Recycled High Density Polyethylene Price Falls 3.2% in USA, 2.2% in Germany — Q1 2026 Update

21-Apr-2026

Summary:

Pulled lower by soft converter demand and competitive import activity, four of five recycled high density polyethylene markets registered quarter-on-quarter declines in Q1 2026, with one gaining on localized supply tightness. Across most regions, procurement stayed broadly cautious. Quarter-on-quarter, recycled high density polyethylene prices moved between a 3.2% decline and a 2.0% gain. Brent crude climbed 36% year-to-date by early March 2026 as conflict-related disruptions across Middle Eastern oil corridors lifted feedstock costs for polymer recyclers.

Recycled High Density Polyethylene Price Q1 2026:

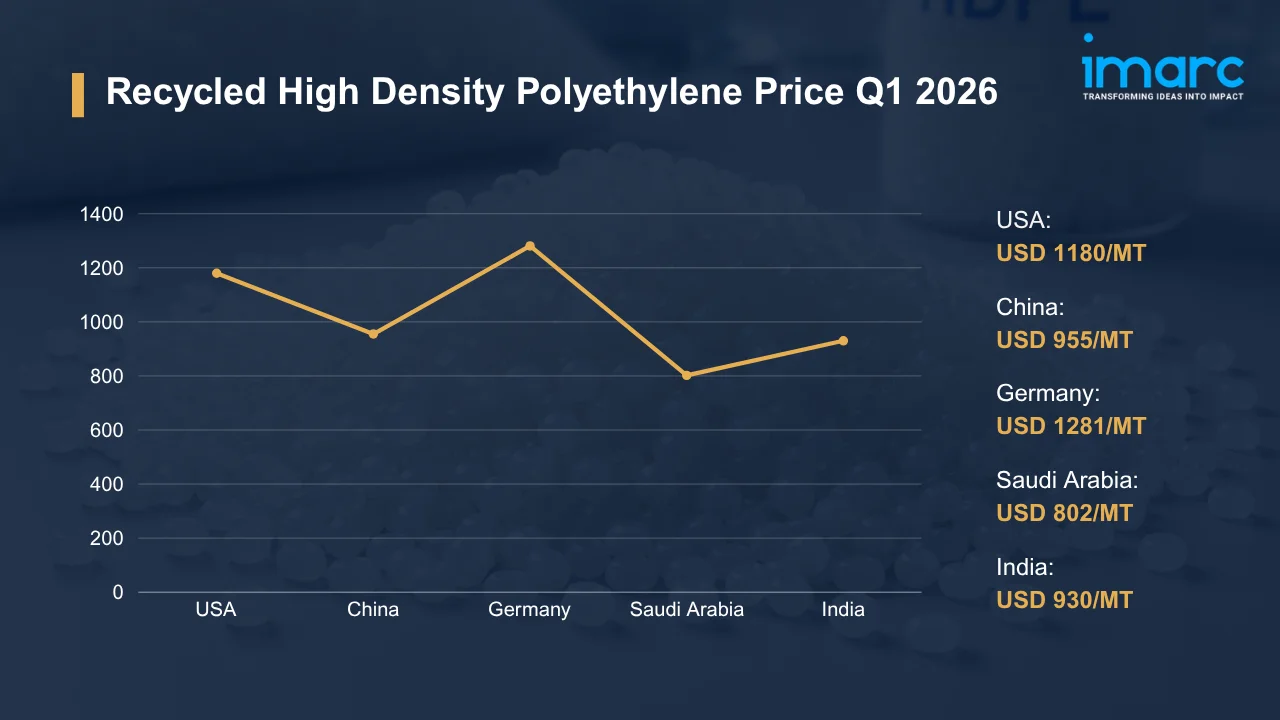

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| USA | 1180 | −3.2% | ↓ Decline |

| China | 955 | −1.2% | ↓ Decline |

| Germany | 1281 | −2.2% | ↓ Decline |

| Saudi Arabia | 802 | +2.0% | ↑ Growth |

| India | 930 | −1.0% | ↓ Decline |

To access real-time prices Request Sample

Kindly note: IMARC’s pricing database tracks recycled high density polyethylene price movements across major global markets.

What Moved Prices:

USA:

- In Q1 2026, USD 1180/MT was the price domestic converters paid for recycled high density polyethylene in the USA, marking a 3.2% QoQ decline as packaging and industrial buyers worked through accumulated carry-over inventory from Q4 2025. Gulf Coast recycling output remained high, capping any recovery in offer levels through the period.

- Asian import offers, arriving at increasingly narrow premiums over virgin resin, further depressed domestic spot levels throughout the quarter. The recycled high density polyethylene price chart showed a consistent downward drift from January onward, with e-commerce fulfillment converters deferring large-volume spot commitments well into March as procurement teams prioritized caution over coverage.

China:

- During Q1 2026, at USD 955/MT, recycled high density polyethylene prices in China eased 1.2% QoQ as domestic recyclers faced soft offtake from packaging converters and construction-linked buyers alike. Post-Lunar New Year restocking, which typically catalyzes a sharp demand recovery in January and February, proved shallower than most market participants had anticipated.

- Guangzhou-area blow-molding and pipe converters operated cautiously through the period, and FOB China offers trended downward as export demand from Southeast Asia failed to compensate for the domestic slowdown. CNY exchange rate dynamics added a layer of uncertainty for importers, keeping cross-border inquiry volumes below seasonal norms through most of February and March.

Germany:

- In Q1 2026, recycled high density polyethylene prices in Germany fell to USD 1281/MT, a 2.2% QoQ decline, as weaker durable goods output and subdued packaging demand led the Mittelstand converter base to cut procurement volumes. EU sustainability mandates provided structural support, but near-term buying momentum stalled despite this long-term regulatory tailwind.

- Rhine corridor freight costs held steady, yet rising energy prices tied to conflict volatility squeezed processing margins at German recycling facilities operating near capacity. The broader recycled high density polyethylene price trend across European markets points to continued softness through early 2026, with contract buyers preferring stock drawdowns over fresh volume commitments.

Saudi Arabia:

- In the first quarter of 2026, at USD 802/MT, recycled high density polyethylene prices in Saudi Arabia advanced 2.0% QoQ as local processors built inventory positions ahead of anticipated supply disruptions from escalating regional conflict. Downstream packaging converters serving food and consumer goods segments drove the bulk of incremental procurement activity.

- Conflict proximity introduced geopolitical risk premiums into local pricing discussions as Hormuz shipping disruptions tightened import availability from Asian origins through January and February. Saudi buyers responded by locking in contract volumes earlier than typical, a procurement shift that helped sustain upward price pressure through Q1 2026.

India:

- During Q1 2026, recycled high density polyethylene prices in India slipped to USD 930/MT, a 1.0% QoQ decline, as post-harvest FMCG restocking demand fell short of offsetting weakness among construction-segment buyers who deferred purchases following slower-than-expected infrastructure project activity. Converters across label and flexible packaging segments held procurement to minimum operational requirements.

- Competitive pricing from Southeast Asian origins and domestically produced grades kept offer levels under pressure throughout the period. Import parity from Middle Eastern sources edged higher as Hormuz-linked freight costs crept up, but the improvement was too narrow to reverse the dominant softening trend across Indian recycled polymer markets.

Recycled High Density Polyethylene Price Outlook After the Israel–Iran–USA Conflict:

Rising Energy Costs and Feedstock Pressure for Recycled High Density Polyethylene: Crude oil prices climb as Hormuz disruptions escalate. At recycled high density polyethylene facilities, sorting, washing, and extrusion costs track crude closely, squeezing processing margins directly. Approximately USD 20–25 Billion in petrochemical products crosses the Strait of Hormuz annually, and sustained hostilities might tighten the virgin polymer benchmark that recycled material prices typically shadow.

Regional Market Exposure and Demand Uncertainty for Recycled High Density Polyethylene: Conflict-driven uncertainty has shaken buyer confidence in forward purchasing across European, Middle Eastern, and Asian markets. Processors facing margin pressure might defer spot purchases until hostility trajectories clarify, and regional price differentials could widen as conflict-related cost structures diverge across supply chains in ways that are hard to predict.

Immediate Market Reaction:

As the conflict unfolds, recycled high density polyethylene markets face cost volatility from two converging forces: energy price surges and fractured trade flows through the Persian Gulf. Growing logistics costs are compounding the pressure. Facing the greatest direct exposure, Middle Eastern feedstock sites see material availability tighten while Asian and European buyers absorb steep freight cost increases. The recycled high density polyethylene price index is under upward pressure as energy costs feed directly into collection, sorting, and pelletizing operations across most major producing regions, even where downstream virgin resin availability might appear relatively stable. Driven by these pressures, procurement teams are revising sourcing horizons.

Impact on Recycled High Density Polyethylene Prices:

The conflict might trigger several key changes in the recycled high density polyethylene market:

- Energy Cost Escalation and Margin Compression: Recycling costs spike with crude oil. At USD 1180/MT in the USA and USD 1281/MT in Germany, recycled high density polyethylene prices already embed margin pressure, yet surging oil lifts sorting, washing, and extrusion costs faster than converters can absorb. Power-intensive facilities face a squeeze that might force smaller operators to curtail output, tightening supply in markets where energy costs are the dominant driver.

- Shipping Route Disruptions and Logistics Cost Increases: Freight costs are climbing very fast. Rerouting recycled high density polyethylene shipments around the Cape of Good Hope adds up to 14 extra transit days on Asia-to-Europe trade lanes, per published carrier guidance, and the cost impact reaches buyers within weeks. Elevated war risk insurance premiums inflate CIF landed costs further, and processors dependent on cross-border material flows will see procurement cost bases climb as these route diversions persist.

- Demand Divergence Between Conflict-Exposed and Insulated Markets: Markets near the conflict zone face a dual problem. Simultaneously, supply disruption and demand contraction threaten, as manufacturing activity might slow amid widening economic uncertainty. Conversely, at USD 930/MT in India and USD 955/MT in China, insulated markets could see incremental procurement gains as buyers redirect orders away from Gulf-adjacent supply chains toward lower-risk origins, sharpening divergences between exposed and sheltered markets.

Taken together, energy cost inflation compresses recycler margins, logistics disruptions push landed costs higher, and demand dislocations between conflict-exposed and insulated markets create price spreads that might persist beyond any foreseeable near-term resolution of hostilities. Recovery across markets will be uneven. Ultimately, these combined pressures will reshape recycled high density polyethylene pricing, forcing procurement rethinks industry-wide.

Supply Chain Disruptions:

Hormuz closures are choking recycled high density polyethylene supply chains. Conflict-driven vessel stranding at Gulf terminals creates petrochemical feedstock bottlenecks that lift virgin polymer benchmarks, transmitting upstream cost pressure to the recycled material pricing tiers that converters and processors actively track. As of early April 2026, over 600 vessels, including 325 tankers, have been stranded in the Gulf, driving war risk insurance premiums to potentially prohibitive levels and cutting effective freight capacity sharply.

Cape of Good Hope rerouting has surged as Hormuz closures escalate, adding up to 14 extra transit days on Asia-to-Europe lanes and substantially lifting per-container freight costs that reach landed recycled high density polyethylene prices within weeks. Across most consuming markets, importer margins are now compressing. Producers are inserting force majeure provisions into contracts as a standard precautionary response to shipping uncertainty, while procurement teams will likely build inventory buffers and accelerate qualification of non-Gulf-origin sources to reduce corridor exposure.

Global Market Overview:

Globally, the recycled high density polyethylene industry reached a volume of 1,686.42 Thousand Tons in 2025. Market projections indicate steady growth, with the industry expected to reach 2,816.98 Thousand Tons by 2034, with a compound annual growth rate (CAGR) of 5.87% during 2026-2034. Extended producer responsibility mandates are expanding globally. Driven by rising demand for sustainable packaging, circular economy frameworks across major economies are pulling recycled content volumes toward regulatory targets, while advances in sorting and extrusion technology continue improving material quality.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In December 2025, ALPLA obtained funding from the Dutch Ministry of Climate Policy and Green Growth and launched a new recycling firm in the Netherlands to test a patented solvent-based method for creating food-grade recycled high-density polyethylene material. The four-year initiative with the National Test Centre for Circular Plastics (NTCP) was undergoing trials at a pilot facility in Heerenveen and sought to secure European Food Safety Authority endorsement.

- In July 2025, LyondellBasell and Genox Recycling’s joint venture Genox LyondellBasell New Material Co., Ltd. obtained No Objection Letters from the US Food and Drug Administration for its processes involving recycled polypropylene and recycled high-density polyethylene, confirming compliance with FDA safety and quality standards. The sanctioned mechanical recycling techniques were employed to create Circulen Recover polymers, allowing the incorporation of recycled PP and PE in injection molding, blow molding, and extrusion applications, such as bottles and caps for the personal care and cosmetic sectors.

Recycled High Density Polyethylene Price Forecast (2026):

Near-term prices face multiple compounding headwinds. Sensitive to conflict-driven energy cost swings and shifting downstream procurement patterns, recycled high density polyethylene markets in conflict-adjacent regions show heightened buyer caution while non-exposed markets hold relatively steady through H1 2026. Any escalation in Middle Eastern hostilities might quickly reverse near-term price stabilization wherever it begins to emerge.

Intensifying hostilities will push prices sharply higher. Energy costs climb and freight rates surge while recycled high density polyethylene recyclers in conflict-exposed regions face output constraints, tightening global supply and compressing buyer procurement options across most consuming markets globally. Conversely, de-escalation could ease freight and feedstock costs, allowing prices to trend lower by mid-2026. These two scenarios will define the recycled high density polyethylene price forecast through the year ahead.

Strategic Takeaways:

Looking ahead, the recycled high density polyethylene market is expected to expand through 2026, with circular economy mandates, rising recycled content requirements in packaging, and improving collection infrastructure across major economies driving volume growth. Geopolitical volatility and energy cost pressures, however, define the key near-term risk profile for pricing decisions.

To navigate this complex landscape, stakeholders should:

- Track Regional Price Movements: Quarterly price differentials across supply regions reveal consistent cost-saving windows. Monitor these variations against prevailing contract rates to optimize timing and reduce the total landed cost of recycled high density polyethylene across buying programs.

- Monitor Geopolitical Risk Exposure: Track conflict escalation dynamics and assess how hostility shifts might affect pricing, feedstock availability, and logistics costs for recycled high density polyethylene. Establish internal risk thresholds that trigger procurement or hedging responses promptly.

- Diversify Supply Chain Routes: Conflict-exposed trade lanes affect recycled high density polyethylene flows directly. Evaluate alternative sourcing geographies and shipping corridors to reduce dependence on Hormuz-adjacent routes; secondary supplier agreements will provide resilience if primary routes face abrupt disruption.

- Adjust Procurement Strategy for Conflict Conditions: Adopt flexible contract structures with price reopener and force majeure provisions to guard against geopolitical price spikes affecting recycled high density polyethylene procurement. Precautionary inventory buffers might absorb exposure if supply tightens abruptly across markets.

- Monitor Upstream Feedstock Dynamics: Feedstock benchmark cycles move fast. Track crude oil and virgin polymer movements alongside the recycled high density polyethylene price per MT to enable timely contract renegotiations before upstream cost shifts reach converter markets.

- Explore High-Value Recycled Grade Segments: Food-grade and specialty applications command premiums. Securing long-term offtake agreements with converters in regulated recycled high density polyethylene segments will stabilize revenue and justify investment in quality-improving sorting and extrusion technology upgrades.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates — 12 deliverables/year

- Quarterly Updates — 4 deliverables/year

- Biannual Updates — 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

.webp)

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)