Magnesium Price Update: Sustained Growth Across Key Markets in Q1 2026

11-Jun-2026

At its core, magnesium is a lightweight metallic element prized for low density, silvery-white appearance, and superior machinability. Magnesium prices are tracked across automotive die casting, aerospace structural parts, electronics housings, and metallurgical desulfurization, where the metal replaces heavier steel and aluminum to cut component weight significantly. Upstream dolomite and magnesite ore costs, coal and coke-oven gas expenditure in Pidgeon-process reduction, container freight rates on Asia-Europe and Asia-Americas lanes, and seasonal procurement cycles in vehicle manufacturing govern pricing sensitivity across all tracked regions.

Global Market Overview:

Globally, the magnesium industry reached a volume of 990.14 Thousand Tons in 2025. Market projections indicate steady growth, with the industry expected to reach a volume of 1232.22 Thousand Tons by 2034, with a compound annual growth rate (CAGR) of 2.46% during 2026-2034. Electric vehicle platform expansions across China, Europe, and North America keep structural alloy demand on an upward trajectory, with magnesium's weight advantage over steel and conventional aluminum alloys sharpening its material substitution case. Constrained smelter capacity outside China, meanwhile, limits supply-side elasticity. Against this backdrop, the magnesium price trend responds to die casting investment cycles and aerospace program ramp-ups, while emerging consumer electronics and medical-device applications steadily diversify the demand base.

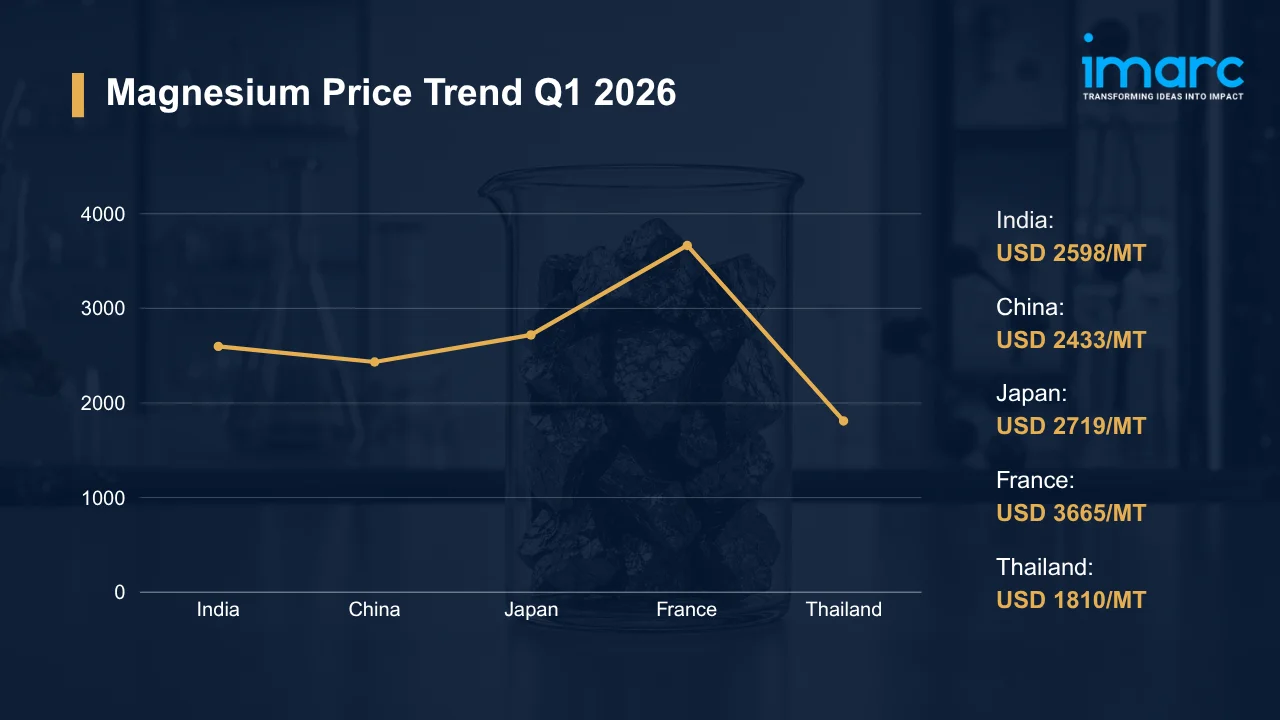

Magnesium Price Trend Q1 2026:

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| India | 2,598 | +3.76% | ↑ |

| China | 2,433 | +4.86% | ↑ |

| Japan | 2,719 | +5.87% | ↑ |

| France | 3,665 | +6.12% | ↑ |

| Thailand | 1,810 | +2.86% | ↑ |

To access real-time prices Request Sample

What Moved Prices:

India:

- In Q1 2026, magnesium prices in India climbed to USD 2,598/MT, marking a 3.76% QoQ gain. Automotive component and aluminum alloy manufacturers accelerated restocking as import availability tightened through the period. Port handling surcharges and firm freight rates on Asia-India corridors added further upward pressure, limiting buyer leverage during spot negotiations.

- Primary smelter operating rates remained cautious, capping spot supply before it could absorb the recovery in downstream procurement. The magnesium price chart through Q1 2026 traced a consistent upward arc, not because of any single demand spike, but because alloy converters and die casting units maintained steady purchase volumes week on week through March.

China:

- During Q1 2026, magnesium prices in China reached USD 2,433/MT, up 4.86% QoQ. Downstream alloy and aluminum sector demand recovered after inventory corrections carried over from Q4 2025, and export inquiries from European and Southeast Asian buyers returned with increased urgency. Producers lifted offers progressively as the supply-demand balance tightened.

- Firm coal and coke-oven gas costs in Shanxi and Shaanxi smelting clusters held back any meaningful capacity expansion through the period. CNY exchange rate stability allowed producers to sustain consistent export offer structures, while recovering overseas demand provided an additional pricing floor that reinforced the domestic market's upward direction into March.

Japan:

- In the first quarter of 2026, magnesium prices in Japan advanced to USD 2,719/MT as full import reliance and steady demand from automotive, electronics, and specialty alloy manufacturers pushed replacement costs higher. Overseas suppliers maintained elevated offer levels, translating directly into firmer contract renewal benchmarks for Japanese industrial purchasers.

- Across trans-Pacific and Asia-Japan trade lanes, port handling and logistics expenses added measurably to delivered prices. Precision component fabricators and alloy processors sustained regular procurement schedules rather than drawing down inventory, while buyers structured advance purchasing to guard against shipment delays that could disrupt production cycles.

France:

- During Q1 2026, magnesium prices in France surged to USD 3,665/MT, the quarter's highest regional value, rising 6.12% QoQ. Firm import costs from Asian origin markets drove the initial uplift, though extended delivery lead times from structural import dependence amplified the effect. Automotive lightweighting programs, aerospace component production, and specialty alloy consumption all maintained active procurement through the period.

- Once inventory depletion from earlier cautious buying became apparent, manufacturers moved to rebuild stock levels, intensifying spot demand in February and March. Sellers raised offers in line with higher logistics costs on Asia-Europe container routes, and aerospace and transport equipment producers sustained elevated activity that kept the French market as the premium-priced regional data point in the quarter.

Thailand:

- In Q1 2026, magnesium prices in Thailand reached USD 1,810/MT, a 2.86% QoQ increase. Die casting operations, aluminum alloying facilities, and industrial manufacturing plants drove the demand improvement, with buyers raising procurement activity to cover near-term production needs. Suppliers adjusted offers upward in line with stronger regional sentiment and firmer replacement costs from Asian origin markets.

- Freight and currency-related pressures held import costs firm throughout the quarter. Overseas supply availability remained balanced rather than abundant, providing sellers the confidence to maintain offer discipline. Inventory overhang across Thai distribution channels stayed minimal.

Drivers Influencing the Market:

Several factors continue to shape magnesium pricing and market behavior:

- Automotive and Aerospace Sector Demand: Electric vehicle platform rollouts across China, Europe, and North America keep structural alloy demand growing, with magnesium alloys gaining share in transmission housings, seat frames, steering components, and structural castings. Aerospace expansions in narrowbody aircraft and defense programs add incremental die casting and wrought alloy demand globally, sustaining upward pressure on the magnesium price index across the medium-term outlook horizon.

- Upstream Dolomite and Smelter Coal Costs: Coke oven gas and coal-derived energy function simultaneously as the heat source and chemical reducing agent in the Pidgeon process, which accounts for the overwhelming share of China's primary magnesium output. According to the USGS Mineral Commodity Summaries 2026, US imports of caustic-calcined magnesia from China increased 66% through August 2025 versus the same period in 2024, highlighting the supply concentration dynamics that channel upstream cost signals directly into international pricing.

- Energy Expenditure in Smelting: Sustained high-temperature calcination and reduction processing make electricity and thermal energy a dominant share of magnesium production costs. Per the EIA, the wholesale US natural gas spot price at Henry Hub averaged USD 3.52/MMBtu in 2025, a 56% rise from 2024's record-low annual average. Chinese smelters draw primarily on coal rather than gas, though broader energy market tightening shapes global cost benchmarks. Regional energy price disparities continue to determine which producing centers hold competitive advantage in export pricing across key destination markets.

- Ocean Freight and Logistics Economics: Container shipping rates on Asia-Europe, Asia-Americas, and Asia-Southeast Asia lanes set the floor for landed costs across import-dependent markets, including Japan, France, India, and Thailand. Rate increases prompt buyers to advance purchases and lock in freight contracts early; rate easings shift negotiating power toward buyers who can defer. Port handling charges, transshipment scheduling at major hub ports, and delivery lead-time variability add further unpredictability to delivered cost structures, contributing measurably to QoQ price movements in every tracked region.

- Trade Policy and Currency Dynamics: Import tariff structures and bilateral trade agreements determine how competitively Chinese-origin magnesium prices into each consuming market. JPY depreciation against the USD raises replacement costs for Japanese buyers, creating a structural regional premium observable in the tracked price data each quarter. For Thai and Indian importers, currency movements against the USD shift landed cost calculations independently of origin price changes, influencing contract negotiation outcomes and spot purchase volumes from quarter to quarter.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In August 2025, Martin Marietta Materials, Inc. completed its acquisition of Premier Magnesia, LLC, a privately-held producer of magnesia-based materials, expanding its footprint in higher-value magnesium-oxide products. The transaction supported the acquirer's strategy to diversify into specialty materials with complementary industrial end uses.

Outlook & Strategic Takeaways:

Looking ahead, the magnesium market is expected to expand, underpinned by EV-driven lightweighting demand, rising aerospace platform deliveries, and growing electronics-grade alloy applications in portable devices and precision machinery. Smelter coal and electricity cost trajectories in China's Shanxi and Shaanxi production corridors will remain the pivotal variable shaping the magnesium price forecast, given the Pidgeon process's structural thermal-energy dependence and the limited pace of capacity diversification outside China.

To navigate this complex landscape, stakeholders should:

- Assess Freight Market Developments: Monitor container shipping rate trends on Asia-Europe and Asia-Americas corridors to anticipate landed cost shifts ahead of contract renewal cycles. Negotiate logistics agreements incorporating rate adjustment mechanisms tied to prevailing spot benchmarks.

- Evaluate Downstream Demand Indicators: Track electric vehicle production output, automotive order books, and aerospace platform delivery schedules across principal consuming regions. Correlating demand signals with procurement cycles improves inventory positioning and reduces exposure to peak-price purchasing.

- Review Regulatory Compliance Expenditures: Audit costs associated with magnesium compound handling, storage, and environmental discharge under applicable chemical safety frameworks. Target operational efficiencies that reduce regulatory burden without compromising product integrity or workplace safety obligations.

- Strengthen Currency Exposure Management: Implement hedging strategies for procurement denominated in JPY, THB, and INR to stabilize landed cost projections against USD-denominated origin prices. Coordinate treasury and procurement functions to align foreign exchange coverage with import payment timelines.

- Explore Emerging Application Segments: Investigate growth potential in structural components for commercial drone platforms, medical implant-grade alloys, and thin-wall die castings for portable electronics. Engaging research partners at feasibility stage ensures supply scalability matches commercial demand timelines.

- Monitor Regional Price Differentials: Track quarterly pricing variations across India, China, Japan, France, and Thailand to identify cost-saving procurement windows. Benchmarking magnesium price per MT landed costs against prevailing contract rates builds the analytical base for optimal sourcing decisions.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates: 12 deliverables/year

- Quarterly Updates: 4 deliverables/year

- Biannual Updates: 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)