UK Insurance Market Size, Share, Trends and Forecast by Type and Region, 2026-2034

UK Insurance Market Size & Forecast 2026-2034

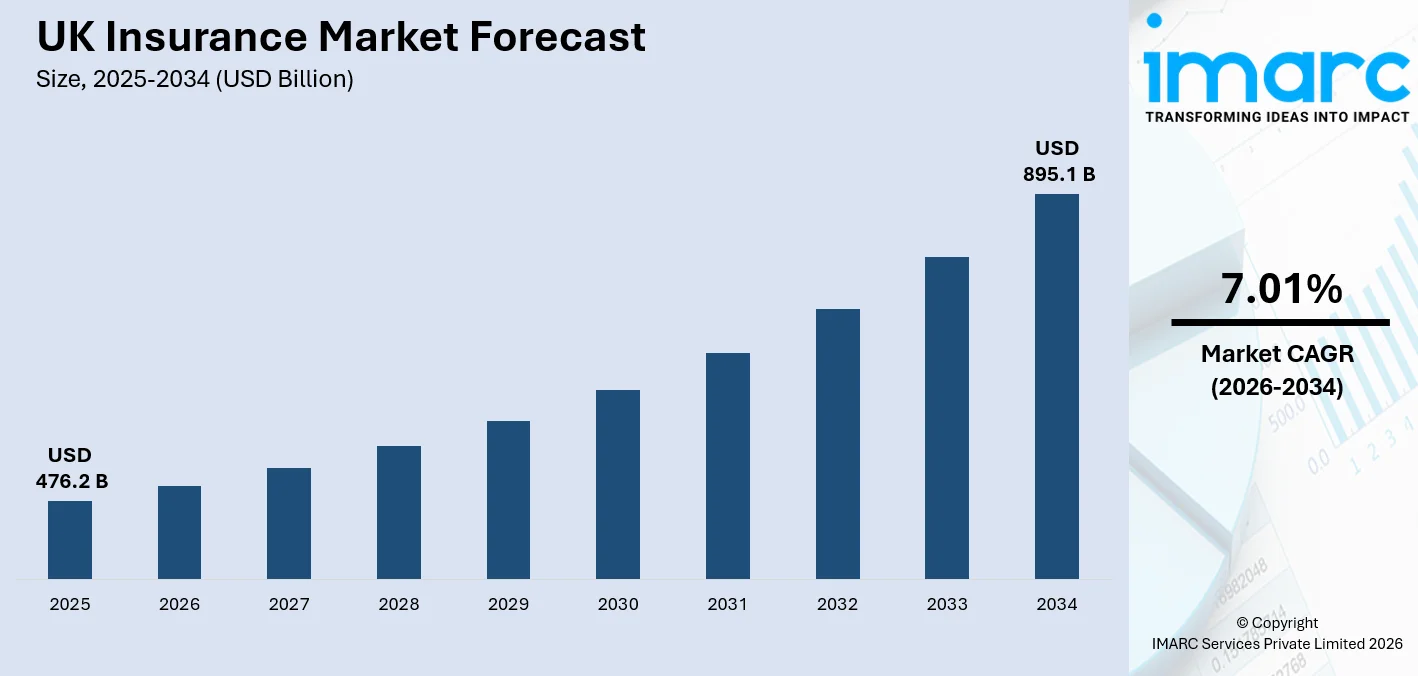

The UK insurance market size, valued at USD 476.2 Billion in 2025, is projected to reach USD 895.1 Billion by 2034, growing at a CAGR of 7.01% from 2026-2034, propelled by robust growth in both life and non-life segments driven by rising consumer demand for comprehensive protection, rapid insurtech adoption, landmark market consolidation, and the structural pull of growing NHS waiting lists expanding private health insurance uptake. According to the UK car insurance statistics, over 44 million motor insurance policies were sold in the UK in 2024, generating total premiums exceeding 20 billion pounds, underpinning the structural scale of the UK insurance market.

To get more information on this market Request Sample

UK Insurance Industry Analysis - Key Insights

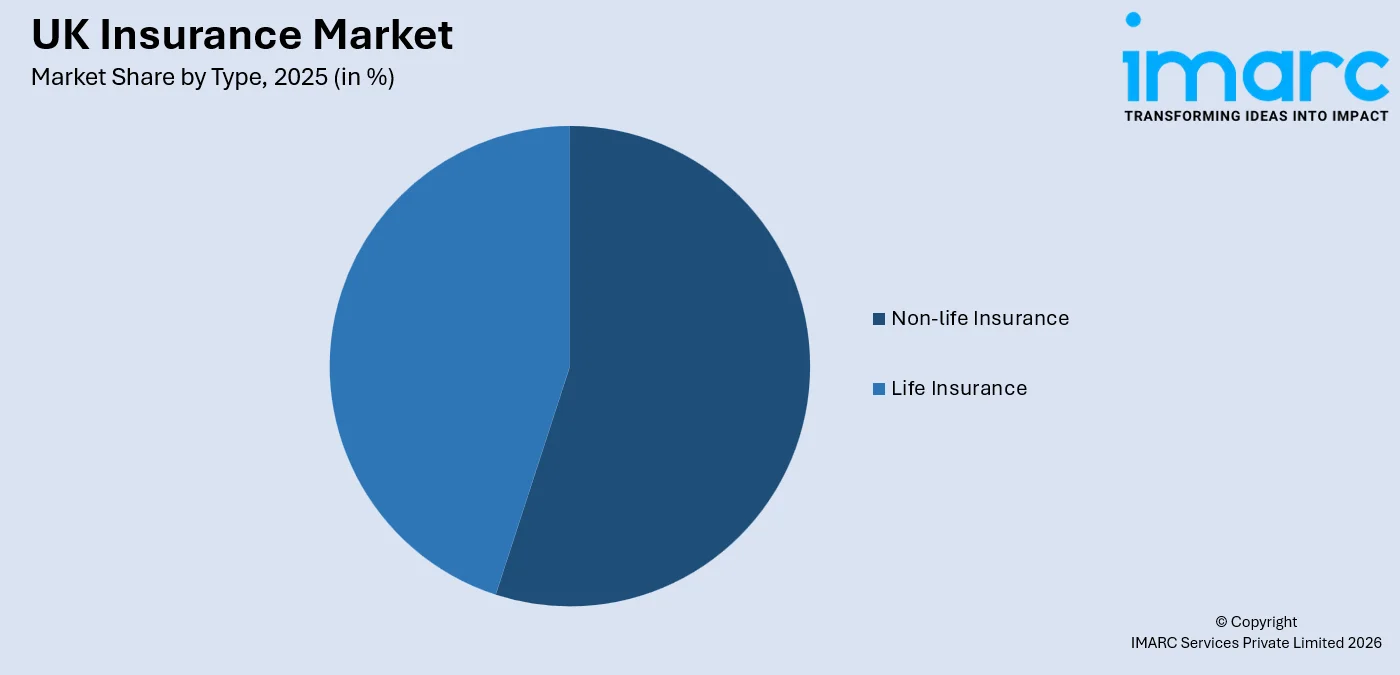

- Non-life insurance commands 52.4% of the type segment - motor, property, liability, and commercial lines collectively drive the majority of premium volume in the UK, anchored by mandatory motor coverage for over 40 million vehicles on UK roads and growing commercial risk complexity.

- London leads regionally at 20.5% - but this is a notably concentrated share for a single region, reflecting the capital's dual role as both the world's specialist insurance marketplace, revealing a genuinely distributed national insurance demand profile.

UK Insurance Trends and Dynamic 2026

Market Trends

Landmark Market Consolidation Reshaping the Competitive Landscape

A wave of mergers and acquisitions is fundamentally redrawing the UK insurance sector's competitive structure, creating scale-driven conglomerates with enhanced pricing power and operational efficiency. Aviva completed its 3.7 billion pound acquisition of Direct Line Insurance Group in July 2025strengthening market consolidation in the UK insurance sector, creating a larger combined player with expanded customer reach and underwriting capacity. The deal enhances pricing power, operational efficiency, and product innovation, helping drive competition and scale in the UK insurance market while accelerating digital and distribution synergies.

Insurtech Innovation Driving Digital Distribution and Product Personalization

The rapid integration of artificial intelligence, telematics, and IoT-enabled risk assessment is transforming underwriting precision, claims automation, and customer acquisition economics across UK insurance. The UK insurtech sector is registering an extraordinary growth trajectory, catalysed by regulatory sandbox support from the FCA and sustained venture investment in AI-powered claims, pay-per-use cover, and embedded distribution platforms. AXA UK signed a five-year exclusive distribution agreement with Lloyds Banking Group, effective from May 2025, enabling insurance solutions to reach Lloyds' 28 million customers, a landmark example of the embedded distribution partnerships reshaping UK insurance market trends.

Growing Private Health Insurance Demand Driven by NHS Capacity Constraints

Sustained pressure on NHS capacity is structurally accelerating private health insurance adoption across both individual and employer-sponsored channels. NHS England reported 7.39 million treatment pathways awaiting care in September 2025, with only 61.8% of patients waiting within the 18-week constitutional standard, compelling households and employers to invest in parallel private medical access. Analysis of the latest PHIN data by Broadstone, a UK-based consultancy, indicated that 338,000 treatments were funded through Private Medical Insurance (PMI) in the first half of 2025, marking the highest number of first-half treatments recorded to date, as health insurers expand product lines covering oncology, mental health, and outpatient diagnostics to meet escalating consumer demand.

- Embedded Insurance Expansion: Distribution partnerships between insurers, banks, retailers, and mobility platforms are embedding coverage at the point of purchase, reducing acquisition costs and expanding policy penetration in previously underserved demographics.

- Climate Risk Repricing in Property Lines: Increasing flood events, storm damage, and climate-driven claims inflation are compelling UK home and commercial property insurers to reprice risk, invest in catastrophe modelling, and adjust coverage terms in high-risk areas.

Growth Drivers

Rising Consumer Demand for Protection Products Across Life and Non-Life Segments

Increasing awareness of financial vulnerability, driven by economic uncertainty, rising living costs, and growing exposure to cyber, climate, and health risks, is structurally expanding demand for both life and non-life protection products across UK demographics. Individual annuity sales at Aviva grew by 32% in Q1 2025 as rising interest rates enhanced annuity attractiveness for retirees, as employers and individuals increasingly prioritize private medical access. This broadening protection gap awareness is a primary structural driver of UK insurance market growth.

Lloyd's of London Marketplace Driving Global Specialty Insurance Premium Growth

Lloyd's of London remains the world's pre-eminent specialty insurance and reinsurance marketplace, directly generating significant premium volumes that underpin the UK market's outsized position relative to national GDP. Lloyd's gross written premium rose to 32.5 billion pounds in the first half of 2025, up from 30.6 billion pounds a year earlier, with return on capital reaching 20.7%, reflecting sustained pricing adequacy and expanding appetite for catastrophe, cyber, marine, and aviation risks. Market capacity is growing as private equity, family offices, and institutional investors allocate capital to the marketplace's high-return, low-correlation risk profile.

Bulk Purchase Annuity Volumes Expanding Life Insurance Premium Base

The UK defined-benefit pension de-risking market is generating substantial bulk purchase annuity (BPA) volumes as corporate pension trustees seek to transfer longevity and investment risk to life insurers following exceptional 2024 conditions enabled by the Solvency UK regime. Life insurers, including Aviva, Legal & General, and Prudential, are competing aggressively for BPA mandates, with high interest rates having improved scheme funding positions to levels that make insurance buy-outs economically viable for a historically large proportion of corporate pension schemes simultaneously. These de-risking flows are embedding multi-year premium revenue commitments into life insurers' books, reinforcing the UK insurance market forecast.

- UK Aging Population and Annuity Demand: The UK's 12.5 million people aged 65 and over represent a structurally growing market for retirement income products, long-term care insurance, and equity release solutions tied to life insurance products.

- Telematics and Usage-Based Insurance Adoption: Telematics motor policies are attracting young and low-mileage drivers with personalized, data-driven pricing, expanding overall market participation while improving underwriting profitability for insurers.

Market Restraints

Claims Inflation and Persistent Cost Pressures: The UK non-life insurance sector experiences ongoing claims inflation through its motor, property, and liability insurance sectors because labor shortages affect vehicle repair, construction, and healthcare services. The combination of rising material expenses and extended supply chain networks results in higher average claim payouts, which decrease operating ratios while creating difficulties for managing personal line premiums because price comparison websites increase market competition.

Regulatory Complexity and Consumer Duty Compliance Burden: The FCA's developing Consumer Duty framework, together with Solvency UK implementation requirements, results in insurers facing heavy compliance obligations, which involve total product governance changes, mandatory disclosure improvements, and continuous fair value evaluations. The smaller insurers, together with mid-tier insurers, experience compliance costs that exceed their revenue base, creating barriers that prevent them from introducing new products and limit their ability to compete with large companies that dominate distribution channels in retail business operations.

Catastrophe Exposure and Climate-Driven Underwriting Uncertainty: The increasing occurrence and intensity of weather events in the UK, which include flooding, storms, and subsidence, create underwriting challenges and unpredictable claims costs for both home and commercial property insurance. The challenge of accurately modelling future climate risks under changing atmospheric conditions complicates long-term product pricing and reserving adequacy and reinsurance treaty structuring for property-focused insurers.

UK Insurance Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Non-life Insurance | 52.4% | 2025 |

| Region | London | 20.5% | 2025 |

Type Insights

Access the comprehensive market breakdown Request Sample

Non-life Insurance - 52.4% Market Share (2025) | Leading Type

The motor insurance sector in UK is the largest individual non-life insurance sub-segment, with more than 44 million motor insurance policies being sold across the country in 2024, generating total premiums exceeding 20 billion pounds. The average comprehensive motor premium reached £589 in Q1 2025, supported by strong pricing adequacy following the industry's most profitable year since 2020 in 2024. Aviva's UK and Ireland general insurance premiums grew 17% to 6.7 billion pounds, reflecting the combined effect of the Direct Line acquisition and strong underlying commercial and personal lines growth.

Commercial and specialty non-life lines are growing rapidly, underpinned by rising cyber insurance demand, supply chain liability coverage, and D&O insurance as businesses navigate complex operating environments. Fire and property insurance is expanding alongside climate-risk repricing. Liability insurance for professional services, public sector bodies, and large corporates is growing as litigation exposure increases. Lloyds of London's specialty marketplace, contributing 32.5 billion pounds in GWP (gross written premium) in HY 2024, is the largest single contributor to UK non-life premium volumes from its global risk portfolio.

|

Segment Breakdown · Non-life Insurance (52.4%)- (Automobile Insurance, Fire Insurance, Liability Insurance, Others) · Life Insurance |

Regional Insights

London - 20.5% Market Share (2025) | Leading Region

London leads the UK insurance market by a clear margin since it combines two unique assets, which are the world's most important specialty insurance marketplace, Lloyd's of London, and the UK's largest consumer insurance market. The geographic distribution of Lloyd's syndicates, managing agents, brokers, and multinational insurance companies, which includes AXA UK, Aviva, Zurich, and Allianz, shows why London holds its dominant market position. The commercial insurance system of London produces insurance premium levels that no other area of the United Kingdom can match. The Lloyd's market capacity has grown from approximately 2.7 billion pounds in 2016 to 5 billion pounds in 2025, as institutional capital, private equity, and family offices scale their Funds at Lloyd's allocations.

|

Regional Breakdown London (20.5%) · South East · North West · East of England · South West · Scotland · West Midlands · Yorkshire and The Humber · East Midlands · Others |

South East:

The South East serves as the UK's most populated area, which exists beyond London, while it generates the second largest insurance premium revenue throughout the country. The area generates demand for motor insurance, home insurance, commercial insurance, and private health insurance due to its high household incomes and residential property values, extensive commuter population, and dense network of small and medium-sized enterprises. Aviva established its main operational centers in Surrey and Hampshire, but the FCA reported that the South East region had the highest rate of optional contents and combined buildings insurance policy purchases because most residents in the area owned homes and valued their property.

North West:

The North West region, which includes Greater Manchester and Liverpool, serves as an important market area for both personal and business insurance products. The manufacturing revival, professional services expansion, and e-commerce logistics growth in Greater Manchester create complex insurance requirements for commercial liability, property, and fleet protection. The region experiences higher motor insurance costs because urban density levels, traffic flow rates, and increasing repair expenses raise risk assessment factors. The Manchester area has become a growing UK insurtech center because its companies develop data analytics and claims technology solutions that create AI-powered underwriting systems for regional brokers and mid-sized insurance companies.

Scotland:

Scotland presents a unique insurance market that operates under different legal standards and handles specific weather and geographic risks, while all financial services activities take place in Edinburgh, which serves as the base for major life and pensions operations. The operations of Scottish Widows, which belongs to Lloyds Banking Group, and Standard Life, which operates under abrdn, will handle significant assets, which include long-term savings and life insurance products. The offshore wind and energy sector in Scotland creates increasing needs for commercial insurance specializations, while the Port of Nigg and Cromarty Firth serve as key logistics centers for the production and installation of offshore wind components, which need marine and engineering insurance protection.

Market Outlook 2026-2034

What is the future outlook of the UK insurance market?

The UK insurance market is expected to sustain steady revenue growth through 2034.

The UK insurance market is structurally positioned for durable, above-average growth through 2034, supported by deepening private health insurance penetration, continued Lloyd's specialty premium expansion, bulk purchase annuity volume growth, and widespread digital distribution adoption, accelerating consumer policy access. Regulatory modernization under Solvency UK and the FCA Consumer Duty will progressively improve product quality and capital efficiency, enabling insurers to expand both product scope and customer reach. The convergence of rising risk awareness, climate-driven insurance demand, and an aging demographic base will sustain the UK insurance market outlook as one of Europe's most resilient and highest-quality growth opportunities through the forecast period.

UK Insurance Market - Leading Key Players

The UK insurance market is served by a tiered competitive landscape combining global composite insurers, specialist Lloyd's market operators, and domestic life and non-life leaders. Leading players are investing heavily in digital claims automation, AI-powered underwriting, product innovation in health and protection, and strategic acquisitions to consolidate market share and expand customer relationships across increasingly data-driven distribution channels.

| Company | Leading Brands | Highlights |

|---|---|---|

| Aviva plc | Aviva, Direct Line (acquired July 2025), RAC Insurance | UK's largest composite insurer, Aviva, completed a 3.7 billion pound acquisition of Direct Line Insurance Group in July 2025; insurance premiums grew 17% to 6.7 billion pounds. |

| Lloyd's of London | Various syndicates (Probitas, Nephila, Convex, Fidelis) | World's premier specialty insurance marketplace; GWP 32.5bn pounds in H1 2024; market capacity grown from 2.7bn pounds in 2016 to 5bn pounds in 2025 |

| AXA UK (AXA S.A.) | AXA Insurance, AXA Health, AXA Commercial | Signed a 5-year exclusive distribution deal with Lloyds Banking Group, effective May 2025, to serve 28 million customers; strong commercial lines and health insurance franchise |

Some of the existing key players in the UK Insurance Market are Legal & General Group Plc, Admiral Group plc, RSA Insurance Group (Intact Financial)¸Zurich Insurance Group Ltd, Allianz Insurance plc, etc.

Latest Development & News

- In July 2025, Aviva completed a 3.7 billion pound acquisition of Direct Line Insurance Group in July 2025, creating the UK's largest composite motor and home insurer. In November 2025, Aviva confirmed it expects to deliver a full-year 2025 group operating profit of approximately 2.2 billion pounds, incorporating six months of Direct Line's contribution.

- In May 2025, AXA UK commenced its 5-year exclusive distribution partnership with Lloyds Banking Group, agreed in December 2024, enabling AXA's insurance products to be offered to Lloyds' 28 million customers across the UK. The bancassurance partnership represents one of the largest embedded distribution agreements in UK insurance history, extending AXA's retail reach into home, travel, and protection products through Lloyds' branch network, digital platforms, and telephone channels.

- In December 2024, Ageas reached an agreement to acquire Saga's Acromas Insurance Company alongside a 20-year over-50s distribution alliance granting Ageas exclusive access to Saga's customer base for home and motor insurance. The transaction strengthens Ageas's position as a leading UK home and motor insurer and provides direct, long-term access to the premium over-50s market segment, which commands above-average policy retention and higher sum-insured property and vehicle cover values.

UK Insurance Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

| Regions Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the UK insurance market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the UK insurance market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the UK insurance industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the UK Insurance Market Report

The UK insurance market was valued at USD 476.2 Billion in 2025.

The UK insurance market is anticipated to reach a value of USD 895.1 Billion by 2034.

Non-life insurance dominates the market with a share of 52.4%, driven by growing commercial liability and property insurance demand, and Lloyd's of London's global specialty premium volumes that collectively anchor the non-life segment's leading position in the UK market.

Some of the major players in the UK insurance market include Aviva plc, Lloyd's of London, AXA UK (AXA S.A.), Legal & General Group Plc, Admiral Group plc, RSA Insurance Group (Intact Financial), Zurich Insurance Group Ltd, Allianz Insurance plc, etc.

Key trends include Aviva's landmark 3.7 billion pounds Direct Line acquisition driving market consolidation, the rapid expansion of embedded insurance distribution through bancassurance and fintech partnerships, accelerating private health insurance uptake driven by NHS capacity constraints with 7.39 million treatment pathways awaiting care in September 2025, Lloyd's specialty market digital transformation under Blueprint Two, and climate-driven repricing in UK home and commercial property lines.

London currently leads the UK insurance market, accounting for a share of 20.5%. The region's dominance is driven by Lloyd's of London's global specialty marketplace alongside the capital's concentration of multinational insurer headquarters, high-value commercial risks, and the UK's most affluent consumer market.

Growth is driven by Lloyd's of London specialty premium expansion with market capacity growing from £2.7 billion in 2016 to £5 billion in 2025, record bulk purchase annuity volumes as pension de-risking accelerates under Solvency UK, rising private health insurance demand as NHS waiting lists surpass 7.39 million pathways, and landmark M&A activity creating scale-driven composite insurers with expanded distribution reach.

Key challenges include persistent claims inflation across motor and property lines driven by vehicle repair costs and construction labour shortages, significant regulatory compliance burden from FCA Consumer Duty and Solvency UK implementation, growing climate risk exposure increasing underwriting uncertainty in home and commercial property lines, and intensifying competition from digital price comparison platforms and insurtech disruptors compressing margins in personal lines retail insurance.

Recent developments include Aviva completing its 3.7 billion pounds Direct Line acquisition in July 2025, AXA UK launching its exclusive distribution partnership with Lloyds Banking Group's 28 million customers in May 2025, and Ageas acquiring Saga's Acromas Insurance with a 20-year distribution alliance targeting the high-value over-50s customer segment in December 2024.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade