Global Itaconic Acid Prices in Q1 2026: Germany Hits USD 1,862/MT as Regional Market Trends Shape Pricing Outlook

19-Jun-2026

Itaconic acid is a white, crystalline organic compound synthesized through microbial fermentation of sugars, valued for its bifunctional monomer structure containing two carboxylic groups and one reactive carbon-carbon double bond. Itaconic acid prices are shaped by corn feedstock procurement costs, fermentation energy intensity, and outbound freight rates on major export corridors out of China, where most global production is concentrated. Downstream consumption spans specialty polymers, superabsorbent materials, coatings, adhesives, synthetic resins, textile auxiliaries, and detergent formulations, with demand cycles across these sectors translating directly into quarterly price movement patterns.

Global Market Overview:

Globally, the itaconic acid industry was valued at USD 122.1 Million in 2025. Market projections indicate steady growth, with the industry expected to reach USD 174.5 Million by 2034, with a compound annual growth rate (CAGR) of 4.04% during 2026-2034. Bio-based polymer adoption and specialty resin diversification sustain the itaconic acid price trend across forecast years, with construction chemical applications and superabsorbent material development adding incremental demand layers that reinforce the long-term volume base.

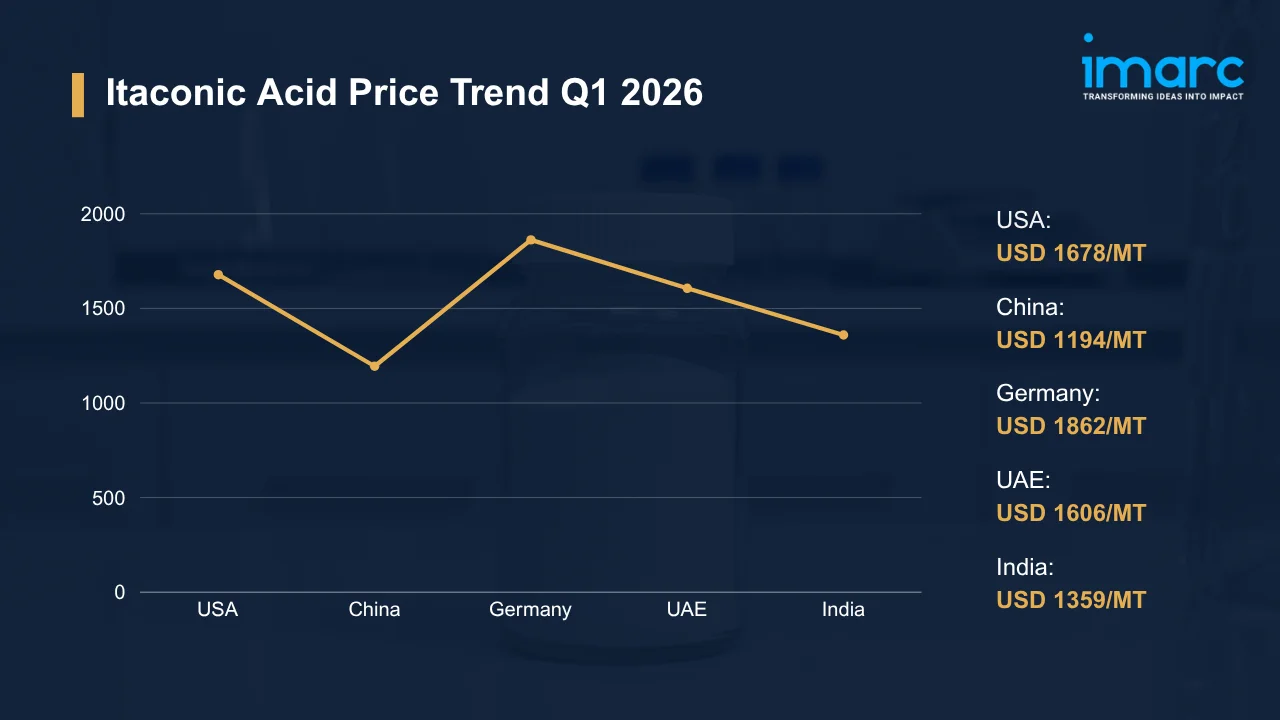

Itaconic Acid Price Trend Q1 2026:

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| USA | 1,678 | +13.09% | ↑ |

| China | 1,194 | +4.45% | ↑ |

| Germany | 1,862 | -1.34% | ↓ |

| UAE | 1,606 | +3.44% | ↑ |

| India | 1,359 | +3.11% | ↑ |

To access real-time prices Request Sample

What Moved Prices:

USA:

- In Q1 2026, itaconic acid prices in the USA surged to USD 1,678/MT, a 13.09% QoQ advance driven by post-holiday procurement recovery across coatings and adhesives manufacturing. Buyers who had deferred restocking through Q4 2025 re-entered the spot market, lifting transaction volumes and tightening available inventory at distribution hubs within the quarter.

- Firmer corn feedstock acquisition costs at domestic fermentation plants lifted supplier cost floors, feeding through to offer levels for both contract and spot buyers. The itaconic acid price chart traced an upward slope across all three months of the quarter, reinforced by tighter Asian export availability that constrained the import alternative channel buyers typically rely on to cap domestic supplier pricing.

China:

- During Q1 2026, itaconic acid prices in China rose to USD 1,194/MT, gaining 4.45% QoQ as post-Lunar New Year restocking drew down spot inventories accumulated during the subdued Q4 2025 demand period. Procurement from polymer modification and adhesive manufacturers across domestic consumption centers picked up from late January onward, shifting the supply-demand balance toward tighter conditions.

- Fermentation output at major Chinese production hubs held steady, but rising export bookings absorbed incremental domestic production, leaving less material for spot market allocation. Coatings producers in Guangzhou and Yiwu sourcing hubs stepped up purchasing as downstream order books recovered, and CNY exchange rate stability during the period supported competitive pricing on export-oriented volumes without meaningful margin compression.

Germany:

- In the first quarter of 2026, itaconic acid prices in Germany fell to USD 1,862/MT, retreating 1.34% against the prior quarter. Coatings additive and specialty polymer processors remained in inventory drawdown mode rather than initiating fresh procurement, as downstream industrial order flows across the German manufacturing sector lacked the momentum needed to justify volume buying at prevailing supplier offer levels.

- Asian-origin import material, competitive on both quality and landed cost after freight rate moderation on the Asia-Europe corridor, narrowed the pricing premium that domestic distributors had historically sustained. Regional chemical plant energy costs normalized relative to 2024 peaks, removing the cost-floor justification that had supported higher price floors in prior quarters and leaving buyers well-positioned to resist supplier uplift attempts.

UAE:

- In Q1 2026, itaconic acid prices in the UAE climbed to USD 1,606/MT, rising 3.44% QoQ as construction chemical and industrial coatings procurement activity recovered following the Q4 2025 seasonal slowdown. Infrastructure project execution resumed across key UAE markets, translating into firm material requirements from construction additives formulators and coatings converters operating within the region.

- Pegged-currency stability kept landed cost projections predictable for import-reliant regional distributors sourcing from Asian suppliers. Throughput at Jebel Ali remained efficient, reducing port dwell surcharges that had intermittently added to landed costs in prior periods. Distributor restocking across UAE free-zone trading centers absorbed available import volumes, tightening domestic spot supply without a corresponding drawdown in buyer urgency.

India:

- During Q1 2026, itaconic acid prices in India advanced to USD 1,359/MT, a 3.11% QoQ gain reflecting fresh manufacturing demand from polymer and textile auxiliary producers following the inventory rebuilding that had already occurred through the Q4 2025 post-monsoon restocking cycle. Industrial clusters in Gujarat and Maharashtra drove the bulk of early-quarter procurement activity, with adhesives and coatings formulators increasing order frequencies against a recovering domestic order book.

- Import flows from Asian producers through Nhava Sheva and Chennai continued without material disruption, maintaining adequate product coverage across regional distribution networks. Buyers engaged in moderate forward procurement rather than spot-only sourcing, factoring in INR-USD exchange rate variability that introduced incremental landed cost uncertainty and led suppliers to embed a modest currency buffer into their Q1 offer structures.

Drivers Influencing the Market:

Several factors continue to shape itaconic acid pricing and market behavior:

- Specialty Polymer and Sustainable Materials Demand: Bio-based chemical building block adoption across the specialty resin, superabsorbent polymer, and biodegradable plastic sectors generates consistent baseline procurement volumes for itaconic acid. Formulators substituting petroleum-derived monomers with fermentation-sourced alternatives broaden the commodity's addressable application base quarter by quarter. Urbanization-led construction chemical growth and bio-polymer mandates in regulated export markets reinforce consumption without significant cyclical volatility.

- Upstream Corn Feedstock Cost Dynamics: Corn is the primary fermentation substrate underpinning itaconic acid production economics, so agricultural commodity price swings pass through directly into manufacturing cost structures. The itaconic acid price index across key producing regions correlates closely with corn procurement costs, which typically constitute the single largest variable in per-unit fermentation economics.

- Energy Expenditure in Fermentation Processing: Fermentation cycles for itaconic acid are energy-intensive, requiring sustained temperature regulation and continuous aeration throughout multi-day production runs. Natural gas and electricity costs at Chinese manufacturing sites carry disproportionate weight in global cost-of-production benchmarks, given China's concentration of fermentation capacity. Structurally higher energy input costs at European production facilities sustain a persistent cost-floor differential between Asian-origin and domestically manufactured material across importing regions.

- Ocean Freight and Logistics Economics: Container shipping rate movements on Asia-to-Europe and Asia-to-North America corridors feed directly into itaconic acid landed costs, given China's dominant position in global export supply. Drewry's World Container Index recorded USD 2,182 per 40ft container for the week of December 18, 2025, extending a streak of consecutive weekly gains on Transpacific and Asia-Europe trade routes. Procurement teams embed prevailing spot freight levels into import cost models, and sustained rate shifts cascade into quarterly contract price reviews across all major import markets.

- Environmental and Regulatory Compliance: Periodic environmental inspection campaigns at Chinese fermentation facilities curtail operating rates during affected windows, compressing export availability without warning and tightening spot supply to import-dependent markets. Registration and evaluation obligations under EU chemical safety frameworks add compliance cost layers for distributors and industrial users across European member states. Supply-side curtailments from regulatory activity typically register as short-duration price inflection points when demand from downstream sectors remains intact.

- Trade Policy and Currency Dynamics: Import tariff structures in major consuming markets, combined with currency volatility in India, Brazil, and Turkey, create procurement cost variability for buyers reliant on import channels. Exchange rate shifts against the US dollar alter the effective local-currency cost of contracted volumes, influencing buyer preferences between spot and forward purchasing commitments. Antidumping reviews and tariff renegotiations can realign supplier market share across regional trade flows with minimal lead time, disrupting established sourcing relationships.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In November 2025, researchers advanced the application of itaconic acid in polymer science by engineering two novel methacrylate-functionalized monomers that resolved persistent limitations in polymer conversion efficiency and molecular weight control. Using reversible deactivation radical polymerization techniques, the work produced well-defined polymers with near-complete conversion and tunable thermal characteristics, demonstrating a viable pathway for integrating bio-renewable itaconic acid into advanced structural polymer applications.

Outlook & Strategic Takeaways:

Looking ahead, the itaconic acid market is expected to sustain gradual volume and value expansion through 2034, underpinned by bio-based polymer adoption, specialty resin application diversification, and construction chemical consumption growth across emerging market economies. Corn feedstock cost trajectories and fermentation energy pricing at Chinese production facilities represent the primary variables that will govern the itaconic acid price forecast and supplier margin dynamics across the medium-term planning horizon.

To navigate this complex landscape, stakeholders should:

- Monitor Regional Price Differentials: Track quarterly pricing variations across the USA, Germany, China, UAE, and India to identify cost-optimized procurement windows. Establish benchmarking protocols that compare landed costs against prevailing contract rates so sourcing decisions are grounded in current market data.

- Assess Freight Market Developments: Monitor container shipping rate movements on Asia-Europe and Asia-North America corridors to project changes in itaconic acid landed costs. Negotiate logistics contracts with rate adjustment provisions linked to recognized freight benchmarks, reducing exposure to unbudgeted cost escalation.

- Evaluate Downstream Demand Indicators: Track specialty polymer output rates, bio-based materials adoption curves, and coatings sector order books across primary consumption markets. Benchmarking itaconic acid price per MT against regional contract averages each quarter supports inventory positioning and prevents overstocking during seasonal demand troughs.

- Review Regulatory Compliance Expenditures: Audit costs tied to chemical handling, environmental discharge obligations, and registration requirements across all operating jurisdictions. Identify workflow efficiencies that reduce the regulatory compliance burden without compromising fermentation product safety standards or legal obligations.

- Strengthen Currency Exposure Management: Deploy hedging instruments for procurement volumes denominated in volatile currencies to stabilize landed cost projections across quarterly purchasing cycles. Align treasury coverage timelines with anticipated import payment schedules to avoid unprotected foreign exchange exposure during periods of rapid rate movement.

- Explore Emerging Application Segments: Investigate commercial potential in bio-based adhesive formulations, superabsorbent polymer innovations, and pharmaceutical intermediate uses to diversify demand commitments and reduce reliance on cyclical end-use sectors. Collaborate with research partners to assess scalability and cost-competitiveness of novel itaconic acid derivatives currently in development-stage pipelines.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates — 12 deliverables/year

- Quarterly Updates — 4 deliverables/year

- Biannual Updates — 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)