United States Prefilled Syringes Market Size, Share, Trends and Forecast by Design, Material, Closing System, Application, End User, and Region, 2026-2034

United States Prefilled Syringes Market Size, Share, Trends & Forecast (2026-2034)

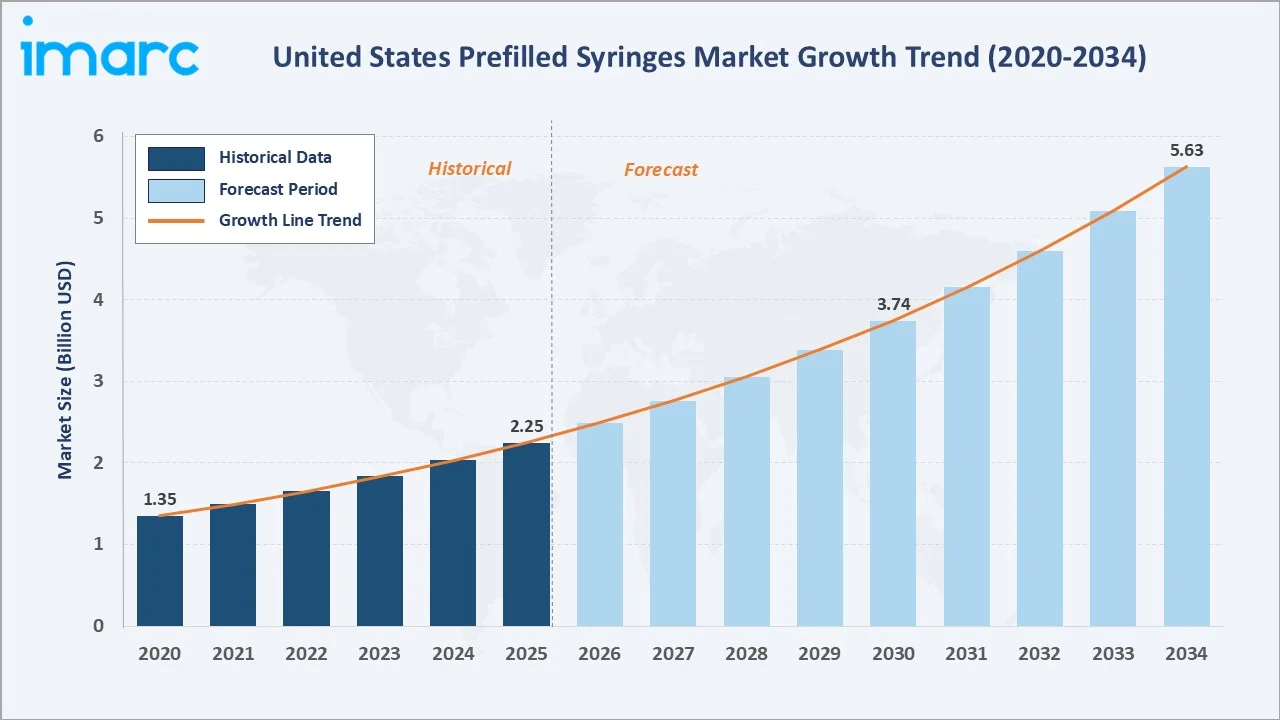

The United States prefilled syringes market was valued at USD 2.25 Billion in 2025 and is projected to reach USD 5.63 Billion by 2034, exhibiting a CAGR of 10.75% during 2026-2034. Growth is anchored by the rapid expansion of biologic drugs, rising prevalence of chronic diseases, and surging preference for self-injection therapies.

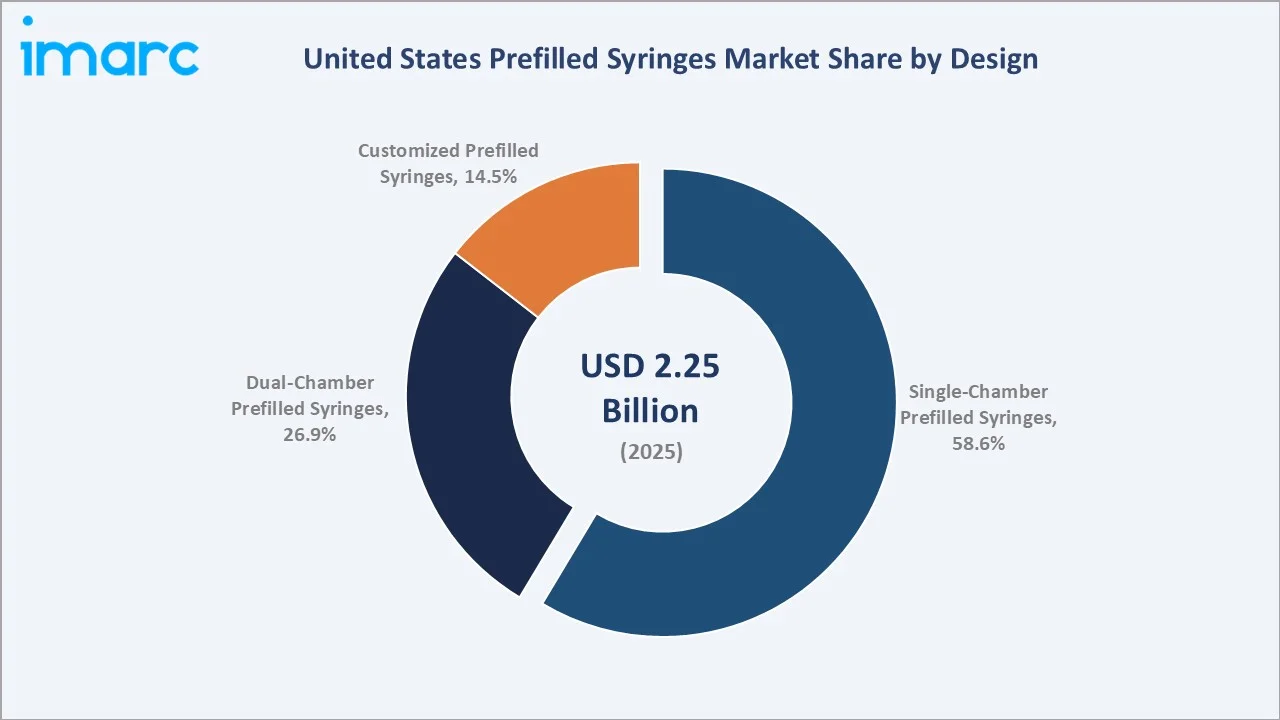

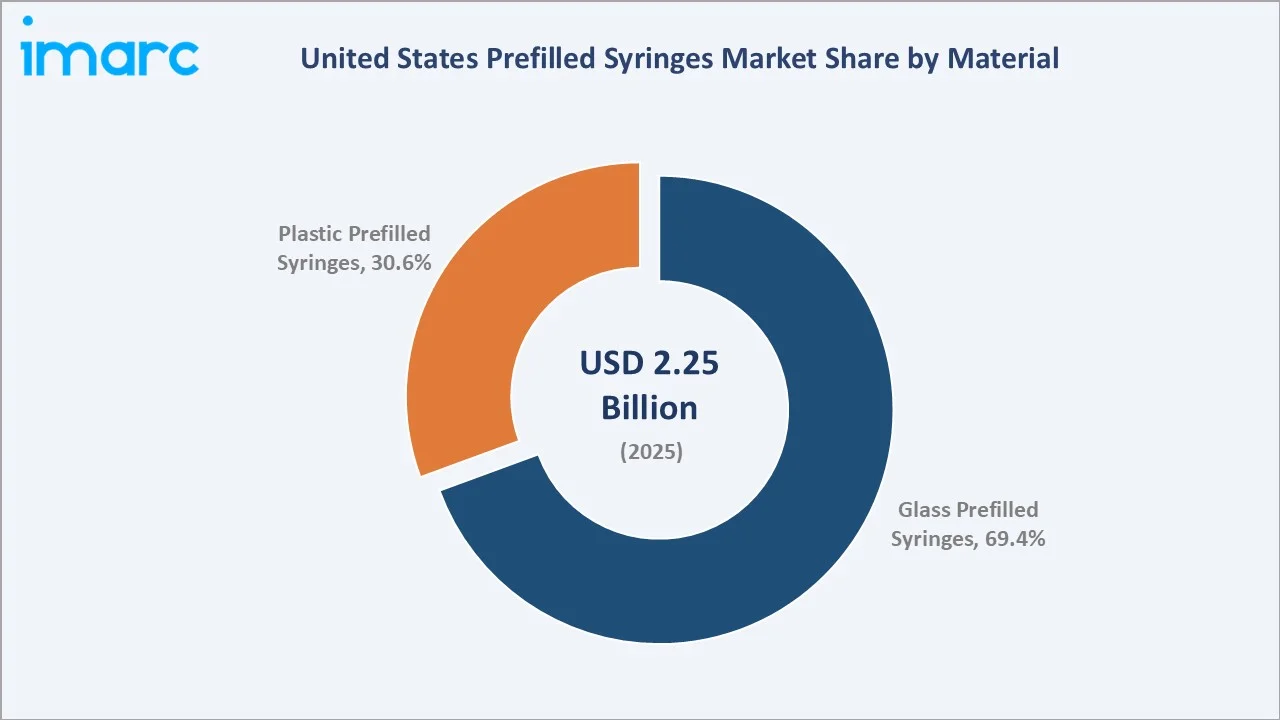

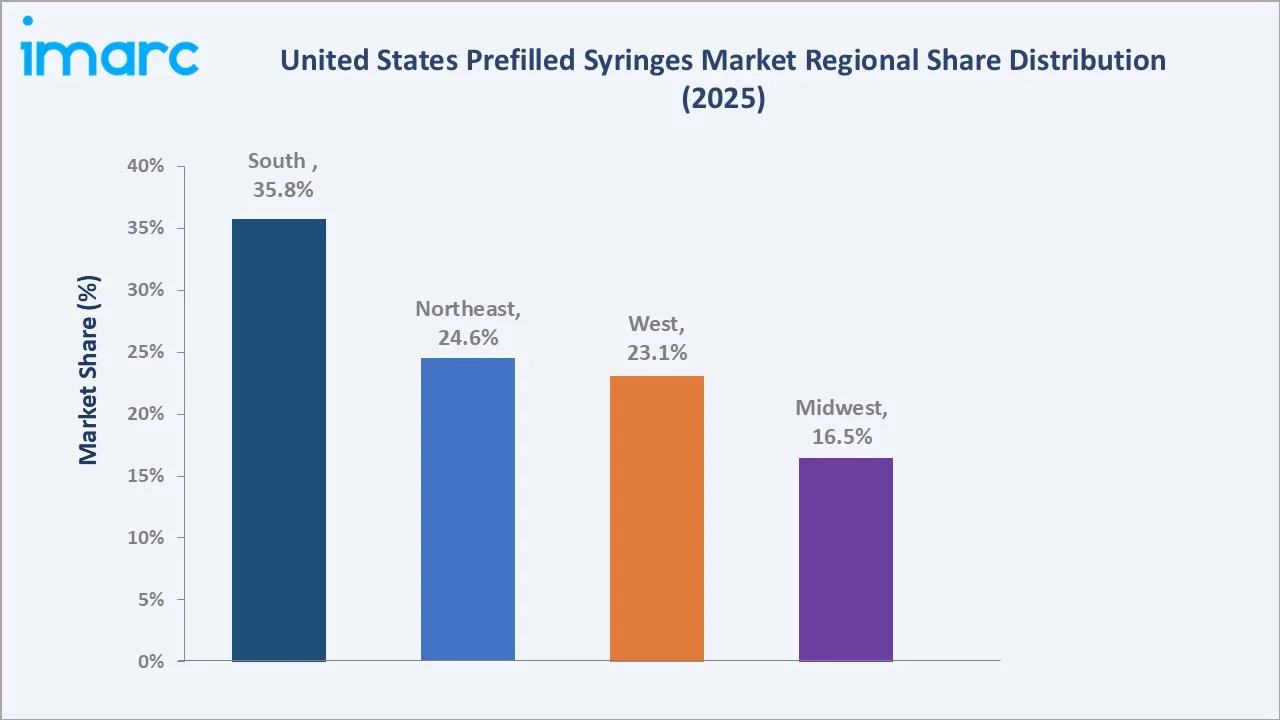

Single-chamber prefilled syringes lead the design segment at 58.6% in 2025, glass prefilled syringes dominate the material segment at 69.4%, and South holds 35.8% of the regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.25 Billion |

|

Forecast Market Size (2034) |

USD 5.63 Billion |

|

CAGR (2026-2034) |

10.75% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South (35.8%, 2025) |

|

Second Largest Region |

Northeast (24.6%, 2025) |

|

Leading Design |

Single-Chamber Prefilled Syringes (58.6%, 2025) |

|

Leading Material |

Glass Prefilled Syringes (69.4%, 2025) |

The United States prefilled syringes market expanded from USD 1.35 Billion in 2020 to USD 2.25 Billion in 2025, propelled by the growing preference for patient-centric drug delivery and increasing demand for ready-to-use injectable formats across healthcare settings. Anchored at USD 3.74 Billion in 2030, the forecast to USD 5.63 Billion by 2034 is supported by the expanding biologics pipeline, greater use of home-based care, and continued innovation in advanced injectable drug delivery systems.

To get more information on this market, Request Sample

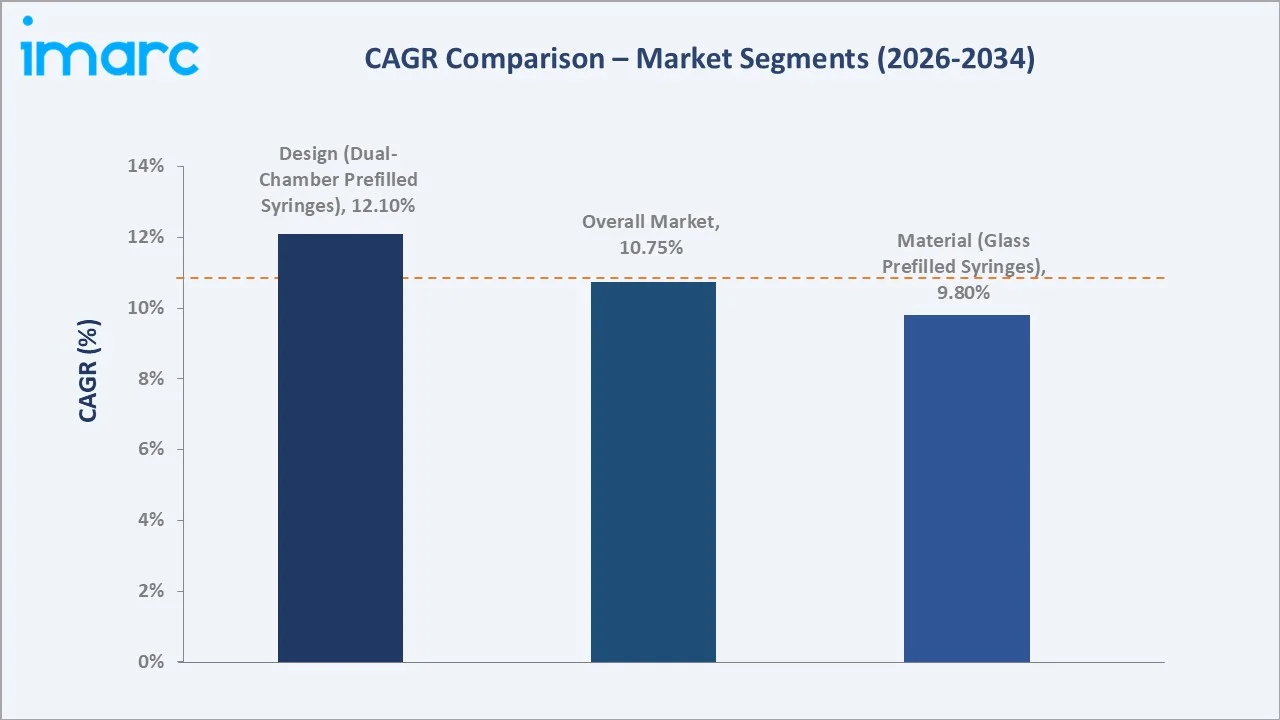

CAGR trajectories across design and material sub-segments show customized prefilled syringes and plastic prefilled syringes expanding faster than the 10.75% overall market CAGR, driven by evolving biologics formulations, temperature-sensitive drug pipelines, and growing pharmaceutical outsourcing activity across the country.

Executive Summary

The United States prefilled syringes market is on a sustained growth trajectory, expanding from USD 1.35 Billion in 2020 to USD 2.25 Billion in 2025 and projected to reach USD 5.63 Billion by 2034 at a CAGR of 10.75%. Rising adoption of biologics, biosimilars, and monoclonal antibodies, combined with increasing demand for self-injection therapies in chronic disease management, forms the primary growth engine of this market. As per IMARC Group, the United States biologics market size was valued at USD 204.4 Billion in 2025.

Single-chamber prefilled syringes lead the design segment at 58.6% in 2025, supported by their simplicity, high compatibility across therapeutic areas, and well-established manufacturing processes. Glass prefilled syringes retain their dominant position in the material segment at 69.4%, owing to their inert properties and compatibility with biologics and sensitive drug formulations. South commands the largest regional share at 35.8%, driven by its extensive hospital infrastructure, large population base, and favorable healthcare reimbursement environment.

Key Market Insights

|

Insight |

Data |

|

Leading Design |

Single-Chamber Prefilled Syringes – 58.6% share (2025) |

|

Second Largest Design |

Dual-Chamber Prefilled Syringes – 26.9% share (2025) |

|

Leading Material |

Glass Prefilled Syringes – 69.4% share (2025) |

|

Second Largest Material |

Plastic Prefilled Syringes – 30.6% share (2025) |

|

Leading Region |

South – 35.8% share (2025) |

|

Second Largest Region |

Northeast – 24.6% share (2025) |

|

Top Companies |

BD, Gerresheimer AG, West Pharmaceutical Services, Inc., Stevanato Group |

Key Analytical Observations Expanding On The Data Above:

- Single-chamber prefilled syringes dominance at 58.6% is driven by broad compatibility across vaccines, biologics, anticoagulants, and small-molecule drugs. Their simplicity in manufacturing and minimal preparation requirement makes them the default choice for pharmaceutical companies and healthcare providers across all major therapeutic categories in the United States.

- Dual-chamber prefilled syringes at 26.9% are gaining relevance as biologics with lyophilized components and reconstitution requirements expand across oncology, autoimmune, and rare disease therapies. The segment is expected to grow faster than single-chamber formats through the forecast period as drug complexity increases.

- Glass prefilled syringes leadership at 69.4% reflects the material's established regulatory track record, superior inertness, and compatibility with a wide spectrum of biologics and temperature-sensitive molecules.

- Plastic prefilled syringes at 30.6% are expanding steadily due to their lightweight design, improved break resistance, and suitability for self-administration and home healthcare settings. Advancements in high-performance polymer materials are also enhancing their compatibility with sensitive drug formulations.

- South at 35.8% leads the United States prefilled syringes market, supported by strong hospital density and expanding pharmaceutical manufacturing and contract development and manufacturing organization (CDMO) activity across, states, such as Texas, North Carolina, and Florida. In its commitment to address the swiftly increasing demands of North Texas, Texas Health Resources revealed intentions, in February 2026, to construct a new hospital and healthcare campus in north McKinney, anticipated to open in early 2029, representing a significant advancement in its ongoing investment to enhance and expand care throughout the area.

United States Prefilled Syringes Market Overview

Prefilled syringes are single- or dual-chamber drug delivery systems preloaded with a precise dose of medication, eliminating the need for manual drug preparation and reducing the risk of contamination, dosage error, and needlestick injury. In the United States, these devices are widely deployed across hospitals, outpatient infusion centers, pharmacies, and home healthcare settings for the delivery of biologics, vaccines, anticoagulants, erythropoietin products, hormones, and chronic disease therapies.

The market ecosystem integrates primary packaging manufacturers, drug fill-and-finish service providers, pharmaceutical and biotechnology companies, CDMOs, needle and plunger component suppliers, regulatory agencies, and end-use institutions, such as hospitals and home care service providers. Together, these stakeholders enable the design, production, filling, labeling, and distribution of prefilled syringe systems across therapeutic areas.

Market Dynamics

To evaluate market opportunities, Request Sample

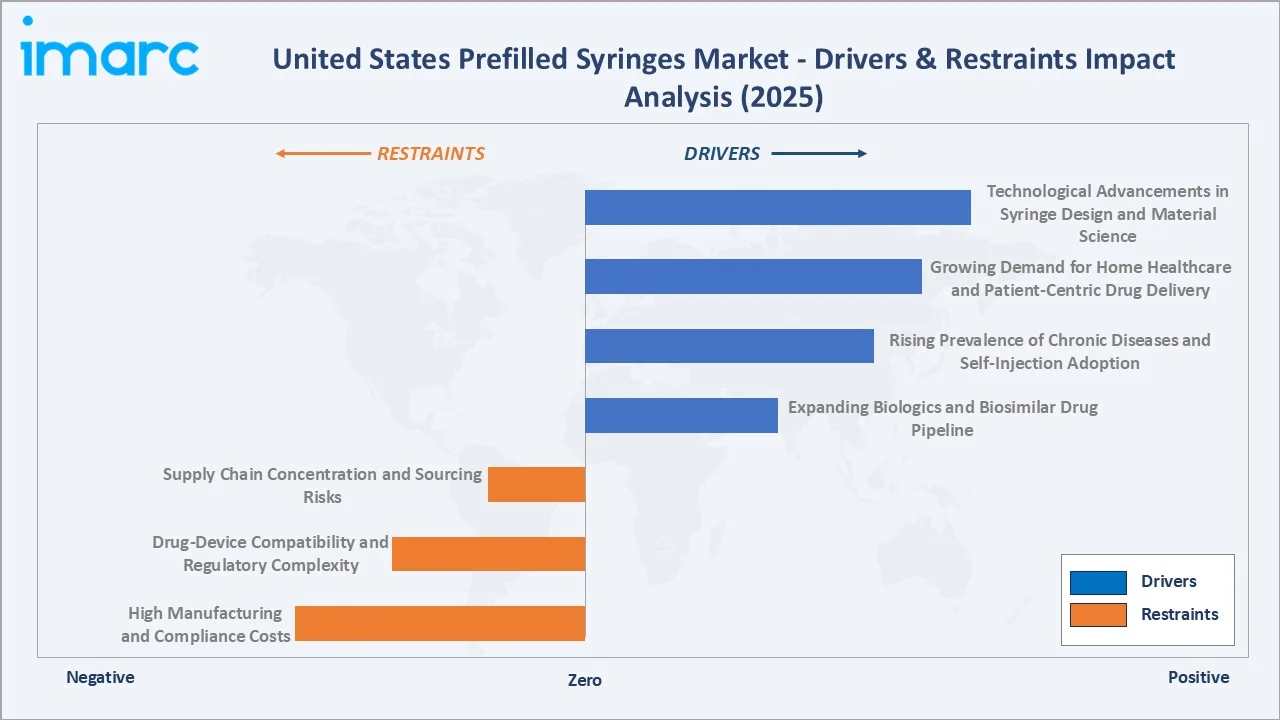

Market Drivers

- Expanding Biologics and Biosimilar Drug Pipeline: The rapid growth of the biologics sector in the United States is fundamentally reshaping demand for primary drug delivery packaging. As pharmaceutical and biotechnology companies advance a widening pipeline of monoclonal antibodies, therapeutic proteins, and fusion molecules, prefilled syringes have become the preferred delivery format.

- Rising Prevalence of Chronic Diseases and Self-Injection Adoption: The growing burden of chronic conditions across the United States is sustaining long-term demand for self-administered injectable therapies. As per NIHCM, 90% of the USD 4.5 Trillion allocated for healthcare in the US in 2022 was devoted to treating individuals with chronic physical and mental health issues. Diseases, such as rheumatoid arthritis, multiple sclerosis, type 2 diabetes, and psoriasis, require consistent, high-frequency dosing that patients increasingly manage at home.

- Growing Demand for Home Healthcare and Patient-Centric Drug Delivery: A sustained shift away from hospital-based treatment toward outpatient and home-based care is creating structural demand for drug delivery systems that patients and caregivers can use independently. Prefilled syringes support this transition by offering ready-to-administer formats that reduce preparation steps, minimize the risk of handling errors, and integrate readily with autoinjector and safety device platforms.

- Technological Advancements in Syringe Design and Material Science: Continuous innovation in glass and polymer syringe materials, needle safety mechanisms, and surface treatment technologies is expanding the range of drug formulations that can be effectively delivered through prefilled systems. Development of silicone-free and PFAS-free syringe platforms, tungsten-free glass manufacturing processes, and cyclic olefin polymer substrates is addressing longstanding compatibility and safety concerns associated with sensitive biologic formulations.

Market Restraints

- High Manufacturing and Compliance Costs: The production of prefilled syringes requires specialized cleanroom infrastructure, highly controlled aseptic filling environments, and multi-step quality validation processes that represent significant capital and operational investment. Meeting current regulatory standards for container-closure integrity, particulate control, and extractables and leachables testing demands both technical expertise and ongoing investment in equipment and systems.

- Drug-Device Compatibility and Regulatory Complexity: The interaction between a drug formulation and the materials that make up a prefilled syringe system, including the glass barrel, rubber stopper, silicone lubricant, and needle components, requires thorough characterization and validation before regulatory approval. Regulatory classification of prefilled syringes as combination products in the United States adds further layers of compliance obligation across design controls, human factors engineering, and post-market surveillance that manufacturers must navigate.

- Supply Chain Concentration and Sourcing Risks: The United States prefilled syringes market relies heavily on a concentrated global supplier base for critical inputs, including borosilicate glass tubing, precision rubber closures, and polymer resin materials, with much of this supply originating from European manufacturers. This geographic concentration introduces vulnerability to disruptions from logistics constraints, geopolitical developments, trade policy changes, and capacity limitations at key upstream producers.

Market Opportunities

- Biosimilar Pipeline Expansion and Fill-and-Finish Demand: The continuing maturation of the United States biosimilar industry is generating sustained incremental demand for prefilled syringe fill-and-finish capacity. As reference biologic patents expire and new biosimilar entrants seek to differentiate their products through improved delivery formats, the demand for glass and polymer prefillable systems and associated contract manufacturing services is growing.

- GLP-1 and Obesity Therapy Drug Delivery Expansion: The commercial success of glucagon-like peptide-1 receptor agonist therapies for diabetes management and obesity treatment is creating substantial new demand for self-injection device platforms. As pharmaceutical companies develop and commercialize multiple GLP-1 products targeting large patient populations requiring regular self-administered doses, the demand for prefilled syringe and autoinjector-compatible systems is expanding rapidly.

Market Challenges

- Competition from Emerging Drug Delivery Platforms: The growing range of alternative self-injection formats, including autoinjectors, pen injectors, wearable patch pumps, and large-volume subcutaneous delivery devices, is intensifying competition for share across the injectable drug delivery market. Pharmaceutical companies evaluating delivery format strategies for new biologic products must weigh patient experience, adherence support, payer positioning, and regulatory pathway considerations across multiple device options.

- Regulatory Evolution and Combination Product Compliance Burden: The regulatory framework governing prefilled syringes as combination products in the United States continues to evolve, with increasing expectations around human factors engineering, design controls, post-market surveillance, and extractables and leachables characterization.

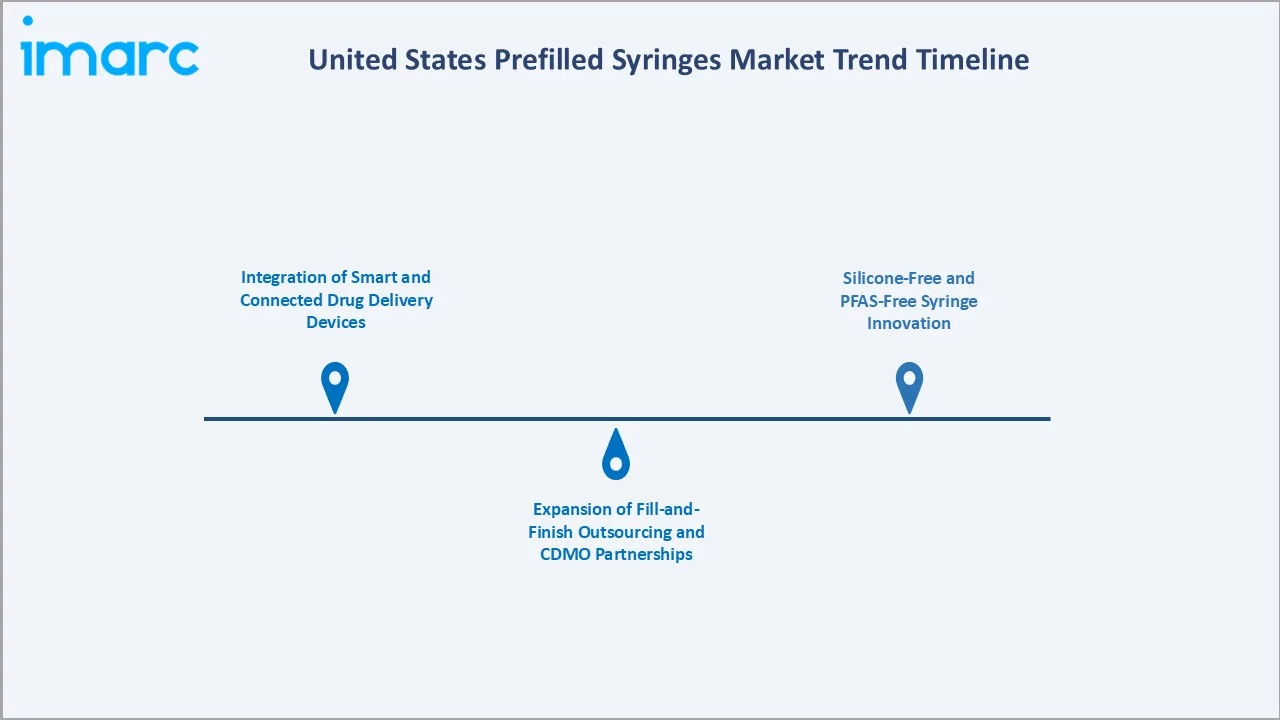

Emerging Market Trends

1. Integration of Smart and Connected Drug Delivery Devices

Pharmaceutical and device manufacturers are increasingly embedding sensing, connectivity, and data-capture capabilities into prefilled syringe systems to support adherence monitoring, dose tracking, and remote patient management. Integration with digital health platforms and connected care ecosystems is enhancing the value proposition of smart prefilled syringe technologies.

2. Expansion of Fill-and-Finish Outsourcing and CDMO Partnerships

Pharmaceutical and biotechnology companies are increasingly outsourcing prefilled syringe fill-and-finish operations to specialized CDMOs to reduce capital expenditure, accelerate time to market, and access dedicated biological manufacturing expertise. This trend is reinforcing capacity expansions by leading contract manufacturers and driving consolidation across the United States fill-and-finish services sector.

3. Silicone-Free and PFAS-Free Syringe Innovation

Growing regulatory and pharmaceutical industry concern over silicone oil-related protein aggregation and PFAS-containing coatings is driving demand for alternative lubrication technologies and syringe surface treatments. Next-generation silicone-free barrel coatings and plasma-treated glass surfaces are entering commercial readiness, positioning manufacturers that invest in these technologies to capture premium positioning in the United States biologics packaging segment.

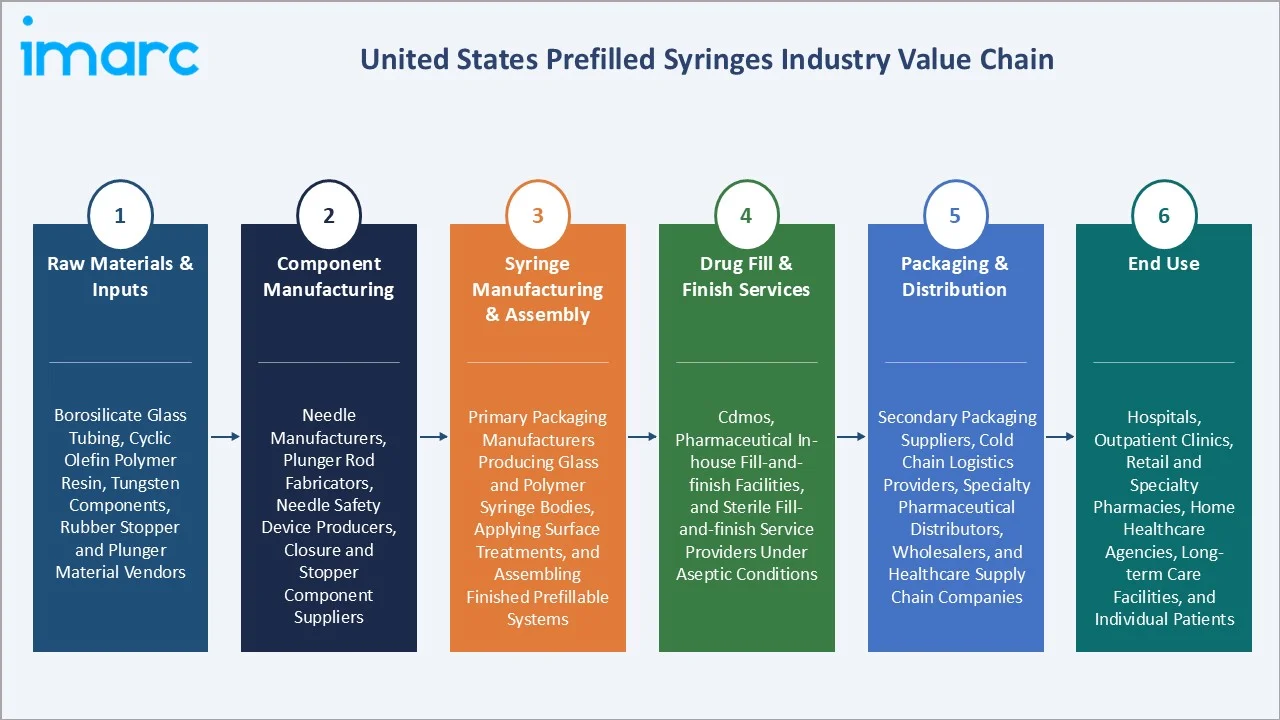

Industry Value Chain Analysis

The United States prefilled syringes value chain spans six stages from raw material supply through end-use patient administration. Primary packaging production, drug fill-and-finish services, and drug-device integration capture the highest value-add, while regulatory compliance and quality system capabilities increasingly determine competitive positioning across the supply chain.

|

Stage |

Key Players / Examples |

|

Raw Materials & Inputs |

Borosilicate glass tubing producers, cyclic olefin polymer resin suppliers, tungsten component manufacturers, and rubber stopper and plunger material vendors supplying primary packaging inputs |

|

Component Manufacturing |

Needle manufacturers, plunger rod fabricators, needle safety device producers, and closure and stopper component suppliers enabling syringe assembly |

|

Syringe Manufacturing & Assembly |

Primary packaging manufacturers producing glass and polymer syringe bodies, applying surface treatments, and assembling needle and closure components into finished prefillable systems |

|

Drug Fill & Finish Services |

CDMOs, pharmaceutical company in-house fill-and-finish facilities, and sterile fill-and-finish service providers filling syringes with drug product under aseptic conditions |

|

Packaging & Distribution |

Secondary packaging suppliers, cold chain logistics providers, specialty pharmaceutical distributors, wholesalers, and healthcare supply chain companies delivering finished prefilled syringes to end-use points |

|

End Use |

Hospitals, outpatient clinics, retail and specialty pharmacies, home healthcare agencies, long-term care facilities, and individual patients self-administering injectable therapies |

Vertically integrated players, especially those owning proprietary technology stacks, original fill-and-finish capability, and direct customer relationships, are positioned to capture greater value than partners reliant on third-party infrastructure.

Technology Landscape in the United States Prefilled Syringes Industry

Advanced Glass and Polymer Material Science

Material innovations in borosilicate glass, including ion exchange strengthening, surface delamination reduction treatments, and tungsten-free needle embedding, are enhancing the performance of glass prefilled syringes for high-value biologics. Cyclic olefin copolymer and cyclic olefin polymer substrates are emerging as the material of choice for biologics requiring extreme break-resistance, superior oxygen and moisture barrier properties, and compatibility with lyophilization and cold-chain storage requirements.

Automated Aseptic Fill-and-Finish Technologies

Robotic isolator-based aseptic filling systems, advanced particle inspection platforms, and in-line container-closure integrity testing technologies are raising manufacturing quality and throughput standards across the United States fill-and-finish sector. Barrier isolator technology and restricted access barrier system configurations are replacing conventional cleanroom filling processes, improving contamination control and regulatory compliance for sterile prefilled syringe production.

Drug-Device Combination Product Integration

The integration of prefilled syringes with autoinjector platforms, electronic dose capture systems, and wearable large-volume injectors is creating a new category of smart injectable combination products. Platform compatibility assessments, human factors engineering studies, and extractables and leachables validation frameworks specific to combination product submissions are becoming standard requirements for pharmaceutical developers targeting the United States self-injection market.

Sustainability and Circular Design Innovation

Environmental sustainability is emerging as a product design consideration for prefilled syringe manufacturers, driven by pharmaceutical company sustainability commitments and growing regulatory interest in pharmaceutical packaging lifecycle impacts. Recyclable polymer formulations, reduced-silicone designs, and bio-based plastic components are under active development, with commercial introductions expected to gain traction in the United States market through the forecast period.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Design |

Single-Chamber Prefilled Syringes |

58.6% |

2025 |

|

Material |

Glass Prefilled Syringes |

69.4% |

2025 |

|

Closing System |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

South |

35.8% |

2025 |

By Design

Single-chamber prefilled syringes command a 58.6% majority share in 2025, driven by their broad applicability across vaccines, anticoagulants, biologics, and hormonal therapies. Their simplicity in manufacturing, drug compatibility across a wide range of formulations, and established regulatory acceptance make them the foundational product format for pharmaceutical companies targeting the United States injectable drug industry.

To access detailed market analysis, Request Sample

Dual-chamber prefilled syringes hold 26.9% share in 2025, serving therapeutic areas where drug components must be stored separately and mixed immediately before administration. Their relevance is growing across lyophilized biologic formulations, reconstituted protein therapies, and two-component pharmaceutical products, particularly in oncology, autoimmune disorders, and rare disease treatments.

By Material

Glass prefilled syringes hold a 69.4% dominant share in 2025, supported by borosilicate glass's established regulatory acceptance, superior chemical inertness, and compatibility across the full breadth of biologic and small-molecule drug formulations.

Plastic prefilled syringes represent a 30.6% share in 2025 and are growing at a faster pace than the glass prefilled syringes segment, driven by cyclic olefin polymer formats that offer break-resistance, low-extractable profiles, and suitability for lyophilization.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

35.8% |

Large and growing population base, dense hospital and healthcare system infrastructure, strong pharmaceutical and biotechnology manufacturing presence, favorable reimbursement environment, and expanding home healthcare services |

|

Northeast |

24.6% |

Concentration of leading academic medical centers, major pharmaceutical and biotech companies, high biologics prescription rates, mature healthcare infrastructure, and strong self-injection therapy adoption |

|

West |

23.1% |

Expanding biotechnology and biopharmaceutical industry presence, growing biologics fill-and-finish capacity, rising chronic disease prevalence, and increasing home healthcare adoption across urban and suburban markets |

|

Midwest |

16.5% |

Growing pharmaceutical manufacturing activity, established healthcare provider networks, rising demand for self-administered injectable therapies, and increasing adoption of prefilled syringe formats across hospital and outpatient settings |

South commands 35.8% of the market in 2025, underpinned by the largest regional population base, a growing concentration of pharmaceutical manufacturing and contract manufacturing facilities in states, such as North Carolina, Texas, and Georgia, and an expanding home healthcare sector.

Northeast at 24.6% is defined by a high concentration of leading academic medical centers, research hospitals, and major pharmaceutical companies in the country. High biologics prescription rates, rapid biosimilar adoption, and strong insurance reimbursement for injectable specialty therapies reinforce the region's sustained position as the second-largest market within the United States prefilled syringes landscape.

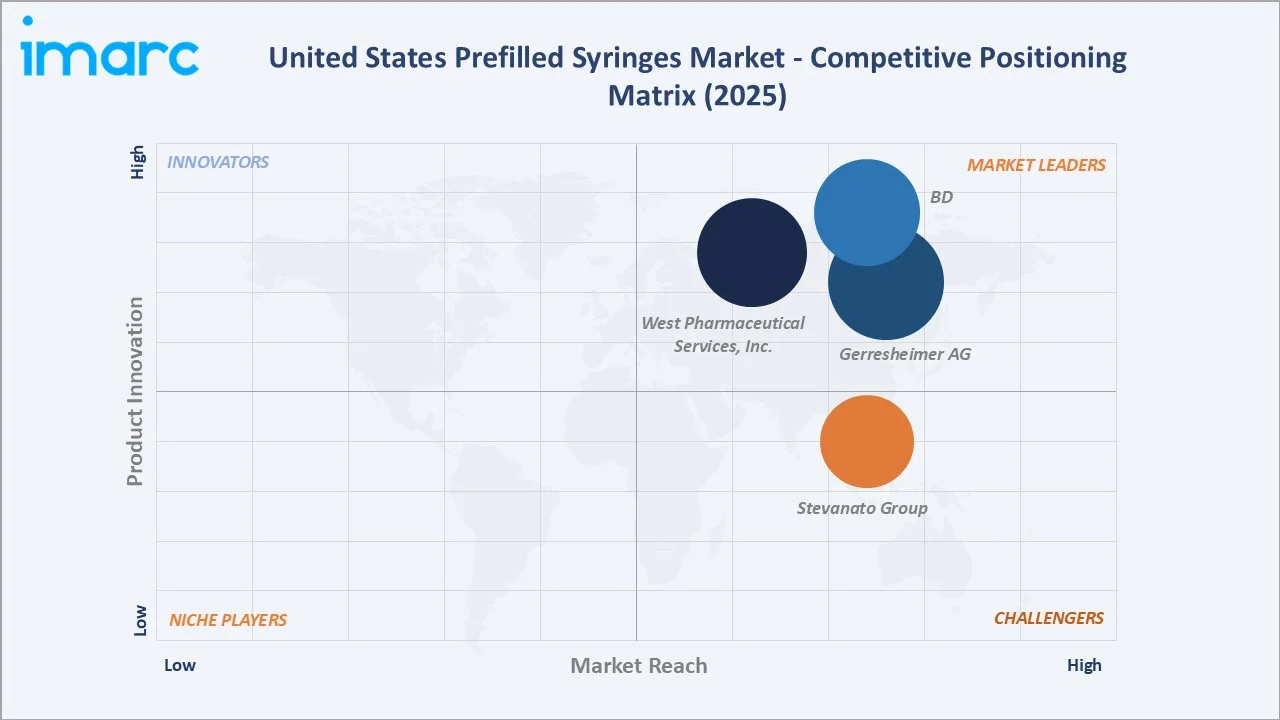

Competitive Landscape

The United States prefilled syringes market is moderately concentrated, with global primary packaging leaders dominating design and material innovation while specialized fill-and-finish contract manufacturers compete on service breadth, drug-device integration capabilities, and regulatory expertise. Market leadership is determined by product portfolio depth, manufacturing capacity, quality systems maturity, and ability to serve an evolving biologics and combination product customer base.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

BD |

BD Neopak™ |

Leader |

Primary packaging leadership, domestic capacity expansion, and drug-device integration for biologics and self-injection platforms |

|

Gerresheimer AG |

Gx Elite RTF® Syringes |

Leader |

Advanced glass and polymer syringe systems with silicone-free and PFAS-free innovation for high-value biologics markets |

|

West Pharmaceutical Services, Inc. |

West Synchrony™ S1 |

Leader |

Primary containment components and biologics self-injection device platforms |

|

Stevanato Group |

Nexa® EZ-fill® |

Challenger |

Ready-to-fill glass syringe systems and integrated drug containment and delivery solutions for pharmaceutical outsourcing |

Key players include BD, Gerresheimer AG, West Pharmaceutical Services, Inc., and Stevanato Group, among others.

Key Company Profiles

BD

BD is a leading global medical technology company and one of the world's largest manufacturers of prefillable syringe systems. The company serves pharmaceutical and biotechnology customers across vaccines, biologics, and specialty injectable drug delivery through a broad portfolio of glass and polymer prefillable syringe platforms.

- Product Portfolio: BD Neopak™ Glass Prefillable Syringe platform and BD Neopak™ XtraFlow™ for high-viscosity biologics, available in multiple formats to support a wide range of formulation and drug delivery requirements for pharmaceutical and biotechnology customers.

- Recent Developments: In January 2026, BD announced a USD 110 Million investment to establish BD Neopak™ Glass Prefillable Syringe production at its Columbus, Nebraska facility, creating approximately 120 new jobs, with supply expected to begin mid-2026.

- Strategic Focus: Primary packaging leadership in the United States, expansion of domestic prefillable syringe manufacturing capacity, and drug-device integration for high-viscosity biologics and self-injection platforms.

Gerresheimer AG

Gerresheimer AG is a global pharmaceutical packaging and drug delivery solutions company headquartered in Düsseldorf, Germany. The company offers a comprehensive portfolio of glass and polymer prefillable syringe systems, primary packaging solutions, and drug delivery devices to pharmaceutical and biotechnology customers worldwide.

- Product Portfolio: Gx Elite RTF® Glass Syringes, cyclic olefin copolymer polymer syringes, specialty prefillable syringe systems for biologics and combination product applications, and a range of primary packaging solutions for injectable drugs.

- Recent Developments: Gerresheimer AG has been advancing its prefillable syringe manufacturing capacity and product innovation, including the development of silicone-free and PFAS-free syringe platforms to address growing pharmaceutical industry demand for next-generation biologic drug packaging solutions.

- Strategic Focus: Innovation in advanced glass and polymer syringe materials, silicone-free and PFAS-free syringe technologies, and strengthening partnerships with biopharmaceutical customers targeting the United States and global markets.

West Pharmaceutical Services, Inc.

West Pharmaceutical Services, Inc. is a global leader in drug packaging and delivery systems. The company designs and manufactures primary containment components, prefillable syringe systems, and self-injection platforms for the pharmaceutical and biotechnology industries.

- Product Portfolio: West Synchrony™ S1 Prefillable Syringe System, NovaPure® high-performance syringe plungers with FluroTec™ barrier film, and a range of primary containment solutions for injectable drug delivery applications.

- Recent Developments: The company has continued to expand its portfolio of advanced containment and drug delivery solutions, with a focus on supporting the growing demand for biologics and high-value injectable therapies. It is also strengthening its manufacturing capabilities and technology platforms to improve product quality, supply chain resilience, and customer support.

- Strategic Focus: Integrated prefillable syringe system development, biologics primary containment leadership, self-injection device platform innovation, and supporting pharmaceutical customers through the development and commercialization of complex combination products.

Market Concentration Analysis

The United States prefilled syringes market is moderately concentrated at the primary packaging and fill-and-finish layers. Key players, including BD, Gerresheimer AG, West Pharmaceutical Services, Inc., and Stevanato Group, collectively account for a substantial share of prefilled syringe primary packaging supply to United States pharmaceutical and biotechnology customers.

Barriers to entry in the United States prefilled syringes market are high, driven by the capital-intensive nature of aseptic manufacturing, the regulatory requirements for combination product and primary packaging validation, and the need for deep expertise in drug-device compatibility and container-closure integrity. These dynamics favor well-capitalized incumbents with established customer bases and global manufacturing networks.

Consolidation in the contract manufacturing segment is ongoing, with strategic acquisitions, capacity expansions, and pharmaceutical company vertical integration transactions reshaping the competitive landscape.

Investment & Growth Opportunities

Fastest-Growing Segments

Customized prefilled syringes are the fastest-growing design segment, driven by demand for bespoke drug-device integration, specialty biologics packaging, and combination product development. Plastic prefilled syringes are growing fastest within the material segment, fueled by cyclic olefin polymer adoption for biologics and autoinjector-compatible applications.

Emerging Markets

West presents the strongest incremental growth opportunities within the United States prefilled syringes market, driven by pharmaceutical manufacturing expansion, growing home healthcare adoption, and an increasing base of specialty pharmaceutical and biotechnology companies. Midwest is also emerging as a growth market, supported by contract manufacturing buildout and rising injectable therapy adoption across hospital and outpatient settings.

Venture & Investment Trends

Investment activity in the United States prefilled syringes sector is concentrated in domestic manufacturing capacity expansion, polymer syringe technology development, smart and connected device platforms, and CDMO fill-and-finish infrastructure. Pharmaceutical companies are also investing in self-injection device platforms to support home-based administration of GLP-1, biologic, and specialty drug therapies, driving demand for high-volume prefilled syringe production capacity.

Future Market Outlook (2026-2034)

The United States prefilled syringes market is projected to expand from USD 2.25 Billion in 2025 to USD 5.63 Billion by 2034 at a CAGR of 10.75%, adding approximately USD 3.38 Billion in incremental market value over the forecast period.

Four forces will shape the market through 2034: continued expansion of the biologics and biosimilar pipeline, GLP-1 and obesity drug delivery growth, accelerating adoption of self-injection and home healthcare formats, and ongoing domestic manufacturing investment driven by supply chain resilience priorities.

By 2034, the United States prefilled syringes market is expected to be characterized by a higher share of customized and combination product-integrated formats, broader adoption of polymer syringe materials, and a more concentrated primary packaging and fill-and-finish supply base.

Research Methodology

Primary Research

Primary research included structured engagement with pharmaceutical packaging executives, contract manufacturing leaders, injectable drug delivery specialists, hospital procurement managers, and regulatory affairs professionals across the United States. These interactions validated market sizing, regional demand patterns, design and material segment evolution, and competitive positioning across the prefilled syringe supply chain.

Secondary Research

Secondary sources encompassed FDA drug approval databases, combination product guidance documents, Centers for Disease Control and Prevention chronic disease prevalence data, pharmaceutical industry association reports, annual reports and investor presentations from key market participants, academic research publications, and industry news sources covering the prefilled syringe and pharmaceutical packaging sectors.

Forecasting Models

Market forecasts used top-down and bottom-up methodologies combining pharmaceutical market sizing, biologics approval pipeline analysis, segment share evolution modeling, regional healthcare expenditure data, and macroeconomic inputs including healthcare inflation, insurance coverage trends, and domestic manufacturing investment flows.

United States Prefilled Syringes Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Designs Covered | Single-Chamber Prefilled Syringes, Dual-Chamber Prefilled Syringes, Customized Prefilled Syringes |

| Materials Covered | Glass Prefilled Syringes, Plastic Prefilled Syringes |

| Closing Systems Covered | Staked Needle System, Luer Cone System, Luer Lock Form System |

| Applications Covered | Diabetes, Anaphylaxis, Rheumatoid Arthritis, Oncology, Others |

| End Users Covered | Hospitals, Clinics, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | BD, Gerresheimer AG, West Pharmaceutical Services, Inc., Stevanato Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States prefilled syringes market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the United States prefilled syringes market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States prefilled syringes industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Prefilled Syringes Market Report

The United States prefilled syringes market was valued at USD 2.25 Billion in 2025, driven by strong demand for biologics, self-injection therapies, and expanding home healthcare adoption across the country.

The market is projected to reach USD 5.63 Billion by 2034, growing at a CAGR of 10.75% from 2026-2034, supported by the expanding biologics pipeline, biosimilar adoption, and rising chronic disease prevalence.

Single-chamber prefilled syringes lead the design segment at 58.6% in 2025, driven by their broad applicability across therapeutic areas, manufacturing efficiency, and established compatibility with vaccines, biologics, and anticoagulants.

Glass prefilled syringes hold 69.4% of the material segment in 2025, reflecting the material's superior inertness, regulatory acceptance, and established compatibility with biologics and sensitive parenteral drug formulations.

South commands 35.8% of the United States prefilled syringes market in 2025, fueled by a large population base and expanding home healthcare services.

Leading players include BD, Gerresheimer AG, West Pharmaceutical Services, Inc., and Stevanato Group, among others.

CDMOs provide critical fill-and-finish services for prefilled syringes, enabling pharmaceutical and biotechnology companies to access aseptic manufacturing capacity without capital-intensive in-house investment, supporting faster time-to-market for injectable therapies.

Key trends include polymer syringe adoption for biologics, smart and connected device integration, and domestic manufacturing capacity expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)