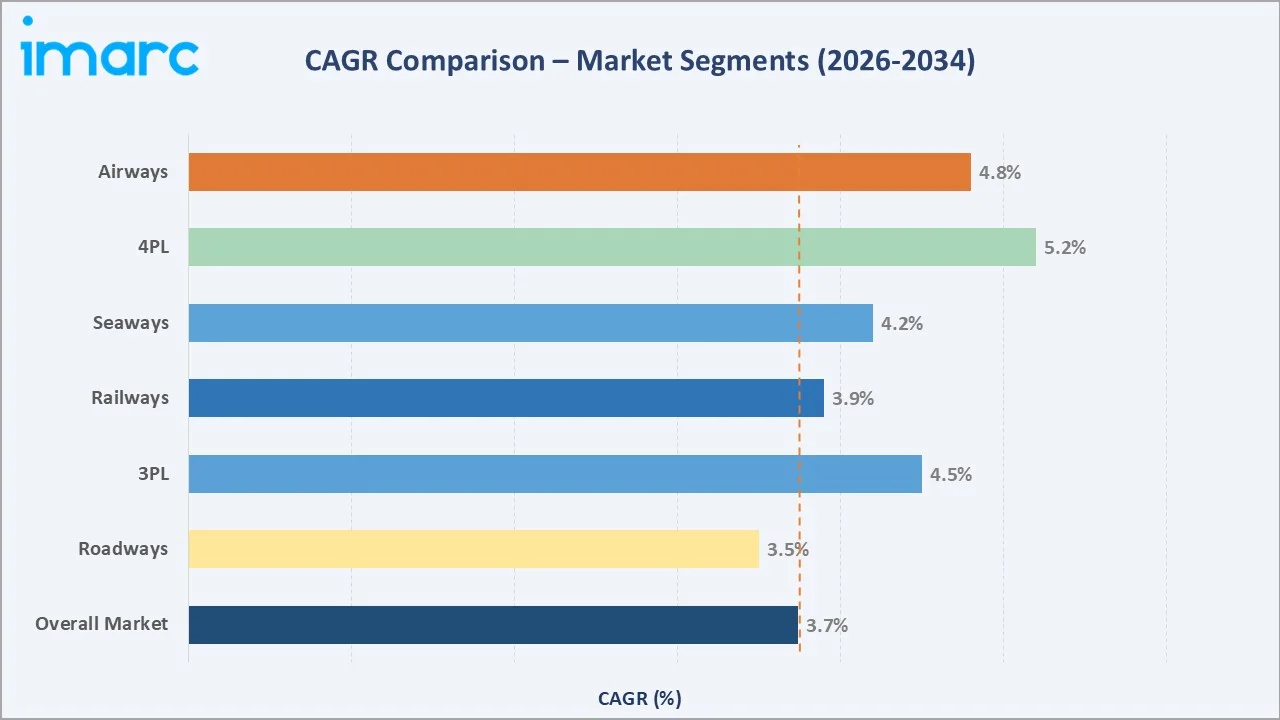

The CAGR trajectories across key model type and transportation sub-segments, with 4 PL at ~5.2% CAGR and Airways at ~4.8% CAGR, represent the fastest-growing categories within the Brazil logistics industry analysis through 2034.

Executive Summary

The Brazil logistics market is on a sustained growth trajectory from USD 126.97 Billion in 2025 to USD 176.74 Billion by 2034. Logistics, encompassing warehousing, transport management, distribution, and fulfilment, benefits from Brazil's position as Latin America's largest economy and a major global trade hub for agricultural and manufactured goods.

3 PL dominates model type at 51.0% in 2025, driven by growing outsourcing of supply chain operations by manufacturers, retailers, and e-commerce platforms. 4 PL (16.6%) is the fastest-growing model, while 2 PL (32.4%) serves transport-focused contracts in automotive, chemicals, and bulk commodity sectors.

Roadways lead transportation mode at 60.0% in 2025, supported by Brazil's 1.7-million-kilometre highway network. Seaways (18.4%) are critical for commodity exports, Railways (13.2%) are expanding through infrastructure investment, and Airways (8.4%) serve pharmaceutical and electronics cargo requiring rapid national distribution.

The Southeast region (42.3%) dominates, driven by São Paulo's manufacturing base and the Port of Santos. South (22.6%), Northeast (18.4%), Central-West (9.8%), and North (6.9%) follow, with federal infrastructure investment reshaping logistics flows toward interior regions.

Key Market Insights

|

Insight |

Data |

|

Leading Model Type |

3 PL – 51.0% share (2025) |

|

Second Model Type |

2 PL – 32.4% share (2025) |

|

Leading Region |

Southeast – 42.3% revenue share (2025) |

|

Leading Transport Mode |

Roadways – 60.0% revenue share (2025) |

|

Top Companies |

DHL Group, CEVA Logistics, Braspress, JSL S.A., Luft Logistics |

Key Analytical Observations:

- 3 PL's 51.0% share in 2025 reflects growing enterprise preference for outsourced, technology-enabled supply chain management. E-commerce growth, lean inventory adoption, and omnichannel fulfillment requirements have made 3 PL the default logistics model for mid-to-large Brazilian enterprises.

- Roadways' 60.0% dominance reflects Brazil's extensive highway network and last-mile delivery flexibility. Door-to-door connectivity across Brazil's vast and diverse geography, including remote municipalities, is achievable only via road transport, cementing its structural leadership.

- The Southeast's 42.3% share reflects São Paulo's industrial clusters, Rio de Janeiro's commercial hubs, and the Port of Santos, Latin America's largest container terminal, creating an unparalleled logistics demand concentration in the São Paulo, Santo’s corridor.

- The South region's 22.6% reflects Brazil's agribusiness logistics intensity; Paraná and Rio Grande do Sul generate the highest logistics demand per km², as they are origins for soybean, corn, and poultry export logistics through the Paraná Port complex.

Brazil Logistics Market Overview

Brazil's logistics market is Latin America's largest, encompassing the full spectrum of freight transport, warehousing and distribution, 3PL/4PL services, customs clearance, and integrated supply chain management. The market integrates infrastructure owners, carriers, third-party logistics providers, technology vendors, and diverse end-use industries spanning manufacturing, retail, food and beverages, healthcare, oil and gas, and agribusiness.

The market ecosystem spans six interconnected layers, from transport infrastructure provision through to end-customer fulfillment, each with distinct players, margin structures, and competitive dynamics. Digital transformation across all layers is accelerating through warehouse management systems, AI-powered route optimisation, IoT cargo tracking, and cloud-based platform integration.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

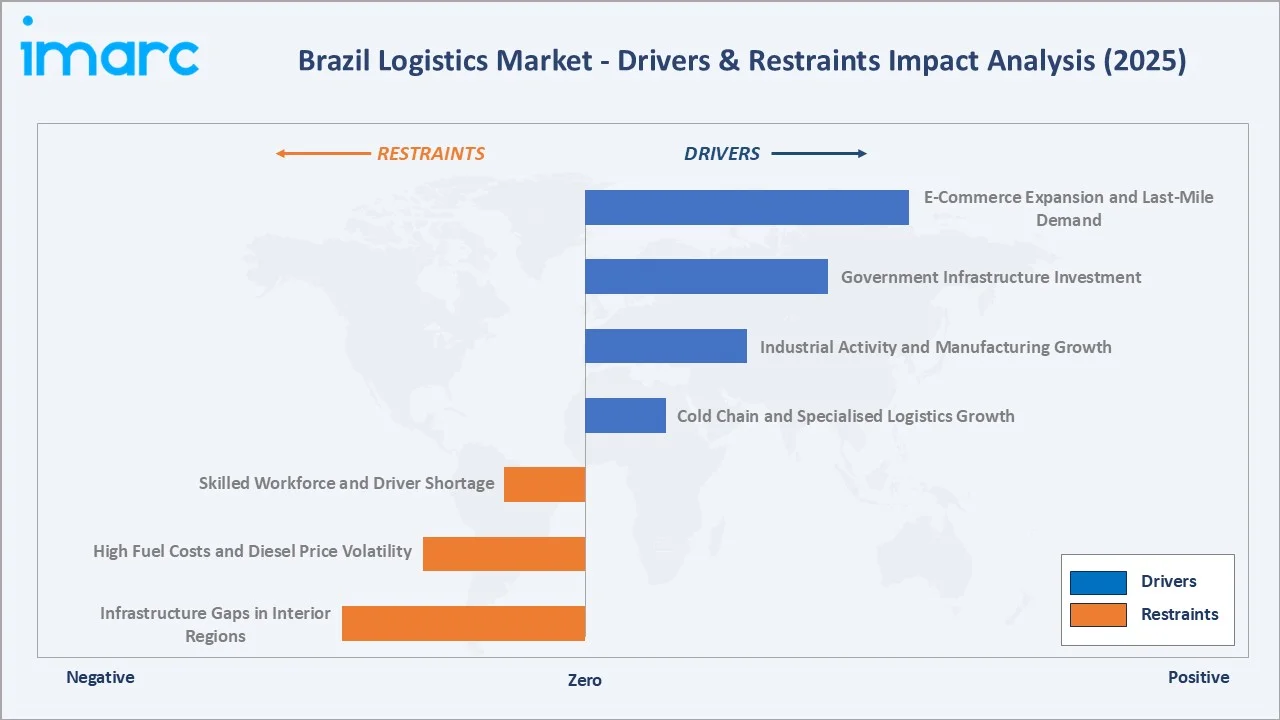

- E-Commerce Expansion and Last-Mile Demand: Brazil's online retail sector grew 16% in 2024, generating dense demand for micro-fulfilment centres, same-day delivery networks, and reverse logistics infrastructure. Mercado Libre announced a USD 5.8 billion Brazil investment in 2025, expanding logistics infrastructure and workforce.

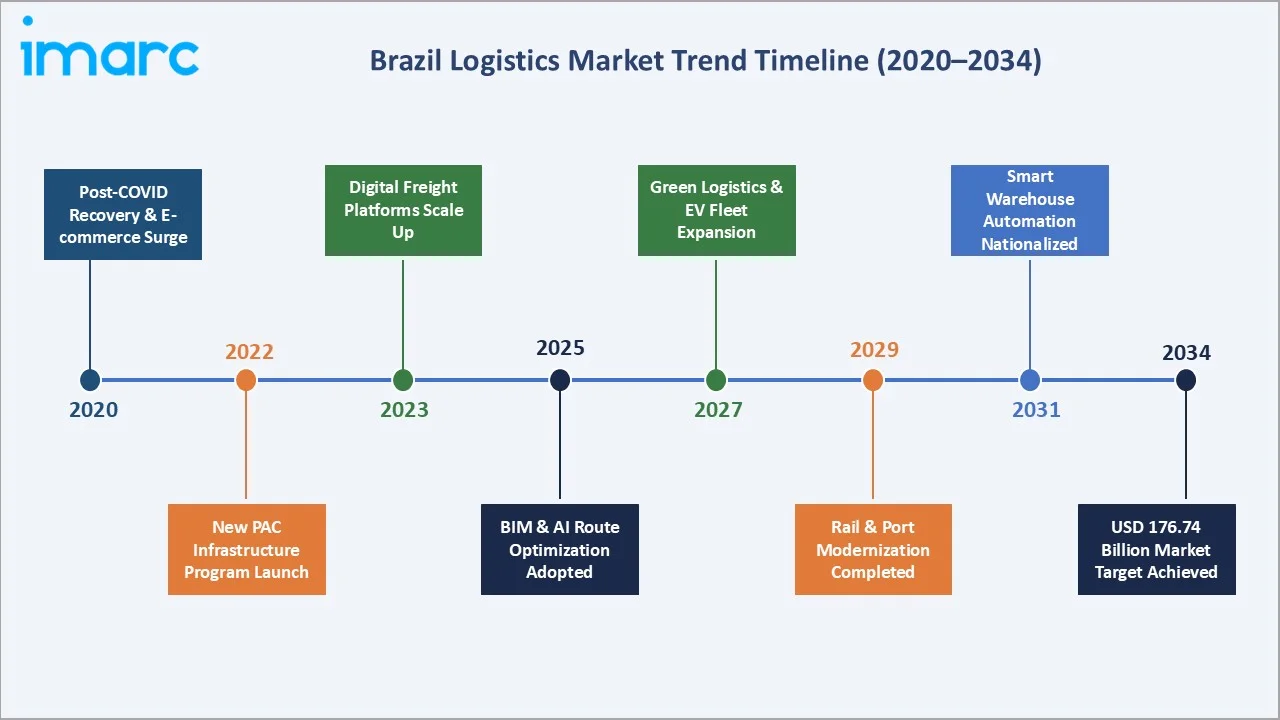

- Government Infrastructure Investment (Novo PAC): The Novo PAC programme has allocated R$54.7 billion for port modernisation and multimodal corridor development. The Northern Arc infrastructure programme and the North-South Railroad expansion are integrating agricultural producing regions with Atlantic export ports.

- Industrial Activity and Manufacturing Growth: Brazil's manufacturing sector, spanning automotive, chemicals, food and beverages, and electronics, generates non-discretionary logistics demand for inbound raw material procurement, inter-plant transfers, and finished goods distribution across domestic and export channels.

Market Restraints

- Infrastructure Gaps in Interior Regions: Despite coastal and metropolitan logistics sophistication, Brazil's interior regions, particularly the North and Central-West, face significant deficits in paved road density, rail connectivity, and intermodal terminal availability, limiting efficient supply chain penetration.

- High Fuel Costs and Diesel Price Volatility: Road freight accounts for approximately 60% of cargo movement, making the market highly exposed to diesel price fluctuations. Petrobras pricing policy changes and global oil market volatility directly affect carrier cost structures and freight rate stability.

Market Opportunities

- Cabotage and Coastal Shipping Expansion: Regulatory reforms and port concession modernisation under the Novo PAC are enabling coastal cabotage routes to capture freight from overloaded highway corridors, reducing transport costs for bulk and containerised cargo along Brazil's 7,400-kilometre coastline.

- Cold Chain and Specialised Logistics Growth: Brazil's dominant position in food and agribusiness exports, the world's largest exporter of soybeans, sugar, and poultry, is driving demand for refrigerated transport, temperature-controlled warehousing, and specialised food-grade logistics networks.

Market Challenges

- Regulatory Complexity and Customs Efficiency: Brazil's multi-layered tax system (ICMS, PIS/COFINS) creates compliance complexity across state borders, and customs clearance at major ports continues to impose delays that increase supply chain cycle times and working capital requirements for importers and exporters.

- Skilled Workforce and Driver Shortage: A chronic shortage of certified truck drivers, warehouse automation technicians, and digital logistics platform specialists is constraining capacity expansion, particularly in last-mile delivery and cold chain operations across secondary Brazilian markets.

Emerging Market Trends

1. Accelerated Digital Transformation and AI-Powered Logistics

AI-powered route optimisation, IoT cargo tracking, and cloud-based WMS platforms are reshaping Brazil's logistics industry. Major 3PL providers are deploying autonomous mobile robots in urban fulfilment centres, reducing labour intensity and improving order accuracy for e-commerce and FMCG clients.

2. Multimodal Integration and Intermodal Corridor Development

Brazil is systematically building integrated multimodal corridors connecting agricultural producing areas in Mato Grosso and Goiás with Atlantic seaports through rail-road-port interfaces. RUMO's North-South Railroad extension and Wilson Sons' port terminal expansions are creating cost-efficient export corridors.

3. E-Commerce Fulfilment Network Densification

Regional fulfilment centres, micro-distribution hubs, and same-day delivery networks are expanding beyond São Paulo into secondary markets including Manaus, Recife, and Fortaleza. Investment from platforms including Mercado Libre and Shopee is accelerating regional logistics infrastructure development.

4. Green Logistics and Sustainable Fleet Adoption

Brazilian logistics operators are piloting electric truck deployments in urban last-mile routes, investing in solar-powered warehouse facilities, and adopting sustainable packaging to meet ESG commitments from multinational clients and respond to growing consumer sustainability expectations.

Industry Value Chain Analysis

The Brazil logistics value chain spans six stages from transport infrastructure through end-customer fulfilment. 3PL/4PL management and last-mile delivery capture the highest value-add margins, while infrastructure ownership and carrier operations generate asset-intensive, volume-driven revenue streams.

|

Stage |

Key Players / Examples |

|

Transport Infrastructure |

ANTT (federal roads), ANTAQ (ports), ANAC (airports); Porto Itapoá, Porto do Açu |

|

Carrier Operations |

Braspress, Jadlog, Azul Cargo, Latam Cargo |

|

Warehousing & Storage |

GLP Brasil, Prologis, Localfrio, JSL Logistica |

|

3PL / 4PL Management |

DHL Group, CEVA Logistics, Luft Logistics, JSL S.A. |

|

Last-Mile Delivery |

Correios, Total Express, Loggi, Mercado Envios |

|

End-Use Industries |

Manufacturing, Retail, Food & Beverages, Healthcare, Oil & Gas, Agribusiness |

Integrated logistics providers with captive trucking fleets, owned warehouse networks, and proprietary technology platforms achieve superior cost structures relative to asset-light orchestrators. Vertical integration across warehousing and road transport is a meaningful competitive advantage in Brazil's price-sensitive logistics market.

Technology Landscape in the Brazil Logistics Industry

Warehouse Management and Automation Technology

Brazil's major urban fulfilment centres are deploying automated storage and retrieval systems (AS/RS), autonomous mobile robots (AMRs), and conveyor sorting systems. Leading developers including GLP Brasil and Prologis are constructing smart warehouses pre-fitted with robotics infrastructure to serve e-commerce and FMCG client requirements.

Transportation Management Systems and Digital Freight Platforms

Cloud-based TMS platforms enabling carrier procurement, route optimisation, real-time shipment tracking, and freight audit are achieving broad adoption among Brazilian shippers. Digital freight-matching platforms connecting shippers and carriers through API-enabled load tendering are reducing spot rate volatility and improving carrier utilisation.

Cold Chain Technology and Temperature Monitoring

IoT-enabled temperature loggers, blockchain-based food safety certification, and GPS-tracked refrigerated containers are gaining adoption driven by Brazilian food export regulatory compliance requirements. Localfrio and Tegma lead specialised cold chain infrastructure investment, supporting pharmaceutical and perishable food sectors.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Model Type |

3 PL |

51.0% |

2025 |

|

Transportation Mode |

Roadways |

60.0% |

2025 |

|

End Use |

Manufacturing |

15.0% |

2025 |

|

Region |

Southeast |

42.3% |

2025 |

By Model Type

To access detailed market analysis, Request Sample

3 PL commands a 51.0% majority share in 2025, owing to its comprehensive service offering encompassing transportation management, warehousing, inventory control, and distribution. The segment benefits from growing enterprise outsourcing of non-core logistics functions and the complexity of e-commerce fulfilment requirements for same-day and next-day delivery.

2 PL, at 32.4% in 2025, captures transport-focused contracts where companies require carrier management and freight execution without full supply chain outsourcing. The segment remains significant in automotive, chemicals, and bulk commodity transport sectors. 4 PL (16.6%) is the fastest-growing model type, driven by supply chain complexity requiring strategic orchestration layers above individual service execution.

By Transportation Mode

Roadways dominate the transportation mode segment at 60.0% in 2025, reflecting Brazil's 1.7-million-kilometers paved highway network and the door-to-door connectivity advantage of truck transport across the country's diverse geographic regions and dispersed consumer population centres.

Seaways (18.4%) are essential for agricultural commodity exports through the Northern Arc ports and Santos, and for coastal cabotage linking the industrial Southeast with Northern and Northeastern regions. Railways (13.2%) are expanding through RUMO and Vale's network investments, primarily serving agribusiness and mining corridors. Airways (8.4%) serve pharmaceutical, electronics, and perishables requiring rapid national distribution.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Southeast |

42.3% |

São Paulo manufacturing; Port of Santos; Rio de Janeiro commercial hubs; advanced multimodal networks |

|

South |

22.6% |

Agribusiness logistics (soybeans, poultry); Paraná Port complex; automotive manufacturing |

|

Northeast |

18.4% |

Suape and Pecém port expansion; Fortaleza e-commerce hub; Novo PAC infrastructure investment |

|

Central-West |

9.8% |

Cerrado agribusiness exports; FICO railway corridor; grain logistics from Mato Grosso and Goiás |

|

North |

6.9% |

Amazonian waterway logistics; Manaus free trade zone; Northern Arc port infrastructure |

The Southeast's 42.3% market dominance in 2025 is driven by the concentration of Brazil's manufacturing, retail, and financial services industries in the São Paulo metropolitan region and the port connectivity advantage of Santos, which handles approximately 30% of Brazil's total international trade volume.

The South region, with 22.6% in 2025, benefits from Brazil's position as the world's largest soybean and chicken exporter. The Northeast (18.4%) is experiencing accelerated logistics investment driven by port modernisation at Suape and Pecém under the Novo PAC, creating new distribution capacity to serve Brazil's second-largest consumer population corridor.

Competitive Landscape

The Brazil logistics market is moderately fragmented, with global 3PL multinationals competing against strong domestic operators. Global providers hold advantages in technology platforms, international network connectivity, and multinational client relationships, while domestic players benefit from local regulatory expertise, deeper geographic coverage, and established carrier relationships.

|

Company Name |

Key Services |

Market Position |

Global Strategic Focus |

|

DHL Group |

DHL Express, DHL Supply Chain, MyDHL+, Air Transport, Maritime Transport |

Leader |

Multinational clients; tech-driven 3PL; green logistics |

|

CEVA Logistics |

Air freight, Ocean freight, Ground and Rail Freight Solutions, Contract Logistics Solutions, Project Logistics Solutions |

Leader |

Integrated multimodal; automotive; healthcare segments |

|

Braspress |

Road freight, express delivery, Air Transport, Road-Waterway Transport |

Leader |

Brazil's largest express carrier; full national coverage |

|

JSL S.A. |

Road transport, Commodities Logistics |

Leader |

Largest Brazilian domestic 3PL by fleet size and revenue |

|

Luft Logistics |

Luft Agro, Luft Healthcare, Luft Solutions |

Challenger |

Brazil's leading healthcare logistics specialist by revenue |

Key players include DHL Group, CEVA Logistics, Braspress, JSL S.A., Luft Logistics, and others.

Key Company Profiles

DHL Group

DHL Group is the largest contract logistics provider operating in Brazil. The company manages warehouse space across automotive, retail, healthcare, and e-commerce sectors.

- Product Portfolio: DHL Express, MyDHL+, Air Transport, Maritime Transport, DHL Services

- Recent Developments: In February 2024, DHL Group partnered with Adidas to enhance its logistics operations in Brazil through the launch of a modern, omnichannel distribution center. The facility serves as a central hub supporting e-commerce, retail, and direct-to-consumer channels, enabling a more integrated and efficient supply chain. The new center incorporates semi-automated technologies such as conveyors, sorting systems, and digital warehouse management tools to improve speed, accuracy, and scalability of operations.

- Strategic Focus: DHL's Brazil strategy centres on technology leadership—deploying AI-powered WMS, robotics, and IoT tracking—to command premium pricing from multinational clients while expanding e-commerce fulfilment capabilities into secondary Brazilian markets beyond São Paulo.

Braspress

Braspress is Brazil's leading express road freight carrier, with a network covering all Brazilian states and municipalities, providing fractional-load (LTL) express road freight network nationwide with time-definite delivery commitments.

- Product Portfolio: Road freight, express delivery, Air Transport, Road-Waterway Transport.

- Recent Developments: In May 2025, Braspress Air Cargo officially launched its operations, marking its entry into the air freight sector as part of its broader logistics expansion strategy. The company began services after receiving regulatory approval, with initial routes focused on connecting key domestic cargo hubs in Brazil.

- Strategic Focus: Braspress differentiates on national coverage depth and service reliability, maintaining the densest branch network of any Brazilian road carrier, enabling competitive transit time commitments into remote municipalities where competing carriers have limited reach.

CEVA Logistics

CEVA Logistics, a subsidiary of CMA CGM Group, provides global supply chain management, contract logistics, freight forwarding, and distribution services across Brazil, serving automotive, industrial, healthcare, and retail sectors from different operating locations nationwide.

- Product Portfolio: Air freight, Ocean freight, Ground and Rail Freight Solutions, Contract Logistics Solutions, Project Logistics Solutions.

- Recent Developments: In October 2020, CEVA Logistics partnered with Ri-Happy Group to manage its logistics and e-commerce operations in Brazil, supporting the retailer’s omnichannel growth strategy. Under the agreement, CEVA oversees key supply chain functions including warehousing, inventory management, and order fulfilment through a centralized distribution network.

- Strategic Focus: CEVA leverages CMA CGM's global sea freight network to offer seamless Brazilian export and import logistics solutions, targeting multinational manufacturers and commodity exporters requiring integrated end-to-end supply chain services across all transport modes.

Market Concentration Analysis

The Brazil logistics market is moderately fragmented at the national level, with no single company holding more than 8–10% of total market revenue. The market is bifurcated between global 3PL multinationals and large domestic operators in the corporate segment, and tens of thousands of independent truckers and small carriers in the fragmented spot freight market.

Consolidation in the 3PL segment is accelerating through acquisitions—Scan Global Logistics acquired Blu Logistics Brasil in September 2024—as global providers seek scale and geographic coverage in South America's largest logistics market. Technology-led consolidation is also occurring as platform providers aggregate fragmented carrier capacity through digital freight-matching applications.

Investment & Growth Opportunities

Fastest-Growing Segments

4 PL at ~5.2% CAGR through 2034 is the highest-growth model segment, driven by supply chain digitisation, nearshoring of manufacturing to Brazil, and the growing need for strategic supply chain orchestration across multi-tier supplier networks. Airways at ~4.8% CAGR reflects pharmaceutical and electronics sector growth.

Emerging Markets

The Northeast region is the fastest-growing logistics geography within Brazil, benefiting from Novo PAC port infrastructure investment at Suape and Pecém, a growing consumer market in Fortaleza and Recife, and lower labour and warehouse rental costs attracting new distribution centre development from national and international operators.

Venture & Investment Trends

Private equity investment in Brazilian logistics platforms is accelerating, with significant capital flowing into freight-tech startups targeting the fragmented spot trucking market. ESG-driven investment in green warehouse certification and electric fleet transition is emerging as a key differentiating investment theme in institutional logistics asset acquisition.

Future Market Outlook (2026-2034)

The Brazil logistics market is forecast to expand from USD 126.97 Billion in 2025 to USD 176.74 Billion by 2034 at a CAGR of 3.74%, adding USD 49.77 Billion in incremental annual market value over the forecast period. This growth reflects structural drivers including e-commerce penetration, infrastructure modernisation, and increasing supply chain complexity.

Three technological forces will most significantly shape Brazil's logistics landscape through 2034: autonomous vehicle and drone delivery pilots reshaping last-mile economics; blockchain-enabled trade documentation accelerating customs clearance cycle times; and AI-powered demand sensing enabling higher asset utilisation through dynamic route and inventory optimisation across all logistics modes.

Research Methodology

Primary Research

Primary research encompassed structured interviews with logistics industry stakeholders, including senior commercial managers at Brazilian 3PL providers, freight forwarding executives, port terminal operators, supply chain directors at manufacturing and retail firms, and transportation regulatory officials at ANTT and ANTAQ. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include ANTT Annual Freight Statistical Report (2020–2024), ANTAQ Maritime Transport Statistics, IBGE National Statistics (GDP, industrial output), CNT Road Transport Performance Survey, Brazilian Association of Logistics Operators (ABOL) reports, ABRALOG industry publications, and trade media including Revista Tecnologística and Portal Mundo Logístico.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, e-commerce GMV expansion, industrial output indices, government infrastructure spending commitments, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty.

Brazil Logistics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Model Types Covered | 2 PL, 3 PL, 4 PL |

| Transportation Modes Covered | Roadways, Seaways, Railways, Airways |

| End Uses Covered | Manufacturing, Consumer Goods, Retail, Food and Beverages, IT Hardware, Healthcare, Chemicals, Construction, Automotive, Telecom, Oil and Gas, Others |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | DHL Group, CEVA Logistics, Braspress, JSL S.A., Luft Logistics, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Brazil Logistics Market Report

The Brazil logistics market reached USD 126.97 Billion in 2025, reflecting consistent demand from e-commerce expansion, industrial activity growth, and ongoing infrastructure modernisation under federal investment programmes.

The market is projected to reach USD 176.74 Billion by 2034, growing at a CAGR of 3.74% during 2026-2034, driven by 3PL outsourcing growth, government infrastructure investment, and digital supply chain transformation.

3 PL leads with a 51.0% share in 2025, valued for its comprehensive outsourced supply chain services including warehousing, transport, fulfilment, and technology integration that enable clients to focus on core business activities.

Roadways lead at 60.0% in 2025, reflecting Brazil's extensive 1.7-million-kilometre highway network and the flexibility of truck transport for door-to-door delivery across the country's vast and geographically diverse territory.

The Southeast commands a dominant 42.3% market share in 2025, driven by São Paulo's industrial and commercial concentration, the Port of Santos container terminal, and advanced multimodal logistics infrastructure serving Brazil's primary economic hub.

4 PL is the fastest-growing model at ~5.2% CAGR through 2034, driven by supply chain complexity, digital transformation, and growing enterprise demand for strategic orchestration above individual logistics service execution.

Leading companies include DHL Group, CEVA Logistics, Braspress, JSL S.A., Luft Logistics, and others.

Key challenges include infrastructure deficits in interior regions, regulatory complexity from Brazil's multi-layered tax system, diesel price volatility, and a shortage of skilled truck drivers and logistics technology professionals that constrains capacity expansion.

The Southeast's 42.3% share reflects the concentration of São Paulo's industrial clusters, Rio de Janeiro's commercial hubs, and the Port of Santos, Latin America's largest container terminal, creating an unparalleled logistics demand concentration in Brazil's primary economic region.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)