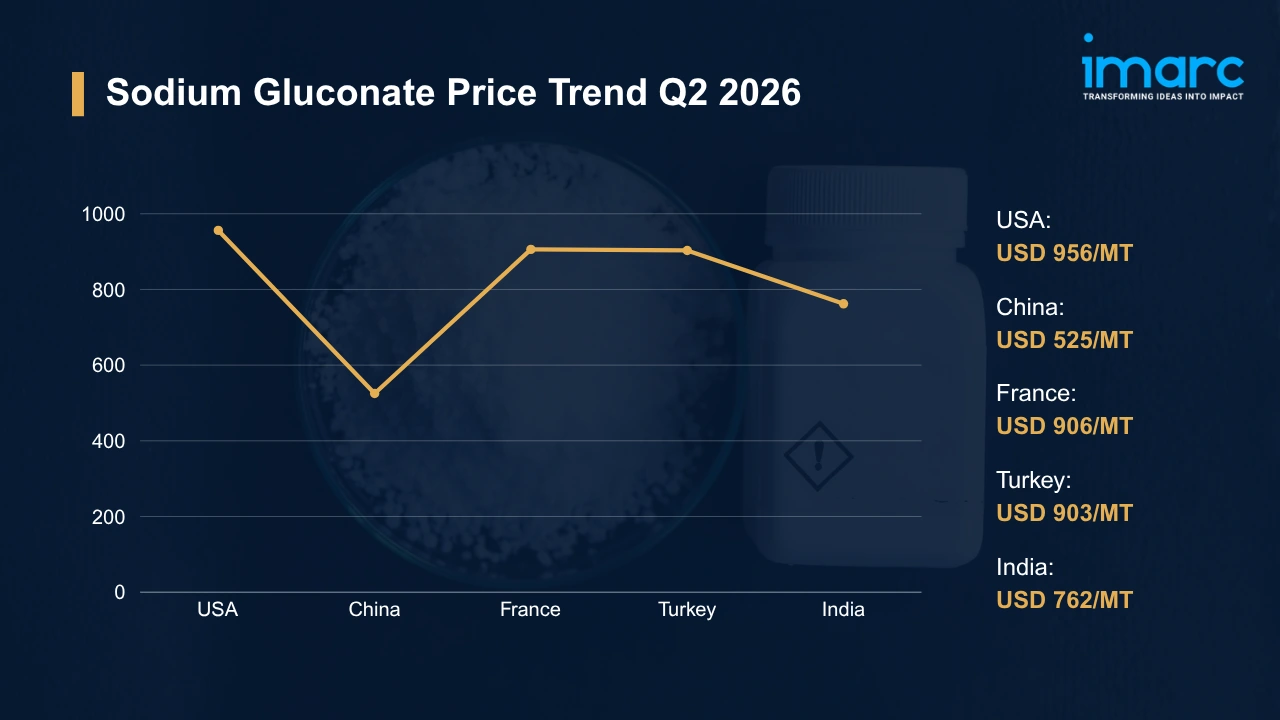

Detergent Alcohol Price Falls 3.5% in Germany, 3.0% in China — Q1 2026 Update

07-May-2026

Summary:

Q1 2026 split the global detergent alcohol market three ways down and two ways up, with import-driven supply pressure trumping demand recovery across most tracked regions while industrial cleaning offtake stayed soft through the quarter. Quarter-on-quarter, detergent alcohol prices ranged from a 3.5% decline to a 2.9% gain, leaving feedstock economics and regional consumption strength as the primary swing factors. Brent crude settled up 6.08% to USD 118.03 per barrel in late April 2026, sharpening input outlooks.

Detergent Alcohol Price Q1 2026:

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| USA | 2214 | +2.9% | ↑ Growth |

| China | 2201 | -3.0% | ↓ Decline |

| Germany | 2569 | -3.5% | ↓ Decline |

| Singapore | 2532 | -2.9% | ↓ Decline |

| Saudi Arabia | 3116 | +1.9% | ↑ Growth |

To access real-time prices Request Sample

Kindly note: IMARC's pricing database tracks detergent alcohol price movements across major global markets.

What Moved Prices:

USA:

- During Q1 2026, USA detergent alcohol prices climbed to USD 2214/MT, supported by steady FMCG offtake from home care and personal care converters operating across Gulf Coast and Midwest plants. Domestic feedstock economics remained largely stable, offering limited cost-side volatility. Fatty alcohol availability and ethylene supply remained within expected ranges, with producers maintaining disciplined output aligned with actual order flow.

- Across the surfactant segment, the detergent alcohol price chart traced a measured upward path through March, helped by consistent end user offtake. Asian import flows arrived at competitive but not aggressive levels. Inland freight stayed steady through the quarter, and buyers held near-term cover without rushing forward purchases.

China:

- In Q1 2026, China detergent alcohol prices eased to USD 2201/MT as ample supply met cooler demand from surfactant and cleaning product makers. Domestic plants kept run rates flat. Export demand showed only limited growth, and comfortable inventory positions across Yiwu and Guangzhou discouraged urgent restocking.

- Throughout the period, oleochemical producers across Northeast Asia operated at restrained run rates, while Southeast Asian import offers stayed available at competitive landed costs. Port freight conditions held steady throughout. Procurement teams negotiated from a position of strength, securing favorable terms on contract renewals into Q2.

Germany:

- During Q1 2026, detergent alcohol prices in Germany retreated to USD 2569/MT, the steepest decline among tracked markets. Demand stayed conspicuously thin through Q1. Balanced supply met subdued offtake from industrial cleaning and personal care formulators, while uninterrupted import availability removed any scarcity premium from spot quotations.

- Within the Mittelstand converter base, purchasing patterns stayed conservative as cautious consumer spending tempered downstream order books. EU sustainability mandates kept reshaping formulation choices but failed to lift volume. Asian CIF offers were assessed below prevailing domestic quotes, thereby eroding the limited pricing power retained by local producers over the course of the quarter.

Singapore:

- In the first quarter of 2026, detergent alcohol prices in Singapore eased to USD 2532/MT, pressured by ample supply and lukewarm pull from regional manufacturing. Production stayed flat across Jurong Island. Export activity showed limited expansion, and balanced inventories kept the trading hub from absorbing any supply tightness.

- Stable feedstock costs and even-keeled freight rates blocked any cost-push lift on offer levels. Southeast Asian buyers stayed selective, leaning on FOB pricing rather than forward commitments. Across regional warehouses, distributors trimmed exposure to a market without clear growth signals, slowing inventory turnover into late March.

Saudi Arabia:

- During Q1 2026, detergent alcohol prices in Saudi Arabia advanced to USD 3116/MT, lifted by firm Gulf demand and tight producer discipline at Jubail. Feedstock supply conditions remained stable throughout the quarter, with no significant disruptions observed. Consumption from cleaning and industrial brands held firm across the GCC, reinforcing upward momentum into the quarter-end.

- Heavy export pull from African and South Asian buyers tightened domestic availability through the quarter, with shipment volumes building steadily into March. Producers kept operating rates disciplined throughout. Buyers absorbed higher offers with limited resistance, given how few substitution options exist within the Gulf petrochemical complex.

Detergent Alcohol Price Outlook After the Israel–Iran–USA Conflict:

Rising Energy Costs and Feedstock Cost Pressure for Detergent Alcohol: Conflict-driven energy disruption is rippling through ethylene and fatty alcohol supply chains, lifting input cost exposure for detergent alcohol producers. Freight markets are signaling acute pressure. CNBC noted benchmark rates for Very Large Crude Carriers (VLCCs) hauling Middle East crude to Asia hit a record USD 423,736/day in early March 2026, a 94% jump from the prior session that might cascade into petrochemical feedstock costs.

Regional Demand Volatility and Cross-Border Pricing Uncertainty for Detergent Alcohol: Across consuming regions, the detergent alcohol price trend over the coming quarters might diverge sharply with the conflict's path. Forward-buying behavior is shifting fast across regions. Asian converters may accelerate cover to lock in supply while European buyers pull back on procurement to protect margins, leaving regional spreads to widen as logistics costs and currency moves reset landed economics.

Immediate Market Reaction:

The detergent alcohol market is moving in tight, defensive postures as Persian Gulf trade routes face disruption. Producers are rewriting shipment schedules while buyers track Strait of Hormuz transits hour by hour. For Middle Eastern shippers, exposure is direct. Cargoes routed to Asian and African destinations may need re-routing via Cape of Good Hope, adding roughly two weeks of transit time and a stack of war-risk surcharges that few buyers expected. Across Asian processors handling palm kernel oil and ethylene streams, delivery slippage is becoming routine. The detergent alcohol price index will likely widen between conflict-exposed origins and other hubs.

Impact on Detergent Alcohol Prices:

The conflict might trigger several key changes in the detergent alcohol market:

- Feedstock Cost Inflation: Energy-driven volatility in petrochemical feedstock chains might push ethylene and fatty alcohol input costs higher across producing regions. Margin pressure builds quickly across the chain. Manufacturers reliant on Middle East-linked petrochemical feedstocks could face compression, particularly in Asia where olefin pricing tracks crude movements closely, and pass-through to end-buyers will hinge on contract structures, competitive intensity within each downstream segment, and how fast FMCG converters absorb sustained increases.

- Supply Chain Re-routing: Strait of Hormuz disruption might force palm kernel oil and oleochemical cargoes bound for Europe onto longer Cape of Good Hope routes, adding fuel and insurance overheads at every shipment leg. Schedules will stretch by ten to fourteen days. Higher carrier surcharges will lift landed costs for European converters, while Indonesian and Malaysian producers might pivot toward shorter Asian and African destinations to preserve margin efficiency.

- Demand Pattern Shifts: Persistent geopolitical uncertainty might push detergent alcohol buyers to build precautionary inventory buffers, lifting near-term spot demand while pulling forward consumption from later quarters of 2026. Demand patterns are flipping fast across regions. Cleaning and personal care brands will likely accelerate forward purchases through Q3 to insulate production schedules from further escalation, while industrial cleaning end users might curtail volume commitments as macroeconomic confidence wavers across energy-intensive economies.

Together, these pressures might push detergent alcohol prices into a sustained upward trajectory through Q3 2026 if hostilities persist. Volatility will rule the next two quarters. Buyers caught between feedstock cost inflation and demand uncertainty will pivot toward longer-term supply contracts and hedging instruments to manage exposure into the second half.

Supply Chain Disruptions:

Detergent alcohol supply chains lean heavily on Strait of Hormuz transit for Middle Eastern petrochemical feedstocks and on Southeast Asian palm kernel oil shipments routed through the same chokepoint. That exposure runs deep across processors. Even short-lived disruptions at this transit point can quickly cascade into shipment delays, extended lead times, and tighter near-term availability across dependent markets.

Producers might pursue alternative sourcing as the disruption persists, with Asian and African buyers locking in inventory from Indonesian and Malaysian palm kernel oil suppliers to bypass Middle Eastern transit. Across the basin, risk premiums are widening fast. European converters reliant on Asian-routed shipments will see inventory tighten and price-reopener clauses activate. For large detergent alcohol producers, cost escalation might accelerate vertical integration talks aimed at chokepoint insulation. Across every major hub, logistics teams recalibrate routes weekly.

Global Market Overview:

Globally, the detergent alcohol industry was valued at USD 8.55 Billion in 2025. Market projections indicate steady growth, with the industry expected to reach USD 13.22 Billion by 2034, with a compound annual growth rate (CAGR) of 4.96% during 2026-2034. Across global markets, demand from household and industrial cleaning product manufacturers anchors volume growth, while rising hygiene awareness and accelerating urbanization across emerging economies widen consumption pools beyond traditional consumer segments. Bio-based and sustainable formulations might capture rising market share.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In January 2025, CNOOC and Shell Petrochemicals Company Limited (CSPC), a joint venture between Shell Nanhai B.V. and CNOOC Petrochemicals Investment Ltd, finalized investment plans for an expansion of its petrochemical complex in Daya Bay, Huizhou, in southern China. The broadening added a third ethylene cracker with planned annual output of 1.6 Million Tons of ethylene, a critical building block for linear alpha olefins used in detergent alcohol manufacturing.

Detergent Alcohol Price Forecast (2026):

Detergent alcohol prices will stay volatile through mid-2026. Conflict-driven feedstock movements and shifting downstream demand patterns might keep procurement teams in defensive postures, while any easing of geopolitical risk could open a window for price stabilization as supply chains gradually normalize across major trading hubs. Caution will persist among industrial cleaning and personal care buyers.

If geopolitical hostilities intensify further, detergent alcohol prices will likely face renewed upward pressure as energy and logistics costs climb, with risk premiums widening across trade routes and producer margins compressing through the second half of 2026. Producers in conflict-exposed zones might curtail output. Conversely, a diplomatic resolution might ease freight rates and restore feedstock supply flows. Together, these dynamics will continue shaping the detergent alcohol price forecast throughout the year ahead.

Strategic Takeaways:

Looking ahead, the detergent alcohol market is expected to navigate persistent geopolitical risk, feedstock volatility, and uneven regional demand recovery through 2026. Strategic procurement decisions will hinge on the conflict trajectory, energy market stability, and how fast substitute formulations gain ground across cleaning and personal care end uses around the world.

To navigate this complex landscape, stakeholders should:

- Monitor Geopolitical Risk Exposure: Track escalation dynamics in the current conflict and assess how shifts in hostility levels might affect detergent alcohol pricing, feedstock availability, and logistics costs. Establish internal alert thresholds that trigger rapid procurement or hedging action.

- Diversify Supply Chain Routes: Evaluate alternative sourcing geographies and shipping corridors to reduce dependence on conflict-exposed trade lanes. Secondary supplier agreements and pre-arranged contingency freight options will provide critical resilience if primary detergent alcohol supply routes face sustained disruption.

- Adjust Procurement Strategy for Conflict Conditions: Adopt flexible contract structures with price reopener clauses and force majeure provisions to protect against geopolitical price spikes. Precautionary inventory buffers and dual-sourcing arrangements might reduce exposure if detergent alcohol supply tightens abruptly across markets.

- Track Regional Price Differentials Monthly: Monitor the detergent alcohol price per MT across the USA, China, Germany, Singapore, and Saudi Arabia each month to identify cost-saving procurement windows. Build benchmark dashboards that flag widening regional spreads early for opportunistic sourcing decisions.

- Evaluate Feedstock Cost Pass-Through Mechanisms: Assess how palm kernel oil, ethylene, and fatty alcohol cost movements transmit into detergent alcohol pricing across each major producing region. Negotiate index-linked contracts that align supplier and buyer exposure to upstream feedstock volatility cycles.

- Monitor Sustainability Regulatory Shifts: Track evolving EU, US, and Asia Pacific regulations on bio-based and biodegradable detergent formulations to anticipate compliance-driven cost shifts. Engage early with regulators and industry associations to shape favorable transition timelines for portfolio reformulation strategy.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates — 12 deliverables/year

- Quarterly Updates — 4 deliverables/year

- Biannual Updates — 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)