Construction Equipment Market Size, Share, Trends and Forecast by Solution Type, Equipment Type, Type, Application, Industry, and Region, 2026-2034

Global Construction Equipment Market Size, Share, Trends & Forecast (2026-2034)

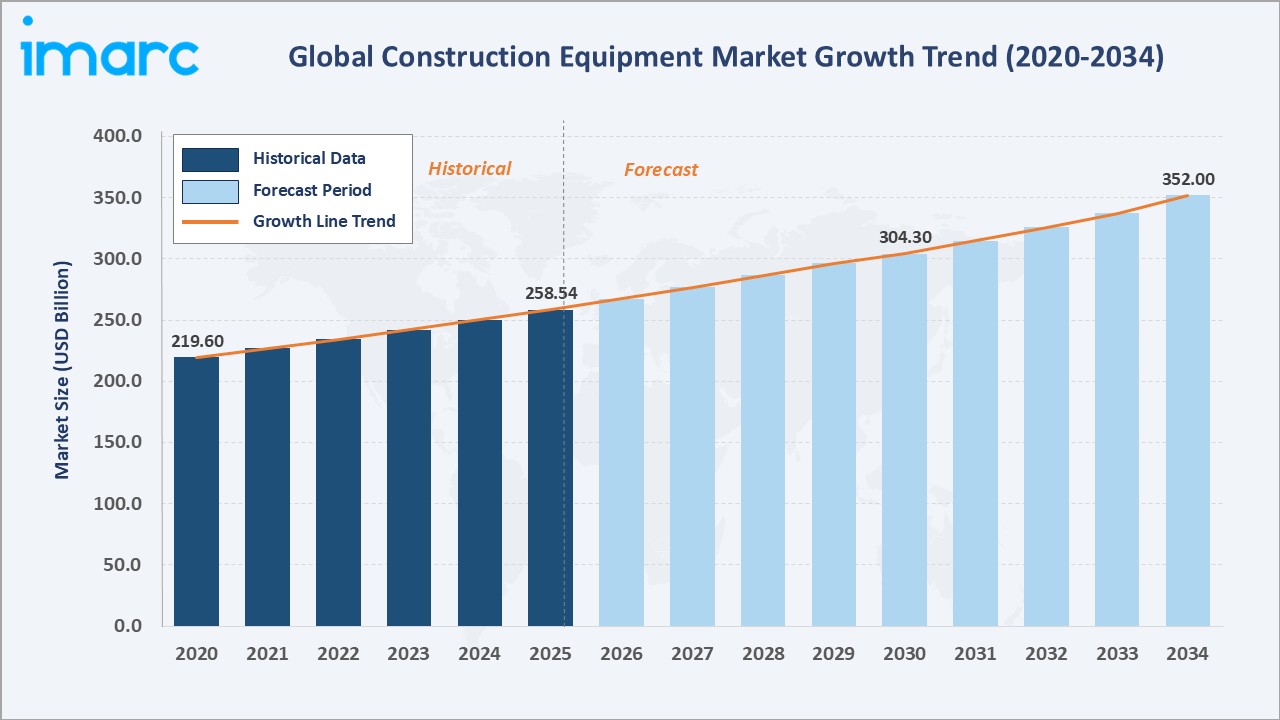

The global construction equipment market size reached USD 258.54 Billion in 2025 and is projected to reach USD 352.00 Billion by 2034, exhibiting a CAGR of 3.31% during 2026-2034.

Accelerating global infrastructure investment, robust expansion of industrial and commercial construction, and rapid urbanization across emerging economies are the primary forces driving construction equipment market growth.

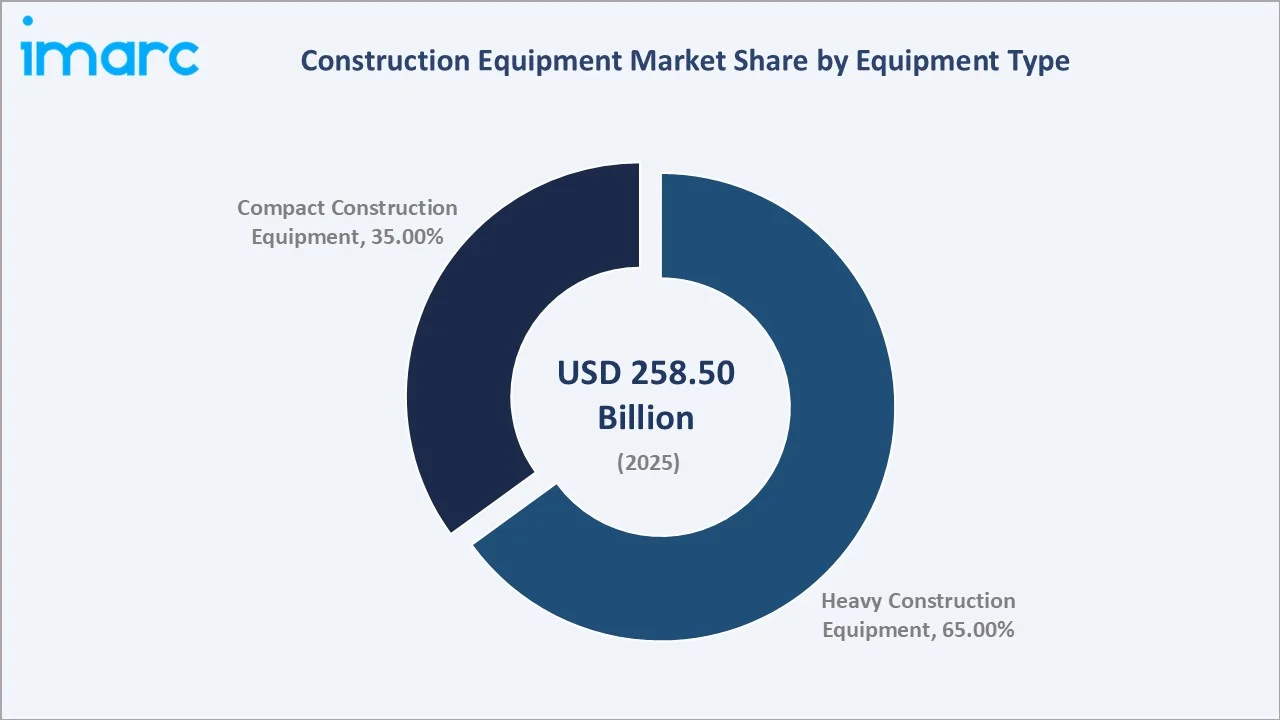

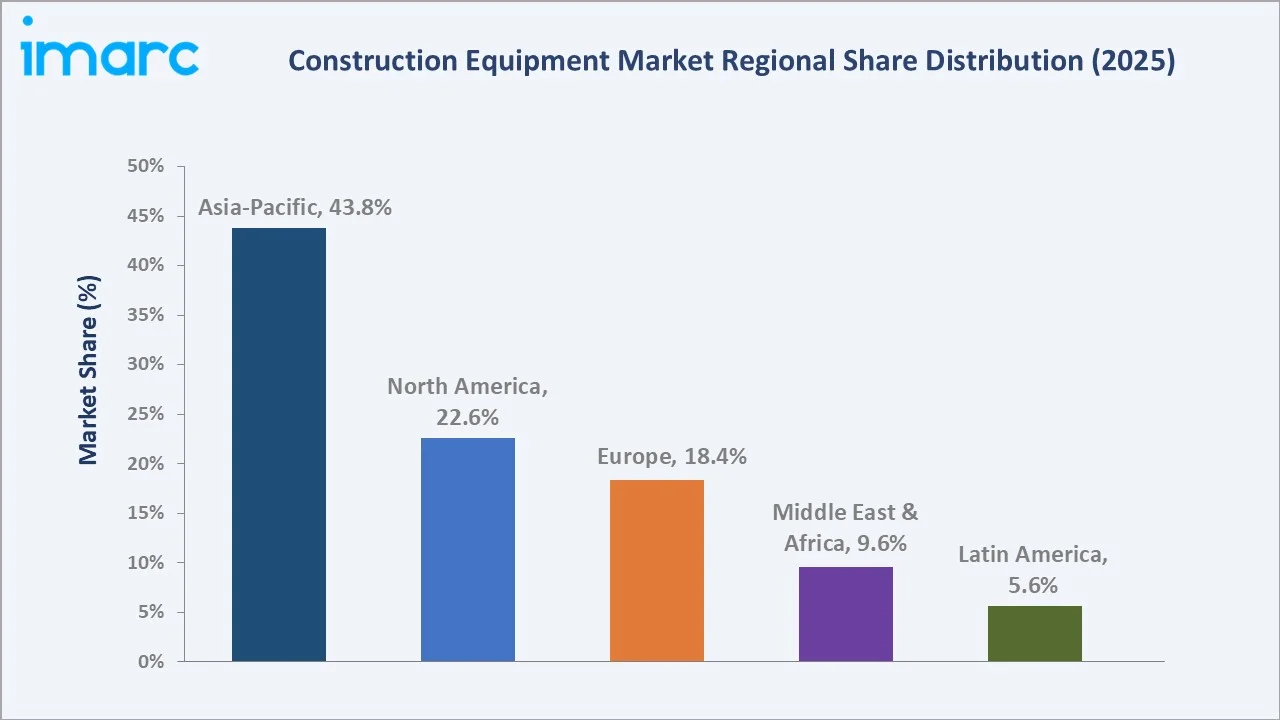

Heavy construction equipment dominates the equipment type mix at 65.0% in 2025, while earth moving leads the application segment at 51.0%. Asia-Pacific commands a dominant 43.8% regional share in 2025, reflecting China and India's unparalleled construction activity.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 258.54 Billion |

|

Forecast Market Size (2034) |

USD 352.00 Billion |

|

CAGR (2026-2034) |

3.31% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (43.8% share, 2025) |

|

Second Region |

North America (22.6% share, 2025) |

|

Leading Equipment Type |

Heavy Construction Equipment (65.0%, 2025) |

|

Leading Application |

Earth Moving (51.0%, 2025) |

The global construction equipment market growth trajectory from 2020 through 2034, with the historical expansion to USD 258.54 Billion in 2025, reflects consistent infrastructure-driven demand, while the forecast to USD 352.00 Billion in 2034 captures accelerating energy transition investment, industrial construction, and Asia-Pacific urbanization-led demand.

To get more information on this market, Request Sample

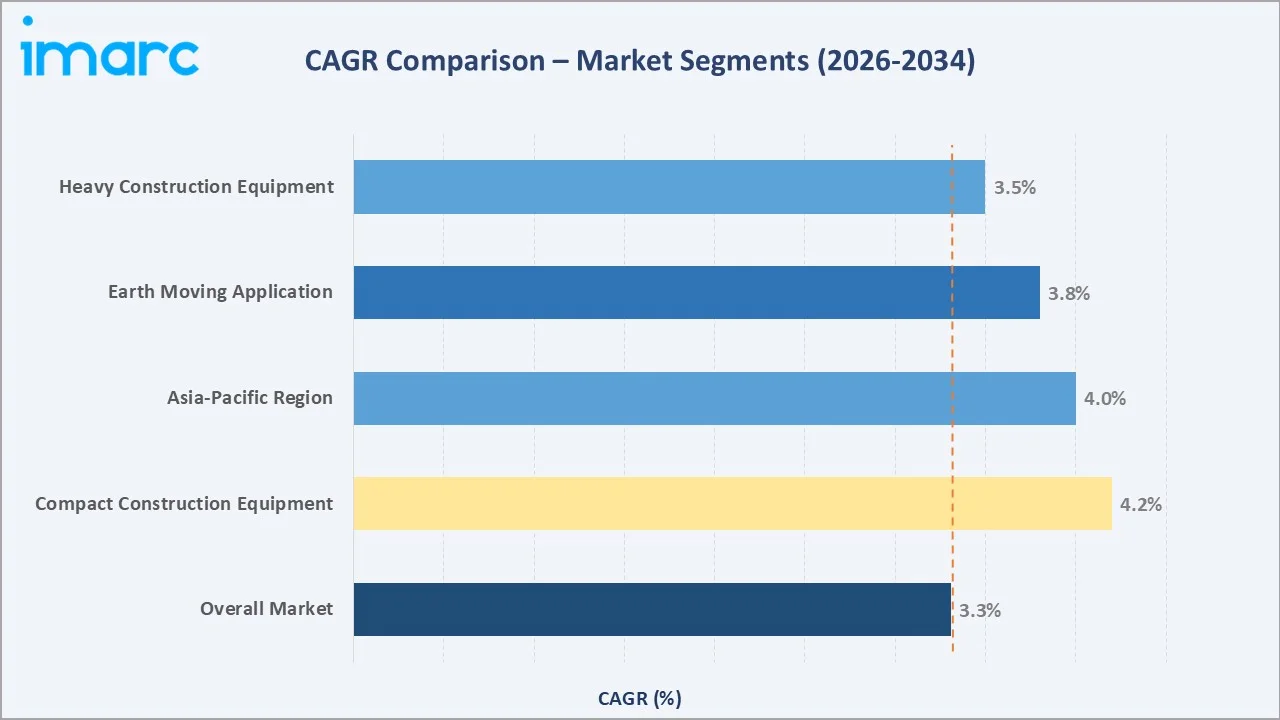

The CAGR trajectories across key equipment type, application, and regional sub-segments, with compact construction equipment at ~4.2% CAGR and earth moving applications at ~3.8% CAGR, are the fastest-growing categories within the global construction equipment industry through 2034.

Executive Summary

The global construction equipment market is on a sustained growth trajectory from USD 258.54 Billion in 2025 to USD 352.00 Billion by 2034. Construction equipment is essential across earthmoving, excavation, lifting, and transportation tasks in infrastructure and industrial construction.

Heavy construction equipment dominates at 65.0% in 2025, owing to its indispensable role in large-scale infrastructure, mining, and industrial projects. The Global Mining Dataset identifies 15,188 mining and/or processing facilities, producing 47 different primary commodities, increasing the demand of construction equipment’s globally.

Compact construction equipment (35.0%) is the fastest-growing segment, driven by urban densification, space-constrained renovation projects, and rapid expansion of the global equipment rental market in emerging economies.

Asia-Pacific dominates at 43.8% in 2025, reflecting China's and India's massive construction programmes. North America (22.6%) and Europe (18.4%) follow, driven by infrastructure reinvestment cycles and semiconductor facility construction waves respectively.

Key Market Insights

|

Insight |

Data |

|

Largest Equipment Type |

Heavy Construction Equipment – 65.0% share (2025) |

|

Leading Application |

Earth Moving – 51.0% share (2025) |

|

Leading Region |

Asia-Pacific – 43.8% revenue share (2025) |

|

Second Region |

North America – 22.6% revenue share (2025) |

|

Top Companies |

AB Volvo, Caterpillar Inc., CNH, Deere & Company, Hitachi Construction Machinery, Komatsu Ltd., Liebherr-International AG |

Key analytical observations expanding on the above data:

- Heavy construction equipment, with 65.0% in 2025, dominates because it is indispensable for large-scale infrastructure projects, road building, dam construction, port expansion, and mining, all characterized by long project timelines and high per-unit procurement values.

- Earth moving, with 51.0% in 2025, leads application because excavators, bulldozers, and motor graders underpin virtually every construction project type globally, from site preparation and grading to tunnelling and foundation excavation, ensuring consistent procurement.

- Asia-Pacific's 43.8% dominance reflects China's Belt and Road infrastructure pipeline, India's National Infrastructure Pipeline of USD 1.4 Trillion, and ASEAN's accelerating industrialization, creating unparalleled construction equipment demand across the region.

- North America, with 22.6% in 2025, benefits from the US Bipartisan Infrastructure Law's USD 1.2 Trillion investment and the CHIPS Act semiconductor fabrication construction wave, generating sustained earthmoving and lifting equipment procurement from domestic manufacturers.

Global Construction Equipment Market Overview

Construction equipment encompasses a wide range of heavy machinery and vehicles, including excavators, bulldozers, loaders, cranes, motor graders, dump trucks, and compactors, used across earthmoving, lifting, material handling, and transportation applications in construction projects globally.

The global ecosystem integrates steel and component manufacturers, OEMs, dealership and distribution networks, rental fleet operators, EPC contractors, and diverse end-use industries spanning infrastructure, mining, oil and gas, manufacturing, and commercial real estate construction.

Market Dynamics

To evaluate market opportunities, Request Sample

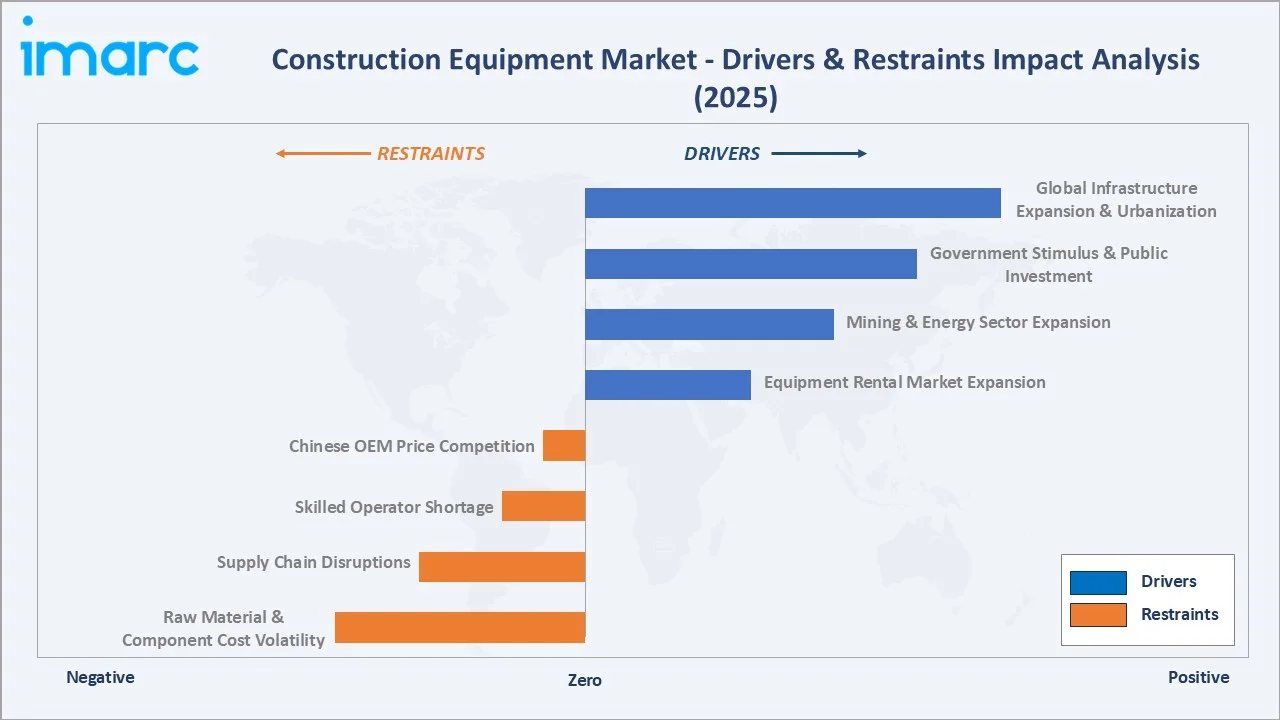

Market Drivers

- Global Infrastructure Expansion and Urbanization: The World Bank estimates USD 94 Trillion in global infrastructure investment is needed through 2040 to meet developing economic urbanization demands, directly driving sustained equipment procurement across all categories.

- Government Stimulus and Public Investment Programmes: The US Bipartisan Infrastructure Law (USD 1.2 Trillion), India's NIP (USD 1.4 Trillion through 2025), and China's infrastructure stimulus packages are generating record construction equipment procurement cycles globally.

- Mining and Energy Sector Expansion: LNG capacity additions of approximately 200 million additional tonnes by 2030 and expanding mineral extraction for energy transition supply chains drive heavy earthmoving and excavation equipment demand from resource-rich economies.

Market Restraints

- Raw Material and Component Cost Volatility: Steel prices fluctuated between USD 605 and USD 900 per tonne from 2019 through 2022, directly impacting OEM manufacturing costs and creating margin pressure when contract pricing cannot absorb input cost escalation rapidly.

- Skilled Operator Shortage and Labour Constraints: A global shortage of qualified equipment operators limits construction productivity and delays infrastructure projects, indirectly constraining equipment utilization rates and dampening procurement expansion in key markets.

Market Opportunities

- Electrification and Green Equipment Transition: Tightening emission standards (EU Stage V, US Tier 4 Final) and corporate ESG mandates are accelerating demand for electric and hybrid construction equipment.

- Equipment Rental Market Expansion: The shift toward construction equipment rental is driven by contractors prioritizing capital efficiency and flexible cost structures, as renting converts large upfront investments into variable expenses. Project-based demand and fluctuating equipment need make ownership less viable, while rental reduces idle time and improves utilization.

Market Challenges

- Supply Chain Disruptions and Component Shortages: Semiconductor shortages impacting telematics and engine control systems extend equipment lead times to 12-18 months, creating order backlogs and delivery challenges that constrain revenue realization for OEMs globally.

- Intense Competition from Chinese OEMs: Intense competition from Chinese OEMs is reshaping the global construction equipment landscape, particularly in price-sensitive emerging markets. Their cost-competitive offerings and rapid international expansion are putting downward pressure on pricing and margins for Western manufacturers. Additionally, strong local distribution networks and financing support enhance their competitiveness across regions like Southeast Asia, Africa, and Latin America. This intensifies market fragmentation and forces incumbents to rethink pricing, localization, and value propositions.

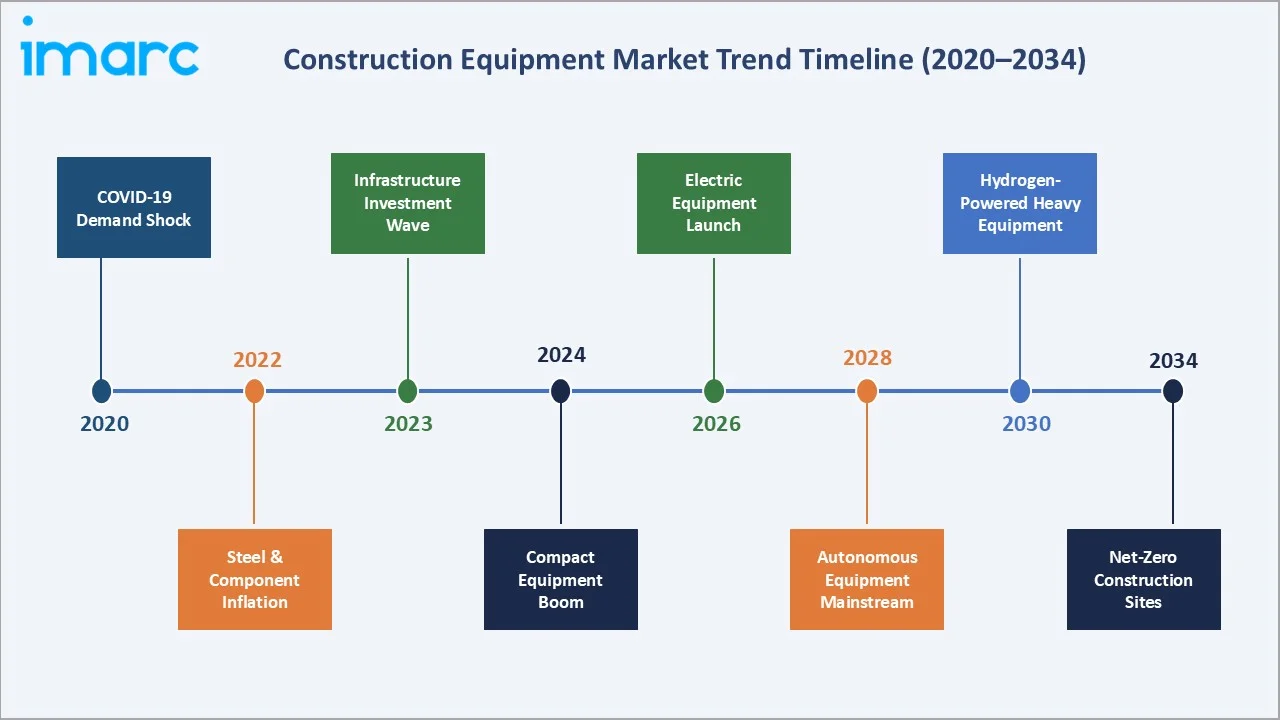

Emerging Market Trends

1. Telematics and IoT-Enabled Fleet Management

Connected construction equipment with embedded telematics is transforming fleet management, maintenance scheduling, and utilization optimization. IoT integration reduces unplanned downtime by up to 30%, improving asset utilization rates across rental and owned fleets globally.

2. Electrification and Hybrid Powertrain Adoption

Electric excavators, loaders, and compact equipment are gaining specification in urban construction zones where emission and noise regulations restrict diesel operation.

3. Autonomous and Semi-Autonomous Equipment

Autonomous haulage systems and GPS-guided grading are advancing from mining applications toward mainstream construction deployment. Komatsu's Smart Construction and Caterpillar's Command for Dozing represent the frontier of operator-assist and remote-control capability.

4. Modular and Rental-Optimized Equipment Design

OEMs are redesigning product lines for rental market optimization, incorporating standardized quick-attach interfaces, simplified maintenance access, and robust telematics to reduce total cost of ownership and accelerate the shift away from ownership-based procurement models.

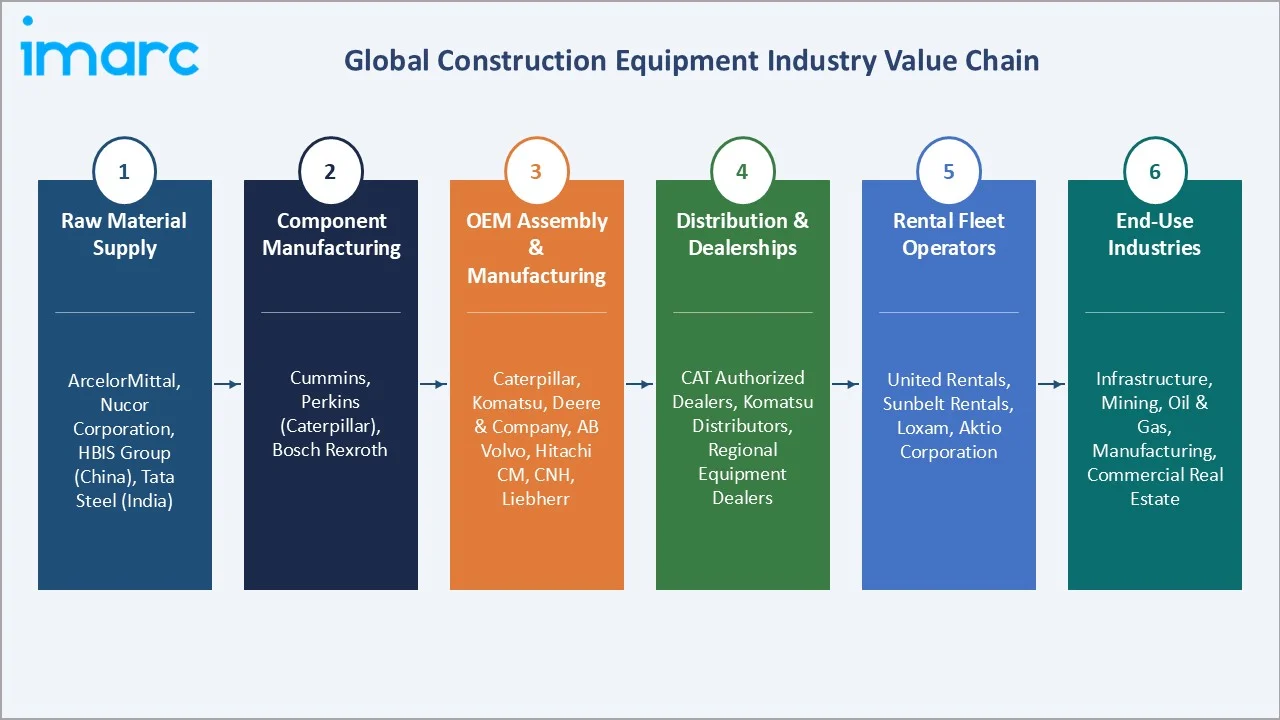

Industry Value Chain Analysis

The construction equipment value chain spans six stages from raw material input through end-use deployment. OEM manufacturing and aftermarket services capture the highest value-add margins, while distribution and rental logistics generate significant working capital requirements.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

ArcelorMittal, Nucor Corporation, HBIS Group (China), Tata Steel (India) |

|

Engine & Component Mfg. |

Cummins, Perkins (Caterpillar), Bosch Rexroth |

|

OEM Manufacturing |

Caterpillar, Komatsu, Deere & Company, AB Volvo, Hitachi CM, CNH, Liebherr |

|

Distribution & Dealerships |

CAT authorized dealers, Komatsu distributors, regional equipment dealers |

|

Rental Fleet Operators |

United Rentals, Sunbelt Rentals, Loxam, Aktio Corporation |

|

End-Use Industries |

Infrastructure, Mining, Oil & Gas, Manufacturing, Commercial Real Estate |

Technology Landscape in the Construction Equipment Industry

Powertrain Technology: Diesel to Electrification

Diesel powertrains remain dominant at approximately 85% of new equipment sales in 2025, but electrification is accelerating. Battery-electric compact equipment under 6 tonnes is commercially viable, while hydrogen fuel cell technology is piloted for larger equipment categories through 2030.

Hydraulics and Control Systems Innovation

Electro-hydraulic control systems, load-sensing hydraulics, and advanced joystick controls are improving fuel efficiency by 10-20% and enhancing precision in grading, trenching, and lifting applications, while GPS machine guidance systems reduce rework and improve job site productivity.

Digital Connectivity and Machine Learning

AI-powered predictive maintenance platforms analyze telematics data streams from connected fleets, enabling condition-based maintenance that reduces unplanned failures. Caterpillar's Cat Connect and Komatsu's KOMTRAX are the industry benchmarks for connected equipment ecosystems globally.

Market Segmentation Analysis

By Equipment Type

Heavy construction equipment commands a 65.0% majority share in 2025, owing to its essential role in large-scale infrastructure, mining, and industrial construction projects globally. In January 2026, Volvo Construction Equipment introduced the EC950 High Reach, its largest demolition excavator to date, designed for high-rise dismantling applications. The machine combines a modular, multi-configuration design with enhanced stability, advanced demolition technology, and integrated safety features to deliver efficient performance in complex jobsite conditions.

To access detailed market analysis, Request Sample

Compact construction equipment at 35.0% in 2025, benefits from urban construction densification, renovation activity, and the rapid expansion of the global equipment rental market, particularly mini excavators, skid steers, and compact track loaders in emerging economies.

By Application

Earth moving dominates at 51.0% in 2025, as excavators, bulldozers, and motor graders underpin every construction project category, from road building and foundation excavation to mining site preparation, ensuring sustained, non-discretionary demand regardless of economic cycle.

Excavation and mining (18.6%) are driven by copper, lithium, and iron ore expansion for energy transition supply chains. Lifting and material handling (14.3%) benefits from e-commerce warehouse and high-rise construction demand. Transportation (10.4%) and others (5.7%) complete the application landscape.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

43.8% |

China's Belt & Road; India's NIP; ASEAN industrialization; offshore energy |

|

North America |

22.6% |

CHIPS Act semiconductor fabs; Bipartisan Infrastructure Law; LNG expansion; data centers |

|

Europe |

18.4% |

Industrial reinvestment; EU Green Deal; offshore wind; CBAM compliance |

|

Latin America |

5.6% |

Brazil Petrobras offshore; Chile/Peru mining; Mexico nearshoring manufacturing |

|

Middle East & Africa |

9.6% |

GCC Vision 2030; NEOM mega-projects; African mining & infrastructure investment |

Asia-Pacific's 43.8% market dominance in 2025 is driven by China's sustained infrastructure investment and India's accelerating road, metro, port, and affordable housing construction activity under the National Infrastructure Pipeline through 2030.

North America, with 26.5% in 2025, is experiencing a pronounced industrial renaissance. The Bipartisan Infrastructure Law's USD 1.2 Trillion investment, combined with the CHIPS Act semiconductor fabrication facility construction wave, generates sustained equipment procurement demand.

Competitive Landscape

The global construction equipment market is moderately consolidated, with the top five players accounting for approximately 50-55% of global revenue. Regional competition is intense, with Chinese OEMs rapidly expanding share in Asia, Africa, and Latin America.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

AB Volvo (Volvo CE) |

Excavators, Articulated Haulers, Wheel Loaders |

Leader |

Europe & Americas; electrification leadership; Tier 1 markets |

|

Caterpillar Inc. |

Full Equipment Range, VisionLink Telematics |

Leader |

Global market leader; vertically integrated; services and digital |

|

CNH |

Case & New Holland Equipment Ranges |

Challenger |

Americas & Europe; construction and agriculture synergies |

|

Deere & Company |

Excavators, Dozers, Motor Graders, Loaders |

Leader |

Americas leader; smart construction; precision earthmoving |

|

Hitachi Construction Machinery |

Excavators, Wheel Loaders, Rigid Dump Trucks |

Challenger |

Asia-Pacific; mining and quarry; IoT-connected fleet solutions |

|

Komatsu Ltd. |

Full Range, KOMTRAX Telematics, Autonomous Haul |

Leader |

Global; autonomous mining; Smart Construction platform leader |

|

Liebherr-International AG |

Cranes, Earthmoving, Mining Equipment |

Challenger |

Europe & global; premium engineering; specialty cranes and mining |

The competitive positioning of key global construction equipment market participants is AB Volvo (Volvo CE), Caterpillar Inc., CNH, Deere & Company, Hitachi Construction Machinery, Komatsu Ltd., Liebherr-International AG, and others.

Key Company Profiles

Caterpillar Inc.

Caterpillar Inc. is the world's largest construction equipment manufacturer, headquartered in Irving, Texas. Its vertical integration from components through distribution and financial services creates unmatched total value capture across the global equipment industry.

- Product Portfolio: Full range of earthmoving, mining, lifting, and paving equipment plus Product Link (hardware) + VisionLink (software) and Cat Financial products.

- Recent Developments: In January 2026, Caterpillar announced an expanded collaboration with NVIDIA to accelerate physical AI and robotics across heavy industry, debuting the Cat AI Assistant on a Cat 306 CR Mini Excavator.

- Strategic Focus: Caterpillar's strategy leverages its global dealer network across 190 countries, Cat Financial services, and Cat Connect digital platform to generate recurring services revenue exceeding 30% of total revenues while expanding electric and autonomous product ranges.

Komatsu Ltd.

Komatsu Ltd. is the world's second-largest construction and mining equipment manufacturer, headquartered in Tokyo, Japan. Its KOMTRAX telematics system, deployed across 600,000+ machines globally, is the industry's most extensive connected equipment network.

- Product Portfolio: Excavators, bulldozers, motor graders, articulated dump trucks, autonomous mining haul trucks, and KOMTRAX connected equipment solutions.

- Recent Developments: In August 2025, Komatsu launched the PC20E-6 electric mini excavator in Europe, featuring a 23.2 kWh battery with zero emissions, backed by the Komatsu E-Support maintenance programme.

- Strategic Focus: Komatsu's Smart Construction platform integrates drones, GPS guidance, compaction measurement, and KOMTRAX telematics to deliver connected job site solutions creating switching costs through data continuity and workflow integration that differentiates beyond the machine itself.

Deere & Company

Deere & Company, headquartered in Moline, Illinois, is a leading manufacturer of construction and agricultural equipment. Its construction division leverages precision agriculture technology into precision earthmoving and grade control applications across global markets.

- Product Portfolio: Excavators, bulldozers, motor graders, wheel loaders, and John Deere Operations Center connected fleet management platform.

- Recent Developments: In January 2026, Deere & Company announced the expansion of its domestic manufacturing footprint by establishing two new U.S. facilities, a distribution center in Indiana and an excavator factory in North Carolina, as part of its long-term investment strategy. The move is aimed at strengthening supply chain efficiency, enhancing parts availability, and localizing production by shifting some manufacturing from Japan to the U.S.

- Strategic Focus: Deere's construction equipment strategy differentiates on grade control technology, rapid dealer service response times, and competitive John Deere Financial programs, critical advantages in the North American mid-market contractor segment where service uptime is the primary criterion.

AB Volvo (Volvo CE)

AB Volvo's construction equipment division is a global leader headquartered in Gothenburg, Sweden, recognized as the pioneer in electric construction equipment and an industry leader in articulated haulers, excavators, and wheel loaders across global markets.

- Product Portfolio: Excavators, articulated haulers, wheel loaders, motor graders, and an expanding range of battery-electric and hybrid construction equipment models.

- Recent Developments: In January 2025, Volvo CE revealed articulated hauler, featuring innovations for interconnected solutions, enhanced productivity, and significantly reduced emissions.

- Strategic Focus: Volvo CE's strategy focuses on leading the industry's transition to carbon-neutral construction through battery-electric and hydrogen fuel cell powertrains, targeting urban construction zones with strict emission regulations and corporate clients with science-based emissions targets.

Market Concentration Analysis

The global construction equipment market is moderately consolidated at the global level, with the top five players accounting for approximately 50-55% of global revenue. No single company holds more than 15-18% of total global market revenue in 2025.

Consolidation through M&A is ongoing at the component and regional distributor level. Global OEMs are acquiring telematics, software, and rental platform companies to expand recurring revenue streams beyond equipment sales cycles, creating defensible competitive positions.

Investment & Growth Opportunities

Fastest-Growing Segments

Compact construction equipment at ~4.2% CAGR through 2034 is the highest-growth equipment type segment, driven by urban construction densification and rental market expansion. Earth moving at ~3.8% CAGR represents the broadest-based growth opportunity across all construction categories.

Emerging Markets

The Middle East and Africa at ~4.1% CAGR is the fastest-growing region through 2034. Saudi Arabia's NEOM project, UAE industrial zone expansion, and African mining infrastructure investment create large-scale equipment procurement from a region with limited domestic manufacturing capacity.

Venture & Investment Trends

Private equity interest in equipment rental consolidation, telematics software platforms, and electrification component suppliers is growing strongly. OEM investment in autonomous systems and AI-based job site optimization represents the frontier of technology-led competitive differentiation through the forecast period to 2034.

Future Market Outlook (2026-2034)

The global construction equipment market is forecast to expand from USD 258.54 Billion in 2025 to USD 352.00 Billion by 2034 at a CAGR of 3.31%, adding USD 93.5 Billion in incremental annual market value over the forecast period, reflecting infrastructure-linked demand.

Three technological forces will most significantly shape the construction equipment industry through 2034: full electrification of compact equipment, autonomous haulage and grade control becoming mainstream, and AI-enabled job site platforms creating new recurring service revenues.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews with construction equipment industry stakeholders, including senior OEM commercial managers, EPC procurement specialists, fleet managers, rental operators, and construction contractors across Asia-Pacific, North America, and Europe in 2024-2025.

Secondary Research

Key secondary sources include Association of Equipment Manufacturers (AEM) data, IEA World Energy Investment Report (2024), G20 Infrastructure Investment Hub, US Census Bureau construction spending data, and trade publications including Equipment World and Construction Equipment magazine.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, infrastructure investment data, and historical market evolution patterns. Scenario analysis covered base, optimistic, and conservative cases to account for macroeconomic uncertainty.

Construction Equipment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Solution Types Covered | Products, Services |

| Equipment Types Covered | Heavy Construction Equipment, Compact Construction Equipment |

| Types Covered | Loader, Cranes, Forklift, Excavator, Dozers, Others |

| Applications Covered | Excavation and Mining, Lifting and Material Handling, Earth Moving, Transportation, Others |

| Industries Covered | Oil and Gas, Construction and Infrastructure, Manufacturing, Mining, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | AB Volvo (Volvo CE), Caterpillar Inc., CNH, Deere & Company, Hitachi Construction Machinery, Komatsu Ltd., Liebherr-International AG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, construction equipment market forecast, historical and current market trends, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global construction equipment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the construction equipment industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Construction Equipment Market Report

The global construction equipment market reached USD 258.54 Billion in 2025, reflecting consistent demand from global infrastructure investment, industrial construction, and energy sector expansion.

The market is projected to reach USD 352.00 Billion by 2034, growing at a CAGR of 3.31% during 2026-2034, driven by Asia-Pacific construction, energy transition infrastructure, and semiconductor facility investment.

Heavy construction equipment leads with a 65.0% share in 2025, valued for its essential role in large-scale infrastructure, mining, and industrial construction projects.

Earth moving leads at 51.0% in 2025, representing the foundational requirement across virtually every construction project from road building and foundation excavation to mining site preparation globally.

Asia-Pacific commands a dominant 43.8% market share in 2025, driven by China's infrastructure investment, India's National Infrastructure Pipeline, and ASEAN industrialization generating unparalleled equipment demand.

Compact construction equipment is the fastest-growing segment at 4.2% CAGR through 2034, driven by urban construction densification, renovation activity, and global equipment rental market expansion.

Leading companies include AB Volvo (Volvo CE), Caterpillar Inc., CNH, Deere & Company, Hitachi Construction Machinery, Komatsu Ltd., Liebherr-International AG, and others.

Key applications include earthmoving, excavation and mining, lifting and material handling, transportation, road building, and demolition across infrastructure, oil and gas, mining, and commercial real estate.

Renewable energy infrastructure construction including offshore wind, solar farms, and hydrogen production plants is generating specialized heavy equipment demand growing at 2-3x standard market rates through 2034.

China operates the world's largest construction market, India's NIP targets USD 1.4 Trillion in infrastructure, and ASEAN's rapid industrialization combine to create unparalleled demand scale in the region through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)