UK Energy Drinks Market Size, Share, Trends and Forecast by Product, Target Consumer, Distribution Channel, and Region, 2026-2034

UK Energy Drinks Market Summary:

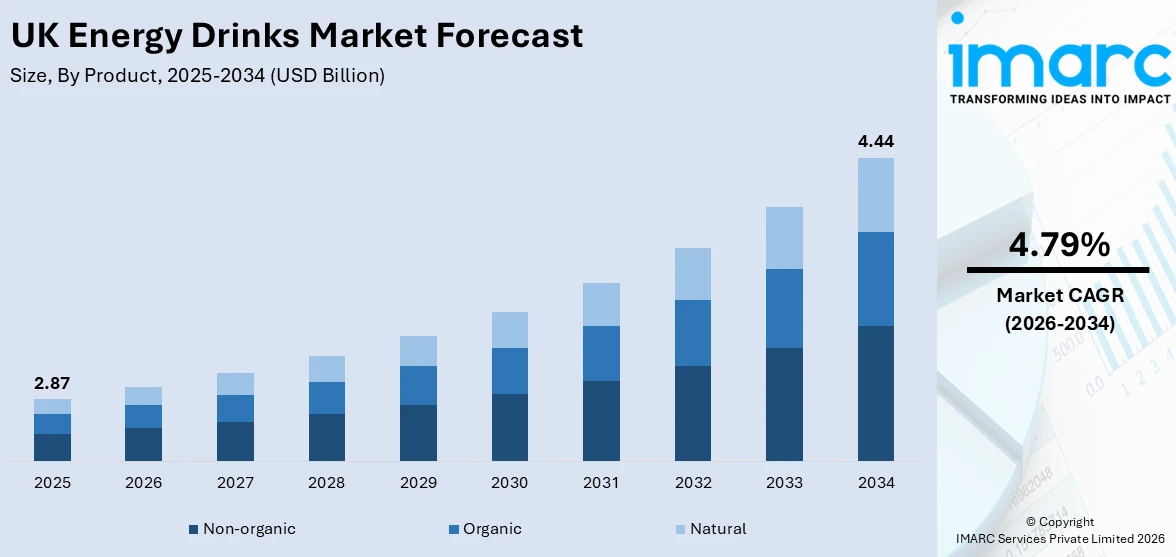

The UK energy drinks market size was valued at USD 2.87 Billion in 2025 and is projected to reach USD 4.44 Billion by 2034, growing at a compound annual growth rate of 4.79% during 2026-2034.

The UK energy drinks market is experiencing steady growth driven by rising health consciousness, increasing adoption of functional beverages among active adults, and continuous product innovation toward sugar-free and clean-label formulations. The proliferation of fitness-oriented lifestyles across urban centers, combined with expanding offline and online retail penetration, is attracting a progressively broader consumer base and reinforcing competitive positioning across UK.

Key Takeaways and Insights:

- By Product: Non-organic dominates the market with a share of 58.3% in 2025, driven by entrenched brand loyalty, competitive price positioning, and extensive availability across UK convenience stores, supermarkets, and online retail.

- By Target Consumer: Adults lead the market with a share of 52.4% in 2025, supported by rising demand from fitness enthusiasts and working professionals seeking performance-enhancing and functional beverage options throughout their daily routines.

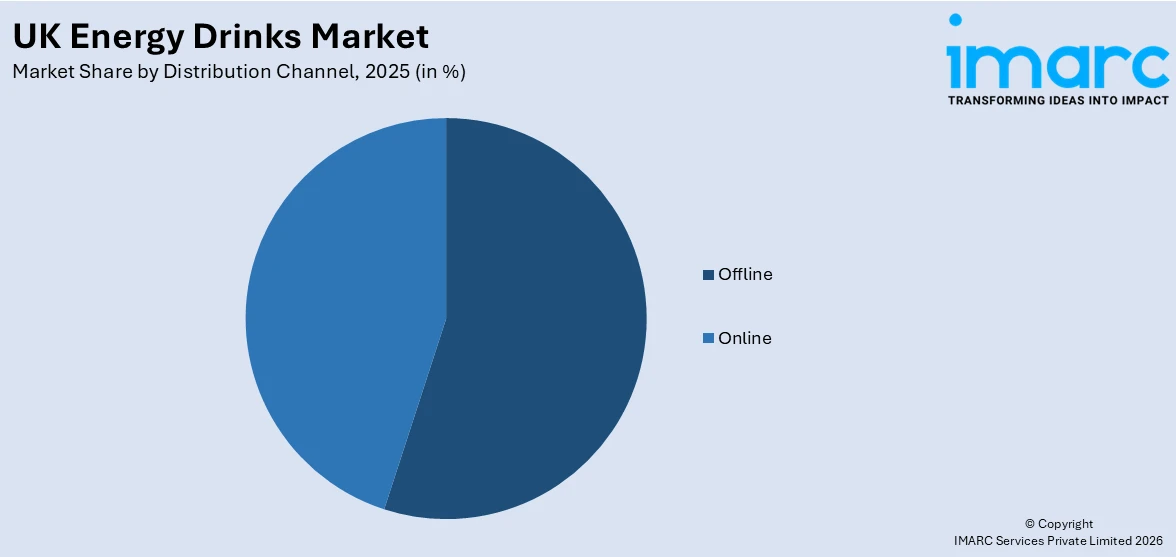

- By Distribution Channel: Offline represents the largest segment with a market share of 44.2% in 2025, reflecting the impulse-purchase nature of energy drinks and their prominent placement across supermarkets, convenience stores, and specialist retail outlets.

- By Region: London dominates the market with a share of 22.6% in 2025, underpinned by its dense population of young professionals, students, and fitness-conscious consumers within a well-developed retail environment.

- Key Players: The UK energy drinks market features intense competition between established global beverage corporations and emerging domestic brands, differentiated by health-focused formulations, sports sponsorships, premium positioning, and expanding digital distribution strategies.

To get more information on this market Request Sample

The UK energy drinks market is experiencing growth driven by changing consumer preferences toward flavored, functional, and healthier beverage options. Rising awareness regarding sugar consumption and overall wellness is encouraging demand for zero-sugar formulations and drinks made with natural ingredients, vitamins, and added functional benefits. Consumers are increasingly seeking convenient, ready-to-consume beverages that align with active and fast-paced lifestyles, particularly within convenience and on-the-go retail channels. Reflecting this trend, in 2026, UK-based Nichols launched Vimto Energy Tropical Cooler, a zero-sugar drink featuring natural caffeine, fruit juice, and added vitamins, targeting growing demand for flavorful and functional energy beverages. The increasing popularity of tropical flavors, combined with strong product visibility and impulse purchasing behavior, is further supporting category expansion. Continuous product innovation, expanding retail presence, and evolving consumer preferences are further contributing to the market growth.

UK Energy Drinks Market Trends:

Growing Demand for Functional and Health-Oriented Energy Drinks

The UK energy drinks market is increasingly driven by consumer preference for beverages that offer additional health and performance benefits beyond basic energy. Consumers are actively seeking products formulated with natural ingredients, vitamins, and functional compounds that support focus, endurance, and overall well-being. This shift is encouraging brands to move toward clean-label formulations and incorporate adaptogens and micronutrients into their offerings. For example, in 2026, UK-based Tenzing launched its Natural Energy+ range with a Lion’s Mane variant, expanding into functional energy drinks. The product combines mushroom extract, natural caffeine, magnesium, and vitamin D to support focus and sustained energy. This move reflects rising demand in the UK for benefit-led, clean-label energy drinks beyond traditional caffeine-based offerings.

Product Format Innovation to Enhance Accessibility and Trial

Innovation in product formats and packaging is playing an important role in expanding the consumer base for energy drinks in the UK. Smaller pack sizes and price-marked options are making products more accessible and affordable, encouraging trial among new users and occasional consumers. These formats also support impulse purchases, particularly within convenience retail environments. As evidentiary support, in 2025, Rockstar Energy (UK) introduced a new 330ml price-marked pack format to expand its consumer base. The smaller can, launched with a Blood Orange Zero Sugar variant alongside other flavors, targets non-traditional energy drink consumers. This strategy aimed to increase category penetration and drive trial by offering a more accessible size and price point.

Rising Influence of Celebrity Endorsements and Athlete-Led Branding

The UK energy drinks market is increasingly influenced by celebrity endorsements and athlete-led branding, which are shaping consumer preferences and strengthening product positioning. Brands are leveraging well-known personalities to enhance credibility, attract new audiences, and build stronger emotional connections with consumers. This approach is particularly effective among younger and fitness-oriented demographics who associate such endorsements with performance and lifestyle aspirations. In 2025, Más+ by Messi energy drink launched in the UK exclusively through Spar across England, Scotland, and Wales. The range included four flavors and focuses on hydration with electrolytes, vitamins, and low sugar, without caffeine. The exclusive rollout leveraged celebrity branding and functional positioning to attract health-conscious and sports-oriented consumers.

.webp)

Market Outlook 2026-2034:

The UK energy drinks market demonstrates strong revenue expansion potential throughout forecast period, underpinned by demographic shifts toward active lifestyles and sustained product innovation. The market generated a revenue of USD 2.87 Billion in 2025 and is projected to reach a revenue of USD 4.44 Billion by 2034, growing at a compound annual growth rate of 4.79% from 2026-2034. Progressive adoption of functional, sugar-reduced, and organically certified formulations is broadening the consumer base, while expanding offline and digital distribution networks ensure sustained market penetration across the UK.

UK Energy Drinks Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product |

Non-organic |

58.3% |

|

Target Consumer |

Adults |

52.4% |

|

Distribution Channel |

Offline |

44.2% |

|

Region |

London |

22.6% |

Product Insights:

- Non-organic

- Organic

- Natural

The non-organic dominates with a market share of 58.3% of the total UK energy drinks market in 2025.

Non-organic represents the largest segment because of its widespread availability, affordability, and strong consumer familiarity. This segment offers products by well established brands that have built strong recognition and loyalty over time. The competitive pricing makes it accessible to a broad consumer base, including students and working professionals. Additionally, non-organic variants are widely distributed across supermarkets, convenience stores, and vending machines, ensuring easy access. The presence of a wide range of flavors and formulations further supports their popularity, driving consistent demand across various consumer groups in the UK market.

The dominance of non-organic energy drink is also attributed to the strong marketing strategies, wide distribution networks, and consistent product availability. Leading brands invest heavily in promotions, digital campaigns, and retail visibility to maintain consumer engagement and brand recognition. These products also benefit from longer shelf life and cost-efficient large-scale production, enabling competitive pricing and reliable supply. Reflecting this trend, in 2025, Ghost Energy (UK) announced the launch of its Sour Pink Lemonade flavor, expanding its portfolio and leveraging digital-first distribution channels. Such strategies continue to reinforce the strong market position of non-organic energy drinks.

Target Consumer Insights:

- Teenagers

- Adults

- Geriatric Population

Adults lead with a market share of 52.4% of the total UK energy drinks market in 2025.

Adults lead the UK energy drinks market in terms of target consumer due to their high consumption frequency and strong demand for functional beverages that support energy, focus, and productivity. Working professionals often rely on energy drinks to manage long hours, demanding schedules, and physically or mentally intensive tasks. The need for convenient and quick energy solutions during work, travel, or daily routines further drives consumption. Additionally, adults have greater purchasing power, allowing them to explore a wide range of products, including premium and specialized variants. This consistent demand across different adult age groups supports their dominant share in the market.

The leadership of the adult consumer segment in the market is driven by the growing awareness about benefits like improved alertness, enhanced performance, and convenience. Adults increasingly incorporate energy drinks into daily routines across work, fitness, and social settings, driving consistent consumption. Product diversification, including low-sugar and functional variants, further caters to varied preferences within this group. Reflecting this trend, in 2025, Spar UK introduced a 4-pack format for its Blue Bear energy drink range, enhancing value and convenience for regular consumption. Strong retail availability and targeted marketing continue to reinforce adult-driven demand in the market.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Offline

- Supermarket/Hypermarket

- Mass Merchandiser

- Drug Store

- Food Service/Sports Nutrition Chain

- Others

- Online

Offline exhibits a clear dominance with a 44.2% share of the total UK energy drinks market in 2025.

Offline holds the biggest market share owing to its widespread presence and strong consumer reliance on physical retail outlets. Supermarkets, convenience stores, and petrol stations offer easy accessibility and immediate product availability, which is crucial for impulse purchases. Energy drinks are often bought on the go, making offline stores the preferred choice for quick consumption needs. Strategic product placement, promotional displays, and in store discounts further influence purchasing decisions. Additionally, established retail networks ensure consistent supply and brand visibility, supporting high sales volumes across urban and suburban regions throughout the UK market.

The dominance of offline distribution channels in also influenced by strong consumer preference for in-store purchases, particularly when exploring new flavors and product variants. Retail outlets offer a wide assortment of brands, pack sizes, and price options, enabling easy comparison and immediate availability. High footfall in supermarkets, gyms, and convenience stores further drives frequent purchases among working professionals and students. Reflecting this trend, in 2025, Ghost Energy launched in the UK through NutriStore and Pure Gym locations, strengthening its physical retail presence. Such strategies continue to reinforce the importance of offline channels in driving sales.

– Ghost Energy launched in the UK with a localized formula and initial distribution through NutriStore and Pure Gym locations. The brand, expected to expand rapidly into supermarkets and convenience stores, strengthened its presence in the UK energy drink segment.

Regional Insights:

- London

- South East

- North West

- East of England

- South West

- Scotland

- West Midlands

- Yorkshire and The Humber

- East Midlands

- Others

London dominates with a market share of 22.6% of the total UK energy drinks market in 2025.

London leads the market due to its high population density, fast paced lifestyle, and strong demand for convenient energy boosting beverages. The city hosts a large working population, including professionals and students who often rely on energy drinks to manage long working hours and busy schedules. Additionally, the presence of numerous retail outlets, supermarkets, and convenience stores ensures easy product availability. The growing café culture and on the go consumption habits further support demand. High brand visibility, frequent product launches, and aggressive marketing campaigns in urban areas continue to strengthen London’s leading position in the market.

The dominance of the segment is also supported by strong consumer demand for premium and innovative beverage options, driven by its diverse and youthful population. Consumers in the city show a higher willingness to try new flavors, functional formulations, and low-calorie variants, contributing to dynamic product adoption. Reflecting this trend, in 2026, UK-based Icona London announced the launch of Ekonic Energy Drink, targeting students and working professionals with a balanced, low-calorie formulation. The city’s dense network of retail outlets, gyms, and workplaces further supports consistent consumption, reinforcing London’s role as a key market hub.

Market Dynamics:

Growth Drivers:

Why is the UK Energy Drinks Market Growing?

Increasing Preference for Zero-Sugar and Low-Calorie Variants

Health-conscious consumption trends are significantly influencing the UK energy drinks market, with consumers increasingly prioritizing reduced sugar intake and calorie control. This shift is driving the demand for zero-sugar and low-calorie alternatives that still deliver strong flavor and energy benefits. Manufacturers are expanding product portfolios with innovative flavor combinations to enhance appeal while maintaining healthier formulations. Reflecting this, in 2025, Celsius expanded its energy drink range in the UK and Ireland with multiple zero-sugar fruit flavors, including Mango Lemonade and Strawberry Watermelon, targeting health-conscious consumers. This expansion aimed to drive category growth and increase retail value by offering flavorful, better-for-you energy drink options.

Rising Demand for High-Performance Energy Beverages

The UK market is witnessing increasing demand for high-performance energy drinks designed for consumers seeking stronger and more sustained energy output. These beverages are often formulated with higher caffeine content and functional ingredients to support endurance, alertness, and physical performance. This trend is particularly evident among fitness enthusiasts and individuals with active lifestyles. For instance, in 2024, UK-based Tenzing launched a new “Super Natural Energy” drink positioned as the strongest natural energy beverage. The Fiery Mango variant contained 200mg natural caffeine per serving, along with cordyceps mushrooms, vitamins, and electrolytes. The drink targeted high-performance consumers seeking plant-based, functional energy drinks with higher caffeine intensity.

Shift Toward Clean-Label and Natural Ingredient-Based Products

Consumers in the UK are increasingly prioritizing ingredient transparency and natural sourcing in their beverage choices, leading to a growing preference for clean-label energy drinks. Products made with plant-based caffeine, natural extracts, and minimal artificial additives are gaining traction among wellness-focused consumers. This trend is encouraging manufacturers to reformulate existing products and introduce new offerings aligned with health-conscious expectations. In 2024, Monster Energy launched REIGN Storm, a clean energy drink, across the UK targeting wellness-focused consumers. The product featured plant-based caffeine, zero sugar, and added vitamins and minerals, offering a healthier alternative to traditional energy drinks. Its nationwide rollout reflected the growing demand for functional, “better-for-you” beverages in the UK energy drink market.

Market Restraints:

What Challenges is the UK Energy Drinks Market Facing?

Escalating Regulatory Complexity and Compliance Costs

The UK energy drinks market is experiencing increasing regulatory pressure due to stricter taxation policies, advertising restrictions, and potential age-related sales limitations. These evolving regulations are raising compliance costs and limiting promotional activities, creating operational challenges for manufacturers. Smaller companies are particularly impacted, as they often lack the resources to manage complex regulatory requirements compared to larger, well established industry participants.

Competition from Alternative Functional Beverages

The UK market faces intensifying competition from alternative functional beverages, including cold brew coffee, adaptogenic teas, herbal tonics, and nootropic-infused drinks. These products target similar consumer occasions with perceived cleaner ingredient profiles and lower caffeine levels, attracting health-conscious consumers who might otherwise choose conventional energy drinks, potentially limiting category penetration among premium wellness-oriented demographics throughout the forecast period.

Consumer Health Concerns and Category Stigma

Persistent consumer concerns about the health effects of high caffeine intake, excessive sugar, and synthetic additives continue to sustain negative perceptions around regular energy drink consumption. These concerns create adoption barriers among potential new consumer segments, particularly parents and older adults, while fueling ongoing advocacy for stricter regulatory intervention that could further constrain the market's promotional and distribution capabilities.

Competitive Landscape:

The UK energy drinks market is characterized by a competitive landscape featuring established multinational beverage corporations alongside a growing cohort of domestic and independent challenger brands. Leading players leverage extensive distribution networks, marketing investments in sports sponsorships, and continuous product development cycles to maintain positioning. Emerging brands capture health-conscious and premium-oriented segments by emphasizing clean-label ingredients, organic certifications, and functional benefit differentiation. Competitive dynamics are increasingly shaped by regulatory compliance capabilities, sustainability credentials, and the ability to deploy effective omnichannel distribution balancing offline impulse purchasing with accelerating digital retail engagement.

Recent Developments:

- March 2026: Suntory (UK) announced the permanent return of Lucozade Energy Grafruitti, driven by strong consumer demand. The product will relaunch in zero-sugar variants across multiple pack sizes and retail channels starting April 2026. The move aims to boost energy drink category growth, supported by a major marketing campaign and rising demand for new flavors.

- January 2026: Monster Energy introduced its new “Viking Berry” flavor in the Juiced range to expand its offerings in the flavored energy drinks segment. The product blends energy drink ingredients with Nordic-inspired berry juices to cater to changing consumer tastes.

UK Energy Drinks Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Non-organic, Organic, Natural |

| Target Consumers Covered | Teenagers, Adults, Geriatric Population |

| Distribution Channels Covered |

|

| Regions Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the UK Energy Drinks Market Report

The UK energy drinks market size was valued at USD 2.87 Billion in 2025.

The UK energy drinks market is expected to grow at a compound annual growth rate of 4.79% during 2026-2034 to reach USD 4.44 Billion by 2034.

The non-organic segment accounted for the largest revenue share of 58.3% in 2025, driven by strong brand loyalty, extensive retail availability, and established consumer preference for familiar stimulant-based formulations at accessible price points.

Key factors driving the UK energy drinks market include packaging innovation that improves affordability and accessibility, encouraging trial among new consumers. In 2025, Rockstar Energy introduced a 330ml price-marked pack in the UK, targeting non-traditional consumers and supporting impulse purchases across convenience retail channels.

Major challenges include escalating regulatory complexity under the Soft Drinks Industry Levy and HFSS frameworks, intensifying competition from alternative functional beverages, and persistent consumer health concerns surrounding caffeine and sugar content in conventional energy drink formulations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)