Castor Oil Price Falls 1.9% in USA, 1.4% in Germany — Q1 2026 Update

29-Apr-2026

Summary:

Q1 2026 brought further softening to the global castor oil market. Every tracked region posted quarter-on-quarter declines as castor oil prices eased amid moderated downstream demand and ample import flows. Castor oil prices slipped between 1.0% and 1.9% quarter-on-quarter. Against this backdrop, the Israel–Iran–USA conflict continues to inject volatility into feedstock channels. Crude swung from around USD 70 per barrel before the conflict to peaks above USD 119 in March 2026, a shift that might reshape input costs.

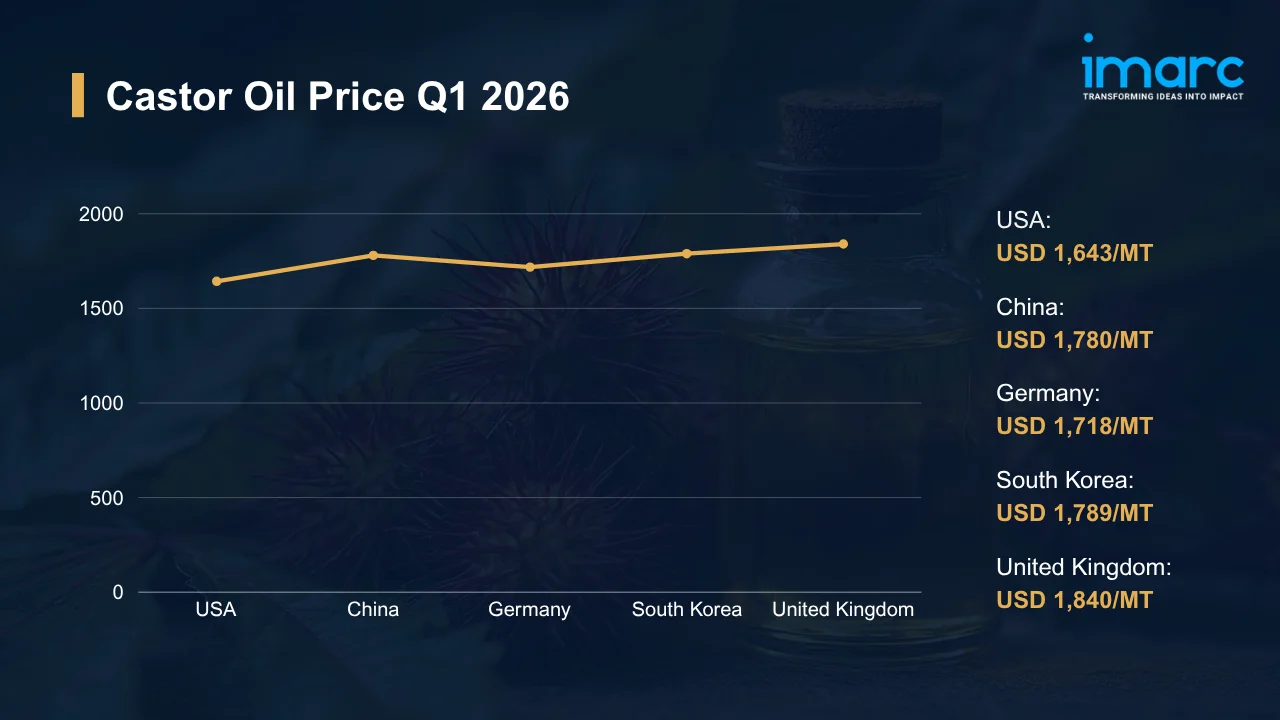

Castor Oil Price Q1 2026:

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| USA | 1,643 | -1.9% | ↓ Decline |

| China | 1,780 | -1.0% | ↓ Decline |

| Germany | 1,718 | -1.4% | ↓ Decline |

| South Korea | 1,789 | -1.2% | ↓ Decline |

| United Kingdom | 1,840 | -1.3% | ↓ Decline |

To access real-time prices Request Sample

Kindly note: IMARC's pricing database tracks castor oil price movements across major global markets.

What Moved Prices:

USA:

- During Q1 2026, castor oil prices in the USA slid to USD 1,643/MT, a 1.9% QoQ decline amid softer pull from bio-based chemical and lubricant manufacturers. Import arrivals from India remained ample through February and March, while domestic distributors held comfortable inventory positions that reduced any urgency around spot-market buying.

- The castor oil price chart for North America reflected a shallow downward drift sustained by steady Gulf Coast port throughput and orderly inland freight conditions. Specialty chemical and cosmetics buyers drew down existing stocks rather than chasing new contracts, keeping spot demand subdued. Cautious converter sentiment capped any attempt at near-term price recovery.

China:

- In Q1 2026, castor oil prices in China eased to USD 1,780/MT, down 1.0% QoQ as coatings, lubricants, and pharmaceutical processors trimmed procurement volumes. Consistent domestic crushing activity and stable seed imports from India kept regional supply comfortable. Buyers at Guangzhou and Yiwu trading hubs worked through accumulated inventory rather than replenishing.

- Softer export pull from Southeast Asian converters dampened upward momentum, while FMCG absorption within the domestic market held steady but lacked directional strength. Producers operating close to rated capacity absorbed some cost pressure internally rather than passing it through to customers. Spot negotiations favored buyers throughout the quarter.

Germany:

- During Q1 2026, castor oil prices in Germany trended to USD 1,718/MT, a 1.4% QoQ decline driven by subdued pull from the automotive lubricant and specialty chemicals base. Imports from Asian origins flowed consistently into Hamburg and Rotterdam feeder routes, and Rhine corridor logistics operated without material disruption, which supported comfortable inland distribution.

- Mittelstand converters, focused on working through existing stock, limited fresh commitments to short-tenor purchases. EU packaging sustainability mandates pushed some buyers toward longer-dated contracting only where sustainability certification was fully documented. Stable energy costs across the quarter further removed one potential source of upward pressure on delivered pricing.

South Korea:

- In the first quarter of 2026, castor oil prices in South Korea eased to USD 1,789/MT, a 1.2% QoQ decline as cosmetics and polymer producers aligned procurement with restrained end-user offtake. Import volumes through Busan held steady, and competitive pricing from Indian and Chinese suppliers weighed on domestic spot offers through the period.

- Export-oriented personal care manufacturers faced softer overseas demand, which muted their replenishment cadence for castor derivatives. Freight arrivals remained orderly despite broader Middle East routing pressures, since Korean importers source predominantly from India rather than Persian Gulf transit routes. Buyers negotiated from a position of stock comfort throughout.

United Kingdom:

- During Q1 2026, castor oil prices in the United Kingdom settled at USD 1,840/MT, down 1.3% QoQ as personal care and pharmaceutical manufacturers moderated their purchasing cadence. Import availability into Felixstowe and Southampton remained consistent, and sterling's moderate range against the US dollar limited FX-driven cost escalation at the quayside.

- Specialty chemical formulators favored short-dated contracts to preserve flexibility, reflecting ongoing caution across industrial buyers. Slower specialty chemical manufacturing activity further capped any attempt at a mid-quarter price recovery. Competitive distributor strategies across Europe reinforced the soft tone, with discounting visible on larger spot parcels.

Castor Oil Price Outlook After the Israel–Iran–USA Conflict:

Energy Cost Volatility and Castor Oil Feedstock Exposure: With Brent crude oil prices rising amid active hostilities, castor oil's delivered-cost structure faces mounting pressure from bunker surcharges, packaging costs, inland transport fuel premiums, and competing chemical feedstock economics. Import-reliant markets will feel the squeeze first. Should energy prices stay elevated, delivered castor oil costs might climb even as end-use demand leans soft.

Regional Price Volatility and Demand Uncertainty Across Castor Oil Markets: The castor oil price trend might diverge more sharply across regions if the conflict extends beyond Q2 2026, as import-reliant markets absorb shipping premiums unevenly. Buyers across Europe and East Asia face heightened uncertainty on delivered cost timing, while producers reassess inventory positioning. Consumption in cosmetics, lubricants, and pharmaceuticals could hold steady, though procurement teams will likely favor shorter-tenor contracts.

Immediate Market Reaction:

As hostilities unfold, the global castor oil market reacts primarily through its sensitivity to freight routing and feedstock competition rather than direct production exposure. India, the dominant supply origin, sits outside the immediate conflict zone, yet castor shipments share Middle East-adjacent shipping corridors. The castor oil price index signals near-term firmness risk if Strait of Hormuz disruptions widen bunker surcharges on Asia-Europe container routes. Buyers in Europe, the UK, and North America might front-load small volumes against contingencies, while East Asian processors lean on short-haul India-origin flows that remain comparatively insulated from Gulf routing pressures.

Impact on Castor Oil Prices:

The conflict might trigger several key changes in the castor oil market:

- Freight and Bunker Surcharge Pass-through: Rising bunker fuel costs and emergency carrier surcharges on Asia-to-Europe lanes will likely inflate delivered castor oil costs for European and UK buyers, even if origin prices at Gujarat ports hold steady. This pass-through might widen the FOB-versus-CIF spread meaningfully. Procurement teams negotiating Q2 contracts will need to price surcharge volatility into their cost models rather than assume freight stability.

- Feedstock Competition from Energy-Intensive Substitutes: Elevated petroleum prices could push industrial users to revisit bio-based castor derivatives as substitutes for petroleum-based lubricants and polymer intermediates. Increased substitution demand might offset softer current fundamentals, selectively lifting castor oil prices in specialty segments where sustainability positioning matters. Offsetting this, broader packaging and chemical end use demand will likely remain cautious while macro uncertainty persists, limiting the scale of any substitution-driven price lift.

- Supply Route Reconfiguration for Indian Exports: India's castor oil exports might reroute through alternative shipping corridors if Persian Gulf transit restrictions extend, adding cost and time to deliveries bound for European and North American buyers. Longer transit windows will lengthen inventory cycles at destination, requiring buyers to hold larger safety stocks. This structural shift might anchor a persistent delivered-cost premium even if the underlying price at origin remains moderate.

Taken together, these pressures will keep castor oil delivered costs under varying degrees of stress through mid-2026. Whether the end-to-end impact shows as meaningful price appreciation depends on conflict duration and freight normalization timing. Buyers might face sustained cost volatility even as origin-market fundamentals continue to lean soft, keeping hedging and contract flexibility relevant.

Supply Chain Disruptions:

Castor oil supply chains face concentrated exposure at the Persian Gulf transshipment layer, since the bulk of Indian-origin cargoes bound for Europe and the Americas transit adjacent to the conflict zone. Bunker surcharges, rerouting premiums, and extended vessel dwell times compound delivered-cost inflation. On March 2, 2026, very large crude carrier (VLCC) rates from the Middle East to China hit a record USD 423,736 per day, up more than 94% from the prior session, signaling magnitude of ongoing shipping stress.

Alternative routing options remain limited given the geographic concentration of castor production in western India. Producers might shift some volumes toward longer transit paths via the Cape of Good Hope, but the additional 10 to 14 days adds working capital burden and inventory carry costs. European and UK buyers will increasingly favor consolidated buying through fewer, larger contracts to amortize surcharge risk. Meanwhile, East Asian processors might lean harder on short-haul sourcing arrangements to reduce exposure to Gulf-transit volatility.

Global Market Overview:

Globally, the castor oil industry reached a volume of 812.14 Kilo Tons in 2025. Market projections indicate steady growth, with the industry expected to reach 890.97 Kilo Tons by 2034, with a compound annual growth rate (CAGR) of 1.03% during 2026-2034. Growth is underpinned by rising demand for bio-based lubricants, specialty chemicals, and personal care applications. Expanding pharmaceutical use, polymer substitution, and sustainability mandates across industrial coatings add further support. Evolving consumption patterns and regulatory shifts continue to shape the outlook.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In April 2026, Casterra Ag, a subsidiary of Evogene, reported successful commercial field trials in Brazil that validated mechanized castor cultivation at scale. The trials, carried out across varied growing conditions, confirmed cost efficiencies for growers while supporting castor's role as a feedstock for biofuel and bio-based industrial applications.

- In July 2025, Arkema launched the Castor Farmer Education Fund (CFEF) to reinforce sustainability across Indian castor cultivation. The fund scales up farmer training in climate-resilient, socially responsible practices and aims to reach up to 150,000 farmers by 2030, building on the existing Pragati program.

Castor Oil Price Forecast (2026):

Near-term castor oil prices will remain tethered to downstream industrial demand signals and conflict-driven freight dynamics through the first half of 2026. Cautious procurement behavior might persist across European and North American buyers, while Indian export pricing holds the origin baseline steady. Any easing of Gulf shipping pressures could open a window for delivered-cost stabilization.

If geopolitical hostilities intensify further, delivered castor oil prices will likely face upward pressure as bunker surcharges climb and Persian Gulf transit risk widens. Producers could absorb some of the cost internally, though sustained escalation might push quotations higher in import-reliant markets. Conversely, a meaningful de-escalation could ease freight premiums and restore orderly routing, allowing delivered costs to stabilize. These combined dynamics will continue to shape the castor oil price forecast through 2026.

Strategic Takeaways:

Looking ahead, the castor oil market is expected to navigate a mixed environment of moderated downstream demand, ample India-origin supply, and elevated freight cost volatility from Middle East conflict dynamics. Sustained buyer caution, evolving substitution dynamics, and shipping route recalibration will shape how delivered pricing resets across the coming quarters.

To navigate this complex landscape, stakeholders should:

- Monitor Regional Price Differentials: Track monthly and quarterly castor oil price movements across origin and destination markets to identify cost-arbitrage windows. Establish consistent benchmarking between FOB India and CIF European or North American landed costs for sharper sourcing decisions.

- Monitor Geopolitical Risk Exposure: Track escalation dynamics in the current conflict and assess how shifts in hostility levels might affect castor oil pricing, feedstock availability, and logistics costs. Establish internal alert thresholds that trigger timely procurement or hedging action.

- Diversify Supply Chain Routes: Evaluate alternative sourcing geographies and shipping corridors to reduce dependence on conflict-exposed trade lanes. Secondary supplier agreements and contingency freight arrangements will provide critical resilience if primary routes face sudden disruption or extended rerouting delays.

- Adjust Procurement Strategy for Conflict Conditions: Adopt flexible contract structures with price reopener clauses and force majeure provisions to protect against geopolitical price spikes. Precautionary inventory buffers might reduce exposure if supply tightens abruptly during active hostilities or sudden shipping restrictions.

- Benchmark Castor Oil Price per MT Against Contract Rates: Compare prevailing spot castor oil price per MT against existing contract pricing to identify renegotiation opportunities. Regular benchmarking enables procurement teams to lock in favorable terms during softening cycles and avoid overpaying during short-lived spikes.

- Evaluate Feedstock Substitution Dynamics: Assess castor oil's competitive position against petroleum-based alternatives in lubricants, polymers, and specialty chemicals. Shifts in relative cost economics might create specialty segment opportunities where bio-based sourcing commands sustainability-driven pricing premiums over the coming quarters.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates — 12 deliverables/year

- Quarterly Updates — 4 deliverables/year

- Biannual Updates — 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)