Europe Bottled Water Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, Packaging Type, and Country, 2026-2034

Europe Bottled Water Market Size, Share, Trends & Forecast (2026-2034)

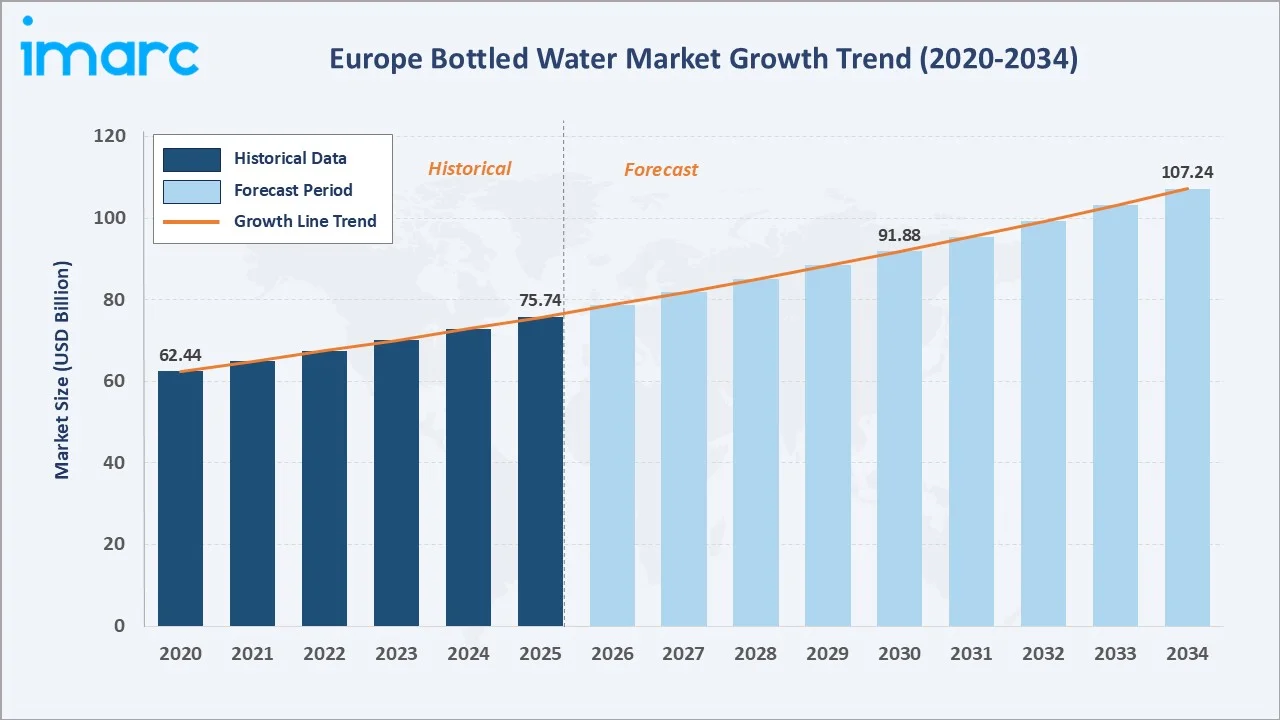

The Europe bottled water market reached USD 75.74 Billion in 2025 and is projected to reach USD 107.24 Billion by 2034, growing at a CAGR of 3.94% during 2026-2034. Surging health consciousness, rising preference for convenient on-the-go hydration, robust tourism and hospitality activity, and a broad shift from sugary carbonated soft drinks toward healthier water alternatives are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 75.74 Billion |

|

Forecast Market Size (2034) |

USD 107.24 Billion |

|

CAGR (2026-2034) |

3.94% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

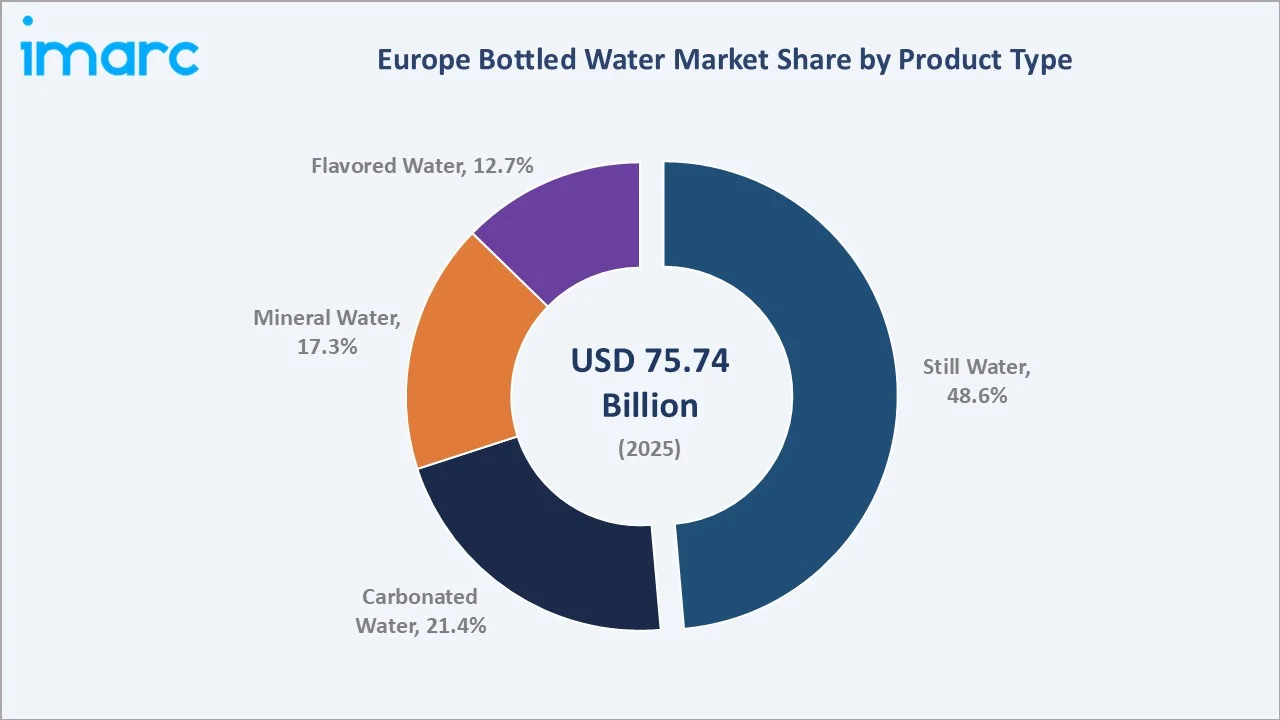

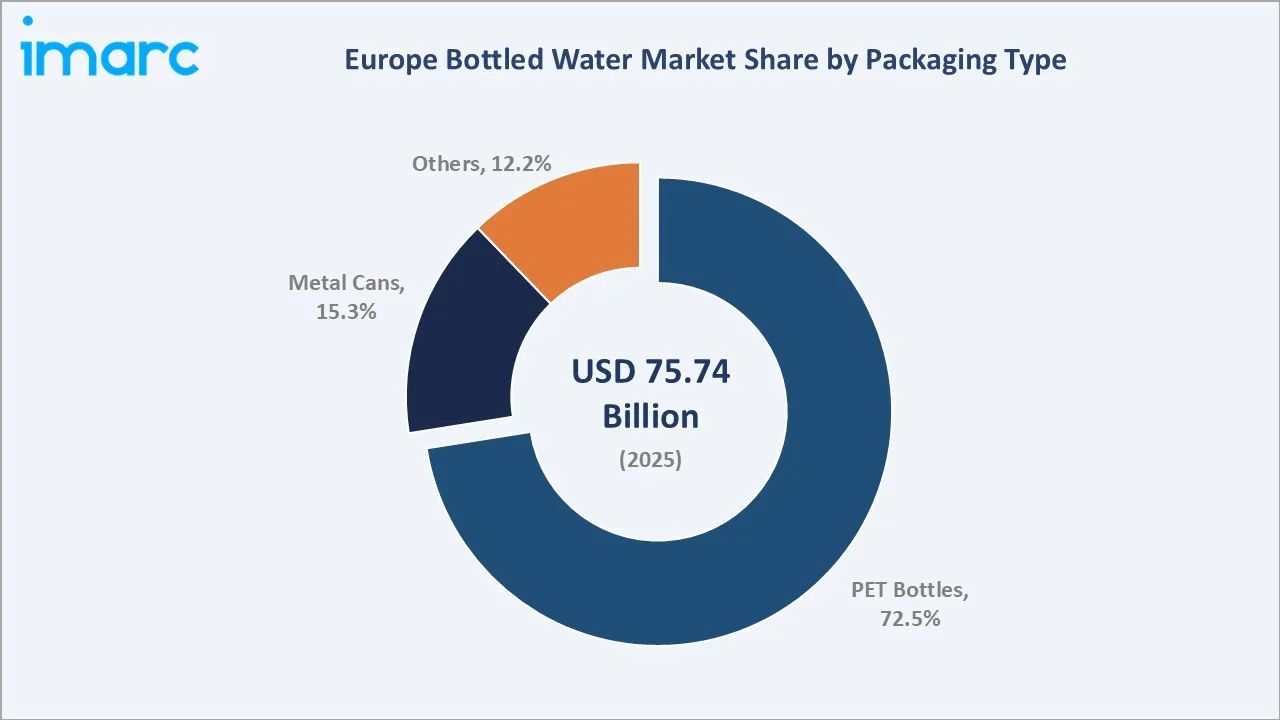

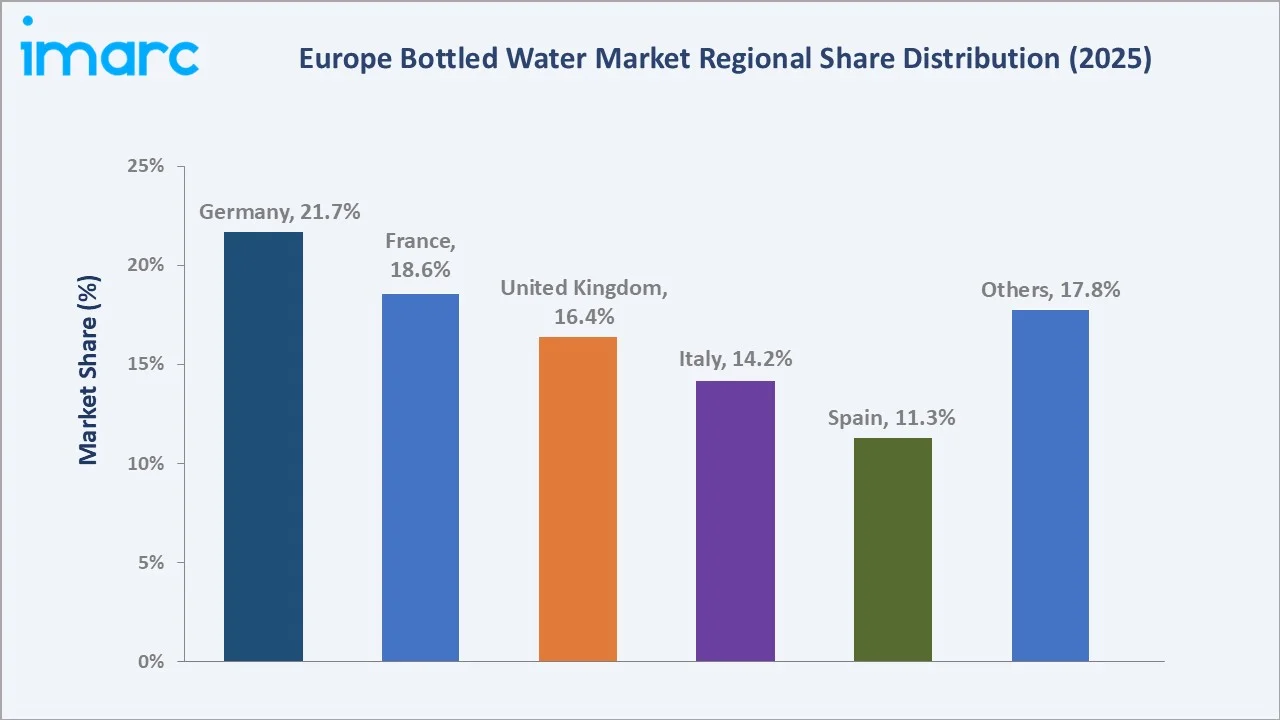

Still water commands the largest product share at 48.6% in 2025, while PET bottles account for 72.5% of total packaging volume. Germany leads regionally with a 21.7% market share, underpinned by one of Europe's highest per-capita bottled water consumption rates.

To get more information on this market, Request Sample

Europe's bottled water market is underpinned by three structural forces: a continent-wide pivot toward healthier hydration, EU regulatory frameworks compelling sustainable packaging transitions, and the progressive premiumization of the category through functional, flavored, and origin-certified water products.

Executive Summary

The Europe bottled water market is experiencing steady, broad-based expansion, driven by health-and-wellness megatrends, an active tourism sector, and accelerating eco-packaging innovation. The market was valued at USD 75.74 Billion in 2025 and is forecast to reach USD 107.24 Billion by 2034, growing at a CAGR of 3.94%. This trajectory is underpinned by Europe's rising consumer preference for premium water options, regulatory mandates on recyclable packaging, and the expanding presence of functional and flavored water in mainstream retail.

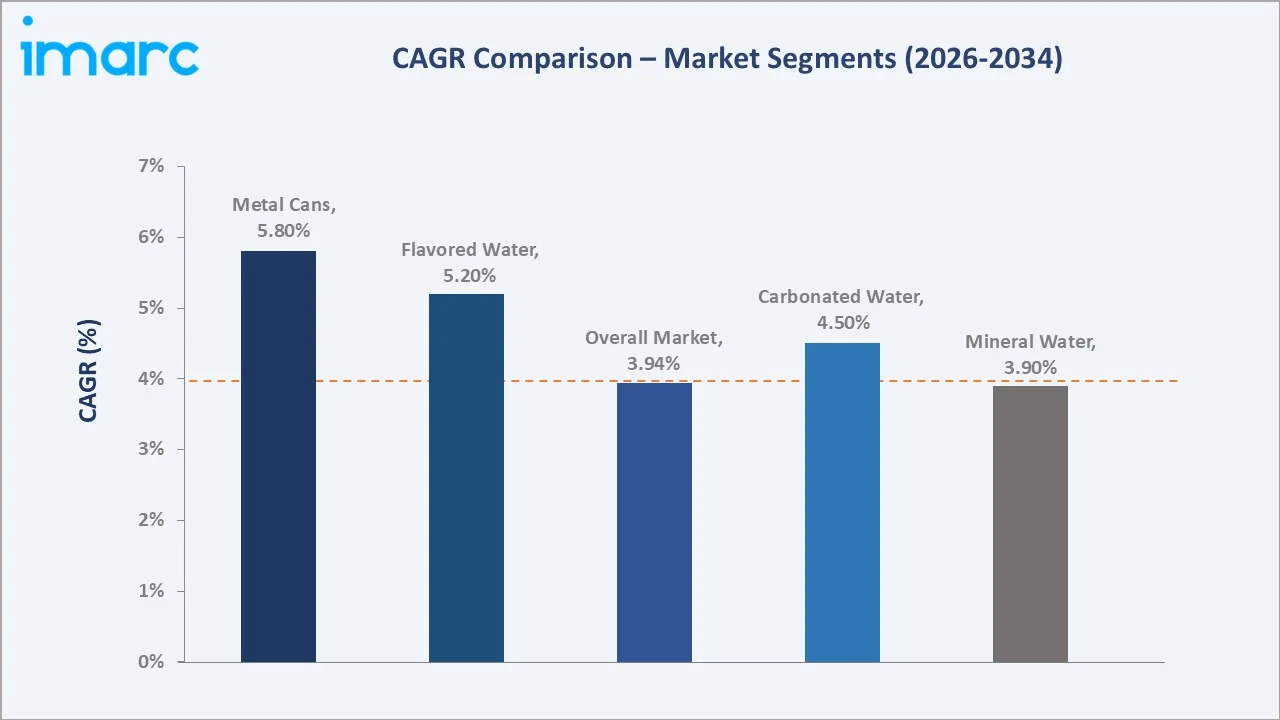

Still water commands the largest product share at 48.6% in 2025. Carbonated water holds 21.4%, mineral water accounts for 17.3%, and flavored water at 12.7% is the fastest-growing sub-segment. On the packaging front, PET bottles lead at 72.5%, while metal cans at 15.3% are growing fastest at ~5.8% CAGR, driven by sustainability mandates and premium brand adoption. Germany leads the regional landscape at 21.7%, followed by France at 18.6% and the United Kingdom at 16.4%. Danone, The Coca-Cola Company, PepsiCo, Gerolsteiner Brunnen GmbH & Co. KG, and Spadel Group collectively hold over 60% of market revenue.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Still Water – 48.6% share (2025) |

|

Fastest Growing Type |

Flavored Water (~5.2% CAGR, 2026-2034) |

|

Largest Packaging |

PET Bottles – 72.5% share (2025) |

|

Fastest Growing Pkg |

Metal Cans (~5.8% CAGR, 2026-2034) |

|

Leading Country |

Germany – 21.7% share (2025) |

|

Top Companies |

Danone, The Coca-Cola Company, PepsiCo, Gerolsteiner Brunnen GmbH & Co. KG, and Spadel Group |

Key Analytical Observations Supporting the Above Data:

- Still water at 48.6% in 2025 dominates due to broad demographic appeal and strong private-label penetration across retail. Its dominance reflects everyday hydration demand and the widest price-tier coverage from economy to premium.

- Flavored water at 12.7% (2025) is growing fastest as younger European consumers seek low-calorie, taste-differentiated alternatives. Natural fruit extracts and herbal infusions are resonating strongly with Gen Z and millennial shoppers across the UK, France, and Germany.

- PET bottles at 72.5% (2025) remain the format of choice due to recyclability, lightweight logistics, and evolving compliance with EU rPET mandates (30% recycled content target by 2030). The transition to rPET is also neutralizing sustainability criticism.

- Germany at 21.7% (2025) reflects its uniquely high per-capita consumption (~147 L/year), deep-rooted sparkling water culture, and strong brand loyalty to domestic mineral water brands including Gerolsteiner.

Europe Bottled Water Market Overview

Bottled water encompasses all commercially sealed purified, mineral, spring, carbonated, and flavored water products packaged for direct consumer use. The European market spans a diverse product ecosystem, from premium Alpine mineral waters to private-label still water in rPET bottles, serving retail, foodservice, on-trade hospitality, and direct-to-consumer channels.

Europe's bottled water landscape is defined by an exceptionally quality-aware consumer base, stringent EU regulatory oversight, and an embedded premium water culture in Germany, France, and Italy. At USD 75.74 Billion in 2025, the market reflects both mature Western European volume markets and rapidly emerging Eastern European growth hubs.

Macroeconomic drivers include Europe's sustained tourism recovery (international arrivals across Europe exceeded 793 million in 2025), EU packaging legislation mandating 30% recycled content in PET bottles by 2030, and growing consumer willingness to pay premiums for sustainable or health-enhanced water products.

The revised EU Drinking Water Directive (EU) 2020/2184 reinforces consumer confidence in bottled water quality, while the EU's packaging waste reduction roadmap (5% by 2030, 10% by 2035, 15% by 2040) is reshaping production economics across the bottling value chain. The Europe bottled water market size is projected to grow from USD 75.74 Billion in 2025 to USD 91.88 Billion in 2030, and USD 107.24 Billion by 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

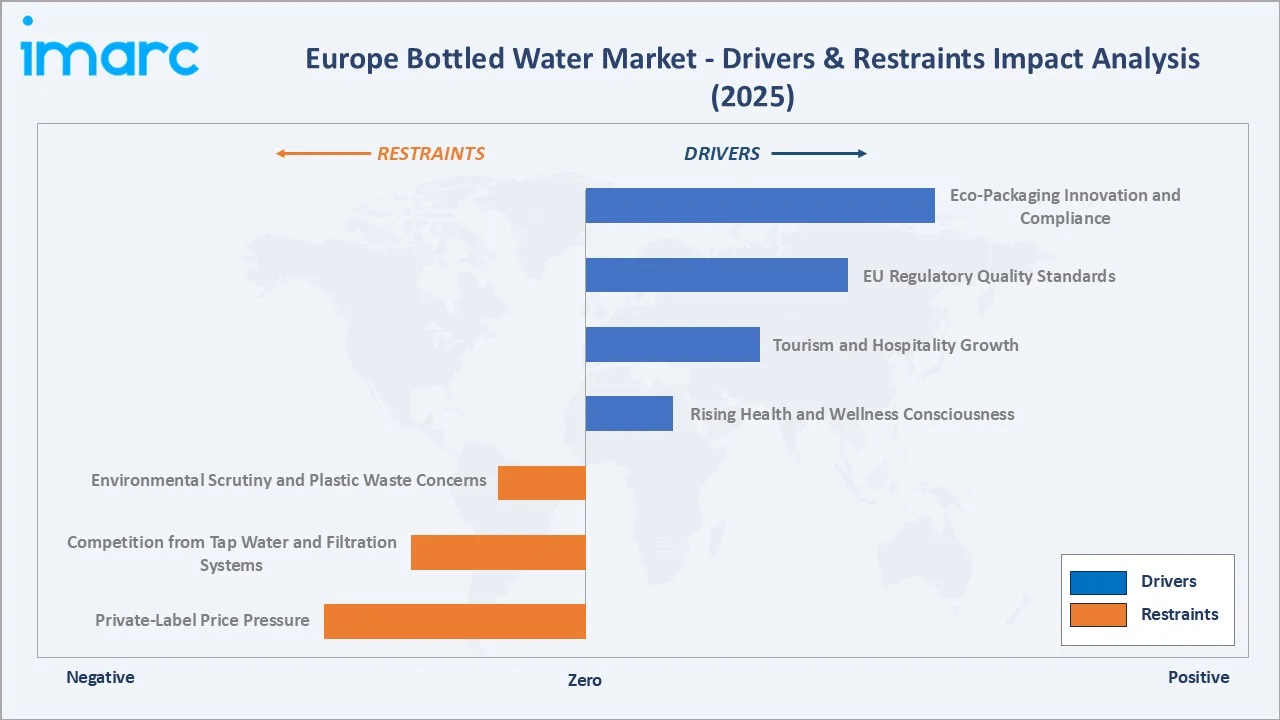

Market Drivers

- Rising Health and Wellness Consciousness: European consumers are increasingly replacing sugary carbonated beverages with bottled water. A recent study indicated 40% of European consumers actively reduced sugar intake, directly boosting bottled water demand across Germany, France, and the UK.

- Tourism and Hospitality Growth: Europe hosted over 793 million international arrivals in 2025. Countries including Spain, France, and Italy rank among the world's top global tourism destinations, sustaining high-volume hospitality channel demand particularly in premium mineral and carbonated water categories.

- EU Regulatory Quality Standards: The European Union's revised Drinking Water Directive (EU) 2020/2184 mandates bottled water meet standards exceeding those for tap water. This regulatory framework sustains consumer trust, reinforces brand premiumization, and maintains a strong credibility moat against substitutes.

- Eco-Packaging Innovation and Compliance: EU regulations targeting 90% PET bottle collection rates by 2029 and mandatory 30% recycled content by 2030 are accelerating rPET investment. Brands including Evian and Volvic have already committed to 100% rPET, strengthening brand loyalty and driving compliance-led demand across the supply chain.

Market Restraints

- Environmental Scrutiny and Plastic Waste Concerns: Growing consumer awareness about single-use plastic pollution is generating reputational pressure for PET-dominant brands. NGO campaigns and media coverage on plastic leaching and ocean pollution are influencing purchase behavior, particularly among eco-conscious younger consumers.

- Competition from Tap Water and Filtration Systems: In Northern Europe, the Netherlands, Germany, and Nordic countries, high-quality municipal tap water directly substitutes for bottled water consumption. Premium home filtration brands (Brita, TAPP Water) further erode addressable bottled water volume in price-sensitive segments.

- Private-Label Price Pressure: Major European retailers (Lidl, Aldi, Carrefour, Tesco) have aggressively expanded private-label bottled water ranges undercutting branded products by 30–50%. This price competition compresses margins in the mass-market still water segment.

Market Opportunities

- Premiumization and Functional Water Innovation: Consumer demand for vitamin-enriched, electrolyte-infused, alkaline, and hydrogen-enriched water is creating a high-value growth segment. EFSA regulatory approvals for novel functional water ingredients are enabling brands to target specific wellness outcomes, driving flavored water toward ~5.2% CAGR through 2034.

- Eastern Europe Greenfield Expansion: Poland, Czech Republic, Hungary, and Romania represent the fastest-growing sub-markets within Europe, driven by rising disposable incomes, modernizing retail infrastructure, and increasing aspirational demand for premium international water brands. Poland alone is projected to grow at a CAGR exceeding 7% through 2034.

Market Challenges

- Water Source Stress and Regulatory Risk: Climate change is reducing natural spring water availability in Southern Europe, particularly in Italy and Spain. Growing regulatory scrutiny over water extraction rights and aquifer depletion is creating supply-side uncertainty for source-dependent premium mineral water brands.

- Supply Chain and Input Cost Volatility: PET resin price fluctuations driven by crude oil market dynamics, combined with aluminum commodity price volatility for can-format growth, create ongoing cost management challenges for bottlers operating on thin retail margins in a competitive landscape.

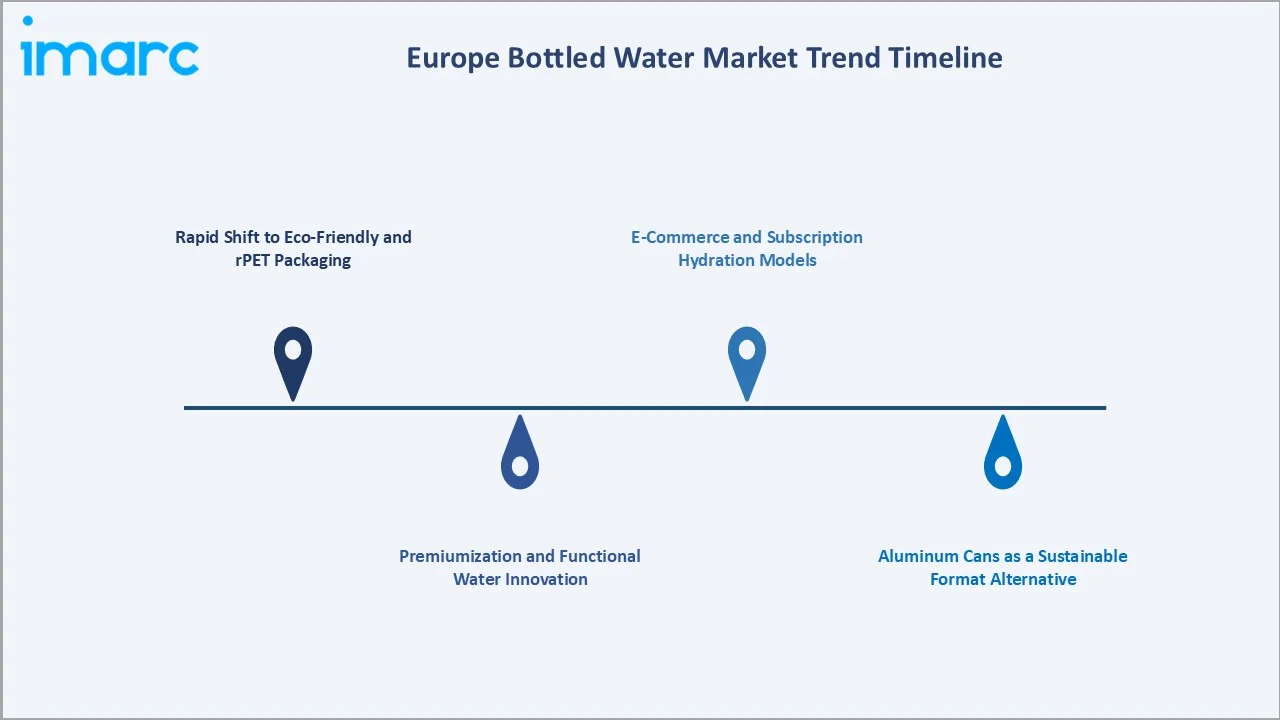

Emerging Market Trends

1. Rapid Shift to Eco-Friendly and rPET Packaging

Nestlé’s Valvert brand in Belgium launched a 100% recycled PET water bottle, marking Nestlé’s first such initiative in Europe. The move supports bottle-to-bottle circularity and aligns with Nestlé’s goal to raise rPET content in water bottles globally. EU Packaging Regulation (2022/0396/COD), effective from 2030, mandates 30% recycled content in PET bottles, a threshold brands including Evian (Danone) and Volvic have already exceeded.

2. Premiumization and Functional Water Innovation

EFSA regulatory approvals for functional water ingredients (including glucosyl hesperidin) are enabling brands to target specific wellness outcomes, immunity support, cognitive performance, and hydration optimization, driving flavored water toward ~5.2% CAGR through 2034. Premium positioning strategies leveraging geographical origin storytelling command 15–25% price premiums over commodity-tier products.

3. Aluminum Cans as a Sustainable Format Alternative

In November 2025, Ball Corporation signed an eight-figure, five-year agreement to supply millions of aluminum bottles to Re:Water, supporting the brand’s expansion across UK retail, catering, and hospitality. Metal cans are projected to grow at ~5.8% CAGR through 2034, making them the fastest-growing packaging format in the European bottled water market.

4. E-Commerce and Subscription Hydration Models

European e-commerce channels for bottled water grew at an estimated 12% year-on-year in 2024, as subscription hydration services gained traction among urban professionals. Direct-to-consumer (DTC) models are enabling smaller artisanal brands, including Welsh spring water and Scandinavian glacier water, to access pan-European audiences without traditional retail intermediaries.

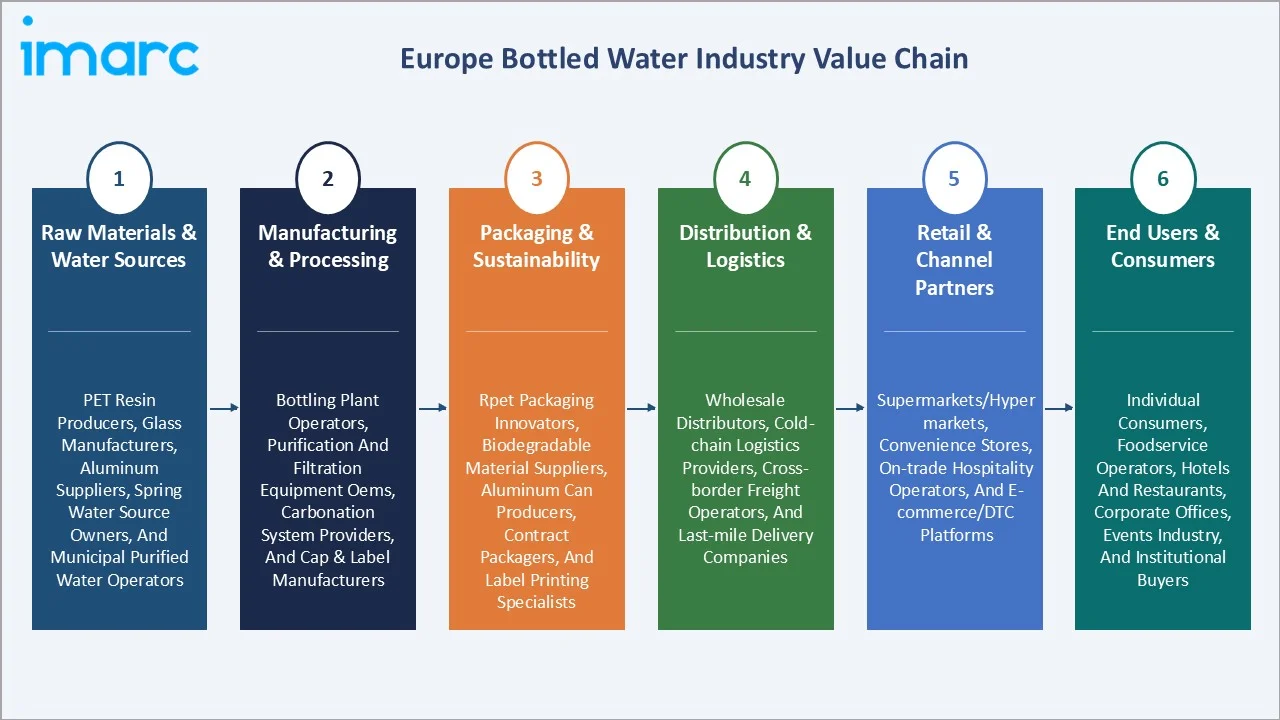

Industry Value Chain Analysis

Europe's bottled water value chain spans from natural water source extraction and raw material supply through to end-consumer hydration, with each stage occupied by specialized manufacturers, packaging innovators, and distribution operators whose performance directly influences product quality, sustainability compliance, and market pricing.

|

Stage |

Key Players / Examples |

|

Raw Materials & Water Sources |

PET resin producers, glass manufacturers, aluminum suppliers, spring water source owners, and municipal purified water operators. |

|

Manufacturing & Processing |

Bottling plant operators, purification & filtration equipment OEMs, carbonation system providers, and cap & label manufacturers. |

|

Packaging & Sustainability |

rPET packaging innovators, biodegradable material suppliers, aluminum can producers, contract packagers, and label printing specialists. |

|

Distribution & Logistics |

Wholesale distributors, cold-chain logistics providers, cross-border freight operators, and last-mile delivery companies. |

|

Retail & Channel Partners |

Supermarkets/hypermarkets, convenience stores, on-trade hospitality operators, and e-commerce/DTC platforms. |

|

End Users & Consumers |

Individual consumers, foodservice operators, hotels and restaurants, corporate offices, events industry, and institutional buyers. |

Technology Landscape in the Europe Bottled Water Industry

rPET and Recycled Material Bottling

Recycled PET (rPET) bottling technology is the defining technological transition in the European bottled water industry. Advanced rPET processing systems from companies including SIPA, Husky, and Sidel can produce bottles with up to 100% post-consumer recycled content while meeting EU food-contact safety standards. Food-grade rPET production capacity in Europe has expanded by an estimated 35% between 2022 and 2025, driven by brand commitments and regulatory mandates.

Functional Water and Ingredient Technology

Advanced functional water formulations are leveraging food-science innovations to deliver measurable health benefits. Electrolyte-enhanced waters use mineral blending technologies to precisely calibrate sodium, potassium, and magnesium ratios. Alkaline water production employs electrolysis systems to achieve pH 8–9.5. EFSA's regulatory framework for novel food ingredients is enabling ingredient suppliers to introduce scientifically validated health-functional components into bottled water.

Aluminum Can and Sustainable Packaging Innovation

Slim aluminum can formats (250 ml–500 ml) are being developed specifically for the premium on-trade water segment, where aesthetics and sustainability credentials jointly influence procurement decisions. Can body weight reduction (downgauging) technology has reduced aluminum material use per can by approximately 12–15% since 2020, cutting both material costs and embedded carbon.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Still Water |

48.6% |

2025 |

|

Packaging Type |

PET Bottles |

72.5% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Country |

Germany |

21.7% |

2025 |

By Product Type

Still water dominates with a 48.6% share in 2025. This segment encompasses all non-carbonated, non-flavored purified, spring, and mineral water products across all packaging formats. Its dominance reflects universal everyday hydration appeal, broad accessibility across price tiers from economy private-label to premium Alpine mineral water, and the widest retail distribution coverage across all European trade channels.

To access detailed market analysis, Request Sample

Carbonated water holds 21.4%, driven particularly by Germany's established sparkling culture where carbonated varieties have traditionally outsold still water in volume. Mineral water accounts for 17.3%, with iconic brands including S.Pellegrino, Evian, Perrier, and Gerolsteiner commanding premium loyalty. Flavored water at 12.7% is the fastest-growing type at ~5.2% CAGR through 2034.

By Packaging Type

PET bottles command a dominant 72.5% share in 2025. This format's supremacy is driven by cost efficiency, lightweight logistics advantages, and recyclability aligned with EU 90% plastic bottle collection rate targets by 2029. PET's ongoing transition to rPET formulations is neutralizing its environmental criticism while preserving its operational cost advantages for mass-market retail supply chains.

Metal cans represent 15.3% of packaging volume and are growing at the fastest rate at ~5.8% CAGR, driven by aluminum's infinite recyclability, premium shelf appeal, and alignment with EU single-use plastic restriction legislation.

Regional Market Insights

Germany's market leadership at 21.7% in 2025 reflects the country's uniquely high per-capita bottled water consumption (~147 liters per year), deeply embedded sparkling water culture, and a robust network of domestic mineral water brands. Germany's pfand (deposit) bottle return system achieves 98% recollection rates, which aligns market practices with EU regulatory evolution and sustains structural long-term demand.

France at 18.6% leverages its deep mineral water heritage; Evian, Volvic, and Perrier are globally recognized origin-brand icons, combined with 100M+ annual tourist arrivals in 2024. The United Kingdom at 16.4% is driven by rising functional and flavored water consumption, expanding e-commerce, and aggressive rPET commitments from domestic brands.

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

21.7% |

High per-capita bottled water consumption; strong domestic mineral water culture; well-established premium and sparkling water segment. |

|

France |

18.6% |

Long-standing mineral water heritage; significant inbound tourism sustaining on-trade demand; leadership in both still and sparkling premium water categories. |

|

United Kingdom |

16.4% |

Growing demand for functional and flavored water varieties; increasing health-conscious consumer base; expanding digital and direct-to-consumer retail channels for premium hydration products. |

|

Italy |

14.2% |

Among the highest per-capita bottled water consumption rates in Europe; strong mineral water tradition; significant on-trade channel penetration through hospitality and tourism sectors. |

|

Spain |

11.3% |

Warm climate driving sustained seasonal demand; high inbound tourism volumes supporting on-trade consumption; growing interest in premium still and sparkling water sub-segments. |

|

Others |

17.8% |

Emerging markets in Eastern Europe experiencing above-average growth, driven by rising disposable incomes, improving retail infrastructure, and increasing consumer premiumization trends. |

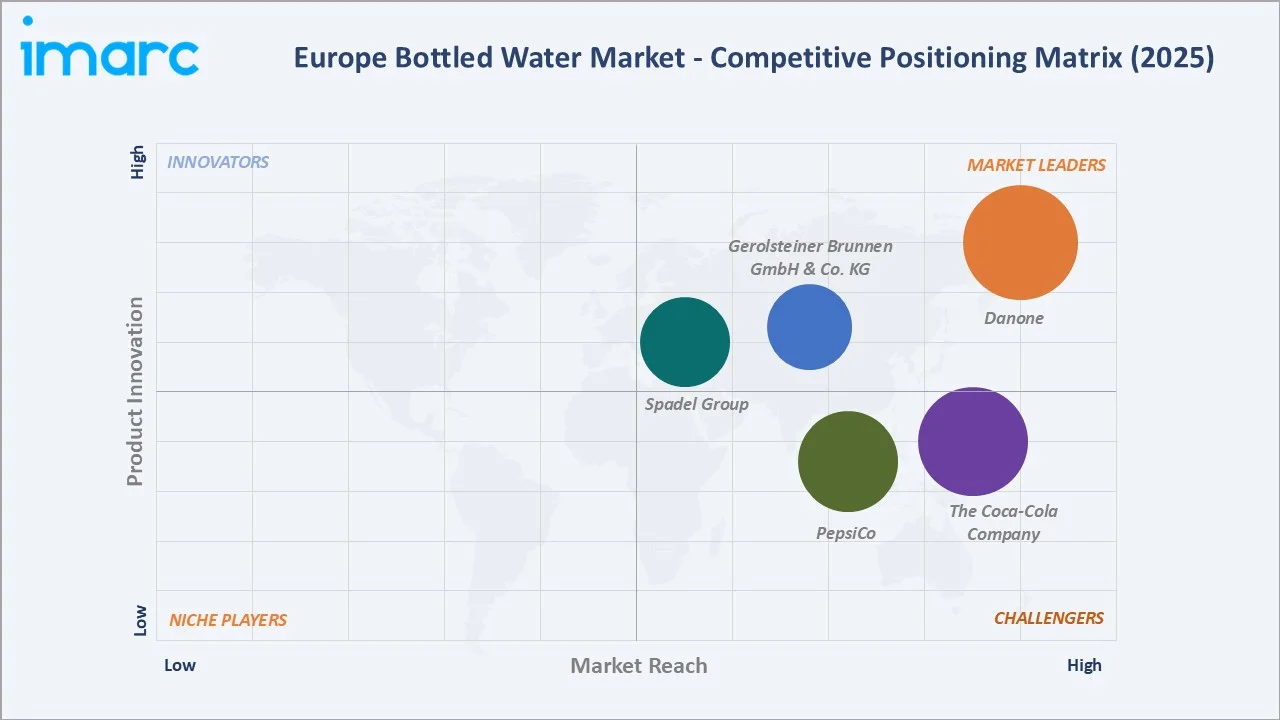

Competitive Landscape

Europe's bottled water market exhibits moderate-to-high concentration, with the top five vendors collectively accounting for over 60% of total market revenue in 2025, according to the European Federation of Bottled Waters. Innovation in sustainable packaging, functional water formulations, and digital-channel distribution is the primary competitive differentiator.

|

Company |

Key Brands |

Position |

Core Strength |

|

Danone |

Evian, Volvic, Hayat, Żywiec Zdrój |

Market Leader |

Alpine origin heritage; functional water innovation |

|

The Coca-Cola Company |

Smartwater, Aquarius, POWERADE, Topo Chico, vitaminwater |

Strong Challenger |

Unmatched retail distribution; premium functional water; aluminum can expansion. |

|

PepsiCo |

Aquafina |

Strong Challenger |

Lifestyle branding; health-focused water innovation; beverage portfolio synergies. |

|

Gerolsteiner Brunnen GmbH & Co. KG |

Gerolsteiner |

Regional Leader |

Germany market dominance; mineral content credentials; loyal consumer base; glass packaging. |

|

Spadel Group |

Spa, BRU, Carola, Wattwiller, Devin |

Regional Leader |

Pioneering position in eco-packaging and circular materials; brands deeply anchored to territorial water sources |

Regional players, including Highland Spring (UK), Radenska (Slovenia), and Mattoni (Czech Republic), are gaining traction through provenance storytelling, local sourcing credentials, and B-Corp sustainability certifications. Private-label competition from major retailers continues to exert sustained margin pressure in the mass-market still water segment.

Key Company Profiles

Danone

Danone, headquartered in Paris, France, is Europe's second-largest bottled water player through its Evian, Volvic, and other brands. The company reported Q1 2026 sales of EUR 6,708 Million, up +2.7% on a like-for-like (LFL) basis, driven by its successful premium portfolio repositioning and sustainability leadership.

- Product Portfolio: Evian (premium Alpine mineral), Volvic (volcanic still), Hayat, and Żywiec Zdrój

- Recent Developments: In April 2026, Danone announced investment of EUR 20 million in its Evian bottling site and EUR 8 million in water-source preservation, as health trends and reduced sugar consumption drive demand for low-calorie hydration options.

- Strategic Focus: Eco-system packaging; Evian brand premiumization through cultural and wellness partnerships; Volvic functional water innovation targeting active lifestyle consumers.

The Coca-Cola Company

The Coca-Cola Company, headquartered in Atlanta, US, operates in the European bottled water market primarily through Coca-Cola European Partners (CCEP). The company leverages its unmatched European retail distribution network across all trade channels.

- Product Portfolio: Smartwater (premium vapor-distilled), Aquarius (electrolyte-enhanced functional). POWERADE, Topo Chico, and vitaminwater.

- Recent Developments: In May 2025, Coca-Cola agreed to revise recycling-related claims on its plastic bottles across Europe. The company clarified packaging labels and adjusted claims such as recycled-content information to align with EU consumer protection expectations.

- Strategic Focus: Aluminum can expansion for on-trade and premium retail; Smartwater premium brand growth; 100% rPET bottle rollout across European markets; functional water innovation targeting health-conscious consumers.

Market Concentration Analysis

Europe's bottled water market exhibits moderate-to-high concentration at the top tier, with the leading five global brand owners holding an estimated 60%+ of total market revenue in 2025. Below the top tier, a competitive mid-market of 20–30 specialized regional bottlers and private-label operators serves specific national sub-markets, on-trade channels, and emerging functional water niches.

Consolidation is occurring primarily at the premium sustainability-innovation intersection. Danone's recycling consortium partnerships and Coca-Cola's Italian brand acquisition reflect strategic portfolio strengthening rather than direct competitor M&A. Regional players including Spadel Group, which reached the billion-liter milestone and maintains B-Corp status, and Highland Spring are carving out sustainable premium positioning to defend market share against global brand dominance.

Investment & Growth Opportunities

Fastest Growing Segments

Flavored water (~5.2% CAGR), metal cans packaging (~5.8% CAGR), functional/fortified water (projected 6%+ CAGR), and premium mineral water in glass packaging represent the highest-growth investment vectors through 2034. Eastern European market expansion, particularly Poland, the Czech Republic, and Romania, offers greenfield distribution opportunities for established Western European brands. Together, these sub-categories represent an incremental addressable value of approximately USD 15+ Billion by 2034.

Emerging Market Expansion

- Eastern Europe Greenfield: Poland (projected CAGR 7.14%), Czech Republic, and Romania offer early-mover advantages for brands investing in local distribution and logistics ahead of regional retail modernization curves.

- rPET Infrastructure Investment: Closed-loop rPET collection and reprocessing partnerships offer strong ROI as EU mandatory recycled content regulations create compliance-driven capex cycles across all major bottlers from 2030.

- DTC and Subscription Commerce: Subscription hydration services growing at 12% annually represent a high-margin, low-churn revenue stream for premium water brands targeting urban professional consumers in the UK, Germany, and France.

Venture and Institutional Investment Trends

- Premium Brand M&A: Smaller artisanal European water brands with strong provenance storytelling and B-Corp certification are becoming attractive acquisition targets for global FMCG conglomerates seeking to add premium SKUs to existing distribution networks.

- Functional Water R&D: Investment in EFSA-approved functional water ingredient research is enabling new product category creation. Brands commanding health-functional premiums of 25–40% over standard water are attracting both brand investment and ingredient supplier co-development capital.

- Sustainable Packaging Ventures: Biodegradable packaging material startups (PHA bioplastics, compostable carton innovations) are attracting ESG-aligned investment as brand owners seek compliance pathways ahead of future EU packaging waste regulation milestones.

Future Market Outlook (2026-2034)

Europe's bottled water market is positioned for sustained, steady-growth expansion through 2034. From a base of USD 75.74 Billion in 2025, the market is projected to pass USD 91.88 Billion by 2030 and reach USD 107.24 Billion by 2034, representing total incremental value creation of USD 31.50 Billion at a CAGR of 3.94%.

This growth is structurally supported by the multi-year EU packaging transition cycle, Europe's entrenched hydration culture, and the progressive premiumization of the category. The Europe bottled water market forecast reflects both volume expansion in emerging Eastern European markets and value premiumization in mature Western European markets.

Still water's volume dominance is expected to be maintained, while the product mix evolves increasingly toward flavored and functional varieties. Carbonated water will sustain growth anchored by Germany and Southern Europe's sparkling water cultures. Aluminum cans will grow from 15.3% to an estimated 20%+ of packaging volume as sustainability regulation and brand investment converge.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 85 industry stakeholders in 2024–2025, including bottled water brand managers, retail category buyers, sustainability officers, packaging engineers, and institutional investors across Germany, France, the UK, Italy, and Spain. Expert input validated market sizing, regional demand dynamics, and packaging technology adoption rates across European sub-markets.

Secondary Research

Secondary research encompassed European Federation of Bottled Waters (EFBW) reports, EU packaging legislation documentation (EU Packaging Regulation 2022/0396/COD), Euromonitor and Statista beverage market databases, company annual reports (Danone FY2024, Coca-Cola HBC FY2024), EFSA regulatory filings, and trade publications (Beverage Daily, The Grocer, Food Navigator Europe).

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting methodologies, incorporating retail volume data, per-capita consumption trends by country, packaging format transition rates, and vendor revenue disclosures. A base-case CAGR of 3.94% reflects consensus estimates validated against announced brand investments, regulatory compliance timelines, and historical market performance from 2020 to 2025.

Europe Bottled Water Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Still, Carbonated, Flavored, Mineral |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Direct Sales, On-Trade, Others |

| Packaging Types Covered | PET Bottles, Metal Cans, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Danone, The Coca-Cola Company, PepsiCo, Gerolsteiner Brunnen GmbH & Co. KG, Spadel Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe bottled water market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global Europe bottled water market.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe bottled water industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Bottled Water Market Report

The Europe bottled water market reached USD 75.74 Billion in 2025, up from USD 62.44 Billion in 2020.

The Europe bottled water market is projected to exhibit a CAGR of 3.94% during 2026-2034, reaching USD 107.24 Billion by 2034.

PET bottles dominate the Europe bottled water market with a 72.5% packaging share in 2025, driven by cost efficiency, lightweight logistics advantages, and recyclability.

Still dominate the Europe bottled water market with a 48.6% share in 2025, reflecting universal everyday hydration appeal and broad accessibility across price tiers.

Germany currently dominates the Europe bottled water market, accounting for a share of 21.7% in 2025, driven by high per-capita consumption, deeply embedded sparkling water culture, and strong domestic brand loyalty.

The major players in the Europe bottled water market include Danone, The Coca-Cola Company, PepsiCo, Gerolsteiner Brunnen GmbH & Co. KG, and Spadel Group.

Rising health consciousness shifting consumers from sugary beverages to water, robust European tourism sustaining on-trade demand, and stringent EU quality and sustainability regulations are the primary growth drivers.

Flavored water is the fastest-growing product type in the Europe bottled water market, growing at an estimated ~5.2% CAGR during 2026–2034. Growth is driven by younger European consumers seeking low-calorie, health-forward alternatives with natural fruit extract and herbal infusion profiles.

Eastern European markets are the fastest-growing national sub-markets within the Europe bottled water market. Growth is driven by rising disposable incomes, retail infrastructure modernization, and increasing aspirational demand for premium international and private-label bottled water brands.

Key challenges include growing consumer and regulatory scrutiny over single-use plastic waste, increasing competition from high-quality municipal tap water and premium home filtration systems in Northern Europe, and PET resin and aluminum commodity price volatility impacting bottler profitability.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)