Europe Digital Health Market Size, Share, Trends and Forecast by Type, Component, and Country, 2026-2034

Europe Digital Health Market Size, Share, Trends & Forecast (2026-2034)

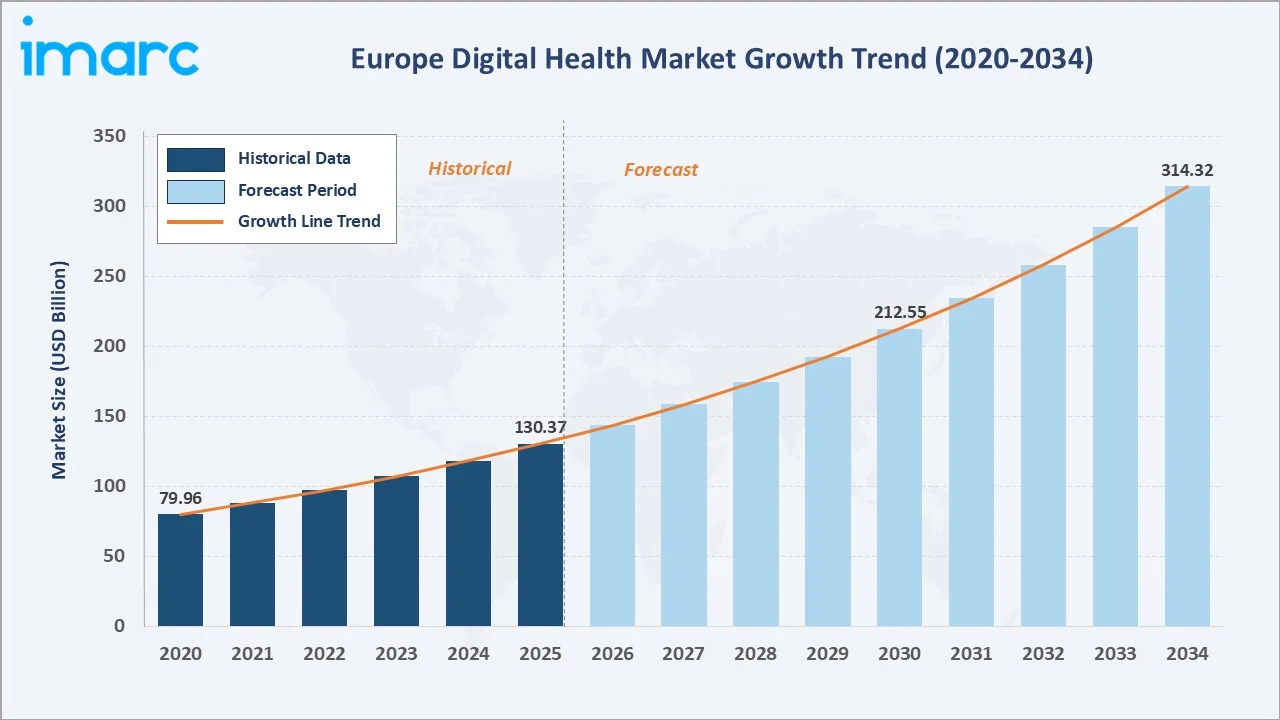

The Europe digital health market reached USD 130.37 Billion in 2025 and is projected to reach USD 314.32 Billion by 2034, exhibiting a CAGR of 10.27% during 2026-2034. Growth is anchored by accelerated digital transformation across national health systems, the European Health Data Space (EHDS) regulatory rollout, demographic pressure from an aging EU population, AI-enabled clinical workflows, and rising consumer adoption of telehealth, wearables, and remote monitoring platforms.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 130.37 Billion |

|

Market Forecast (2034) |

USD 314.32 Billion |

|

CAGR (2026-2034) |

10.27% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

Rising demand for telemedicine, remote patient monitoring, electronic health records, mobile health applications, and AI-enabled diagnostics is being supported by aging populations, increasing chronic disease burden, and the need to reduce pressure on hospitals and clinics.

To get more information on this market, Request Sample

Strong government focus on healthcare digitization, cross-border health data exchange, and connected care infrastructure is further encouraging investment in digital platforms. In addition, the expansion of wearable devices, cloud-based healthcare systems, and personalized medicine is transforming how patients, providers, and payers interact across the European healthcare ecosystem.

Executive Summary

Europe's digital health market is among the fastest-growing healthcare technology categories globally, driven by structural demographic pressure (about one-fifth of the EU population is aged 65 or older as of 2025), persistent workforce shortages, and ambitious regulatory frameworks anchored by the European Health Data Space (EHDS), the EU AI Act, and Germany's DiGA reimbursement scheme.

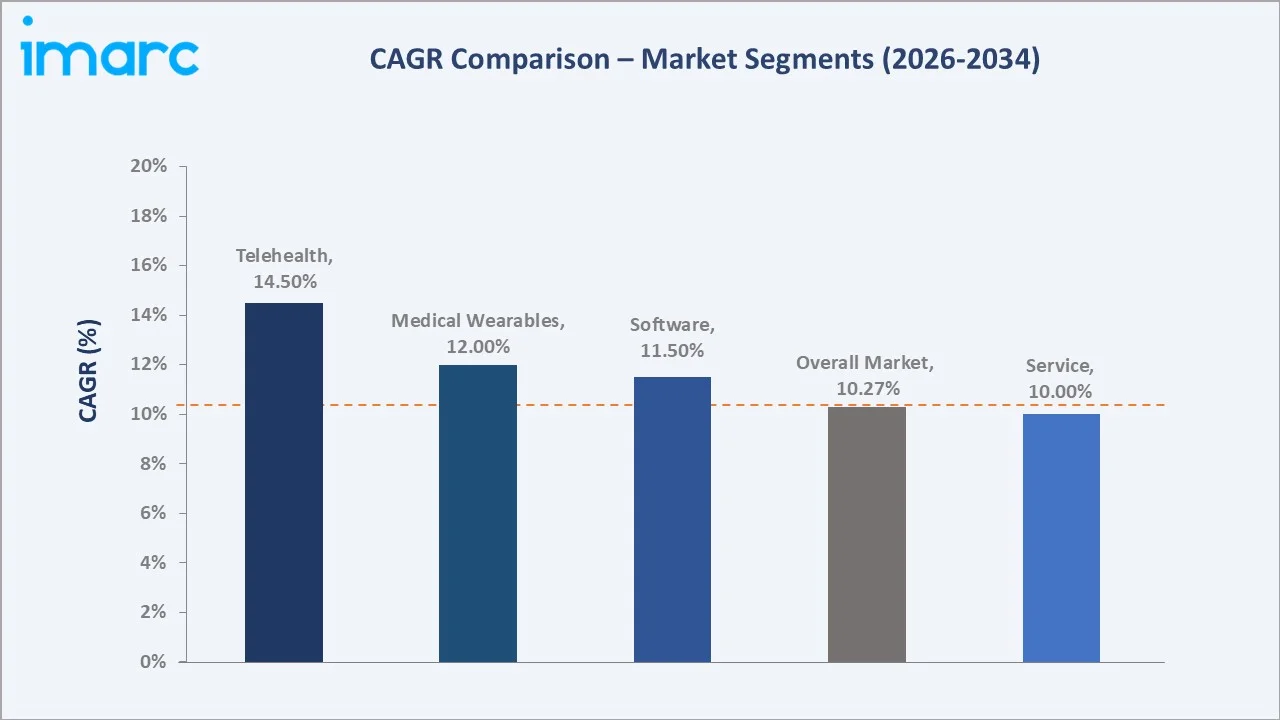

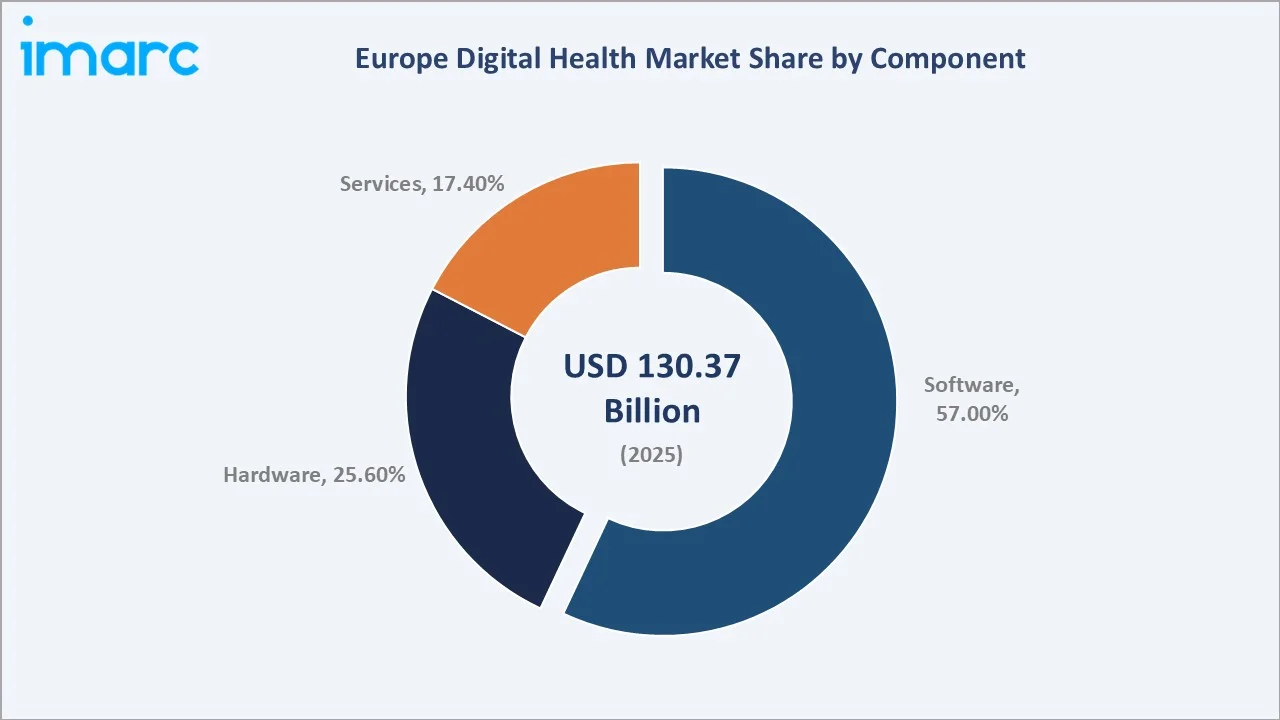

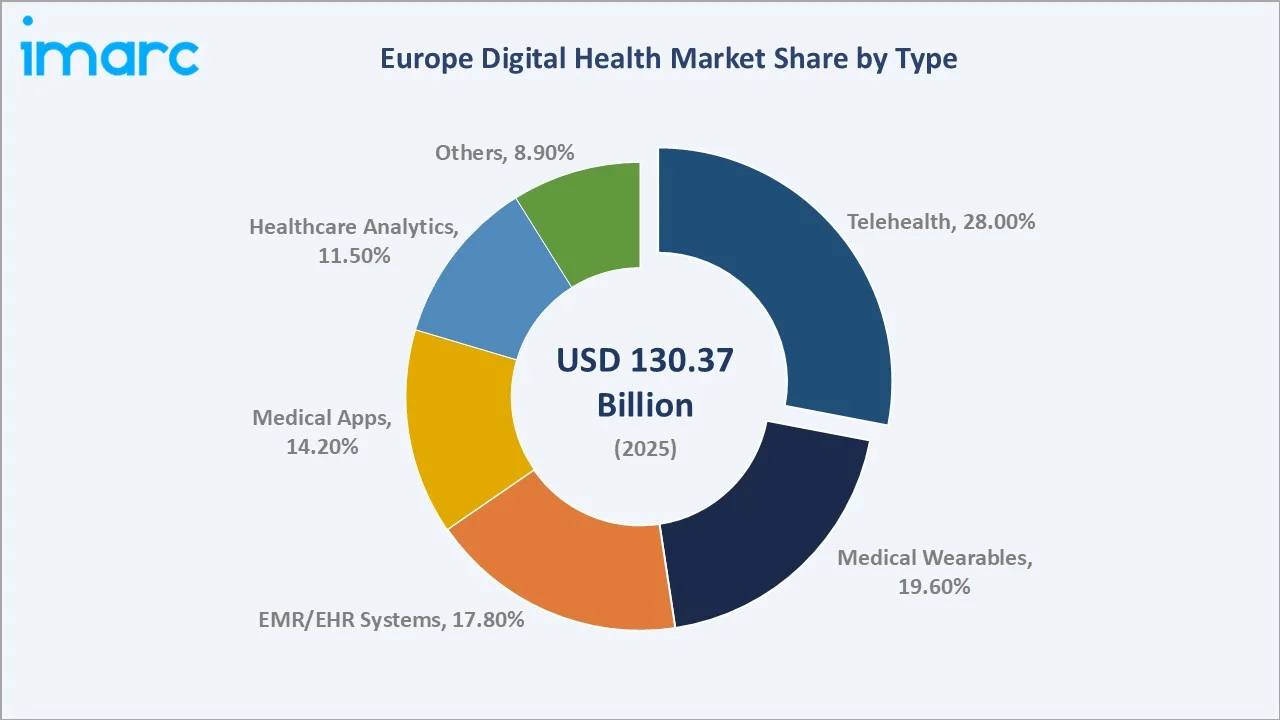

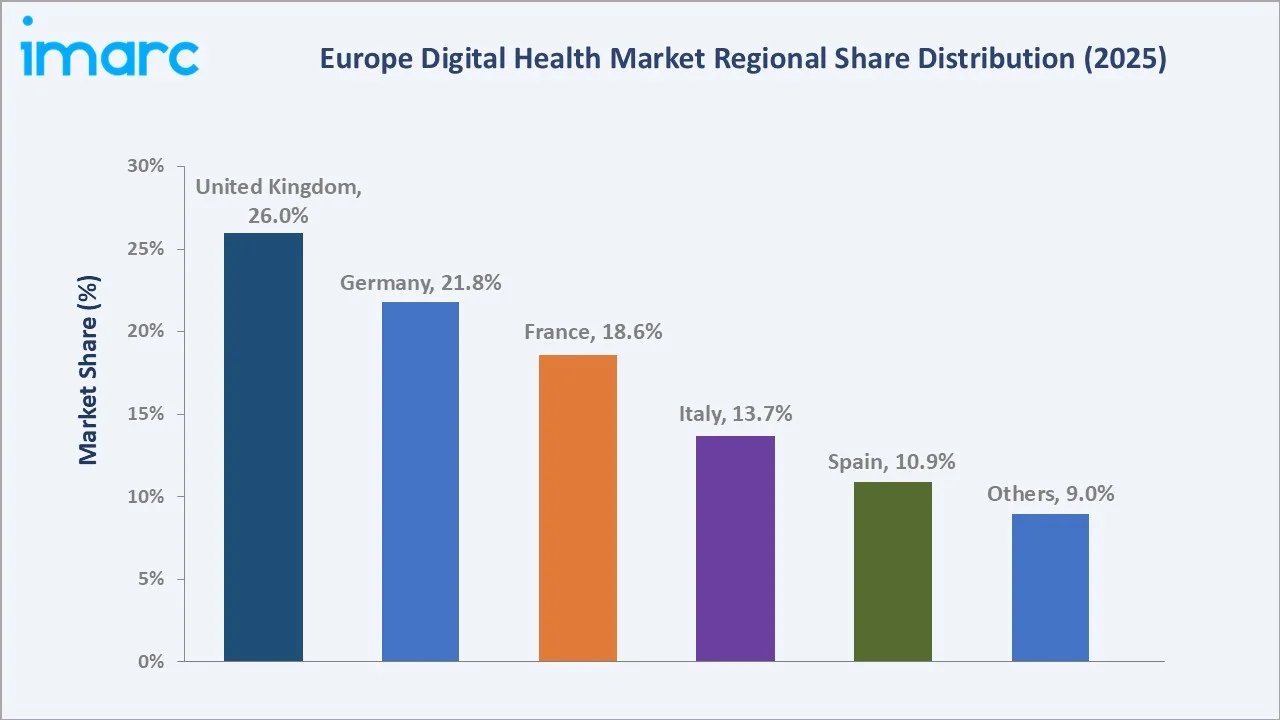

The market is structurally fragmented at the application layer, with the top five vendors controlling under 20% of total revenue, leaving substantial room for regional specialists and platform consolidators. Software dominates the component mix at 57.0% in 2025, telehealth leads types at 28.0%, and the United Kingdom anchors regional share at 26.0%.

In October 2025, the European Commission launched a EUR 1 Billion Apply AI strategy funding AI-powered screening centers, while in November 2025 the European Health and Digital Executive Agency (HaDEA) signed EU4Health contracts strengthening EHDS implementation. Hims & Hers entered the European market via its June 2025 acquisition of UK-based ZAVA, signaling intensifying cross-border M&A.

Key Market Insights

|

Indicator |

Value (2025) |

|

Leading Component |

Software (57.0%) |

|

Fastest-Growing Component |

Software (~11.5% CAGR) |

|

Leading Type |

Telehealth (28.0%) |

|

Fastest-Growing Type |

Telehealth (~14.5% CAGR) |

|

Largest Country |

United Kingdom (26.0%) |

|

Key Players (Top 5) |

Siemens, Koninklijke Philips N.V., Medtronic, Oracle, Epic Systems Corporation |

Key Analytical Observations Supporting the Above Data:

- Software accounts for 57.0% of the Europe digital health market in 2025, reflecting the dominance of cloud-based EHR platforms, AI-powered clinical decision support, patient engagement applications, and healthcare analytics tools across both public and private health systems.

- Hardware at 25.6% covers wearable devices, RPM sensors, smart medical devices, and connected diagnostic equipment, with Siemens, Koninklijke Philips N.V., and Medtronic supplying integrated hardware-software stacks across European hospitals.

- Telehealth at 28.0% leads the type segmentation, supported by permanent reimbursement codes, clinician familiarity with video workflows, and continued post-pandemic adoption. The European telehealth segment alone was valued at USD 36.5 Billion in 2025 and is projected to reach approximately USD 88 Billion by 2034.

- Medical wearables at 19.6% and EMR/EHR systems at 17.8% form the next-largest type segments, with Germany's DiGA framework enabling reimbursable "apps on prescription," and in May 2026, Doctolib acquired UK-based Medicus Health to enter the UK digital health market.

- The United Kingdom's 26.0% regional share reflects NHS Long Term Plan digital transformation funding, robust UK health-tech venture capital activity, and the global concentration of health technology startups in London and Cambridge.

Europe Digital Health Market Overview

Digital health refers to the use of information and communication technologies (ICTs) to improve disease prevention, diagnosis, treatment, monitoring, and health system management. Europe's digital health market spans telehealth and telemedicine platforms, mobile health (mHealth) applications, electronic health records (EHR/EMR), medical wearables and remote patient monitoring (RPM) devices, healthcare data analytics, and AI-driven diagnostic and decision-support tools.

In 2025, the EU published the European Health Data Space (EHDS) Regulation, aiming to enhance access, interoperability, and innovative use of electronic health data across member states. National systems are scaling digital infrastructure to address aging populations, workforce shortages, rising healthcare costs, and rising patient demand for accessible, data-driven, and personalized services. The EU AI Act, which entered into force in August 2024 with phased application through 2027, sets requirements for high-risk medical AI systems.

Market Dynamics

To evaluate market opportunities, Request Sample

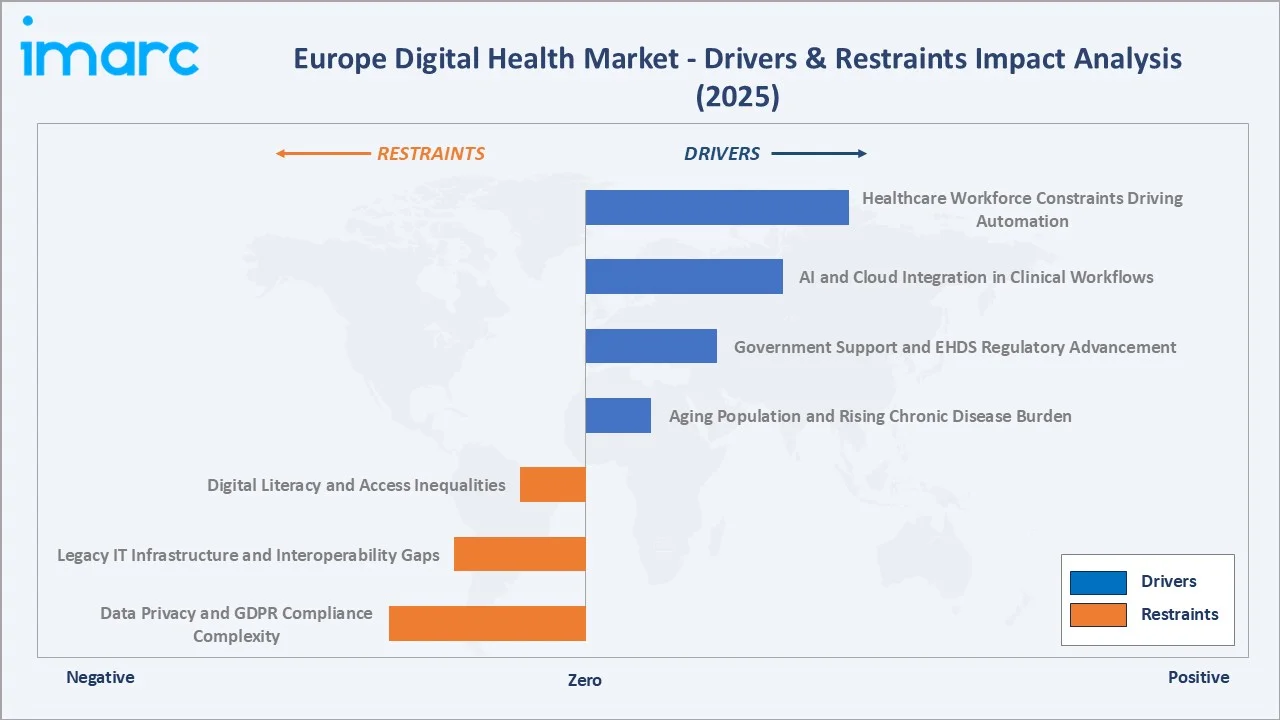

Market Drivers

- Aging Population and Rising Chronic Disease Burden: Europe holds one of the world's oldest demographic profiles, with approximately one-fifth of the EU population aged 65 or older as of early 2025. RPM, telehealth consultations, and digital therapeutics enable proactive intervention and continuous care for chronic-disease patients, reducing acute episodes and hospitalizations.

- Government Support and EHDS Regulatory Advancement: Germany's DiGA framework allows certified digital health apps to be prescribed and reimbursed under statutory healthcare; France's PECAN fast-track reimburses evidence-based apps after review (up to 60 days); Italy's EUR 15.6 Billion healthcare mission, covering community care, telemedicine, and digitalization under the National Recovery and Resilience Plan (2021–2026).

- AI and Cloud Integration in Clinical Workflows: In October 2025, the European Commission launched the EUR 1 Billion Apply AI strategy funding AI-powered screening centers. Siemens, Koninklijke Philips N.V., and Oracle are embedding AI diagnostic modules, predictive analytics, and population health tools into EHR and imaging platforms, accelerating multi-country deployments.

- Healthcare Workforce Constraints Driving Automation: A 2025 survey of 442 healthcare executives across 13 European countries found severe staffing shortages, with 90% of German hospitals affected. Digital scheduling, RPM, virtual care, and AI-assisted documentation enable redistribution of clinical workload across teams, supporting service continuity amid demographic pressure.

Market Restraints

- Data Privacy and GDPR Compliance Complexity: Strict GDPR requirements combined with emerging EU AI Act compliance obligations raise cost and complexity for digital health vendors. Healthcare organizations also face escalating cybersecurity investment requirements alongside patient data breach risk.

- Legacy IT Infrastructure and Interoperability Gaps: Many European health systems operate fragmented legacy IT environments, requiring substantial investment in infrastructure modernization, FHIR standards adoption, and change management. EHDS interoperability mandates create both opportunity and short-term integration burden across member states.

- Digital Literacy and Access Inequalities: Older adults, low-income populations, and rural residents face barriers to digital health adoption, risking widening health disparities. Differences in broadband access, device ownership, and digital skills slow technology deployment in underserved communities across Eastern and Southern Europe.

Market Opportunities

- AI-Powered Diagnostic and Decision-Support Platforms: EHDS combined with Apply AI funding creates substantial opportunity for AI clinical decision support, computer vision in radiology, and predictive analytics. Vendors meeting EU AI Act high-risk system requirements can win multi-country framework agreements with national health services.

- Remote Patient Monitoring and Connected Care: London's Doccla raised GBP 35 Million in September 2024 to expand RPM across the UK and Europe, enabling 24/7 patient tracking and reducing emergency admissions. Connected medical devices and wearable sensors support proactive chronic-disease management and are recognized as essential infrastructure by national health systems.

Market Challenges

- Reimbursement Pathway Fragmentation: Reimbursement frameworks vary substantially across member states. Germany's DiGA, France's PECAN, and the UK's NICE evidence framework each impose different evidentiary, pricing, and integration requirements, limiting vendor speed-to-market across Europe.

- Cybersecurity Threats and Ransomware Exposure: European hospitals face escalating ransomware risk, with high-profile attacks on health systems disrupting clinical operations. NIS2 and DORA regulations are raising cybersecurity baselines while imposing additional compliance overhead on digital health vendors and provider organizations.

Emerging Market Trends

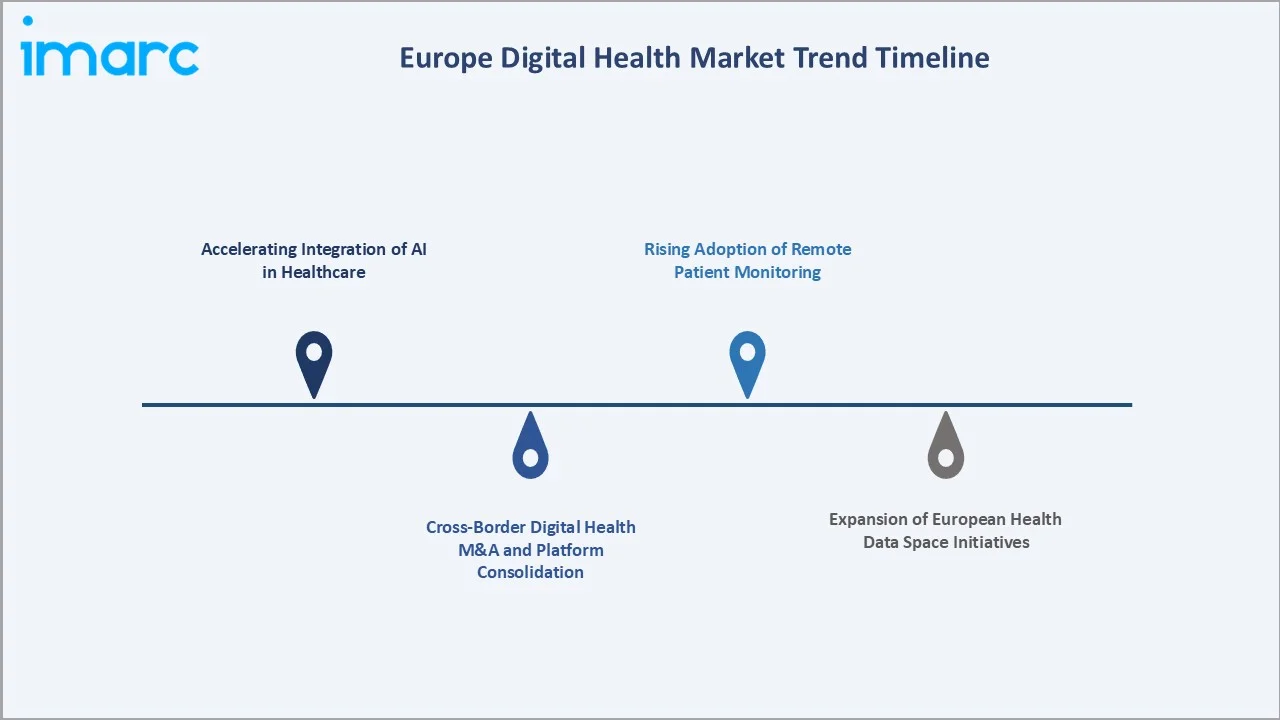

1. Accelerating Integration of AI in Healthcare

European healthcare is rapidly adopting AI across diagnostics, clinical decision support, and predictive analytics. In October 2025, the European Commission launched the EUR 1 Billion Apply AI strategy, funding AI-powered screening centers for early disease detection. The EU AI Act (effective 2024) governs high-risk medical AI systems, ensuring patient safety and algorithmic transparency across the bloc.

2. Rising Adoption of Remote Patient Monitoring

Healthcare providers are expanding RPM programs to manage chronic conditions and extend care to home settings. London-based Doccla raised GBP 35 Million in September 2024 to scale RPM across the UK and Europe; in April 2024, OMRON Healthcare Co., Ltd. acquired Luscii Healthtech, whose multi-condition RPM software is deployed in 70% of the Netherlands' hospitals. Connected wearables enable continuous data capture and proactive intervention.

3. Expansion of European Health Data Space Initiatives

In November 2025, the European Health and Digital Executive Agency (HaDEA) signed new EU4Health contracts to strengthen the EHDS and help stakeholders comply with secondary-use data requirements. EHDS establishes standardized EHR specifications, enabling citizens to access health information across member states and supporting research, innovation, and AI development.

4. Cross-Border Digital Health M&A and Platform Consolidation

In June 2025, Hims & Hers entered Europe by acquiring digital health platform ZAVA, accelerating its move into the UK, Germany, France, and Ireland across dermatology, mental health, and weight loss. Kry rolled out its internet cognitive behavioral therapy (ICBT) mental health program across Europe in 2022, having launched in Sweden earlier.

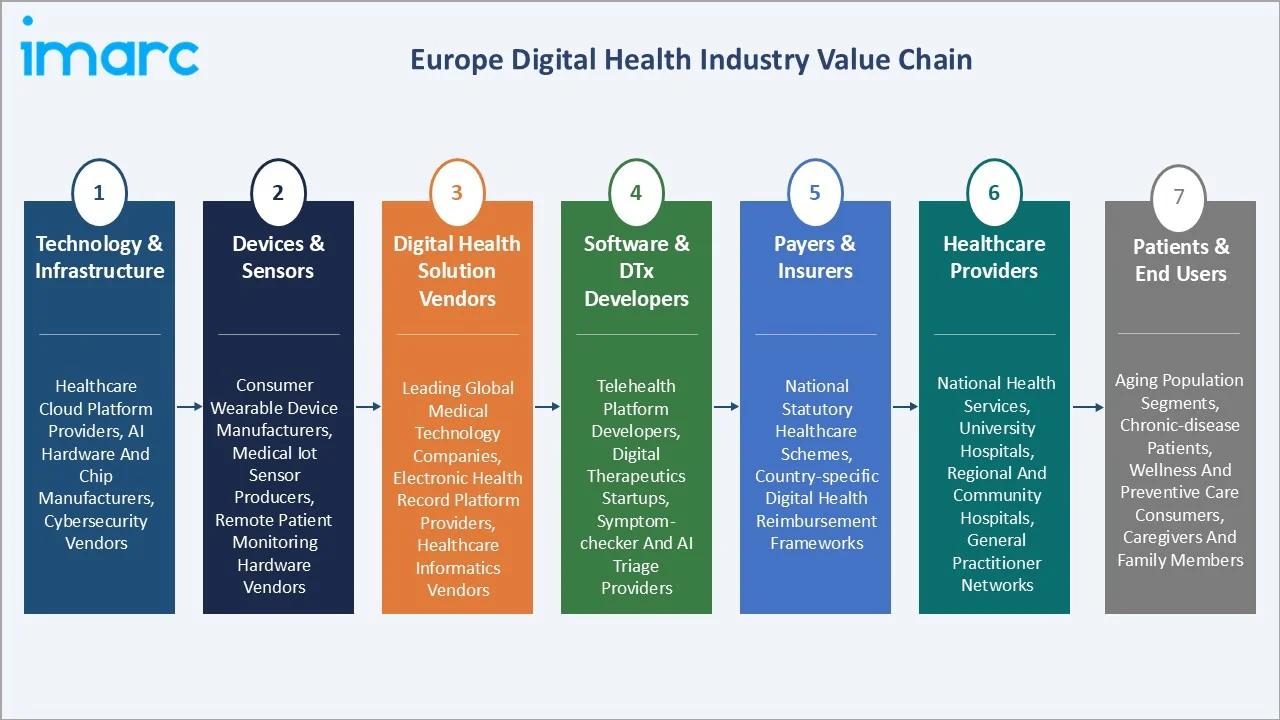

Industry Value Chain Analysis

|

Stage |

Key Players / Activities |

|

Technology & Infrastructure |

Healthcare cloud platform providers, AI hardware and chip manufacturers, semiconductor suppliers, cybersecurity vendors |

|

Devices & Sensors |

Consumer wearable device manufacturers, medical IoT sensor producers, remote patient monitoring hardware vendors |

|

Digital Health Solution Vendors |

Leading global medical technology companies, electronic health record platform providers, healthcare informatics vendors |

|

Software & DTx Developers |

Telehealth platform developers, digital therapeutics startups, symptom-checker and AI triage providers |

|

Payers & Insurers |

National statutory healthcare schemes, country-specific digital health reimbursement frameworks |

|

Healthcare Providers |

National health services, university hospitals, regional and community hospitals, general practitioner networks |

|

Patients & End Users |

Aging population segments, chronic-disease patients, wellness and preventive care consumers, caregivers and family members |

Technology Landscape in the Europe Digital Health Industry

Cloud-Based EHR and Clinical Platforms

Cloud-native EHR and clinical platforms anchor digital health infrastructure across Europe. In February 2025, Koninklijke Philips N.V. expanded its radiology informatics cloud on AWS to European data centers, enabling remote diagnostic reading with AI post-processing. Siemens Healthineers' Teamplay Digital Health Platform added AI diagnostic modules and discharge-planning tools, enabling plug-in licensing without integration overhead.

AI and Machine Learning Diagnostic Tools

AI applications span medical imaging, pathology, clinical decision support, and population health analytics. In December 2024, Siemens Healthineers unveiled Luminos Q.namix, a fluoroscopy and radiography platform with AI-guided workflows. Apply AI funding (EUR 1 Billion, October 2025) accelerates deployment of AI screening centers for early disease detection across the bloc.

Wearables and Remote Patient Monitoring

Connected medical wearables and home RPM devices enable continuous health data capture. Apple Watch, Fitbit, and Samsung consumer wearables integrate with Koninklijke Philips N.V., Medtronic, and OMRON Healthcare Co., Ltd. medical-grade RPM platforms. Doccla and Luscii Healthtech lead Europe-specific RPM deployments, with the latter reaching 70% of Netherlands hospitals through OMRON Healthcare Co., Ltd.’s April 2024 acquisition.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Software |

57.0% |

2025 |

|

Type |

Telehealth |

28.0% |

2025 |

|

Country |

United Kingdom |

26.0% |

2025 |

By Component

Software dominates with a 57.0% share in 2025, encompassing EHR platforms, clinical decision support systems, patient engagement applications, healthcare analytics, and AI diagnostic tools. Cloud-based deployment enables scalable, cost-effective implementation across providers of all sizes.

To access detailed market analysis, Request Sample

Hardware accounts for 25.6% in 2025, spanning medical wearables, RPM devices, connected diagnostic equipment, smart medical devices, and patient-facing IoT sensors. Service revenue at 17.4% covers implementation, training, support, and managed services delivered by system integrators and digital health vendors across European health systems.

By Type

Telehealth leads with a 28.0% share in 2025, supported by widespread virtual consultation adoption, RPM integration, and reimbursement formalization across France, Germany, the UK, Italy, and Spain. The Europe telehealth segment was valued at USD 36.5 Billion in 2025 and is projected to reach approximately USD 88 Billion by 2034 as institutionalized reimbursement codes accelerate uptake.

Medical wearables (19.6%), EMR/EHR systems (17.8%), medical apps (14.2%), and healthcare analytics (11.5%) form the next-largest type segments. The others category at 8.9% (2025) includes digital therapeutics, healthcare blockchain solutions, and patient engagement platforms.

Regional Market Insights

The United Kingdom leads at 26.0% in 2025, anchored by the NHS Long Term Plan digital transformation, sustained UK health-tech venture capital flows, and the concentration of innovation hubs across London, Cambridge, and Oxford. Post-Brexit regulatory autonomy enables flexible approaches to new digital health technologies while maintaining alignment with international safety standards.

Germany at 21.8% remains the second-largest market, anchored by plans to invest around EUR 2 billion in a national healthcare cybersecurity program running until 2029 to strengthen the resilience of hospitals and critical health infrastructure. France at 18.6% leads telehealth adoption with PECAN fast-track and Doctolib's e-prescribing expansion.

|

Region |

Share (2025) |

Key Growth Drivers |

|

United Kingdom |

26.0% |

National health service digital transformation programs; strong domestic health-tech venture capital ecosystem; established life-sciences innovation hubs |

|

Germany |

21.8% |

National reimbursement framework for prescription digital health apps; substantial hospital digitalization funding; leading academic AI and digital health research |

|

France |

18.6% |

Fast-track digital health reimbursement framework; strong domestic telehealth platform leadership; national e-prescription rollout |

|

Italy |

13.7% |

Multi-billion-euro community-care digitalization plan; widespread local health hub deployment; EU recovery fund-supported initiatives |

|

Spain |

10.9% |

Growing telehealth adoption across regions; public-private partnerships strengthening regional health systems |

|

Others |

9.0% |

Netherlands with near-universal electronic health record adoption; Nordic states advancing cross-border health data exchange |

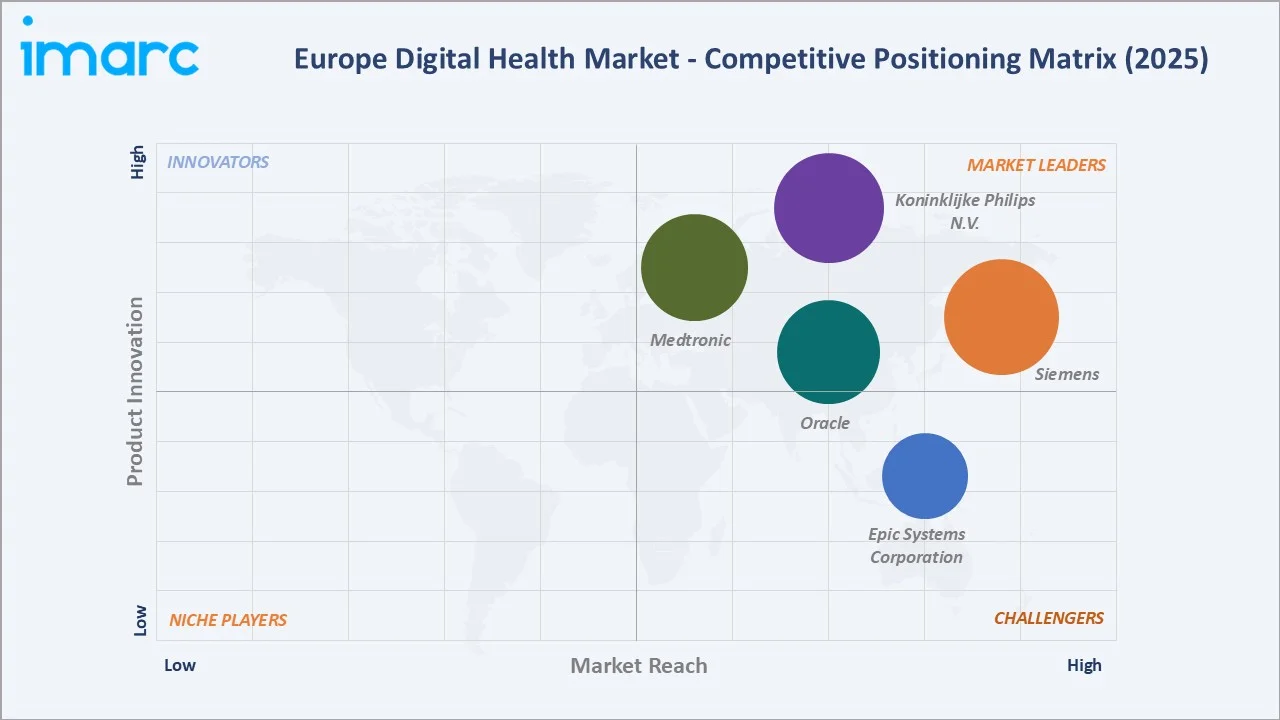

Competitive Landscape

Europe's digital health market is structurally fragmented, with the top five vendors controlling under 20% of total revenue. Leading players include Siemens, Koninklijke Philips N.V., Medtronic, Oracle, and Epic Systems Corporation.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Siemens |

teamplay Digital Health Platform, syngo Carbon, WeScan, teamplay Fleet, AI-Rad Companion |

Market Leader |

Imaging diagnostics, digital health platform with AI workflow integration, lab diagnostics |

|

Koninklijke Philips N.V. |

Philips HealthSuite, IntelliSpace, Cardiovascular Workspace, IntelliVue, Azurion |

Market Leader |

Cloud-based digital health platform, enterprise imaging informatics, patient monitoring |

|

Medtronic |

MiniMed, Guardian, CareLink |

Market Leader |

Remote patient monitoring ecosystem, diabetes technology with closed-loop systems |

|

Oracle |

Oracle Clinical AI Agent, Health Data Intelligence, Oracle Health Patient Accounting |

Market Leader |

Cloud-based EHR platforms, hospital information systems, AI-powered clinical data analytics |

|

Epic Systems Corporation |

MyChart, Cosmos, Hyperspace, Healthy Planet, Beaker, Rover |

Strong Challenger |

Enterprise EHR adoption in major European hospitals, patient portal with significant user base, AI-enabled clinical documentation |

Cloud infrastructure providers (AWS, Microsoft Azure, Google Cloud) are emerging as adjacent competitors, offering scalable healthcare services.

Key Company Profiles

Siemens

Siemens includes Siemens Healthineers, which is a leading global medical technology company and one of Europe's most influential digital health vendors. The teamplay Digital Health Platform anchors its enterprise software portfolio with AI-powered diagnostic, workflow, and discharge-planning modules.

- Product Portfolio: teamplay Digital Health Platform, AI-Rad Companion clinical decision support suite, syngo Carbon, WeScan, and teamplay Fleet.

- Recent Developments: In August 2025, Siemens Healthineers and Sony Healthcare Solutions Europe announced a strategic global collaboration integrating Siemens’ ARTIS angiography systems with Sony’s NUCLeUS audio-visual management platform.

- Strategic Focus: AI-enabled diagnostic platforms; EHDS-aligned interoperability; plug-in licensing model reducing TCO; multi-country framework agreements with national health services.

Koninklijke Philips N.V.

Koninklijke Philips N.V. is a diversified health technology company with a strong Connected Care segment encompassing telehealth, RPM, sleep and respiratory care, and enterprise informatics solutions deployed across European hospitals.

- Product Portfolio: IntelliVue patient monitors, IntelliSpace clinical informatics, Philips HealthSuite, Cardiovascular Workspace, and Azurion.

- Recent Developments: In May 2026, a Koninklijke Philips N.V.-included consortium with Cuviva and Vingmed was selected to support Region Stockholm’s hospital-at-home initiative, enabling advanced remote monitoring for up to 15,000 patients annually.

- Strategic Focus: Connected Care platform expansion; remote diagnostic services; AI post-processing in radiology; cardiac RPM rollouts in Germany and France; hospital-to-home continuum.

Market Concentration Analysis

Europe's digital health market is structurally fragmented at the application layer, with the top five vendors collectively controlling under 20% of total revenue. Established players Siemens, Koninklijke Philips N.V., Medtronic, Oracle, and Epic Systems Corporation lead the enterprise segment through scale, regulatory expertise, and hospital relationships.

Regional specialists Doctolib, Doccla, and Ada Health anchor the country-specific layer, with Doctolib leveraging local reimbursement frameworks. M&A activity is intensifying, exemplified by Hims & Hers' June 2025 acquisition of ZAVA.

Investment & Growth Opportunities

Fastest Growing Segments

- Telehealth is projected to grow at approximately 14.5% CAGR through 2034, supported by permanent reimbursement codes, clinician familiarity, and rising consumer adoption across France, Germany, and the UK.

- Medical wearables and RPM platforms are projected to expand at approximately 12.0% CAGR, with chronic-disease management and home-based care driving sustained adoption.

Emerging Market Expansion

- Eastern European and Nordic markets present substantial growth headroom as EU recovery and structural funds accelerate national digital health investments.

- Cross-border telehealth and digital therapeutics deployment is enabled by EHDS interoperability, opening pan-European go-to-market opportunities for vendors with multi-country compliance capability.

Venture and Institutional Investment Trends

- UK health-tech venture capital remains the most active funding source in Europe, with London-based Doccla raising GBP 35 Million in 2024 to expand RPM, and German hospitals receiving EUR 300 Million in government allocation for EHR and cybersecurity upgrades.

- AI-focused digital health rounds are accelerating, supported by the EUR 1 Billion Apply AI strategy and EU AI Act compliance demand for high-risk medical AI systems.

Future Market Outlook (2026-2034)

Europe's digital health market is positioned for sustained double-digit expansion through 2034. From USD 130.37 Billion in 2025, the market is projected to reach USD 314.32 Billion by 2034, representing incremental value of USD 183.95 Billion at a 10.27% CAGR, increasingly composed of AI-enabled platforms, telehealth services, RPM ecosystems, and interoperable EHR infrastructure.

Software is expected to expand its share toward 60% by 2034, while telehealth grows toward 35% of the type segment. The UK, Germany, and France will retain combined leadership above 65% of regional revenue. EHDS interoperability, EU AI Act compliance maturity, and demographic pressure will collectively drive continued investment, with AI diagnostics, predictive analytics, and DTx representing the highest-growth subcategories.

Research Methodology

Primary Research

Primary research included structured interviews with over 100 industry participants in 2024–2025, health system CIOs, digital health platform executives, EHR vendors, telehealth operators, and EU policy stakeholders, validating market sizing, segmentation, regional shares, and adoption trends across the EHDS and DiGA frameworks.

Secondary Research

Secondary research covered Eurostat demographic and healthcare data, European Commission EHDS and Apply AI publications, EU AI Act documentation, OEM annual reports, national digital health strategies, HaDEA EU4Health contracts, and industry publications including Eurostat, EC, OECD, WHO Europe, HIMSS, HaDEA, ENISA, BfArM, and NHS Digital.

Forecasting Models

Market size estimations used combined top-down and bottom-up forecasting, incorporating country-level digital health expenditure, segment-level penetration rates, vendor revenue disclosures, and policy-driven reimbursement uptake. The 10.27% CAGR reflects validation against EU policy timelines, EHDS implementation milestones, and announced national investment pipelines through 2034.

Europe Digital Health Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Telehealth, Medical Wearables, EMR/EHR Systems, Medical Apps, Healthcare Analytics, Others |

| Components Covered | Software, Hardware, Service |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Siemens, Koninklijke Philips N.V., Medtronic, Oracle, Epic Systems Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Digital Health Market Report

The Europe digital health market reached USD 130.37 Billion in 2025 and is projected to reach USD 314.32 Billion by 2034.

The market is expected to grow at a CAGR of 10.27% during 2026-2034, driven by aging demographics, EHDS regulatory rollout, AI integration, and workforce-driven automation.

The United Kingdom leads with a 26.0% share in 2025, supported by NHS Long Term Plan digital transformation and strong UK health-tech venture capital activity.

Software dominates with a 57.0% share in 2025, encompassing EHR platforms, clinical decision support, patient engagement applications, and AI diagnostic tools.

Telehealth leads with a 28.0% share, supported by permanent reimbursement codes, RPM integration, and rising virtual consultation adoption across EU member states.

Key players include Siemens, Koninklijke Philips N.V., Medtronic, Oracle, and Epic Systems Corporation.

Telehealth is growing at approximately 14.5% CAGR through 2034 due to permanent reimbursement codes, clinician familiarity with video workflows, and EHDS-enabled cross-border virtual care.

Key challenges include GDPR and AI Act compliance complexity, legacy IT and interoperability gaps, digital literacy inequalities, fragmented reimbursement pathways, and rising cybersecurity threats.

AI-powered diagnostic platforms, RPM and connected care, DTx and DiGA-reimbursable apps, and cross-border platform consolidation represent the highest-growth investment opportunities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)