Europe Smartphone Market Size, Share, Trends and Forecast by Operating System, Display Technology, RAM Capacity, Price Range, Distribution Channel, and Country, 2026-2034

Europe Smartphone Market Size, Share, Trends & Forecast (2026-2034)

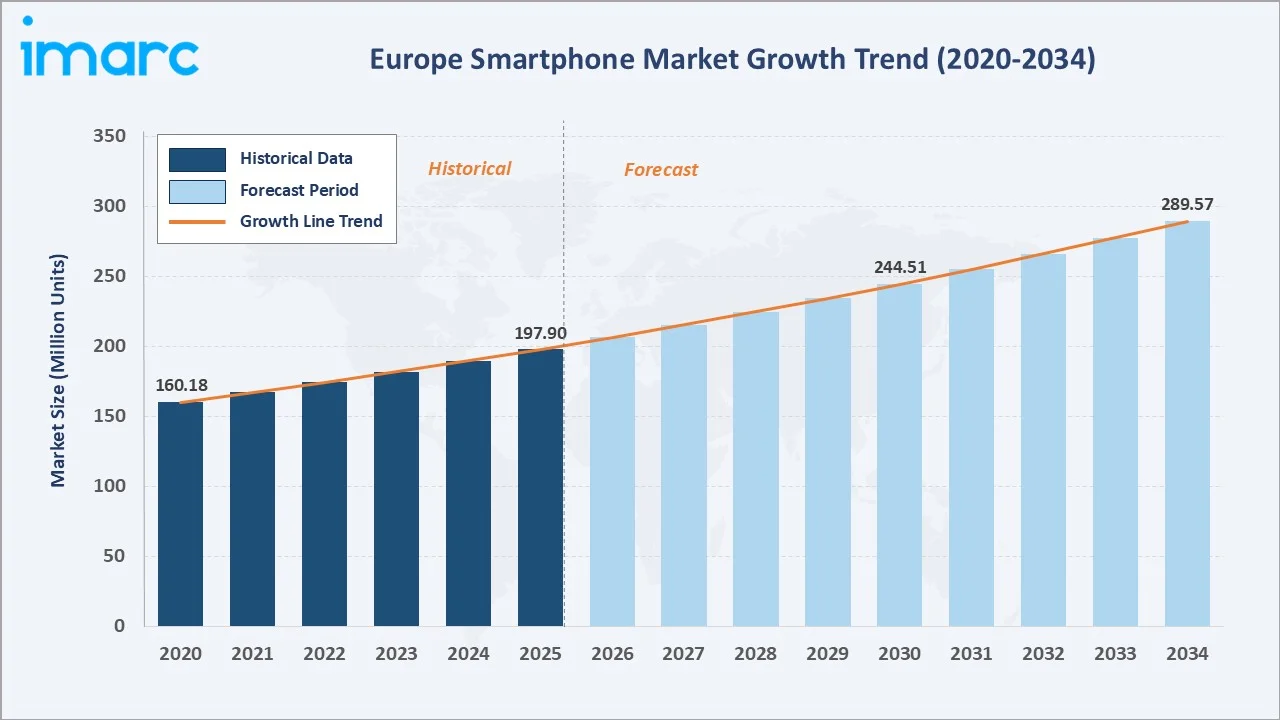

The Europe smartphone market size reached 197.90 Million Units in 2025 and is projected to reach 289.57 Million Units by 2034, exhibiting a CAGR of 4.3% during 2026-2034. Expanding 5G network coverage, accelerating premium flagship demand, AI-enabled device innovation, and growing foldable display adoption are the primary forces driving regional growth.

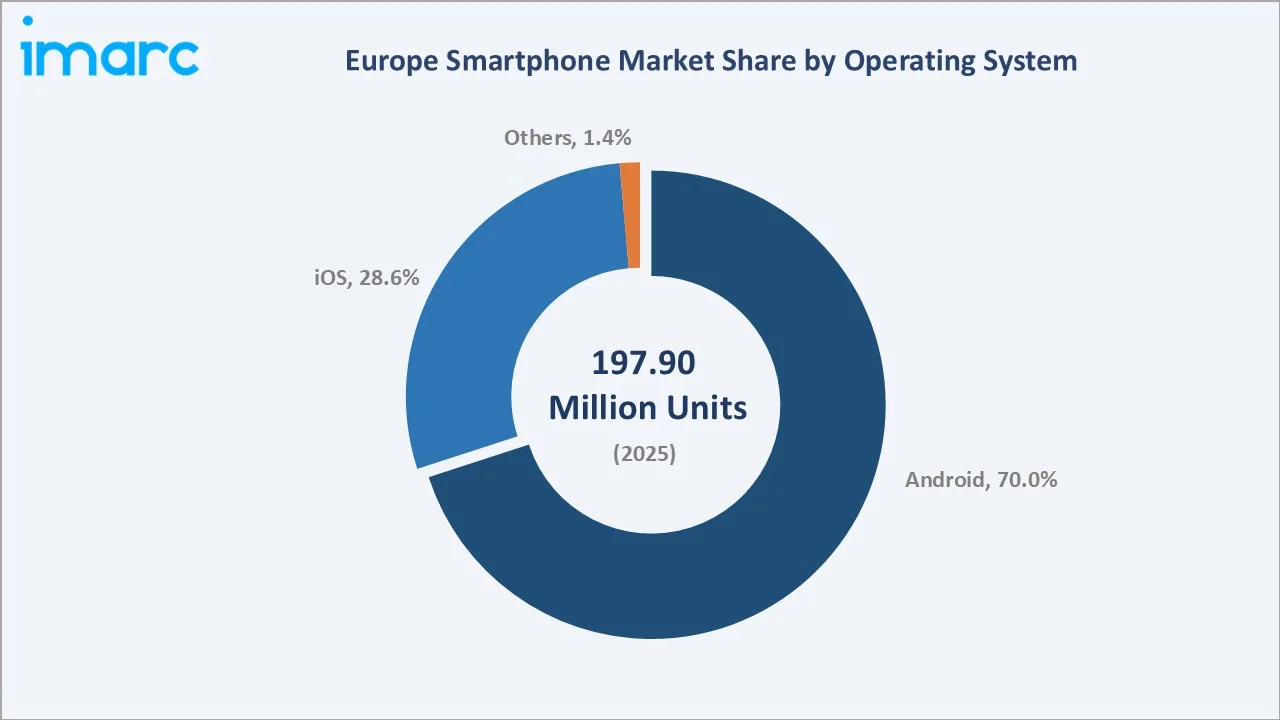

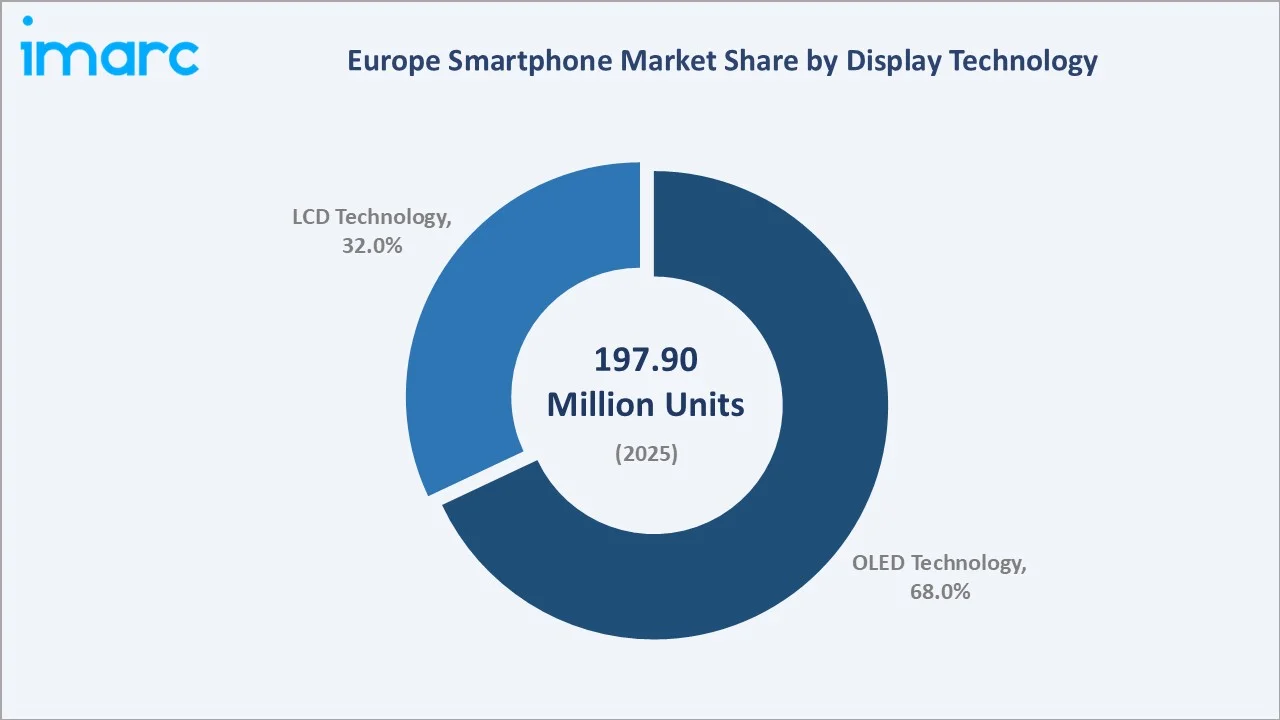

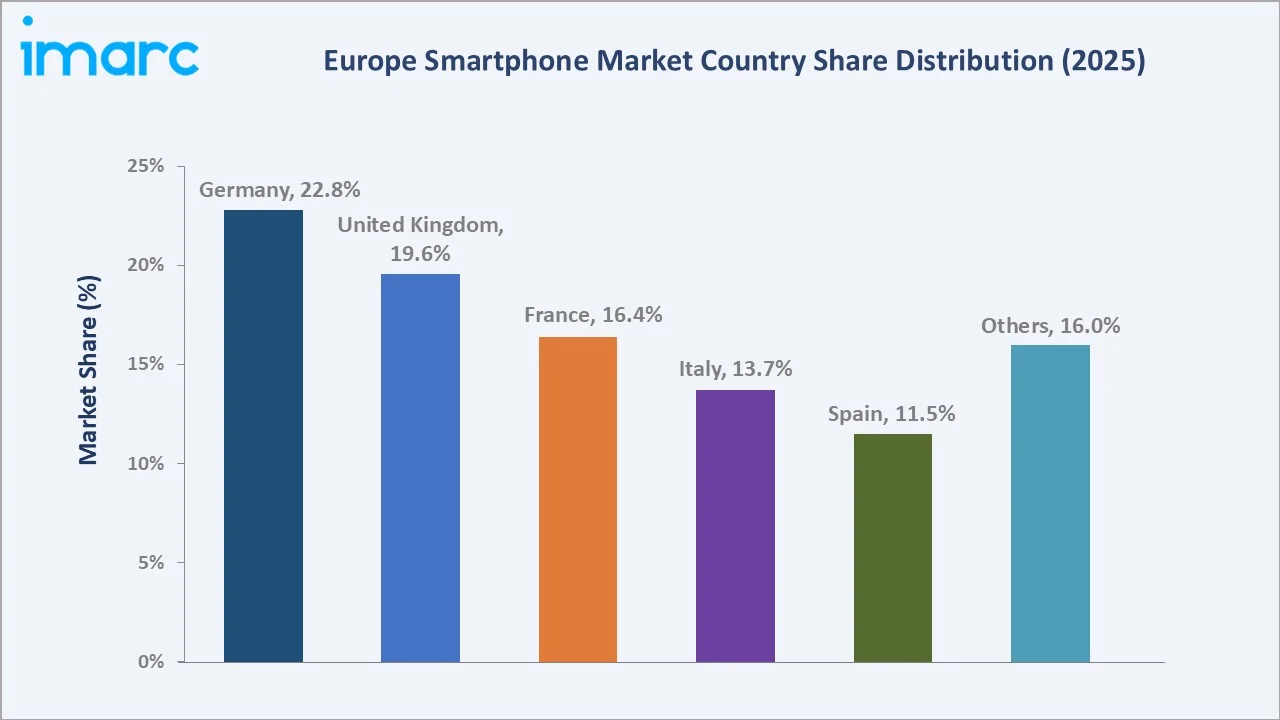

Android dominates the operating system mix at 70.0% in 2025, while OLED technology leads display segmentation at 68.0%. Germany commands the largest country share at 22.8% in 2025, reflecting strong consumer purchasing power, dense 5G infrastructure, and robust carrier-subsidized replacement demand across premium segments.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

197.90 Million Units |

|

Forecast Market Size (2034) |

289.57 Million Units |

|

CAGR (2026-2034) |

4.3% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Germany (22.8% share, 2025) |

|

Second Largest Region |

United Kingdom (19.6% share, 2025) |

|

Leading Operating System |

Android (70.0%, 2025) |

|

Leading Display Technology |

OLED Technology (68.0%, 2025) |

The Europe smartphone market trajectory from 2020 through 2034, expanding from 160.18 Million Units to 289.57 Million Units, reflects sustained 5G refresh demand, rising premium spend, and the structural transition from LCD to OLED displays across the regional installed base.

To get more information on this market, Request Sample

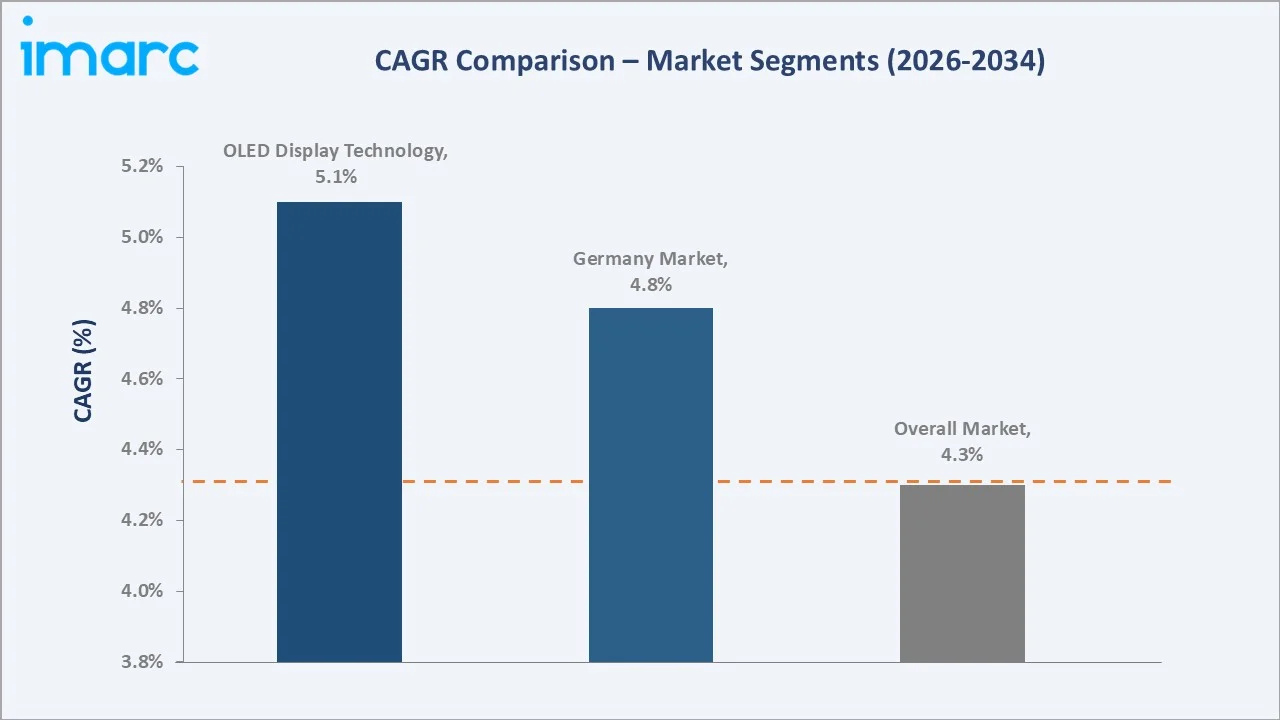

CAGR trajectories across key operating system, display technology, and Region sub-segments, with OLED displays at ~5.1% CAGR and Germany at ~4.8% CAGR, are the fastest-growing categories within the Europe smartphone industry analysis through 2034.

Executive Summary

The Europe smartphone market is on a sustained growth trajectory from 197.90 Million Units in 2025 to 289.57 Million Units by 2034. Smartphones serve as the primary computing, communication, and digital commerce device for European consumers, benefiting from structural 5G adoption and recurring upgrade cycles.

Android dominates the operating system segment at 70.0% in 2025, owing to multi-vendor ecosystem flexibility, broad price-tier coverage, and strong mid-range penetration led by Samsung, Xiaomi, and OPPO. iOS holds 28.6% share, concentrated in premium tiers where Apple's installed-base stickiness and ecosystem advantages command durable pricing power.

OLED technology leads display segmentation at 68.0% in 2025, reflecting mainstream flagship migration, thinner form factors, higher contrast ratios, and foldable architecture compatibility. LCD retains 32.0% in entry and mid-tier devices. Germany commands 22.8% in 2025, followed by the United Kingdom, France, Italy, and Spain.

Key Market Insights

|

Insight |

Data |

|

Largest Operating System |

Android - 70.0% share (2025) |

|

Leading Display Technology |

OLED Technology - 68.0% share (2025) |

|

Leading Region |

Germany - 22.8% share (2025) |

|

Second Largest Region |

United Kingdom - 19.6% share (2025) |

|

Top Companies |

Apple Inc., SAMSUNG, Xiaomi, OPPO, vivo Mobile Communication Co., Ltd., OnePlus |

Key Analytical Observations Expanding on the Above Data:

- Android, with 70.0% share in 2025, dominates because of ecosystem breadth spanning sub-EUR 200 entry devices to flagship foldables. Samsung, Xiaomi, OPPO, vivo, Motorola, and Google collectively address every European price tier, enabling carrier bundle flexibility.

- iOS, with 28.6% share in 2025, commands premium positioning in Western Europe, with Apple retaining disproportionate value share. Germany, the UK, and France concentrate iOS penetration above regional averages, reflecting higher disposable income and tight ecosystem lock-in.

- OLED technology leads at 68.0% in 2025 as Samsung Display and LG Display scale capacity, pushing OLED into the EUR 300-500 mid-tier band. Foldable formats, including Galaxy Z Fold and Flip, rely exclusively on flexible OLED panels.

- Germany's 22.8% leadership in 2025 reflects Europe's largest economy, high smartphone spends per capita, mature 5G rollout, and a concentration of carrier-subsidized refresh cycles through Deutsche Telekom, Vodafone, and Telefónica Deutschland.

Europe Smartphone Market Overview

A smartphone is a mobile device integrating cellular voice, broadband data, high-resolution display, application processing, multi-camera imaging, wireless connectivity, and application ecosystems. Product configurations are defined by operating system, display technology, form factor, chipset performance tier, camera specification, battery capacity, and 5G connectivity standard.

The regional ecosystem integrates semiconductor designers, display panel suppliers, contract manufacturers, original equipment manufacturers, operating system and software providers, distributors, mobile network operators, specialty and online retailers, and the aftermarket refurbishment channel serving value-conscious and sustainability-oriented European consumers.

Market Dynamics

To evaluate market opportunities, Request Sample

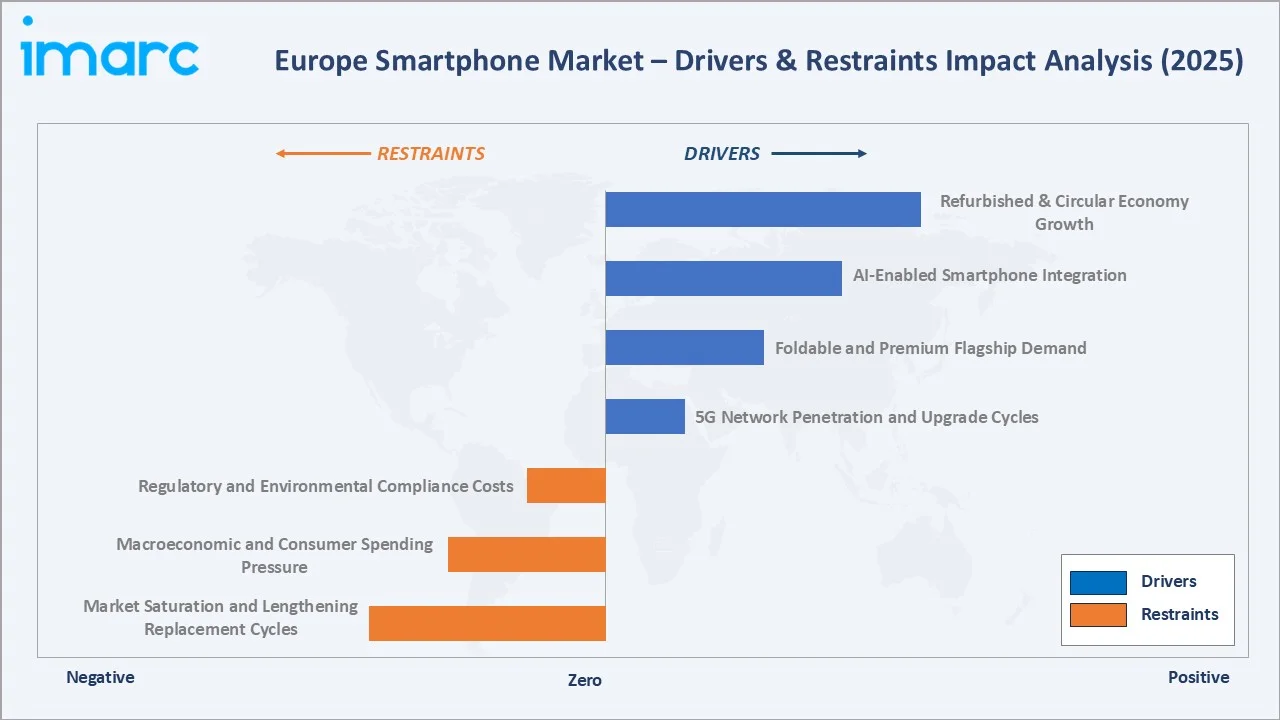

Market Drivers

- 5G Network Penetration and Upgrade Cycles: European 5G coverage has reached majority population in Germany, UK, France, Italy, and Spain, with carriers accelerating mid-band deployments. Europe boasts the highest 5G coverage, at 72% of the population. 5G-capable smartphones now dominate new sales, driving sustained replacement demand as consumers migrate from 4G devices across all price tiers.

- Foldable and Premium Flagship Demand: Demand for premium smartphones continues to rise, particularly for devices that offer innovative and differentiated form factors such as foldable designs, which are helping expand the high-end segment. Consumers are increasingly willing to pay more for advanced features, design, and overall user experience, signaling a shift toward value-driven purchasing. This momentum is supporting consistent growth in average selling prices as premium devices capture a larger share of the market. In response, manufacturers are prioritizing innovation and product differentiation to strengthen their positioning and appeal to premium-focused buyers.

- AI-Enabled Smartphone Integration: On-device generative AI features, including Samsung Galaxy AI, Apple Intelligence, and Google Gemini Nano, are creating a new purchase driver. AI capabilities require newer chipsets and higher memory configurations, incentivizing earlier-than-cycle upgrades across premium and upper mid-range European buyers.

Market Restraints

- Market Saturation and Lengthening Replacement Cycles: European smartphone penetration exceeds 80% of adults in major markets. Average replacement cycles have extended from 26 months in 2019 to over 36 months in 2025 as hardware improvements slow and consumers retain devices longer, constraining unit volume growth.

- Macroeconomic and Consumer Spending Pressure: Elevated European inflation through 2022-2024, energy-cost shocks, and cost-of-living pressures have compressed discretionary spending. Entry-tier and mid-tier buyers are trading down or extending ownership, particularly in Southern European markets where real wages have lagged headline inflation.

Market Opportunities

- Refurbished and Circular Economy Growth: The European refurbished smartphone market, led by Back Market, Swappie, and Recommerce, is growing at double-digit rates. EU sustainability directives, right-to-repair legislation, and consumer environmental awareness are mainstreaming refurbished devices across Germany, France, and the Nordics.

- Enterprise and Ruggedized Segment: Workforce digitalization across European logistics, field service, healthcare, and manufacturing is expanding the enterprise smartphone and ruggedized handset segment. Zebra, Samsung XCover, and Sonim lines are capturing specialized deployment demand with longer device lifecycles and premium support contracts.

Market Challenges

- Regulatory and Environmental Compliance Costs: The EU USB-C charger mandate, Digital Markets Act gatekeeper obligations, battery replaceability requirements, and upcoming Ecodesign rules are increasing compliance complexity. OEMs face higher engineering costs and narrow product differentiation levers across the European single market.

- Component and Supply Chain Volatility: Semiconductor allocation cycles, display panel pricing, and geopolitical exposure to Asian manufacturing hubs create margin pressure. Tariff uncertainty, shipping disruptions, and critical mineral sourcing constraints periodically affect European availability of mid-range and entry-tier smartphones.

Emerging Market Trends

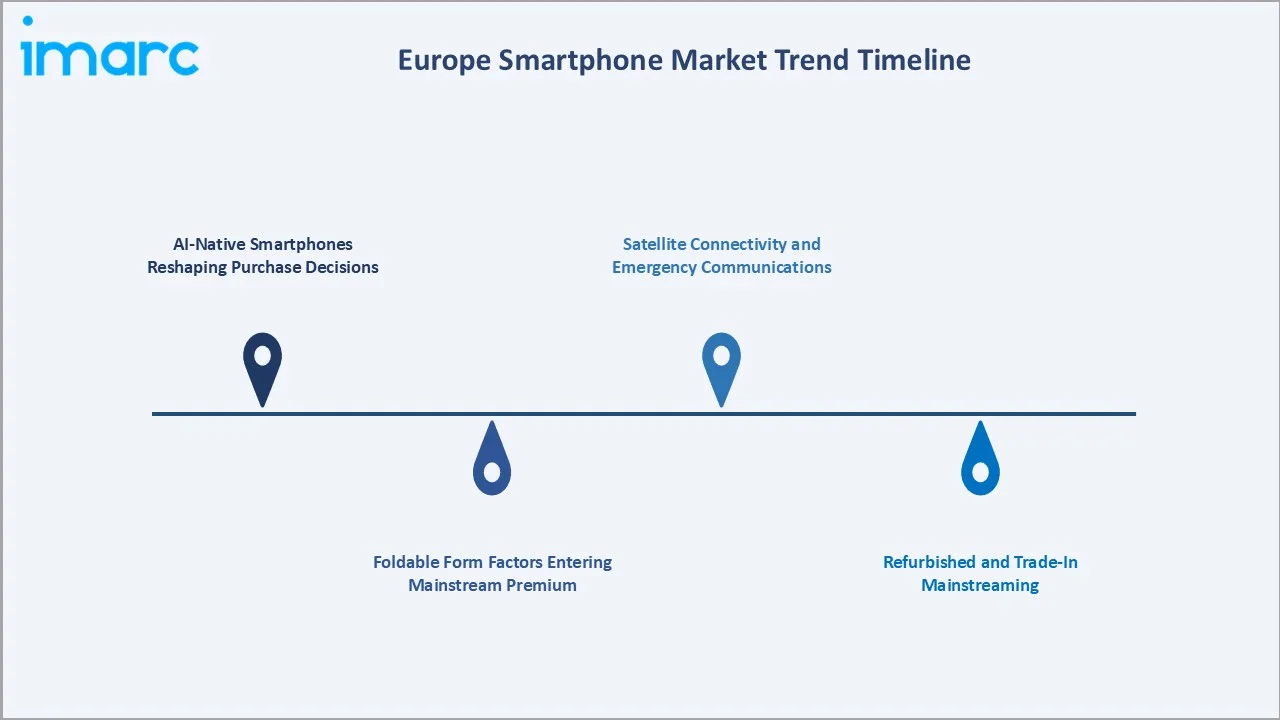

1. AI-Native Smartphones Reshaping the Purchase Decision

On-device AI is evolving from feature to platform, with Galaxy AI, Apple Intelligence, and Pixel AI powering live translation, generative imaging, and contextual assistants. European buyers increasingly evaluate handsets on NPU performance and memory, accelerating flagship and premium mid-range refresh.

2. Foldable Form Factors Entering Mainstream Premium

Foldable smartphone shipments in Europe are growing at strong double-digit rates, led by Samsung's Galaxy Z series. Pricing is declining as second-generation hinges and ultra-thin glass mature, moving foldables toward the mainstream flagship price band of EUR 1,000-1,400 in Germany and the UK.

3. Refurbished and Trade-In Mainstreaming

EU right-to-repair regulation, extended software support mandates, and dedicated marketplaces such as Back Market have normalized refurbished smartphones. Carriers across Germany, France, and the Nordics are embedding certified pre-owned devices into retail portfolios, extending device lifecycles and value recovery.

4. Satellite Connectivity and Emergency Communications

Apple Emergency SOS via satellite, Qualcomm's Snapdragon Satellite, and Mediatek NTN integration are making satellite messaging standard in flagship tiers. European alpine, maritime, and rural use cases are creating differentiated marketing angles and justifying premium positioning through 2030.

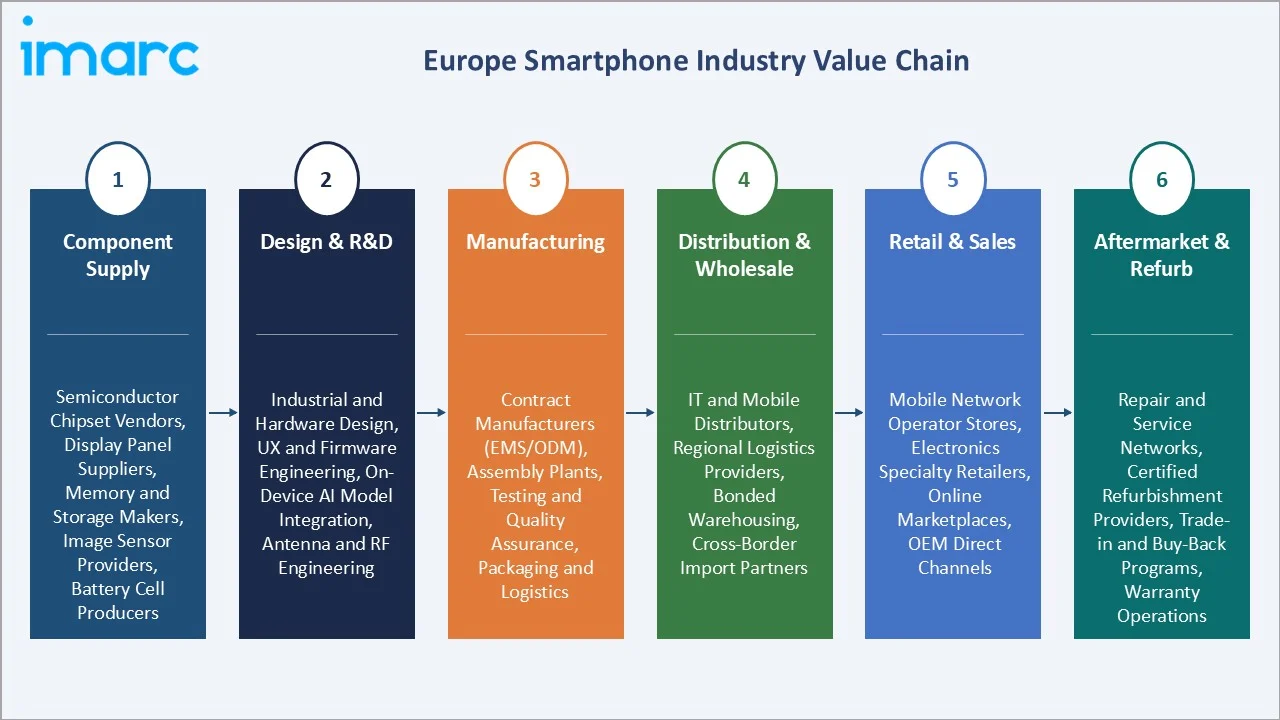

Industry Value Chain Analysis

The Europe smartphone value chain spans six stages from component supply through aftermarket service. OEM brand and software platform stages capture the highest value-add margins, while distribution and retail generate volume-driven economics across carrier and specialty channels in the regional single market.

|

Stage |

Key Players / Examples |

|

Component Supply |

Semiconductor chipset vendors, display panel suppliers, memory and storage makers, image sensor providers, battery cell producers |

|

Design & R&D |

Industrial and hardware design, UX and firmware engineering, on-device AI model integration, antenna and RF engineering |

|

Manufacturing |

Contract manufacturers (EMS/ODM), assembly plants, testing and quality assurance, packaging and logistics |

|

Distribution & Wholesale |

IT and mobile distributors, regional logistics providers, bonded warehousing, cross-border import partners |

|

Retail & Sales |

Mobile network operator stores, electronics specialty retailers, online marketplaces, OEM direct channels |

|

Aftermarket & Refurb |

Repair and service networks, certified refurbishment providers, trade-in and buy-back programs, warranty operations |

Integrated OEMs with captive display and chipset sourcing, such as Samsung's vertically aligned Display and Semiconductor divisions, and Apple's captive silicon design, achieve cost-to-performance advantages over vendors reliant on spot merchant semiconductor and panel procurement across European distribution.

Technology Landscape in the Europe Smartphone Industry

Chipset and Connectivity: 5G SA, Wi-Fi 7, and On-Device AI

The dominant chipset platforms are Apple A-series, Qualcomm Snapdragon 8 Gen/Elite, MediaTek Dimensity 9000-series, and Samsung Exynos. 5G Standalone, Wi-Fi 7, UWB, and integrated NPUs capable of running 7-10 billion parameter models on-device are redefining flagship specifications in European markets through 2027.

Display Innovation: LTPO OLED, Flexible Panels, and Peak Brightness

LTPO OLED enables 1-120Hz adaptive refresh, extending battery life while supporting always-on displays. Samsung Display and LG Display drive flexible OLED innovation for foldables, while peak brightness above 3,000 nits and Dolby Vision support are differentiating premium European flagships from mid-range alternatives.

Imaging: Computational Photography and Sensor Scale

Sony Semiconductor Solutions and Samsung ISOCELL supply most smartphone image sensors. European flagships increasingly feature 1-inch Type main sensors, variable aperture, and AI-driven computational photography pipelines developed in partnership with Leica, Hasselblad, and Zeiss to justify premium positioning against competitors.

Software and Ecosystem Continuity

Google Android 15 and Apple iOS 18 anchor platform innovation, with extended software support commitments (up to seven years from Google and Samsung) reshaping European purchase decisions. EU Digital Markets Act gatekeeper obligations are expanding third-party app store access, sideloading rights, and default app competition across iOS and Android.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Operating System | Android | 70.0% | 2025 |

| Digital Technology | OLED Technology | 68.0% | 2025 |

| RAM Capacity | 4GB - 8GB | 52.0% | 2025 |

| Price Range | Mid-Range ($200-<$400) | 40.0% | 2025 |

| Distribution Channel | Online Stores | 39.0% | 2025 |

| Country | Germany | 22.8% | 2025 |

By Operating System

Android commands a 70.0% majority share in 2025 owing to OEM breadth, price-tier coverage, and regional OEM flexibility. Samsung, Xiaomi, OPPO, vivo, Motorola, Google, and Nothing compete aggressively across entry, mid-range, and flagship tiers, enabling carrier differentiation and consumer choice across European markets.

To access detailed market analysis, Request Sample

iOS at 28.6% in 2025 concentrates in premium segments across Western and Northern Europe where Apple's installed-base loyalty, iCloud integration, and retail footprint sustain disproportionate value share. Others (1.4%) covers legacy and niche platforms, including HarmonyOS and KaiOS feature-smartphone hybrids.

By Display Technology

OLED dominates display segmentation at 68.0% in 2025, reflecting mainstream flagship and premium mid-range migration. LTPO variants extending to 1-120Hz adaptive refresh, flexible panels for foldables, and under-display camera technology are pushing OLED deeper into the EUR 400-700 tier across German, UK, and French retail channels.

LCD retains 32.0% share in 2025, concentrated in entry-tier and mid-tier devices below EUR 300. IPS LCD remains cost-competitive for budget Android handsets from Xiaomi Redmi, Motorola G-series, and Samsung Galaxy A0x lines, though panel suppliers are gradually shifting OLED capacity to erode the remaining LCD cost advantage.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Germany |

22.8% |

Largest EU economy; dense 5G; carrier subsidies; premium adoption |

|

United Kingdom |

19.6% |

High iOS penetration; carrier tradecycles; enterprise deployment |

|

France |

16.4% |

Orange/SFR/Bouygues competition; refurbished mainstreaming |

|

Italy |

13.7% |

Carrier promo intensity; mid-tier price sensitivity; 5G rollout |

|

Spain |

11.5% |

MasOrange consolidation; youth adoption; prepaid mix |

|

Others |

16.0% |

Nordics premium mix; Benelux density; CEE catch-up growth |

Germany's 22.8% dominance in 2025 reflects Europe's largest economy and highest smartphone spend per capita. Deutsche Telekom, Vodafone Germany, and Telefónica Deutschland sustain high-subsidy refresh cycles, while MediaMarkt and Saturn specialty retail drive premium and mid-tier sell-through across a digitally mature consumer base.

The United Kingdom at 19.6% in 2025 maintains elevated iOS penetration, driven by Apple's retail footprint and EE/O2/Vodafone/Three carrier subsidy intensity. France at 16.4% benefits from Orange, SFR, Bouygues Telecom, and Free Mobile competition that keeps replacement cycles comparatively active across mid-tier and flagship segments.

Italy at 13.7% and Spain at 11.5% reflect price-sensitive mid-tier demand with strong carrier promotional cycles. The remaining 16.0% aggregates the Nordics, Benelux, Switzerland, Austria, and Central and Eastern Europe, where premium mix in the North contrasts with catch-up growth in Poland, Romania, and Czechia.

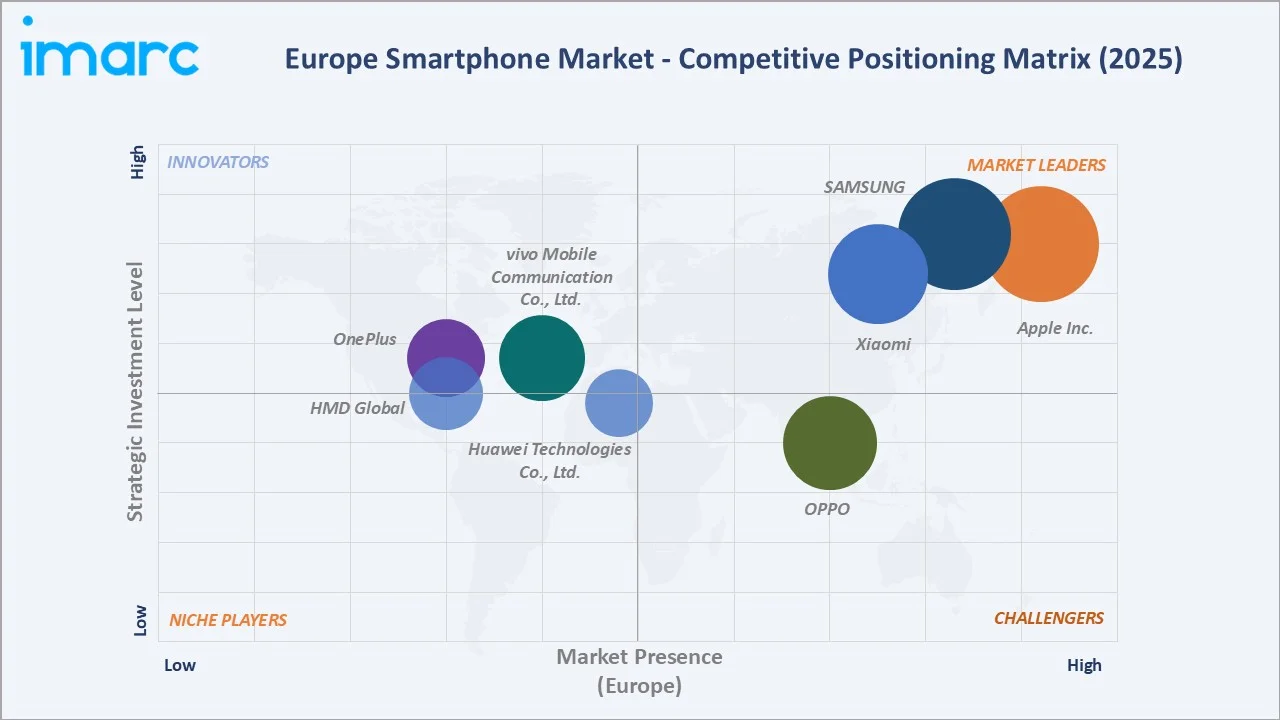

Competitive Landscape

The Europe smartphone market is moderately concentrated, with Apple and Samsung holding the leading unit and value positions, followed by Xiaomi, OPPO, vivo, Motorola, HMD Global, Google, OnePlus, and Huawei. Android OEMs compete on price-to-performance across every tier, while Apple commands premium value share.

|

Company Name |

Key Products |

Market Position |

Regional Strategic Focus |

|

Apple Inc. |

iPhone 17 series |

Leader |

Premium tier dominance; Apple Retail in Western Europe; ecosystem lock-in |

|

SAMSUNG |

Galaxy S25/S26, Galaxy Z Fold/Flip, Galaxy A series |

Leader |

Full-tier coverage; carrier partnerships; foldable leadership |

|

Xiaomi |

Xiaomi 15/17, Redmi Note, POCO |

Leader |

Price-performance mid-range; rapid European retail expansion |

|

OPPO |

Find X9, Reno series, A-series |

Challenger |

Mid-premium growth; imaging partnerships (Hasselblad) |

|

vivo Mobile Communication Co., Ltd. |

X200, V-series, Y-series |

Emerging |

Camera-led mid-premium; selective European rollout |

|

HMD Global |

HMD Skyline |

Emerging |

Finnish heritage; sustainability; repairable design |

|

OnePlus |

OnePlus 12/13, Nord series |

Emerging |

Performance-focused mid-premium; online-first model |

|

Huawei Technologies Co., Ltd. |

Pura 80, Mate X series (limited EU) |

Emerging |

Constrained distribution; photography focus |

Key players include Apple Inc., SAMSUNG, Xiaomi, OPPO, vivo Mobile Communication Co., Ltd., HMD Global, OnePlus, Huawei Technologies Co., Ltd., and others.

Key Company Profiles

Apple Inc.

Apple Inc. is the value leader in the Europe smartphone market, with iOS commanding elevated shares in Germany, the UK, France, and the Nordics. Apple's vertically integrated silicon, retail footprint, and ecosystem stickiness sustain durable premium pricing and industry-leading profit share across the region.

- Product Portfolio: Offers iPhone 17 series, including (iPhone 17, 17 Air, 17 Pro, 17 Pro Max, 17e), and extended trade-in certified pre-owned programs.

- Recent Developments: In March 2026, Apple Inc. introduced the iPhone 17e as a more accessible addition to its latest smartphone lineup, combining strong performance with everyday usability. The device is powered by the A19 chip, offering improved speed and efficiency, along with upgraded base storage and a refined camera system to enhance overall user experience.

- Strategic Focus: Apple's European strategy leverages premium iOS ecosystem advantages, direct retail presence, and sustained software-support commitments to defend value share, while adapting to Digital Markets Act gatekeeper obligations and expanding satellite messaging and AI-native features.

SAMSUNG

SAMSUNG is the leading Android OEM in Europe, with the broadest portfolio across Galaxy S, Z foldables, and A-series mid-range. Vertical integration with Samsung Display for OLED panels and Samsung Semiconductor for select Exynos chipsets supports cost-to-performance advantages across flagship and mid-tier positioning.

- Product Portfolio: Galaxy S25/S26 flagship line, Galaxy Z Fold/Flip foldables, Galaxy A mid-range, and XCover ruggedized enterprise devices.

- Recent Developments: In March 2026, Samsung announced its latest Galaxy A series smartphones, the Galaxy A57 5G and Galaxy A37 5G, bringing enhanced features and improved performance to a wider audience. The new devices focus on delivering a balanced experience with upgrades in design, camera capabilities, display quality, and overall usability.

- Strategic Focus: Samsung's strategy centers on full-tier Android coverage, foldable form-factor leadership, seven-year software support for flagships, and Galaxy AI differentiation, backed by captive display and semiconductor sourcing that insulates margins from merchant component volatility.

Xiaomi

Xiaomi has rapidly scaled European share through aggressive mid-range pricing, Redmi entry-tier penetration, and expanding flagship positioning with the Xiaomi 14/15 series. The company has established Mi retail stores across Germany, Spain, France, and Italy, complementing online and carrier distribution channels.

- Product Portfolio: Xiaomi 15/17 flagship series, Redmi Note mid-range, POCO performance sub-brand, and accessories ecosystem across AIoT.

- Recent Developments: In April 2026, Xiaomi Corporation introduced its latest smartphone lineup, REDMI A7 Pro, emphasizing a combination of performance, design, and advanced features aimed at a broad user base. The new devices focus on delivering a refined user experience through upgrades in processing power, camera capabilities, and display quality. The lineup integrates enhanced software and AI-driven functionalities to improve everyday usability, including photography, multitasking, and overall system efficiency. These improvements reflect Xiaomi’s ongoing strategy to make advanced technology more accessible across different price segments.

- Strategic Focus: Xiaomi's European strategy prioritizes price-to-performance value disruption in the EUR 900+ band, imaging differentiation via Leica partnership, and ecosystem cross-sell through AIoT devices, targeting Samsung's mid-tier Galaxy A base.

Market Concentration Analysis

The Europe smartphone market is moderately concentrated, with the top two OEMs, Apple and Samsung, collectively holding roughly half of unit shipments and a clear majority of value share. The following tier, Xiaomi, OPPO, vivo, Motorola, and Google, compete intensely across mid-tier and entry segments.

Concentration at the Region level varies: Apple's share is elevated in the UK and Nordics, while Xiaomi and OPPO hold stronger positions in Spain, Italy, and Central/Eastern Europe. Consolidation pressure is limited at OEM level but intensifies among retailers and refurbished marketplaces through scale-driven economics.

Investment & Growth Opportunities

Fastest-Growing Segments

OLED display smartphones at ~5.1% CAGR through 2034 are the highest-growth technology segment, driven by foldable mainstreaming and mid-tier OLED migration. AI-native premium devices growing at ~5.0%+ CAGR represent the largest value-creation opportunity, as on-device generative AI features command premiums across Europe.

Emerging Markets

Central and Eastern European markets, including Poland, Romania, Czechia, and Hungary, are the fastest-growing sub-region. Rising disposable income, catching-up 5G rollout, and Android OEM retail expansion are creating mid-tier and entry-tier unit volume growth from a smaller installed base relative to Western Europe.

Venture & Investment Trends

Private equity and strategic investment are flowing into European refurbished smartphone marketplaces, with Back Market, Swappie, and Recommerce attracting growth capital. Sustainability, right-to-repair compliance, and EU battery regulations are reshaping investment theses toward circular-economy business models and longer-life device strategies.

Future Market Outlook (2026-2034)

The Europe smartphone market is forecast to expand from 197.90 Million Units in 2025 to 289.57 Million Units by 2034 at a CAGR of 4.3%, adding over 91 Million Units in annual shipments. Growth reflects recurring replacement demand, 5G upgrade cycles, and premium-tier expansion.

Three forces will most significantly shape the industry through 2034. On-device generative AI will redefine flagship specifications and shorten replacement cycles. Foldable form factors will mainstream into the EUR 1,000-1,400 band. Refurbished and circular-economy channels will absorb extended device lifecycles across Western European markets.

Research Methodology

Primary Research

Primary research encompassed over 40 structured interviews in 2024-2025 with European smartphone industry stakeholders, including OEM country managers, mobile operator procurement leads, specialty and online retail category buyers, refurbished marketplace executives, and component distribution specialists across Germany, the UK, France, Italy, and Spain.

Secondary Research

Key secondary sources include GSMA Intelligence, Eurostat ICT usage statistics, European Commission Digital Economy and Society Index, IDC and Canalys European smartphone tracker publications, OEM annual reports, carrier group results (Deutsche Telekom, Vodafone, Orange, Telefónica), and EU regulatory publications covering DMA and right-to-repair.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating European GDP growth, smartphone penetration and replacement cycles, 5G adoption curves, and historical installed-base evolution. Scenario analysis (base, optimistic, conservative) was performed to account for macroeconomic uncertainty.

Europe Smartphone Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Units |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Operating Systems Covered | Android, iOS, Others |

| Digital Technologies Covered | LCD Technology, OLED Technology |

| RAM Capacities Covered | Below 4GB, 4GB – 8GB, Over 8GB |

| Price Ranges Covered | Ultra-Low-End (Less Than $100), Low-End ($100-<$200), Mid-Range ($200-<$400), Mid- to High-End ($400-<$600), High-End ($600-<$800), Premium ($800-<$1000) and Ultra-Premium ($1000 And above) |

| Distribution Channels Covered | OEMs, Online Stores, Retailers |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Comnpanies Covered | Apple Inc., SAMSUNG, Xiaomi, OPPO, vivo Mobile Communication Co., Ltd., HMD Global, OnePlus, Huawei Technologies Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Smartphone Market Report

The Europe smartphone market reached 197.90 Million Units in 2025, reflecting steady 5G upgrade demand, recurring premium refresh cycles, and expanding foldable and AI-enabled flagship adoption across Germany, the UK, France, Italy, Spain, and other European countries.

The market is projected to reach 289.57 Million Units by 2034, growing at a CAGR of 4.3% during 2026-2034, driven by 5G Standalone, on-device AI, foldable adoption, and sustained replacement demand.

Android leads with a 70.0% share in 2025, driven by Samsung, Xiaomi, OPPO, vivo, Motorola, and Google across every price tier. iOS holds 28.6%, concentrated in premium segments.

OLED technology leads at 68.0% in 2025, reflecting flagship migration, mid-tier adoption, and foldable compatibility. LCD retains 32.0%, concentrated in entry and mid-tier devices priced below EUR 300.

Germany commands 22.8% share in 2025, driven by Europe's largest economy, dense 5G infrastructure, carrier-subsidized refresh cycles via Deutsche Telekom, Vodafone, and Telefónica Deutschland, and high consumer spending.

OLED display smartphones are fastest growing at ~5.1% CAGR through 2034, driven by foldable mainstreaming, LTPO adoption, and panel supplier capacity shifting from LCD toward flexible and rigid OLED lines.

Leading companies include Apple Inc., SAMSUNG, Xiaomi, OPPO, vivo Mobile Communication Co., Ltd., HMD Global, OnePlus, Huawei Technologies Co., Ltd., and others.

Key applications include mobile communication, digital payments, streaming, mobile gaming, enterprise productivity, e-commerce, navigation, social networking, health tracking, and on-device generative AI across consumer and enterprise users.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)