Sulphuric Acid Prices Surge Across Key Markets: Access Real-Time Data, Historical Trends, and 2026 Forecast

04-Jun-2026

Corrosive, dense, and highly reactive with water, sulphuric acid is one of the most widely produced inorganic chemicals worldwide and serves as a critical input across numerous industrial value chains. Sulphuric acid prices respond directly to procurement patterns across fertilizer synthesis, petroleum refining, metal ore leaching, battery-grade chemical production, and industrial intermediates. Upstream elemental sulphur costs, energy intensity in contact-process conversion units, ocean freight surcharges on corrosive cargo, and seasonal demand cycles from agricultural and industrial end users define the principal variables governing price movement for this commodity.

Global Market Overview:

Globally, the sulphuric acid industry was valued at USD 16.0 Billion in 2025. Market projections indicate steady growth, with the industry expected to reach USD 18.0 Billion by 2034, with a compound annual growth rate (CAGR) of 1.35% during 2026-2034. Phosphate fertilizer output expansion across Asia and South America anchors the demand baseline, pulling consistent acid volumes even when industrial procurement softens. Environmental mandates capping sulphur dioxide emissions from refineries and smelters enforce byproduct acid recovery, sustaining available supply and reinforcing the sulphuric acid price trend across the medium-term outlook.

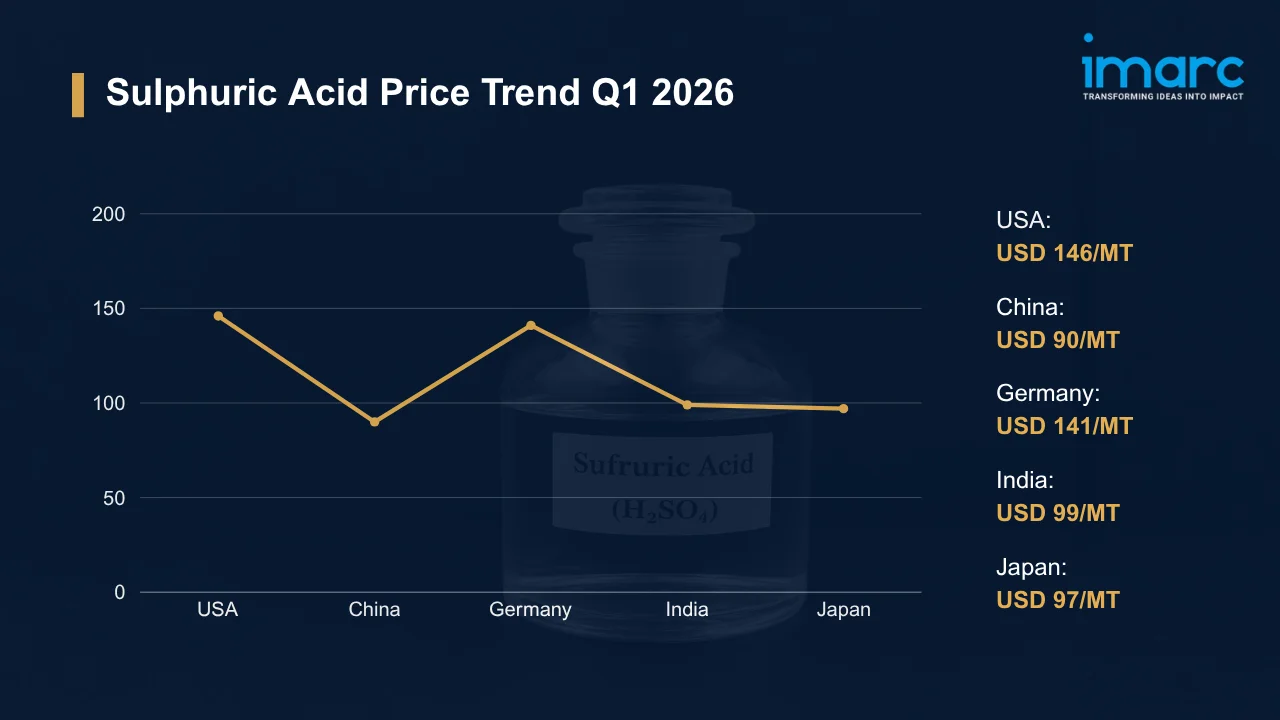

Sulphuric Acid Price Trend Q1 2026:

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| USA | 146 | +2.89% | ↑ |

| China | 90 | +1.09% | ↑ |

| Germany | 141 | +0.78% | ↑ |

| India | 99 | +1.02% | ↑ |

| Japan | 97 | +2.92% | ↑ |

To access real-time prices Request Sample

What Moved Prices:

USA:

- In Q1 2026, USD 146/MT marked the highest sulphuric acid price recorded across tracked USA transactions since Q2 2025, up 2.89% QoQ as fertilizer manufacturers accelerated spring-season contract volumes. Gulf Coast and Midwest distribution hubs tightened as integrated smelter byproduct output held below prior-quarter levels, limiting spot market availability through March.

- Constrained byproduct acid recovery from smelting operations kept supply discipline intact even as downstream pull strengthened. Handling surcharges for corrosive cargo pushed logistics costs above year-earlier averages. Tracking the sulphuric acid price chart through Q1 2026, the appreciation curve was demand-led rather than supply-shock driven, distinguishing this move from prior quarters where smelter outages had underpinned prices.

China:

- During Q1 2026, sulphuric acid prices in China reached USD 90/MT, a 1.09% QoQ gain that underperformed the other four tracked regions. Smelter and refinery acid generation remained high, yet phosphate fertilizer producers and industrial chemical converters across Shandong and Yunnan absorbed available volumes without triggering surplus accumulation at distribution points.

- Across export channels, international buyers drew on competitively priced Chinese cargoes, reducing domestic inventory overhang. Cautious procurement prevailed inside China, though not from demand weakness. Buyers read the steady supply picture as removing urgency from restocking decisions. The net result was gradual, supply-balanced appreciation rather than demand-spike pricing.

Germany:

- In Q1 2026, at USD 141/MT, sulphuric acid prices in Germany registered a 0.78% QoQ gain, the smallest increase among tracked European and Western markets. Battery material producers alongside specialty chemical manufacturers held procurement schedules steady, while import inflows from Eastern European origins declined, tightening spot availability against firm industrial consumption.

- Pushed higher by mandatory sulphur dioxide emission controls, producer compliance costs limited any capacity expansion response to the firming demand signal. Market participants managed inventory close to operational minimums. Procurement decisions reflected preference for supply certainty over price speculation, with contract-based buying dominating spot transactions through the quarter.

India:

- During Q1 2026, sulphuric acid prices in India climbed to USD 99/MT, a 1.02% QoQ advance driven by phosphoric acid and DAP sector procurement ahead of kharif season fertilizer blending activity. Agricultural policy incentives sustaining upstream fertilizer output translated into reliable baseline acid offtake from producers at coastal and inland plants.

- With domestic sulphur feedstock availability stretched at several inland conversion facilities, import flows from Middle East suppliers supplemented production, though lead times on those cargoes introduced near-term pricing variability. Buyers balanced the need for supply continuity against the cost risk of premature restocking. Transit delays at major western ports contributed to localized spot tightness in February.

Japan:

- In Q1 2026, sulphuric acid prices in Japan surged to USD 97/MT, a 2.92% QoQ increase that led all five tracked regions. Semiconductor fabrication and battery-grade chemical producers drove consistent purchasing activity, while limited domestic acid production capacity concentrated supply pressure in a market structurally dependent on imported sulphur feedstock.

- Across procurement channels, elevated global elemental sulphur benchmarks fed directly into Japanese producer cost structures, compressing margins and incentivizing price recovery. Cautious inventory management by buyers, wary of overcorrecting after prior periods of supply tightness, reduced the buffer available to absorb demand surges. Spot availability stayed restricted through the quarter.

Drivers Influencing the Market:

Several factors continue to shape sulphuric acid pricing and market behavior:

- Fertilizer and Agricultural Sector Demand: Phosphate fertilizer manufacturing forms the foundation of sulphuric acid demand, making the agricultural sector the primary driver of consumption. Seasonal agricultural calendars introduce procurement surges that the sulphuric acid price index consistently reflects, particularly in Q1 ahead of Northern Hemisphere spring planting.

- Upstream Sulphur Feedstock Availability: Recovered as a byproduct from petroleum refining, natural gas processing, and metal smelting, elemental sulphur is the sole viable feedstock for contact-process acid synthesis. Per the USGS 2026 Mineral Commodity Summary, the average US elemental sulphur price jumped to USD 180 per Ton in 2025 from USD 46 per Ton in 2024, a near-fourfold increase that transmitted directly into producer cost structures globally. Shifts in refinery run rates, gas plant throughput, and smelter scheduling alter byproduct acid availability, making upstream operating decisions at non-acid facilities a material price variable downstream.

- Energy Expenditure in Acid Production: Throughout contact process operations, natural gas and electricity costs account for a substantial portion of total production expenditure per ton of acid output. European acid manufacturers face significantly higher energy expenses compared to their counterparts in China or the Middle East, leading to ongoing cost-floor disparities that influence regional delivered price variations. Fixed contract obligations limit short-term pass-through speed; when energy costs spike, margin compression precedes price adjustment by one to two quarters.

- Ocean Freight and Logistics Economics: Across trade lanes, sulphuric acid travels as a hazardous corrosive cargo, attracting elevated handling fees, specialized tanker premiums, and port dwell surcharges not applicable to non-classified commodities. Freight rates on Asia-Europe and Middle East-Asia corridors directly set CIF landed costs for import-reliant markets, such as Japan and India. Container or specialized tanker tightness on key routes can delay restocking cycles, amplifying spot price moves when import-dependent producers need prompt supply.

- Environmental and Regulatory Compliance: Mandatory sulphur dioxide recovery at refineries, smelters, and acid plants sets a compliance-driven production floor, but simultaneously elevates fixed costs for operators. Capital expenditure on tail gas treatment units and continuous emission monitoring systems increases per-unit production costs, limiting capacity expansion responses when demand firms. Hazardous chemical registration and handling requirements across Europe and North America add administrative layers, filtering cost increases progressively into contract pricing across jurisdictions with the strictest enforcement regimes.

- Trade Policy and Currency Dynamics: When major producing economies adjust export quotas or tariff structures, global sulphuric acid trade flows realign, redirecting supply surpluses and creating regional deficits that reprice local markets. Currency depreciation in import-dependent markets, specifically yen and rupee weakness against the US dollar, inflates landed costs for Japanese and Indian buyers independently of any change in benchmark dollar prices. Procurement teams in those markets who lack active currency hedges absorb exchange losses directly into their effective cost of goods.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In March 2026, Union Home and Cooperation Minister of India, Amit Shah, announced plans to inaugurate IFFCO's newly developed SAP III sulphuric acid plant at the Paradip complex in Odisha. The facility was designed to expand domestic fertilizer production capacity and improve chemical processing efficiency, strengthening agricultural supply chain infrastructure.

- In April 2025, BASF announced the establishment of a new semiconductor-grade sulphuric acid production unit at its Ludwigshafen facility in Germany. Equipped with advanced purification technology, the unit targeted stringent chip-manufacturing quality requirements, positioning BASF to serve growing procurement demand from global semiconductor producers.

Outlook & Strategic Takeaways:

Looking ahead, the sulphuric acid market is expected to sustain measured expansion through 2034, with fertilizer sector procurement, LFP battery chemical demand, and semiconductor-grade acid consumption collectively underpinning volume growth across all five tracked regions. Upstream elemental sulphur cost trajectories and tightening emission compliance mandates across major producing jurisdictions will serve as the principal variables defining the sulphuric acid price forecast over the medium-term planning horizon.

To navigate this complex landscape, stakeholders should:

- Assess Freight Market Developments: Monitor hazardous-cargo tanker and container rate trends on Asia-Europe and Middle East-Asia corridors to anticipate CIF landed cost movements ahead of procurement cycles. Negotiate logistics agreements that include rate-adjustment provisions linked to prevailing freight benchmarks.

- Evaluate Downstream Demand Indicators: Track fertilizer production schedules, semiconductor fab output, and battery material procurement volumes across key consumption markets. Correlate those demand signals with inventory planning to prevent supply shortfalls during peak agricultural and electronics procurement windows.

- Monitor Regional Price Differentials: Track quarterly price movements across the USA, Germany, China, India, and Japan to isolate cost-advantaged procurement windows. Benchmarking sulphuric acid price per MT against contract rates across these five markets enables procurement teams to validate sourcing decisions against live market conditions.

- Review Regulatory Compliance Expenditures: Audit handling, storage, emissions monitoring, and chemical registration costs associated with sulphuric acid operations across all active jurisdictions. Identify process efficiencies that reduce compliance overhead without compromising chemical safety or environmental discharge obligations.

- Strengthen Currency Exposure Management: Implement hedging instruments for rupee- and yen-denominated procurement to stabilize US-dollar-equivalent landed costs against exchange rate volatility. Align treasury coverage timelines with anticipated import payment schedules to avoid gap exposures.

- Explore Emerging Application Segments: Assess commercial potential in LFP battery precursor manufacturing, high-purity semiconductor acid supply chains, and specialty chemical intermediates as diversification avenues. Engage research and technology partners to evaluate whether existing supplier relationships can support quality and purity requirements in these higher-margin segments.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates: 12 deliverables/year

- Quarterly Updates: 4 deliverables/year

- Biannual Updates: 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)