Test and Measurement Equipment Market Size, Share, Trends and Forecast by Product, Service Type, End Use Industry, and Region 2026-2034

Global Test and Measurement Equipment Market Size, Share, Trends & Forecast (2026-2034)

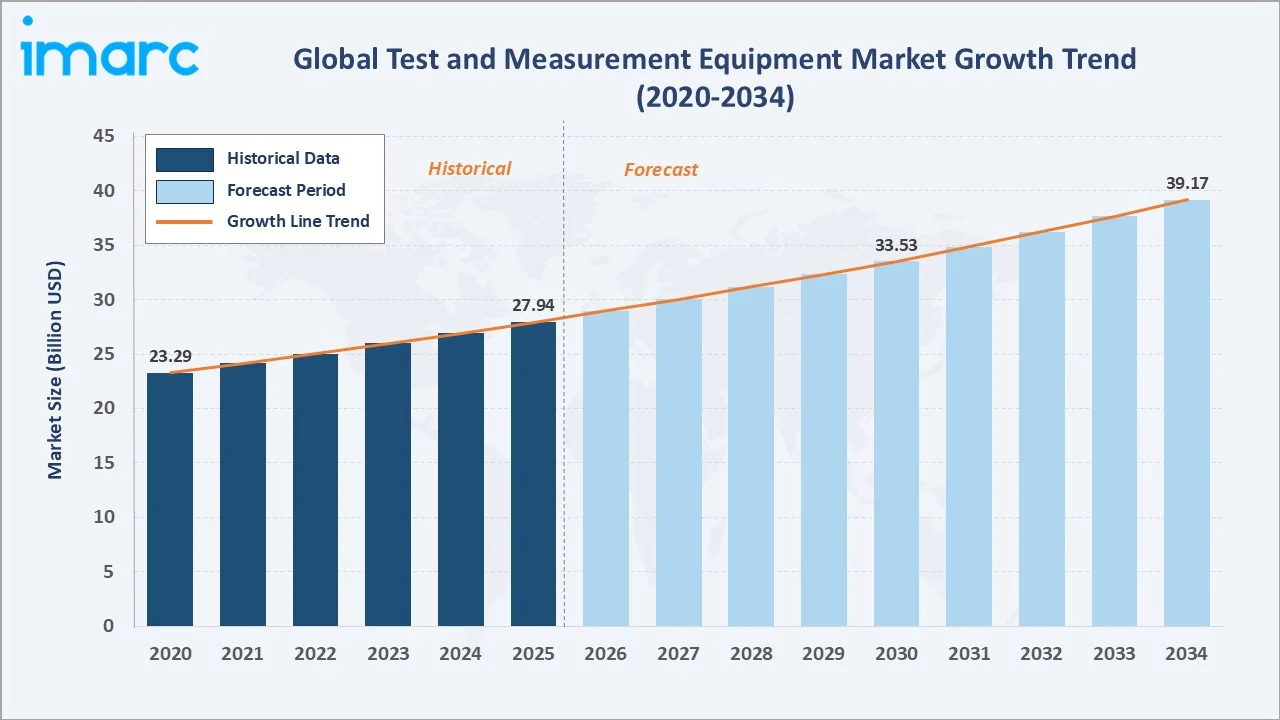

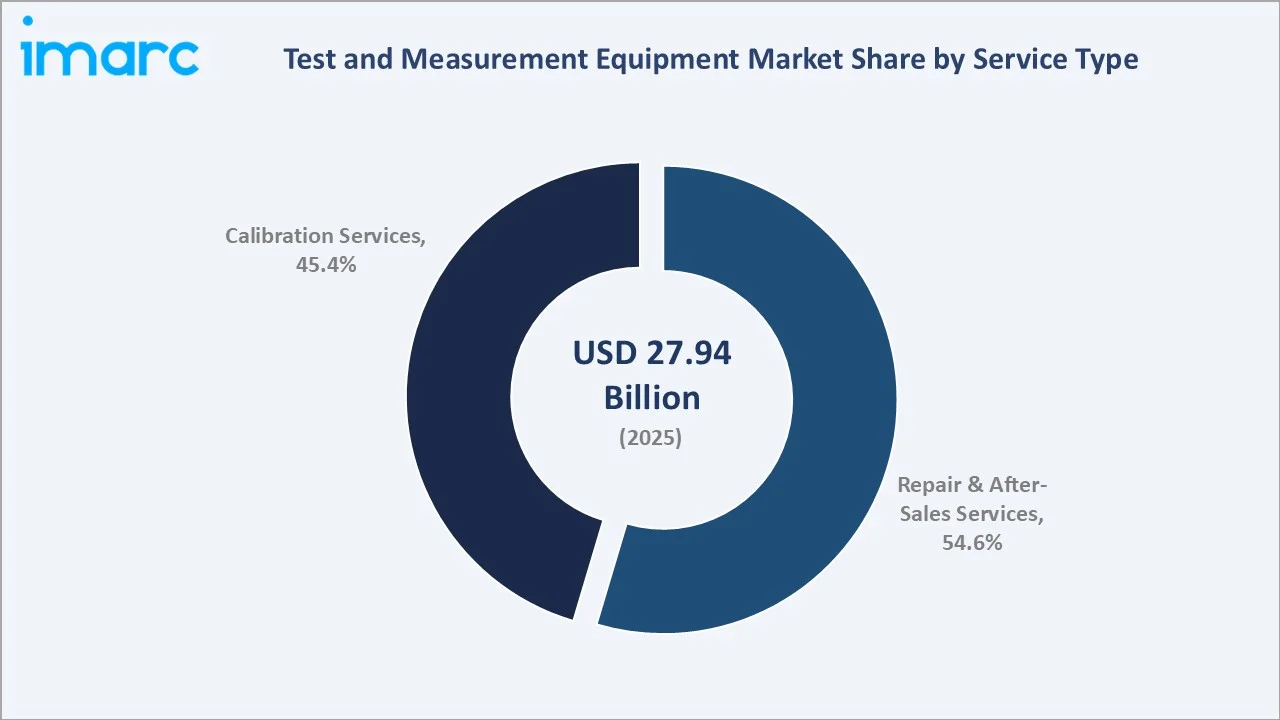

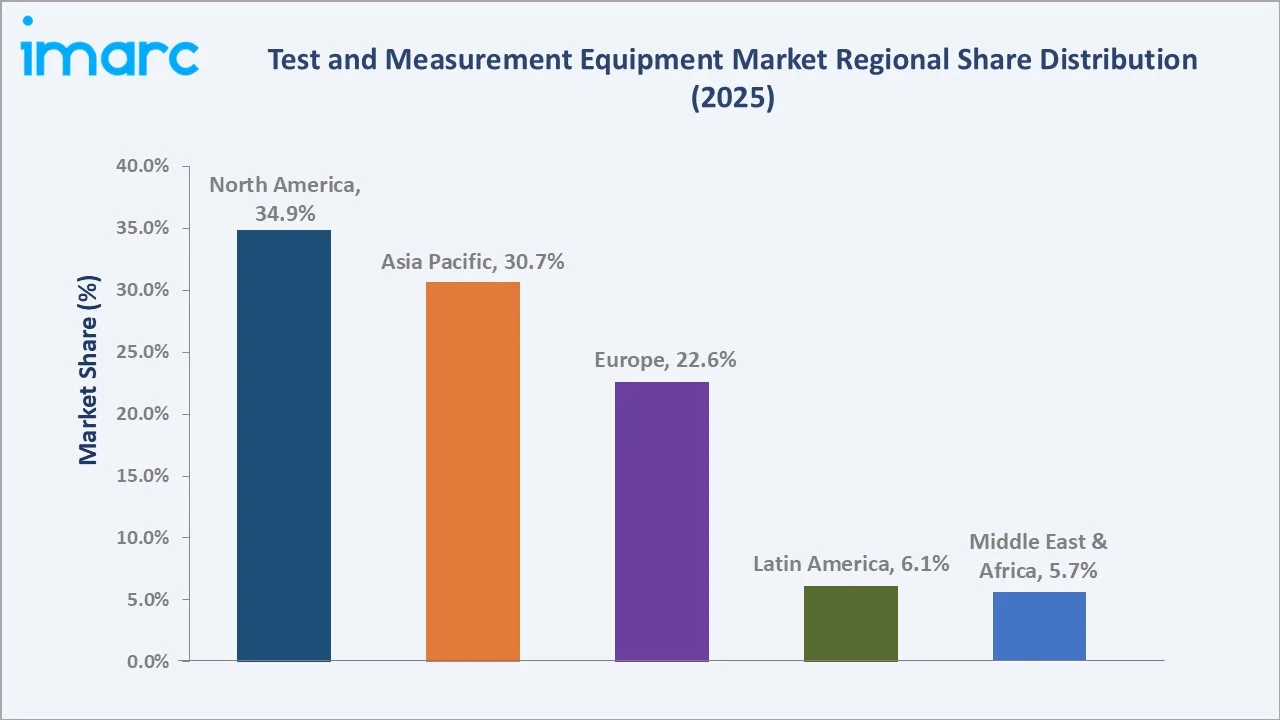

The global test and measurement equipment market size was valued at USD 27.94 Billion in 2025 and is projected to reach USD 39.17 Billion by 2034, exhibiting a CAGR of 3.71% during the forecast period 2026-2034. Rising demand for precision measurement across 5G, semiconductor, and EV manufacturing, coupled with expanding industrial automation, rapid IoT device validation requirements, and defence modernisation budgets, is driving the test and measurement equipment market growth. General Purpose Test Equipment (GPTE) leads the product segment at 62.8% in 2025, while Repair and After-Sales Services dominate the service segment at 54.6%. North America accounts for 34.9% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 27.94 Billion |

|

Forecast Market Size (2034) |

USD 39.17 Billion |

|

CAGR (2026-2034) |

3.71% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (34.9% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~4.8%) |

|

Leading Product Segment |

General Purpose Test Equipment (62.8%, 2025) |

|

Leading Service Segment |

Repair & After-Sales Services (54.6%, 2025) |

The global test and measurement equipment market trajectory from 2020 through 2034 shows a consistent historical expansion from USD 23.29 Billion in 2020 to USD 27.94 Billion in 2025, followed by a steady forecast curve driven by 5G rollouts, semiconductor capital expenditure cycles, and EV/ADAS validation programmes.

To get more information on this market, Request Sample

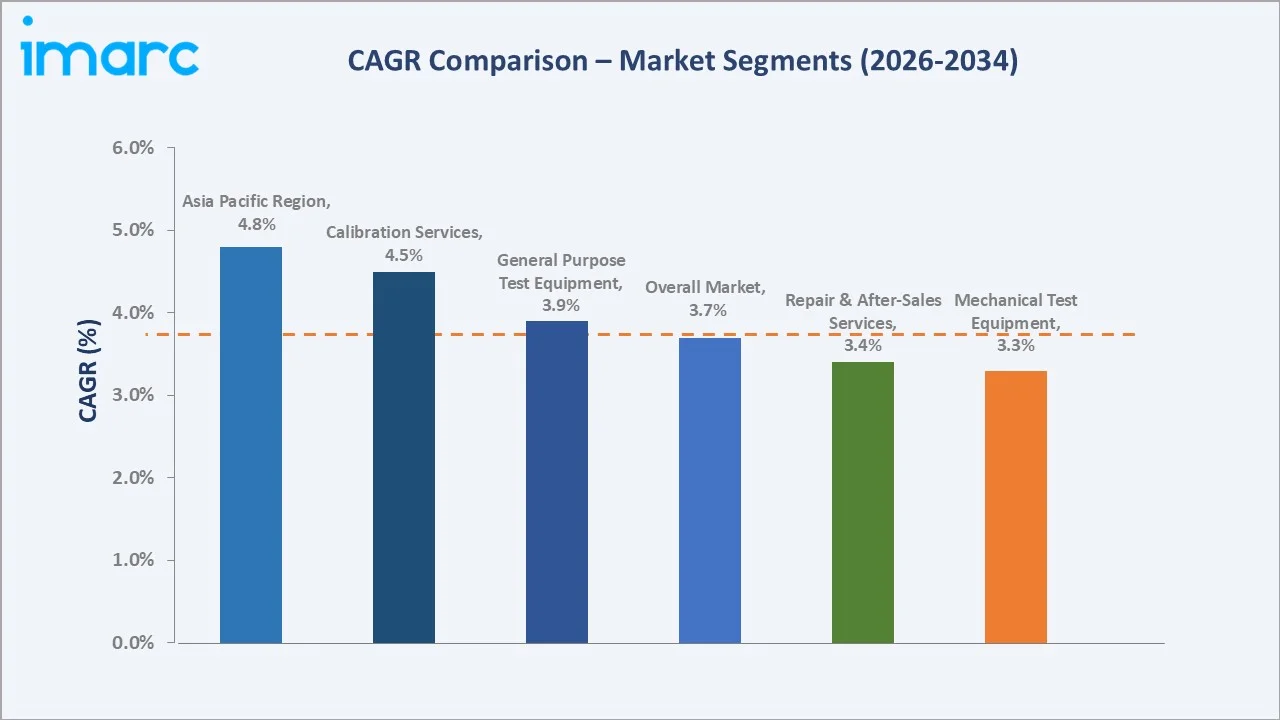

Segment-level CAGR comparisons highlight Asia Pacific and calibration services as the fastest-growing pockets within the global test and measurement equipment industry analysis through 2034, outpacing the overall market's 3.71% growth rate.

Executive Summary

The global test and measurement equipment market is transitioning through a mature growth phase, driven by the convergence of 5G infrastructure deployment, semiconductor capacity expansion, and the electrification of mobility. Valued at USD 27.94 Billion in 2025, the market is forecast to reach USD 39.17 Billion by 2034 at a CAGR of 3.71%. China alone had deployed over 4.8 million 5G base stations by the end of 2025, exceeding its national planning targets, while South Korea and Japan have been early global leaders in 5G rollout, collectively driving sustained demand for high-frequency RF test and measurement equipment across the Asia-Pacific region.

General Purpose Test Equipment (GPTE) commands a dominant product-segment share of 62.8% in 2025, led by oscilloscopes, spectrum analyzers, signal generators, and multimeters used in R&D, manufacturing, and field service applications. Mechanical Test Equipment (MTE) at 37.2% is anchored by materials testing, vibration testing, and dimensional metrology in aerospace and automotive verticals. On the service side, Repair and After-Sales Services account for 54.6% of revenue in 2025, reflecting the high-value installed base of legacy instruments that require ongoing support.

North America leads with a 34.9% global revenue share in 2025, anchored by Keysight, Tektronix, and National Instruments' domestic installed base, alongside heavy defence and semiconductor R&D spending. Asia Pacific follows at 30.7% in 2025 and is the fastest-growing region, propelled by China's semiconductor self-sufficiency drive and India's IT-services-led test infrastructure build-out. Europe holds 22.6% in 2025, supported by Germany's automotive test leadership and the UK's aerospace cluster.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

General Purpose Test Equipment – 62.8% share (2025) |

|

Largest Service Type Segment |

Repair & After-Sales Services – 54.6% share (2025) |

|

Leading Region |

North America – 34.9% revenue share (2025) |

|

Fastest-Growing Region |

Asia Pacific – 30.7% share in 2025, ~4.8% CAGR |

|

Top Companies |

Keysight Technologies, Rohde & Schwarz, TEKTRONIX, INC., NATIONAL INSTRUMENTS CORP, Anritsu, Advantest Corporation, Fluke Corporation, Yokogawa Electric Corporation, Teledyne Technologies Incorporated, and VIAVI Solutions Inc. |

Key Analytical Observations Supporting the Above Data:

- General Purpose Test Equipment's 62.8% dominance in 2025 reflects the broad deployment of oscilloscopes, spectrum analyzers, and signal generators across electronics, telecom, and R&D laboratories, where precision measurement underpins product development cycles.

- Repair and After-Sales Services at 54.6% in 2025 underscore the extended lifecycle of high-value instruments with many flagship spectrum analyzers remaining in service for 10-15 years, creating structural recurring revenue for OEMs.

- North America's 34.9% global share in 2025 is powered by the CHIPS Act-funded semiconductor build-out, with major chipmakers accelerating private investment commitments to re-shore and expand domestic manufacturing capacity.

Global Test and Measurement Equipment Market Overview

Test and measurement equipment encompasses electronic, mechanical, and software-based instruments used to evaluate the electrical, physical, and functional performance of devices, materials, and systems. Core product categories include oscilloscopes, signal analyzers, spectrum analyzers, multimeters, power analyzers, vector network analyzers, materials testing machines, and automated test equipment (ATE) used in semiconductor production.

Applications span telecommunications (5G/6G network validation), semiconductors (wafer and device test), automotive (EV battery, ADAS, radar), aerospace and defence (radar, avionics), industrial manufacturing (predictive maintenance), and academic research laboratories. Macroeconomic enablers include AI-driven data centre expansion, semiconductor revenues exceeding USD 600 billion, and accelerating electrification across automotive and industry, driving demand for advanced electrical, RF, and reliability testing solutions.

Market Dynamics

To evaluate market opportunities, Request Sample

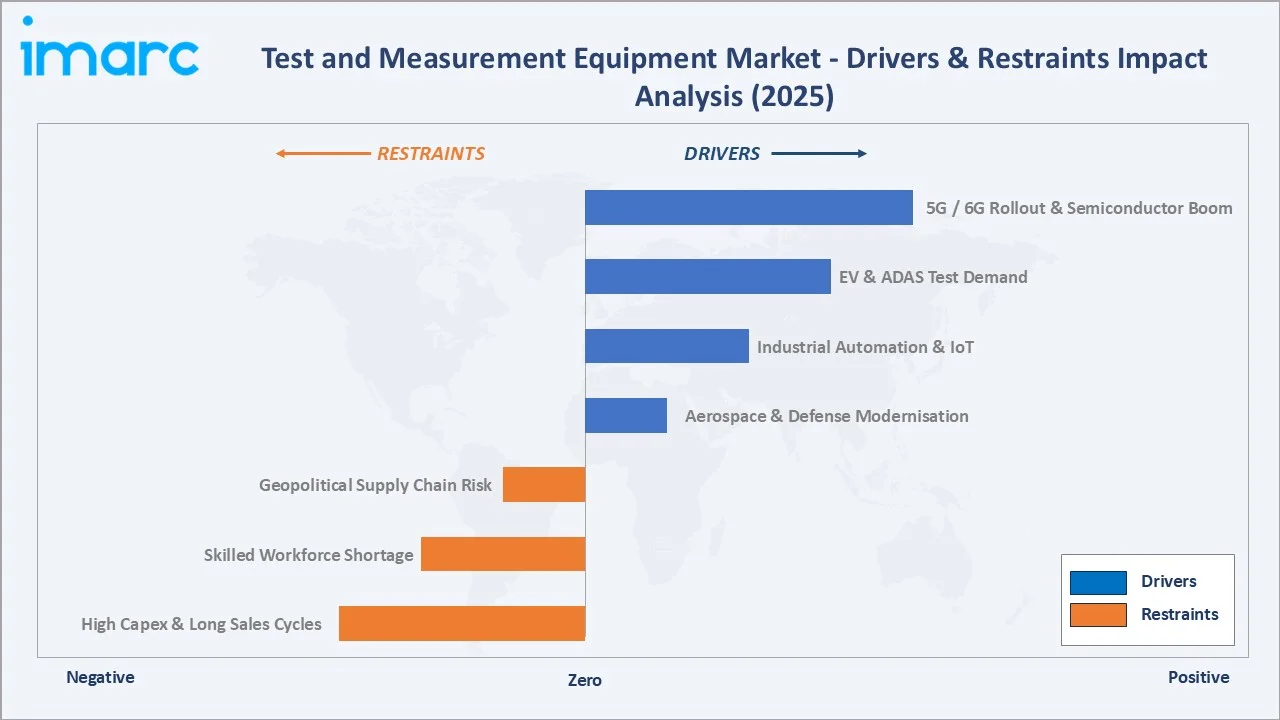

Market Drivers

- 5G, 6G, and Semiconductor Capex: Over 2.25 billion 5G connections existed globally in 2024, and the ITU has allocated additional mmWave spectrum, driving sustained demand for vector network analyzers and spectrum test instruments up to 110 GHz.

- EV and ADAS Validation: Global EV sales crossed 17 million units in 2024 (IEA), with each EV platform requiring bidirectional power supply testing, battery cell cycling, and radar/lidar validation.

- Industrial Automation and IoT Expansion: Smart factory deployments and the rollout of over 39 billion connected IoT devices projected by 2030 are creating continuous demand for electrical, RF, and protocol test instruments, particularly in predictive maintenance applications.

- Aerospace and Defence Modernisation: Global defence spending crossed USD 2.4 Trillion in 2024 (SIPRI), funding radar, avionics, and electronic warfare programmes that depend on high-frequency mmWave and satellite communication test systems.

Market Restraints

- High Capital Expenditure and Long Sales Cycles: Flagship vector network analyzers and high-end ATE systems can cost USD 0.5-2 Million per unit, with procurement cycles stretching 6-18 months in enterprise accounts, slowing total market acceleration.

- Skilled Workforce Shortage: Operating advanced mmWave, quantum, and semiconductor test platforms requires specialised engineers; global shortages in RF and test engineering talent are constraining utilisation rates.

- Geopolitical Supply Chain Risk: US-China export controls on advanced semiconductor testing equipment introduced since 2023 have created compliance complexity and market-access constraints for Tier-1 suppliers in strategic geographies.

Market Opportunities

- AI-Augmented Test Automation: An estimated 70% of enterprises are projected to adopt AI-augmented test automation by 2026, creating an entirely new software-defined instrumentation revenue category, with Liquid Instruments' 2025 Generative Instrumentation launch as a reference deployment.

- Quantum and Advanced Packaging Testing: Quantum computing validation and 3D-IC chiplet packaging testing represent emerging high-margin niches where venture-backed specialists are building modular platforms.

- Calibration-as-a-Service and Rentals: Electro Rent's October 2025 AI-driven cloud portal for rental fleet optimisation illustrates how service-layer monetisation is becoming a growth vector beyond hardware sales.

Market Challenges

- Technology Obsolescence Risk: Rapid evolution from 5G to 6G and from silicon to compound semiconductors means instruments face shorter useful lives, increasing capex churn for end-users and creating inventory risk for suppliers.

- Fragmentation in Low-End Segments: Aggressive pricing from Chinese manufacturers like UNI-T and Hioki in entry-level multimeters and oscilloscopes is compressing margins for Western suppliers in emerging markets.

- Cybersecurity for Connected Instruments: IoT-enabled test instruments with cloud-based analytics introduce attack surfaces that require ongoing security patch management and certification overhead.

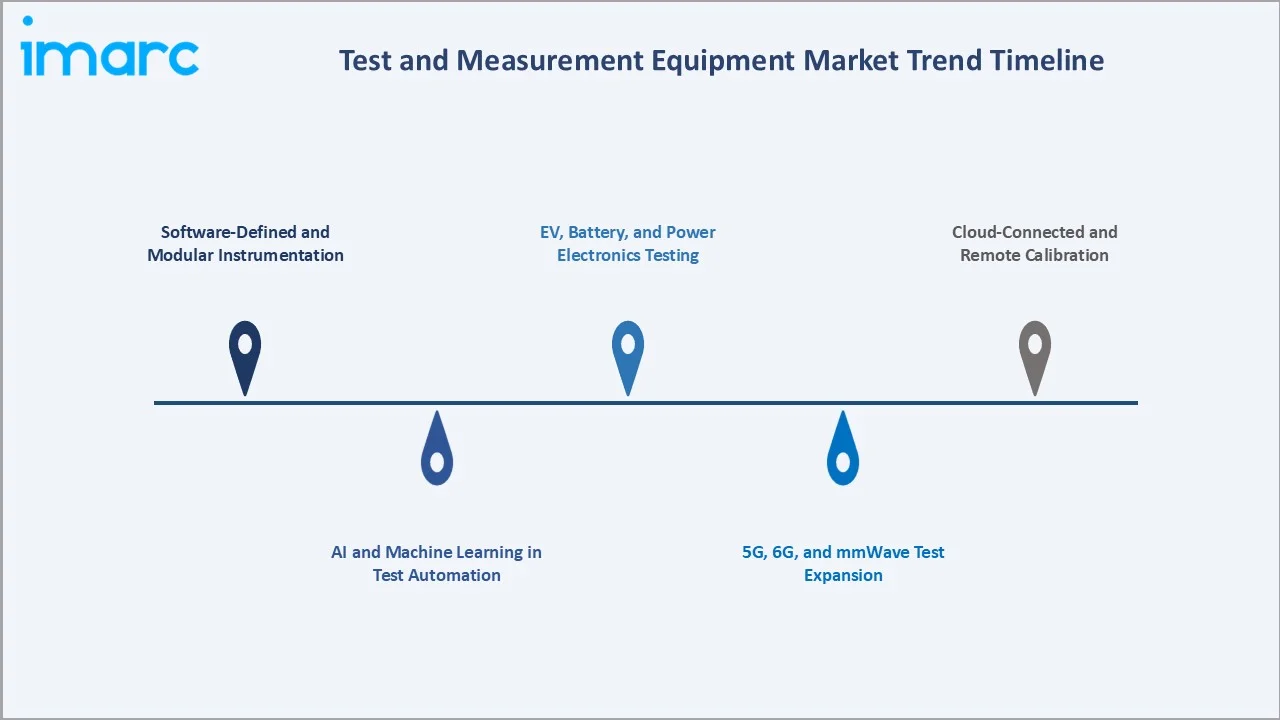

Emerging Market Trends

1. Software-Defined and Modular Instrumentation

The industry is shifting from hardware-centric fixed-function boxes to software-defined platforms where a single chassis performs multiple measurement functions via firmware. NI's PXI platform and Rohde & Schwarz's modular R&S ZNA are reference architectures. This model extends instrument lifecycles and enables subscription-based feature monetisation.

2. AI and Machine Learning in Test Automation

Generative AI and ML are entering test workflows at speed. Emerson's July 2025 Nigel AI Advisor integration and Liquid Instruments' Generative Instrumentation launch, which lets engineers create custom instruments using natural language, mark the technology's mainstream arrival.

3. 5G, 6G, and mmWave Test Expansion

Rapid densification of 5G infrastructure across Asia, particularly in China, South Korea, and Japan, has accelerated large-scale base station deployments, driving increased demand for high-frequency spectrum and network analysis solutions up to 110 GHz.

4. EV, Battery, and Power Electronics Testing

The migration from engine dynamometers to electric-drive test cells is opening opportunities for modular instrumentation reconfigurable across battery, inverter, and motor benches. Axiometrix’s CANSASflex HISO-T-8-2L module, launched in 2025, exemplifies high-voltage measurement innovation for next-generation e-mobility testing.

5. Cloud-Connected and Remote Calibration

Cloud-based calibration platforms, remote instrument access, and digital twin integration are transitioning calibration from on-site service to distributed service delivery, reducing downtime and enabling predictive calibration for high-value assets.

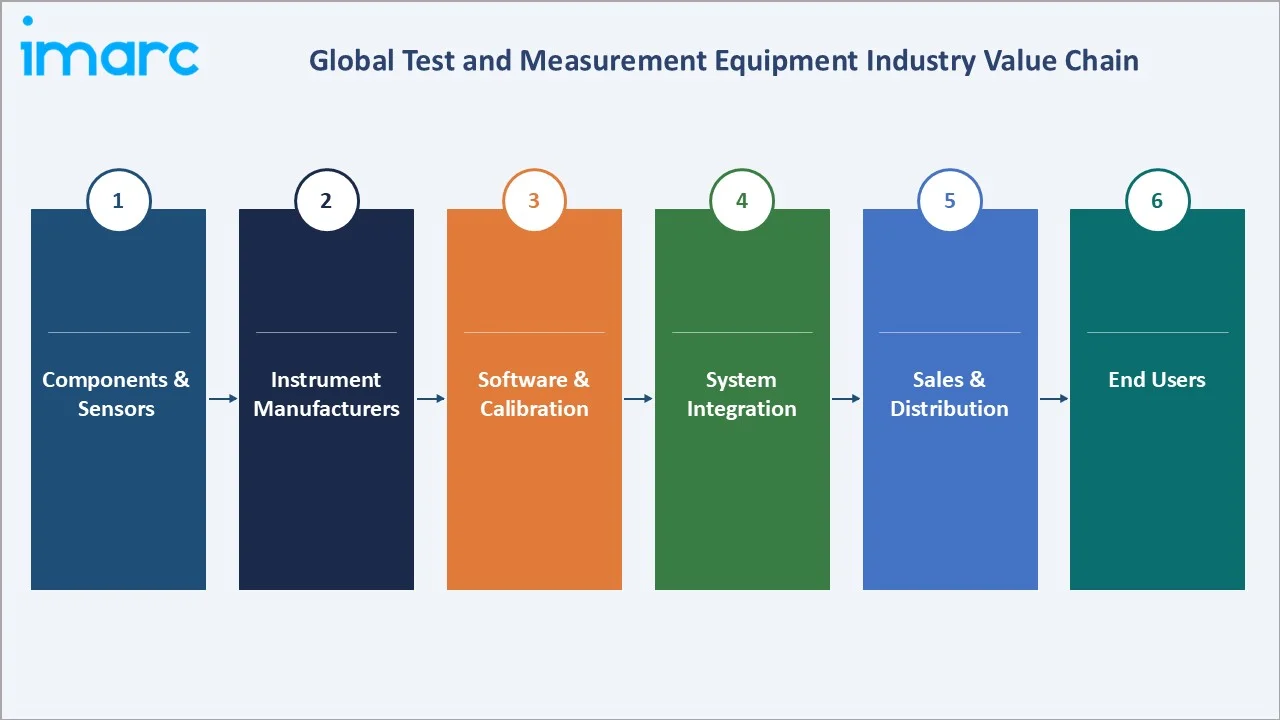

Industry Value Chain Analysis

The test and measurement equipment value chain spans six integrated stages from raw material and semiconductor supply through end-user laboratories. Each stage presents distinct margin profiles and technology investment requirements.

|

Stage |

Key Players / Examples |

|

Components & Sensors |

Components and sensors provide foundational inputs enabling accurate measurement, signal capture, and system performance evaluation. |

|

Instrument Manufacturers |

Instrument manufacturers design and produce precision hardware platforms integrated with software for advanced testing applications. |

|

Software & Calibration |

Software and calibration services ensure measurement accuracy, automate workflows, and provide traceability across testing environments. |

|

System Integration |

System integrators combine instruments, software, and automation into turnkey solutions tailored for specific industry requirements. |

|

Sales & Distribution |

Sales and distribution channels deliver equipment globally through direct sales, distributors, and rental service providers. |

|

End Users |

End users apply test equipment across telecom, semiconductor, automotive, aerospace, and research for validation purposes. |

Instrument manufacturers hold the highest strategic value by combining precision hardware with proprietary software, while software and calibration services are emerging as high-margin growth areas, driven by consolidation led by companies like Transcat.

Technology Landscape in the Test and Measurement Equipment Industry

High-Bandwidth Signal Analysis and mmWave

The frontier of signal analysis is advancing into the sub-terahertz range, with solutions such as MPI’s 250 GHz broadband probe system integrated with Keysight’s PNA-X platform. In addition, Keysight’s 800G and 1.6T Ethernet validation platforms for AI and high-performance computing networks highlight the rapid evolution of high-speed signal and interconnect testing.

Materials and Precision Innovation

Advances in precision sensors, low-noise amplifiers, and high-resolution ADCs are pushing measurement floors to sub-femtoampere current levels, enabling next-generation battery, biomedical, and quantum device characterisation. GW Instek's GPP-1000 Series programmable DC power supplies, launched in September 2025, exemplify the precision trend.

Smart Connectivity and IoT Integration

Modern instruments now ship standard with Wi-Fi 6, Ethernet, and cloud connectivity. Fluke Corporation and Keysight are embedding cloud analytics capabilities into portable field instruments, enabling real-time data streaming to enterprise dashboards and supporting predictive maintenance across distributed industrial assets.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Product | General Purpose Test Equipment (GPTE) |

62.8% |

2025 |

| Service Type | Repair Services/After-Sales Services |

54.6% |

2025 |

| End Use Industry | Automotive and Transportation |

🔒 |

2025 |

|

Region |

North America |

34.9% |

2025 |

By Product Type

General Purpose Test Equipment (GPTE) commands a 62.8% share in 2025, reflecting the broad deployment of oscilloscopes, multimeters, signal generators, and spectrum analyzers across every industrial and research setting. The GPTE segment benefits from high replacement cycles and the entry of Chinese mid-tier suppliers, expanding accessibility.

To access detailed market analysis, Request Sample

Mechanical Test Equipment (MTE) at 37.2% in 2025 covers materials testing machines, vibration and shock test systems, and dimensional metrology instruments, driven by aerospace qualification testing, automotive durability validation, and EV battery mechanical stress testing.

By Service Type

Repair and After-Sales Services lead with 54.6% in 2025, reflecting the long service life of high-value test instruments and the critical role of OEM-authorised repair networks. Keysight, Fluke, and Rohde & Schwarz operate global service depots supporting equipment with 10–15-year operational lives.

Calibration Services at 45.4% in 2025 are anchored by ISO/IEC 17025 and NIST-traceable calibration requirements across aerospace, automotive, and pharmaceutical industries. Market consolidation is accelerating, led by calibration service providers such as Transcat through ongoing acquisitions and network expansion.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

34.9% |

CHIPS Act-funded semiconductor investment, defence R&D, Keysight/Tektronix/NI installed base, EV test labs |

|

Asia Pacific |

30.7% |

China semiconductor localisation, India 6.3% CAGR IT services, Japan ATE leadership, Korea 5G |

|

Europe |

22.6% |

Germany auto/industrial test, UK aerospace, EU 6G research funding, R&S mmWave leadership |

|

Latin America |

6.1% |

Brazil and Mexico manufacturing expansion, automotive electronics, foreign direct investment |

|

Middle East & Africa |

5.7% |

Saudi Vision 2030, UAE telecom and defence build-out, South Africa industrial base |

North America commands a 34.9% global revenue share in 2025, led by the United States, which hosts the headquarters of Keysight Technologies, Tektronix, National Instruments, Fluke, and Teledyne. Demand is anchored by robust defence and aerospace R&D budgets, expanding 5G and emerging 6G network build-outs, accelerating semiconductor onshoring under federal incentive programmes, and the rapid scale-up of EV and battery manufacturing across the region.

Asia Pacific accounts for 30.7% in 2025 and is the fastest-growing region. Europe holds 22.6% in 2025, anchored by Germany's automotive test leadership, the UK's aerospace cluster, and EU-funded 6G research programmes. Latin America at 6.1% and Middle East & Africa at 5.7% remain smaller but feature pockets of high growth around Brazil's automotive base and Saudi Arabia's Vision 2030 smart infrastructure programmes.

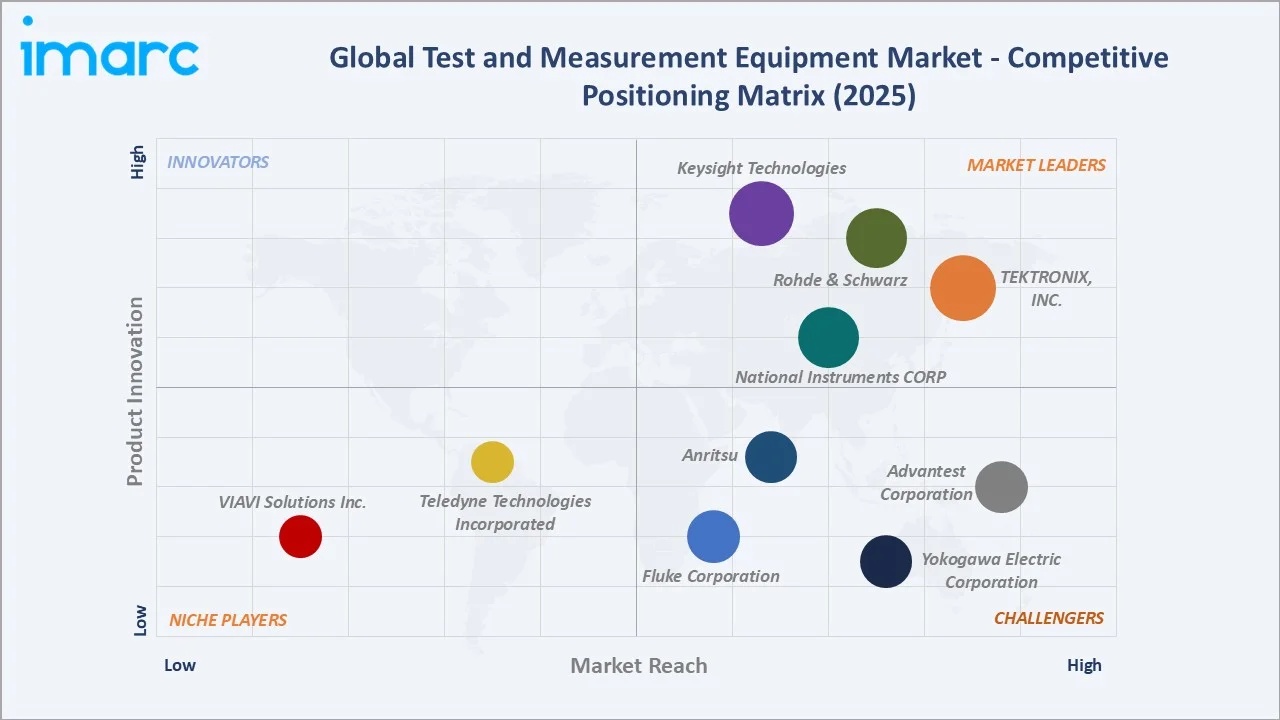

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Position |

Core Strength |

|

Keysight Technologies |

Keysight Ixia |

Leader |

RF/microwave, 5G/6G test, semiconductor, automotive |

|

Rohde & Schwarz |

R&S ZNA, CMX500 |

Leader |

mmWave, network analyzers, cellular protocol test |

|

TEKTRONIX, INC. |

DPO, MSO |

Leader |

Oscilloscopes, real-time analysis, field portables |

|

National Instruments CORP |

LabVIEW, PXI |

Leader |

Modular instrumentation, software-defined test |

|

Anritsu |

Anritsu Site Master |

Challenger |

Network test, optical, wireless/cellular |

|

Advantest Corporation |

V93000, T2000 |

Challenger |

Semiconductor ATE, memory and SoC test |

|

Fluke Corporation |

Fluke DMM Series |

Challenger |

Field service DMMs, industrial instruments |

|

Yokogawa Electric Corporation |

Yokogawa DLM, WT |

Challenger |

Power analyzers, precision measurement |

|

Teledyne Technologies Incorporated |

Teledyne LeCroy Test Solutions |

Emerging |

High-bandwidth oscilloscopes, protocol analysis |

|

VIAVI Solutions Inc. |

ONMSi |

Emerging |

Network and optical test, fiber/monitoring |

The test and measurement equipment competitive landscape is moderately consolidated. The top five suppliers control roughly 50-55% of global revenue in 2025, with Keysight Technologies leading at an estimated 18% market share. Chinese domestic suppliers including Hioki, UNI-T, and Uni-Trend Technology are expanding aggressively in mid-tier segments, while specialist players like Pico Technology and Spectrum Instrumentation thrive in PC-based digitizer niches.

Key Company Profiles

Keysight Technologies

Keysight Technologies is the global market leader in electronic design and test solutions, spun off from Agilent Technologies in 2014 and headquartered in Santa Rosa, California with operations spanning 100+ countries.

- Product & Platform Portfolio: Oscilloscopes (Infiniium series), vector network analyzers (PNA-X), signal generators, spectrum analyzers, protocol analyzers, and the Ixia network test platform.

- Recent Developments: In March 2025, Keysight introduced two new sampling oscilloscopes for 1.6T optical transceiver testing. In July 2025, the company upgraded its PXE EMI Receiver with real-time TDS up to 1 GHz.

- Strategic Focus: Keysight's strategy centres on bandwidth leadership in 5G/6G and semiconductor test, expansion of its software and services portfolio, and strategic alliances with hyperscalers for AI infrastructure validation.

Rohde & Schwarz

Rohde & Schwarz is a privately-held German technology group, headquartered in Munich, specialising in test and measurement, secure communications, broadcast, and cybersecurity.

- Product & Platform Portfolio: R&S ZNA vector network analyzers, R&S CMX500 cellular protocol testers, R&S SMW signal generators, and R&S FSW signal and spectrum analyzers.

- Recent Developments: In November 2025, Nokia and Rohde & Schwarz created and successfully tested a 6G radio receiver using AI technologies, with Nokia Bell Labs validating it using 6G test equipment and methodologies from Rohde & Schwarz.

- Strategic Focus: Rohde & Schwarz prioritises mmWave and sub-THz frontier bandwidth leadership, deep partnerships with cellular standards bodies, and integrated test solutions for 6G research.

Tektronix, Inc.

Tektronix, founded in 1946, is the operating brand within Fortive Corporation's test and measurement platform, headquartered in Beaverton, Oregon. The Tektronix portfolio, combined with Fluke and other Fortive brands, represents one of the largest global test and measurement revenue pools.

- Product & Platform Portfolio: Tektronix DPO/MSO oscilloscopes, arbitrary waveform generators, logic analyzers, and programmable power supplies; Fluke branded DMMs and industrial instruments.

- Recent Developments: In September 2025, Tektronix launched the 7 Series DPO oscilloscope, its first new high-performance platform in nearly two decades, featuring 25 GHz bandwidth, industry-leading low noise, and targeting applications in high-speed communications, AI, and quantum computing.

- Strategic Focus: Tektronix's strategy emphasises field-portable and benchtop oscilloscope leadership, expansion into high-speed optical communications test, and leveraging the broader Fortive platform for calibration and service revenue.

Market Concentration Analysis

The global test and measurement equipment market is moderately concentrated. Top suppliers including Keysight Technologies, Rohde & Schwarz, Tektronix, National Instruments, and Anritsu, collectively hold approximately 50-55% of global revenue in 2025.

The competitive dynamics show two distinct structural patterns. At the high end, flagship vector network analyzers, semiconductor ATE, and mmWave test systems exhibit pronounced consolidation – the R&D intensity and multi-year customer certification cycles create barriers that only a handful of suppliers can sustain. This tier is essentially a three-to-five-company oligopoly with pricing power and high customer switching costs.

At the mid and entry tiers, the market is fragmenting, with players like Hioki and UNI-T gaining share through aggressive pricing, while niche specialists such as Pico Technology and Spectrum Instrumentation compete in modular and PC-based segments, alongside startups targeting emerging applications like quantum and battery testing.

Investment & Growth Opportunities

Fastest-Growing Segments

Asia Pacific regional growth represents the single largest geographic opportunity, driven by China's semiconductor capex and strong growth momentum in India. Calibration services and cloud-based calibration platforms represent the fastest-growing service category, benefiting from rising compliance demands in aerospace, pharma, and automotive sectors.

Emerging Market Expansion

AI-augmented test automation, 6G research instrumentation, quantum computing validation, and EV battery cycling platforms are the most attractive emerging technology sub-markets. Turkey's EMC chamber capacity expansion and the Gulf Cooperation Council's infrastructure modernisation programmes create incremental regional opportunities for calibration, rental pools, and modular instrumentation.

Venture & Private Investment Trends

Notable 2024-2025 transactions include Liquid Instrument’s new round of funding totaling $12 million in June 2024 and Teradyne's acquisition of Infineon's ATE operations in Regensburg in January 2025.

Future Market Outlook (2034)

The global test and measurement equipment market is projected to grow from USD 27.94 Billion in 2025 to USD 39.17 Billion by 2034, representing an absolute increase of USD 11.23 Billion over the forecast period at a CAGR of 3.71%. The market will cross USD 33.53 Billion by 2030, with the second half of the forecast period accelerating marginally due to 6G instrumentation purchases and mass EV test bench deployment.

Three technology discontinuities are most likely to reshape the market through 2034. First, the transition from 5G to 6G between 2028 and 2032 will drive a replacement super-cycle in vector network and spectrum analyzers. Second, AI-driven software-defined instruments will gradually displace fixed-function hardware in mid-tier applications, restructuring the industry margin profile. Third, quantum computing validation and compound semiconductor testing will emerge as distinct revenue categories.

By 2034, the industry will complete a partial transformation from a hardware-dominated market to a hybrid hardware-software-services economy, with recurring revenue from calibration, software subscriptions, and cloud-based test orchestration accounting for a larger share of total supplier revenue. Asia Pacific will continue to close the gap with North America, potentially rebalancing to near-parity by the end of the forecast period.

Research Methodology

Primary Research

Primary research comprised over 50 structured interviews in 2024-2025 with test and measurement stakeholders including product managers at Keysight, Tektronix, Rohde & Schwarz, Anritsu, and National Instruments; procurement leads at semiconductor fabs and EV OEMs; calibration lab directors; and institutional investors. Primary insights were used to validate market sizing assumptions, segment growth rates, and technology adoption timelines.

Secondary Research

Secondary sources included company annual reports (Keysight, Fortive, Emerson, Advantest), IEA Global EV Outlook, GSMA mobile connectivity reports, SIPRI defence expenditure data, SEMI semiconductor capex reports, and trade publications including Electronic Design, EDN, and Evaluation Engineering.

Forecasting Models

Market size estimations and growth projections were developed using a combination of top-down and bottom-up forecasting models, incorporating GDP and industrial production indices, semiconductor capex cycles, 5G/6G rollout timelines, and EV penetration trajectories. Scenario analysis (base, optimistic, conservative) accounted for macroeconomic uncertainty and geopolitical risk factors.

Test and Measurement Equipment Market Report Scope

|

Attribute |

Details |

|

Market Size (2025) |

USD 27.94 Billion |

|

Forecast (2034) |

USD 39.17 Billion |

|

CAGR |

3.71% (2026-2034) |

|

Historical Period |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segmentation – Product |

General Purpose Test Equipment (GPTE), Mechanical Test Equipment (MTE) |

|

Segmentation – Service |

Repair & After-Sales Services, Calibration Services |

|

Regions Covered |

North America, Asia Pacific, Europe, Latin America, Middle East & Africa |

|

Key Companies |

Keysight Technologies, Rohde & Schwarz, TEKTRONIX, INC., National Instruments CORP, Anritsu, Advantest Corporation, Fluke Corporation, Yokogawa Electric Corporation, Teledyne Technologies Incorporated, VIAVI Solutions Inc., etc. |

|

Report Format |

PDF, Excel |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the test and measurement equipment market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global test and measurement equipment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the test and measurement equipment industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Test and Measurement Equipment Market Report

The global test and measurement equipment market was valued at USD 27.94 Billion in 2025, driven by semiconductor capex, 5G rollouts, and EV battery and power electronics testing demand.

The market is projected to reach USD 39.17 Billion by 2034, growing at a CAGR of 3.71% during 2026-2034, driven by 6G research, AI-augmented test automation, and calibration services.

General Purpose Test Equipment (GPTE) leads with a 62.8% share in 2025, supported by broad demand for oscilloscopes, spectrum analyzers, multimeters, and signal generators across R&D and manufacturing.

Repair and After-Sales Services dominate with a 54.6% share in 2025, reflecting the long operational lives of high-value instruments and extensive OEM-authorised service networks worldwide.

North America leads with a 34.9% share in 2025, anchored by CHIPS Act-funded semiconductor investment, defence R&D budgets, and the presence of Keysight, Tektronix, Fluke, and NATIONAL INSTRUMENTS.

Key drivers include 5G and 6G rollouts, semiconductor capex exceeding USD 185 Billion in 2024, EV and ADAS validation, industrial automation, and aerospace/defence modernisation programmes.

Asia Pacific is the fastest-growing region at ~4.8% CAGR, while calibration services is the fastest-growing service sub-segment at ~4.5% CAGR through 2034, fuelled by compliance demand.

Leading companies include Keysight Technologies, Rohde & Schwarz, TEKTRONIX, INC., NATIONAL INSTRUMENTS CORP, Anritsu, Advantest Corporation, Fluke Corporation, Yokogawa Electric Corporation, Teledyne Technologies Incorporated, and VIAVI Solutions Inc.

Approximately 75% of organisations are projected to adopt AI-augmented test automation by 2026, enabling predictive maintenance, anomaly detection on ATE, and natural-language generative instrumentation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)