Global Phosphorus Pentachloride Prices in Q1 2026: Netherlands Reaches USD 1,276/MT Amid Strong European Demand

25-Jun-2026

Phosphorus pentachloride is a white crystalline solid, exhibiting strong reactivity with moisture to yield phosphorus oxychloride and hydrogen chloride. Phosphorus pentachloride prices are driven by demand from agrochemical synthesis, pharmaceutical intermediates, and specialty chemical manufacturing, where the compound serves as a chlorinating agent in producing organophosphorus pesticides, plasticizers, and active pharmaceutical ingredients (APIs). Upstream elemental phosphorus and chlorine feedstock costs, energy expenditure in industrial chlorination processes, ocean freight economics on key trade lanes, and demand cycles within agriculture and pharmaceutical production collectively govern pricing sensitivity.

Global Market Overview:

Globally, the phosphorus pentachloride industry reached a volume of 807.44 Thousand Tons in 2025. Market projections indicate steady growth, with the industry expected to reach a volume of 1,026.90 Thousand Tons by 2034, with a compound annual growth rate (CAGR) of 2.71% during 2026-2034. Agrochemical output expansion across Asia and the Americas, rising pharmaceutical API production, and growing use in battery electrolyte precursors together underpin the phosphorus pentachloride price trend over the medium term. Tightening environmental compliance requirements are simultaneously reshaping supplier economics in producing regions.

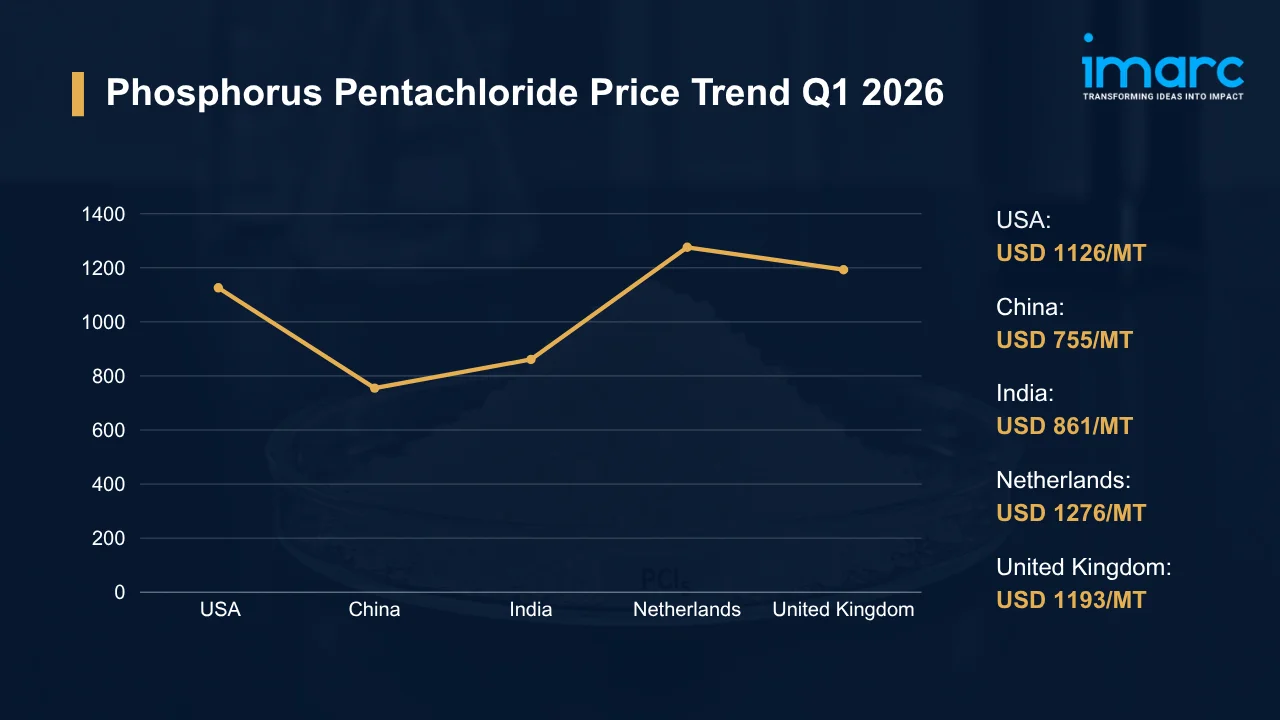

Phosphorus Pentachloride Price Trend Q1 2026:

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| USA | 1,126 | +5.80% | ↑ |

| China | 755 | +2.33% | ↑ |

| India | 861 | +1.90% | ↑ |

| Netherlands | 1,276 | +2.11% | ↑ |

| United Kingdom | 1,193 | +1.80% | ↑ |

To access real-time prices Request Sample

What Moved Prices:

USA:

- In Q1 2026, phosphorus pentachloride prices in the USA climbed to USD 1,126/MT, a 5.80% QoQ advance driven by firm procurement from pharmaceutical and agrochemical manufacturers. Chemical distributors facing tighter inventories accelerated contract nominations as domestic production capacity operated at elevated utilization rates throughout the quarter.

- Hazardous-material compliance checks at Gulf Coast facilities created supply constraints, cutting spot availability and amplifying landed cost pressure for buyers reliant on domestic sourcing. Across the quarter, the phosphorus pentachloride price chart traced a consistent upward arc, reinforced by higher energy input costs and constrained feedstock flows from upstream chlor-alkali operations.

China:

- During Q1 2026, phosphorus pentachloride prices in China rose to USD 755/MT, up 2.33% QoQ, as domestic demand from agrochemical converters and glyphosate producers maintained steady absorption. Seasonal restocking ahead of the spring planting season tightened near-term availability across key distribution channels in Guangzhou and Shandong production clusters.

- Intermittent output curtailments at provincial facilities under environmental compliance inspections reduced the buffer stock cushion available to spot buyers. Adding to this pressure, export inquiries from Southeast Asian and South Asian customers kept domestic producer offers firm, even as baseline production capacity remained broadly adequate entering the period.

India:

- In Q1 2026, phosphorus pentachloride prices in India advanced to USD 861/MT, a 1.90% QoQ gain, supported by rising consumption from pharmaceutical API producers and fertilizer intermediate manufacturers. Port-level delays at Nhava Sheva and Mundra extended import clearance timelines, tightening spot availability for import-dependent buyers across western industrial zones.

- Raw material procurement costs for elemental phosphorus and chlorine gas rose incrementally, filtering through into producer offers and sustaining upward price momentum. Currency volatility layered additional landed cost unpredictability onto importer calculations, compelling buyers to accept modest contract price revisions in exchange for secured forward allocation through peak agrochemical production months.

Netherlands:

- In the first quarter of 2026, phosphorus pentachloride prices in the Netherlands reached USD 1,276/MT, rising 2.11% QoQ amid stable industrial demand from specialty chemical and fine-chemical processors. European producer adjustments to regulatory compliance costs for hazardous material storage and handling raised operational expenditure at distribution hubs serving the Benelux region.

- Buyers responded to extended lead times from Asian suppliers by shifting procurement toward regional European producers, accepting firmer terms to guarantee supply continuity. Downstream chemical manufacturers also pursued inventory optimization ahead of anticipated spring demand peaks, further tightening near-term product availability at Rotterdam and Amsterdam distribution points.

United Kingdom:

- Consistent industrial demand from pharmaceutical and specialty chemical converters absorbed available UK supply through Q1 2026, pushing phosphorus pentachloride prices to USD 1,193/MT, a 1.80% QoQ rise. Post-Brexit border compliance requirements on hazardous chemical consignments extended customs clearance times, compressing effective import availability in key industrial corridors.

- With regional production capacity concentrated among a small number of suppliers, price discipline on offer sheets held firm throughout the period. Rising inland freight charges and stricter packaging requirements for corrosive materials increased per-unit distribution costs, and producers progressively reflected these burdens in contract pricing discussions.

Drivers Influencing the Market:

Several factors continue to shape phosphorus pentachloride pricing and market behavior:

- Agrochemical and Pharmaceutical Sector Demand: Pesticide formulators, pharmaceutical API producers, and specialty chemical converters collectively provide the foundational volume base for phosphorus pentachloride consumption globally. Rising API production pipelines across India and China further reinforce upstream procurement commitments from buyers.

- Upstream Elemental Phosphorus and Chlorine Feedstock Costs: White phosphorus mining output and chlorine availability from chlor-alkali facilities directly shape production economics for phosphorus pentachloride manufacturers. Supply disruptions at major phosphate rock mining sites, reinforced by periodic chlorine generation curtailments tied to power cost cycles, amplify feedstock cost volatility. Geographically concentrated elemental phosphorus supply introduces concentration risk, translating into unpredictable input cost movements throughout the production chain.

- Energy Expenditure in Industrial Chlorination: Natural gas and electricity costs are central determinants of manufacturing margin in phosphorus pentachloride production, given the energy intensity of chlorination reactions. Per the EIA, benchmark Henry Hub spot prices averaged USD 3.52 per Million Btu in 2025, a 56% increase from 2024 lows, directly pressuring cost structures for US-based chemical manufacturers. Tracking the phosphorus pentachloride price index against energy benchmarks reveals a consistent cost-pass-through pattern among producers, particularly when gas price spikes coincide with constrained downstream demand elasticity.

- Ocean Freight and Logistics Economics: Under IMDG regulations, hazardous chemical classification imposes additional documentation, packaging, and stowage costs on phosphorus pentachloride shipments, amplifying the freight cost component of landed prices. Container availability fluctuations on Asia-Europe and trans-Pacific corridors expose import-dependent buyers in the UK, Netherlands, and India to variable lead time risk. Port congestion at major chemical cargo hubs periodically compounds transit uncertainty, prompting buyers to hold precautionary buffer inventory that distorts spot market demand timing.

- Environmental and Regulatory Compliance: Classified as a highly corrosive and moisture-reactive hazardous substance under REACH in Europe and OSHA guidelines in the USA, phosphorus pentachloride generates ongoing compliance cost obligations across the value chain. Expanding chemical safety frameworks in India and Southeast Asia are progressively extending registration, storage protocol, and disposal requirements to regional participants. Facility permitting timelines for new production capacity have lengthened in several jurisdictions, constraining supply-side expansion and reducing the buffer available to absorb incremental demand growth.

- Trade Policy and Currency Dynamics: Evolving bilateral trade frameworks and import tariffs between the USA, China, and the EU reshape cross-border phosphorus pentachloride flows and widen regional price differentials. Currency depreciation in import-dependent markets, such as India, amplifies procurement costs for buyers relying on USD-denominated Asian supply. CNY exchange rate movements simultaneously shape competitive positioning for Chinese exporters. Procedural documentation requirements for hazardous chemical shipments under international conventions add cost layers that affect effective landed price calculations.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In June 2025, Anupam Rasayan India Ltd. signed a Letter of Intent with E-Lyte Innovations and Fuchs Lubricants Germany covering supply of up to 1,500 TPA of lithium hexafluorophosphate, a key lithium-ion battery electrolyte salt synthesized using phosphorus pentachloride as a primary raw material. The agreement highlights phosphorus pentachloride's expanding role as an upstream precursor in battery supply chains, signaling incremental demand from the EV sector.

Outlook & Strategic Takeaways:

Steady volumetric expansion is expected to characterize the phosphorus pentachloride market through 2034, driven by growing agrochemical consumption across Asia's agricultural economies, expanding pharmaceutical API pipelines, and emerging electrolyte precursor demand from the lithium-ion battery sector. Feedstock cost trajectories for elemental phosphorus and chlorine, alongside evolving REACH and OSHA compliance frameworks, will remain the pivotal variables shaping the phosphorus pentachloride price forecast across major producing and consuming regions.

To navigate this complex landscape, stakeholders should:

- Assess Freight Market Developments: IMDG-hazmat container shipping rate trends on Asia-Europe and trans-Pacific corridors warrant close tracking to anticipate landed cost movements. Flexible logistics contracts incorporating rate adjustment clauses tied to spot freight index movements will limit exposure to sudden freight market spikes on key trade lanes.

- Evaluate Downstream Demand Indicators: Agrochemical production output indices and pharmaceutical API dispatch data across major consuming markets provide reliable leading indicators for phosphorus pentachloride demand cycles. Procurement planning aligned with seasonal agricultural purchasing patterns reduces the risk of inventory shortfalls during peak spring and fall demand windows.

- Review Regulatory Compliance Expenditures: Current REACH, OSHA, and national-level hazardous chemical compliance costs across phosphorus pentachloride handling, storage, and waste disposal warrant periodic audit. Consolidated logistics solutions and process efficiencies can reduce regulatory burden without compromising chemical safety obligations across the supply chain.

- Strengthen Currency Exposure Management: Forward hedging strategies for USD-denominated phosphorus pentachloride procurement protect import-dependent markets facing INR, GBP, or EUR volatility from landed cost escalation. Treasury and procurement functions should be coordinated so that foreign exchange coverage schedules align with anticipated import payment timelines across quarterly purchasing cycles.

- Explore Emerging Application Segments: Lithium-ion battery electrolyte salt synthesis and advanced semiconductor doping applications represent meaningful demand growth avenues for phosphorus pentachloride portfolio diversification. Downstream R&D partnerships can help assess the commercial viability and volume scale of these segments before 2034 growth materializes at scale.

- Monitor Regional Price Differentials: Benchmark the phosphorus pentachloride price per MT quarterly across the USA, Netherlands, India, China, and UK to identify cost-saving procurement windows. Establish benchmarking protocols that compare landed costs against prevailing contract rates for optimal sourcing decisions.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates: 12 deliverables/year

- Quarterly Updates: 4 deliverables/year

- Biannual Updates: 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)