Europe Esports Market Size, Share, Trends and Forecast by Revenue Model, Platform, Games, and Region, 2026-2034

Europe Esports Market Size, Share, Trends & Forecast (2026-2034)

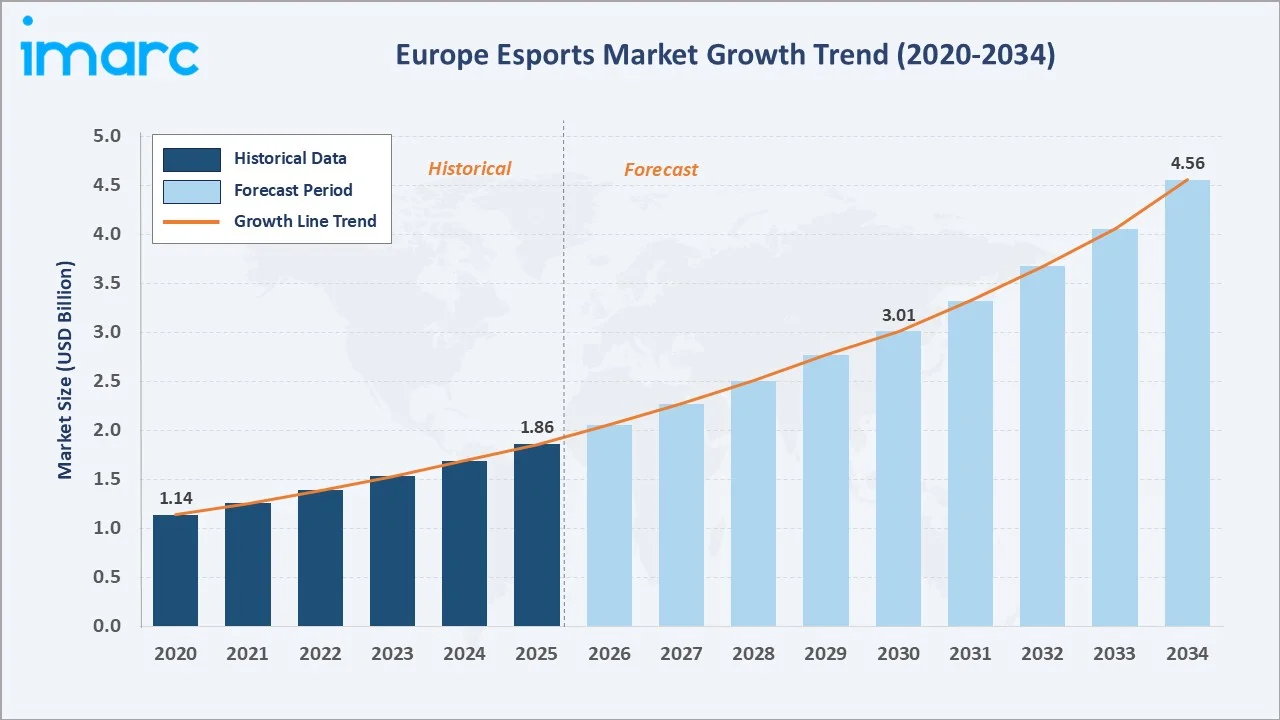

The Europe esports market size reached USD 1.86 Billion in 2025 and is projected to reach USD 4.56 Billion by 2034, exhibiting a CAGR of 10.17% during 2026-2034. Escalating sponsorship investment, expanding digital viewership, rising professionalization, and rapid mobile gaming adoption are the primary growth engines.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.86 Billion |

|

Forecast Market Size (2034) |

USD 4.56 Billion |

|

CAGR (2026-2034) |

10.17% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

The Europe esports market growth trajectory from 2020 through 2034, with historical expansion to USD 1.86 Billion in 2025, reflects consistent demand from digital viewership, sponsorship growth, and tournament proliferation, while the forecast to USD 4.56 Billion by 2034 is driven by mobile esports and 5G adoption.

To get more information on this market, Request Sample

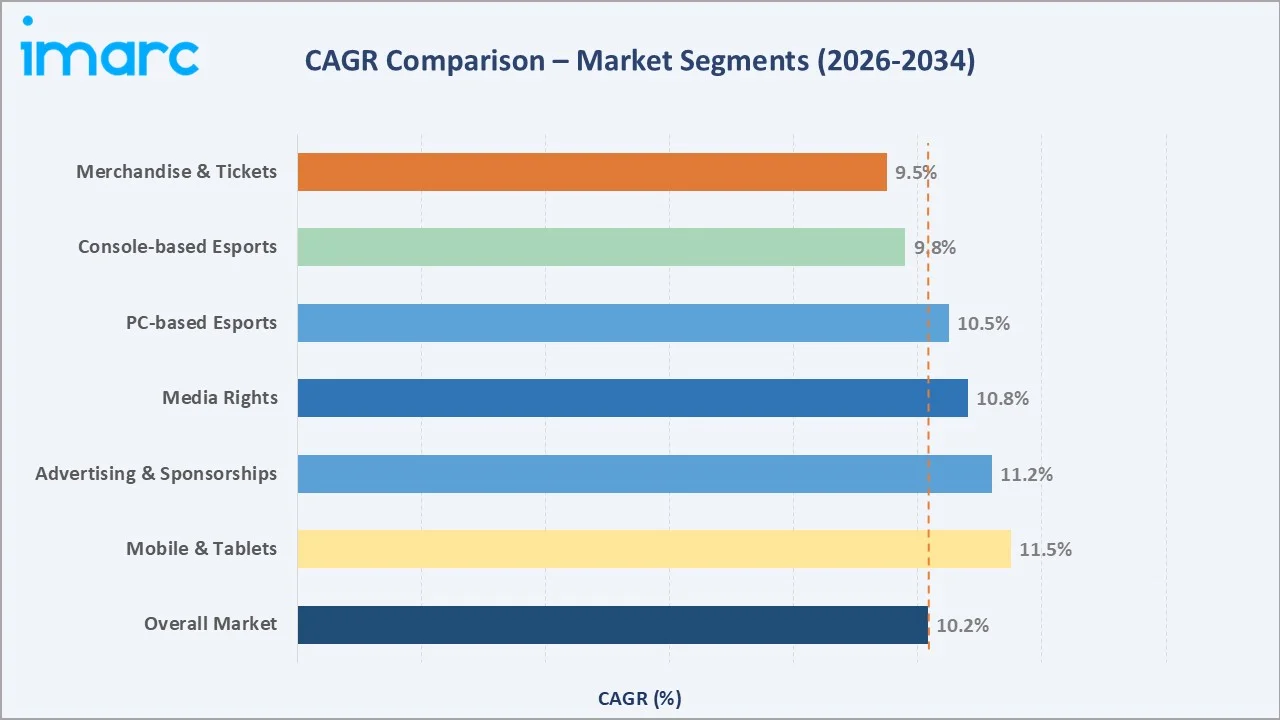

CAGR trajectories across key revenue model and platform sub-segments, with mobile and tablets at ~11.5% CAGR and advertising & sponsorships at ~11.2% CAGR, represent the fastest-growing segments within the European esports landscape through 2034.

Executive Summary

The Europe esports market is on a sustained growth trajectory from USD 1.86 Billion in 2025 to USD 4.56 Billion by 2034. Esports have evolved from niche online communities to a mainstream entertainment and media industry commanding premium sponsorship rates, dedicated broadcast deals, and significant infrastructure investment across Europe.

Advertising and sponsorships dominate revenue model at 38.4% in 2025, driven by non-endemic brands such as BMW, Red Bull, and Mastercard entering the space targeting young digital-native audiences. Media rights at 28.6% are growing as national broadcasters and streaming platforms compete for exclusive tournament content.

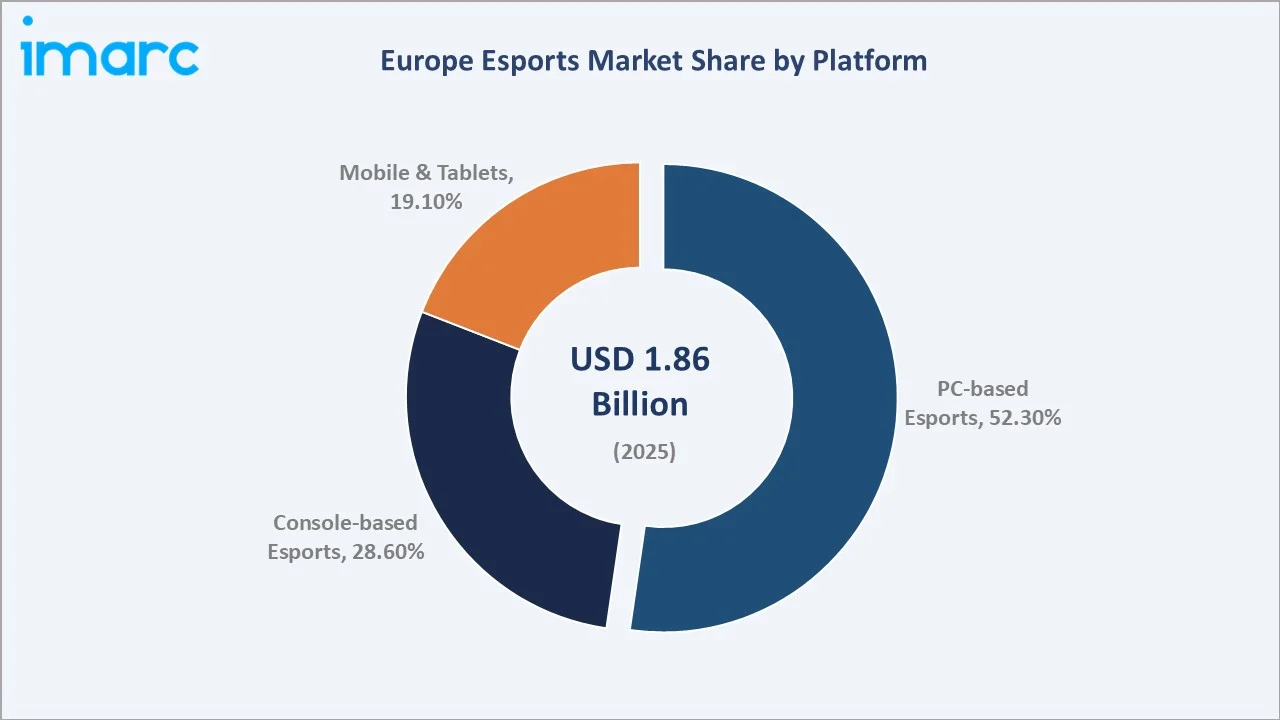

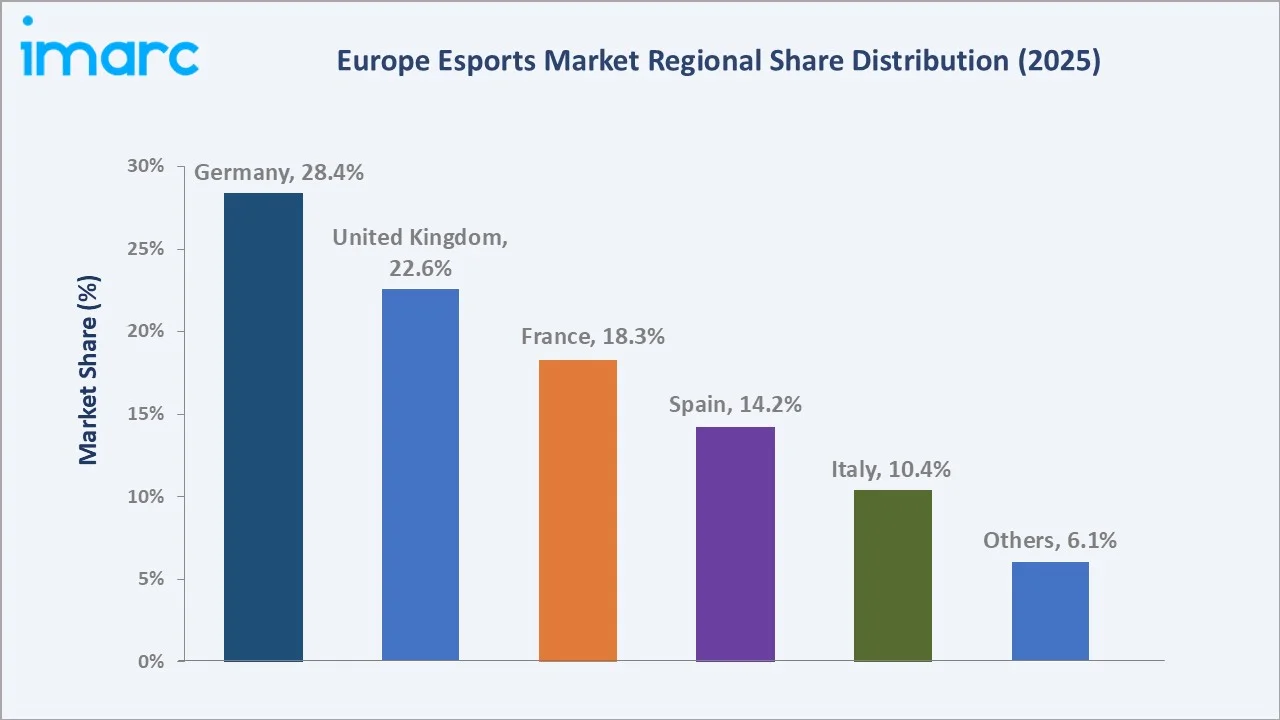

PC-based esports commands 52.3% platform share in 2025, reflecting Europe's strong PC gaming heritage and established competitive titles. Germany leads with 28.4% country share, hosting major tournaments including ESL Pro League events, reflecting robust digital infrastructure and government support.

Key Market Insights

|

Insight |

Data |

|

Leading Revenue Model |

Advertising & Sponsorships – 38.4% share (2025) |

|

Second Revenue Model |

Media Rights – 28.6% share (2025) |

|

Leading Platform |

PC-based Esports – 52.3% share (2025) |

|

Leading Country |

Germany – 28.4% country share (2025) |

|

Second Country |

United Kingdom – 22.6% country share (2025) |

Key Analytical Observations Expanding On The Above Data:

- Advertising and sponsorships, with 38.4% in 2025, dominates because non-endemic brands recognize esports as the most cost-effective channel to reach 18–34-year-old digital audiences. Corporate partnerships with tournament organizers grew 22% year-over-year in 2024.

- Media rights at 28.6% in 2025 reflect accelerating broadcaster competition for exclusive content. Twitch, YouTube Gaming, and national platforms are investing heavily in long-form tournament broadcasting rights across League of Legends, Valorant, and CS2.

- PC-based esports at 52.3% in 2025 maintains dominance through Europe's deeply embedded gaming culture. Professional competitive titles including CS2, League of Legends, and Valorant are optimized for PC hardware, sustaining tournament scale and viewership.

- Germany's 28.4% dominance reflects its position as Europe's largest esports hub, hosting ESL FACEIT Group headquarters, DreamHack, and benefiting from EUR 50 million in government digital infrastructure investment supporting competitive gaming ecosystems.

Europe Esports Market Overview

Esports represent the intersection of competitive gaming, digital media, and live entertainment, encompassing professional tournaments, franchised leagues, player development academies, streaming ecosystems, and branded content partnerships. The European market operates through a multi-layered structure of game publishers, tournament organizers, team operators, broadcast platforms, and hardware providers.

The European ecosystem integrates game publishers such as Riot Games and Electronic Arts, professional tournament organizers including ESL FACEIT Group and Gfinity, esports organizations such as Fnatic and G2 Esports, streaming platforms, sponsorship networks, and fan engagement communities across Germany, UK, France, Spain, and Italy.

Market Dynamics

To evaluate market opportunities, Request Sample

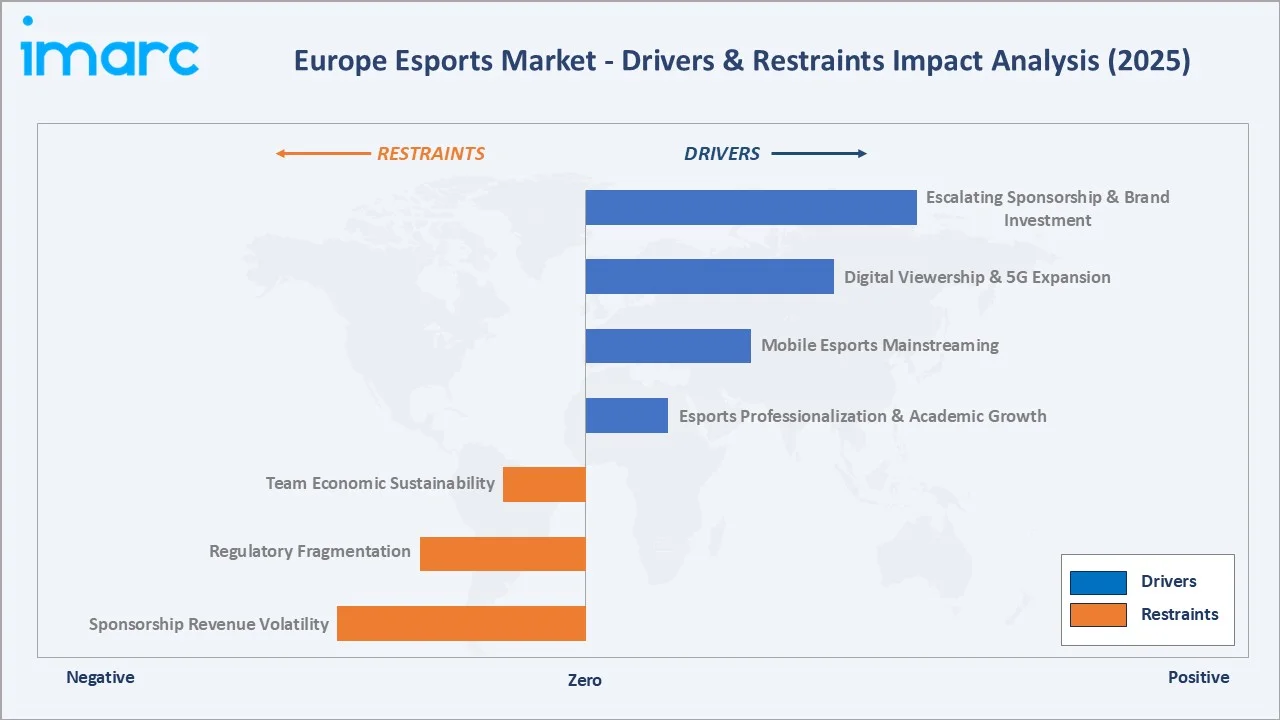

Market Drivers

- Escalating Sponsorship and Brand Investment: European corporations across technology, automotive, and consumer goods sectors are recognizing esports as a high-engagement advertising platform targeting 18-34 demographics. MOUZ's new Hamburg headquarters in 2024 exemplifies the infrastructure investment surge transforming European esports professionalization.

- Digital Viewership Expansion and 5G Adoption: As per various research, over £7.6 billion were spent on video games by UK consumers in 2024, signalling accelerating digital engagement. 5G network expansion is broadening access to live tournament streams and enabling mobile esports at unprecedented quality levels across European markets.

- Professionalization and Academic Programs: British Esports launched student PUBG Mobile tournaments in 2024 with 16 competing teams, reflecting deepening integration of esports into educational frameworks. Growing player salary structures are attracting traditional sports capital into European esports organizations.

Market Restraints

- Sponsorship Revenue Volatility: Sponsorship revenue in esports has become increasingly unstable as broader shifts in digital advertising have led major brands like Intel and Mastercard to scale back their involvement. This has resulted in reduced brand investment and the loss of key partnerships, creating financial uncertainty for organizations that rely heavily on sponsorship-driven income. As a result, esports companies are facing greater pressure to diversify their revenue streams and reduce dependence on a few large sponsors.

- Regulatory Fragmentation: Non-EU players historically required country-specific work permits for each tournament, creating operational complexity. While the European Parliament's 2025 non-binding resolution urges harmonization, enforcement fragmentation continues to constrain international roster flexibility.

Market Opportunities

- Mobile Esports Monetization: The mobile esports segment is establishing itself as a primary revenue driver globally, with the M7 World Championship in Jakarta attracting Red Bull as an official partner. European mobile gaming audience expansion creates significant monetization opportunities for tournament operators across the region.

- Blockchain and Digital Asset Integration: Non-fungible token ecosystems enabling verified in-game item ownership are creating recurring royalty revenue streams. Riot Games secured a US patent in August 2025 covering blockchain-verified item ownership, with European Securities and Markets Authority regulatory clarity improving investment confidence.

Market Challenges

- Team Sustainability and Player Retention: Team sustainability and player retention have become growing concerns in esports, as many organizations struggle to maintain financially viable operations. Structural challenges within franchise models have made it difficult for teams to achieve consistent profitability, prompting publishers like Riot Games to revisit compensation frameworks and cost structures. These pressures have also led to downsizing and consolidation across leagues, affecting overall ecosystem stability. As a result, teams are finding it harder to retain talent, with increased player turnover and uncertainty around long-term contracts.

- Audience Fragmentation Across Platforms: Viewership is dispersed across Twitch, YouTube, proprietary publisher platforms, and national broadcasters, complicating audience measurement and sponsor ROI attribution. Inconsistent metrics frameworks reduce advertiser confidence and constrain premium sponsorship pricing.

Emerging Market Trends

1. AR/VR Integration Transforming Live Tournament Experiences

Augmented and virtual reality technologies are transforming how European audiences experience esports events. Tournament organizers are deploying AR overlays for broadcast enhancement and VR spectator modes allowing remote fans to experience arenas immersively, driving new premium subscription and ticket revenue streams across the region.

2. Franchise League Models Attracting Traditional Sports Capital

Permanent franchise slots in leagues such as the League of Legends EMEA Championship eliminate relegation risk, enabling institutional investment frameworks comparable to traditional sports franchises. European private equity is increasingly evaluating esports team investments using franchise-adjusted valuation multiples for long-term positioning.

3. AI-Powered Coaching and Performance Analytics

AI coaching tools are becoming standard across European professional esports organizations, with startups receiving funding from innovation programs. Performance analytics platforms processing player data in real-time are improving training efficiency and reducing the talent development timeline for emerging European competitors.

4. Mobile Esports Scaling to Mainstream Competitive Tier

British Esports' 2024 student PUBG Mobile tournament demonstrates mobile's entry into structured competitive frameworks. As 5G infrastructure matures across Europe, mobile esports viewership and participation are expected to narrow the gap with PC esports by 2028, expanding the overall audience addressable market significantly.

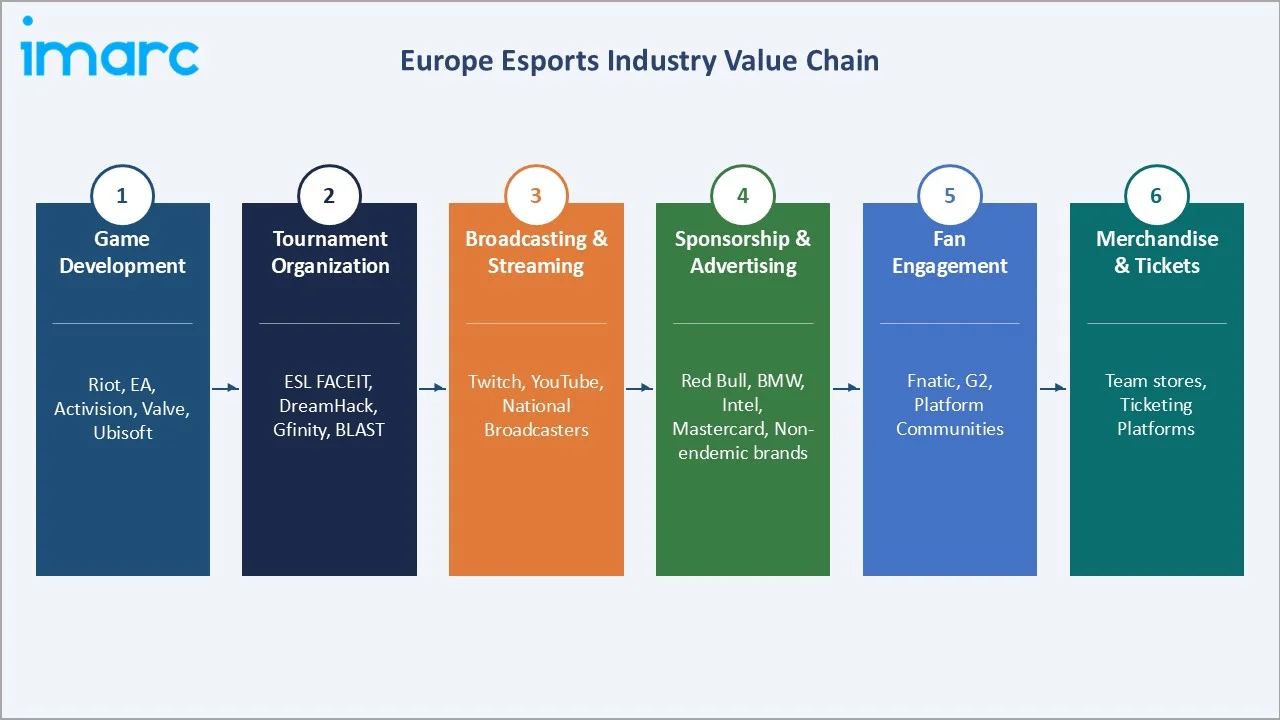

Industry Value Chain Analysis

The esports value chain spans six stages from game development through merchandise and tickets, with tournament organization and broadcasting capturing the highest value-add margins. Publishers retain intellectual property leverage, while tournament organizers and streaming platforms capture audience monetization through media rights and advertising revenue.

Integrated tournament operators with owned streaming infrastructure and multi-title publisher partnerships, maintain structurally superior positions.

|

Stage |

Key Players / Examples |

|

Game Development |

Riot Games, Electronic Arts, Activision Blizzard, Valve Corporation, Ubisoft Entertainment |

|

Tournament Organization |

ESL FACEIT Group, BLAST |

|

Broadcasting & Streaming |

Twitch (Amazon), YouTube Gaming (Alphabet), national public broadcasters |

|

Sponsorship & Advertising |

Red Bull, BMW, Mastercard, endemic and non-endemic brand partners |

|

Fan Engagement |

Fnatic, G2 Esports, NAVI, platform communities, digital ticketing providers |

|

Merchandise & Tickets |

Team stores, licensed apparel, event ticketing platforms across Europe |

Technology Landscape in the Europe Esports Industry

Streaming and Broadcasting Infrastructure

Content delivery network optimization and adaptive bitrate streaming are enabling simultaneous broadcasts to millions of concurrent European viewers. Low latency streaming protocols reducing end-to-end delay below 2 seconds are becoming standard for major tournament broadcasts, critically improving live audience engagement metrics and advertiser measurement capabilities.

Cloud Gaming and Edge Computing

Cloud gaming platforms are reducing hardware barriers to competitive play, potentially expanding European esports participation by reaching audiences without dedicated gaming PCs or consoles. Edge computing infrastructure deployed by major European telecom operators is reducing latency for cloud-rendered competitive gaming to viable competitive thresholds.

AI and Data Analytics Platforms

Machine learning platforms processing real-time gameplay telemetry are transforming coaching methodologies across European professional teams. Automated clip generation, performance heatmapping, and opponent behavior prediction tools are becoming standard technology investments for organizations competing at tier-one European tournament levels.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Revenue Model |

Advertising and Sponsorships |

38.4% |

2025 |

|

Platform |

PC-based Esports |

52.3% |

2025 |

|

Games |

🔒 |

🔒 |

2025 |

| Country |

Germany |

28.4% |

2025 |

By Revenue Model

Advertising and sponsorships command a 38.4% majority share in 2025, driven by the structural advantage of esports as a direct channel to 18–34-year-old digital audiences that have largely abandoned traditional television. Non-endemic brands are allocating increasing proportions of digital marketing budgets to esports, attracted by documented audience quality metrics.

To access detailed market analysis, Request Sample

Media rights at 28.6% in 2025 represent the fastest-institutionalizing revenue stream, with broadcasters competing for exclusive viewing windows. Merchandise and tickets at 22.4% benefit from growing live event attendance, with European tournament venues increasingly selling out major CS2, League of Legends, and Valorant championship events.

By Platform

PC-based esports dominate the platform segment at 52.3% in 2025, representing Europe's most established competitive infrastructure. High-performance PC hardware, precision input peripherals, and dedicated gaming monitors define the professional competitive standard across titles including CS2, League of Legends EMEA Championship, and Valorant Champions Tour EMEA.

Console-based esports at 28.6% in 2025 are supported by EA SPORTS FC competitive leagues and fighting game circuits including the European Street Fighter League. Mobile and tablets at 19.1% are growing fastest, driven by PUBG Mobile, Mobile Legends, and Clash Royale competitive ecosystems gaining European tournament infrastructure.

Regional Market Insights

Germany's 28.4% market dominance in 2025 is driven by hosting ESL FACEIT Group's headquarters in Hamburg, DreamHack events, and EUR 50 million government digital infrastructure investment. Germany's regulatory environment increasingly recognizes esports as a legitimate competitive activity, supporting professional player frameworks and visa structures for international competitors.

United Kingdom at 22.6% in 2025 benefits from over 2,000 registered gaming companies and Gfinity's domestic tournament infrastructure. France at 18.3% is experiencing growth through Ubisoft's Rainbow Six ecosystem and government support for competitive gaming. Spain at 14.2% and Italy at 10.4% are developing strong grassroots scenes with growing tournament hosting ambitions.

Competitive Landscape

The Europe esports market is highly competitive, with game publishers, tournament organizers, and esports teams competing for audience engagement and sponsorship revenues. Companies focus on content innovation, global partnerships, and digital platform expansion to strengthen market presence. Increasing collaborations between brands, media companies, and esports organizations are shaping competitive dynamics.

|

Company Name |

Key Products |

Market Position |

European Strategic Focus |

|

Electronic Arts Inc. |

NHL 26, FC26, MADDEN 26, Battlefield 6 |

Leader |

Publisher-controlled leagues; media rights ownership; cross-media brand partnerships |

|

ESL FACEIT GROUP |

ESL Pro League (CS2), FACEIT platform, Dreamhack platform |

Leader |

Europe premier organizer; 287M social fans; multi-title portfolio; sponsor diversification |

|

Fnatic Ltd |

CS2, League of Legends, Valorant |

Challenger |

Pan-European team brand; cross-title rosters; merchandise and content monetization |

|

Riot Games, Inc. |

League of Legends (LEC), Valorant (VCT EMEA), Wild Rift, Teamfight tactics, 2XKO |

Leader |

Publisher-owned franchise leagues; European regional championships |

|

Tencent |

PUBG Mobile, Honor of Kings |

Leader |

Mobile esports titles; European mobile gaming audience; cross-platform digital content |

|

Ubisoft Entertainment |

Rainbow Six Siege esports, For Honor competitive circuit |

Challenger |

European HQ advantage; Rainbow Six EU league; endemic brand partnerships across EMEA |

|

Valve Corporation |

CS2 (Counterstrike 2), Dota 2 |

Leader |

Community-driven tournament model; Steam platform ecosystem; Major event prize pool structure |

Key players include Electronic Arts Inc., ESL FACEIT GROUP, Fnatic Ltd, Riot Games, Inc., Tencent, Ubisoft Entertainment, Valve Corporation, and others.

Key Company Profiles

Riot Games, Inc.

Riot Games is the publisher of League of Legends and Valorant, the two most-watched esports titles in Europe. Its Valorant Champions Tour EMEA and League of Legends EMEA Championship create the foundational competitive calendar around which European esports sponsorship, media rights, and team investment are structured globally.

- Product Portfolio: League of Legends, Valorant, Teamfight Tactics, Wild Rift, and associated competitive esports league structures including VCT EMEA and LEC across Europe.

- Recent Developments: In April 2026, Riot Games announced a major overhaul of the Valorant Champions Tour (VCT) starting in 2027, shifting toward a more open, tournament-focused ecosystem. The new structure replaces the traditional league and franchise-heavy model with a system centered on frequent competitions, including open qualifiers that allow any team to compete for top-tier events

- Strategic Focus: Riot Games' esports strategy focuses on building sustainable franchise league economics through shared revenue models and reducing reliance on publisher subsidies, while growing viewership and improving sponsorship quality metrics across European competitive circuits.

ESL FACEIT Group

ESL FACEIT Group operates as Europe's premier esports organizer headquartered in Germany, delivering competitive experiences through brands including ESL, FACEIT, and DreamHack.

- Product Portfolio: ESL Pro League (CS2), Intel Extreme Masters, FACEIT community platform, DreamHack AB events, and others

- Recent Developments: In January 2022, ESL Gaming and FACEIT announced a merger to form the ESL FACEIT Group, bringing together their complementary strengths to create a unified and comprehensive platform for competitive gaming. The combined entity aims to offer an end-to-end ecosystem that supports players, teams, developers, and publishers, covering everything from grassroots competitions to large-scale esports events.

- Strategic Focus: ESL FACEIT Group's strategy centers on converting Intel sponsorship revenue losses into diversified partnership portfolios while scaling FACEIT's community platform to create sustainable recurring revenue independent of single-title prize pool events.

Electronic Arts Inc.

Electronic Arts is a leading global interactive entertainment publisher with significant European esports presence through EA SPORTS FC competitive leagues, which replaced FIFA esports after the licensing transition

- Product Portfolio: EA SPORTS FC competitive league, Apex Legends Global Series, Battlefield esports initiatives, and EA SPORTS FC Mobile competitive formats targeting European and global audiences.

- Recent Developments: In October 2025, Electronic Arts partnered with Stability AI to explore the use of generative AI in game development. The collaboration focuses on leveraging advanced AI models to enhance creative workflows, enabling developers to produce game content more efficiently while maintaining high-quality standards. Through this partnership, EA aims to integrate AI-driven tools into its development pipeline to support areas such as design, storytelling, and asset creation. The initiative reflects a broader effort to innovate how games are built, while also emphasizing responsible and ethical use of AI technologies within the gaming industry.

- Strategic Focus: EA focuses on monetizing esports through direct publisher-controlled league structures rather than third-party organizers, enabling tighter control over branding, broadcast rights, and sponsorship revenue allocation across European and global markets.

Market Concentration Analysis

The Europe esports market is highly competitive at the publisher level, with Riot Games and Activision Blizzard controlling the two dominant viewer-hours titles. Tournament organization is consolidating, with ESL FACEIT Group's acquisition by Savvy Games Group for USD 1.5 billion in January 2024 creating a structurally dominant operator across European esports infrastructure.

Consolidation at the team and organization level is less advanced. Fnatic, G2 Esports, and NAVI maintain strong brand recognition and cross-title rosters but lack the structural barriers available to publisher-controlled or tournament-operator entities. Investor appetite for team consolidation remains cautious following 2022-2024 valuation corrections across the sector.

Investment & Growth Opportunities

Fastest-Growing Segments

Mobile and tablets esports at ~11.5% CAGR through 2034 is the highest-growth platform segment, driven by 5G infrastructure maturation across Europe and expanding smartphone gaming demographics. Tournament infrastructure for mobile-native titles is under-built relative to audience demand, creating investment opportunities in dedicated mobile event production facilities.

Emerging Markets

Southern and Eastern European markets including Spain, Italy, Poland, and the Netherlands are growing fastest within Europe, supported by expanding digital infrastructure, government esports recognition programs, and young demographic profiles. Spain and Italy combined represent over 24% of Europe's incremental esports growth opportunity through 2034.

Venture & Investment Trends

Traditional sports organizations including European football clubs are investing in esports roster slots within EA SPORTS FC competitive leagues, leveraging existing fan bases for cross-promotional audience development. Private equity interest in consolidating regional tournament organizers is growing as market maturation provides clearer valuation and exit frameworks.

Future Market Outlook (2026-2034)

The Europe esports market is forecast to expand from USD 1.86 Billion in 2025 to USD 4.56 Billion by 2034 at a CAGR of 10.17%, adding USD 2.70 Billion in incremental annual market value over the forecast period. Mobile platform growth, media rights institutionalization, and sponsorship recovery will be the primary value drivers through 2034.

Three structural forces will shape the European esports landscape through 2034. First, the maturation of franchise league economics will stabilize team valuations and attract institutional capital at scale. Second, AR/VR integration will create new premium audience experiences and revenue layers beyond current advertising models. Third, EU regulatory harmonization will remove structural barriers to cross-border player mobility and tournament hosting.

Research Methodology

Primary Research

Primary research encompassed structured interviews with Europe esports stakeholders including senior commercial managers at tournament organizers, marketing executives at endemic and non-endemic sponsors, team operators, platform product managers, and regulatory advisors. Primary data collection focused on revenue model trends, platform preference shifts, and regional market dynamics.

Secondary Research

Key secondary sources include ESL FACEIT Group company disclosures, British Esports organizational reports, European Parliament legislative updates, Newzoo European esports audience data, Twitch and YouTube streaming analytics, and national gaming industry association publications from Germany, United Kingdom, and France.

Forecasting Models

Market size estimations and growth projections were derived using bottom-up revenue stream modelling incorporating sponsorship deal velocity, media rights auction outcomes, mobile gaming audience penetration rates, and macro digital advertising expenditure forecasts across European markets through 2034.

Europe Esports Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Revenue Models Covered | Media Rights, Advertising and Sponsorships, Merchandise and Tickets, Others |

| Platforms Covered | PC-based Esports, Consoles-based Esports, Mobile and Tablets |

| Games Covered | Multiplayer Online Battle Arena (MOBA), Player vs Players (PvP), First Person Shooters (FPS), Real Time Strategy (RTS) |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Electronic Arts Inc., ESL FACEIT GROUP, Fnatic Ltd, Riot Games, Inc., Tencent, Ubisoft Entertainment, Valve Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe esports market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe esports market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe esports industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Esports Market Report

The Europe esports market reached USD 1.86 Billion in 2025, reflecting strong demand from sponsorship investment, digital viewership expansion, and tournament infrastructure growth across key markets including Germany, United Kingdom, and France.

The market is projected to reach USD 4.56 Billion by 2034, growing at a CAGR of 10.17% during 2026-2034, driven by mobile esports growth, media rights institutionalization, and 5G-enabled audience expansion across the continent.

Advertising and sponsorships lead with a 38.4% share in 2025, driven by non-endemic brand entry targeting digital-native 18–34-year-old audiences and growing corporate recognition of esports as a premium and measurable advertising channel.

PC-based esports lead at 52.3% in 2025, supported by Europe's strong PC gaming heritage, established competitive titles including CS2 and League of Legends, and professional tournament infrastructure built around high-performance PC hardware standards.

Germany commands a dominant 28.4% country share in 2025, driven by hosting ESL FACEIT Group's headquarters, DreamHack events, government digital infrastructure investment, and the country's recognized position as Europe's largest esports hub.

Mobile and tablets is the fastest-growing platform at ~11.5% CAGR through 2034, driven by 5G adoption, expanding smartphone gaming demographics, and growing tournament infrastructure for PUBG Mobile and Clash Royale competitive ecosystems.

Leading companies include Electronic Arts Inc., ESL FACEIT GROUP, Fnatic Ltd, Riot Games, Inc., Tencent, Ubisoft Entertainment, Valve Corporation, and others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)