Europe Electric Car Market Size, Share, Trends and Forecast by Type, Vehicle Class, Vehicle Drive Type, and Country, 2026-2034

Europe Electric Car Market Summary:

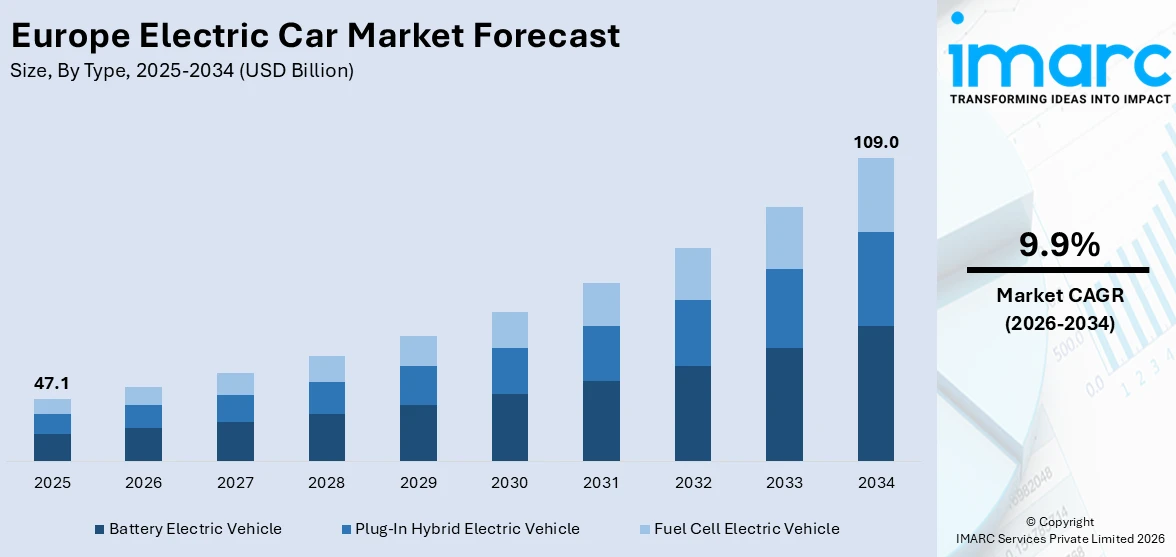

The Europe electric car market size was valued at USD 47.1 Billion in 2025 and is projected to reach USD 109.0 Billion by 2034, growing at a compound annual growth rate of 9.9% from 2026-2034.

The market is driven by increasingly stringent emission regulations, growing consumer demand for sustainable mobility, rapid expansion of charging infrastructure, and favorable government policies promoting zero-emission transportation. Accelerating technological advancements in battery performance, declining vehicle costs, and heightened environmental awareness are reshaping the automotive landscape across the continent. Supportive fiscal incentives, fleet electrification mandates, and the expanding diversity of available models are collectively propelling the Europe electric car market share.

Key Takeaways and Insights:

- By Type: Battery electric vehicle dominates the market with a share of 62.4% in 2025, driven by stricter emission regulations, expanding model availability, and growing consumer preference for zero-tailpipe-emission mobility solutions across the continent.

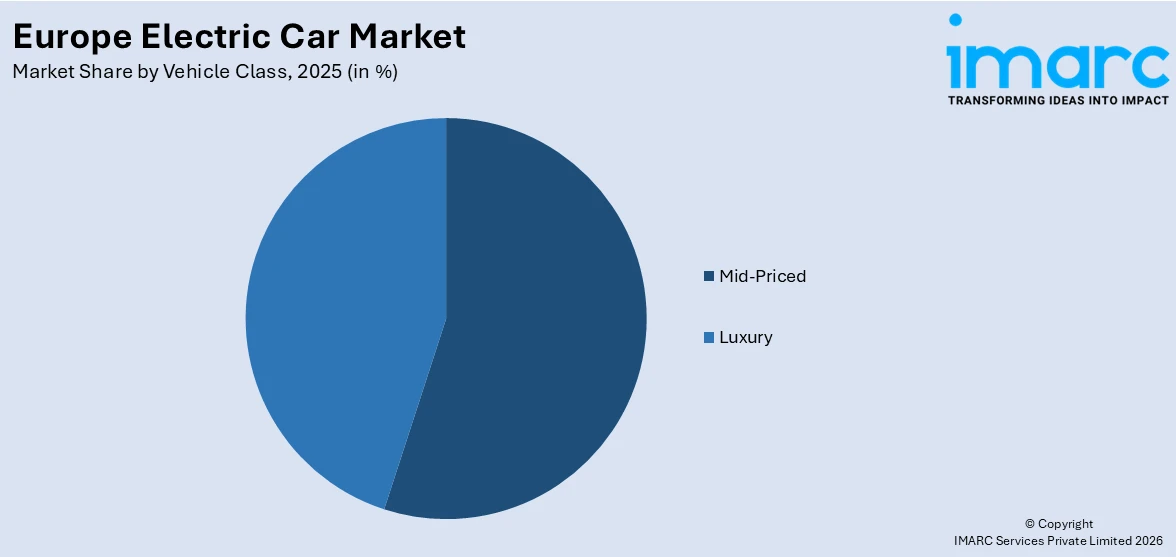

- By Vehicle Class: Mid-priced leads the market with a share of 52.3% in 2025, owing to increasing affordability of mainstream electric models and strong demand from cost-conscious European consumers.

- By Vehicle Drive Type: Front wheel drive represents the largest segment with a market share of 48.5% in 2025, driven by lower manufacturing costs, superior energy efficiency, and strong alignment with the design priorities of mass-market electric vehicle (EV) platforms.

- By Country: Germany leads the market with a share of 24.6% in 2025, owing to robust domestic automotive manufacturing, stringent emission policies, and accelerating corporate and consumer adoption of electric vehicles (EVs).

- Key Players: The Europe electric car market features a competitive landscape with established domestic manufacturers competing alongside global entrants. Players differentiate through product breadth, battery range, digital connectivity, pricing strategy, and charging network accessibility across premium and mass-market segments.

To get more information on this market Request Sample

The Europe electric car market is experiencing robust momentum, driven by evolving regulatory frameworks, rapid technological advancements, and shifting consumer preferences toward sustainable mobility. Governments across the region have enacted comprehensive emission reduction policies, compelling automakers to accelerate electrification strategies and introduce diverse vehicle offerings across multiple price segments. According to reports, the European Commission confirmed it is preparing legislation to tie EV subsidies and public incentives to a “Europe First” rule, requiring new electric vehicles to be assembled in the EU with at least 70% of non‑battery components sourced locally to qualify for support. The rapid expansion of public and private charging infrastructure is effectively addressing range anxiety concerns, making EVs an increasingly practical and convenient choice for everyday consumers. Continuous improvements in battery technology are enhancing vehicle performance, extending driving ranges, and gradually reducing overall ownership costs. Growing environmental awareness, strengthening corporate sustainability commitments, and supportive fiscal incentive programs are collectively reinforcing consumer confidence in electric mobility.

Europe Electric Car Market Trends:

Rapid Expansion of Charging Infrastructure Across Europe

The proliferation of public and semi-public charging networks is fundamentally reshaping the EV adoption landscape across Europe. According to reports, Europe deployed nearly 1.14 million public charging points, with Denmark’s DC chargers growing 55%, Belgium 52% and Austria 45% year‑on‑year, highlighting rapid infrastructure expansion. Regulatory mandates requiring high-power charging stations along major transport corridors are driving systematic infrastructure deployment throughout the region. National governments and private operators are channeling significant resources into building comprehensive charging ecosystems spanning highways, urban centers, and commercial premises. Enhanced charging speeds, improved cross-border interoperability through standardized connectors, and the rollout of smart-charging solutions are collectively reducing consumer hesitation and accelerating the broader transition toward electric mobility adoption.

Growing Affordability and Democratization of Electric Vehicles

The Europe electric car market is witnessing a significant shift toward price accessibility, as automakers respond to regulatory pressures by launching more affordable models targeting mainstream consumers. Declining battery costs, economies of scale, and technological improvements are enabling manufacturers to introduce competitively priced options across multiple vehicle segments. The growing availability of sub-premium electric models is broadening the consumer base beyond early adopters, with price parity emerging in higher-end segments. As per sources, Volkswagen confirmed development of a new all‑electric entry‑level model priced around EUR 20,000 to broaden access to EV ownership in Europe, with the world premiere scheduled for 2027. This democratization trend is expanding the addressable market and reinforcing long-term adoption momentum across the continent.

Strengthening Regulatory Framework and Policy-Driven Market Expansion

Government policy continues to serve as a primary catalyst shaping the Europe electric car market. The European Union's progressive carbon dioxide emission standards for new passenger vehicles are compelling automakers to increase electrified model offerings while reducing internal combustion engine dependence. In January 2026, Germany launched EV subsidy programme for low‑ and middle‑income households, providing up to 6,000 euros per fully electric car to benefit around 800,000 purchases. National purchase incentives, tax exemptions, and fleet electrification mandates are further stimulating consumer demand. The alignment of domestic and supranational policies is creating a stable environment that encourages sustained investment in vehicle development, charging infrastructure, and supporting technologies across the electric mobility ecosystem.

Europe Electric Car Market Outlook 2026-2034:

The Europe electric car market is poised for sustained and significant growth throughout the forecast period, driven by progressively stricter emission regulations, expanding charging infrastructure, and continuous improvements in vehicle affordability. Rising consumer confidence in electric mobility, growing model diversity across all vehicle classes, and deepening corporate sustainability commitments are expected to accelerate mainstream adoption. Supportive government policies, advancing battery technologies, and increasing price competitiveness with conventional vehicles will collectively drive robust revenue expansion, solidifying Europe's position as a globally leading EV market. The market generated a revenue of USD 47.1 Billion in 2025 and is projected to reach a revenue of USD 109.0 Billion by 2034, growing at a compound annual growth rate of 9.9% from 2026-2034.

.webp)

Europe Electric Car Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Battery Electric Vehicle |

62.4% |

|

Vehicle Class |

Mid-Priced |

52.3% |

|

Vehicle Drive Type |

Front Wheel Drive |

48.5% |

|

Country |

Germany |

24.6% |

Type Insights:

- Battery Electric Vehicle

- Plug-In Hybrid Electric Vehicle

- Fuel Cell Electric Vehicle

Battery electric vehicle dominates with a market share of 62.4% of the total Europe electric car market in 2025.

Battery electric vehicles represent the dominant force within the Europe electric car market, driven by their complete elimination of tailpipe emissions and alignment with the continent's ambitious decarbonization objectives. Increasingly stringent regulatory targets are compelling automakers to prioritize BEV platforms, resulting in a rapidly expanding portfolio of models across mainstream and premium categories. In January 2026, BEVs accounted for 19.3% of new car registrations in the EU, up from 14.9% a year earlier, reinforcing their growing preference over conventional powertrains.

The dominance of battery electric vehicles is further underpinned by sustained investment in battery technology, delivering meaningful improvements in energy density, charging speed, and overall vehicle range. Automakers are scaling dedicated electric platforms to achieve greater manufacturing efficiency and cost competitiveness, accelerating model introductions across previously underserved segments. Supportive government policies, expanding public and private charging ecosystems, and heightened environmental consciousness are creating a stable foundation for continued BEV leadership throughout the forecast period across the European market.

Vehicle Class Insights:

Access the comprehensive market breakdown Request Sample

- Mid-Priced

- Luxury

Mid-priced leads with a share of 52.3% of the total Europe electric car market in 2025.

The mid-priced commands the leading position within the Europe electric car market, reflecting the growing accessibility of EVs beyond luxury and premium buyer groups. Automakers responding to regulatory pressure and competitive dynamics have prioritized expanding their mainstream electric offerings, resulting in a diversifying lineup of well-equipped models at accessible price points. As per sources, China’s BYD launched its low‑cost Dolphin Surf EV in Europe, priced from 19,990-24,990 euros, putting pressure on traditional manufacturers to offer more affordable EVs.

Ongoing growth in this segment is fueled by declining battery costs, thus reducing the cost differential with similar conventional vehicles. The addition of compact electric crossovers and hatchbacks designed specifically for everyday use in urban and suburban environments has helped to significantly increase consumer interest. Improved residual values, lower operating costs, and the proliferation of flexible financing options are helping to reinforce consumer purchasing confidence, thus continuing to drive the segment's dominant share of the total Europe electric car market revenue.

Vehicle Drive Type Insights:

- Front Wheel Drive

- Rear Wheel Drive

- All-Wheel Drive

Front wheel drive exhibits a clear dominance with a 48.5% share of the total Europe electric car market in 2025.

Front wheel drive holds the leading position within the Europe electric car market, reflecting their strong alignment with the design priorities of mass-market electric platforms. Front wheel drive (FWD) configuration delivers inherent engineering advantages, including simplified drivetrain architecture, reduced vehicle weight, and superior energy efficiency, directly improving range performance. These characteristics make front wheel drive particularly well-suited to compact and crossover body styles that account for the majority of European consumer demand, enabling automakers to offer compelling products at competitive price points across mainstream categories.

The sustained presence of front wheel drive is also supported by the decisions of automobile manufacturers that have standardized this configuration in their main high-volume electric platforms. Moreover, the use of FWD layouts in the market is beneficial in reducing complexity and optimizing costs, which is essential in ensuring accessibility in the mid-priced range. As additional electric platforms that are specifically designed with regard to consumer demand patterns in Europe are introduced in the market, the sustained presence of front wheel drive in the leading position is ensured.

Country Insights:

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

Germany leads with a market share of 24.6% of the total Europe electric car market in 2025.

Germany commands the largest country-level position within the Europe electric car market, underpinned by its stature as the continent's foremost automotive manufacturing nation. The country hosts a dense concentration of vehicle production facilities, advanced supplier networks, and engineering expertise that collectively accelerate the development and domestic rollout of electric models. Progressive emission reduction policies, evolving fleet procurement requirements, and renewed fiscal support mechanisms are stimulating both corporate and private consumer demand, reinforcing Germany's central role in driving the region's broader electrification transition.

The leadership position is also underpinned by Germany’s advanced automotive manufacturing capabilities and the high level of commitment displayed by local automotive companies towards their ambitious plans for electric vehicle rollouts. The large consumer base with high disposable incomes, coupled with improving availability of local electric models across both volume and premium segments, underpins a healthy demand landscape. Progression in urban charging points, fast-charging corridors between cities, and consumer familiarity with electric vehicle ownership are all removing barriers to adoption, ensuring that Germany’s leading position is maintained and extended through the forecast period.

Market Dynamics:

Growth Drivers:

Why is the Europe Electric Car Market Growing?

Rising Environmental Awareness and Evolving Consumer Preferences

A fundamental shift in consumer values is serving as a powerful growth driver across the Europe electric car market. Growing public awareness of climate change, urban air quality challenges, and the environmental consequence of conventional transportation is actively motivating purchase decisions toward cleaner alternatives. As per sources, a Europe‑wide survey of 8,000+ consumers showed nearly three in five respondents likely to own an EV by 2030, with younger demographics showing stronger intent. Younger demographics are demonstrating strong preference for sustainable mobility solutions, influencing broader household purchasing behavior.

Accelerating Corporate Fleet Electrification

The electrification of corporate vehicle fleets represents a significant and expanding demand driver within the Europe electric car market. Organizations across diverse sectors are integrating EVs into their sustainability strategies, responding to investor expectations, emissions reporting obligations, and internal decarbonization commitments. In 2026, a new EU Fleets Law study found corporate fleet electrification targets could deliver up to 57% of the electric vehicle sales needed to meet 2030 climate goals. Government procurement policies in several European countries are further mandating or incentivizing the adoption of zero-emission fleet vehicles.

Advances in Battery Technology and Energy Ecosystem Integration

Continuous innovation in battery chemistry, energy management systems, and vehicle-to-grid capabilities is materially strengthening the value proposition of EVs across Europe. Improved energy density translates into longer driving ranges without proportional increases in battery size or weight, directly addressing residual consumer concerns. The growing integration of EVs within broader renewable energy ecosystems, including smart-charging platforms and bidirectional energy exchange, is enhancing their utility beyond transportation. This deepening synergy between electric mobility and the continent's energy transition is creating compelling new ownership benefits that drive sustained consumer interest.

Market Restraints:

What Challenges the Europe Electric Car Market is Facing?

High Upfront Purchase Costs in Entry-Level Segments

Despite declining battery costs, EVs continue to carry a significant price premium over comparable internal combustion engine alternatives across many mainstream segments. This cost gap remains a material barrier for budget-conscious consumers, particularly in markets where government purchase subsidies have been reduced or eliminated. The persistence of elevated entry-level pricing slows the pace of adoption among middle-income households and limits penetration in markets with lower average disposable incomes.

Uneven Charging Infrastructure Across Regions

The distribution of charging infrastructure across Europe remains deeply unequal, with significant disparities between well-equipped western markets and underdeveloped networks in parts of Eastern Europe and rural regions. Consumers in areas with limited public charging access face practical constraints that dampen purchasing with intent. Addressing this imbalance requires substantial coordinated investment, policy alignment, and private sector participation across member states to ensure equitable charging access and sustain broader adoption momentum.

Consumer Uncertainty and Residual Concerns About Electric Mobility

A proportion of European consumers continues to exhibit hesitation toward EV adoption, driven by concerns about battery longevity, uncertainty surrounding used vehicle residual values, and perceived complexity around home and public charging arrangements. Evolving policy environments and occasional reversals of government incentive programs introduce additional uncertainty, complicating long-term purchase decisions for prospective buyers. Building sustained consumer confidence requires consistent and transparent communication of EV benefits alongside stable, predictable policy frameworks.

Competitive Landscape:

The Europe electric car market is characterized by a highly dynamic and intensely competitive landscape, with established domestic automotive groups competing alongside global manufacturers and new entrants across all price segments. Domestic manufacturers have invested heavily in dedicated EV platforms, battery supply chain integration, and strategic partnerships with energy providers to strengthen their market positions. The competitive environment is further shaped by the growing presence of international entrants offering competitively priced electric models with advanced technology. Rivalries are intensifying across both premium and mass-market tiers, with manufacturers differentiating through range performance, digital connectivity, ownership cost, and charging network accessibility. Consolidation of compliance pools and strategic industrial alliances are emerging as key competitive mechanisms shaping the market's evolving structure.

Europe Electric Car Market News:

- In March 2026, Mercedes‑Benz unveiled all‑electric VLE, replacing the EQV and built on the VAN.EA platform. It features up to 435‑mile range, 115 kWh battery, ultra‑fast 800 V charging, modular five-to-eight passenger seating, and optional Vehicle-to-Grid functionality, marking a significant step in luxury and commercial electric van innovation in Europe.

Europe Electric Car Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Battery Electric Vehicle, Plug-In Hybrid Electric Vehicle, Fuel Cell Electric Vehicle |

| Vehicle Classes Covered | Mid-Priced, Luxury |

| Vehicle Drive Types Covered | Front Wheel Drive, Rear Wheel Drive, All-Wheel Drive |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Electric Car Market Report

The Europe electric car market size was valued at USD 47.1 Billion in 2025.

The Europe electric car market is expected to grow at a compound annual growth rate of 9.9% from 2026-2034 to reach USD 109.0 Billion by 2034.

Battery Electric Vehicle held the largest Europe electric car market share, driven by stringent emission regulations compelling automaker electrification, expanding model availability across price segments, and growing consumer preference for zero-emission mobility solutions throughout the continent.

Key factors driving the Europe electric car market include stringent emission regulations compelling automaker electrification, rapid expansion of charging infrastructure, declining battery costs improving vehicle affordability, and growing consumer preference for sustainable mobility solutions across the continent.

Major challenges include high upfront vehicle costs, limited charging infrastructure in remote areas, inconsistent government incentives, long battery replacement times, supply chain constraints, and low consumer awareness about electric mobility benefits.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade