Europe Artificial Intelligence Market Size, Share, Trends and Forecast by Type, Offering, Technology, System, End-Use Industry, and Country, 2026-2034

Europe Artificial Intelligence Market Size, Share, Trends & Forecast (2026-2034)

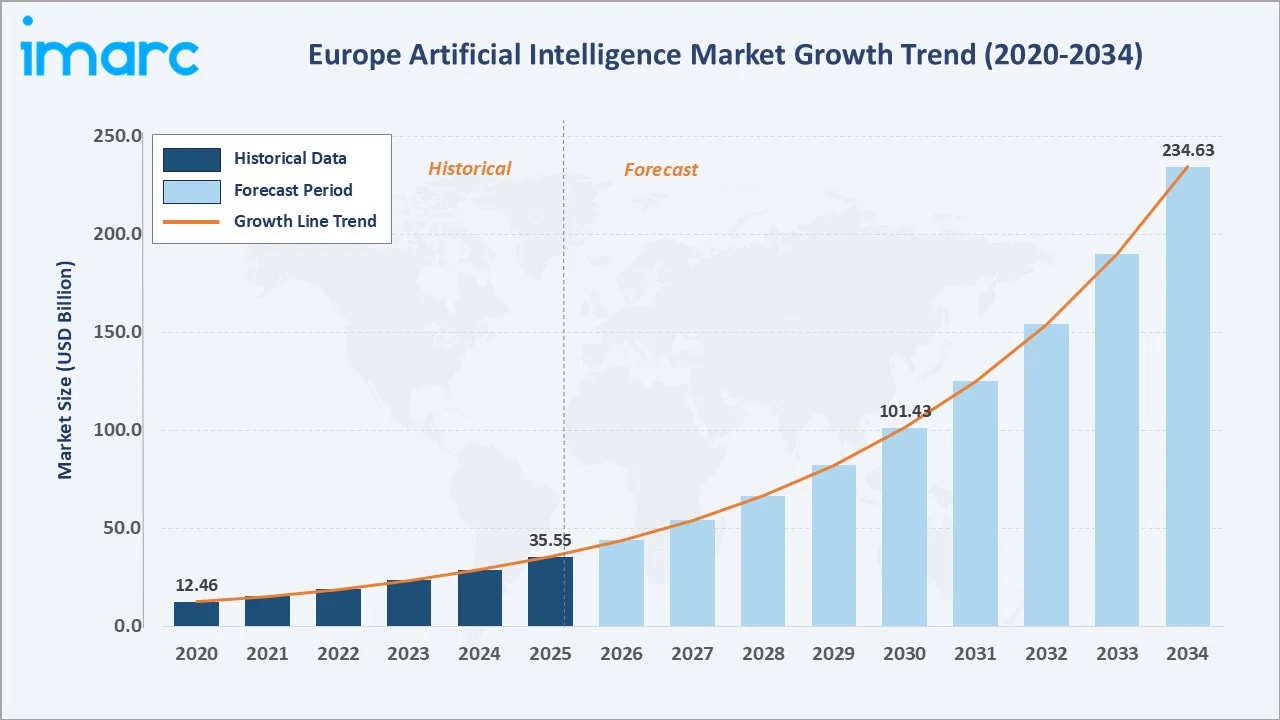

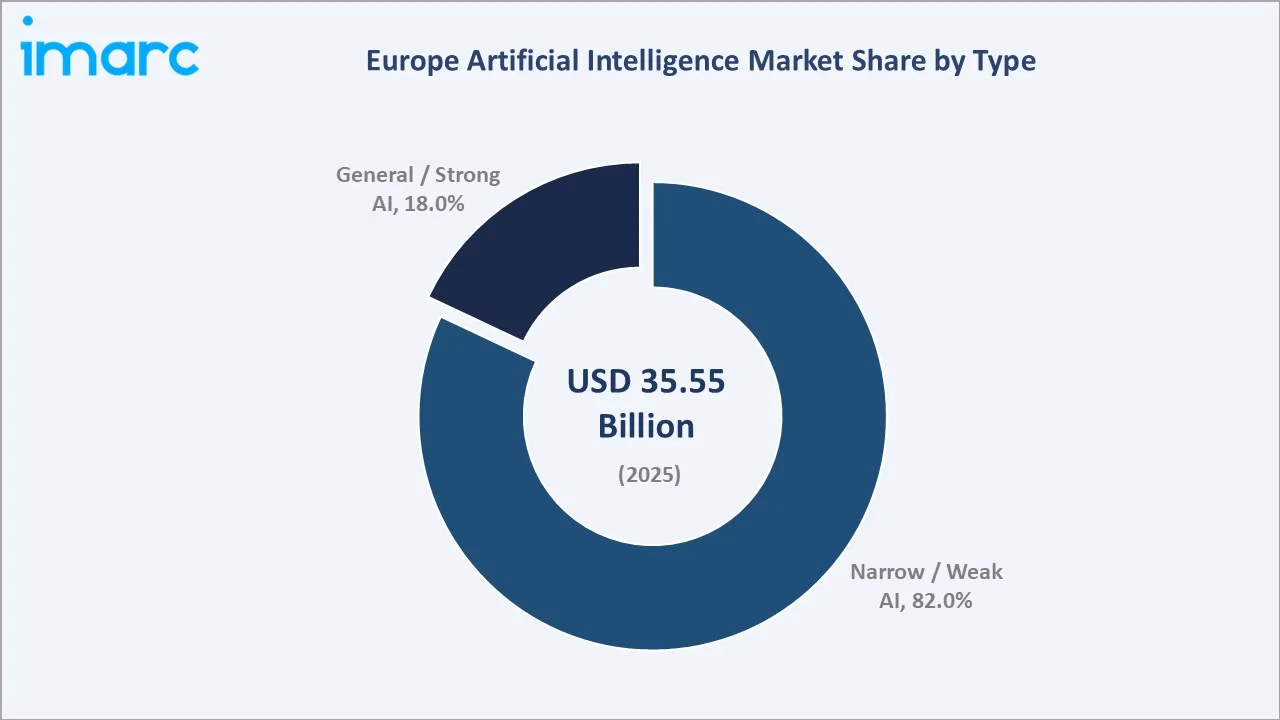

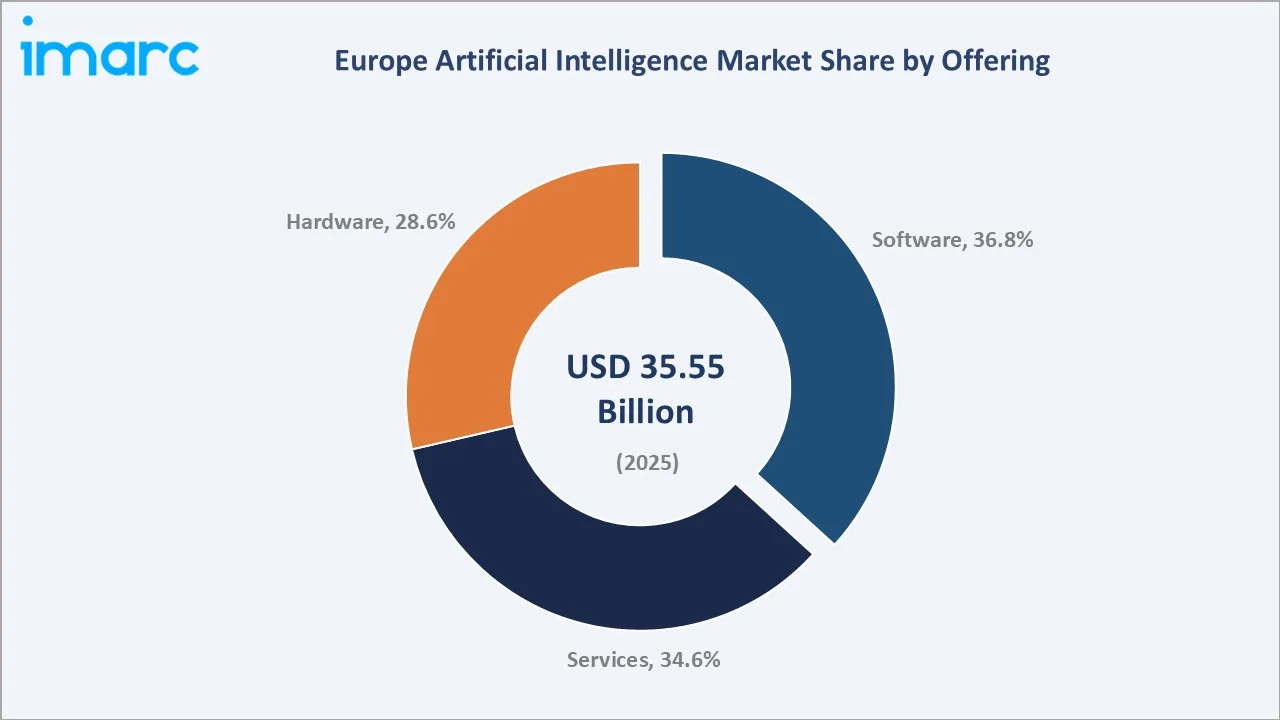

The Europe artificial intelligence market size reached USD 35.55 Billion in 2025 and is projected to reach USD 234.63 Billion by 2034, growing at a CAGR of 23.33% during 2026-2034. Rapid digital transformation across industries, increasing adoption of automation and smart technologies, and strong government support for AI research and development are key growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 35.55 Billion |

|

Forecast Market Size (2034) |

USD 234.63 Billion |

|

CAGR (2026-2034) |

23.33% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

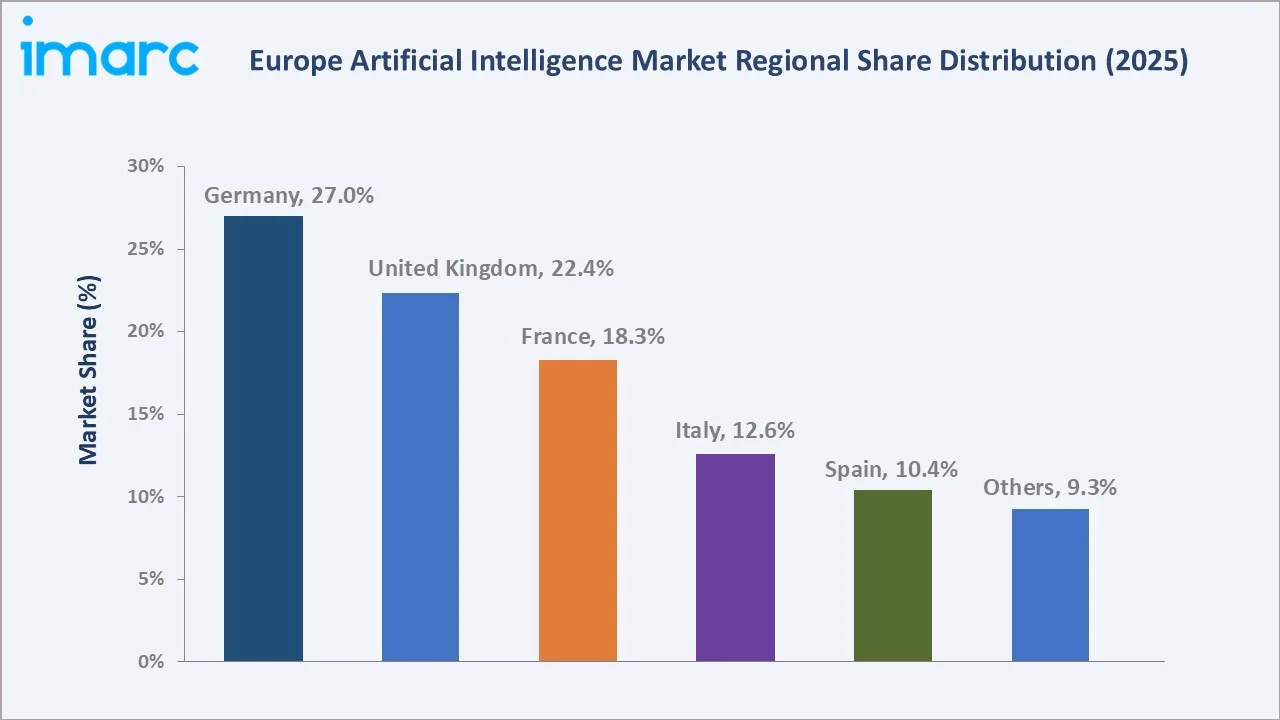

Largest Country |

Germany (27.0% share, 2025) |

|

Leading Segment (Type) |

Narrow/Weak AI – 82.0% share (2025) |

|

Leading Segment (Offering) |

Software – 36.76% share (2025) |

To get more information on this market, Request Sample

Germany leads the Europe AI market with a 27.0% country share in 2025, while narrow/weak artificial intelligence dominates the type segment at 82.0%. Software leads the offering segment at 36.76%. Europe's focus on ethical AI frameworks, strong data protection regulations, and sustained public-private R&D investments is collectively shaping the continent's AI leadership trajectory.

With applications spanning healthcare, manufacturing, financial services, automotive, and retail, the Europe AI market is expected to continue expanding, supported by the EU AI Act governance framework, generative AI proliferation, and increasing adoption of machine learning across industrial verticals.

Executive Summary

The Europe artificial intelligence market is on a sustained high-growth path, underpinned by accelerating enterprise digitalization, rising investment in AI infrastructure, and a landmark regulatory framework in the form of the EU AI Act. The market reached USD 35.55 Billion in 2025 and is forecast to surpass USD 234.63 Billion by 2034, reflecting a healthy CAGR of 23.33% over the forecast period.

Germany leads at 27.0% country share in 2025, supported by its industrial strength and R&D ecosystem, followed by the United Kingdom at 22.4% and France at 18.3%. Narrow/weak AI dominates the type segment at 82.0%, reflecting the maturity of task-specific automation, virtual assistants, and predictive analytics. Software is the leading offering at 36.76%, driven by enterprise AI platforms and machine learning tools.

Key players, including Microsoft, Google LLC, OpenAI, DeepSeek, Mistral AI, and SAP SE, continue to invest in next-generation AI capabilities aligned with European regulatory and ethical standards.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Narrow/Weak Artificial Intelligence – 82.0% share (2025) |

|

Largest Segment (Offering) |

Software – 36.76% share (2025) |

|

Leading Country |

Germany – 27.0% revenue share (2025) |

|

Second Largest Country |

United Kingdom – 22.4% (2025) |

|

2030 Market Milestone |

USD 101.43 Billion |

|

Top Companies |

Microsoft, Google LLC, OpenAI, DeepSeek, Mistral AI, and SAP SE |

Key Analytical Observations Supporting the Above Data:

- Narrow/weak AI accounts for 82.0% of the Europe AI market in 2025, reflecting widespread deployment of task-specific systems in virtual assistants, recommendation engines, fraud detection, and industrial quality inspection.

- Software leads the offering segment at 36.76% (2025), driven by rising enterprise adoption of AI platforms, MLOps tools, and large language model (LLM) APIs across healthcare, BFSI, and manufacturing verticals.

- Germany holds 27.0% of the European market in 2025, supported by deep industrial AI integration in automotive, mechanical engineering, and smart factory deployments under the Industry 4.0 paradigm.

- The United Kingdom represents 22.4% of the market, bolstered by a vibrant AI startup ecosystem in London, government AI Safety Institute investments, and strong fintech and life sciences AI adoption.

- France, at 18.3%, is emerging as a major AI innovation hub, driven by strategic investments in LLM development (Mistral AI), national AI strategies, and partnerships with leading European research institutions.

Europe Artificial Intelligence Market Overview

Artificial intelligence encompasses a broad spectrum of technologies that enable machines to simulate human cognitive functions, including perception, reasoning, learning, and decision-making. The European AI market ecosystem spans semiconductor and hardware manufacturers, cloud platform providers, AI software developers, system integrators, and end-use industry verticals ranging from healthcare diagnostics to industrial automation.

Macroeconomic factors, including rapid enterprise digitalization, cloud infrastructure scaling, and Europe's push for AI sovereignty, are primary growth catalysts. The EU AI Act, fully enforced from 2025, establishes the world's first comprehensive AI regulatory framework, creating compliance-driven demand for certified, auditable AI systems across high-risk verticals.

Market Dynamics

To evaluate market opportunities, Request Sample

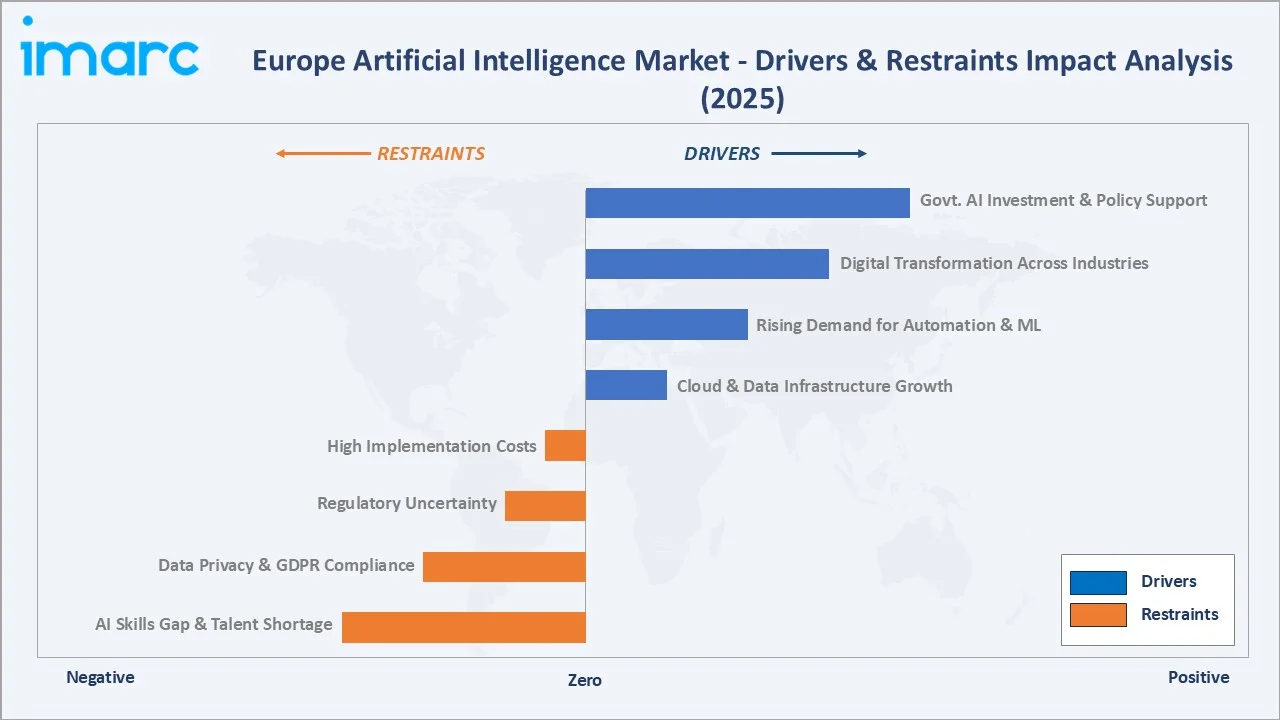

Market Drivers

- Government AI Investment & Policy Support: The European Commission’s Horizon Europe program allocated over EUR 13.6 billion to digital and AI research for 2021–2027, with member states committing an additional EUR 20 billion annually in AI public investment under the Coordinated Plan on Artificial Intelligence.

- Rapid Digital Transformation Across Industries: AI continues to be a top priority for many companies, with a growing number beginning to see tangible business outcomes from their scaled efforts. From the third quarter of 2024 to the third quarter of 2025, the percentage of companies listing AI as one of their top-three strategic priorities increased from 60% to 74%.

- Cloud & Data Infrastructure Growth: Hyperscaler investments in European data centers exceeded USD 40 billion between 2023 and 2025, with sovereign AI cloud platforms reducing latency barriers and enabling compliant large-scale AI model training under GDPR requirements.

- Rising Demand for Automation & Machine Learning: Labor shortages across European manufacturing and logistics sectors are accelerating machine learning adoption for predictive maintenance, quality control, and supply chain optimization, directly expanding the addressable market for AI platforms and services.

These drivers reinforce a self-sustaining growth cycle: regulatory clarity builds trust, which accelerates enterprise adoption, which drives platform investment, which reduces per-unit AI deployment costs, expanding accessibility to SMEs and the public sector.

Market Restraints

- Data Privacy & GDPR Compliance: Strict data protection requirements under GDPR, combined with new EU AI Act obligations for high-risk AI systems, increase compliance costs for AI vendors serving European enterprises, raising barriers to rapid model deployment.

- AI Skills Gap & Talent Shortage: While the tech workforce is expanding, with approximately 500,000 ICT specialists joining the EU labor market between 2020 and 2021, Europe currently has around 9 million ICT specialists, significantly below the EU's target of 20 million by 2030.

- High Implementation Costs: Enterprise-grade AI system deployment, including custom model training, system integration, and ongoing compliance auditing, can range from EUR 500,000 to EUR 5 million for large organizations, limiting adoption among smaller institutions.

- Regulatory Uncertainty in Emerging AI Domains: Generative AI and foundation model governance under the EU AI Act remains subject to ongoing interpretation, creating short-term uncertainty for companies developing or deploying LLMs in high-stakes applications.

Market Opportunities

- Generative AI Enterprise Adoption: Europe’s enterprise generative AI market is estimated to reach USD 18 billion by 2028, driven by demand for multilingual content generation, GDPR-compliant AI assistants, and automated knowledge workflows across BFSI, legal, and pharmaceutical sectors.

- AI for Industrial Automation & Industry 4.0: Germany’s Plattform Industrie 4.0, combined with EU-funded smart factory initiatives, positions industrial AI as a USD 30+ billion addressable segment in Europe by 2030, spanning predictive maintenance, collaborative robotics, and digital twin applications.

- Healthcare AI Expansion: EU medical AI regulations are evolving to enable certified AI diagnostics deployment, with the healthcare AI segment estimated to grow from USD 5.2 billion in 2025 to USD 28 billion by 2034, driven by radiology AI, drug discovery, and clinical decision support systems.

Market Challenges

- AI Model Transparency & Explainability: EU AI Act high-risk classification requirements mandate explainability and auditability for AI systems in healthcare, credit, and employment, necessitating significant technical investment in XAI (Explainable AI) tools that are not yet standardized across the industry.

- Cross-Border Data Flow Restrictions: Differing national AI data governance frameworks within EU member states create friction for pan-European AI platform deployments, increasing compliance overhead for companies serving multiple jurisdictions simultaneously.

Emerging Market Trends

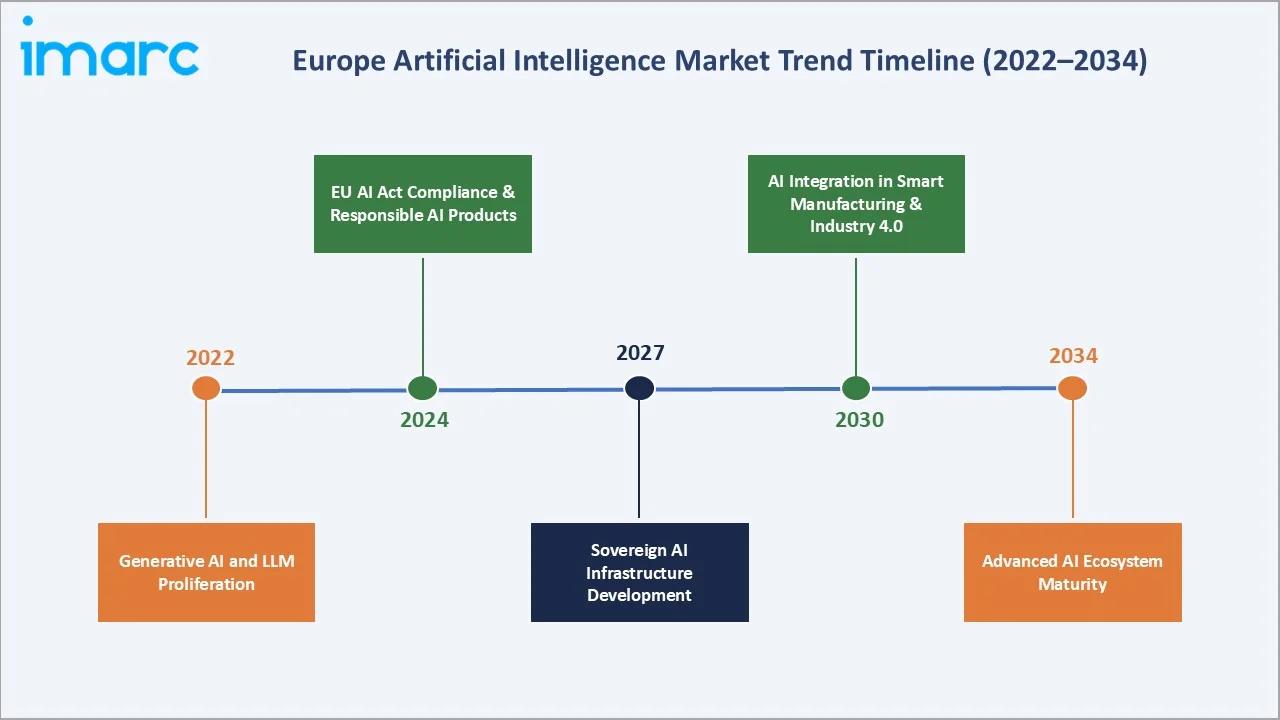

1. EU AI Act Compliance Driving Certification-Ready AI Products

The EU AI Act, the world’s first comprehensive AI law, entered enforcement in 2025, requiring conformity assessments for high-risk AI systems in healthcare, employment, and critical infrastructure. This is creating a new market for AI compliance tooling, audit services, and certified AI models, estimated at EUR 2.5 billion annually by 2027.

2. Generative AI and LLM Proliferation

European AI startups, including Mistral AI (France) and Aleph Alpha (Germany), are developing GDPR-compliant large language models in multiple European languages. Enterprise adoption of generative AI for customer service automation, code generation, and knowledge management is growing at over 35% annually, with banking and professional services leading deployments.

3. Sovereign AI Infrastructure Development

European governments are investing in sovereign AI computing infrastructure to reduce dependence on US and Chinese hyperscalers. France’s Mistral Compute platform, powered by 18,000 NVIDIA Grace Blackwell systems, and Germany’s national AI computing initiative represent a combined EUR 5+ billion investment in localized AI infrastructure between 2024 and 2026.

4. AI Integration in Smart Manufacturing and Industry 4.0

Machine vision, collaborative robotics, and AI-powered predictive maintenance are being deployed across European automotive OEMs, precision engineering, and chemical manufacturing facilities. Industry studies indicate that predictive maintenance can cut equipment downtime by up to 50% and reduce maintenance costs by 12-18%, driving strong ROI-driven procurement decisions.

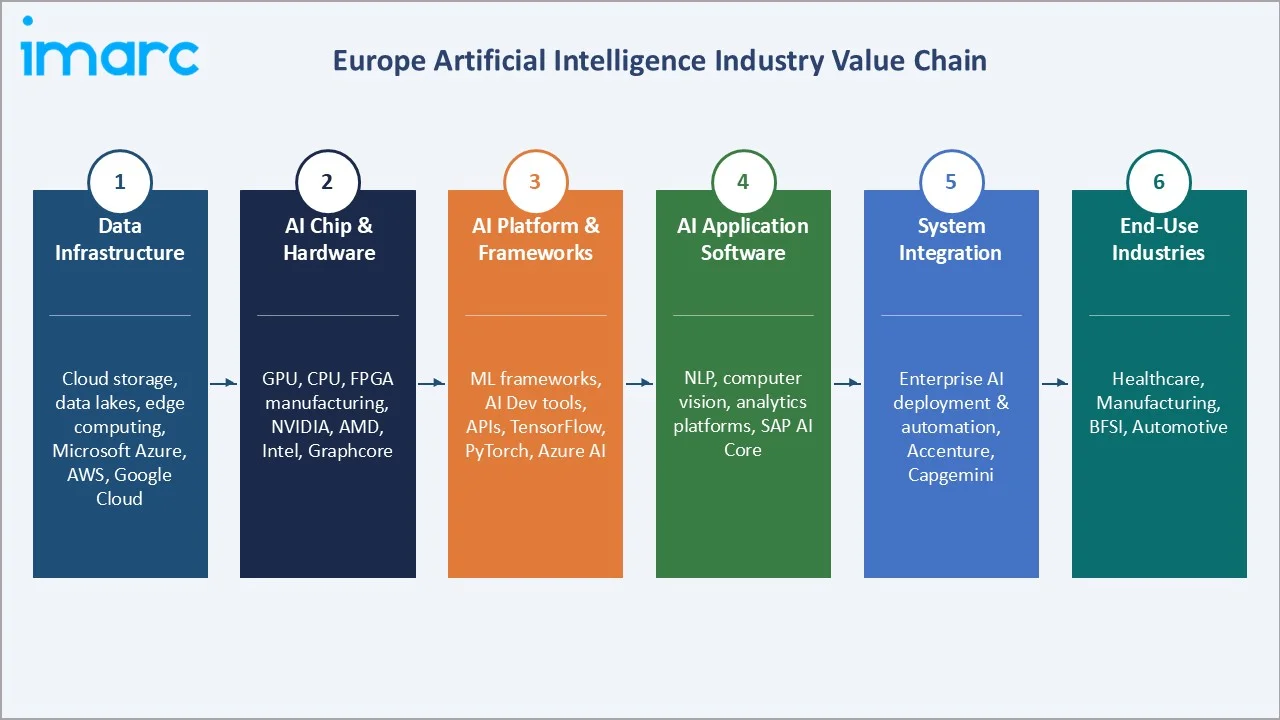

Industry Value Chain Analysis

The European AI value chain spans from semiconductor and hardware manufacturing through platform development and system integration to end-use deployment, with each stage populated by specialized operators whose capabilities directly influence product quality, compliance posture, and total cost of AI ownership.

|

Stage |

Key Activities |

Key Players / Examples |

|

Data Infrastructure |

Cloud storage, data lakes, edge computing |

Microsoft Azure, AWS, Google Cloud |

|

AI Chip & Hardware |

GPU, CPU, FPGA manufacturing for AI workloads |

NVIDIA, AMD, Intel |

|

AI Platform & Frameworks |

ML frameworks, AI development tools, APIs |

TensorFlow, PyTorch (open-source frameworks), Hugging Face |

|

AI Application Software |

NLP, computer vision, analytics platforms |

Microsoft, Google LLC, OpenAI, DeepSeek, Mistral AI, and SAP SE |

|

System Integration |

Enterprise AI deployment, customization |

Accenture, Capgemini |

|

End Users |

Healthcare, manufacturing, BFSI, automotive |

Siemens, AstraZeneca, BNP Paribas |

Technology Landscape in the Europe Artificial Intelligence Industry

Machine Learning & Deep Learning

Machine learning represents the largest technology segment at 39% of the European AI market in 2025. Deep neural network architectures, including transformer models and convolutional networks, are underpinning advances in natural language processing, computer vision, and autonomous systems across European industry verticals.

Natural Language Processing & Generative AI

NLP technologies are experiencing accelerated adoption driven by generative AI capabilities. Multilingual NLP is particularly strategic in Europe, with demand for AI systems capable of processing 24 official EU languages spanning legal, government, financial, and healthcare applications.

Computer Vision & Industrial AI

Computer vision applications in manufacturing quality inspection, autonomous vehicles (EU AV regulations framework), and medical imaging diagnostics are scaling rapidly. European medical imaging AI alone is estimated at EUR 1.2 billion in 2025, with regulatory approval pathways under the EU MDR and AI Act creating a structured market for certified diagnostic AI.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Narrow/Weak Artificial Intelligence |

82.0% |

2025 |

|

Offering |

Software |

36.76% |

2025 |

|

Technology |

Machine Learning |

39.0% |

2025 |

|

System |

Intelligence Systems |

30.0% |

2025 |

|

End Use Industry |

Manufacturing |

18.0% |

2025 |

|

Country |

Germany |

27.0% |

2025 |

By Type

To access detailed market analysis, Request Sample

Narrow/weak artificial intelligence dominates the type segment with an 82.0% share in 2025 (equivalent to approximately USD 29.15 Billion). Its dominance reflects the maturity of task-specific AI deployments across virtual assistants, recommendation systems, fraud detection engines, and industrial process automation throughout European enterprises.

General/strong artificial intelligence accounts for 18.0% of the market and represents the highest-growth sub-segment, driven by investments in foundation models, multi-modal AI systems, and AGI research by European academic institutions and technology companies.

By Offering

Software leads the offering segment with a 36.76% share in 2025, driven by rising demand for AI platforms, enterprise machine learning solutions, LLM APIs, and MLOps tools that extract actionable insights from large-scale organizational datasets. Cloud-native AI software deployment is reducing time-to-value for enterprise AI projects from months to weeks.

Services account for 34.62% (approximately USD 12.31 Billion in 2025), encompassing AI consulting, system integration, managed AI operations, and training services. The services segment is expanding as enterprises seek specialized expertise to navigate EU AI Act compliance, model governance, and large-scale AI transformation programs.

Regional Market Insights

Germany’s market leadership (27.0%, 2025) reflects decades of industrial R&D investment, a world-class engineering ecosystem, and deep integration of AI in automotive, mechanical engineering, and chemical manufacturing. The German AI strategy commits EUR 5 billion to AI research through 2025, with the DFKI (German Research Center for Artificial Intelligence) coordinating one of the world’s largest applied AI research programs.

|

Country |

Share (2025) |

Key Growth Drivers |

Major Focus Areas |

|

Germany |

27.0% |

Industry 4.0, automotive AI, smart manufacturing |

Industrial AI, autonomous vehicles |

|

United Kingdom |

22.4% |

Fintech AI, life sciences, AI Safety Institute |

BFSI, healthcare, defence AI |

|

France |

18.3% |

LLM development (Mistral), national AI plan |

Generative AI, defence, energy |

|

Italy |

12.6% |

Manufacturing AI, agri-tech, SME digitalization |

Smart manufacturing, agriculture |

|

Spain |

10.4% |

Tourism AI, smart cities, renewable energy AI |

Smart cities, green AI, logistics |

|

Others |

9.3% |

Nordic AI hubs (Sweden, Netherlands), CEE growth |

Cleantech AI, public sector AI |

The United Kingdom, holding 22.4% of the European AI market in 2025, benefits from a world-leading AI research ecosystem anchored by Oxford, Cambridge, and DeepMind’s London headquarters. The UK’s post-Brexit ‘pro-innovation’ AI regulatory approach contrasts with the EU’s prescriptive AI Act framework, enabling faster deployment of AI in financial services, defense, and biomedical research.

Competitive Landscape

The Europe artificial intelligence market exhibits a moderately concentrated structure at the platform and software layer, with global technology giants commanding significant share, while a vibrant ecosystem of European AI startups and mid-tier specialists competes across vertical-specific applications. The top players collectively hold an estimated 45–52% of total European AI software and services revenue in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Microsoft |

Microsoft Copilot; Azure AI; GitHub Copilot |

Market Leader |

Azure AI, Copilot, OpenAI partnership, enterprise AI dominance |

|

Google LLC |

Gemini; Vertex AI; Google AI Studio |

Market Leader |

Vertex AI, Gemini models, DeepMind research, cloud AI platform |

|

OpenAI |

ChatGPT; GPT-5; OpenAI API |

Strong Challenger |

ChatGPT, GPT-4o API adoption across European enterprises |

|

DeepSeek |

DeepSeek; DeepSeek-R1; DeepSeek-V3.1/V3.2 |

Challenger |

Open-weight LLMs (DeepSeek-V3), cost-competitive AI models |

|

Mistral AI |

Le Chat; Mistral Large |

European Leader |

GDPR-compliant LLMs, multilingual models, sovereign AI focus |

|

SAP SE |

SAP Business AI; Joule; SAP AI Core |

Enterprise Specialist |

SAP AI Core, Joule AI copilot, ERP-embedded AI solutions |

Key Company Profiles

Microsoft

Microsoft, headquartered in Redmond, USA, is the dominant AI vendor in the European market through its Azure OpenAI Service, Microsoft Copilot suite, and strategic EUR 3.2 billion investment in German AI infrastructure (2024). The company’s deep integration of AI across Azure, Office 365, and Dynamics 365 gives it unparalleled enterprise market penetration.

- Product Portfolio: Azure AI, Microsoft Copilot (M365, GitHub, Dynamics), Azure OpenAI Service, Azure Machine Learning.

- Recent Developments: Announced EUR 3.2 billion investment in German AI infrastructure (2024); expanded Azure AI compliance certifications for EU AI Act high-risk system categories.

- Strategic Focus: Enterprise AI platform leadership; EU AI Act compliance tooling; sovereign cloud expansion across Germany, France, and Spain.

Google LLC

Google, through its Google Cloud and DeepMind divisions, represents one of the largest AI research and platform players in Europe. DeepMind’s London headquarters serves as a global AI research hub, with breakthroughs in protein folding (AlphaFold), healthcare AI, and scientific AI directly relevant to European industrial and academic use cases.

- Product Portfolio: Google Vertex AI, Gemini models, DeepMind AlphaFold, Google Workspace AI features.

- Recent Developments: Launched Gemini 2.5 Pro and Gemini 3.

- Strategic Focus: AI research leadership via DeepMind; enterprise cloud AI platform growth; responsible AI compliance with EU regulatory frameworks.

OpenAI

OpenAI’s ChatGPT and GPT-4o models have achieved widespread enterprise adoption across European markets since 2023. The company’s API platform is embedded in thousands of European software products, SaaS applications, and enterprise AI workflows, making it one of the most widely deployed AI infrastructure layers in the region.

- Product Portfolio: ChatGPT Enterprise, GPT-4o API, Sora (video generation), DALL-E image generation.

- Recent Developments: Opened first EU data residency option in 2025 to support GDPR compliance.

- Strategic Focus: Enterprise API monetization; GDPR-compliant deployment infrastructure; expanding European partner ecosystem.

Market Concentration Analysis

The European AI market exhibits moderate concentration at the platform layer, with global technology giants holding approximately 45–52% of software and services revenue, while a long tail of 2,000+ European AI startups and SMEs commands the remainder across vertical-specific applications. Horizon Europe and Digital Europe programs will invest EUR 1 billion annually in AI and the European Innovation Council investments are actively nurturing homegrown European AI companies to reduce strategic dependency on non-European AI platforms.

Consolidation activity is accelerating, driven by AI Act compliance costs, GPU infrastructure investment requirements, and the need for certified AI model portfolios. Between 2022 and 2025, over 40 significant M&A transactions reshaped the European AI competitive landscape, with particular activity in healthcare AI, fintech AI, and industrial automation verticals.

Investment & Growth Opportunities

Fastest Growing Segments

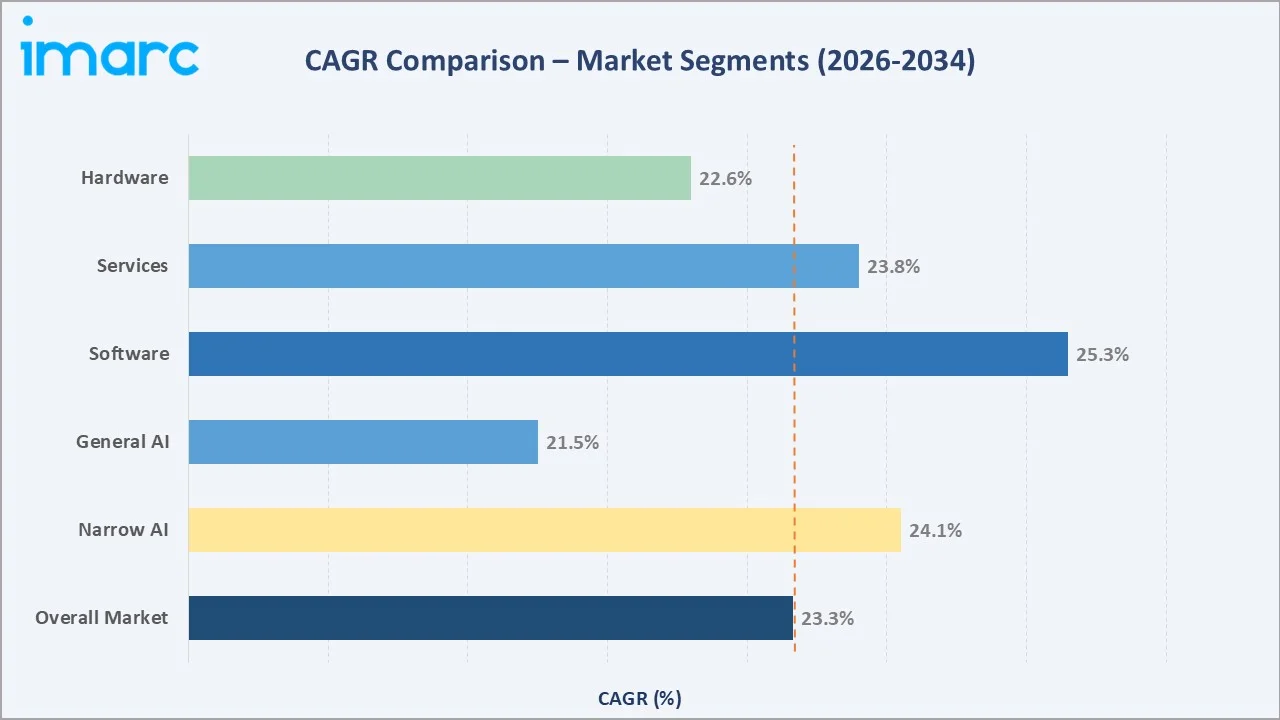

Generative AI enterprise applications (estimated CAGR 35%+), industrial AI for smart manufacturing (CAGR 28%), and healthcare AI diagnostics (CAGR 30%) represent the three highest-growth investment vectors through 2034. Together, these segments address a total addressable market of approximately USD 85 billion within the European AI landscape by 2030.

Emerging Country Markets

Poland, the Netherlands, Sweden, and the Nordics collectively represent an incremental USD 12 billion AI opportunity by 2034. Entry via partnerships with local system integrators, EU structural fund co-investments, and alignment with national AI strategies are the preferred investment modalities for international AI vendors.

Venture and Institutional Investment Trends

- European AI companies raised more than $13 billion in 2024, reflecting a 22% increase in capital investment, with generative AI, healthcare AI, and industrial AI attracting the largest funding rounds.

- Sovereign wealth funds and national development banks (EIB, KfW, Bpifrance) are increasing direct AI infrastructure investments to USD 8+ billion annually across Europe.

- Key investment themes include GDPR-compliant AI data platforms, edge AI for industrial IoT, and AI governance and compliance tooling as the EU AI Act creates a new compliance market.

Future Market Outlook (2026-2034)

The European artificial intelligence market is positioned for robust, broad-based growth through 2034. From a base of USD 35.55 Billion in 2025, the market is projected to reach USD 234.63 Billion by 2034, representing total incremental value creation of USD 199.08 Billion over the forecast decade.

Regulatory evolution, particularly full EU AI Act enforcement, GDPR AI guidance, and national AI sector strategies, will drive significant product certification investment. AI vendors achieving EU AI Act conformity assessments and GDPR-compliant deployment architectures by 2026 are positioned to capture a disproportionate share of institutional and public sector procurement budgets across Europe.

Long-term, the European AI market’s trajectory is tied to three structural macro-themes: the continent’s drive for digital and AI sovereignty (reducing dependence on non-European AI infrastructure), the green energy transition (accelerating demand for AI-optimized energy management and climate modeling), and Europe’s demographic challenges (driving AI-powered productivity enhancement in manufacturing, healthcare, and professional services).

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 180 industry participants in 2024–2025, including AI platform vendors, enterprise AI procurement officers, system integrators, regulatory experts, and end consumers across Germany, the UK, France, and other major European markets.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, EU Commission regulatory documents, national AI strategy papers, industry databases, trade publications, and publicly available financial data. Over 320 secondary sources were reviewed and triangulated, including European AI Office publications, OECD AI policy observatory data, and market intelligence from Statista, IDC, and Gartner.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating macroeconomic indicators, enterprise IT spending indices, AI patent activity, and historical market evolution. A base-case CAGR of 23.33% reflects consensus analyst estimates validated against reported AI vendor revenue growth rates and EU digital economy investment data.

Europe Artificial Intelligence Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Segment Coverage |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Type Covered | Narrow/Weak Artificial Intelligence, General/Strong Artificial Intelligence |

| Offering Covered | Hardware, Software, Services |

| Technology covered | Machine Learning, Natural Language Processing ,Context-Aware Computing, Computer Vision, Others |

| System Covered | Intelligence Systems, Decision Support Processing, Hybrid Systems, Fuzzy Systems |

| End-Use Industry covered | Healthcare, Manufacturing, Automotive, Agriculture, Retail, Security, Human Resources, Marketing, Financial Services, Transportation and Logistics, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Microsoft, Google LLC, OpenAI , DeepSeek, Mistral AI, SAP SE, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Artificial Intelligence Market Report

The Europe artificial intelligence market reached USD 35.55 Billion in 2025. It is projected to reach USD 234.63 Billion by 2034.

The Europe AI market is expected to grow at a CAGR of 23.33% during the forecast period from 2026-2034, supported by consistent demand from enterprise AI software, services, and hardware across all major European economies.

Germany leads the market with a 27.0% country revenue share in 2025, driven by its industrial AI adoption, strong R&D ecosystem, and government investment in AI through the national AI strategy and Horizon Europe programs.

Narrow/weak artificial intelligence dominates the type segment with an 82.0% share in 2025, valued at approximately USD 29.15 Billion. Its dominance is driven by widespread deployment of task-specific AI systems in virtual assistants, recommendation engines, fraud detection, and industrial automation.

The software segment holds the largest offering share at 36.76% in 2025 (approximately USD 13.07 Billion), driven by rising enterprise adoption of AI platforms, ML tools, LLM APIs, and cloud-native AI application software across all major European verticals.

Key players include Microsoft, Google LLC, OpenAI, DeepSeek, Mistral AI, and SAP SE, among others, operating across the AI platform, application software, and hardware layers.

The EU AI Act, fully enforced from 2025, is creating a new compliance market for certified AI systems, audit tooling, and conformity assessment services. While it increases short-term compliance costs, it is expected to strengthen enterprise trust in AI deployments and create sustainable demand for regulation-ready AI products.

Key challenges include GDPR and EU AI Act compliance complexity, the AI talent shortage (estimated 500,000 professional shortfall in 2025), high implementation costs for enterprise AI systems, and cross-border data flow restrictions across EU member states.

Highest-growth investment opportunities include generative AI enterprise applications, industrial AI for Industry 4.0 and smart manufacturing, healthcare AI diagnostics and drug discovery, sovereign AI infrastructure development, and EU AI Act compliance tooling and audit services across the EUR 200+ billion European AI market opportunity by 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade