Sodium Bromide Price Increases 17.2% in Spain, 15.4% in Netherlands — Q1 2026 Update

05-May-2026

Summary:

Across all five tracked markets, Q1 2026 delivered firm gains for sodium bromide on tight upstream conditions. Restricted import availability, persistent oilfield offtake, and elevated freight collectively tilted the market upward. Quarter-on-quarter, sodium bromide prices moved between a 10.2% and 17.2% rise. Buying-side leverage stayed thin throughout the quarter. Against this backdrop, Brent crude pushed past USD 108 per barrel after late-April US-Iran peace talks collapsed.

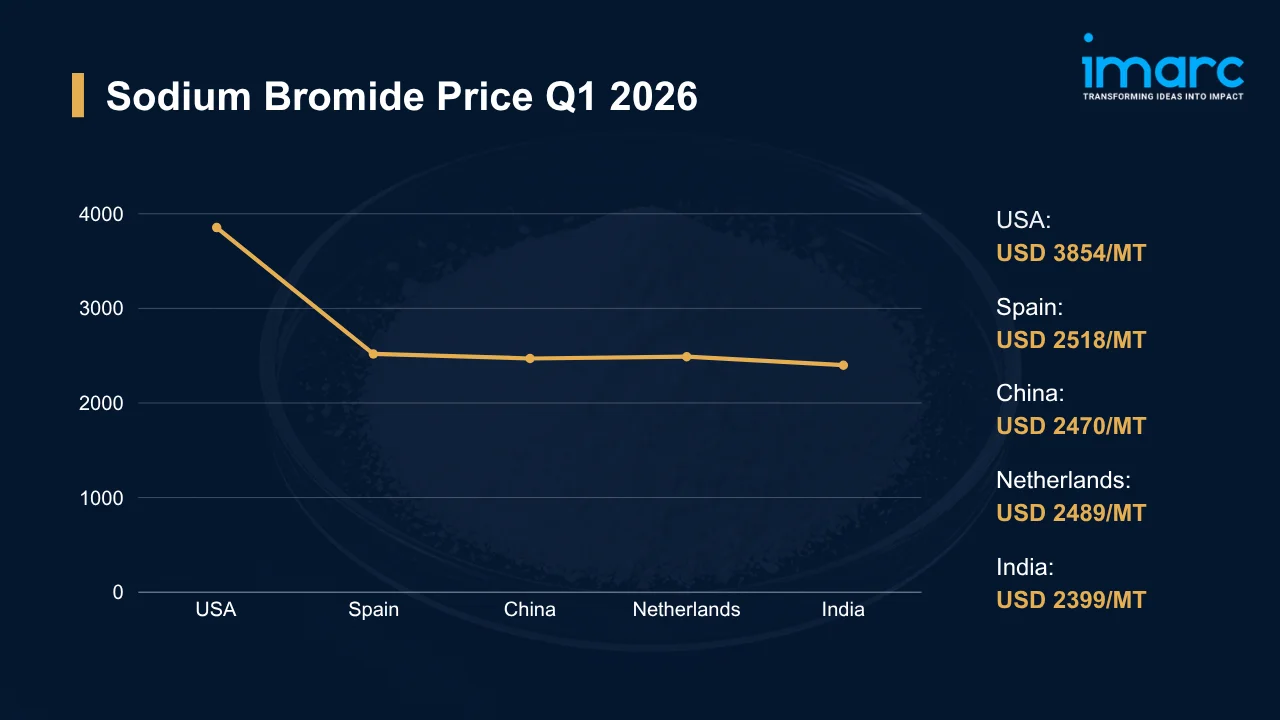

Sodium Bromide Price Q1 2026:

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| USA | 3854 | +12.0% | ↑ Growth |

| Spain | 2518 | +17.2% | ↑ Growth |

| China | 2470 | +10.2% | ↑ Growth |

| Netherlands | 2489 | +15.4% | ↑ Growth |

| India | 2399 | +12.2% | ↑ Growth |

To access real-time prices Request Sample

Kindly note: IMARC's pricing database tracks sodium bromide price movements across major global markets.

What Moved Prices:

USA:

- During Q1 2026, sodium bromide prices in the USA climbed to USD 3854/MT. Tightening domestic supply, persistent procurement from Permian and Eagle Ford oilfield service operators, and disciplined drilling fluid restocking through the winter completion cycle pushed the regional market firmly into sellers' hands. Spot tonnage stayed thin all quarter.

- Across the quarter, the sodium bromide price chart for the USA showed unbroken upward drift. Competitive contract execution and inventory drawdowns reinforced regional pricing. With domestic producers running at firm utilization, most contract negotiations through Q1 resolved close to seller-led offer levels, particularly across Gulf Coast and inland hubs where buyer-side leverage stayed limited.

Spain:

- During Q1 2026, sodium bromide prices in Spain rose 17.2% QoQ to USD 2518/MT, the steepest gain across the panel, lifted by firm chemical and water treatment demand against persistent import dependence and stretched supplier lead times. Domestic output stayed thin all quarter. With limited buying-side leverage, spot offers ratcheted higher through March.

- Active export commitments by regional traders compressed available spot tonnage further, prompting downstream formulators to lock in volumes ahead of schedule and absorb the resulting price premium without major resistance. Throughout Q1, distributor margins held firm. Across the Iberian peninsula, energy sector consumers drove the bulk of incremental demand, with construction-grade water treatment offtake adding modest baseline support.

China:

- During Q1 2026, sodium bromide prices in China advanced to USD 2470/MT, with steady chemical synthesis demand, disciplined production output across Shandong-cluster manufacturers, and regulatory oversight on chlor-alkali capacity capping any meaningful supply expansion. Domestic spot availability tightened materially through March. Across the export channel, sustained inquiries from regional buyers added structural pull.

- Outbound shipments to Southeast Asian and South Asian markets remained the structural anchor for Chinese suppliers, who calibrated offers carefully to match firm international interest while preserving disciplined domestic delivery commitments through the quarter. Across the production base, plant utilization stayed in disciplined ranges. Procurement teams built incremental positions ahead of expected logistics tightening near major export corridors.

Netherlands:

- In the first quarter of 2026, sodium bromide prices in the Netherlands climbed to USD 2489/MT, lifted by persistent drilling and industrial chemical demand, sustained import dependence, and intra-regional trade tightness. Supplier lead times stretched across the quarter. Through March, buyers had little room to delay procurement decisions.

- Rotterdam port handling activity stayed firm despite broader freight headwinds, channeling consistent material flows to inland chemical processors and adjacent European converters that relied on reliable terminal throughput across the quarter. Throughout March, most procurement decisions anchored to forward terms. With buyers focused on supply security rather than price discovery, spot deviations stayed minimal.

India:

- Throughout Q1 2026, sodium bromide prices in India advanced to USD 2399/MT, supported by sustained demand from oilfield services and chemical intermediate manufacturers, while domestic capacity proved insufficient to fully cover quarter-end consumption peaks. Import flows bridged the persistent gap. With domestic capacity tight, buyers absorbed higher landed costs without major resistance.

- Subcontinental pharmaceutical intermediate producers added incremental tonnage to their forward books, anchoring procurement against potential rupee volatility, escalating global freight risk, and the broader uncertainty cascading through international chemical supply chains. Through March, importer offers held firm. Most negotiations resolved close to landed cost rather than discounted parity.

Sodium Bromide Price Outlook After the Israel–Iran–USA Conflict:

Rising Energy Costs and Feedstock Pressure for Sodium Bromide: Energy-intensive sodium bromide production might face structural cost pressure. Globally, the conflict reshapes hydrocarbon pricing across regions. Across freight, power, and bromine inputs, Middle Eastern exposure remains material.

Regional Price Volatility and Demand Uncertainty for Sodium Bromide: Regional sodium bromide price spreads might widen further as conflict-driven uncertainty reshapes global import-export flows, with Asian and European buyers facing the steepest premiums given heavier reliance on Middle East-linked logistics chains. Throughout 2026, demand uncertainty will compound the volatility. Across the import landscape, North American producers might capture incremental share.

Immediate Market Reaction:

As the conflict unfolds, the sodium bromide market recalibrates rapidly. Israel and Jordan together account for a major share of global bromine extraction, leaving downstream producers heavily exposed to operational disruption and severe shipping delays near Dead Sea production hubs. Across drilling fluid and chemical formulation segments, the sodium bromide price index reflects sustained upward pressure as buyers accelerate procurement to lock in pre-escalation rates. European converters face the sharpest immediate impact given route exposure through Mediterranean and Suez transit lanes. Within the Asian channel, buyers might delay non-critical purchases until logistics conditions clarify.

Impact on Sodium Bromide Prices:

The conflict might trigger several key changes in the sodium bromide market:

- Bromine Feedstock Tightening: Disruption to Dead Sea bromine extraction operations or Mediterranean shipping corridors might constrain feedstock availability for sodium bromide producers reliant on long-standing Israeli or Jordanian source agreements through the rest of the year. Across alternative origins, producers in the United States and China will face heightened pricing power as global buyers actively seek substitution. If hostilities deepen, spot premiums might widen further.

- Shipping and Insurance Cost Escalation: Rising war-risk insurance premiums and diverted vessel routes might push delivered sodium bromide costs sharply higher for buyers dependent on East Mediterranean and Persian Gulf transit lanes through 2026. Across major lanes, marine carriers will likely apply emergency freight surcharges and bunker adjustments, layering additional cost onto every contracted ton. Within procurement teams, decisions might force renegotiation across major sourcing geographies.

- Regional Demand Reorientation: Across oilfield-heavy markets including the United States and India, buyers might bring forward procurement aggressively to hedge against further geopolitical escalation through the rest of 2026 and into early 2027. Suppliers will adjust contract terms to reflect higher risk premiums going forward. Within distributor networks, inventory positioning might shift toward longer-cycle holdings as a structural hedge against tightening supply.

Together, these dynamics will reshape sodium bromide pricing across major regions, leaving buyers exposed to elevated cost structures, persistent supply uncertainty, and a less predictable forward planning horizon through the remainder of 2026. Procurement strategies might require structural revision. Outside Middle East-linked corridors, producers will likely capture pricing leverage, while demand concentration might amplify volatility.

Supply Chain Disruptions:

Sodium bromide supply chain elements at greatest risk include Mediterranean shipping lanes serving Dead Sea producers, Persian Gulf transit corridors moving Asian-origin tonnage, and feedstock flows from Israeli bromine extraction operations. Across major routes, vessel diversions continue to extend transit times. In early March 2026, benchmark Very Large Crude Carrier (VLCC) rates for Middle East-to-China shipments hit a record USD 423,736 per day, roughly 94% above pre-conflict levels, with insurance premiums and bunker costs layering further landed-cost inflation.

Sodium bromide producers might shift incremental tonnage toward Cape of Good Hope routings to bypass Middle Eastern chokepoints, accepting longer transit times of two to three weeks in exchange for predictable arrivals. For buyers, cost recovery becomes considerably harder. Throughout 2026, inventory buffers across European and Asian distributors will likely expand to absorb extended lead-time risk. Among alternative origins, US Smackover operations and Chinese inland producers might gain priority, although qualification cycles can stretch across multiple quarters.

Global Market Overview:

Globally, the sodium bromide industry reached a volume of 160.3 Thousand Tons in 2025. Market projections indicate steady growth, with the industry expected to reach 233.0 Thousand Tons by 2034, with a compound annual growth rate (CAGR) of 4.24% during 2026-2034. Expanding demand from oilfield drilling fluids, water treatment chemistry, and bromine-derived intermediates anchors the growth path. Tightening environmental regulations and substitution patterns shape the sodium bromide price trend across end-use sectors. Technological advances in well completion fluids reinforce baseline growth.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In October 2025, a novel laboratory demonstrator at the University of Warwick highlighted the capabilities of ammonia salt resorption heat pump technology in minimizing carbon emissions from heating and cooling buildings. The system employed specialized gas-to-adsorbent heat exchangers incorporating sodium bromide as the low-temperature salt and manganese chloride as the high-temperature salt. It provided robust efficiency and enduring cycling performance, highlighting the first uninterrupted functioning of this combination. Despite the ongoing issues with thermal mass and contact resistance, the findings indicated potential applications in home heating and the enhancement of waste heat.

Sodium Bromide Price Forecast (2026):

Near-term sodium bromide prices will remain firm through mid-2026, anchored by sustained oilfield demand, conflict-driven energy cost inflation, and persistent supply-side tightening across major bromine-producing regions including Dead Sea corridors and Mediterranean export hubs. Across the buyer base, procurement caution will likely persist as logistics conditions evolve. Any easing of geopolitical risk might open a partial stabilization window.

If geopolitical hostilities intensify further, sodium bromide prices will face renewed upward pressure as energy costs climb and freight rates widen risk premiums across global trade routes. Producers in conflict-exposed zones might curtail output, tightening international availability further. Conversely, a diplomatic resolution might ease freight rates and restore feedstock flows, allowing prices to drift back toward pre-conflict ranges by year-end and reshaping the sodium bromide price forecast through the remainder of 2026.

Strategic Takeaways:

Looking ahead, the sodium bromide market is expected to navigate a complex landscape shaped by oilfield-driven demand, geopolitical risk, and shifting feedstock economics tied to bromine extraction in the Middle East. Procurement strategy, sourcing diversification, and disciplined inventory management will determine which buyers maintain cost competitiveness through the year ahead.

To navigate this complex landscape, stakeholders should:

- Monitor Regional Price Differentials: Track quarterly pricing variations across the USA, Spain, China, Netherlands, and India to identify cost-saving procurement opportunities. Establish benchmarking protocols that compare landed costs against contract rates for optimal sourcing decisions across distinct demand cycles.

- Monitor Geopolitical Risk Exposure: Track escalation dynamics in the current conflict and carefully assess how shifts in hostility levels might affect sodium bromide pricing, feedstock availability, and logistics costs. Establish internal alert thresholds that trigger procurement or hedging action.

- Diversify Feedstock Supply Channels: Evaluate alternative bromine suppliers beyond Israeli and Jordanian sources to mitigate concentration risk. Secure secondary supply agreements with US Smackover operations or Chinese producers that activate during periods of primary source disruption or capacity constraint.

- Diversify Supply Chain Routes: Evaluate alternative sourcing geographies and shipping corridors to reduce dependence on conflict-exposed trade lanes. Secondary supplier agreements and contingency freight arrangements will provide critical resilience if primary routes face disruption through the remainder of 2026.

- Adjust Procurement Strategy for Conflict Conditions: Adopt flexible contract structures with price reopener clauses and force majeure provisions to protect against geopolitical price spikes. Precautionary inventory buffers might reduce exposure if supply tightens abruptly across primary sourcing geographies during the year.

- Monitor Upstream Bromine and Energy Costs: Closely track bromine extraction costs, ethylene-derived energy inputs, and freight surcharges to anticipate forward sodium bromide price per MT movements. Continuous market tracking enables proactive cost containment as upstream signals shift through the procurement window.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates — 12 deliverables/year

- Quarterly Updates — 4 deliverables/year

- Biannual Updates — 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)