Iron Scrap Price Increases 4.5% in Germany, 2.2% in France — Q1 2026 Update

10-Apr-2026

Summary:

With gains in four of five tracked markets, Q1 2026 delivered a broadly firmer pricing outcome for iron scrap than the prior quarter. Iron scrap prices moved between a 4.5% decline and a 4.5% gain QoQ. Constrained by reduced demolition activity and tighter domestic collection across most markets, available supply stayed well below demand through the period. Brent crude surged approximately 55% in March 2026, marking a record monthly gain for the contract since its inception in 1988, a cost shock feeding directly into steelmaking energy and logistics budgets worldwide.

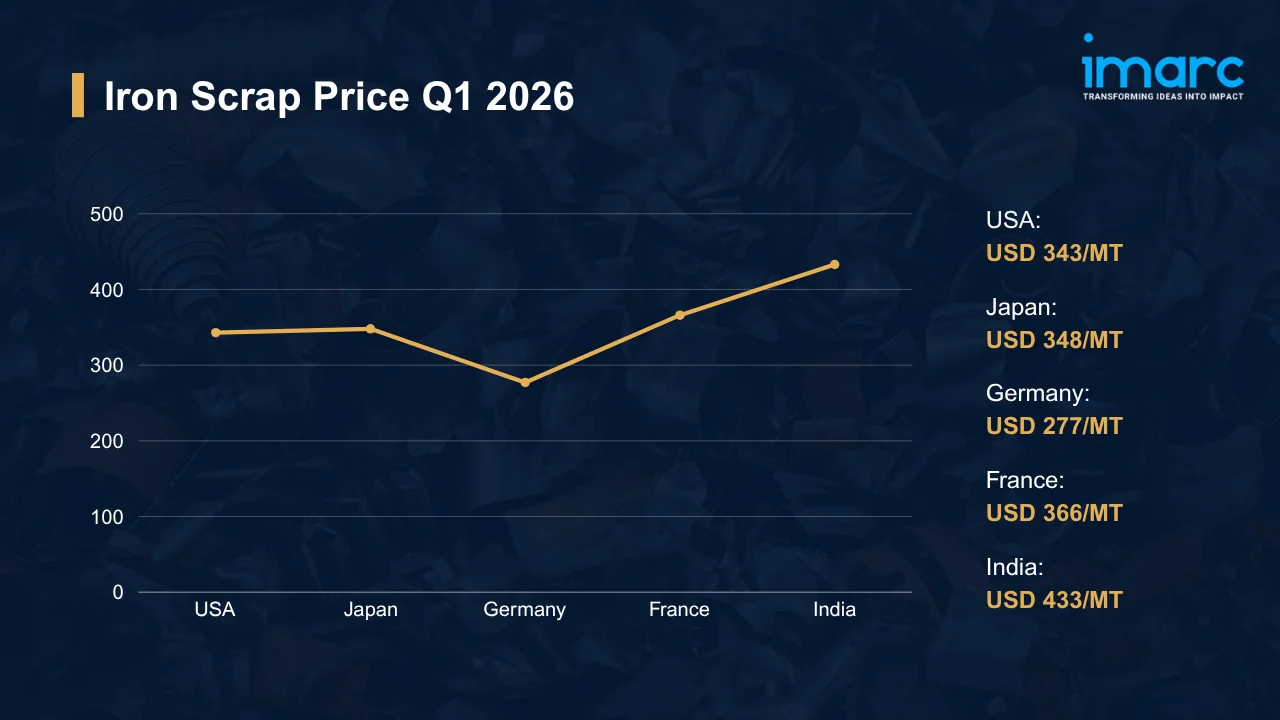

Iron Scrap Price Q1 2026:

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| USA | 343 | −4.5% | ↓ Decline |

| Japan | 348 | +1.2% | ↑ Growth |

| Germany | 277 | +4.5% | ↑ Growth |

| France | 366 | +2.2% | ↑ Growth |

| India | 433 | +1.2% | ↑ Growth |

To access real-time prices Request Sample

Kindly note: IMARC’s pricing database tracks iron scrap price movements across major global markets.

What Moved Prices:

USA:

- In Q1 2026, US iron scrap fell to USD 343/MT, a 4.5% QoQ decline. EAF operators pulled back procurement as downstream steel demand softened across structural and construction segments, leaving dealers with accumulating inventory and fewer incentives to hold offers firm through January and February. Buyers preferred drawing down existing stock rather than committing to new spot purchases.

- Adequate domestic supply gave buyers little urgency to chase the market. The iron scrap price chart for the USA showed a consistent retreat through Q1, with spot bids declining steadily from January through mid-March as export demand offered no compensating pull, inland logistics remained fully functional, and dealers eventually yielded to sustained buyer resistance across all major traded grades.

Japan:

- In Q1 2026, Japanese iron scrap advanced to USD 348/MT, a 1.2% QoQ gain. Absorbing available domestic volumes faster than collection could replenish them, Southeast Asian EAF demand tightened the local prompt pool steadily through the bulk of the quarter. Industrial scrap generation held below seasonal norms throughout.

- Currency tailwinds pulled additional Japanese-origin volumes into export channels, tightening the domestic supply picture. Combined with consistent EAF melt schedules sustaining procurement through the period, the export draw left local dealers navigating a thinner prompt market and, from mid-quarter onward, contending with war-risk surcharges that raised landed costs for buyers sourcing Japanese material via Gulf-adjacent routes. Procurement teams deepened engagement with tier-two domestic suppliers to hedge exposure.

Germany:

- During Q1 2026, German iron scrap climbed to USD 277/MT, a 4.5% QoQ increase. Prompt scrap generation dropped below seasonal norms as manufacturing output softened across key industrial segments. Driving further urgency, energy surcharges tied to the Middle East conflict accelerated mill procurement timelines and pushed buyers to lock in tonnages well ahead of expected Q2 cost increases.

- Neighboring European export inquiries further drained domestic availability, reinforcing the upward price trajectory through the period. Recyclers reported demolition-linked collection running well below seasonal benchmarks across processing centers. Despite maintaining steady melt schedules, German producers found the combination of tighter generation, cross-border export pull, and conflict-linked energy cost pressure too acute to absorb without repricing successive cargoes higher.

France:

- In Q1 2026, French iron scrap rose to USD 366/MT, up 2.2% QoQ. Firm mill melt schedules and below-seasonal demolition-linked collection kept the spot market structurally short through February and March, with export-oriented traders competing for the same limited prompt volumes and driving bids steadily higher across all major traded grades. A broadly positive iron scrap price trend across European markets held through quarter-end.

- Cross-border export demand prevented any meaningful accumulation of spot supply, stripping out the inventory buffer that had cushioned French market pricing in the prior quarter. Running efficiently throughout, scrap processing infrastructure nonetheless saw fuel-linked logistics cost increases feeding into processing margins from February onward. Buyers accelerated forward purchasing commitments through March to prioritize volume security over short-term price optimization.

India:

- During Q1 2026, Indian iron scrap reached USD 433/MT, up 1.2% QoQ. Active procurement from secondary steelmakers and rolling mills sustained demand across both imported and domestically collected material, while limited domestic availability pushed the market toward heavier reliance on seaborne imports through the period. Port congestion compressed delivery schedules and added to landed costs on imported cargoes.

- Freight disruptions tied to the Middle East conflict raised CIF costs for material transiting Gulf-adjacent routes, compressing scrap dealer margins on imported lots through the quarter. Steelmakers maintained healthy melt rates, ensuring continuous consumption across secondary rolling mills. Rather than engage the volatile spot market, most buyers locked into bilateral supply arrangements with established counterparties to cap freight-linked cost exposure.

Iron Scrap Price Outlook After the Israel–Iran–USA Conflict:

Rising Energy and Electricity Costs for Iron Scrap Operations: The ongoing conflict is driving sharp cost increases across energy-intensive iron scrap operations. Electric arc furnaces depend on electricity and fossil fuels, both facing severe disruption as the Strait of Hormuz closure continues. Tightening energy supplies might push electricity costs higher across key markets, potentially squeezing processing margins and lifting the delivered cost of iron scrap at trading desks worldwide.

Regional Price Volatility and Demand Uncertainty for Iron Scrap: Geopolitical uncertainty from the Israel–Iran–USA conflict is reshaping demand patterns for iron scrap across key consuming markets. Across Asia and Europe, buyers might reconsider procurement volumes as energy price volatility feeds through to downstream steel production economics and quarterly planning assumptions. The conflict disrupts the forecasting frameworks that scrap dealers and steel producers rely on when setting quarterly pricing commitments.

Immediate Market Reaction:

As the conflict unfolds, the iron scrap market is absorbing a wave of cost and logistical pressures that cut across supply routes, processing economics, and procurement behavior simultaneously. Supply corridors through the Strait of Hormuz, which carries a significant share of Asian-bound ferrous metal trade, now face acute disruption, tightening vessel availability and raising freight costs on key trade lanes connecting major scrap exporters to EAF operators across Asia. Against this backdrop, the iron scrap price index is under sustained upward pressure as conflict-driven energy cost volatility reshapes procurement decisions worldwide. Buyers might delay spot purchases pending clearer signals on freight normalization.

Impact on Iron Scrap Prices:

The conflict might trigger several key changes in the iron scrap market:

- Energy-Driven Processing Cost Escalation: At EAF operators and scrap processors across the supply chain, rising electricity and fuel costs are feeding through as the conflict disrupts global energy markets, with some European processors already imposing surcharges on processed grades. Soaring energy prices will increase the cost of melting, shredding, and processing iron scrap, potentially narrowing margins for secondary producers and forcing upward price adjustments at point-of-sale for traded grades.

- Freight Cost Pass-Through to Procurement Budgets: Rising war-risk insurance premiums and vessel rerouting surcharges will increase the delivered cost of iron scrap imported by buyers across Asia. These freight-driven cost increases might render previously competitive import offers unviable, shifting demand toward domestically collected material in markets such as India and Japan. Compression of price differentials between domestic and imported grades might then accelerate procurement strategy pivots across the region.

- Regional Demand Disruption and Inventory Repositioning: Uncertainty around conflict duration is already prompting procurement teams to reassess forward-buying commitments across key iron scrap consuming markets. Extending destocking cycles rather than committing to fresh spot volumes becomes the likely procurement response in markets most exposed to freight-linked cost volatility. This shift will create temporary demand softness even where underlying steel production fundamentals remain broadly supportive of scrap consumption.

Taken together, these dynamics might exert upward pressure on iron scrap prices in freight-exposed markets while simultaneously creating demand softness in others, producing a bifurcated pricing environment that complicates the planning horizon across all major scrap trade flows globally. The net outcome depends on how long the Hormuz disruption persists.

Supply Chain Disruptions:

Iron scrap supply chains face acute exposure to the Strait of Hormuz disruption, given the waterway’s critical role connecting scrap exporters in the Americas and Europe with import-dependent steelmakers across Asia that rely on seaborne material to fill domestic collection shortfalls. In early March 2026, shipping traffic through the Strait fell at least 80%, with freight costs on Gulf-adjacent routes already spiking sharply. Delivery timelines lengthen and CIF costs climb with each passing week.

Producers and traders are rerouting shipments around Africa’s Cape of Good Hope, a detour that adds weeks to transit times and measurably raises freight costs on each cargo cleared through alternative channels. Inventory buffers are draining across key import markets. Across South and Southeast Asia, secondary steel producers will face the most severe exposure given their considerable dependence on seaborne iron scrap imports to sustain melt schedules through the coming quarters.

Global Market Overview:

Globally, the iron scrap industry reached a volume of 628.6 Million Tons in 2025. Market projections indicate steady growth, with the industry expected to reach 827.6 Million Tons by 2034, with a compound annual growth rate (CAGR) of 3.10% during 2026-2034. Rising electric arc furnace steel production, increasing sustainability commitments, expanding global infrastructure investment, and the growing adoption of scrap-based steelmaking across emerging and developed economies are expected to sustain steady long-term demand for iron scrap through the forecast period.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In October 2025, JSW Steel unveiled plans to build a new scrap processing facility in Chennai, India, designed to recycle iron and steel scrap from end-of-life vehicles and other discarded products. The plant was designed to process and provide recycled iron scrap to JSW’s steel production units in Karnataka and Andhra Pradesh, reinforcing the company’s local supply chain and supporting circular economy objectives.

Iron Scrap Price Forecast (2026):

Conflict-driven energy cost volatility and freight market disruptions stemming from the Strait of Hormuz crisis will keep near-term iron scrap prices sensitive to rapid, potentially severe shifts in procurement economics. Procurement caution will persist into Q2 2026. Any escalation in electricity or diesel costs might push processed scrap prices above current offer levels in key consuming markets well before mid-year.

Escalation will drive iron scrap costs sharply higher across import-exposed markets. With energy and freight premiums climbing in parallel, import-dependent buying economics would become increasingly unworkable, potentially causing steelmakers across Asia and Europe to curtail output and tighten the global supply balance faster than alternative procurement routes could compensate. De-escalation offers the other path, potentially easing freight conditions and allowing prices to normalize, a trajectory market participants will track in the iron scrap price forecast throughout 2026.

Strategic Takeaways:

Looking ahead, the iron scrap market is expected to maintain broadly positive demand momentum through 2026, supported by continuing EAF capacity buildout, growing sustainability mandates across major steel-producing economies, and an expanding base of scrap-centric secondary steelmaking capacity. Geopolitical volatility and energy costs complicate the near-term pricing outlook.

To navigate this complex landscape, stakeholders should:

- Monitor Regional Price Differentials: Track quarterly pricing variations across the five monitored markets to identify cost-effective procurement windows. Establish benchmarks comparing iron scrap price per MT on a landed CIF basis against contract rates to highlight optimal sourcing windows before each procurement cycle.

- Monitor Geopolitical Risk Exposure: Track escalation dynamics in the current conflict and assess how shifts in hostility levels might affect iron scrap pricing, feedstock availability, and logistics costs. Establish internal alert thresholds that trigger procurement or hedging action when defined risk parameters are breached.

- Diversify Supply Chain Routes: Evaluate alternative sourcing geographies and shipping corridors to limit dependence on conflict-exposed trade lanes before disruption forces immediate adoption. Secondary supplier agreements and contingency freight contracts will provide critical resilience when primary routes face sustained disruption or capacity constraints.

- Adjust Procurement Strategy for Conflict Conditions: Adopt flexible contract structures including price reopener clauses and force majeure provisions to protect against geopolitical price spikes in iron scrap markets. Precautionary inventory buffers might reduce exposure to supply disruptions if market conditions tighten abruptly.

- Evaluate Scrap Grade Substitution Options: Assess whether higher-grade iron scrap can be substituted with alternative grades or shred blends when category-specific supply tightness develops. Proactive grade flexibility reduces concentration risk and may unlock cost advantages during periods of differential price volatility.

- Monitor Upstream Feedstock and Freight Cost Trends: Track changes in energy prices, shipping rates, and scrap collection costs to anticipate iron scrap pricing shifts before they materialize in spot markets. Early identification of cost-side pressures enables proactive hedging and forward procurement repositioning across buying horizons.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates — 12 deliverables/year

- Quarterly Updates — 4 deliverables/year

- Biannual Updates — 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

.webp)

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)