Metal Injection Molding Market Size, Share, Trends and Forecast by Material Type, End Use Industry, and Region, 2026-2034

Global Metal Injection Molding Market Size, Share, Trends & Forecast (2026-2034)

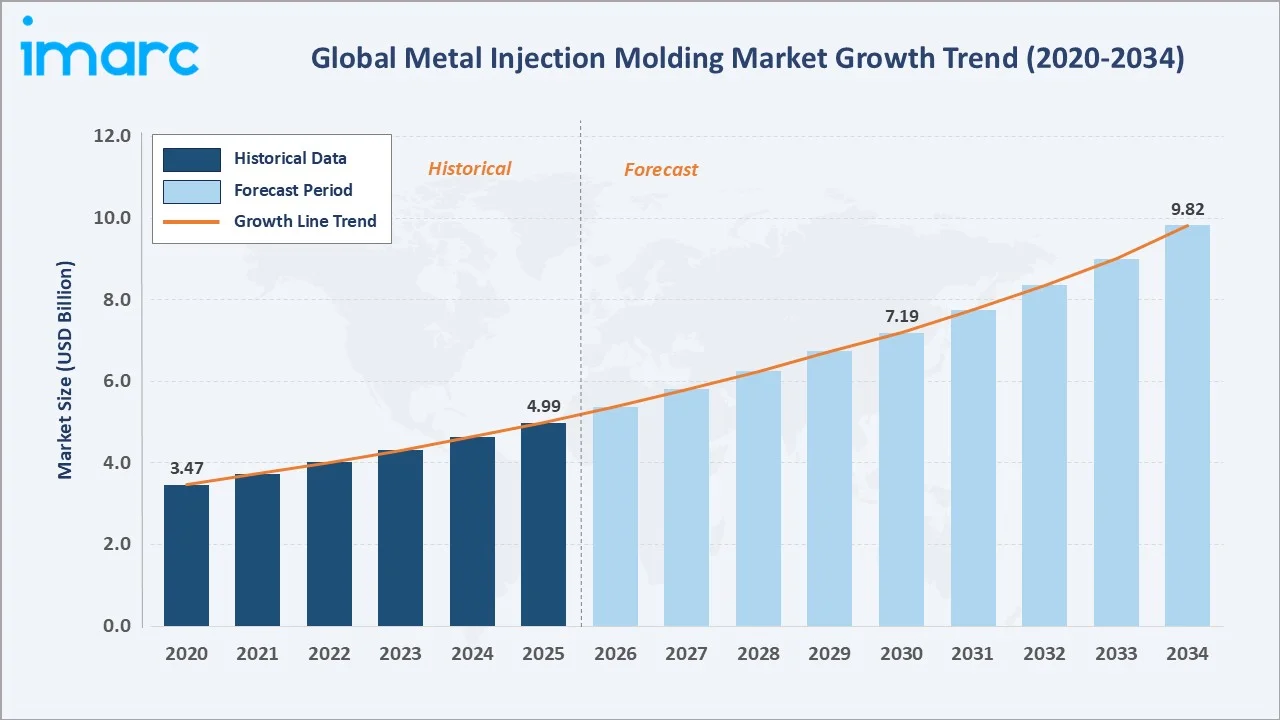

The global metal injection molding market size was valued at USD 4.99 Billion in 2025 and is projected to reach USD 9.82 Billion by 2034, exhibiting a CAGR of 7.57% during the forecast period 2026-2034. Rising demand for complex, high-precision components across automotive, medical, and consumer electronics sectors is driving the metal injection molding market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.99 Billion |

|

Forecast Market Size (2034) |

USD 9.82 Billion |

|

CAGR (2026-2034) |

7.57% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (47.1% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (~8.1% CAGR) |

|

Leading End Use Industry |

Consumer Products (30.5%, 2025) |

|

Leading Material Type |

Stainless Steel (51.6%, 2025) |

The global metal injection molding market growth trajectory from 2020 through 2034 contrasts historical expansion against a sustained forecast curve powered by demand for miniaturized, high-precision parts in defense, automotive electrification, and minimally invasive medical devices.

To get more information on this market, Request Sample

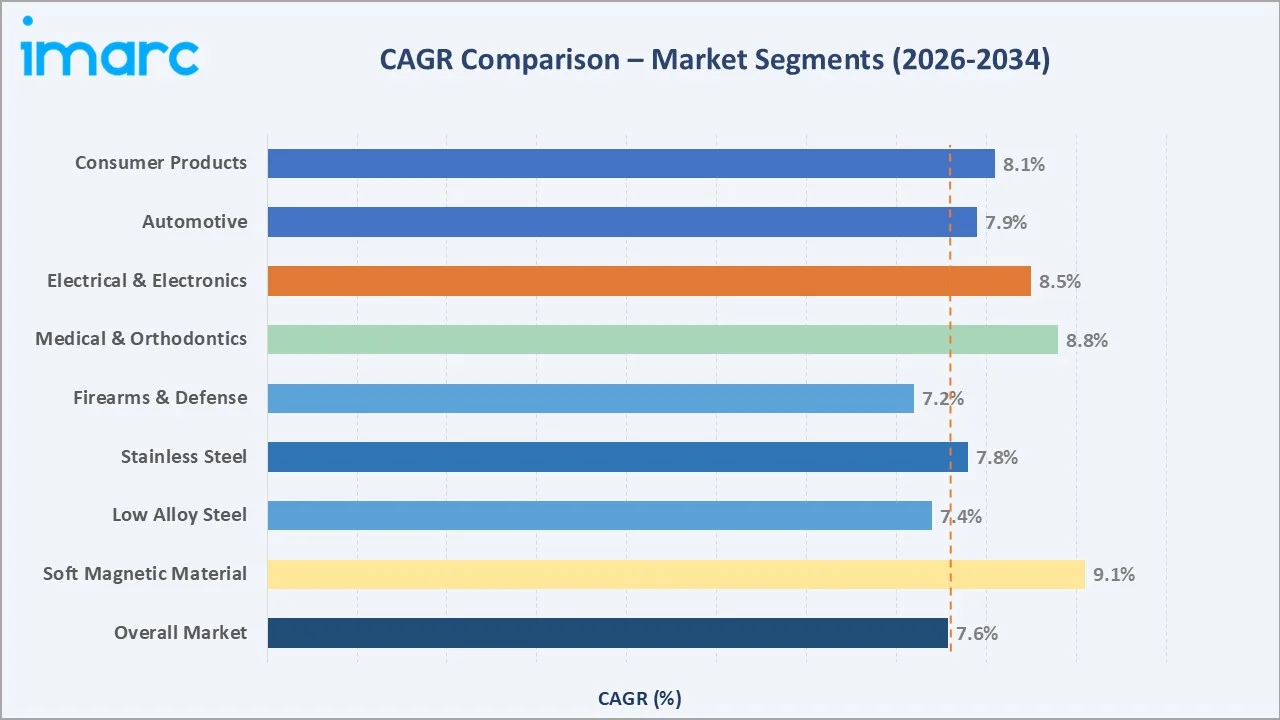

Segment-level CAGR comparisons below highlight medical device adoption and soft magnetic material as the fastest-growing sub-categories within the global metal injection molding market forecast through 2034.

Executive Summary

The global metal injection molding (MIM) market is experiencing robust expansion. It is underpinned by surging demand for complex, near-net-shape metallic components that traditional machining cannot economically produce. Valued at USD 4.99 Billion in 2025, the market is projected to nearly double, reaching USD 9.82 Billion by 2034, at a CAGR of 7.57%.

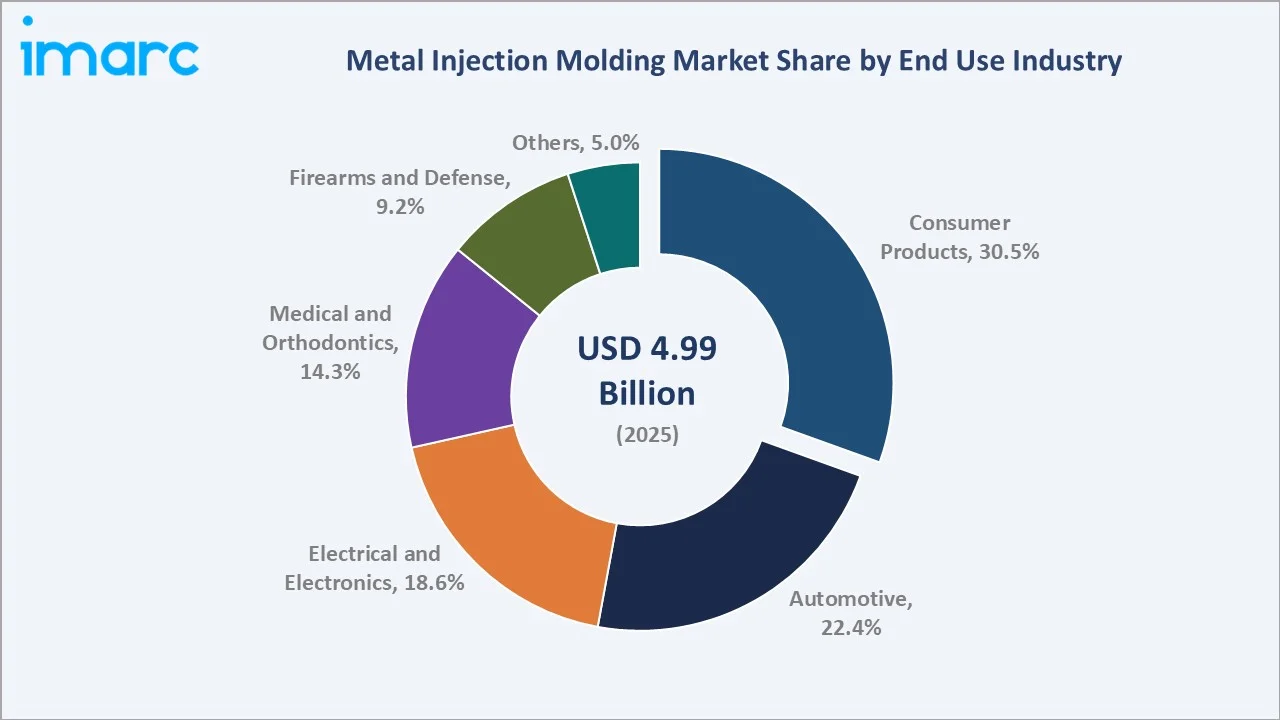

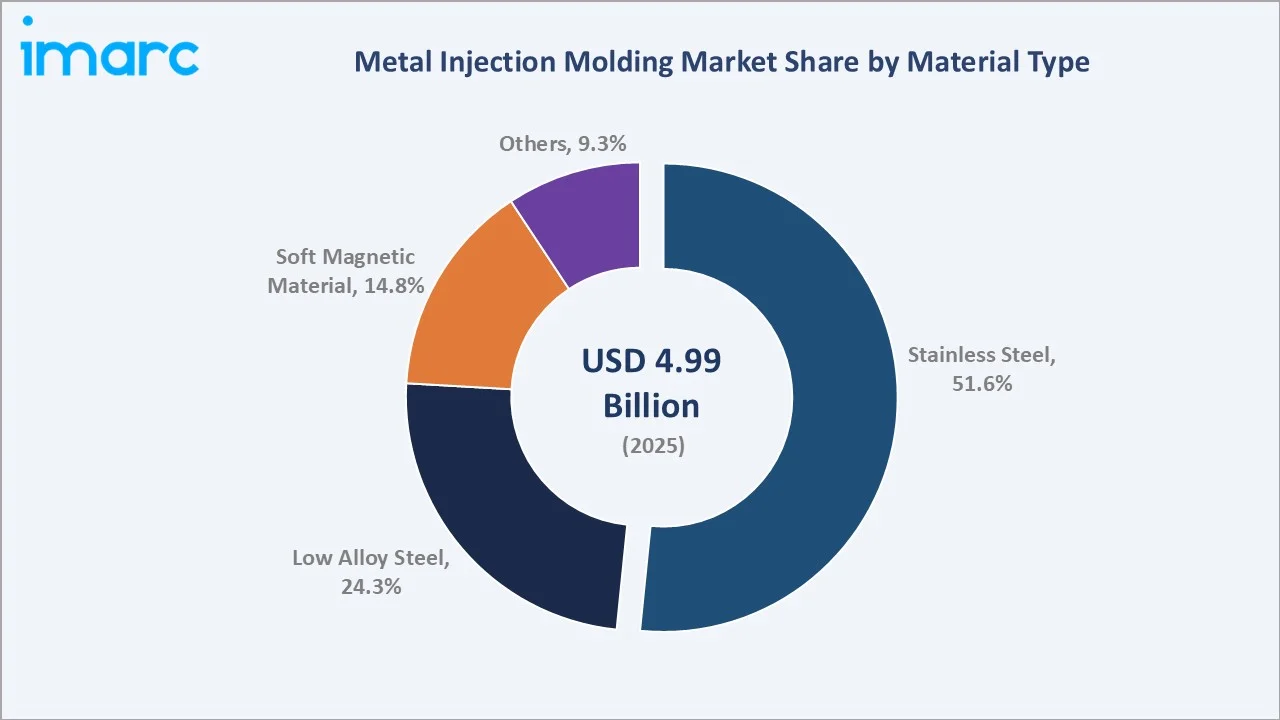

Consumer Products command 30.5% of total end-use share in 2025, reflecting surging demand for wearable device hardware, eyewear hinges, and precision consumer electronics. The Automotive segment holds 22.4%, propelled by lightweighting mandates and EV powertrain component sourcing. Medical and Orthodontics represents 14.3%, driven by growing adoption of MIM for surgical instruments, implant components, and orthodontic brackets. Among materials, Stainless Steel dominates at 51.6% owing to its superior corrosion resistance and FDA compliance for medical applications.

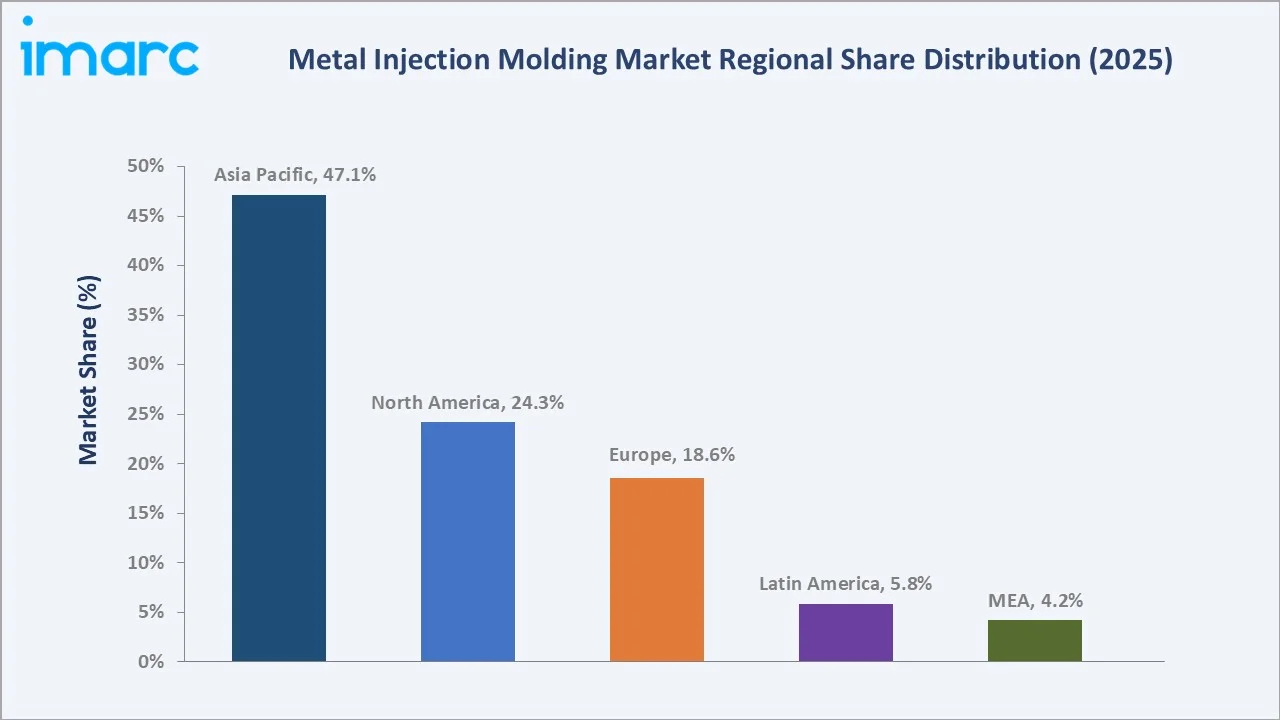

Asia Pacific leads global revenue with a 47.1% share in 2025, anchored by China's expansive manufacturing base and South Korea's electronics supply chain. North America holds 24.3% and Europe 18.6%. The metal injection molding market outlook remains positive as smart manufacturing adoption, additive-MIM hybrid techniques, and increasing defense procurement converge across all major regions through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest End Use Industry |

Consumer Products – 30.5% share (2025) |

|

Second End Use Industry |

Automotive – 22.4% share (2025) |

|

Largest Material Type |

Stainless Steel – 51.6% share (2025) |

|

Fastest Growing Material Type |

Soft Magnetic Material – ~9.1% CAGR (2026-2034) |

|

Leading Region |

Asia Pacific – 47.1% revenue share (2025) |

|

Top Companies |

GKN Powder Metallurgy, Amphenol Corporation, ATW Companies, CMG Technologies, Dean Group International, Ernst REINER GmbH & Co. KG, Parmaco Metal Injection Molding AG, Smith Metal Products, Tanfel Metal |

|

Market Opportunity (2025-2034) |

USD 4.83 Billion incremental revenue pool |

Key Analytical Observations Supporting The Above Data:

- Consumer Products' 30.5% dominance in 2025 reflects surging demand for precision wearable components, smartphone hardware, eyewear hinges, and luxury goods closures manufactured via the MIM process.

- Stainless Steel's 51.6% material share is driven by its corrosion resistance, high mechanical strength, and FDA compliance, making it the preferred substrate for medical-grade, food-contact, and outdoor-use MIM parts.

- The Soft Magnetic Material sub-segment is the fastest-growing material category at ~9.1% CAGR (2026-2034), fueled by expanding EV motor component demand and miniaturized electromagnetic actuator applications.

- Asia Pacific's 47.1% global dominance reflects China's role as the world's largest MIM production hub, supported by extensive powder metallurgy infrastructure, low-cost skilled labor, and proximity to electronics OEMs.

- The Medical and Orthodontics segment (14.3%, 2025) is gaining momentum as minimally invasive surgical instrument demand rises globally, supported by aging demographics in North America, Europe, and Japan.

- The global MIM market is projected to add USD 4.81 Billion in incremental revenue between 2025 and 2034, creating substantial investment opportunities across feedstock, debinding technology, and sintering equipment.

Global Metal Injection Molding Market Overview

Metal injection molding (MIM) is an advanced powder metallurgy manufacturing process that combines the geometric freedom of plastic injection molding with the material performance of metal. The process involves blending fine metal powders with a thermoplastic binder, injecting the mixture into a mold, removing the binder (debinding), and sintering to near-full density.

The global MIM ecosystem spans upstream metal powder suppliers, feedstock compounders, MIM contract manufacturers, post-processing specialists, and OEM end users across medical, automotive, consumer electronics, and defense sectors. The market's growth is supported by macroeconomic drivers including industrialization in emerging markets, rising defense expenditure, and the global transition to electric vehicles – all of which require precision metal components at high volumes and tight tolerances.

Market Dynamics

To evaluate market opportunities, Request Sample

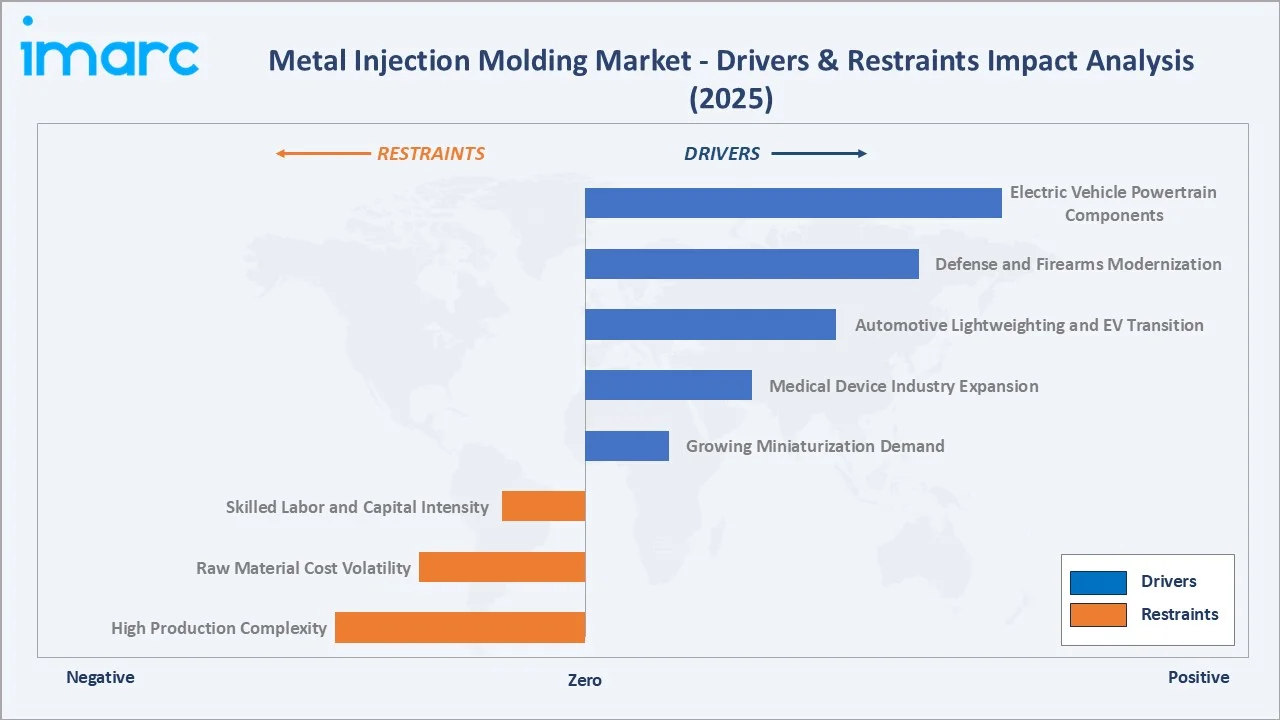

Market Drivers

- Growing Miniaturization Demand: The global trend toward smaller, lighter, and more complex hardware – particularly in consumer electronics, wearables, and IoT devices – is accelerating MIM adoption. Devices such as smartwatches, wireless earbuds, and endoscopic instruments increasingly rely on MIM for components with complex geometries.

- Medical Device Industry Expansion: The global medical device market exceeded USD 595 Billion in 2024. Growing demand for surgical tools, orthodontic brackets, bone anchors, and drug delivery components manufactured to ISO 13485 standards is sustaining double-digit MIM adoption growth within the healthcare vertical.

- Automotive Lightweighting and EV Transition: Automakers face mounting pressure to reduce vehicle weight and enhance electric powertrain efficiency. MIM enables production of complex gearbox components, fuel system parts, and EV motor actuators at densities approaching forged metal, while offering significant design freedom over conventional machining.

- Defense and Firearms Modernization: Global defense budgets exceeded USD 2.63 Trillion in 2025, with modernization programs driving procurement of precision weapon components. MIM's ability to produce high-volume, tight-tolerance firearm parts – including triggers, sears, and magazine catches – at lower per-unit cost than CNC machining is increasing defense-sector adoption.

Market Restraints

- High Production Complexity: MIM requires precisely controlled feedstock formulation, multi-stage thermal debinding, and high temperature sintering above 1,200°C. Process variability during any stage can lead to dimensional non-conformance, warpage, or porosity defects, resulting in elevated scrap rates and quality costs, particularly for new market entrants.

- Raw Material Cost Volatility: Fine metal powders including carbonyl iron, gas-atomized stainless steel, and nickel alloys – are energy-intensive to produce and remain sensitive to commodity price cycles. Powder represents a significant share of MIM feedstock costs, leading to margin pressure during periods of base metal price escalation.

- Skilled Labor and Capital Intensity: MIM operations require specialized metallurgical expertise, precision mold tooling, and capital-intensive sintering furnaces, creating significant barriers to entry and limiting capacity expansion, particularly in lower-income manufacturing regions.

Market Opportunities

- Electric Vehicle Powertrain Components: EV adoption is forecast to represent over 40% of global vehicle sales by 2030. MIM is well-positioned to supply high-volume powertrain components including shift fork assemblies, solenoid actuators, and thermal management hardware for electric drivetrains across major automotive OEM supply chains.

- Medical Robotics and Minimally Invasive Surgery: The global surgical robot market is forecast to exceed USD 25.47 Billion by 2030, creating sustained demand for small, high-precision MIM components for robotic surgical instruments, trocar systems, and laparoscopic tool heads that require biocompatibility and complex geometries.

- Smart Manufacturing and Industry 4.0 Integration: Deployment of AI-driven process monitoring, digital twin simulation for mold filling, and automated sintering control is reducing defect rates and enabling faster new product introduction. Early MIM adopters integrating smart factory systems are achieving reductions in scrap rates and improved dimensional consistency.

Market Challenges

- Competition from Additive Manufacturing: Metal 3D printing technologies, including selective laser melting and binder jetting, are emerging as competitive alternatives for low-to-mid volume complex metal parts. While MIM retains cost advantages at higher production volumes, additive manufacturing’s growing throughput and falling system prices represent a longer-term competitive threat.

- Stringent Regulatory Compliance: Medical and aerospace applications require extensive material certification, traceability documentation, and process validation under ISO 13485, AS9100, and FDA 21 CFR regulations, adding time and cost to market entry and increasing the compliance burden for smaller MIM contract manufacturers.

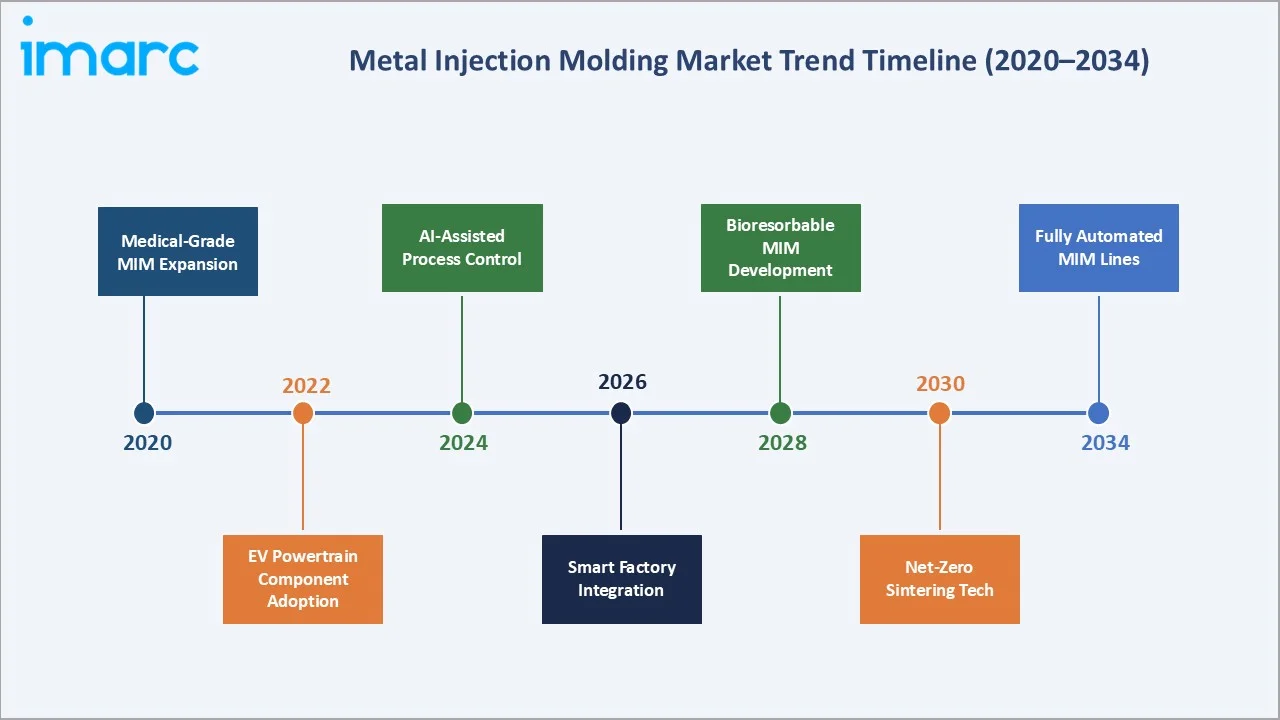

Emerging Market Trends

1. EV Powertrain Component Adoption

Electric vehicle production exceeded 17.3 million units globally in 2024 and is projected to surpass 40 million by 2030. MIM manufacturers are increasingly developing EV-specific material grades, including soft magnetic composites for motor applications, positioning the technology as a critical enabler of electric mobility component supply chains.

2. Medical-Grade MIM and Bioresorbable Material Innovation

The medical MIM sub-market is projected to grow at approximately 8.8% CAGR through 2034. Innovation in bioresorbable metallic alloys, including magnesium-zinc and iron-manganese systems processable via MIM, is opening new applications in temporary bone fixation implants that eliminate the need for secondary removal surgeries.

3. AI-Assisted Process Control and Smart Sintering

Leading MIM manufacturers are integrating machine learning algorithms into sintering furnace control systems, enabling real-time adjustment of thermal profiles based on batch composition and atmospheric conditions. Early deployments have demonstrated reductions in energy consumption per sintered batch and measurable improvements in dimensional consistency across high-volume production runs.

4. Hybrid Additive-MIM Manufacturing

A growing number of MIM specialists are adopting binder jetting additive manufacturing as a complementary technology for low-volume, highly complex geometries before scaling to traditional MIM for volume production. This hybrid approach reduces tooling investment during product development, accelerates time-to-market, and improves design validation cycles.

5. Sustainability and Circular Feedstock Initiatives

Environmental pressures are driving MIM producers to develop closed-loop feedstock recycling systems that reclaim rejected green parts and recycle sintering debind waste. Producers adopting recycled powder blends report raw material cost reductions while meeting emerging ESG procurement criteria from automotive and medical OEM customers.

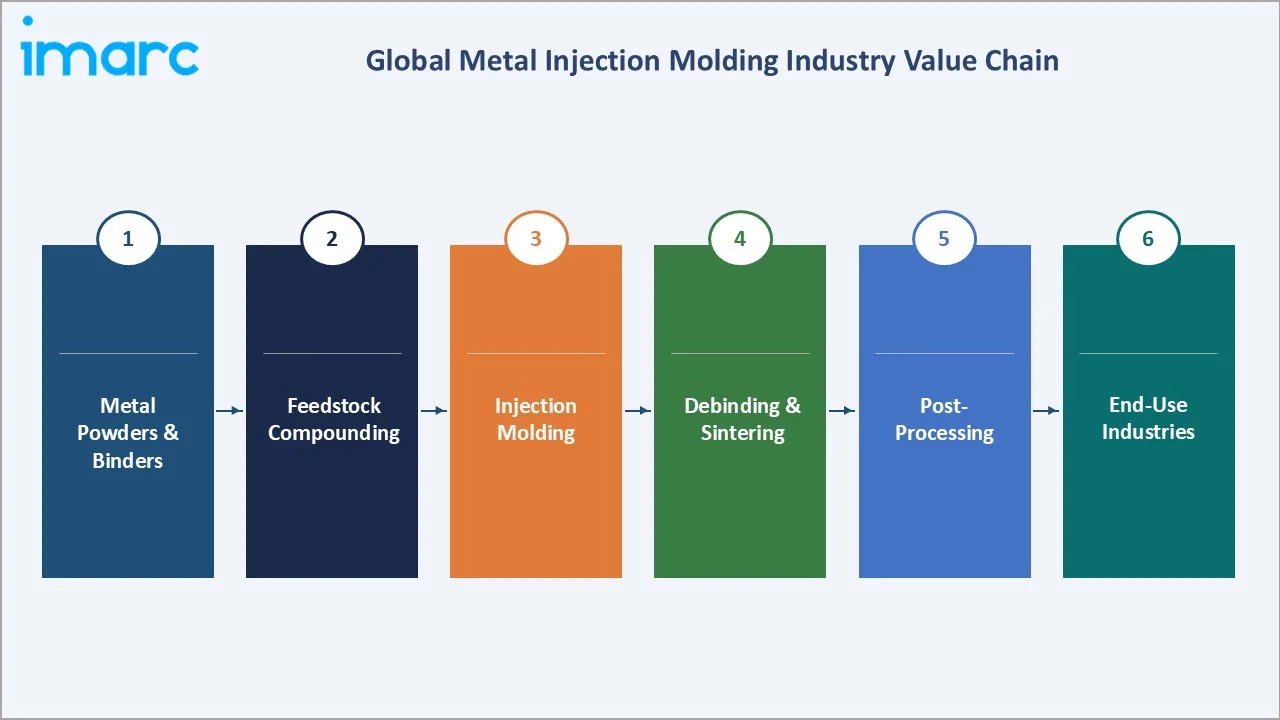

Industry Value Chain Analysis

The global MIM industry value chain spans six integrated stages from raw material supply through end-consumer delivery. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements relevant to the overall metal injection molding market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Carbonyl iron powder, gas-atomized stainless steel, nickel alloys, tungsten carbide, and titanium powders supplied by producers including Höganäs, and Sandvik AB |

|

Feedstock Production |

Powder-binder compounding using wax-based, polyacetal, or catalytic binder systems. Specialized feedstock suppliers include BASF and PolyMIM GmbH |

|

MIM Manufacturing |

Injection molding of green parts in high-precision steel tooling; thermal, solvent, or catalytic debinding; sintering in controlled-atmosphere furnaces above 1,200°C. |

|

Post-Processing |

CNC finishing, heat treatment, surface coating (PVD, electroplating), non-destructive testing, dimensional inspection, and clean-room assembly for medical/aerospace parts. |

|

Distribution |

Direct OEM supply agreements (dominant in automotive/medical), distributor networks for aftermarket/industrial channels, and e-commerce for standard component catalogs. |

|

End Users |

Consumer product brands, automotive OEMs, medical device manufacturers, defense contractors, electronics companies, and industrial equipment producers. |

MIM contract manufacturers hold the highest strategic value by integrating feedstock expertise, precision tooling, and process know-how into turnkey component supply. OEMs increasingly prefer qualified MIM suppliers with integrated post-processing and quality system certifications to simplify their supply chains.

Technology Landscape in the Metal Injection Molding Industry

Feedstock and Binder Innovation

Catalytic debinding systems are gaining share over traditional thermal wax systems, reducing debinding cycle times and enabling higher green part strength. Water-soluble binder systems are under active development, targeting reduced VOC emissions and lower energy consumption during the debinding stage.

Smart Sintering and Furnace Control

Continuous sintering furnaces with AI-assisted atmosphere control are replacing batch systems in high-volume MIM operations, improving energy efficiency per cycle. Vacuum sintering at controlled partial pressure is becoming standard for stainless steel and titanium alloy parts requiring high densities of theoretical maximum.

Digital Twin and Simulation

Mold flow simulation software (Moldflow, Sigmasoft) is now routinely applied during MIM tooling design to optimize gate placement, predict weld lines, and minimize residual stress in complex geometries. Digital twin models are being extended to sintering furnace loading, enabling virtual optimization of batch density and thermal uniformity before physical trials.

Additive-MIM Hybrid Manufacturing

Binder jetting additive manufacturing of metal parts uses the same powder-binder-sinter sequence as traditional MIM, enabling tool-free prototyping and low-volume production. Hybrid workflows that share MIM infrastructure are being commercialized, reducing capital requirements for design validation before high-volume production transitions.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Material Type |

Stainless Steel |

51.6% |

2025 |

|

End Use Industry |

Consumer Products |

30.5% |

2025 |

|

Region |

Asia Pacific |

47.1% |

2025 |

By End Use Industry

To access detailed market analysis, Request Sample

Consumer Products leads the global metal injection molding market by end use with a 30.5% share in 2025. Demand is driven by precision hardware for wearable electronics, luxury goods closures, eyewear hinges, and smartphone components requiring MIM's ability to produce complex shapes at high volumes with consistent dimensional accuracy.

By Material Type

Stainless Steel dominates the global MIM market by material type with a 51.6% share in 2025. Its dominance stems from excellent corrosion resistance, biocompatibility for medical-grade applications, and FDA compliance. 316L and 17-4PH stainless steel grades are the most widely specified MIM materials across medical, consumer, and industrial segments.

Regional Market Insights

The global metal injection molding market exhibits distinct regional growth profiles, driven by varying end-use sector maturity, manufacturing infrastructure, and regulatory environments.

|

Region |

2025 Share |

Key Growth Drivers |

|

Asia Pacific |

47.1% |

China electronics, EV supply chain, South Korea tech |

|

North America |

24.3% |

Defense spending, medical device innovation, automotive |

|

Europe |

18.6% |

German automotive OEMs, precision engineering, medical |

|

Latin America |

5.8% |

Brazil automotive sector, industrial equipment growth |

|

Middle East & Africa |

4.2% |

Defense procurement, GCC industrialization programs |

Asia Pacific

Asia Pacific commands 47.1% of global metal injection molding revenue in 2025. China is the region's dominant force, hosting the world's largest concentration of MIM contract manufacturers serving consumer electronics OEMs including Apple, Samsung, and Xiaomi. South Korea's advanced electronics supply chain and Japan's precision industrial components sector further contribute to regional leadership. India is an emerging growth market, with government manufacturing incentives under PLI schemes attracting MIM capacity investment for medical and defense applications. The region is projected to grow at approximately 8.1% CAGR through 2034.

Competitive Landscape

The global metal injection molding market is moderately fragmented, with a mix of large-scale diversified industrial manufacturers, specialized MIM contract producers, and vertically integrated metal powder and feedstock suppliers. Competition is driven by process capability breadth, material portfolio, quality system certifications (ISO 13485, AS9100, IATF 16949), and geographic proximity to end-use OEMs.

|

Company Name |

Brand / Division |

Market Position |

Key Strength |

|

GKN Powder Metallurgy |

GKN Sinter Metals / GKN Hoeganaes |

Leader |

Vertically integrated |

|

Amphenol Corporation |

Amphenol MCP |

Leader |

Electronics connectivity |

|

ATW Companies |

Parmatech |

Challenger |

Firearms components |

|

CMG Technologies |

CMG Technologies |

Emerging |

UK defence & medical |

|

Dean Group International |

Dean Group International |

Emerging |

European aerospace focus |

|

Ernst REINER GmbH & Co. KG |

REINER MIM |

Emerging |

German precision engineering |

|

Parmaco Metal Injection Molding AG |

Parmaco MIM |

Emerging |

Swiss watch & medical |

|

Smith Metal Products |

Smith Metal Products |

Emerging |

North America consumer |

|

Tanfel Metal |

Tanfel |

Emerging |

Custom MIM components |

Key Company Profiles

GKN Powder Metallurgy

GKN Powder Metallurgy is one of the world's leading manufacturers of metal powder components, including sintered parts and metal injection molded components. GKN Powder Metallurgy operates production facilities across North America, Europe, and Asia Pacific, serving the automotive, electrical, and industrial sectors.

- Product Portfolio: The company's MIM product portfolio includes precision automotive drivetrain components, complex sintered structural parts, and metal powder feedstocks.

- Recent Developments: In 2022, GKN Powder Metallurgy announced its entry into the EV permanent magnet market, leveraging its metal powder expertise and sintering capabilities. The move aligns with rising demand for localized, stable supply chains in electric mobility and highlights the company’s expansion beyond traditional MIM components into advanced powder-based applications, strengthening its positioning in the broader Global Metal Injection Molding ecosystem.

- Strategic Focus: GKN Powder Metallurgy's strategic focus centers on automotive electrification, lightweight component innovation, and sustainable manufacturing. The company is actively pursuing ISO 14001 environmental certification across its global manufacturing network and targeting net-zero sintering operations by 2035.

Amphenol Corporation

Amphenol Corporation is a global leader in interconnect systems and sensor solutions, with a significant MIM manufacturing capability serving its electronic connector and sensor housing production. Headquartered in Wallingford, Connecticut, USA. Amphenol’s continued expansion across EVs, data centers, and advanced electronics is indirectly supporting demand for MIM components in next-generation interconnect applications.

- Product Portfolio: Amphenol utilizes MIM technology to produce high-precision metal connector housings, shielding components, and sensor bodies for telecommunications, defense, aerospace, and consumer electronics applications.

- Recent Developments: In 2024, Amphenol Corporation continues to expand through an aggressive acquisition strategy, strengthening its position in connectors and advanced interconnect solutions. This growth supports rising demand across automotive, industrial, and electronics sectors, indirectly driving opportunities for precision components manufactured using Metal Injection Molding (MIM), particularly in high-performance connector and miniaturized part applications.

- Strategic Focus: Amphenol's strategic focus emphasizes vertical integration, geographic diversification, and technology leadership in precision metal manufacturing. The company leverages MIM as a key process technology to maintain competitive cost positions and achieve the tight tolerances demanded by next-generation electronic connector standards.

ATW Companies

ATW Companies is a leading North American metal injection molding manufacturer specializing in high-volume firearm components, consumer products, and industrial hardware. The company operates dedicated MIM production facilities in the United States, serving commercial firearms OEMs and consumer goods brands.

- Product Portfolio: ATW's MIM product range focuses heavily on firearms components including triggers, hammers, sears, and magazine releases manufactured from low alloy and stainless steel grades. The company also produces consumer product hardware for sporting goods, tools, and industrial equipment applications.

- Recent Developments: In 2021, Parmatech Corporation, part of ATW Companies, received a Powder Metallurgy Design Excellence Award from Metal Powder Industries Federation for a 3D-printed stainless steel golf putter component developed for Cobra Puma Golf. The achievement highlights the growing role of additive manufacturing alongside MIM in producing complex, high-performance metal components.

- Strategic Focus: ATW Companies' strategic direction emphasizes volume leadership in the North American firearms component MIM market while expanding into adjacent consumer and industrial hardware segments. Cost optimization through high-volume production efficiency and automation investment defines the company's competitive positioning.

Market Concentration Analysis

The global metal injection molding market exhibits a moderately fragmented competitive structure. The top five players – GKN Powder Metallurgy, Amphenol Corporation, ATW Companies, CMG Technologies– collectively account for an estimated 35-42% of global market revenue in 2025.

Market fragmentation is driven by the technology's process-specific nature, where quality system certifications (ISO 13485 for medical, IATF 16949 for automotive, AS9100 for aerospace), geographic proximity to OEM customers, and material specialization create distinct competitive niches. No single player commands a dominant global position, creating a competitive landscape characterized by regional leaders and application-specific specialists.

Consolidation activity is expected to increase through 2034 as larger industrial manufacturers seek to acquire MIM capabilities to serve OEM customers demanding integrated component supply. The trend toward supplier base reduction by automotive and medical OEMs is incentivizing scale-up through mergers and acquisitions. Cross-border MIM acquisitions by Asian manufacturers targeting North American and European market access represent a growing consolidation vector.

Investment & Growth Opportunities

Fastest Growing Segments

- Soft Magnetic Material MIM: The fastest-growing material segment at ~9.1% CAGR (2026-2034), driven by EV motor actuators, solenoid valves, and electromagnetic shielding applications. Investment in soft magnetic MIM production capabilities is positioned to capture growing EV component supply chain spending.

- Medical and Orthodontics: Projected to grow at ~8.8% CAGR (2026-2034), supported by aging demographics, minimally invasive surgical technology adoption, and orthodontic treatment penetration in emerging markets. ISO 13485-certified MIM capacity commands premium pricing and long-term OEM supply agreements.

- Electrical and Electronics: 5G infrastructure rollout, IoT device proliferation, and data center expansion are generating sustained demand for precision MIM connector housings, shielding components, and antenna hardware, particularly in Asia Pacific and North America.

Emerging Market Opportunities

- India: Government manufacturing incentives under PLI (Production Linked Incentive) schemes are attracting MIM investment for defense component localization and medical device manufacturing. India's MIM market is estimated to grow at above 10% CAGR through 2030.

- Southeast Asia: Vietnam, Thailand, and Indonesia are emerging as MIM manufacturing hubs as electronics OEMs diversify supply chains away from China. Regional MIM capacity investment is growing to serve consumer electronics and automotive component demand.

- Middle East: Saudi Vision 2030's defense localization target of 50% by 2030 represents a multi-billion dollar opportunity for precision metal component manufacturing, including MIM-produced firearm and defense system components.

Investment Trends

Private equity investment in MIM has accelerated, with multiple platform acquisitions consolidating regional MIM specialists in North America and Europe since 2022. Venture capital is flowing into additive-MIM hybrid technology startups. Strategic investors from Asia – particularly Chinese and South Korean powder metallurgy conglomerates – are seeking acquisition targets in European and North American MIM to gain access to technology, certifications, and blue-chip OEM relationships.

Future Market Outlook (2026-2034)

The global metal injection molding market is projected to grow from USD 4.99 Billion in 2025 to USD 9.82 Billion by 2034, representing cumulative incremental revenue of approximately USD 4.83 Billion over the forecast period at a CAGR of 7.57%.

The medium-term outlook (2026-2030) will be shaped by EV powertrain MIM component ramp-up, medical device supply chain localization trends following post-COVID supply disruptions, and continued consumer electronics miniaturization driving small-component MIM adoption. The market is forecast to reach USD 7.19 Billion by 2030.

The long-term outlook (2031-2034) will be influenced by smart manufacturing maturity, widespread adoption of AI-assisted sintering control, and the commercialization of bioresorbable metallic MIM implant technology. Additive-MIM hybrid workflows are expected to become standard practice at leading contract manufacturers, improving new product introduction speed while maintaining the economics of high-volume MIM production.

Research Methodology

Primary Research

Primary research for this report included structured interviews and consultations with MIM industry executives, procurement managers, material scientists, and supply chain specialists across North America, Europe, and Asia Pacific. Insights were gathered through in-depth interviews (IDIs) with over 50 industry stakeholders including MIM contract manufacturers, OEM procurement teams, metal powder suppliers, and industry association representatives.

Secondary Research

Secondary research encompassed analysis of company annual reports, regulatory filings, industry association publications (MPIF, EPMA), trade journals (International Journal of Powder Metallurgy, PM&MIM magazine), patent databases, government trade statistics, and macroeconomic data from the IMF, World Bank, and national statistical agencies. Market sizing data draws on country-level industrial production statistics and trade flow analysis.

Forecasting Models

Market forecasts are developed using a combination of bottom-up demand modeling (aggregating end-use segment demand drivers) and top-down validation against overall manufacturing and industrial output growth trajectories. CAGR projections incorporate regression analysis against historical market data (2020-2025), key demand driver growth rates (EV production forecasts, medical device market growth, defense budget trends), and scenario analysis for technology disruption risks including additive manufacturing substitution.

Metal Injection Molding Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Material Types Covered | Stainless Steel, Low Alloy Steel, Soft Magnetic Material, Others |

| End Use Industries Covered | Electrical and Electronics, Automotive, Medical and Orthodontics, Consumer Products, Firearms and Defense, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | GKN Powder Metallurgy, Amphenol Corporation, ATW Companies, CMG Technologies, Dean Group International, Ernst REINER GmbH & Co. KG, Parmaco Metal Injection Molding AG, Smith Metal Products, Tanfel Metal, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the metal injection molding market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global metal injection molding market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the metal injection molding industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Metal Injection Molding Market Report

The global metal injection molding market was valued at USD 4.99 Billion in 2025 and is projected to reach USD 9.82 Billion by 2034, growing at a CAGR of 7.57%.

The metal injection molding market is expected to grow at a CAGR of 7.57% during the forecast period 2026-2034, driven by demand from automotive, medical, and consumer sectors.

Asia Pacific dominates with a 47.1% global revenue share in 2025, led by China's electronics and consumer goods manufacturing, South Korea's tech sector, and Japan's precision engineering industry.

Consumer Products leads with 30.5% share in 2025, driven by demand for precision wearable components, smartphone hardware, and luxury goods closures manufactured via MIM technology.

Stainless Steel is the dominant material with 51.6% market share in 2025, favored for its corrosion resistance, biocompatibility, and FDA compliance across medical and consumer applications.

Key drivers include growing miniaturization demand in consumer electronics, medical device industry expansion, automotive lightweighting for EVs, and defense modernization programs globally.

Leading companies include GKN Powder Metallurgy, Amphenol Corporation, ATW Companies, CMG Technologies, Dean Group International, Ernst REINER GmbH & Co. KG, Parmaco Metal Injection Molding AG, Smith Metal Products, and Tanfel Metal.

The global metal injection molding market is projected to reach USD 7.19 Billion by 2030, reflecting sustained mid-single to high-single-digit annual growth across all key end-use segments.

MIM offers significant cost advantages over CNC machining for high-volume production of complex, small metal parts, achieving near-net-shape geometries with high densities of theoretical maximum at lower per-unit cost in large-scale production.

Soft Magnetic Material is the fastest-growing material segment at approximately 9.1% CAGR (2026-2034), driven by electric vehicle motor actuators, solenoid components, and electromagnetic shielding applications.

Key challenges include high production complexity, raw material cost volatility for fine metal powders, competition from metal additive manufacturing for low-volume applications, and stringent regulatory compliance burdens for medical and aerospace applications.

China, the United States, Germany, Japan, and South Korea are the largest national markets for MIM, collectively accounting for a significant share of global market revenue based on their manufacturing scale and end-use sector depth.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)