Brazil Pet Food Market Size, Share, Trends and Forecast by Product, Animal Type, Ingredient Type, Sales Channel, and Region, 2026-2034

Brazil Pet Food Market Size, Share, Trends & Forecast (2026-2034)

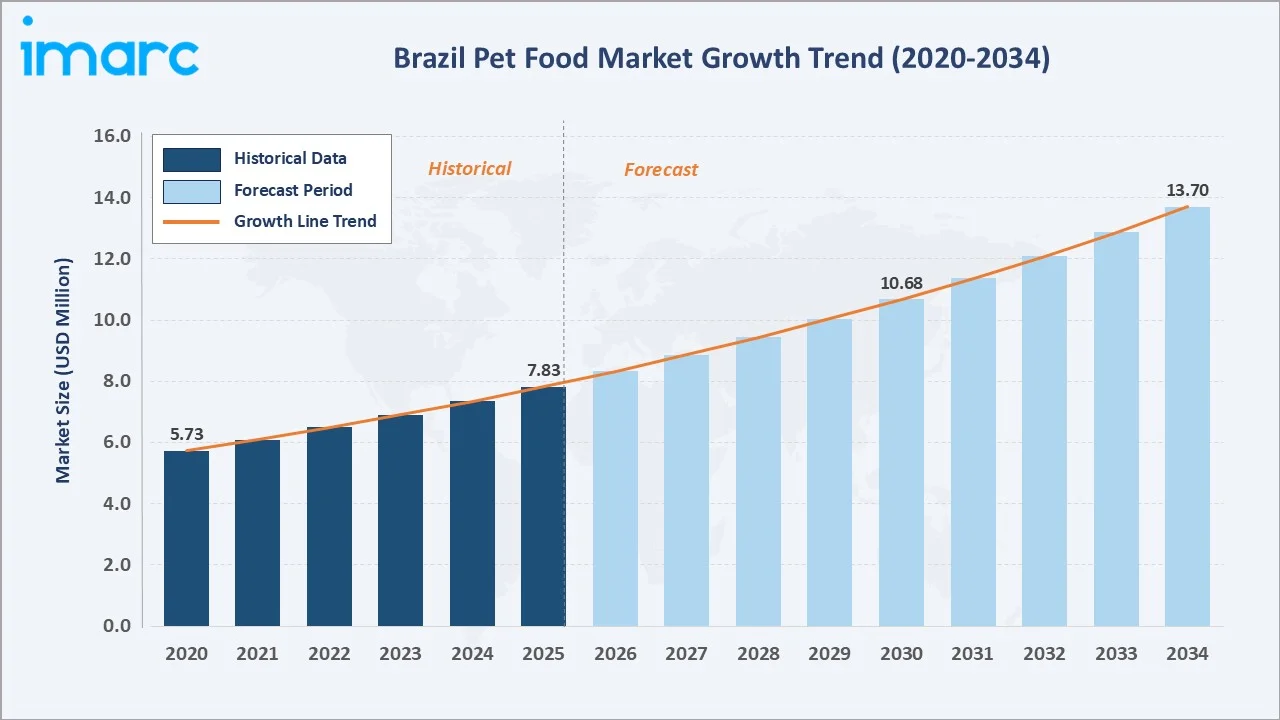

The Brazil pet food market size was valued at USD 7.83 Million in 2025 and is projected to reach USD 13.70 Million by 2034, exhibiting a CAGR of 6.42% during the forecast period 2026-2034. Rising pet humanization, expanding middle-class households, and surging demand for premium nutrition are the primary growth catalysts. The dog segment dominates with a 61.4% share in 2025, while animal-derived ingredients lead at 58.6%. Southeast Brazil commands 46.2% of the national market, anchored by São Paulo and Rio de Janeiro.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 7.83 Million |

|

Forecast Market Size (2034) |

USD 13.70 Million |

|

CAGR (2026-2034) |

6.42% |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Animal Segment |

Dog (61.4%) |

|

Leading Ingredient Type |

Animal-derived (58.6%) |

|

Leading Region |

Southeast (46.2%) |

To get more information on this market, Request Sample

The Brazil pet food market growth trajectory from 2020 through 2034 is driven by therapeutic nutrition, e-commerce and subscription growth, grain-free premiumization, sustainable proteins, and personalized pet diets.

Executive Summary

The Brazil pet food market is undergoing a structural transformation powered by pet humanization, rising disposable incomes, and rapidly evolving consumer nutrition awareness. Valued at USD 7.83 Million in 2025, the market is on a sustained upward trajectory projected to reach USD 13.70 Million by 2034 – a robust CAGR of 6.42%, making Brazil one of Latin America's most attractive pet nutrition markets.

The dog segment commands 61.4% of the market in 2025, reflecting Brazil's massive canine population. Cats hold a 27.6% share, while birds account for 6.2%. Animal-derived formulations dominate ingredients at 58.6%, followed by plant-derived at 31.4%. Premium, functional, and health-specific pet food formats are displacing standard kibble as consumers seek life-stage and breed-specific nutrition solutions.

Southeast Brazil leads regional distribution at 46.2%, anchored by São Paulo and Rio de Janeiro. The South follows at 22.8%, while the Northeast accounts for 14.6%. E-commerce growth, expanding specialized pet retail, and international brand investments continue to reshape the competitive landscape. The market outlook remains decidedly positive through 2034.

Key Market Insights

|

Insight Category |

Data Point |

|

Largest Animal Segment |

Dog – 61.4% share (2025) |

|

Fastest Growing Segment |

Cat food – urban millennial adoption driving premium demand |

|

Leading Ingredient Type |

Animal-derived – 58.6% share (2025) |

|

Leading Region |

Southeast – 46.2% of the national market (2025) |

|

Top Companies |

Mars Petcare, Nestlé Purina, BRF Global, PremieRpet, Adimax |

|

Market Opportunity |

Premium & functional nutrition; North and Central-West remain underpenetrated |

Key analytical observations supporting the above data:

- Dog segment's 61.4% dominance in 2025 reflects Brazil's status as the world's second-largest canine market, with approximately 35 million dogs – fueling high-frequency purchases across all income brackets.

- Animal-derived ingredients (58.6%) maintain leadership due to high protein bioavailability and superior palatability. Chicken, beef, and fish-based proteins dominate formulations across both mass and premium tiers.

- Cat food demand is accelerating, driven by urban apartment living and increasing cat adoption among millennials aged 25–40 – a demographic showing 3× higher premium product spending than older cohorts.

- Southeast Brazil's 46.2% dominance is underpinned by São Paulo State alone accounting for an estimated 35%+ of national pet food retail turnover, with dense specialized pet shop networks and high e-commerce penetration.

- The North and Central-West regions – representing 7.2% and 9.2% respectively – are emerging growth frontiers as retail infrastructure and pet ownership rates rise with ongoing urbanization.

Brazil Pet Food Market Overview

Pet food encompasses commercially manufactured products designed to meet the complete nutritional requirements of companion animals, including dogs, cats, birds, and other domestic species. The Brazil market spans dry kibble, wet food, treats, snacks, and specialized therapeutic formulations. Products are distributed via specialized pet shops, internet channels, hypermarkets, and veterinary clinics.

Brazil's pet food ecosystem operates at the intersection of veterinary science, agricultural supply chains, retail evolution, and shifting consumer lifestyle trends. The country's agricultural strength provides a cost-competitive raw material base for both domestic manufacturers and multinationals. Macroeconomic factors such as GDP growth, real wage increases, and urbanization continue to expand the addressable market. Pet humanization – the cultural phenomenon of treating pets as family – is the most transformative demand driver, elevating food quality expectations and per-pet spending.

Market Dynamics

To evaluate market opportunities, Request Sample

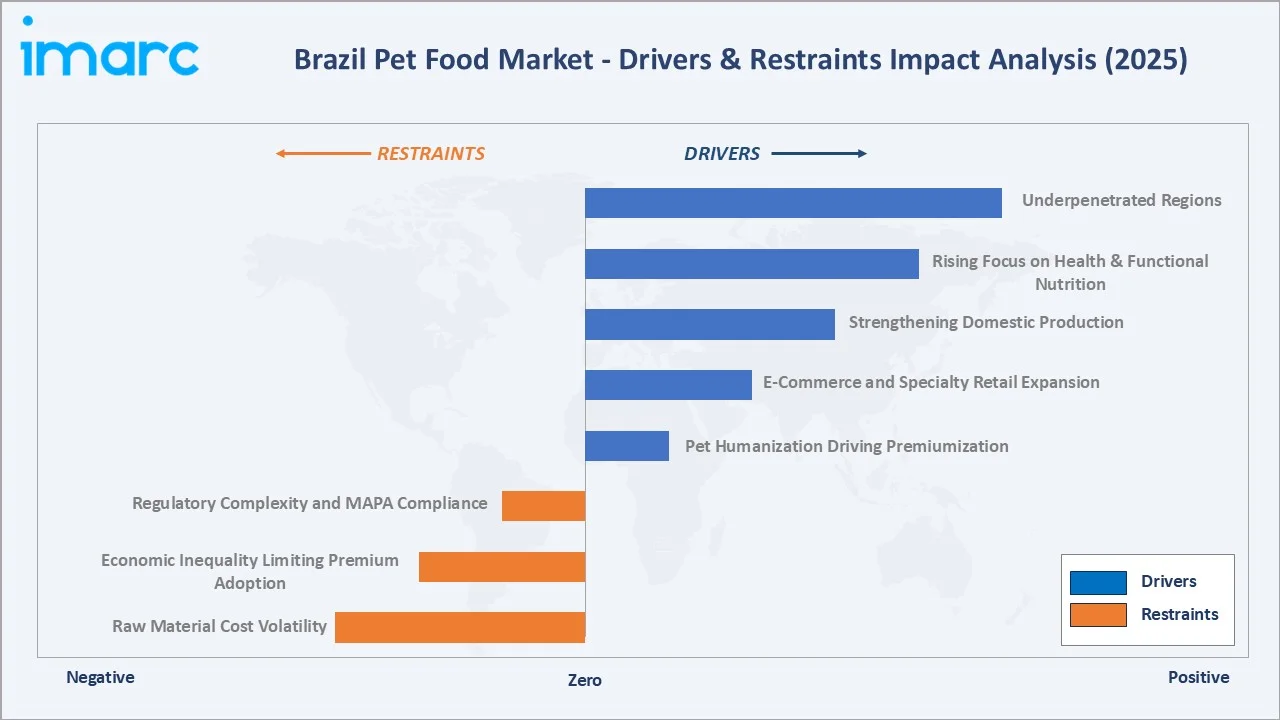

Market Drivers

- Pet Humanization Driving Premiumization: Pets are increasingly treated as family, boosting demand for premium, natural, and functional foods (e.g., grain-free, high-protein, life-stage-specific). Millennials and Gen Z are the primary growth drivers.

- E-Commerce and Specialty Retail Expansion: Specialty pet stores lead sales, while e-commerce is growing steadily through subscriptions, convenience, and wider reach beyond major cities.

- Strengthening Domestic Production: Local manufacturers are expanding capacity and premium portfolios, reducing import dependence and improving cost competitiveness.

- Rising Focus on Health & Functional Nutrition: Growing awareness of pet health is driving demand for veterinary-recommended and functional diets targeting digestion, mobility, and overall wellness.

Market Restraints

- Raw Material Cost Volatility: Prices of key protein inputs such as poultry, fish meal, and beef by-products remain highly volatile, driven by global commodity cycles, feed costs, and export demand. The 2022–2023 inflationary cycle significantly increased input costs, pressuring manufacturer margins and limiting expansion, particularly for mid-sized and regional players.

- Economic Inequality Limiting Premium Adoption: High income inequality in Brazil (Gini ~0.5+) constrains widespread premium pet food adoption. The market remains volume-driven, with economy and mid-tier products dominating sales. Premium demand is concentrated in higher-income urban regions—especially São Paulo and the South—while penetration in the North and Northeast remains comparatively low.

Market Opportunities

- Underpenetrated Regions: North and Central-West Brazil offer strong growth potential due to low current penetration and improving retail and logistics infrastructure.

- Sustainable & Natural Products: Rising demand for clean-label, sustainable, and alternative-protein pet foods creates opportunities for innovation and premium differentiation.

Market Challenges

- Regulatory Complexity and MAPA Compliance: Brazil’s pet food industry is regulated by the Ministry of Agriculture, Livestock, and Food Supply (MAPA), which enforces ingredient approvals, product registration, and labeling standards. Approval timelines for new or functional ingredients can be lengthy, creating delays in product innovation and market entry.

- Highly Competitive and Fragmented Market: The market is highly fragmented, with a large number of domestic and international brands competing across price segments. Intense competition drives pricing pressure, while requiring continuous innovation, strong branding, and distribution capabilities to sustain market share.

Emerging Market Trends

1. Functional and Therapeutic Nutrition Mainstreaming

Health-focused pet foods (joint, digestive, immunity, cognitive support) are moving beyond veterinary channels into mass retail. Brands like Royal Canin and Hill's Pet Nutrition are expanding condition- and breed-specific portfolios, reflecting growing alignment with human wellness trends.

2. E-Commerce and Subscription Model Expansion

Online platforms such as Petlove and Cobasi are accelerating digital adoption through subscriptions, auto-replenishment, and personalized offerings—driving recurring revenue and wider geographic reach.

3. Premiumization and Grain-Free Formulation Growth

Demand for premium, grain-free, and high-protein diets is rising, particularly in urban centers. Growth is driven by higher-income consumers and the increasing availability of international and specialized brands.

4. Sustainable Packaging and Eco-Conscious Branding

Sustainable packaging, responsible sourcing, and transparency are becoming key differentiators. Environmentally conscious consumers—especially millennials—are influencing brand preference toward eco-friendly offerings.

5. Veterinary Channel and Prescription Diet Growth

Veterinary-recommended and prescription diets are gaining traction due to rising pet health awareness. Therapeutic nutrition for conditions like obesity, renal issues, and sensitivities is emerging as a high-growth niche.

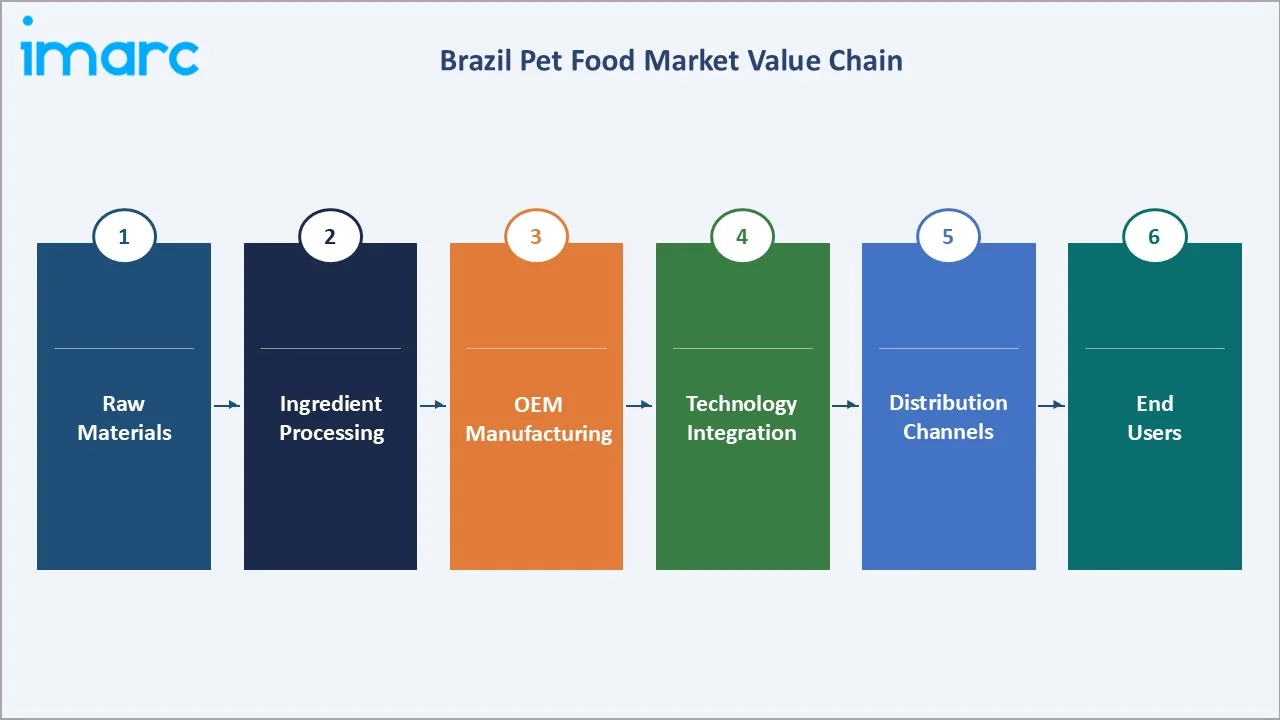

Industry Value Chain Analysis

Brazil's pet food industry value chain spans five integrated stages from raw material sourcing through consumer delivery. Brazil's agricultural abundance provides a competitive foundation for the industry, with domestic soy, corn, chicken, and beef by-product supplies supporting cost-efficient formulation.

|

Stage |

Key Activities |

Key Players / Examples |

|

Raw Materials |

Protein meals, grains, vitamins, minerals, fats |

BRF S.A., JBS, and agricultural cooperatives |

|

Ingredients & Components |

Premix formulation, flavor enhancers, preservatives |

ADM, Cargill, DSM-Firmenich |

|

Manufacturing |

Extrusion, wet processing, and treat manufacturing |

PremieRpet, Adimax, Mars Petcare Brazil |

|

Distribution |

Wholesale logistics, regional distributors, cold chain |

Cobasi, Pet Smile, and regional wholesalers |

|

End Users / Retail |

Specialized pet shops, e-commerce, hypermarkets, vets |

Petlove, Petz, Cobasi, Carrefour, Mercado Livre |

OEMs and branded manufacturers hold the highest strategic value by converting raw inputs into finished nutritional solutions.

Technology Landscape in the Pet Food Industry

Advanced Extrusion and Processing Technology

High-moisture extrusion and twin-screw extrusion technology enable complex kibble textures, enhanced palatability profiles, and superior nutrient retention. Brazilian manufacturers are investing in precision extrusion lines that support breed-specific and life-stage-optimized formulations, reducing production costs while improving product quality consistency.

Nutritional Genomics and Personalization

Advances in pet nutritional genomics are enabling breed-specific and health-condition-specific formulation science. Companies are developing data-driven personalization platforms where pet owners input breed, age, weight, and health conditions to receive customized nutrition recommendations and subscription delivery – a significant differentiator for premium brands.

Sustainable Protein Innovations

Novel protein sources – including insect protein, mycoproteins, and single-cell proteins – are entering Brazil's pet food innovation pipeline. In June 2025, Enifer partnered with FS to produce mycoprotein from corn ethanol by-products, creating a sustainable protein source for pet food and aquaculture.

Digital Supply Chain and Traceability

Blockchain-based ingredient traceability and digital supply chain platforms are enabling manufacturers to verify ingredient provenance claims and support clean-label marketing. As Brazilian consumers demand greater transparency in pet food sourcing, digital traceability investment is becoming a competitive differentiator for premium and natural product brands.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the Brazil pet food market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on animal type, ingredient type, sales channel, and product type.

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Animal Type |

Dog |

61.4% |

2025 |

|

Ingredient Type |

Animal-derived |

58.6% |

2025 |

|

Product |

🔒 |

🔒 |

2025 |

|

Sales Channel |

🔒 |

🔒 |

2025 |

|

Region |

Southeast |

46.2% |

2025 |

By Animal Type

To access detailed market analysis, Request Sample

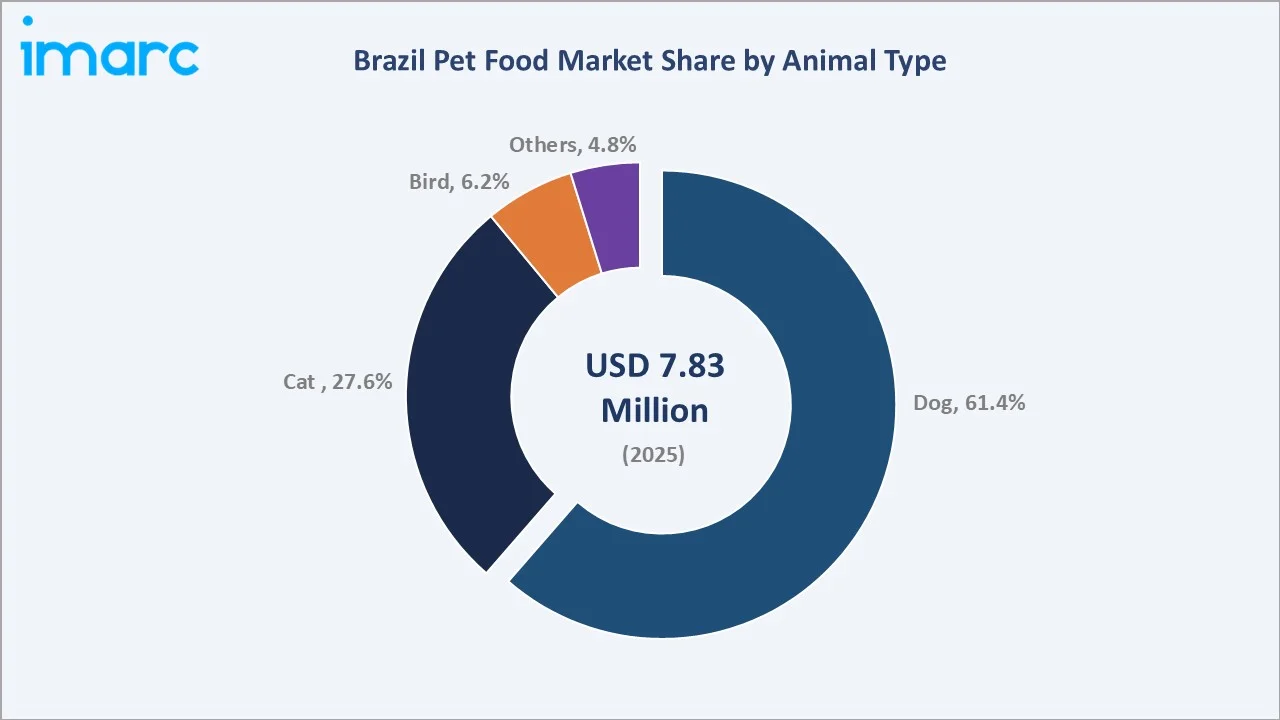

Dogs represent the dominant animal segment with a 61.4% share in 2025, reflecting Brazil's massive canine population of approximately 35 million dogs. Demand is driven by high purchase frequency and strong owner investment in canine nutrition across all price tiers. The segment encompasses dry food, wet food, treats, and specialized health formulations targeting breed-specific needs.

Cats hold a 27.6% share and represent the fastest-growing sub-segment. Rising urban cat adoption – fueled by apartment-friendly lifestyles and lower maintenance requirements – is driving demand for premium wet cat food, functional treats, and breed-specific nutrition. Birds account for 6.2%, with seed-based, grain, and specialized pellet formulations serving a loyal consumer base primarily in Northeast and Southeast Brazil.

By Ingredient Type

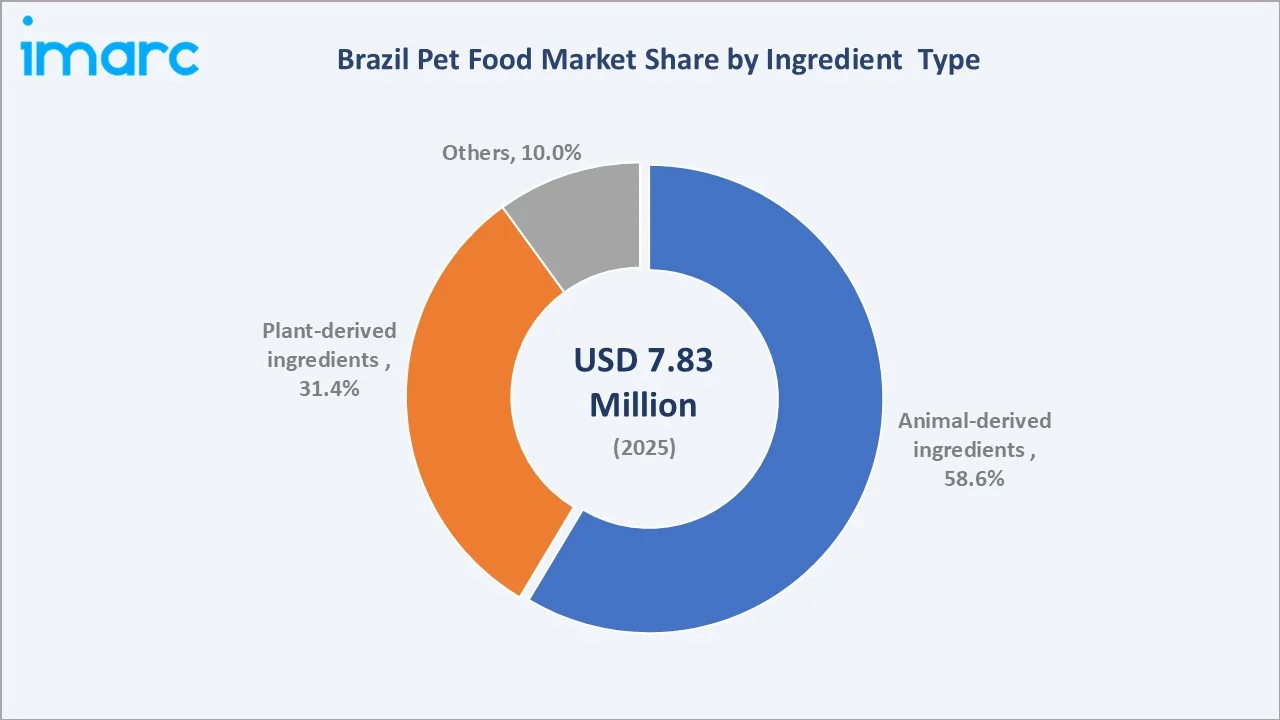

Animal-derived ingredients dominate with a 58.6% share in 2025. Chicken, beef, pork, and fish-based protein sources are the foundational building blocks of Brazilian pet food formulations. Their high protein bioavailability and superior palatability make them the preferred choice for both premium and mass-market segments. The category encompasses meat meals, fresh meat inclusions, organ meats, and marine-derived proteins.

Plant-derived ingredients account for 31.4% of the market, reflecting growing interest in grain-free, legume-based, and plant-protein formulations. While animal-derived proteins retain dominance, plant-derived ingredients are gaining traction in vegan pet food niches and as cost-effective filler alternatives in mass-market products. Others – including synthetic vitamins, minerals, and novel proteins – account for 10.0%.

Regional Market Insights

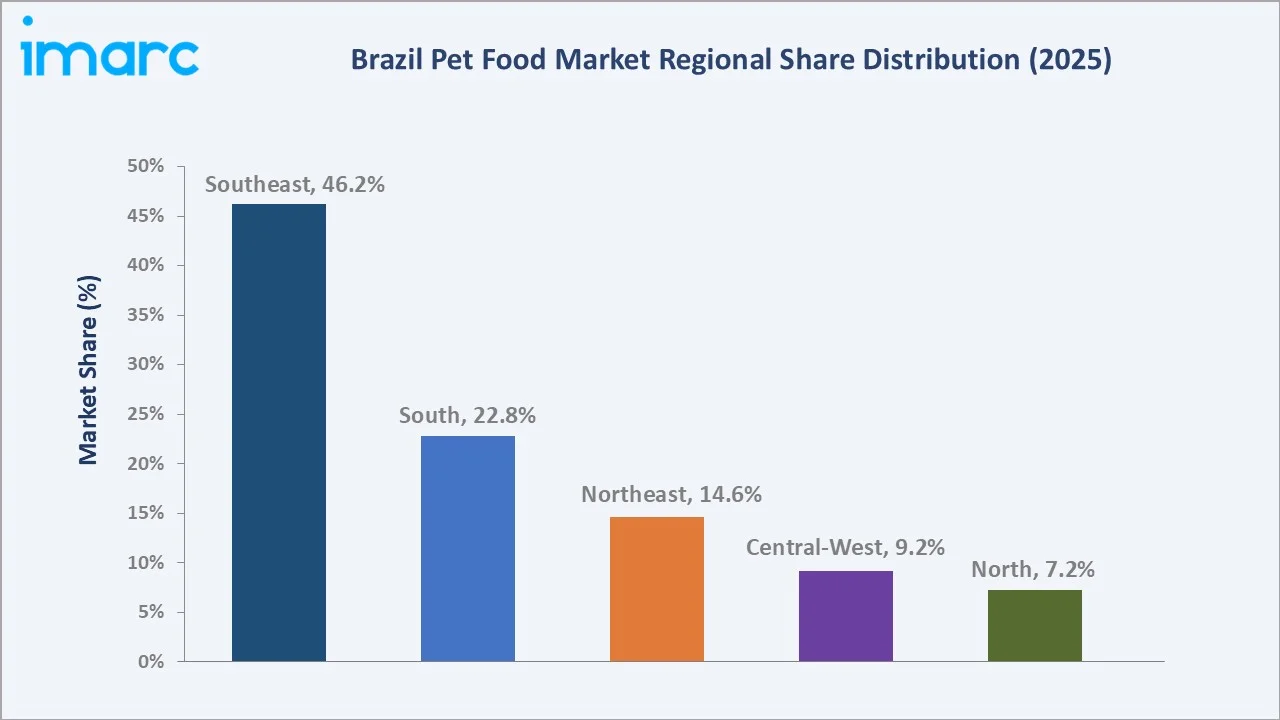

Brazil's vast geographic and economic diversity creates distinct regional pet food market dynamics. The Southeast leads with 46.2% of the national market in 2025, while the South holds 22.8%, the Northeast 14.6%, Central-West 9.2%, and the North 7.2%.

Southeast Brazil commands 46.2% of the national market, driven by São Paulo and Rio de Janeiro's combined pet population of approximately 15 million animals and sophisticated multi-channel retail infrastructure. The South (22.8%) benefits from above-average household incomes, strong German and Italian heritage pet care cultures in Rio Grande do Sul, and a mature, specialized pet retail network.

|

Region |

Share (2025) |

Key Growth Driver |

Strategic Outlook |

|

Southeast |

46.2% |

São Paulo & Rio de Janeiro density; premium retail |

Dominant market; premiumization and e-commerce expansion |

|

South |

22.8% |

High incomes, strong European pet culture heritage |

Above-average premium adoption; strong local brand base |

|

Northeast |

14.6% |

Growing middle class; urban adoption in Fortaleza, Recife |

Value-segment growth; accessible retail formats needed |

|

Central-West |

9.2% |

Agribusiness income growth; Brasília urban market |

Emerging opportunity; specialty retail expanding in capitals |

|

North |

7.2% |

Urbanization in Manaus and Belém; rising pet adoption |

Underpenetrated frontier; logistics investment needed |

The Northeast (14.6%) is an emerging growth frontier where a rising middle class in Fortaleza, Recife, and Salvador is driving pet adoption and food quality upgrades. Central-West (9.2%) and North (7.2%) remain underpenetrated but offer significant long-term opportunity as urbanization accelerates and retail logistics improve.

Competitive Landscape

Brazil's pet food competitive landscape is moderately fragmented. Global multinationals compete alongside strong domestic champions and emerging regional brands. Competition centers on brand equity, nutritional science capabilities, distribution reach, and pricing strategy. Premium and super-premium segments are the primary battlegrounds as multinationals and domestic leaders vie for the growing high-spend consumer cohort.

The matrix shows Mars Petcare and Nestlé Purina leading in both market presence and innovation, while PremieRpet and Adimax are strong regional challengers with growing capabilities.

|

Company |

Brand(s) |

Position |

Key Strength |

|

Mars Petcare |

Pedigree, Whiskas, Royal Canin |

Market Leader |

Largest portfolio; veterinary channel strength |

|

Nestlé Purina |

Pro Plan, Friskies, Dog Chow |

Strong Challenger |

Premium science-based nutrition; deep R&D investment |

|

PremieRpet |

Premier, Quatree |

Domestic Leader |

Scale + local knowledge; BRL 200M capacity expansion |

|

Adimax Pet |

Magnus, Fórmula Natural |

Growing Challenger |

Premium-to-economy coverage; acquisition-led growth |

|

Colgate-Palmolive |

Hill's Pet Nutrition |

Specialist |

Veterinary and therapeutic diet leadership |

|

BRF Global |

Gran Plus, Biofresh |

Regional Player |

Vertical integration; agricultural raw material access |

Key Company Profiles

Mars Petcare

Mars Petcare is the global leader in pet nutrition, headquartered in McLean, Virginia, USA, and operating in over 50 countries. In Brazil, Mars held approximately 20.7% market share in 2020 and has maintained leadership through brand investment and broad retail penetration across all five regions.

- Product Portfolio: Pedigree, Whiskas, Royal Canin, Sheba, Cesar. Royal Canin's breed-specific and veterinary diet lines are the cornerstone of Mars's premium positioning in Brazil.

- Recent Developments: In May 2025, Mars strengthened its Brazil presence through a new distribution center investment to expand supply and reach across regions, supporting brands including Royal Canin.

- Strategic Focus: Dual-market strategy targeting mass-market volume through Pedigree and Whiskas, while driving premium revenue growth through Royal Canin's specialist positioning in veterinary and specialized pet retail channels.

Nestlé Purina PetCare

Nestlé Purina PetCare, headquartered in St. Louis, Missouri, operates manufacturing facilities in Brazil, supporting local production of flagship brands for the domestic market. Purina is one of the world's largest pet nutrition companies.

- Product Portfolio: Purina Pro Plan, Dog Chow, Cat Chow, Friskies, Purina ONE. Pro Plan's science-based formulations target the premium and super-premium segments with high-protein, life-stage-specific nutrition.

- Recent Developments: In March 2026, Nestlé Purina invested BRL 2.5 billion in a new Brazil facility, nearly doubling wet pet food capacity and reinforcing its premiumization strategy.

- Strategic Focus: Premium segment leadership through science-backed nutrition, veterinary channel development, and digital consumer engagement, leveraging Nestlé's retail scale across Southeast and South Brazil.

PremieRpet

PremieRpet is Brazil's leading domestic pet food manufacturer, headquartered in Dourados, Mato Grosso do Sul, with an investment of over BRL 200 million in production capacity expansion between 2022 and 2024.

- Product Portfolio: Premier Nattu, Premier Golden, Quatree, SuperFino – covering premium grain-free, natural, and functional formulations across all life stages for dogs and cats.

- Recent Developments: In May 2025, PremieRpet invested ~R$1 million to support a veterinary research center at the University of São Paulo, enabling the first pet-specific DEXA scanner in Latin America for obesity and health studies.

- Strategic Focus: Defend domestic market leadership through continuous premium innovation, large-scale domestic production efficiency, and superior distribution in Central-West and Southeast Brazil.

Market Concentration Analysis

The Brazil pet food market exhibits moderate concentration. The top 5 players – Mars Petcare, Nestlé Purina, PremieRpet, Adimax, and Colgate-Palmolive (Hill's) – collectively account for an estimated 55–60% of total market revenue in 2025. The remaining 40–45% is distributed among over 200 registered domestic and regional brands.

Global multinationals hold premium and veterinary segment share through brand authority and R&D investment, while domestic champions compete on price-value ratios, local ingredient sourcing, and regional distribution strength. Consolidation is a growing trend, as evidenced by Adimax's acquisition of Magnus and Fórmula Natural brands, signaling a wave of M&A activity as players seek scale to compete with multinationals.

The market is expected to see further consolidation through 2030, with mid-sized domestic brands likely targets for acquisition by regional and international investors seeking Brazil market entry or scale-up. The premium segment is bifurcating into science-based nutrition brands and natural/clean-label brands.

Investment & Growth Opportunities

- Premium and Functional Pet Nutrition: The fastest-growing segment commands 40–70% price premiums. Investment in R&D for breed-specific, life-stage, and health-condition formulations will capture the rapidly expanding high-spend consumer cohort, particularly in Southeast and South Brazil.

- North and Central-West Regional Expansion: With 16.4% combined share but growing pet populations, these regions are the highest-growth white-space opportunities. Investment in regional distribution infrastructure and local retail partnerships can deliver above-market growth rates.

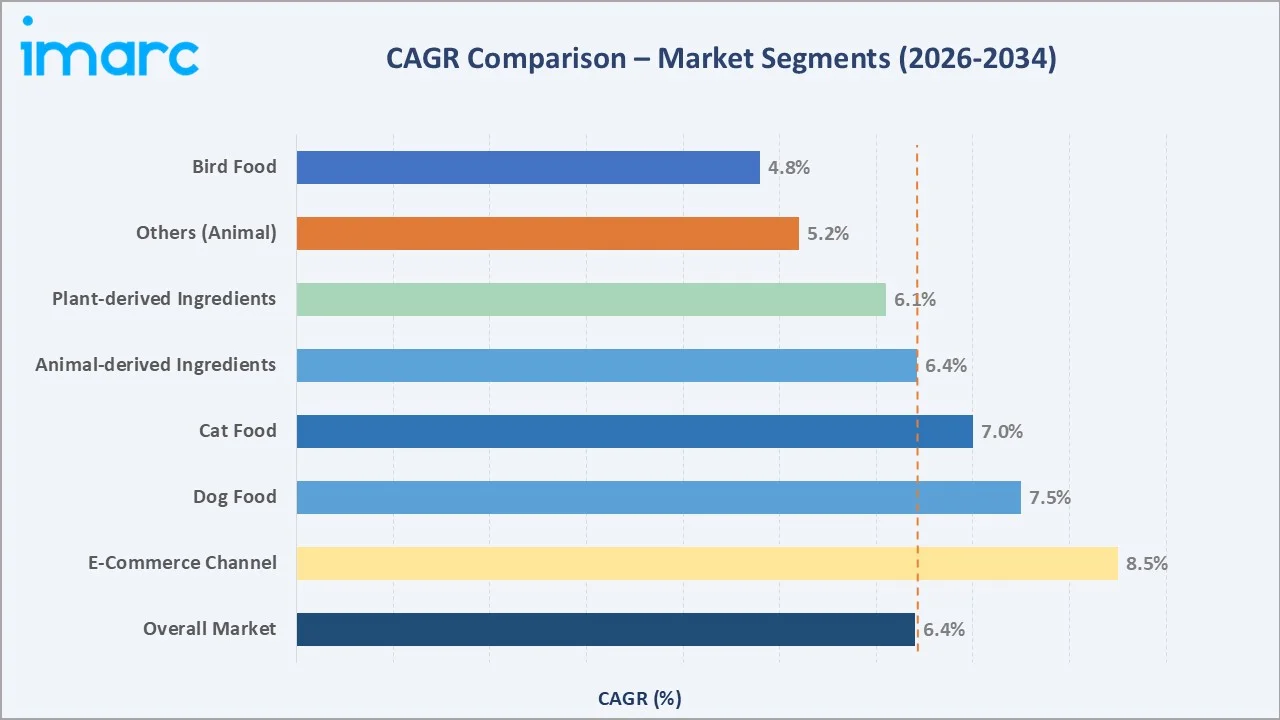

- E-Commerce and Direct-to-Consumer Platforms: Online pet food sales are growing at over 8% CAGR, outpacing overall market growth. Investment in subscription models, AI-driven personalization, and last-mile delivery logistics will capture the digital-native pet owner segment.

- Sustainable Protein and Eco-Innovation: Novel proteins (insects, mycoproteins, plant-based alternatives) and sustainable packaging are emerging strategic differentiators for premium brands. The Enifer-FS mycoprotein partnership represents an investable trend with strong long-term demand drivers.

- Veterinary and Therapeutic Diet Channel: Prescription and veterinary-recommended diets are growing at 10–12% CAGR – approximately double the overall market rate. Partnerships with veterinary clinic networks and investment in therapeutic formulation capabilities present strong returns for specialist nutrition brands.

Future Market Outlook (2026-2034)

The Brazil pet food market is positioned for sustained growth through 2034. From a base of USD 7.83 Million in 2025, the market will reach USD 13.70 Million by 2034, supported by a 6.42% CAGR. This trajectory is underpinned by structural demand drivers unlikely to reverse: rising pet ownership, deepening pet humanization culture, income growth, and expanding retail infrastructure.

Premiumization will remain the dominant value-growth driver. By 2030, premium and super-premium formulations are expected to account for over 30% of market value, up from approximately 20% in 2025. Functional nutrition, subscription e-commerce, and veterinary channel expansion will be the three structural growth engines. Domestically manufactured products will gain share as Brazilian manufacturers continue to invest in scale and quality.

Technology disruption – including AI-driven nutrition personalization, sustainable protein innovation, and blockchain traceability – will reshape competitive dynamics. The North and Central-West regions will emerge as growth frontiers as urbanization and income convergence continue. Brazil's market is expected to become one of the top 5 global pet food markets by value within the next decade.

Research Methodology

IMARC Group employs a rigorous three-stage research methodology to ensure data accuracy, analytical depth, and forecast reliability for the Brazil Pet Food Market study.

Primary Research

In-depth interviews with 50+ industry stakeholders, including pet food manufacturers, distributors, specialized retailers, veterinarians, and regulatory experts across Brazil's five regions. Consumer surveys capturing pet owners' purchasing behavior, brand preferences, and spending patterns.

Secondary Research

Comprehensive review of MAPA regulatory databases, IBGE data, trade association publications (ANFALPET), company annual reports, scientific journals, and industry news sources spanning 2019–2025.

Quantitative Forecasting Models

Statistical regression models, bottom-up market sizing, and scenario-based forecasting incorporating macroeconomic variables (GDP, inflation, disposable income), demographic trends, and pet population data to project market values through 2034.

Brazil Pet Food Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessmen:

|

| Products Covered | Dry Pet Food, Wet Pet Food, Treats and Snacks, Others |

| Animal Types Covered | Dog, Cat, Bird, Others |

| Ingredient Types Covered | Plant-derived, Animal-derived, Others |

| Sales Channels Covered | Specialized Pet Shops, Internet Sales, Hypermarkets, Others |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | Mars Petcare, Nestlé Purina, PremieRpet, Adimax Pet, Colgate-Palmolive, BRF Global, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil pet food market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Brazil pet food market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil pet food industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Brazil Pet Food Market Report

The Brazil pet food market was valued at USD 7.83 Million in 2025 and is forecast to reach USD 13.70 Million by 2034, growing at a CAGR of 6.42%.

The market is projected to grow at a CAGR of 6.42% during the forecast period from 2026-2034, driven by premiumization and rising pet ownership.

Dogs dominate with a 61.4% market share in 2025, reflecting Brazil's status as the world's second-largest canine market with approximately 35 million dogs.

Key drivers include rising pet humanization, premiumization of nutrition, e-commerce expansion, growing middle-class income, and increasing health awareness among pet owners.

The Southeast region leads with a 46.2% market share in 2025, driven by São Paulo and Rio de Janeiro's large urban pet populations and advanced retail infrastructure.

Animal-derived ingredients dominate with a 58.6% share in 2025, valued for high protein bioavailability and superior palatability across all pet food product tiers.

Leading companies include Mars Petcare, Nestlé Purina, PremieRpet, Adimax Pet, Hill's Pet Nutrition (Colgate-Palmolive), and BRF Global, among others.

Key trends include functional and therapeutic nutrition, e-commerce and subscription growth, grain-free premiumization, sustainable proteins, and personalized pet diets.

Cat food accounts for 27.6% of Brazil's pet food market in 2025 and is the fastest-growing segment, driven by urban cat adoption among millennials and Gen Z.

Key challenges include raw material cost volatility, regulatory complexity under MAPA, economic inequality limiting premium penetration, and intense competition among 200+ brands.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)