Essential Oils Market Size, Share, Trends and Forecast by Product, Application, Sales Channel, and Region, 2026-2034

Global Essential Oils Market Size, Share, Trends & Forecast (2026-2034

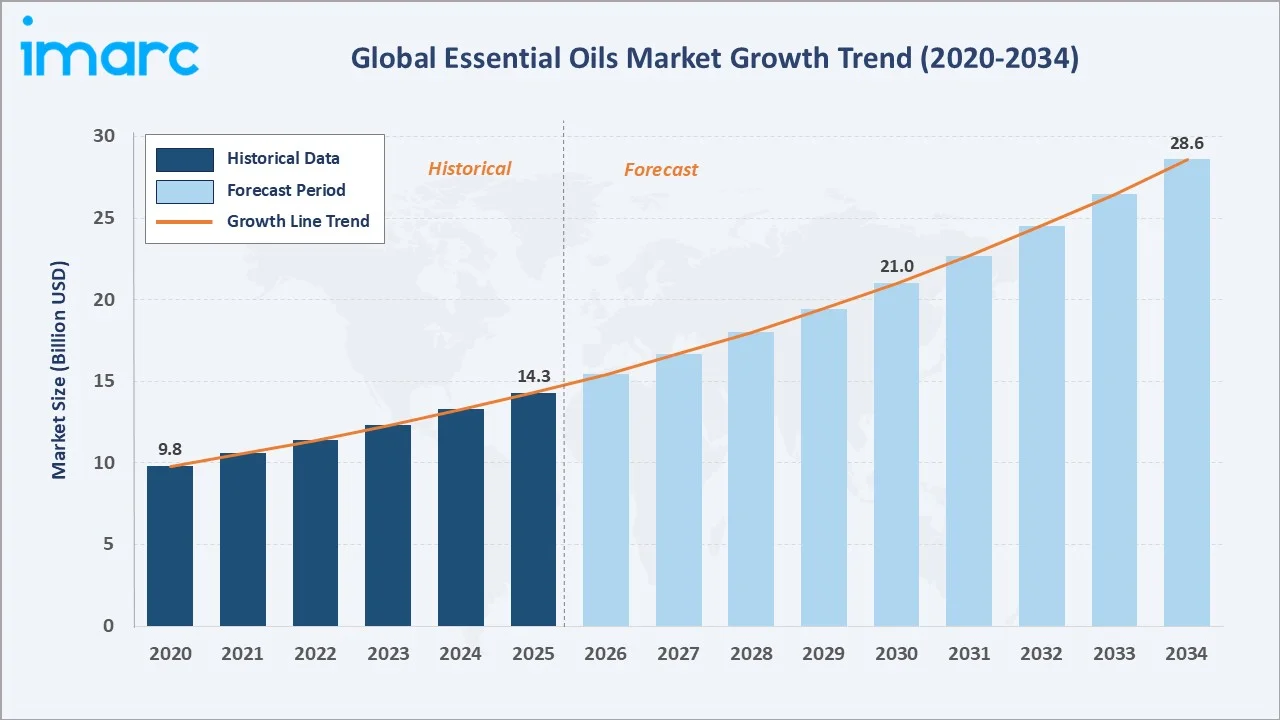

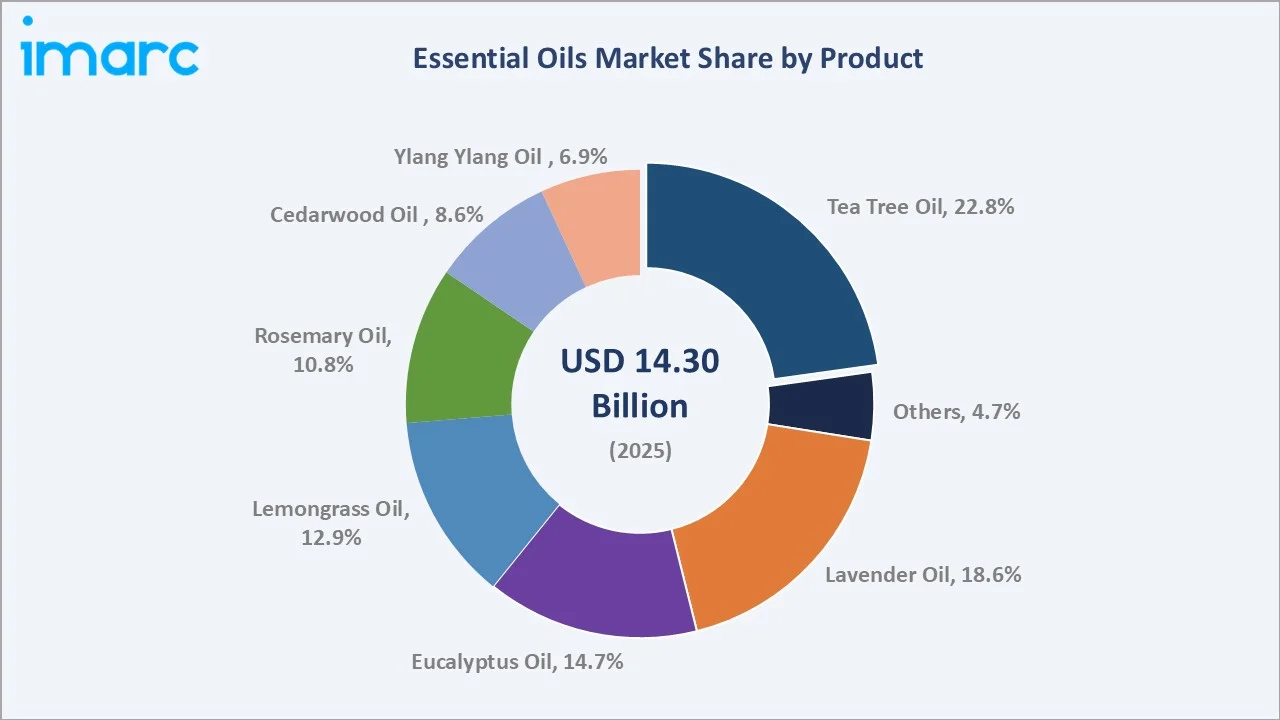

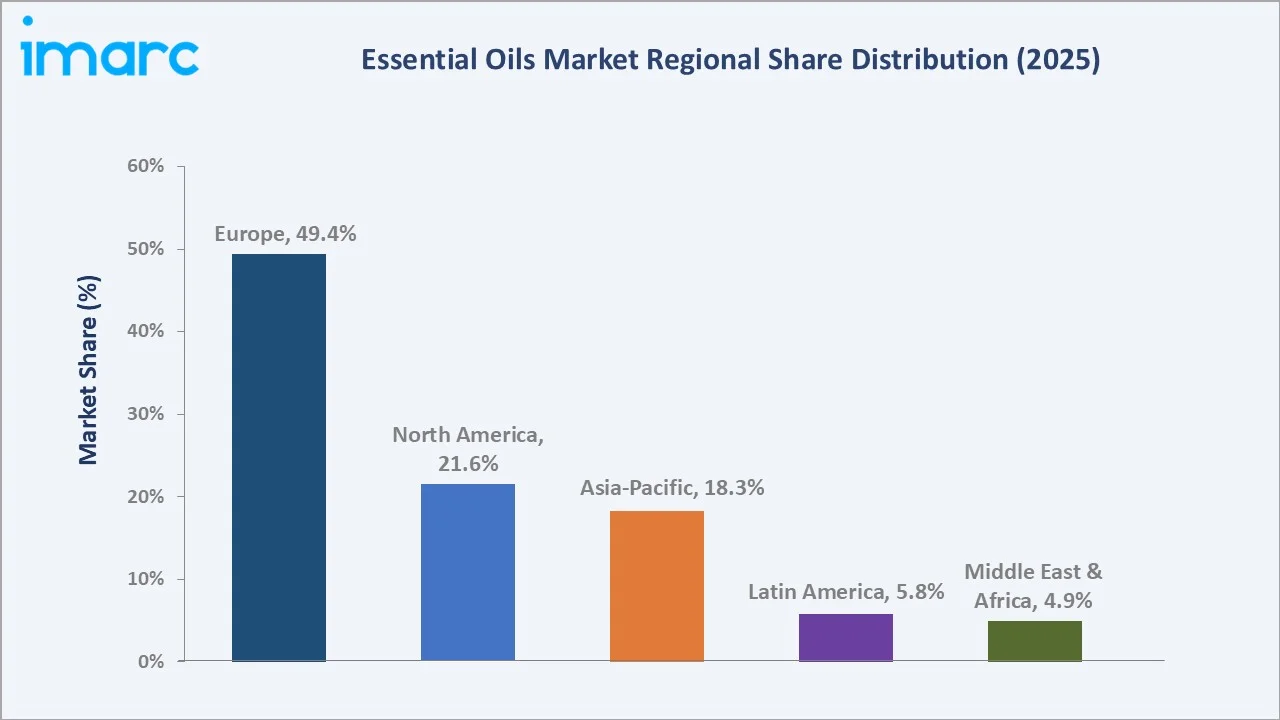

The global essential oils market size was valued at USD 14.3 Billion in 2025 and is projected to reach USD 28.6 Billion by 2034, exhibiting a CAGR of 7.97% during the forecast period 2026-2034. Rising demand for natural wellness and aromatherapy, clean-label food and beverage formulations, plant-based cosmetics, and rapid online channel expansion are driving the essential oils market growth. Tea Tree Oil leads the product at 22.8% share in 2025, while Online Stores account for 55.0% of global sales channels. Europe dominates with 49.4% of global revenue in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 14.3 Billion |

|

Forecast Market Size (2034) |

USD 28.6 Billion |

|

CAGR (2026-2034) |

7.97% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe (49.4% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

|

Leading Product |

Tea Tree Oil (22.8%, 2025) |

|

Leading Sales Channel |

Online Stores (55.0%, 2025) |

The global essential oils market growth trajectory from 2020 through 2034 contrasts historical expansion with a sustained forecast curve powered by wellness trends, natural personal care demand, and accelerating e-commerce penetration across Europe, North America, and Asia-Pacific.

To get more information on this market, Request Sample

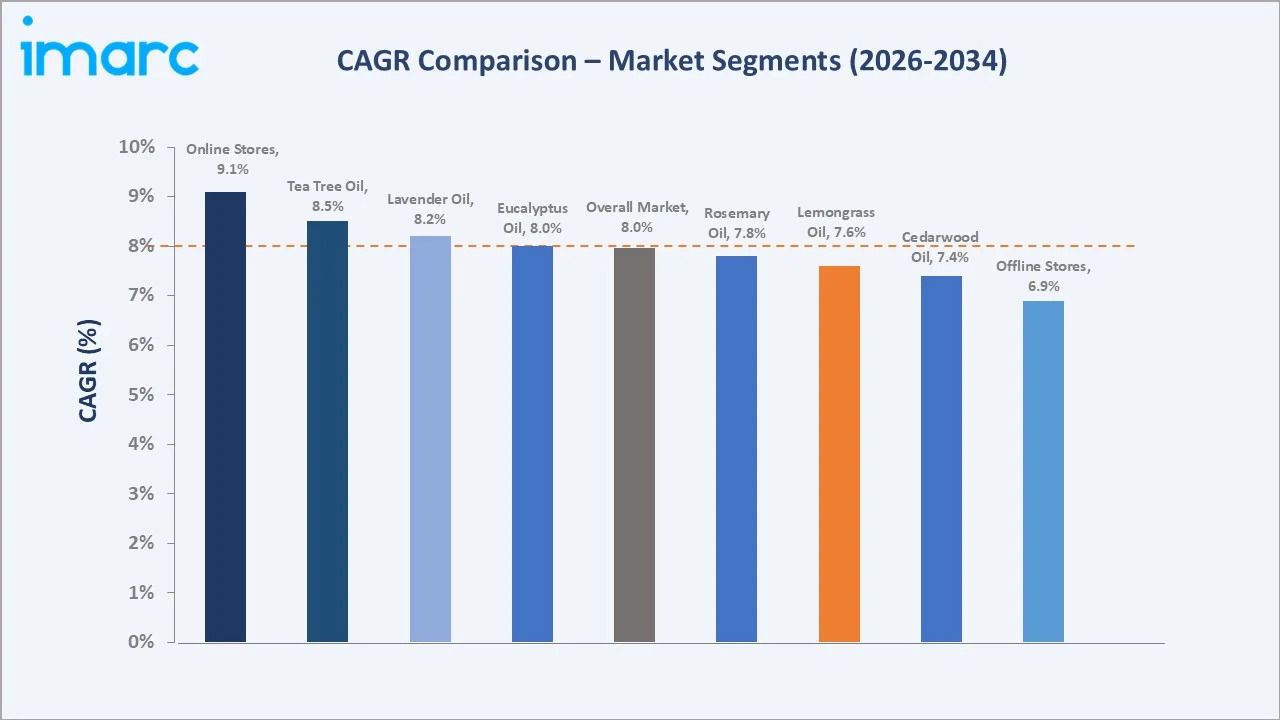

Segment-level CAGR comparisons highlight Online Stores and Tea Tree Oil as the fastest-growing sub-categories within the global essential oils market forecast through 2034, outpacing traditional offline distribution and mature product segments.

Executive Summary

The global essential oils market is undergoing strong structural expansion, driven by consumer preference for natural ingredients, aromatherapy and wellness adoption, and clean-label formulation trends in personal care and food. Valued at USD 14.3 Billion in 2025, the market is forecast to nearly double and reach USD 28.6 Billion by 2034 at a CAGR of 7.97%.

Tea Tree Oil commands the largest product share at 22.8% in 2025, driven by its antimicrobial applications in personal care and cleaning. Lavender Oil follows at 18.6%, anchored by aromatherapy and sleep-wellness demand. On the sales channel front, Online Stores account for 55.0%, overtaking offline distribution and projected to grow fastest at ~9.1% CAGR through 2030.

Europe leads with 49.4% global revenue share in 2025. France and Bulgaria anchor lavender production, while Germany and the UK lead consumption. North America holds 21.6% and Asia-Pacific 18.3%, with India and China emerging as major growth markets. The essential oils market outlook remains strong as premiumization, sustainable sourcing, and blockchain-enabled traceability converge across major markets.

Key Market Insights

|

Insight |

Data |

|

Largest Product |

Tea Tree Oil - 22.8% share (2025) |

|

Second Product |

Lavender Oil - 18.6% share (2025) |

|

Largest Sales Channel |

Online Stores - 55.0% share (2025) |

|

Fastest Growing Channel |

Online Stores - ~9.1% CAGR (2025-2030) |

|

Leading Region |

Europe - 49.4% revenue share (2025) |

|

Top Companies |

doTerra, Young Living, Biolandes, Givaudan, Rocky Mountain Oils. |

|

Market Opportunity |

Clinical aromatherapy, clean-label F&B, natural cosmetics |

Key Analytical Observation Supporting The Above Data:

- Tea Tree Oil's 22.8% dominance in 2025 reflects strong demand across acne care, skincare, and antimicrobial personal care. Advances in analytical techniques are strengthening the authentication of Australian tea tree oil, helping detect adulteration with synthetic or lower-quality substitutes and reinforcing its premium positioning in global markets.

- Lavender Oil's 18.6% share is anchored by the aromatherapy and sleep-wellness segment. France, Bulgaria, and China dominate global lavender oil production, collectively accounting for a majority share of supply and serving as key sources of high-quality and pharmaceutical-grade oils

- Online Stores' 55.0% channel majority reflects consumer preference for direct-to-consumer aromatherapy brands, E-commerce platforms and direct-to-consumer models are playing an increasingly central role in the essential oils market, with online channels accounting for a significant share of sales and subscription-based offerings supporting recurring revenue and customer engagement.

- Europe's 49.4% global dominance reflects France and Bulgaria as major production hubs, Germany and the UK as premium consumption centers, and deep consumer wellness culture. EU natural cosmetics market volumes crossed EUR 15 billion in 2024, creating structural downstream demand.

- Clean-label and aromatherapy demand together account for nearly 60% of new essential oils consumption growth. Aromatherapy adoption is rising globally, with increasing use of diffusers in homes, spas, and wellness environments, though industry metrics are typically measured in revenue and device sales rather than usage sessions.

Global Essential Oils Market Overview

Essential oils are concentrated plant-derived aromatic compounds extracted from botanical sources through processes such as steam distillation, cold pressing, and supercritical CO2 extraction. The global market encompasses a broad product portfolio including Tea Tree Oil, Lavender Oil, Eucalyptus Oil, Lemongrass Oil, Rosemary Oil, Cedarwood Oil, Ylang Ylang Oil, and specialty blends. These oils serve diverse applications ranging from aromatherapy and personal care to pharmaceutical formulation, food and beverage flavoring, and household cleaning.

The industry operates at the intersection of agriculture, botanical extraction, and wellness-driven consumer demand. Growth is supported by macroeconomic drivers such as rising disposable incomes, premiumization of personal care, clean-label regulation, and increasing consumer preference for plant-based wellness. At the same time, the market is undergoing a structural shift toward blockchain-enabled supply chain traceability, therapeutic-grade certification, and sustainable regenerative sourcing, which are redefining quality benchmarks and procurement strategies across global markets.

Market Dynamics

To evaluate market opportunities, Request Sample

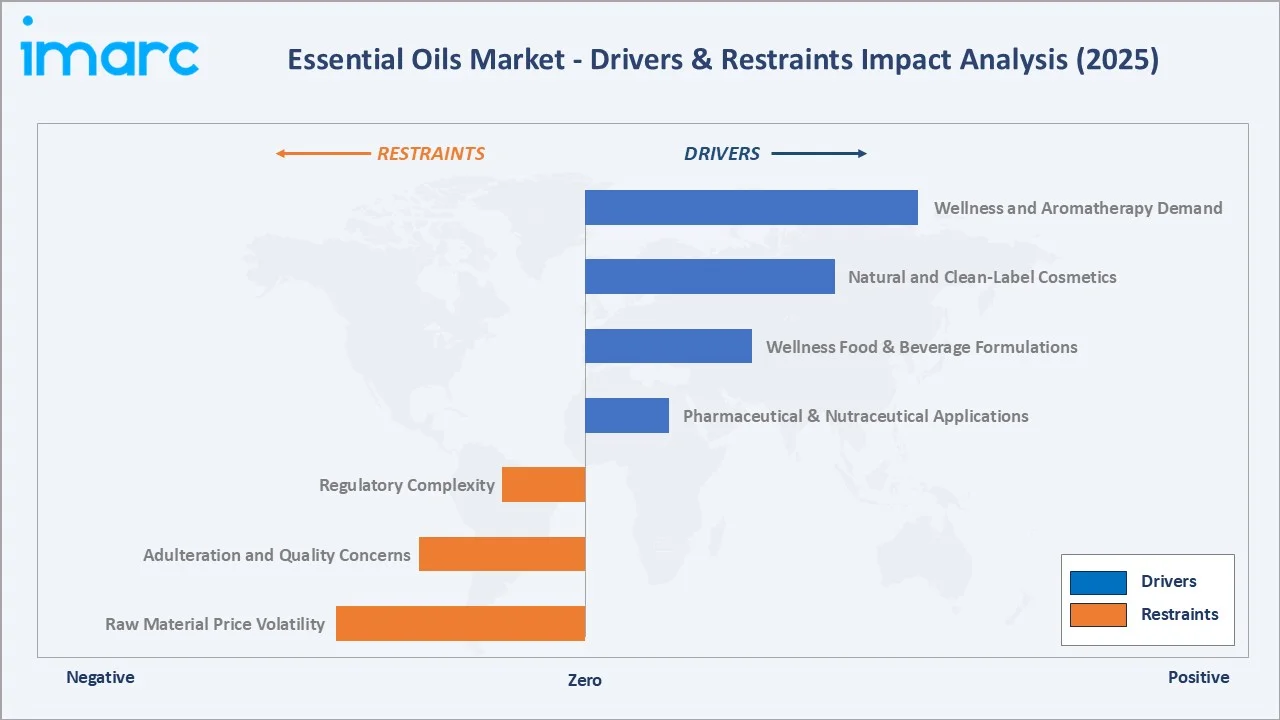

Market Drivers

- Wellness and Aromatherapy Demand: Global aromatherapy adoption continues to surge as consumers seek natural alternatives for stress management, sleep support, and home ambience. The global smart diffuser device installed base exceeded 85 million units in 2024, driving recurring demand for lavender, eucalyptus, and blend formulations across residential and spa channels.

- Natural and Clean-Label Cosmetics: The global natural cosmetics market surpassed USD 15 billion in 2024, per Ecovia Intelligence. Consumer preference for plant-based formulations is pushing essential oil inclusion across skincare, haircare, and perfumery. Brands such as L'Occitane and Aesop anchor premium essential-oil-based product lines across North America, Europe, and Asia.

- Wellness Food and Beverage Formulations: Food manufacturers are replacing artificial flavors and preservatives with natural essential oil extracts. Citrus oils (orange, lemon, bergamot), rosemary extract, and peppermint oil are increasingly used in functional beverages, bakery, and confectionery - with the global market growing 4-5% annually through 2030.

- Pharmaceutical and Nutraceutical Applications: Clinical research supports essential oil use in antimicrobial, digestive, and respiratory applications. Tea tree oil has established WHO monograph status for skin infections, while eucalyptus and peppermint oils are growing in over-the-counter cough and cold product formulations across pharmacy retail channels globally.

Market Restraints

- Raw Material Price Volatility: Weather events, crop disease, and geographic concentration drive significant price swings. Lavender oil prices have experienced significant volatility driven by climate shocks in key producing regions such as Provence, where droughts and frost events have disrupted yields and tightened supply. Similarly, tea tree oil prices remain sensitive to weather conditions in Australia, with climatic variability and production cycles contributing to fluctuations in supply and pricing.

- Adulteration and Quality Concerns: The industry faces widespread adulteration with synthetic additives and cheaper substitute oils. Research published by ISO and IFEAC indicates that up to 30% of commercially sold essential oils contain undisclosed adulterants, undermining consumer trust and premium pricing.

- Regulatory Complexity: Varying regulations across food, cosmetic, and pharmaceutical classifications create compliance burden. EU Cosmetic Regulation 1223/2009, US FDA GRAS standards, and IFRA safety guidelines impose different testing and labelling requirements for the same oil in different applications.

Market Opportunities

- Clinical Aromatherapy and Wellness: Hospital integrative medicine programs and corporate wellness initiatives are adopting clinical-grade essential oils for stress, pain, and sleep management. The US hospital aromatherapy adoption expanded to over 500 facilities in 2024, creating a high-margin institutional procurement opportunity.

- Sustainable and Organic Sourcing: Consumer willingness-to-pay for certified organic and fair-trade essential oils has climbed significantly. Certified organic volumes grew 14% in 2024 globally, with premium pricing over conventional grades, creating attractive margin opportunities for vertically integrated brands.

- Direct-to-Consumer and Subscription Models: Subscription-based aromatherapy brands such as Vitruvi, Rocky Mountain Oils, and Public Goods are scaling rapidly. DTC subscription revenues in the essential oils category grew over 8% in 2024, signaling strong recurring-revenue business model potential.

Market Challenges

- Storage and Shelf-Life Constraints: Essential oils are sensitive to light, heat, and oxygen exposure, creating cold-chain storage requirements and limited shelf life. This constrains retail merchandising options and creates inventory write-off risks for smaller brands and distributors.

- Supply Chain Transparency: Long multi-tier supply chains from farm to end-product make traceability challenging. Blockchain-enabled traceability pilots by doTerra and Young Living have shown the technology's promise but remain costly to implement across smaller suppliers and growers.

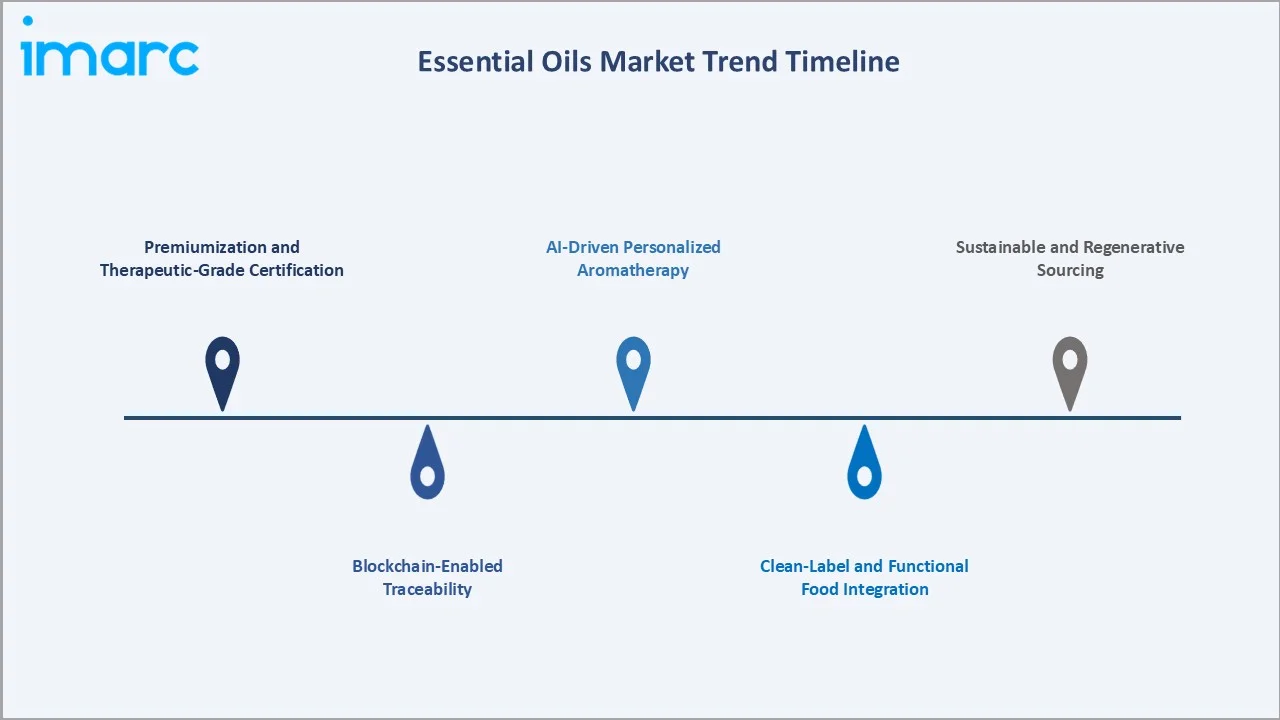

Emerging Market Trends

1. Premiumization and Therapeutic-Grade Certification

Therapeutic-grade and clinical-grade certifications command strong price premiums over standard-grade oils. doTerra's Certified Pure Tested Grade (CPTG) and Young Living's Seed to Seal programs anchor premium positioning with premium prices over mass-market oils. Consumer education around GC-MS testing is driving demand for certification across North American and European premium segments.

2. Blockchain-Enabled Traceability

Leading brands are deploying blockchain platforms to track oils from farm to bottle. doTerra's Co-Impact Sourcing program covers over 40 countries, while Young Living's Seed to Seal initiative provides farm-to-consumer transparency. These platforms address adulteration concerns and strengthen consumer trust in a category with significant counterfeit risk.

3. Clean-Label and Functional Food Integration

Food and beverage manufacturers are replacing synthetic flavors with essential oil-derived natural flavors. Citrus, rosemary, and peppermint oils are increasingly specified in functional beverages, plant-based dairy alternatives, and natural confectionery.

4. AI-Driven Personalized Aromatherapy

AI-enabled aromatherapy platforms recommend custom blends based on user mood, sleep, or stress profile data. Start-ups such as Moodo and Aera are integrating smart diffusers with personalized oil pod subscriptions. This trend is expected to reshape the premium consumer tier through 2030 as wellness tech convergence accelerates.

5. Sustainable and Regenerative Sourcing

Regenerative agriculture practices are being adopted for lavender, tea tree, and rose production. Certified organic volumes grew 14% in 2024, while fair-trade essential oil certification from Ecocert and USDA NOP expanded significantly. Shippers and consumers increasingly factor in carbon footprint and biodiversity credentials across premium tiers.

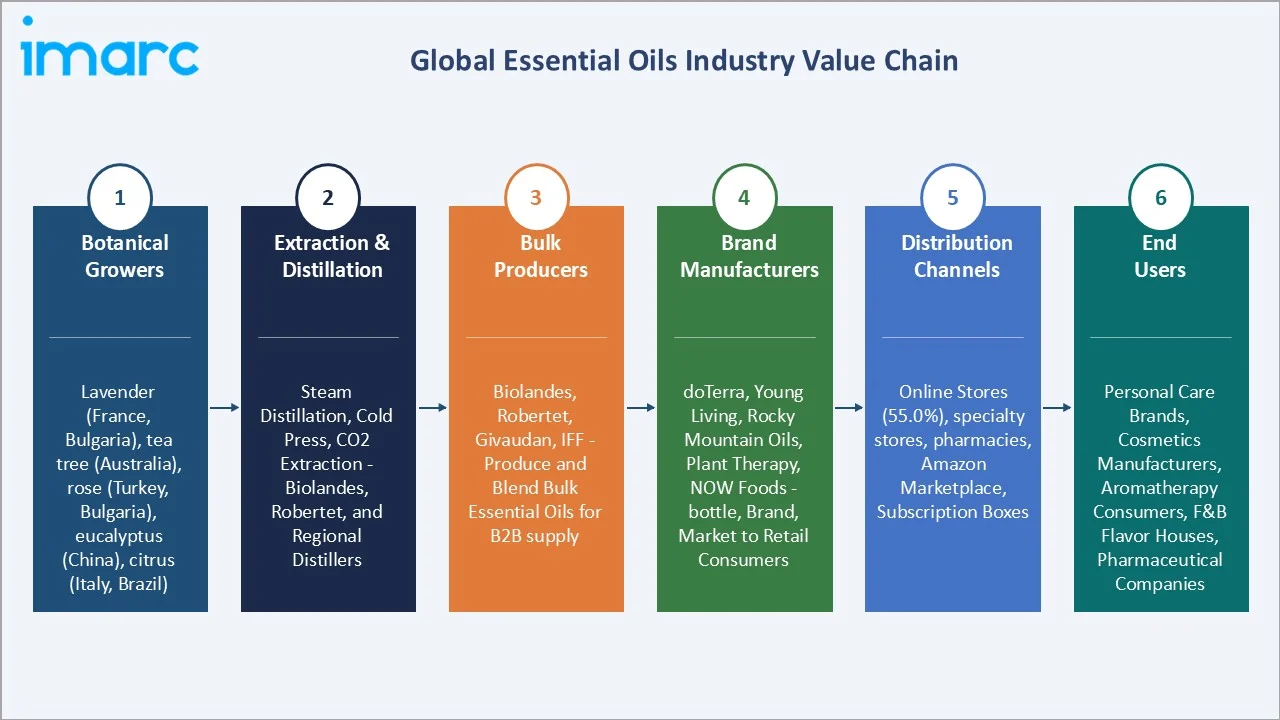

Industry Value Chain Analysis

The global essential oils value chain spans six integrated stages from botanical cultivation through end-consumer use. Each stage has distinct competitive dynamics, margin profiles, and technology investment requirements relevant to the overall essential oils market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Botanical Growers |

Lavender farms (France, Bulgaria), tea tree plantations (Australia), rose farms (Turkey, Bulgaria), eucalyptus (China, Australia), citrus (Italy, USA, Brazil) |

|

Extraction & Distillation |

Steam distillation, cold press, CO2 extraction, solvent extraction - performed by specialist processors including Biolandes, Robertet, and regional distillers |

|

Bulk Producers |

Biolandes, Robertet, Givaudan, IFF - produce and blend bulk essential oils for B2B supply to flavor, fragrance, and cosmetic manufacturers |

|

Brand Manufacturers |

doTerra, Young Living, Rocky Mountain Oils, Plant Therapy, NOW Foods - bottle, brand, and market essential oils to retail consumers |

|

Distribution Channels |

Online Stores (55.0%), Specialty stores, health stores, pharmacy retail, Amazon marketplace, subscription boxes |

|

End Users |

Personal care brands, cosmetics manufacturers, aromatherapy consumers, F&B flavor houses, pharmaceutical companies, cleaning product brands |

Brand manufacturers capture the highest strategic value by integrating cultivation partnerships, extraction quality control, certification programs, and direct consumer engagement into premium turnkey products. Meanwhile, online and DTC channels are reshaping distribution, letting brands bypass traditional intermediaries, strengthen customer relationships, and capture higher margins through subscription models.

Technology Landscape in the Essential Oils Industry

Advanced Extraction Technologies

Supercritical CO2 extraction is gaining traction for premium oils due to higher purity and reduced thermal degradation. Traditional steam distillation remains the dominant method covering over 70% of global volume, while cold-press and enfleurage techniques are used for citrus and delicate floral oils. Manufacturers are investing in solvent-free and closed-loop systems to improve yield and reduce environmental impact.

Blockchain and Supply Chain Traceability

Leading brands are deploying blockchain platforms to verify farm origin, extraction method, and quality testing. doTerra's Co-Impact Sourcing and Young Living's Seed to Seal programs provide consumers with farm-to-bottle transparency. These platforms address adulteration concerns and build premium brand equity in a category where counterfeit products remain a structural issue globally.

GC-MS Testing and Quality Certification

Gas chromatography-mass spectrometry (GC-MS) is the industry-standard method for verifying essential oil purity and chemotype. Certifications such as doTerra's CPTG, Young Living's Seed to Seal, and third-party testing by laboratories including Airase and Eden Labs have become the premium positioning benchmark. Consumer demand for batch-specific GC-MS reports is rising across North American and European markets.

Smart Diffusers and Wellness Tech

Connected aromatherapy devices from brands such as Aera, Moodo, and Pura integrate app-based scheduling, mood-based recommendations, and usage analytics. The global smart diffuser installed base crossed 5 million units in 2024. AI-personalized aromatherapy is emerging as a premium consumer tier, with subscription oil pod business models showing strong retention and recurring revenue economics.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Product | Tea Tree Oil | 22.8% |

2025 |

|

Application |

Spa and Relaxation | 46.5% |

2025 |

|

Sales Channel |

Offline Stores |

45.0% |

2025 |

|

Region |

Europe |

49.4% |

2025 |

IMARC Group provides an analysis of the key trends in each segment of the global essential oils market, along with forecasts at the global, regional, and country levels from 2026 to 2034. The market has been categorized based on product and sales channel.

By Product

Tea Tree Oil leads the global essential oils market product segment with a 22.8% share in 2025. Demand is driven by antimicrobial applications in acne treatment, skincare formulations, and natural cleaning products. Australian tea tree oil production grew exponentially in 2024, with steady price premiums over synthetic alternatives. Brand formulations from The Body Shop, Thursday Plantation, and Dickinson's anchor the mass-to-premium consumer tier globally.

To access detailed market analysis, Request Sample

Lavender Oil accounts for 18.6% of global product demand, anchored by aromatherapy and sleep-wellness applications. Eucalyptus Oil at 14.7% serves respiratory and cleaning uses. Lemongrass Oil (12.9%) and Rosemary Oil (10.8%) cover food flavoring, cosmetics, and haircare applications. Cedarwood Oil at 8.6% supports fragrance and pest-repellent categories. Ylang Ylang Oil (6.9%) anchors premium perfumery demand, and Others (4.7%) covers specialty oils including frankincense, rose, and neroli.

By Sales Channel

Online Stores represent 55.0% of global sales channels in 2025, overtaking offline distribution. E-commerce marketplaces such as Amazon, direct-to-consumer brand websites, and subscription platforms have reshaped essential oils retail. The DTC subscription category grew over 18% year-on-year in 2024, driven by brands such as Rocky Mountain Oils, Vitruvi, and Public Goods. Consumer preference for home delivery, product comparison tools, and verified review ecosystems continues to strengthen the online channel.

Offline Stores account for 45.0% of global channel demand. Specialty aromatherapy stores, health and wellness chains such as GNC and Holland & Barrett, pharmacy retail networks, and department store beauty counters anchor this segment. While offline share is contracting in mature markets, specialty and premium outlets maintain strong margins through personalized consultation, in-store sampling, and curated brand experiences that online channels cannot fully replicate.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe |

49.4% |

France and Bulgaria production hubs, EU natural cosmetics demand, premium aromatherapy culture, organic certification |

|

North America |

21.6% |

Wellness boom, DTC brand scale (doTerra, Young Living), clinical aromatherapy adoption, natural beauty premium |

|

Asia-Pacific |

18.3% |

India production base, China consumption rise, Japan premium fragrance, Australia tea tree plantations |

|

Latin America |

5.8% |

Brazil citrus exports, Mexico lime and bergamot, Argentina aromatic herbs, growing middle-class wellness demand |

|

Middle East & Africa |

4.9% |

Rose production in Morocco and Egypt, UAE premium fragrance imports, frankincense and myrrh from Oman and Somalia |

Europe commands 49.4% global revenue share in 2025. France and Bulgaria anchor global lavender production, while Germany, the UK, and Italy lead consumption. The EU natural cosmetics market volumes crossed EUR 15 billion in 2024, creating strong downstream demand for essential oil inputs. Regulatory frameworks including EU Cosmetic Regulation 1223/2009 and IFRA guidelines shape quality and safety standards, with organic certification (Ecocert, COSMOS) commanding price premiums. Europe's deep aromatherapy culture and premium wellness consumer base sustain structural leadership.

North America holds 21.6% of global revenue, driven by the wellness boom, premium aromatherapy adoption, and DTC brand scale. The United States accounts for the majority of the region, with doTerra and Young Living headquartered in Utah. Integrative medicine programs in U.S. hospitals are increasingly incorporating clinical aromatherapy as a complementary therapy to support patient comfort, pain management, and anxiety reduction, although adoption is not formally quantified at a national facility level, supporting institutional procurement growth alongside strong residential demand.

Asia-Pacific holds 18.3% and is projected to be the fastest-growing region. India is a major production base for sandalwood, jasmine, and spice-derived oils, while China anchors eucalyptus and camphor production. Japan's premium fragrance market and South Korea's K-beauty sector drive incremental consumption. Australia remains the world's dominant tea tree oil producer with over 1,100 tons of annual output.

Latin America accounts for 5.8%, led by Brazil's citrus oil exports, Mexico's lime and bergamot production, and Argentina's aromatic herbs. The Middle East & Africa represents 4.9%, anchored by Moroccan and Egyptian rose production, Omani and Somali frankincense, and UAE premium fragrance imports supplying the GCC luxury perfume market.

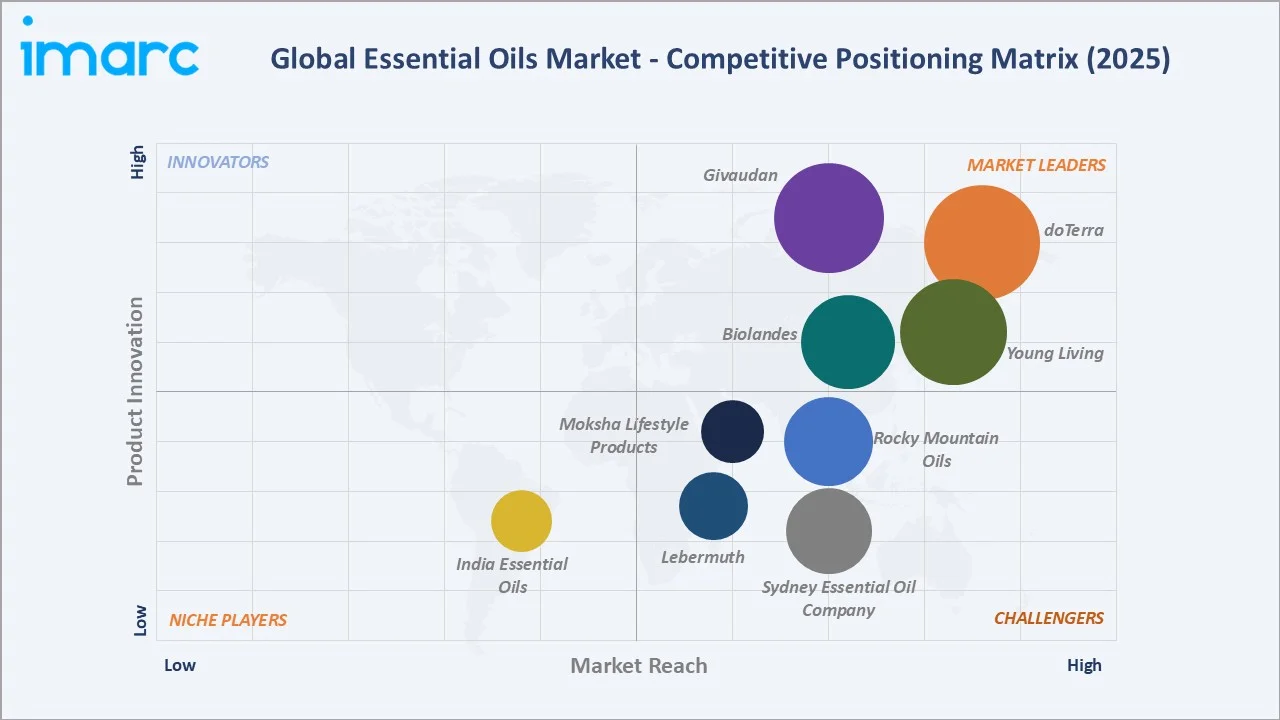

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

doTerra |

doTerra |

Leader |

Co-Impact Sourcing, MLM network, therapeutic-grade positioning |

|

Young Living Essential Oils |

Young Living |

Leader |

Farm-owned model, vertical integration, global MLM distribution |

|

Biolandes |

Biolandes |

Leader |

France-based, upstream extraction leader, B2B flavor-fragrance supply |

|

Givaudan |

Ungerer & Company |

Leader |

Global bulk supplier, flavor-fragrance breadth |

|

Rocky Mountain Oils LLC |

Rocky Mountain Oils |

Challenger |

DTC e-commerce model, GC-MS transparency, US retail focus |

|

Lebermuth |

Lebermuth |

Challenger |

Custom blending, B2B flavor-fragrance, US specialty supply |

|

Moksha Lifestyle Products |

Moksha Lifestyle |

Challenger |

India-based, organic certification, global e-commerce reach |

|

Sydney Essential Oil Company |

Sydney Essential Oil Company |

Challenger |

Australia-based, tea tree specialization, B2B bulk focus |

|

India Essential Oils |

India Essential Oils |

Emerging |

Sandalwood, spice oils, India-led production and export |

The global essential oils market's competitive landscape is moderately fragmented. The market features vertically-integrated branded players (doTerra, Young Living) at the premium MLM tier, specialized upstream extractors (Biolandes, Givaudan) serving B2B flavor-fragrance clients, and a growing set of DTC disruptors (Rocky Mountain Oils, Plant Therapy, NOW Foods) targeting direct consumer channels. Strategic acquisitions and vertical integration are key competitive moves - Givaudan acquired Ungerer to strengthen its portfolio.

Key Company Profiles

doTerra

doTerra is a privately held essential oils and wellness products company headquartered in Pleasant Grove, Utah, USA. Founded in 2008, it operates globally through a multi-level marketing distribution network of over 5 million Wellness Advocates, supported by Co-Impact Sourcing partnerships in over 40 countries.

- Product & Platform Portfolio: doTerra's portfolio spans over 150 single oils and proprietary blends, covering its flagship CPTG Certified Pure Tested Grade range, Deep Blue Rub, On Guard immunity blend, and the Co-Impact Sourcing program. The company also offers supplements, personal care, and household cleaning products integrated with essential oil formulations.

- Recent Developments: doTERRA continues to operate its Co-Impact Sourcing model, enabling traceability and farmer partnerships across its essential oil supply chain, including frankincense sourcing from East Africa and helichrysum sourcing from Mediterranean regions.

- Strategic Focus: doTerra's strategy centers on vertical supply-chain integration through Co-Impact Sourcing, therapeutic-grade positioning via CPTG certification, and expansion of its Wellness Advocate distribution network into Asia-Pacific and Latin America growth markets.

Young Living Essential Oils

Young Living Essential Oils, founded by D. Gary Young in 1993, is a privately held essential oils and wellness products company headquartered in Lehi, Utah, USA. The company operates its Seed to Seal quality commitment across owned farms in the USA, France, Croatia, and Ecuador, serving customers in more than 100 countries.

- Product & Platform Portfolio: Young Living's portfolio includes over 600 products across single oils, blends, personal care, nutritional supplements, and household cleaning. Flagship offerings include the Everyday Oils Collection, Thieves proprietary blend, NingXia Red nutritional drink, and KidScents line for children's wellness.

- Recent Developments: In 2024, Young Living expanded its Seed to Seal quality verification across all farms and global supply partners. The company launched new frankincense and sacred oils collections and extended its Ecuador Finca Botanica Aromatica farm footprint to support premium oil production volumes.

- Strategic Focus: Young Living's strategy emphasizes farm-owned vertical integration, Seed to Seal quality leadership, and MLM-driven distribution expansion. Investment priorities include regenerative farming practices, blockchain-enabled traceability, and clinical research validating therapeutic efficacy of essential oils.

Biolandes

Biolandes, headquartered in Le Sen, France, is a leading global producer of natural aromatic extracts and essential oils. Founded in 1980, the company operates extraction sites and agricultural partnerships across Bulgaria, Madagascar, Morocco, and Turkey, serving flavor, fragrance, cosmetics, and aromatherapy clients globally.

- Product & Platform Portfolio: Biolandes produces a wide portfolio of natural extracts including lavender, rose, jasmine, tuberose, mimosa, and violet absolutes. The company offers steam distillation, CO2 extraction, and solvent extraction services, with specialist capabilities in premium floral absolutes used by luxury perfumery brands.

- Recent Developments: In 2025, Biolandes and its subsidiary Biocosmethic showcased their portfolio of natural cosmetic ingredients and botanical extracts at In-Cosmetics Global in Paris, one of the leading international trade events for the beauty industry.

- Strategic Focus: Biolandes' strategy centers on upstream extraction leadership, sustainable and organic sourcing, and partnerships with premium luxury perfumery clients. The company is expanding blockchain-enabled traceability for floral absolutes to meet growing client demands for supply-chain transparency.

Market Concentration Analysis

The global essential oils market exhibits moderate fragmentation. The top five players - doTerra, Young Living, Biolandes, Givaudan, and Rocky Mountain Oils - collectively account for an estimated 25-32% of global market revenue in 2025. The remaining market share is distributed across specialty B2B extractors such as Robertet, Givaudan, IFF, and Treatt, plus hundreds of regional brands, DTC challengers, and national producers serving local markets.

The market is experiencing a bifurcated competitive dynamic. At the premium MLM and DTC tier, vertical integration and certification programs are creating moats around brand equity and pricing power. Simultaneously, B2B bulk supply consolidation is intensifying as global flavor-fragrance players acquire specialist extractors - Givaudan acquired Ungerer in 2020, Givaudan acquired Vika B.V. and Naturex in recent years, and strategic M&A remains active through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Online Stores are the highest-growth distribution sub-segment at approximately 9.1% CAGR through 2030, driven by DTC brand scale, subscription models, and Amazon marketplace dominance. Tea Tree Oil is the fastest-growing product category at 8.5% CAGR, while premium therapeutic-grade certified oils command 30-60% price premiums, representing the highest-margin growth opportunity across all consumer tiers.

Emerging Market Expansion

India represents the highest-potential emerging market, both as a production base for sandalwood, jasmine, and spice oils and as a rapidly growing domestic consumption market driven by ayurvedic wellness culture. China's premiumization trend, Southeast Asia's spa and hospitality expansion, and Latin America's natural cosmetics growth collectively offer significant volume and value opportunities for brands with local distribution capabilities through 2034.

Venture and Strategic Investment Trends

Strategic acquisitions are reshaping the competitive landscape – Givaudan’s acquisition of Ungerer, Givaudan's acquisition of Naturex, and IFF's merger with DuPont Nutrition reshaped the B2B flavor-fragrance upstream. Venture investment has flowed into AI-personalized aromatherapy platforms (Moodo, Aera), regenerative farming initiatives, and blockchain traceability platforms. Wellness tech convergence and sustainability investment remain primary capital allocation themes through 2034.

Future Market Outlook (2026-2034)

The global essential oils market forecast projects robust value expansion from USD 14.3 Billion in 2025 to USD 28.6 Billion by 2034 at a CAGR of 7.97%. Europe will retain regional leadership while Asia-Pacific emerges as the fastest-growing region. North America will sustain premium-value growth through clinical aromatherapy adoption, natural beauty premium, and DTC brand scale.

Three key shifts will reshape the essential oils market through 2034. First, therapeutic-grade certification and blockchain-enabled traceability will move from premium differentiators to consumer expectations, reshaping brand economics across all price tiers. Second, clean-label food and beverage formulations will drive incremental B2B demand for citrus, rosemary, and herbal oils as manufacturers replace synthetic flavors. Third, AI-personalized aromatherapy and smart diffusion platforms will create new premium consumer tiers, converging wellness, lifestyle tech, and subscription business models by 2030.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with essential oils industry stakeholders, including product directors at brand manufacturers, procurement managers at flavor-fragrance houses, buyers at specialty wellness retail chains, organic certification auditors, and institutional aromatherapy program directors. Primary insights validated market sizing, segmentation estimates, and consumer-adoption timelines.

Secondary Research

Secondary sources include Ecovia Intelligence natural cosmetics data, Organic Trade Association reports, ISO and IFEAC industry guidelines, company annual reports, trade publications including Perfumer & Flavorist, Essential Oil University Journal, and Aroma Research Journal, and regional industry association databases across Europe, North America, and Asia-Pacific.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating wellness consumer spending growth, natural cosmetics and personal care category expansion, clean-label F&B trends, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic and supply-chain uncertainty.

Essential Oils Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Cedarwood Oil, Eucalyptus Oil, Lavender Oil, Lemongrass Oil, Rosemary Oil, Tea Tree Oil, Ylang Ylang Oil, Others |

| Applications Covered |

|

| Sales Channels Covered | Offline Stores, Online Stores |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | doTerra, Young Living Essential Oils, Biolandes, Givaudan, Rocky Mountain Oils LLC, Lebermuth, Moksha Lifestyle Products, Sydney Essential Oil Company, India Essential Oils, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the essential oils market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global essential oils market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the essential oils industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Essential Oils Market Report

The global essential oils market was valued at USD 14.3 Billion in 2025, driven by wellness demand, natural cosmetics growth, clean-label F&B formulation, and rapid online channel expansion globally.

The market is projected to reach USD 28.6 Billion by 2034, growing at a CAGR of 7.97% during 2026-2034, supported by aromatherapy adoption, premiumization, and sustainable regenerative sourcing trends.

Tea Tree Oil leads with a 22.8% share in 2025, driven by antimicrobial applications in acne care, skincare, and natural cleaning products, with Australia as the dominant global production source.

Online Stores dominate with 55.0% share in 2025, driven by DTC brand growth, Amazon marketplace scale, and subscription-based aromatherapy commerce across major consumer markets globally.

Europe dominates with a 49.4% share in 2025, anchored by French and Bulgarian production hubs, strong premium consumer culture, and the region's robust natural cosmetics and aromatherapy industries.

Key drivers include global wellness boom, aromatherapy adoption, natural cosmetics growth, clean-label F&B demand, pharmaceutical applications, rising disposable incomes, and DTC e-commerce expansion globally.

Major players include doTerra, Young Living Essential Oils, Biolandes, Givaudan, Rocky Mountain Oils LLC, Lebermuth, Moksha Lifestyle Products, Sydney Essential Oil Company, India Essential Oils

Online Stores are the fastest-growing sales channel, advancing at approximately 9.1% CAGR through 2030, driven by DTC subscription models, Amazon marketplace dominance, and smart diffuser ecosystem growth.

Key opportunities include clinical aromatherapy platforms, therapeutic-grade certification programs, blockchain traceability, regenerative organic sourcing, AI-personalized blends, and India-Southeast Asia market expansion.

Research indicates up to 30% of lavender and rose oils contain undisclosed adulterants, undermining trust. Brands are investing in blockchain traceability and GC-MS testing to address this structural quality challenge.

Tea Tree Oil is the fastest-growing product at 8.5% CAGR through 2034, driven by skincare, antimicrobial applications, and household cleaning demand across North American, European, and Asia-Pacific consumer markets.

The market is moderately fragmented - the top five players (doTerra, Young Living, Biolandes, Givaudan, Rocky Mountain Oils) hold about 25-32% of global revenue in 2025, with active B2B consolidation ongoing.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)