Nitrosylsulfuric Acid Price Increases 3.45% in Germany, 2.45% in Belgium — Q1 2026 Update

12-May-2026

Summary:

Q1 2026 brought gains across every tracked nitrosylsulfuric acid market. Buyers stayed engaged through the quarter. Backed by steady chemical processing demand and tight feedstock availability, nitrosylsulfuric acid prices firmed across the segment, with quarterly movements clustered between a 2.11% and 3.45% rise QoQ. Energy benchmarks remained volatile through April. According to Al Jazeera, Brent crude jumped more than 6.08% to USD 118.03 per barrel in late April 2026 amid the prolonged Strait of Hormuz blockade and US siege of Iranian ports.

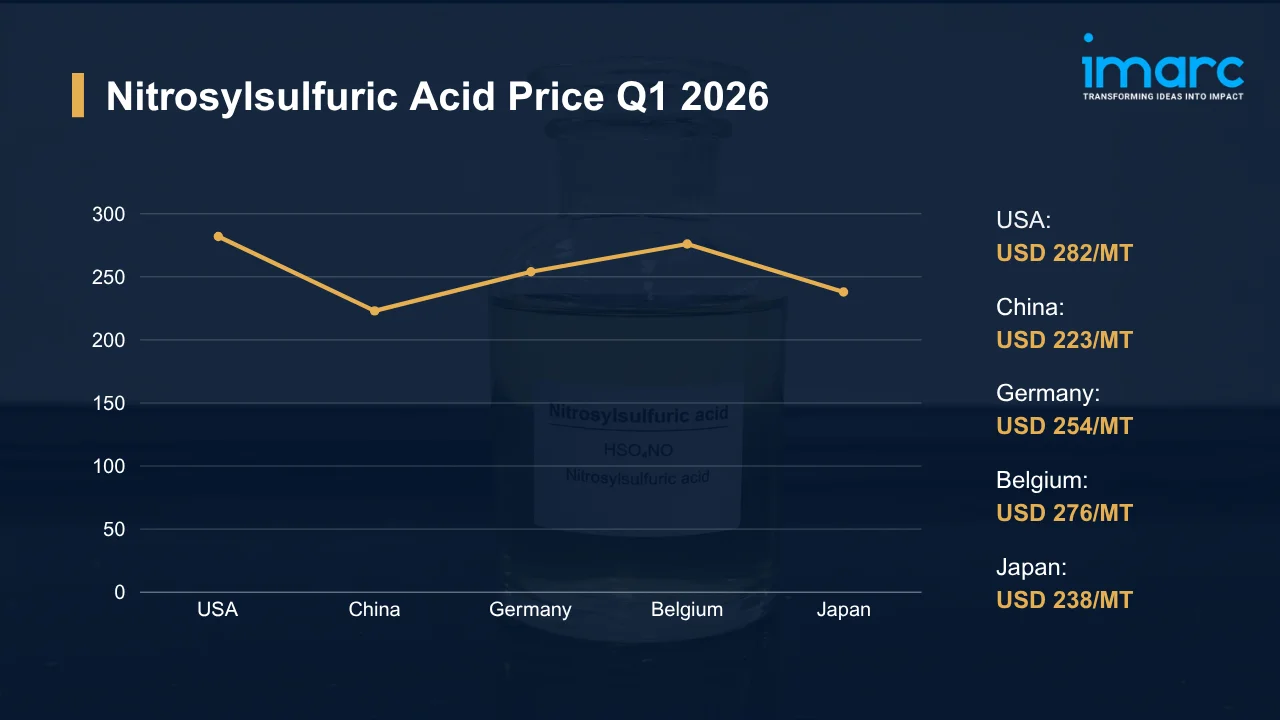

Nitrosylsulfuric Acid Price Q1 2026:

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| USA | 282 | +2.33% | ↑ Growth |

| China | 223 | +2.09% | ↑ Growth |

| Germany | 254 | +3.45% | ↑ Growth |

| Belgium | 276 | +2.45% | ↑ Growth |

| Japan | 238 | +2.11% | ↑ Growth |

To access real-time prices Request Sample

Kindly note: IMARC's pricing database tracks nitrosylsulfuric acid price movements across major global markets.

What Moved Prices:

USA:

- In Q1 2026, nitrosylsulfuric acid prices in the USA climbed to USD 282/MT, lifted by firm chemical manufacturing offtake. Demand from industrial processing units stayed steady. Controlled producer output, contained feedstock availability, and structured procurement from downstream specialty chemical and nylon precursor converters kept spot supply disciplined throughout the quarter.

- Spot tightness, not weak demand, set the tone in March. Across the North American market, the nitrosylsulfuric acid price chart reflected a steady upward trajectory lifted by limited availability, firm Gulf Coast inland transportation costs, and consistent contract fulfillment from specialty chemical and nylon precursor producers. Order books stayed full through the quarter.

China:

- During Q1 2026, nitrosylsulfuric acid prices in China advanced to USD 223/MT, propelled by firm nitration-based chemical demand. Industrial sector consumption added to the pull. With Chinese producers running at disciplined utilization rates, textile dyeing and pigment manufacturers tightened domestic availability through the entire quarter.

- Throughout the quarter, export pull continued tightening spot inventory. Domestic premiums widened gradually over the period. Concentrating procurement around long-term contracts, buyers secured volumes while CNY exchange rate stability buffered landed costs for FMCG-linked downstream chains, reinforcing measured procurement discipline among Guangzhou and Yiwu converter customers throughout the period.

Germany:

- In Q1 2026, nitrosylsulfuric acid prices in Germany advanced to USD 254/MT, marking a 3.45% QoQ rise. That was the strongest tracked gain. Driven by specialty chemical converter activity and balanced sulfuric acid feedstock availability, offer levels held firm while steady import flows and EU regulatory mandates jointly shaped regional supply throughout the quarter.

- Pharmaceutical and dye intermediate manufacturers stayed steady. Throughout the quarter, procurement aligned with confirmed contract throughput. Rhine corridor logistics ran without disruption, while EU compliance rules around chemical handling kept regional buyers structured rather than speculative, leaving inventories measured against potential supply tightening through the entire quarter.

Belgium:

- During Q1 2026, nitrosylsulfuric acid prices in Belgium reached USD 276/MT, a steady 2.45% QoQ gain. Antwerp distribution hubs kept material flowing. Backed by sustained chemical and industrial demand, volumes absorbed easily, while consistent production paired with reliable import flows kept supply balanced and ensured availability for downstream specialty chemical and pigment converters.

- Cautious procurement set the tone in Belgium. With Antwerp and Ghent as anchor hubs, buyers calibrated inventories to confirmed contract throughput rather than opportunistic positions, while intra-European trade flows from Germany and the Netherlands kept logistics costs predictable through the entire period. Restocking remained firm but measured.

Japan:

- In Q1 2026, Japanese nitrosylsulfuric acid prices rose to USD 238/MT, the smallest 2.11% QoQ gain. Domestic supply stayed disciplined throughout the quarter. Backed by stable consumption from chemical and manufacturing sectors, volumes absorbed easily, while controlled production paired with reliable Korean and Taiwanese import flows maintained supply for pharmaceutical and dye intermediate users.

- Asian regional trade flows functioned smoothly. Throughout March, CIF and FOB pricing held balanced. With fine chemical synthesis units absorbing steady volumes, procurement teams favored contractual sourcing over speculative spot purchases, while stable raw material costs kept producer margins intact and reinforced firm offer levels through the quarter.

Nitrosylsulfuric Acid Price Outlook After the Israel–Iran–USA Conflict:

Rising Energy Costs and Feedstock Price Pressure for Nitrosylsulfuric Acid: Tied to broader energy and freight benchmarks, sulfur and ammonia feedstock economics shape nitrosylsulfuric acid input costs. The conflict might push costs further. VLCC freight rates on Middle East to Asia tanker hauls surged to a record USD 423,736 per day in early March 2026, a 94% jump signaling how rapidly logistics costs cascade into petrochemical input pricing.

Regional Price Volatility and Demand Uncertainty for Nitrosylsulfuric Acid: Across regional consumers, the prevailing nitrosylsulfuric acid price trend might pivot fast. Direction depends on the conflict trajectory. With industrial users in Asia, Europe, and North America facing uncertainty around procurement timing as energy benchmarks fluctuate, any deepening of hostilities will likely amplify quarterly volatility across pharmaceutical, dye, and specialty chemical end uses.

Immediate Market Reaction:

Energy market disruptions trigger swift movement in spot trading for nitrosylsulfuric acid, driven by shifts in sulfur and freight costs. Key routes through the Persian Gulf and Red Sea face rising risks, forcing vessel diversions via the Cape of Good Hope and extending transit times. Supply conditions tighten as Northeast Asian producers reassess exports, while buyers in Europe and North America manage higher landed costs and increase inventories where possible, shaping the nitrosylsulfuric acid price index.

Impact on Nitrosylsulfuric Acid Prices:

The conflict might trigger several key changes in the nitrosylsulfuric acid market:

- Feedstock Cost Escalation: Sulfuric acid and nitrogen oxide feedstock costs might climb if regional energy benchmarks remain elevated through mid-2026. Pass-through becomes the central pricing question. Higher input costs will flow through to nitrosylsulfuric acid offer levels within weeks, with producers passing increases to specialty chemical, dye, and pharmaceutical buyers across multiple regions. Margin compression could intensify if contract pass-through structures lag spot escalation timelines.

- Logistics Premium and Routing Disruption: Tanker freight rates for Middle East origin shipments might stay elevated as insurance underwriters reassess Persian Gulf transit risk. War-risk premiums climb across the basin. Longer Cape of Good Hope routing adds 10-14 days to Europe-bound deliveries, swelling working capital tied up in transit, and buyers will face delayed arrivals while potentially shifting sourcing toward Asian or domestic North American producers where geography permits.

- Demand Reallocation and Inventory Adjustments: Downstream pharmaceutical and dye intermediate buyers might accelerate procurement to lock in volumes ahead of further price escalation. Allocation pressure builds across the segment. Speculative inventory accumulation will tighten near-term spot availability, while smaller specialty chemical operators could face constraints as larger industrial users pre-commit to extended supply contracts, and regional rebalancing will continue through Q3 2026 as procurement strategies adjust.

Combined, these forces will compound input cost volatility through mid-2026. Margin pressure cuts both ways here. While specialty chemical and pharmaceutical converters might rebalance procurement timing to manage exposure, producers across the supply chain tighten contract terms and regional pricing differentials widen as alternative routing emerges. Ultimately, pass-through determines final realized margin impact.

Supply Chain Disruptions:

With sulfur, ammonia, and intermediate feedstock cargo flowing through Persian Gulf shipping lanes, direct exposure rises as Strait of Hormuz transit remains constrained. Pipeline alternatives offer only partial relief. Insurance premiums and freight surcharges are also climbing, adding further cost pressure on chemical shipments.

Through Cape of Good Hope rerouting, voyages add two to three weeks to Asia-Europe shipments, swelling working capital and squeezing just-in-time inventory models for downstream specialty chemical converters. Producers might rebalance their order books. With regional sourcing across North American and East Asian feedstock chains, producers will bypass exposed corridors, while spot price volatility widens across regional markets as buyers compete for limited near-term volumes and smaller specialty chemical operators absorb the steepest cost increases through Q2 2026.

Global Market Overview:

Globally, the nitrosylsulfuric acid industry reached a volume of 392.9 Thousand Tons in 2025. Market projections indicate steady growth, with the industry expected to reach 547.9 Thousand Tons by 2034, with a compound annual growth rate (CAGR) of 3.76% during 2026-2034. Expanding nitration applications in pharmaceutical synthesis, dye intermediates, and explosives manufacturing underpin sustained consumption. Industrial expansion across emerging markets, regulatory tailwinds for specialty chemical production, and steady technological adoption in process chemistry will continue shaping market trajectory through the forecast horizon.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In November 2025, Deepak Chem Tech Limited, a wholly owned subsidiary of leading nitrosylsulfuric acid producer Deepak Nitrite, secured INR 32 crore through the issuance of optionally convertible redeemable preference shares allotted to Deepak Phenolics Limited. The capital raise was directed at strengthening the parent group's funding base and supporting ongoing project commitments, while Deepak Nitrite retained complete equity ownership.

Nitrosylsulfuric Acid Price Forecast (2026):

Through mid-to-late 2026, nitrosylsulfuric acid prices will stay sensitive to feedstock cost direction. Geopolitical risk dominates the broader outlook. While procurement caution will persist among specialty chemical and pharmaceutical buyers, restocking activity could lift quarterly demand briefly, and conflict-driven shipping benchmarks remain the dominant directional factor across all five tracked regional markets.

Should hostilities intensify, prices will face further upward pressure as freight, insurance, and feedstock costs climb together. Two paths diverge from here forward. On the other side, a diplomatic resolution might ease tanker premiums and restore feedstock flow, allowing softer offer levels to emerge by late 2026 across all major regional markets, while continued conflict will sustain elevated prices. These combined dynamics will continue shaping the nitrosylsulfuric acid price forecast for the year ahead.

Strategic Takeaways:

Looking ahead, the nitrosylsulfuric acid market is expected to navigate a period of measured price escalation through the second half of 2026, shaped by persistent feedstock cost pressure and ongoing geopolitical risk. Producers and buyers must face heightened uncertainty around delivery timing, contract pricing structures, and shifting regional supply availability.

To navigate this complex landscape, stakeholders should:

- Monitor Geopolitical Risk Exposure: Track escalation dynamics across the Israel-Iran-USA conflict and assess how shifts in hostility levels might affect nitrosylsulfuric acid pricing, feedstock availability, and shipping costs. Establish internal alert thresholds that trigger procurement or hedging responses promptly.

- Diversify Supply Chain Routes: Evaluate alternative sourcing geographies and shipping corridors to reduce dependence on conflict-exposed Persian Gulf trade lanes. Secondary supplier agreements and contingency freight arrangements will provide critical operational resilience if primary routes face prolonged disruption events.

- Adjust Procurement Strategy for Conflict Conditions: Adopt flexible contract structures with reopener clauses and force majeure provisions to protect against geopolitical-driven price spikes. Precautionary inventory buffers might reduce exposure materially if supply tightens abruptly across major exporting regions during conflict escalation.

- Track Regional Price Differentials: Monitor quarterly price gaps between USA, China, Germany, Belgium, and Japan to identify cost-saving procurement windows for nitrosylsulfuric acid buyers. Benchmark landed costs against prevailing contract rates to optimize sourcing decisions across regional markets effectively.

- Benchmark Procurement Against Spot Indices: Compare nitrosylsulfuric acid price per MT across spot transactions and contract negotiations to identify clear timing advantages. Procurement teams should align purchase commitments with demonstrated price differentials to capture cost-saving opportunities consistently across quarters.

- Assess Feedstock Cost Trajectory: Monitor sulfur, sulfuric acid, and nitrogen oxide input pricing across regional markets to anticipate cost pass-through into nitrosylsulfuric acid offer levels. Cost modeling should factor energy benchmarks and freight differentials affecting downstream production economics directly.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates — 12 deliverables/year

- Quarterly Updates — 4 deliverables/year

- Biannual Updates — 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)