Q1 2026 Natural Gas Prices: Wide Gap Between Germany and China Markets

03-Feb-2026

Global natural gas prices are showing mixed momentum in early 2026, influenced by supply fluctuations, weather conditions, and energy demand patterns. The market outlook suggests moderate volatility, with prices expected to remain sensitive to geopolitical developments and seasonal consumption trends.

Natural gas prices are witnessing regional variations, supported by stable supply in some markets and demand surges in others. While Europe faces pricing pressure due to energy security concerns, Asia and North America are experiencing relatively balanced supply-demand conditions, indicating a cautiously stable outlook through 2026.

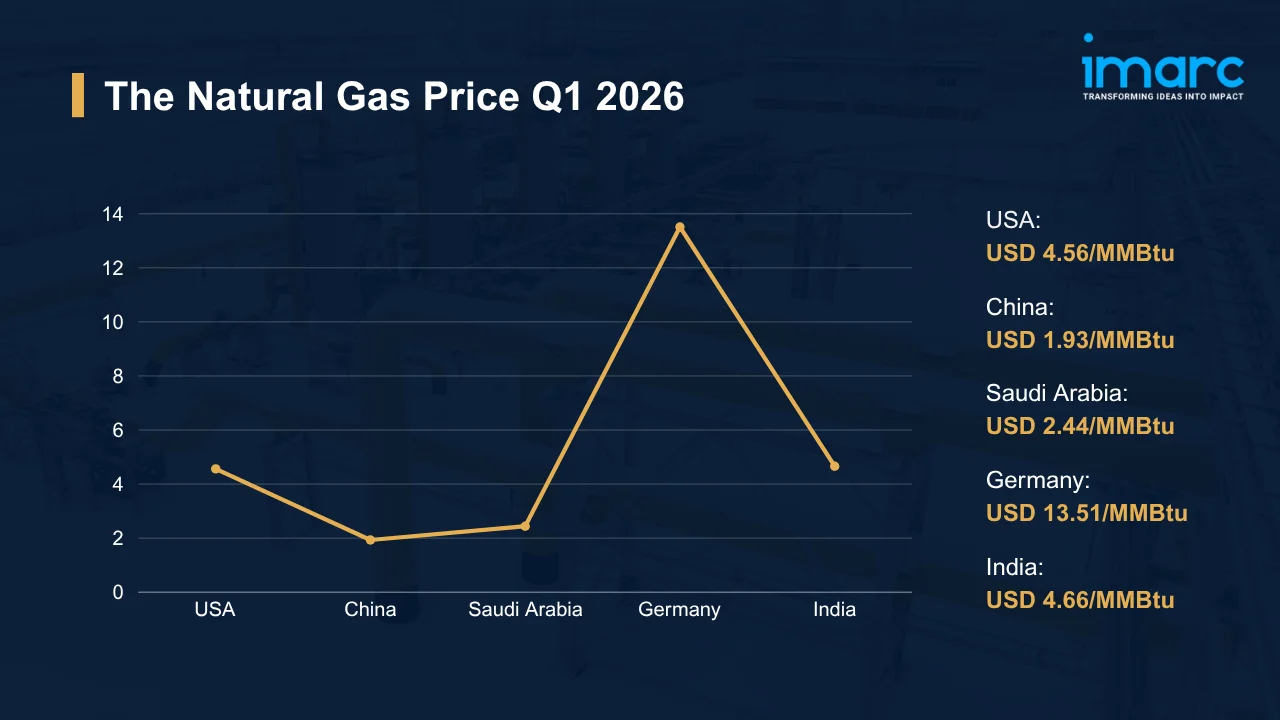

The natural gas prices for Q1 2026 highlight clear regional contrasts:

• USA: USD 4.56/MMBtu

• China: USD 1.93/MMBtu

• Saudi Arabia: USD 2.44/MMBtu

• Germany: USD 13.51/MMBtu

• India: USD 4.66/MMBtu

In Q1 2026, global natural gas prices showed mixed trends across key markets. The USA recorded higher price levels compared to previous quarters, supported by strong winter demand and increased consumption across residential and industrial sectors, despite robust domestic production.

Germany experienced significantly elevated prices at USD 13.51/MMBtu, reflecting continued dependence on imports, high energy costs, and ongoing supply uncertainties in the European market.

In contrast, China and Saudi Arabia reported relatively lower prices due to controlled domestic pricing mechanisms, stable supply, and government-supported energy policies. China’s pricing remained subdued amid sufficient supply and moderated industrial demand.

India saw moderate pricing at USD 4.66/MMBtu, supported by balanced demand conditions and diversified sourcing strategies, including LNG imports and domestic production.

Overall, the natural gas market in Q1 2026 remained moderately volatile, with regional supply-demand dynamics, geopolitical factors, and seasonal demand playing a key role in shaping global pricing trends.

Market Overview:

The global natural gas market has undergone significant changes in recent months, driven by supply chain adjustments and evolving energy demand. The natural gas price index indicates fluctuating trends, especially in regions dependent on imports.

Supply-side factors such as LNG availability, pipeline flows, and storage levels have influenced pricing patterns. At the same time, increased production in North America has helped stabilize global supply.

The natural gas price chart reflects seasonal fluctuations, with higher prices during peak winter demand and softer trends during off-peak periods. Macroeconomic factors, including inflation and industrial activity, continue to impact demand levels.

Overall, the market is transitioning toward a more balanced phase, although short-term volatility remains a key characteristic.

Access a Sample Report Now: https://www.imarcgroup.com/natural-gas-pricing-report/requestsample

Key Market Trends & Latest Developments in 2026:

- Rising LNG Trade Flows: Global LNG shipments are increasing, improving supply flexibility and connecting regional markets more closely.

- Europe’s Energy Security Push: Continued diversification of gas imports, including LNG and alternative suppliers, is reshaping pricing dynamics.

- Strong US Production: Robust shale gas output is stabilizing global supply and supporting export capacity.

- Asia’s Growing Demand: Industrial recovery and power generation needs are driving steady consumption across China, India, and Southeast Asia.

- Seasonal Demand Volatility: Winter heating demand and summer power usage are creating periodic price spikes across key markets.

- Expansion of LNG Infrastructure: New terminals, storage facilities, and pipelines are improving supply access and long-term market stability.

- Shift Toward Cleaner Energy: Natural gas continues to act as a transition fuel, benefiting from global decarbonization efforts.

- Geopolitical Influences: Ongoing global tensions and trade uncertainties remain key drivers of short-term price fluctuations.

- Energy Policy & Regulation Impact: Government policies, emissions targets, and subsidies are increasingly shaping demand and pricing trends.

Cost Structure & Pricing Factors:

- Upstream Production Costs: Exploration, drilling, and extraction expenses play a key role in determining base natural gas prices.

- LNG Processing & Transportation: Liquefaction, shipping, and regasification costs significantly impact international pricing.

- Energy & Fuel Costs: Fluctuations in fuel and electricity prices directly influence production and processing expenses.

- Storage & Inventory Levels: Adequate storage helps stabilize prices, while low inventories can trigger price spikes.

- Weather & Seasonal Demand: Extreme weather conditions increase heating or cooling demand, leading to short-term price volatility.

- Geopolitical Risks: Supply disruptions, trade restrictions, and global conflicts can create sudden price fluctuations.

- Infrastructure & Logistics: Pipeline capacity, LNG terminals, and transportation networks affect supply flow and regional pricing.

- Government Policies & Regulations: Environmental norms, subsidies, and energy policies influence both supply and demand dynamics.

- Currency Exchange Rates: Fluctuations in global currencies impact import/export costs and overall pricing.

- Long-Term Energy Transition: Investments in cleaner energy and decarbonization are reshaping cost structures over time.

Unlock Data-Driven Insights – Talk to an Expert: https://www.imarcgroup.com/request?type=report&id=22409&flag=C

Demand & Consumption Analysis:

Global natural gas consumption remains closely linked to power generation, industrial use, and residential heating. Demand analysis indicates steady growth, particularly in emerging economies.

The power sector continues to be a major consumer, with natural gas serving as a cleaner alternative to coal. Industrial demand also remains strong, especially in manufacturing and chemical production.

Urbanization and population growth are further supporting consumption trends, particularly in Asia. Increased investments in energy infrastructure are also boosting demand.

Government initiatives promoting cleaner energy sources are expected to sustain long-term consumption growth, positioning natural gas as a transitional fuel in the global energy mix.

Historical Price Comparison (Q4 2025 vs Q1 2026):

- USA: Increased from around USD 3.80 to USD 4.56/MMBtu (~18–20% rise) driven by strong winter demand and higher consumption despite stable production levels.

- China: Declined from approximately USD 2.10 to USD 1.93/MMBtu (~7–8% drop) amid sufficient supply and moderated industrial demand.

- Saudi Arabia: Remained relatively stable, moving slightly from USD 2.30 to USD 2.44/MMBtu (~5–6% increase) supported by controlled domestic pricing and steady supply.

- Germany: Surged from around USD 11.50 to USD 13.51/MMBtu (~15–18% increase) due to ongoing import dependency, supply concerns, and elevated energy costs.

- India: Rose from approximately USD 4.20 to USD 4.66/MMBtu (~10–11% growth) driven by balanced demand and increased LNG import prices.

Overall, the comparison between Q4 2025 and Q1 2026 highlights a divergent pricing trend across regions, with Europe witnessing sharp increases, while Asia showed relatively stable to slightly declining patterns. The data reflects how seasonal demand, supply security, and regional energy policies continue to shape the global natural gas pricing landscape.

Natural Gas Price Forecast 2026:

The Natural Gas Price Forecast 2026 indicates a stable yet slightly upward trend, with prices expected to remain within a balanced range throughout the year. The natural gas price trend will largely depend on seasonal demand, especially during winter, along with industrial consumption and power generation needs.

In terms of regional dynamics, the natural gas price today in North America may stay moderate due to strong production levels, while Europe and Asia could experience higher volatility because of LNG dependency. The natural gas price chart reflects steady movements rather than sharp spikes, suggesting controlled market conditions.

Looking ahead, the natural gas future price is expected to show gradual growth, supported by rising global demand and expanding LNG supply. Overall, the Natural Gas Price Forecast 2026 points toward stability with mild fluctuations, making it essential to track the natural gas price trend closely for better decision-making.

About the Report:

The latest Natural Gas Pricing Report provides comprehensive insights into global pricing dynamics, including detailed natural gas historical prices, trend analysis, and future forecasts.

Developed by IMARC Group, the report offers in-depth coverage of price index trends, regional analysis, cost structure, and demand outlook. It serves as a valuable resource for businesses, investors, and industry stakeholders.

For more detailed insights, access the full report here: https://www.imarcgroup.com/natural-gas-pricing-report

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)