India Lubricants Market Size, Share, Trends and Forecast by Product Type, Base Oil, End Use Industry, and Region, 2026-2034

India Lubricants Market Summary:

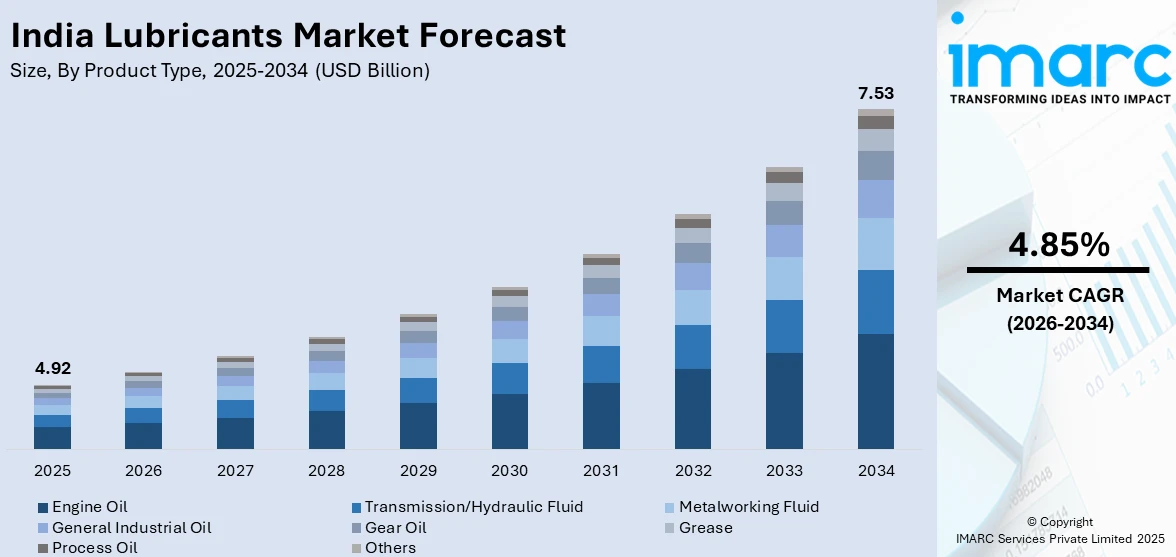

The India lubricants market size was valued at USD 4.92 Billion in 2025 and is projected to reach USD 7.53 Billion by 2034, growing at a compound annual growth rate of 4.85% from 2026-2034.

India's lubricants market is expanding steadily, driven by the rapid growth of the automotive sector and increasing industrial manufacturing activities. The country's rising vehicle ownership, expanding commercial fleet operations, and growing infrastructure development projects are fueling lubricant demand. Advanced formulations meeting stringent emission standards and the shift toward synthetic products are reshaping the competitive landscape, positioning India as a key growth market.

Key Takeaways and Insights:

- By Product Type: Engine oil dominates the market with a share of 29% in 2025, owing to the extensive vehicle parc comprising passenger cars, commercial vehicles, and two-wheelers requiring regular maintenance. The transition to BS-VI compliant formulations and growing preference for high-performance synthetic grades are driving premiumization across automotive applications.

- By Base Oil: Mineral oil leads the market with a share of 55% in 2025. This dominance is driven by cost-effectiveness, widespread availability through established distribution networks, and continued preference among price-sensitive consumers particularly in rural markets and the two-wheeler segment.

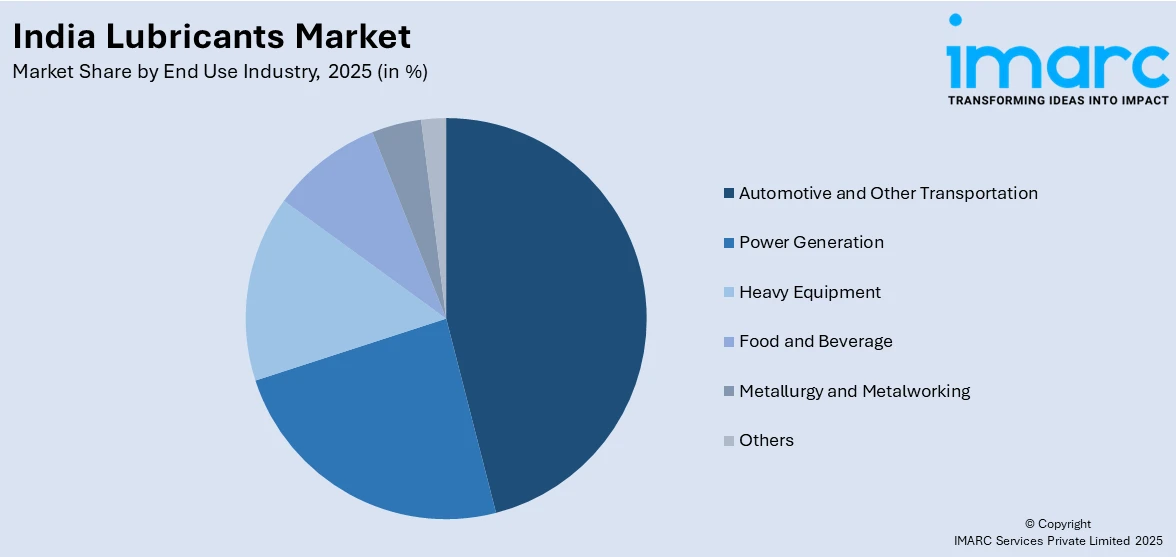

- By End Use Industry: Automotive and other transportation holds the largest segment with a market share of 46% in 2025, reflecting India's position as the third-largest automotive market globally. Rising vehicle production, expanding commercial fleet operations, and increasing maintenance awareness drive consistent lubricant demand across transportation applications.

- By Region: North India represents the leading region with 33% share in 2025, driven by the concentration of manufacturing industries in states like Haryana, Punjab, and Delhi-NCR. Strong industrial activity, dense transportation networks, and established distribution infrastructure support lubricant consumption across automotive and industrial applications.

- Key Players: Key players drive the India lubricants market by expanding product portfolios, investing in advanced manufacturing facilities, and strengthening distribution networks. Their focus on developing BS-VI compliant formulations, synthetic lubricants, and specialized industrial solutions accelerates market premiumization and technology adoption.

To get more information on this market Request Sample

The India lubricants market is experiencing robust expansion propelled by the country's dynamic automotive sector and accelerating industrial development. India's automobile industry produced 3.10 crore vehicles, including commercial vehicles, passenger vehicles, three wheelers, two wheelers, and quadricycles, in FY 2024-25, according to the Society of Indian Automobile Manufacturers, reflecting continued growth that directly translates into increased lubricant consumption for engine maintenance and component protection. The government's Make in India initiative and Production-Linked Incentive schemes are attracting significant manufacturing investments, boosting demand for industrial lubricants across sectors including metal processing, power generation, and heavy machinery operations. Rising consumer awareness about vehicle maintenance benefits, coupled with expanding rural connectivity and increasing disposable incomes, is driving lubricant adoption among first-time vehicle owners. The implementation of Bharat Stage VI emission norms has catalyzed demand for advanced low-ash, low-viscosity formulations compatible with modern exhaust after-treatment systems. Furthermore, the growth of e-commerce logistics, ride-sharing platforms, and commercial fleet operations is intensifying lubricant requirements, contributing to the expanding India lubricants market share.

India Lubricants Market Trends:

Transition to Synthetic and High-Performance Formulations

The Indian lubricants industry is witnessing accelerated adoption of synthetic and semi-synthetic formulations driven by performance requirements of modern engines. BS-VI emission compliance has necessitated low-SAPS lubricants that protect catalytic converters and diesel particulate filters while ensuring optimal engine efficiency. In June 2024, Castrol India launched new EDGE variants specifically designed for passenger cars, demonstrating manufacturers' commitment to developing India-specific premium products that address evolving consumer expectations for enhanced protection and extended drain intervals.

Rising Focus on Sustainability and Bio-Based Alternatives

Environmental consciousness is reshaping lubricant preferences as manufacturers introduce eco-friendly alternatives to conventional mineral-based products. The introduction of Extended Producer Responsibility for used oils from April 2024 is promoting circular economy practices through systematic collection and re-refining infrastructure development. In April 2024, Savsol Lubricants launched Savsol Ester 5, a biodegradable lubricant targeting high-end automotive and railway applications, reflecting the industry's pivot toward sustainable formulations meeting regulatory requirements and corporate sustainability objectives.

Emergence of Electric Vehicle Fluids and Specialty Lubricants

The electric vehicle revolution is creating new lubricant segments as manufacturers develop specialized fluids for EV components. Total EV registrations in India reached 1.97 million units in FY 2024-25, demonstrating accelerating electrification that demands dielectric coolants, e-transmission fluids, and specialty greases for electric powertrains. This transition is prompting established lubricant producers to diversify portfolios beyond traditional engine oils, addressing emerging mobility requirements through innovative formulations. Moreover, leading companies are investing in research and development to capture opportunities in battery thermal management and electric drivetrain lubrication applications.

Market Outlook 2026-2034:

The India lubricants market outlook remains promising, underpinned by sustained automotive production growth, expanding manufacturing capabilities, and infrastructure development initiatives. Government initiatives, including PLI schemes for automotive components and infrastructure projects under PM Gati Shakti, are expected to accelerate industrial lubricant demand. The premiumization trend driven by BS-VI compliance requirements and growing synthetic adoption will enhance market value despite potential volume moderation from extended drain intervals. Additionally, investments in local manufacturing, such as ExxonMobil's INR 900 crore plant in Maharashtra, will strengthen domestic supply capabilities and market competitiveness. The market generated a revenue of USD 4.92 Billion in 2025 and is projected to reach a revenue of USD 7.53 Billion by 2034, growing at a compound annual growth rate of 4.85% from 2026-2034.

India Lubricants Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Engine Oil |

29% |

|

Base Oil |

Mineral Oil |

55% |

|

End Use Industry |

Automotive and Other Transportation |

46% |

|

Region |

North India |

33% |

Product Type Insights:

- Engine Oil

- Transmission/Hydraulic Fluid

- Metalworking Fluid

- General Industrial Oil

- Gear Oil

- Grease

- Process Oil

- Others

Engine oil dominates with a market share of 29% of the total India lubricants market in 2025.

Engine oils constitute the cornerstone of India's lubricants market, serving the country's extensive vehicle parc spanning passenger vehicles, commercial trucks, and two-wheelers. The segment benefits from mandatory periodic oil changes required for optimal engine performance and longevity across all vehicle categories. Passenger vehicle sales in India reached 4.3 million units in FY 2024-25, according to Society of Indian Automobile Manufacturers (SIAM), driving sustained aftermarket demand for engine lubricants. The transition to BS-VI emission standards has necessitated advanced low-SAPS formulations that protect exhaust after-treatment systems while delivering enhanced fuel efficiency benefits.

The premiumization trend within engine oils is accelerating as consumers increasingly recognize performance advantages of synthetic and semi-synthetic grades over conventional mineral-based products. Rising awareness about extended drain intervals, superior engine protection, and fuel economy benefits is driving adoption of high-performance formulations particularly among SUV and premium vehicle owners. Original equipment manufacturers are actively promoting factory-fill partnerships and branded lubricant programs that strengthen product differentiation and build consumer loyalty throughout the vehicle ownership lifecycle.

Base Oil Insights:

- Mineral Oil

- Synthetic Oil

- Bio-Based Oil

Mineral oil leads with a share of 55% of the total India lubricants market in 2025.

Mineral oil-based lubricants maintain commanding market presence driven by established production infrastructure and cost advantages that resonate with price-sensitive Indian consumers. The extensive refinery network operated by public sector undertakings including Indian Oil Corporation, Bharat Petroleum, and Hindustan Petroleum ensures reliable supply and competitive pricing across distribution channels. Two-wheeler owners, who represent the largest vehicle segment in India, predominantly prefer mineral-based lubricants due to affordability considerations and adequate performance for routine commuting applications across urban and rural markets.

The value proposition of mineral oils remains compelling for commercial vehicle operators prioritizing operational cost management over extended service intervals. Fleet managers serving price-competitive logistics segments continue favoring mineral-based products that deliver satisfactory protection at economical price points. However, gradual migration toward Group II and Group III base stocks is improving mineral oil performance characteristics, enabling formulations that bridge the gap between conventional and synthetic products while maintaining cost accessibility for mainstream consumers.

End Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Power Generation

- Automotive and Other Transportation

- Heavy Equipment

- Food and Beverage

- Metallurgy and Metalworking

- Others

The automotive and other transportation exhibits a clear dominance with a 46% share of the total India lubricants market in 2025.

The automotive and transportation sector drives nearly half of India's lubricant consumption, reflecting the country's position as the world's third-largest automotive market. Rising vehicle ownership across urban and rural regions continues generating consistent demand for engine oils, transmission fluids, and greases. The burgeoning e-commerce sector is intensifying commercial vehicle utilization as logistics operators expand delivery networks, increasing lubricant consumption through accelerated replacement cycles and elevated operational hours supporting last-mile connectivity requirements.

The transportation sector benefits from multiple demand drivers including rising vehicle ownership penetration, expanding ride-sharing platforms, and growing interstate freight movement under infrastructure initiatives like PM Gati Shakti. Passenger vehicle sales continue climbing as rising disposable incomes enable automotive purchases among middle-class consumers, while SUV proliferation amplifies per-vehicle lubricant consumption due to larger engine displacements and sump capacities. Commercial fleet operators increasingly recognize lubricant quality impacts on fuel efficiency and maintenance costs, driving gradual premiumization within the transportation segment.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

North India represents the leading segment with a 33% share of the total India lubricants market in 2025.

North India commands the largest regional share driven by substantial industrial concentration and dense transportation networks spanning Delhi-NCR, Haryana, Punjab, and Uttar Pradesh. The region hosts major automotive manufacturing clusters including Gurgaon and Greater Noida that generate significant lubricant consumption through production operations and aftermarket servicing. Industrial hubs across North India encompassing textile, food processing, and engineering sectors create diversified demand for hydraulic fluids, metalworking lubricants, and general industrial oils supporting manufacturing equipment maintenance requirements.

The agricultural prominence of North Indian states including Punjab and Haryana generates consistent tractor lubricant demand during farming seasons, complementing automotive consumption patterns throughout the year. Well-developed distribution infrastructure facilitates efficient lubricant availability across urban retail outlets and rural markets, supported by extensive dealership networks operated by major oil marketing companies. The region's strategic location along major interstate highways intensify commercial vehicle traffic, driving sustained demand for heavy-duty engine oils and transmission fluids serving long-haul trucking operations.

Market Dynamics:

Growth Drivers:

Why is the India Lubricants Market Growing?

Expanding Automotive Production and Rising Vehicle Ownership

India's automotive industry continues demonstrating remarkable growth, directly driving lubricant demand across engine oils, transmission fluids, and specialty formulations. Rising disposable incomes and expanding middle-class population are enabling automotive purchases among first-time buyers, particularly in tier-II and tier-III cities where vehicle penetration rates remain below metropolitan averages. The utility vehicle segment captured substantial percentage of passenger vehicle sales, driving increased lubricant consumption due to larger engine capacities requiring higher oil volumes per service interval. Commercial vehicle utilization intensifies as logistics networks expand supporting e-commerce growth, interstate freight movement, and last-mile delivery operations that collectively accelerate lubricant replacement cycles through elevated operational hours and distance traveled.

Accelerating Industrial Manufacturing Under Government Initiatives

Government programs including Make in India and Production-Linked Incentive schemes are catalyzing manufacturing expansion that generates increased industrial lubricant demand. The Ministry of Commerce and Industry projects India's manufacturing sector to reach USD 1 trillion by FY26, creating substantial opportunities for hydraulic fluids, metalworking lubricants, and machinery oils supporting production equipment. Special economic zones and industrial corridors attract domestic and foreign investments in sectors including automotive components, electronics, and heavy machinery that rely on consistent lubrication for operational efficiency. The electrical equipment market growth demonstrates manufacturing diversification creating specialized lubricant requirements across emerging industrial applications.

Regulatory Push for Advanced Emission-Compliant Formulations

The nationwide implementation of Bharat Stage VI emission standards is fundamentally transforming lubricant formulation requirements, driving premiumization across automotive applications. BS-VI compliant engines incorporate advanced exhaust after-treatment systems including diesel particulate filters and selective catalytic reduction that demand low-SAPS lubricants preventing catalyst poisoning and filter clogging. Lubricant manufacturers are investing substantially in research and development to create India-specific formulations addressing unique driving conditions while meeting international performance specifications. In October 2023, BPCL launched premium synthetic engine oils including MAK TitaniumCK4 and MAK Blaze Synth specifically designed for BS-VI compliant vehicles, reflecting industry commitment to emission-compatible solutions. The regulatory environment encourages consumer education about lubricant quality importance, strengthening brand differentiation opportunities and accelerating transition from conventional to advanced formulations across vehicle categories.

Market Restraints:

What Challenges the India Lubricants Market is Facing?

Crude Oil Price Volatility and Raw Material Cost Fluctuations

The lubricants industry faces persistent margin pressures from volatile crude oil prices that directly impact base oil production costs. India's substantial reliance on imported base oils exposes manufacturers to currency exchange fluctuations and global supply chain disruptions affecting feedstock availability. Price instability complicates long-term planning for manufacturers and distributors while creating challenges for maintaining competitive retail pricing without sacrificing profitability.

Prevalence of Counterfeit Products in Unorganized Distribution Channels

The widespread presence of counterfeit lubricants in India's fragmented distribution network undermines brand credibility and poses risks to equipment performance. Substandard products sold through unauthorized channels affect consumer trust in genuine brands while compromising engine protection and longevity. Addressing counterfeiting requires substantial investment in authentication technologies, distribution channel oversight, and consumer education about identifying legitimate products.

Growing Electric Vehicle Adoption Displacing Traditional Lubricant Demand

The accelerating transition toward electric mobility poses long-term challenges for conventional engine oil demand as EVs eliminate crankcase lubrication requirements. Government electrification targets envision significant EV penetration by 2030, threatening traditional lubricant volumes particularly within the two-wheeler segment leading electrification adoption. Manufacturers must adapt by developing specialized EV fluids while managing portfolio transitions during the combustion-to-electric powertrain evolution.

Competitive Landscape:

The India lubricants market exhibits moderate consolidation with public sector undertakings and multinational corporations competing through differentiated product portfolios and distribution strengths. Domestic oil marketing companies leverage integrated refinery operations and extensive retail networks reaching remote markets across urban and rural geographies. International players emphasize premium synthetic offerings and OEM partnerships capturing higher-margin segments through technological differentiation. Recent strategic developments include cross-border partnerships for brand distribution and significant greenfield manufacturing investments, intensifying competition through localization and distribution expansion strategies. Market participants continue focusing on product innovation, supply chain optimization, and after-sales service enhancement.

Recent Developments:

- In January 2025, Castrol India announced a strategic partnership with Hindustan Petroleum Corporation Limited to explore the development of a re-refined base oil system. The collaboration focuses on establishing circular economy practices for collecting and processing used lubricating oils into high-quality base stocks for sustainable lubricant manufacturing.

- In December 2024, Gulf Oil Lubricants renewed its partnership agreement with Piaggio covering lubricant supply for the manufacturer's vehicle range. The collaboration encompasses advanced BS-VI compliant oils and electric vehicle fluids, strengthening Gulf Oil's position in the OEM lubricant supply segment serving transportation applications.

India Lubricants Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Engine Oil, Transmission/Hydraulic Fluid, Metalworking Fluid, General Industrial Oil, Gear Oil, Grease, Process Oil, Others |

| Base Oils Covered | Mineral Oil, Synthetic Oil, Bio-Based Oil |

| End Use Industries Covered | Power Generation, Automotive and Other Transportation, Heavy Equipment, Food and Beverage, Metallurgy and Metalworking, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Lubricants Market Report

The India lubricants market size was valued at USD 4.92 Billion in 2025.

The India lubricants market is expected to grow at a compound annual growth rate of 4.85% from 2026-2034 to reach USD 7.53 Billion by 2034.

Engine oil dominated the market with a share of 29%, driven by extensive vehicle parc maintenance requirements, BS-VI emission compliance formulations, and growing premiumization toward synthetic grades across passenger and commercial vehicle segments.

Key factors driving the India lubricants market include expanding automotive production, rising vehicle ownership, accelerating industrial manufacturing under government initiatives, and regulatory requirements for BS-VI compliant formulations driving premiumization across applications.

Major challenges include crude oil price volatility affecting production costs, prevalence of counterfeit products undermining brand trust, growing electric vehicle adoption displacing traditional engine oil demand, and import dependency for specialty base oils creating supply chain vulnerabilities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)