Patient Engagement Solutions Market Size, Share, Trends and Forecast by Therapeutic Area, Application, End User, Component, Delivery Type, and Region, 2026-2034

Global Patient Engagement Solutions Market Size, Share, Trends & Forecast (2026-2034)

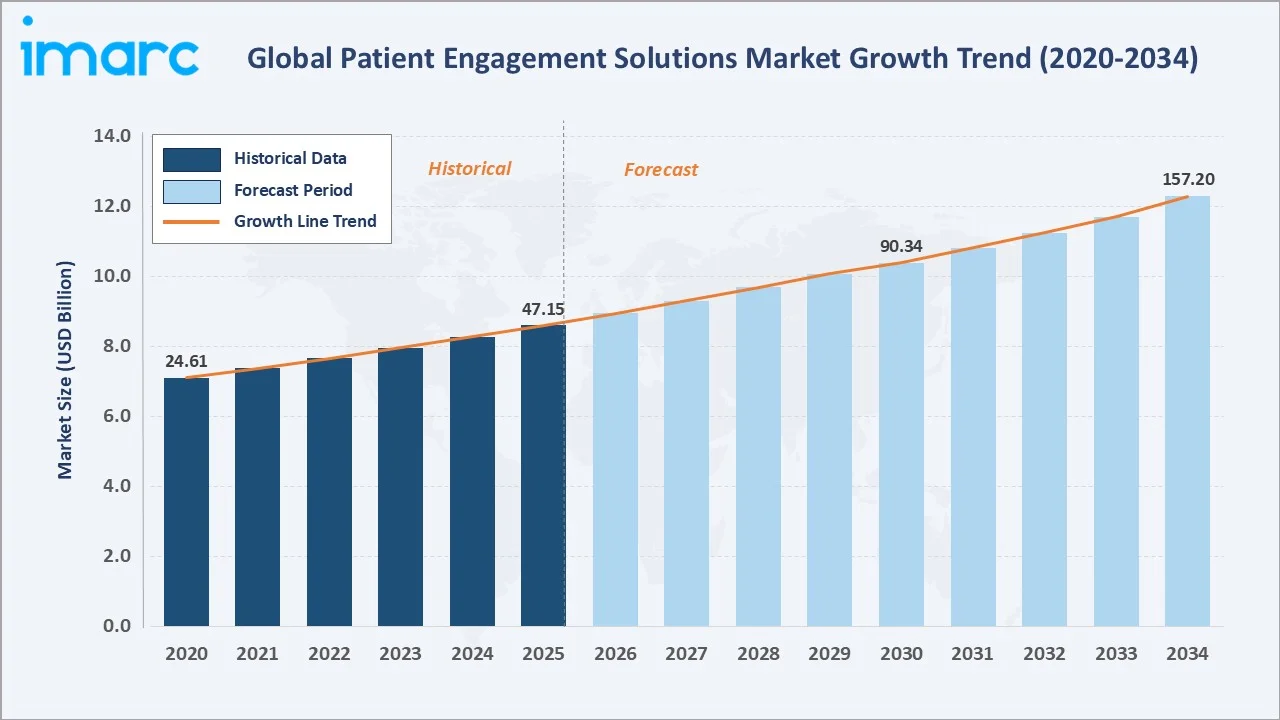

The global patient engagement solutions market size reached USD 47.15 Billion in 2025 and is projected to reach USD 157.20 Billion by 2034, exhibiting a CAGR of 13.89% during 2026-2034. The market's robust trajectory is driven by the global shift toward patient-centered, value-based care models, the rising prevalence of chronic diseases demanding continuous engagement, and the rapid integration of artificial intelligence (AI) and machine learning (ML) into healthcare delivery.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 47.15 Billion |

|

Forecast Market Size (2034) |

USD 157.20 Billion |

|

CAGR (2026-2034) |

13.89% |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

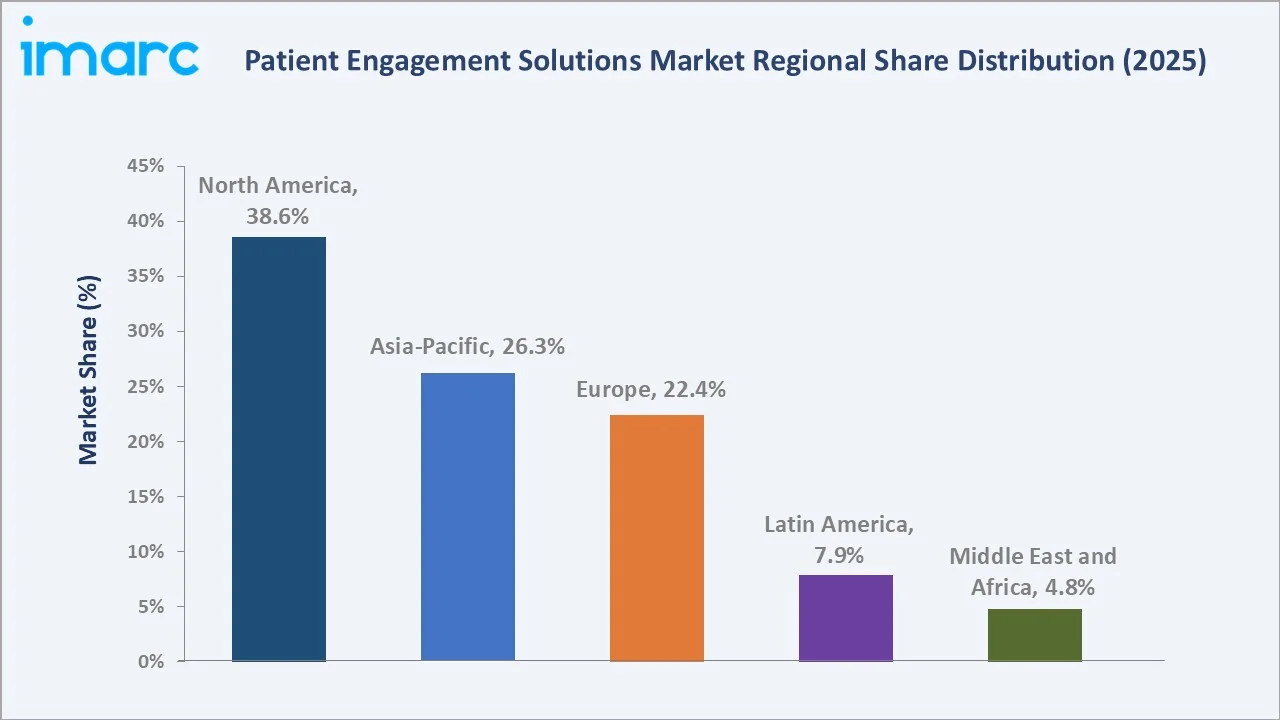

Largest Region (2025) |

North America (38.6% share) |

|

Fastest Growing Region |

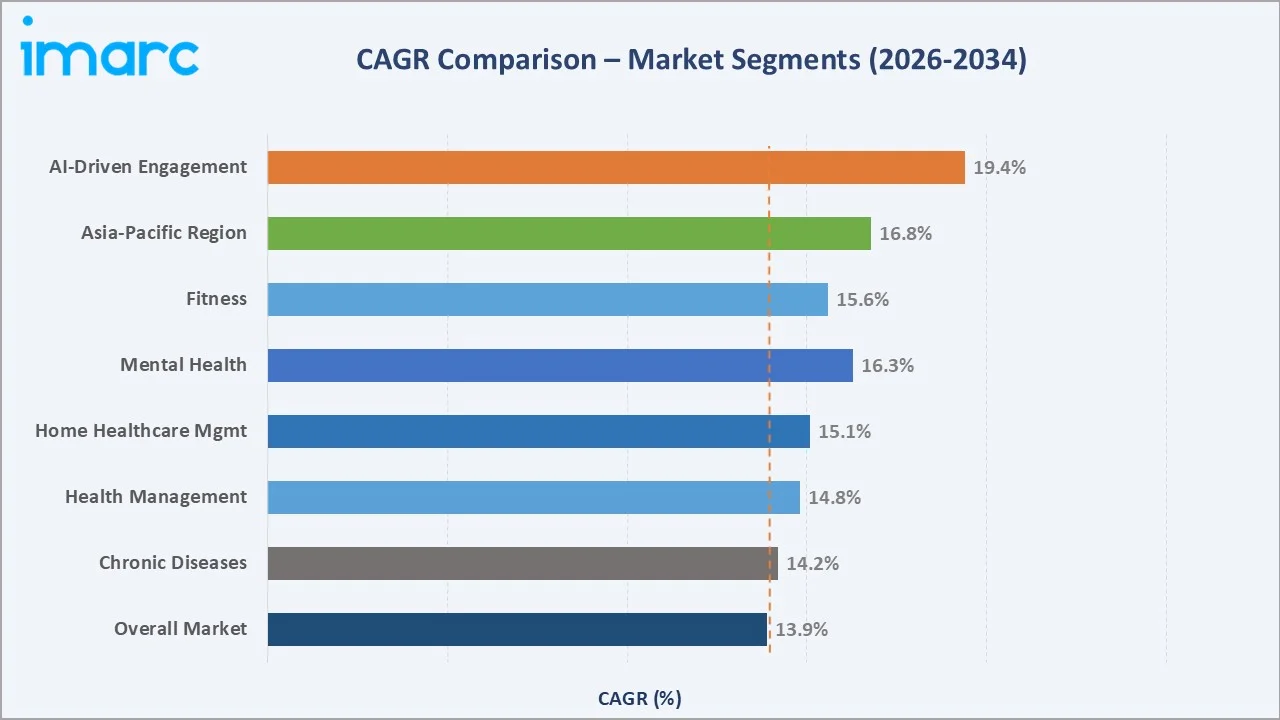

Asia-Pacific – (~16.8% CAGR) |

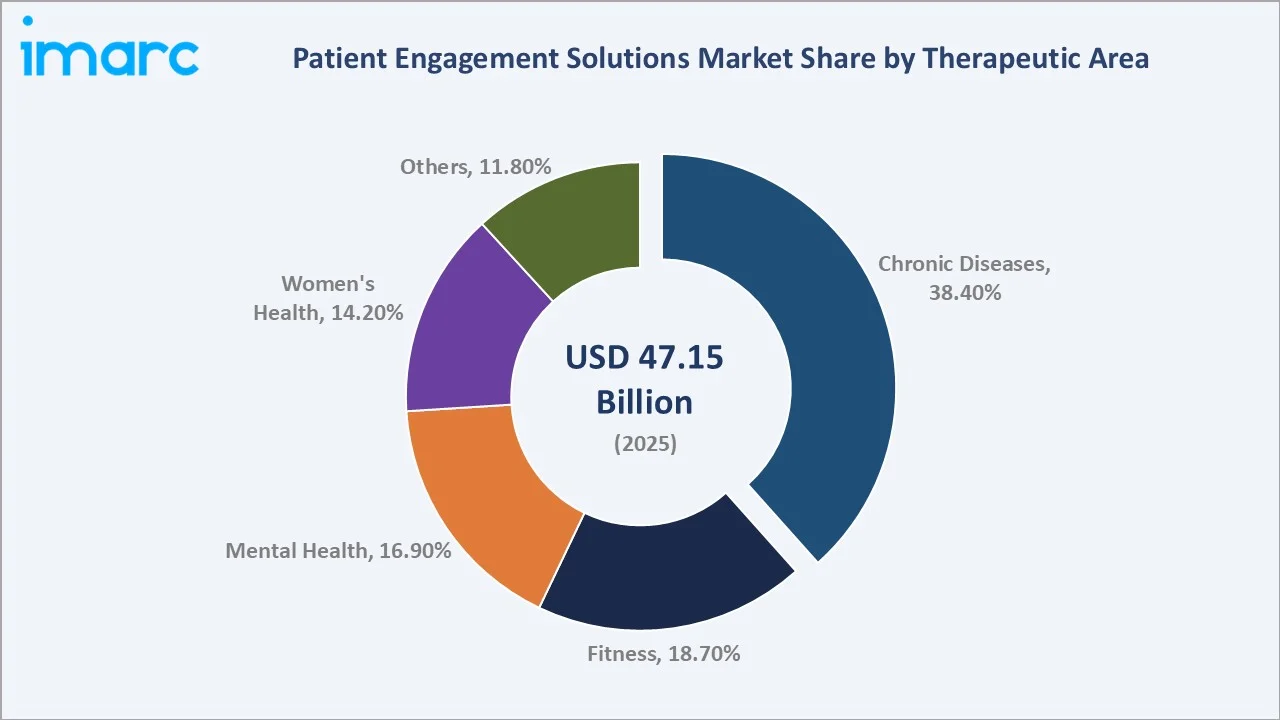

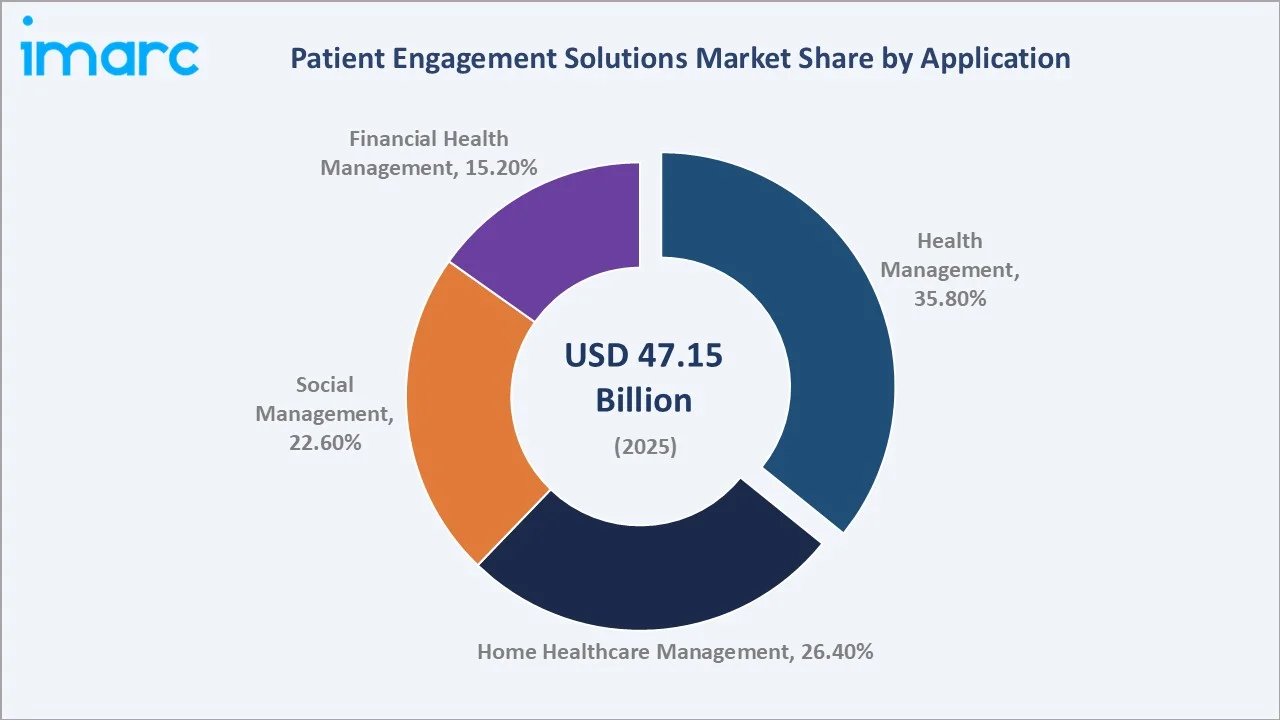

Chronic diseases lead all therapeutic areas with a 38.4% market share in 2025, while health management is the top application at 35.8%. North America commands the largest regional share at 38.6%, underpinned by advanced healthcare IT infrastructure and strong regulatory support for digital patient engagement.

To get more information on this market, Request Sample

The patient engagement solutions market is rapidly evolving, supported by the growing adoption of telehealth, mobile health apps, and personalized care models. Increasing healthcare costs and the need to improve patient adherence, satisfaction, and outcomes are further driving the adoption of these solutions.

Executive Summary

The global patient engagement solutions market is undergoing transformative expansion, fueled by the convergence of digital health technologies, chronic disease management imperatives, and the systemic shift from volume-based to value-based care reimbursement models. Valued at USD 47.15 billion in 2025 and forecast to reach USD 157.20 billion by 2034 at a CAGR of 13.89%, the market represents one of the fastest-growing sectors in global healthcare information technology.

Chronic diseases dominate therapeutic area demand at 38.4% share in 2025, driven by the global burden of diabetes, cardiovascular disease, and obesity, conditions requiring sustained, longitudinal patient engagement rather than episodic intervention. Health management applications command the largest application share at 35.8%, reflecting healthcare systems' prioritization of care coordination, medication adherence monitoring, and preventive health interventions.

North America leads globally with a 38.6% revenue share in 2025, supported by the Affordable Care Act (ACA), HITECH Act mandates for EHR adoption, and a mature ecosystem of healthcare IT companies. Asia-Pacific is the fastest-growing region with 16.8% CAGR, propelled by government-led digital health initiatives in China, India, Japan, and South Korea.

Key Market Insights

|

Insight |

Data |

|

Largest Therapeutic Area |

Chronic Diseases – 38.4% share (2025) |

|

Top Application Segment |

Health Management – 35.8% share (2025) |

|

Leading Region |

North America – 38.6% share (2025) |

|

Fastest Growing Region |

Asia-Pacific – CAGR ~16.8% (2026–2034) |

|

Fastest Growing Application |

Home Healthcare Management – CAGR ~15.1% (2026–2034) |

|

Fastest Growing Therapeutic Area |

Mental Health – CAGR ~16.3% (2026–2034) |

|

Top Companies |

Epic Systems, Cerner, McKesson, Allscripts, Athenahealth, GetWellNetwork |

Key Analytical Observations:

- Chronic diseases dominate at 38.4% (2025), as around 853 million people will be living with diabetes by 2050 (International Diabetes Federation), creating an immense need for digital adherence and monitoring platforms that integrate patient engagement solutions into chronic care management programs.

- Health management leads applications at 35.8% (2025), driven by healthcare providers' deployment of patient portals, medication reminder systems, care plan communication tools, and EHR-integrated engagement workflows.

- Mental health is the fastest-growing therapeutic area (CAGR ~16.3%, 2026-2034). According to the World Health Organization, over 1 billion people globally are estimated to live with a mental or substance use disorder.

- North America leads with 38.6% (2025) backed by ACA and HITECH Act mandates, U.S. healthcare expenditure exceeding USD 8.6 trillion in 2033 (National Health Expenditure, 2025), and dominant market presence of Epic Systems, Cerner, and McKesson.

- Asia-Pacific is the fastest-growing region (CAGR ~16.8%, 2026-2034) driven by China's national digital health strategy, India's Ayushman Bharat Digital Mission (ABDM) targeting 1.4 billion citizens, and Japan and South Korea's aging population requiring sustained remote care management solutions.

Global Patient Engagement Solutions Market Overview

Patient engagement solutions encompass a broad ecosystem of digital health technologies, software platforms, and services designed to actively involve patients in their own healthcare journeys, from disease prevention and chronic condition management to treatment adherence and post-acute recovery. The solutions landscape includes patient portals, mobile health (mHealth) applications, remote patient monitoring (RPM) platforms, AI-powered chatbots, and appointment & medication management systems.

The global patient engagement solutions ecosystem connects technology providers (cloud infrastructure, AI/ML platforms, and EHR vendors), solution developers (software companies and app developers), healthcare payers (insurance companies and government programs), healthcare providers (hospitals, clinics and physician groups), digital health platforms (telehealth, wearables, and portals), and ultimately patients and caregivers.

The patient engagement solutions market growth is powered by structural healthcare transformation trends: the global shift from fee-for-service to value-based care reimbursement, the digitalization of healthcare, government mandates for EHR interoperability, and patient expectations shaped by consumer digital experiences in other sectors. These forces are expected to sustain strong double-digit growth through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

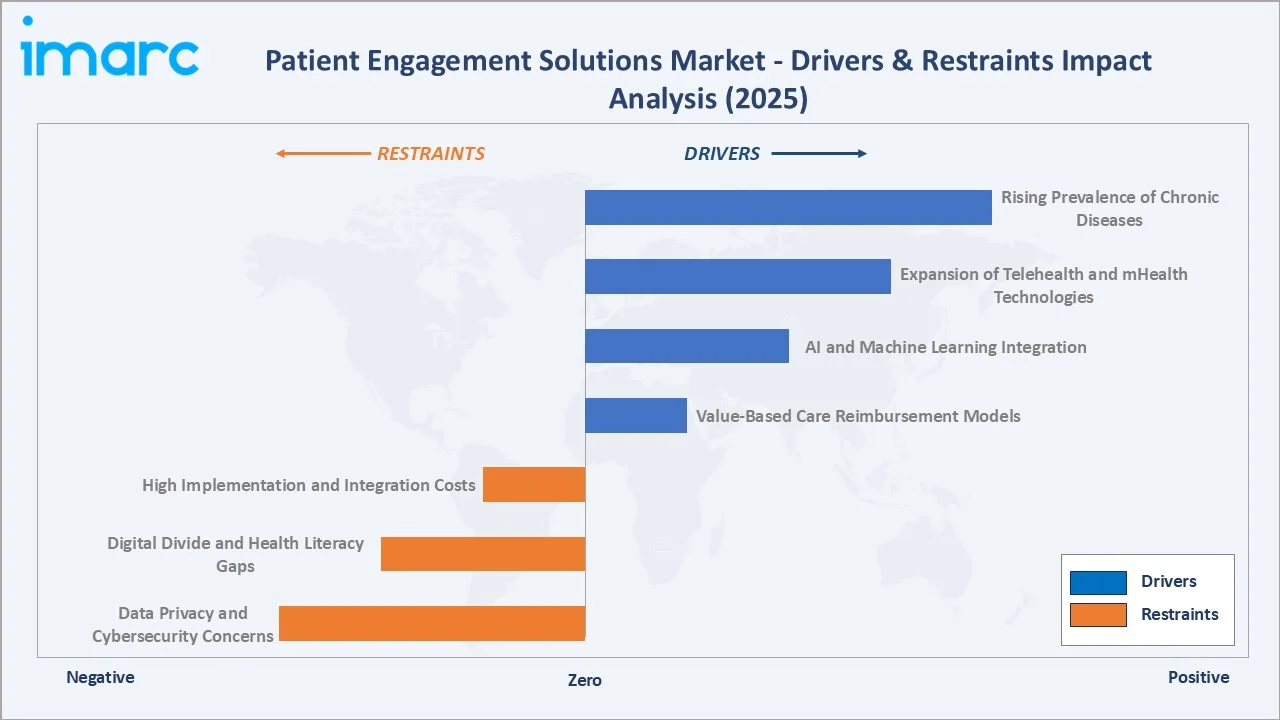

Market Drivers

- Rising Prevalence of Chronic Diseases: Cardiovascular diseases cause approximately 17.9 million deaths annually (WHO). The continuous monitoring, medication adherence, and care coordination requirements of chronic conditions are the primary demand engine for patient engagement solutions.

- Expansion of Telehealth and mHealth Technologies: In a 2022–2023 study published in Financial Express, 76.1% of Type 2 Diabetes patients using the mySugr mHealth app reported improved medication compliance and diabetes management awareness.

- AI and Machine Learning Integration: In February 2026, a coalition of leading U.S. health systems, patient safety experts, and technology innovators launched the AI Care Standard, the first operational framework designed to ensure safe, responsible use of AI that communicates directly with patients.

- Value-Based Care Reimbursement Models: The shift from volume-based to outcome-based reimbursement is compelling healthcare providers and payers to invest in engagement solutions that demonstrably improve patient outcomes, reduce hospital readmissions, and lower total cost of care.

Market Restraints

- Data Privacy and Cybersecurity Concerns: As in previous years, the healthcare industry experienced the highest average breach costs at USD 10.93 million, with data breaches typically remaining undetected for 213 days, longer than the average of 194 days seen in other industries.

- Digital Divide and Health Literacy Gaps: Elderly populations, rural communities, and low-income segments, often those with the highest chronic disease burden, face disproportionate barriers to digital health adoption, limiting the equitable reach of patient engagement solutions.

- High Implementation and Integration Costs: Integrating patient engagement platforms with existing EHR systems is costly, with expenses ranging from USD 10,000 to USD 30,000 depending on the integration phase, such as core system and specialty module integration.

Market Opportunities

- Mental Health Digital Platform Expansion: In November 2025, InteliSense launched InteliChart, a leader in patient engagement technology, today unveiled InteliSense, an intelligent AI platform designed to enhance automation, efficiency, and personalization throughout the patient journey.

- Remote Patient Monitoring (RPM) Scale-Up: RPM technology provider Smart Meter experienced a 300% sales increase from 2022 to January 2025, expanded its customer base fourfold, and now serves over 350,000 patients.

- Emerging Market Digital Health Infrastructure: India's Ayushman Bharat Digital Mission, China's Health China 2030 policy, and ASEAN digital health investment programs are creating greenfield markets for patient engagement solution providers.

Market Challenges

- EHR Interoperability Fragmentation: The healthcare IT landscape across most markets features fragmented, proprietary EHR systems with limited interoperability. Patient engagement platforms must integrate with multiple incompatible systems across care continuum settings, including hospitals, outpatient, pharmacy, and home care.

- Patient Engagement Fatigue: The proliferation of health apps, notifications, and digital touchpoints risks overwhelming patients and reducing engagement quality over time. Maintaining meaningful, sustained patient participation requires sophisticated behavioral science-backed design, personalization algorithms, and clinical workflow integration that many current-generation platforms lack.

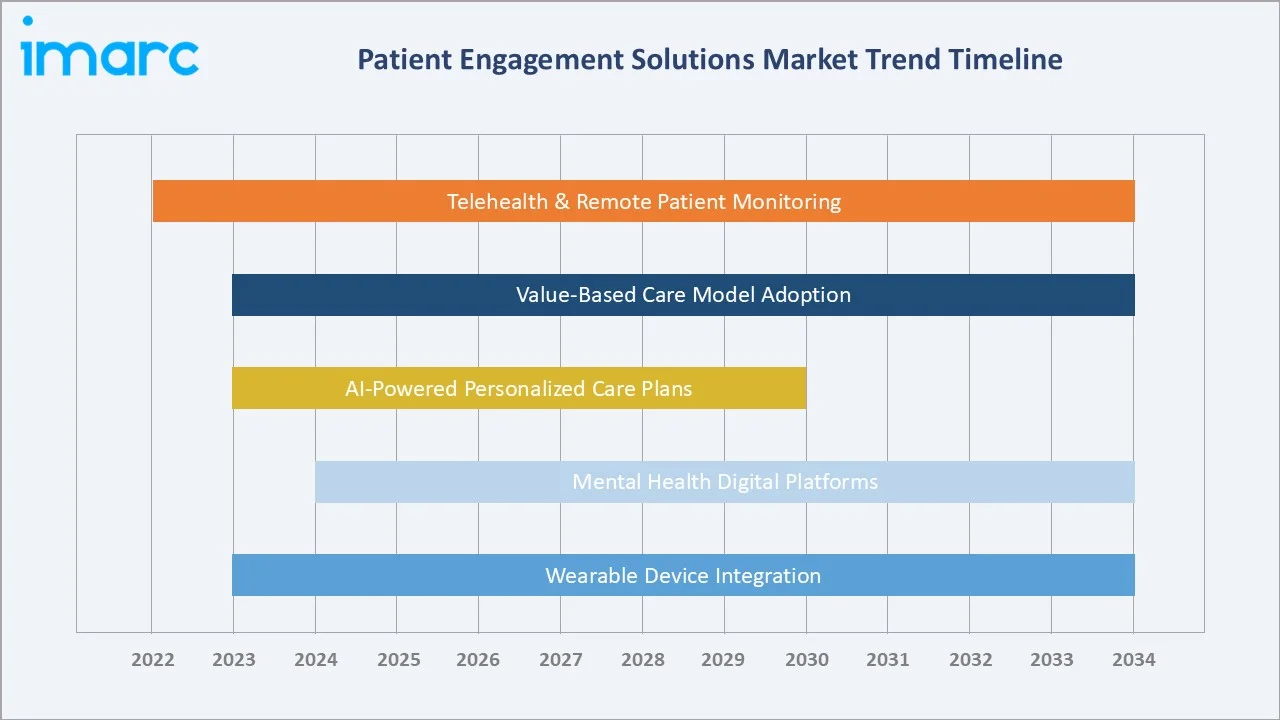

Emerging Patient Engagement Solutions Market Trends

1. AI-Powered Hyper-Personalization of Patient Care Plans

In March 2024, Doceree unveiled Spark at HIMSS 2024, an AI-powered platform integrating personalized clinical messaging into EHR workflows for over 700,000 providers across 50+ platforms. AI-powered chatbots and NLP-based virtual health assistants now handle tier-1 patient inquiries, medication reminders, and symptom triage at scale, reducing clinical staff burden while improving patient responsiveness.

2. Accelerated Telehealth and Remote Patient Monitoring Adoption

Smart Meter's 300% sales growth from 2022 to 2025 and its expansion to serve over 350,000 patients reflect the strong commercial momentum. In January 2025, Huma and Pfizer's collaboration deployed FDA-cleared RPM for hemophilia in the U.S., demonstrating how specialized, condition-specific remote engagement can transform chronic disease outcomes and treatment adherence.

3. Mental Health Digitalization and Behavioral Engagement

In November 2025, InteliSense deployed a next-generation mental health engagement platform leveraging 20+ years of patient engagement expertise. The patient engagement solutions market outlook for mental health applications reflects sustained double-digit growth through 2034.

4. Wearable Device Integration and Continuous Health Monitoring

Consumer wearable devices are increasingly integrated with patient engagement platforms to deliver real-time biometric data into clinical decision workflows. This convergence of consumer wellness technology and clinical patient engagement creates powerful closed-loop care systems where patient-generated health data (PGHD) directly informs provider interventions.

Industry Value Chain Analysis

The patient engagement solutions value chain integrates technology infrastructure providers, solution developers, healthcare payers, healthcare providers, digital engagement platforms, and ultimately patients and caregivers. Each stage contributes distinct capabilities, from AI and cloud infrastructure to clinical integration expertise — with value creation occurring through the quality of patient experience delivered at the point of care.

|

Value Chain Stage |

Representative Players |

|

Technology Providers |

Microsoft Azure, AWS, Google Cloud, IBM Watson Health |

|

Solution Developers |

Epic Systems, Cerner, Allscripts, Athenahealth, GetWellNetwork |

|

Healthcare Payers |

UnitedHealth Group, CVS, Aetna, Anthem, CMS, NHS England |

|

Healthcare Providers |

Mayo Clinic, Kaiser Permanente, NHS Clinical Commissioning Groups, Cleveland Clinic |

|

Digital Health Platforms |

Teladoc Health, Huma, mPulse Mobile, PatientPop, GetWellNetwork, Amwell |

|

Patients & Caregivers |

Chronic disease patients, elderly, fitness users, mental health patients |

Technology Landscape in the Patient Engagement Solutions Industry

Artificial Intelligence and Machine Learning

Machine learning models analyze historical patient data to predict disengagement risk, missed appointments, and medication non-adherence, enabling proactive outreach before clinical deterioration occurs. AI-powered clinical decision support integrated with patient engagement platforms is enabling precision chronic disease management for populations of hundreds of thousands simultaneously.

Generative AI Advancements

Google Cloud announced new generative AI advancements for healthcare and life sciences, including the launch of Vertex AI Search for Healthcare and enhancements to Healthcare Data Engine and MedLM, aimed at improving interoperability, data search, and AI‑driven insights to help reduce administrative burden and support better patient outcomes.

Remote Patient Monitoring and Wearable Integration

RPM platforms integrate biometric alerts, trend analytics, and automated clinical escalation workflows, enabling care teams to manage large patient panels with targeted, data-driven interventions. Rimidi's March 2024 launch of the Rimidi Care Network, enabling healthcare providers to scale RPM, chronic care management, and continuous glucose monitoring through integrated software, exemplifies this technology convergence.

Mobile Health Applications and Patient Portals

In 2025, there were 313 million users of health apps, which were downloaded a total of 405 million times. Multi-channel engagement capabilities spanning SMS, email, in-app notifications, voice, and portal ensure reach across diverse patient populations with varying digital preferences and literacy levels.

Patient Engagement Solutions Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Therapeutic Area |

Chronic Diseases |

38.4% |

2025 |

|

Application |

Health Management |

35.8% |

2025 |

|

End User |

Providers |

🔒 |

2025 |

|

Component |

Software |

🔒 |

2025 |

| Delivery Type | Web-based/Cloud-based | 🔒 | 2025 |

|

Region |

North America |

38.6% |

2025 |

Segmentation by Therapeutic Area

To access detailed market analysis, Request Sample

Chronic diseases command a dominant 38.4% share in 2025, driven by the global epidemic of cardiovascular diseases and obesity, which collectively affect over 1.5 billion people worldwide. Mental health, at 16.9% share, represents the market's fastest-growing therapeutic area (CAGR ~16.3%), reflecting both post-pandemic behavioral health awareness and the growing clinical evidence base for digital mental health intervention efficacy.

Segmentation by Application

Health management leads application segments at 35.8% in 2025, reflecting healthcare providers' deployment of patient portals, medication management systems, care coordination tools, and clinical communication platforms. Home healthcare management, at 26.4%, is the fastest-growing application segment (CAGR ~15.1%), driven by the shift toward aging-in-place care models, post-acute hospital discharge support, and RPM platform deployments enabling clinical oversight of homebound patients.

Regional Patient Engagement Solutions Market Insights

North America commands the largest share at 38.6% in 2025, anchored by the U.S.’s USD 4.5 trillion+ annual healthcare market and a mature ecosystem of healthcare IT companies. ACA mandates patient-centered care, HITECH Act incentives for EHR adoption, and the transition to value-based care reimbursement models have created powerful structural demand for patient engagement technology.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

Major Companies |

|

North America |

38.6% |

ACA/HITECH mandates, value-based care, EHR maturity, chronic disease burden |

ACA, HITECH, HIPAA |

Epic Systems, Teladoc Health, Amwell, UnitedHealth Group |

|

Asia-Pacific |

26.3% |

Digital health strategies, ABDM India, aging populations, mobile-first adoption |

India ABDM, China NHC |

Practo, Ping An Good Doctor, Huma, Ada Health |

|

Europe |

22.4% |

EHDS framework, NHS digital programs, GDPR-compliant platforms |

GDPR, EU EHDS |

Babylon Health, Doctrin, Philips Healthcare, NHS X digital teams |

|

Latin America |

7.9% |

Telehealth expansion, mobile penetration, rural access improvement |

ANVISA, regional MoH |

Docway, Softway Medical, TuoTempo |

|

Middle East and Africa |

4.8% |

Smart hospital investments, national digital health programs, telehealth growth |

GCC eHealth, NHIF |

Malaffi (UAE), Sheba Digital, Okadoc |

Asia-Pacific holds a 26.3% share and is the fastest-growing regional market, projected at approximately 16.8% CAGR through 2034. China's Health China 2030 policy and national telemedicine expansion are accelerating digital health investment. Japan and South Korea's rapidly aging populations require innovative home healthcare management and RPM solutions.

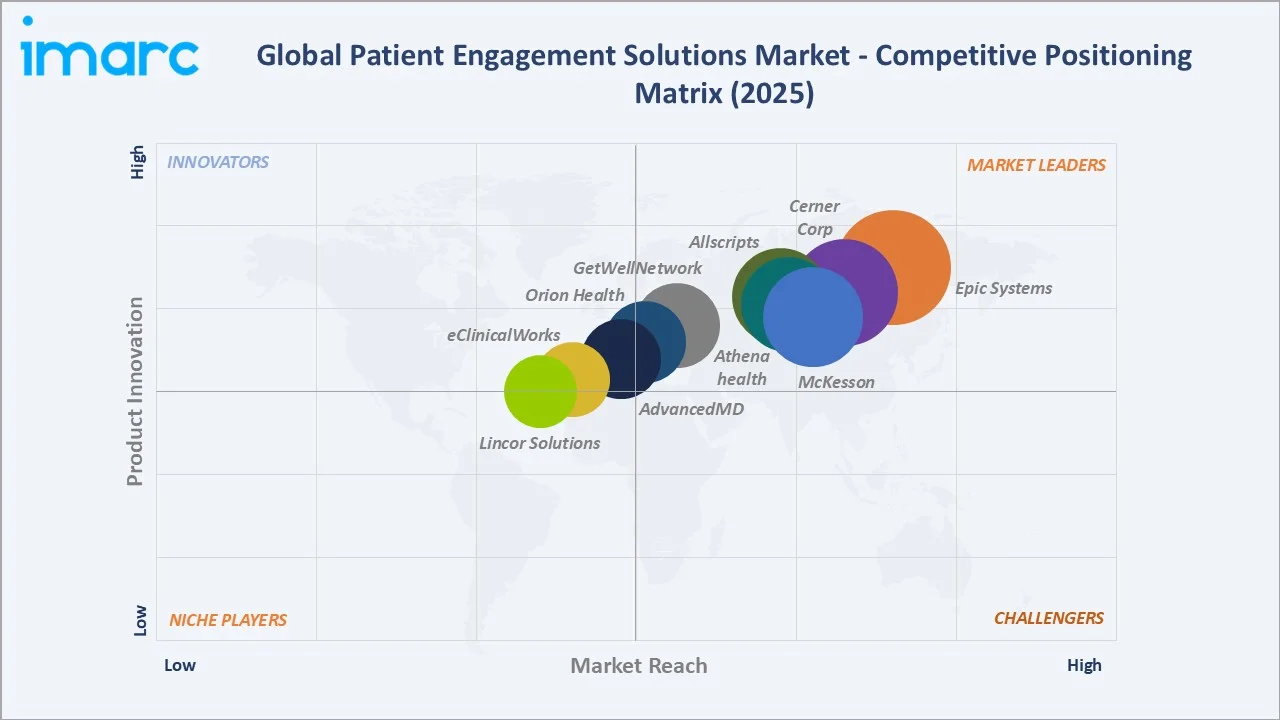

Competitive Landscape

The global patient engagement solutions market is moderately fragmented, with established healthcare IT giants, specialized digital health companies, and emerging AI-native startups competing across enterprise, mid-market, and specialty segments. Market leaders leverage comprehensive EHR integration, broad solution portfolios, and established clinical trust relationships, while innovative challengers differentiate through AI-native capabilities, condition-specific depth, and superior patient user experience design.

The market features intense competition, with players differentiating through user-friendly platforms, AI-driven insights, and interoperability with existing healthcare systems. Strategic collaborations, mergers, and continuous innovation remain key strategies for companies aiming to expand their footprint and strengthen market positioning.

|

Company Name |

Key Products/Brands |

Market Position |

Core Strength |

|

Epic Systems Corporation |

MyChart, Epic Care Everywhere |

Leader |

Comprehensive EHR-native patient engagement; 96% of large US hospitals; interoperability leadership |

|

Cerner Corporation (Oracle) |

HealtheLife |

Leader |

Cloud EHR migration; AI-powered clinical decision support; global expansion |

|

McKesson Corporation |

RelayHealth, CareEnhance |

Leader |

Pharmacy engagement; specialty care programs; medication adherence platforms |

|

Veradigm (Allscripts Healthcare Solutions) |

FollowMyHealth |

Challenger |

Open platform interoperability; ambulatory care focus; patient portal excellence |

|

Athenahealth Inc. |

athenaCommunicator, athenaNet |

Challenger |

Cloud-native ambulatory engagement; integrated billing + clinical workflows |

|

GetWellNetwork Inc. |

GetWell Inpatient, GetWell Loop |

Specialist |

Inpatient & community engagement; care navigation; condition-specific pathways |

|

Orion Health Ltd. |

Amadeus, Engage, Predict |

Specialist |

Population health + engagement convergence; AI-driven risk stratification |

|

AdvancedMD (Global Payments) |

AdvancedMD Patient Engagement |

Emerging |

Small-medium practice focus; integrated billing + engagement; cloud-native SaaS |

|

Medecision Inc. (HCSC) |

Aerial, Conversations |

Emerging |

Payer-centric engagement; care management; population health programs |

|

Lincor Solutions Limited |

LINC Patient Engagement |

Emerging |

Bedside engagement; hospital in-patient entertainment and health education |

Key Company Profiles

Epic Systems Corporation

Privately held, headquartered in Verona, Wisconsin, USA. Epic's MyChart patient portal is deployed across 96% of large US hospitals, making it the world's most widely adopted patient engagement platform.

- Product Portfolio: MyChart (patient portal), Epic Care Everywhere (interoperability), Healthy Planet (population health), Lucy (personal health records), and integrated telehealth capabilities within the Epic suite.

- Recent Developments: Continued investment in AI-powered care gap identification, predictive analytics for patient outreach, and expanded interoperability with Apple Health and Google Health. Active development of ambient AI documentation to reduce physicians' administrative burden.

- Strategic Focus: Deepening AI integration across the Epic platform; international market expansion beyond the US into Canada, Europe, and the Middle East; advancing patient-generated health data (PGHD) integration workflows.

Cerner Corporation (Oracle Health)

Acquired by Oracle Corporation in June 2022 for USD 28.3 Billion. Cerner serves over 27,000 healthcare facilities globally with integrated clinical and patient engagement solutions.

- Product Portfolio: HealtheLife (patient engagement portal), CareAware (IoT/RPM integration), PowerChart (clinical workflow), and Millennium EHR platform with embedded patient communication tools.

- Recent Developments: Oracle is accelerating the migration of Cerner's Millennium platform to Oracle Cloud Infrastructure, adding AI-driven clinical decision support and patient engagement automation capabilities. Active expansion in US federal health agencies, including VA and DoD.

- Strategic Focus: Cloud EHR modernization; AI-enhanced patient engagement automation; federal health market leadership; interoperability with Oracle's enterprise cloud ecosystem.

Veradigm (Allscripts Healthcare Solutions Inc.)

Chicago-based healthcare IT company serving over 180,000 physician practices, 7,500 hospitals, and 17,000 post-acute facilities globally with open, interoperable engagement platforms.

- Product Portfolio: FollowMyHealth (patient engagement portal), Jardogs (patient communication), Sunrise (acute care EHR), Professional EHR (ambulatory), and Allscripts Analytics Platform.

- Recent Developments: FollowMyHealth's open platform architecture enables third-party app integration, making it a preferred choice for health systems seeking flexible, consumer-facing patient engagement capabilities. Active in value-based care contracting support and care management workflow integration.

- Strategic Focus: Open platform interoperability leadership; ambulatory and specialty care engagement expansion; integration with consumer health apps and wearable platforms.

GetWellNetwork Inc.

Bethesda, Maryland-based company specializing in interactive patient engagement solutions for inpatient, ambulatory, and community settings across over 900 provider organizations.

- Product Portfolio: GetWell Inpatient (bedside engagement), GetWell Loop (post-acute follow-up), GetWell Community (population navigation), and GetWell Rounds (care rounding support).

- Recent Developments: Expanded digital care pathway library covering 600+ clinical conditions; integration with Amazon Alexa for voice-based inpatient engagement; growing adoption of GetWell Loop for post-discharge chronic disease management.

- Strategic Focus: Whole-health patient engagement across care settings; social determinants of health screening integration; community-based care navigation partnerships.

Market Concentration Analysis

The global patient engagement solutions market exhibits moderate fragmentation. Epic Systems leads in the US hospital segment, while the broader global market features meaningful competition from Oracle Health (Cerner), McKesson, Allscripts, Athenahealth, and a growing cohort of AI-native digital health companies. The top 5 players collectively hold an estimated 35–40% of global market revenue in 2025, reflecting the market's structural fragmentation across provider sizes, geographies, and specialty verticals.

Market fragmentation is particularly pronounced in the Asia-Pacific and Latin American markets, where local healthcare IT companies, government-backed digital health platforms, and regional telehealth providers compete alongside global incumbents. Condition-specific digital health companies focusing on mental health, diabetes management, and women's health are capturing meaningful share in their therapeutic niches through superior patient experience design and clinical content quality.

Consolidation activity is accelerating, as evidenced by Oracle's USD 28.3 Billion acquisition of Cerner, Teladoc Health's USD 18.5 Billion acquisition of Livongo Health, and Health Union's acquisition of Adfire Health. Platform consolidation toward comprehensive patient engagement ecosystems is expected to be a defining competitive dynamic through 2034.

Investment & Growth Opportunities

Fastest Growing Segments

- Mental Health Digital Platforms (CAGR ~16.3%): Post-pandemic behavioral health demand, clinician shortages, and growing digital mental health evidence base are creating substantial investment opportunities in AI-guided therapy apps and peer support community platforms.

- Home Healthcare Management (CAGR ~15.1%): The aging-in-place macro trend, RPM technology maturation, and post-acute care cost reduction imperatives are driving strong investment in home healthcare management platforms. Smart Meter's 300% sales growth and Huma's Pfizer collaboration demonstrate the strong commercial momentum in this high-growth application segment.

Emerging Markets

- India: India's ABDM digital health mission, digital healthcare projected to reach USD 37 billion by 2030, and a massive underserved patient population of 1.4 billion creates an unparalleled opportunity for mobile-first, multilingual patient engagement platforms serving both urban and rural demographics across chronic disease, maternal health, and primary care segments.

- GCC and North Africa: Saudi Arabia's Vision 2030 healthcare transformation program, UAE's Smart Health initiative, and Egypt's Universal Health Insurance expansion are creating structured demand for patient engagement platforms meeting GCC regulatory standards and Arabic-language user experience requirements.

Venture Investment Trends

Assort Health has closed a USD 76 million Series B funding round led by Lightspeed Venture Partners to expand its agentic AI‑powered patient engagement platform, Assort OS, which uses AI agents across voice, text, and web to automate patient communications from scheduling to care navigation and prescription renewals. The new capital will accelerate product development and workforce growth as the company scales to meet rising demand for AI‑driven patient experience solutions.

Future Patient Engagement Solutions Market Outlook (2026-2034)

The global patient engagement solutions market is positioned for exceptional, sustained growth through 2034, supported by the intersection of aging population demographics and the transformative enabling power of AI & cloud computing. From USD 47.15 billion in 2025, the market will reach USD 157.20 billion by 2034, representing an absolute value addition of over USD 110 billion and confirming patient engagement as one of healthcare's most consequential infrastructure investments in the coming decade.

Asia-Pacific will emerge as the dominant growth engine through 2034, with India, China, and Southeast Asia's digital health investment and large patient populations driving absolute volume growth at CAGR ~16.8%. North America and Europe will retain premium market positions in high-value AI-native, value-based care-aligned engagement platforms.

Research Methodology

Primary Research

Primary research for this report involved structured interviews and surveys with over 250 industry participants in 2025, including healthcare CIOs and CMIOs, patient engagement platform product leaders, healthcare payer technology executives, chronic disease management specialists, digital health investors, and patient advocacy representatives across North America, Europe, and Asia-Pacific.

Secondary Research

Secondary research encompassed comprehensive review of company annual reports, regulatory submissions to FDA and HHS, trade publications (Health Affairs, HIMSS Media, Healthcare IT News, Modern Healthcare), government healthcare IT adoption data (ONC, NHS Digital, NHC), industry association databases (HIMSS Analytics, CHIME), academic medical literature on patient engagement outcomes, and publicly available financial data.

Forecasting Models

Market size estimations were developed using bottom-up application-level demand modeling aggregated across therapeutic areas, applications, delivery types, and end user segments, supplemented by top-down validation against total healthcare IT spend benchmarks and patient engagement technology penetration rates by market segment. Scenario analysis covering base, optimistic, and conservative cases addressed healthcare policy uncertainty, AI adoption rate variability, and cybersecurity-driven adoption constraints.

Patient Engagement Solutions Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Therapeutic Areas Covered |

|

| Applications Covered | Social Management, Health Management, Home Healthcare Management, Financial Health Management |

| End Users Covered | Payers, Providers, Others |

| Components Covered | Software, Services, Hardware |

| Delivery Types Covered | Web-based/Cloud-based, On-premises |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Epic Systems Corporation, Cerner Corporation (Oracle), McKesson Corporation, Veradigm (Allscripts Healthcare Solutions), Athenahealth Inc., GetWellNetwork Inc., Orion Health Ltd., AdvancedMD (Global Payments), Medecision Inc. (HCSC), Lincor Solutions Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the patient engagement solutions market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global patient engagement solutions market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the patient engagement solutions industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Patient Engagement Solutions Market Report

The global patient engagement solutions market was valued at USD 47.15 Billion in 2025 and is projected to reach USD 157.20 Billion by 2034, growing at a CAGR of 13.89% during 2026-2034.

The market is forecast to grow at a CAGR of 13.89% during 2026-2034, driven by chronic disease management demand, value-based care adoption, telehealth expansion, and AI integration across healthcare delivery systems globally.

North America dominates with a 38.6% share in 2025, supported by ACA and HITECH Act mandates, EHR adoption in hospitals, high healthcare IT investment, and a leading ecosystem of patient engagement solution providers.

Asia-Pacific is the fastest-growing region at approximately 16.8% CAGR through 2034, driven by India's ABDM digital health mission, China's Health China 2030 strategy, and rapid mHealth adoption across large underserved patient populations.

Key drivers include rising chronic disease prevalence, telehealth and mHealth technology expansion, AI/ML integration for personalization, value-based care reimbursement models, and government digital health mandates across major markets.

Chronic diseases hold the largest therapeutic area share at 38.4% in 2025. Diabetes, cardiovascular disease, and obesity require continuous digital engagement, monitoring, and adherence support — creating sustained, recurring demand for patient engagement platforms.

Health management leads at 35.8% in 2025, driven by EHR-integrated patient portal deployment, medication adherence platforms, care plan communication tools, and clinical team messaging systems across hospital and ambulatory care settings globally.

Key trends include AI-powered personalized care plans, telehealth and RPM platform adoption, mental health digitalization, wearable device integration for continuous monitoring, and value-based care-aligned population health engagement programs.

Major players include Epic Systems, Cerner (Oracle Health), McKesson, Allscripts Healthcare Solutions, Athenahealth, GetWellNetwork, Orion Health, AdvancedMD (Global Payments), Medecision (HCSC), Lincor Solutions, EMMI Solutions (Wolters Kluwer), and Phytel (IBM).

Key challenges include data privacy and cybersecurity risks, digital divide barriers limiting equitable access, high EHR integration complexity and costs, and patient engagement fatigue from proliferating digital health touchpoints.

Top investment opportunities include AI-native engagement platforms, mental health digital solutions, home healthcare management and RPM platforms, and emerging market digital health infrastructure in India, Southeast Asia, and GCC countries.

The market will reach USD 157.20 Billion by 2034, owing to AI-powered personalization, comprehensive care platform convergence, Asia-Pacific expansion, and value-based care alignment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)