Brazil Fertilizers Market Size, Share, Trends and Forecast by Type, Form, Application Mode, Crop Type, and Region, 2026-2034

Brazil Fertilizers Market Size, Share, Trends & Forecast (2026-2034)

The Brazil fertilizers market reached USD 3.31 Billion in 2025 and is projected to reach USD 6.02 Billion by 2034, growing at a CAGR of 6.86% during 2026-2034. Growing agricultural production driven by soybean, corn, and sugarcane export demand, supportive government incentives, expanding cultivated land across the MATOPIBA frontier, and increasing adoption of specialty fertilizers are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.31 Billion |

|

Forecast Market Size (2034) |

USD 6.02 Billion |

|

CAGR (2026-2034) |

6.86% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

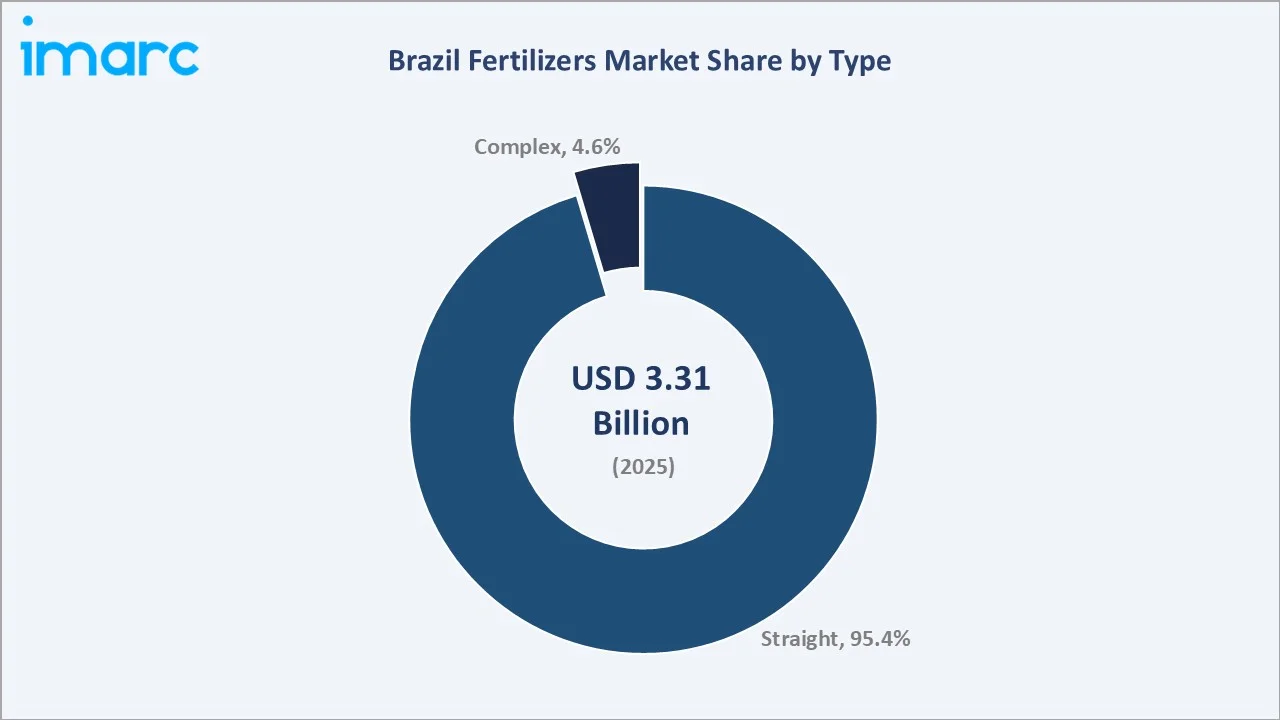

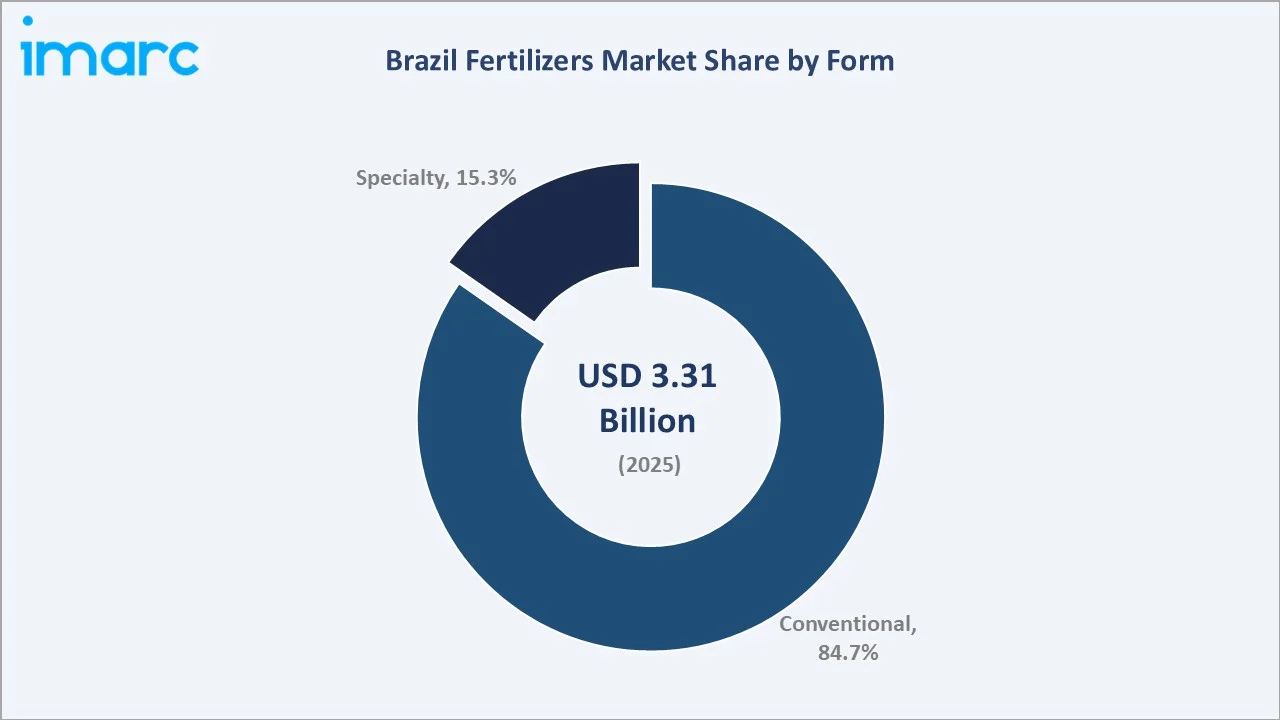

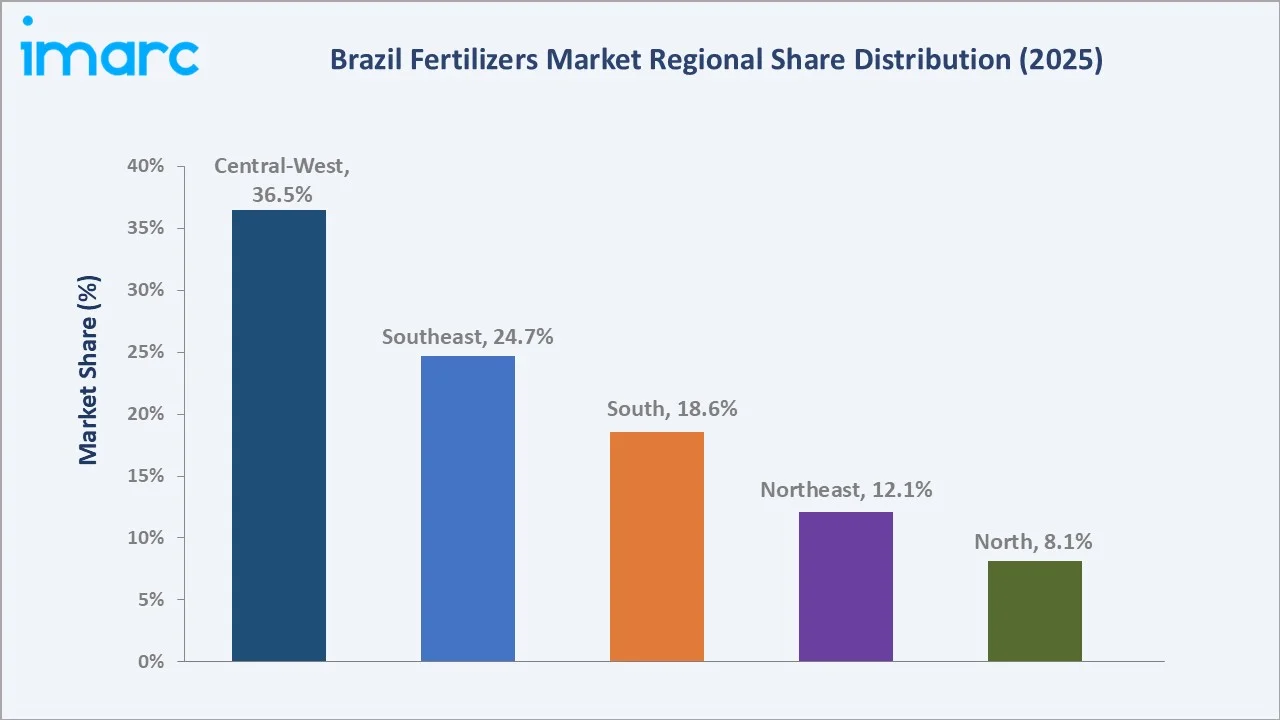

Straight fertilizers dominate with a 95.4% share in 2025, while conventional form fertilizers account for 84.7% of the market. The Central-West region leads with a 36.5% share, anchored by Brazil's most intensive soybean and grain farming activity.

To get more information on this market, Request Sample

Brazil's fertilizers market is underpinned by three structural forces: Brazil's position as the world's largest soybean exporter sustaining intensive fertilizer application, a critical 80%+ import dependency creating domestic production expansion imperatives, and the progressive shift from bulk conventional fertilizers toward precision-applied specialty and controlled-release formulations that optimize nutrient use efficiency in Brazil's diverse soil types.

Executive Summary

The Brazil fertilizers market is experiencing strong, agriculture-led expansion, driven by the world's most intensive commodity crop export economy and increasing adoption of yield-optimizing specialty inputs. The market was valued at USD 3.31 Billion in 2025 and is forecast to reach USD 6.02 Billion by 2034, growing at a CAGR of 6.86%. This robust growth trajectory is supported by Brazil's structural agricultural expansion, government-backed domestic fertilizer production incentives, and the accelerating premiumization of the specialty and controlled-release fertilizer segment.

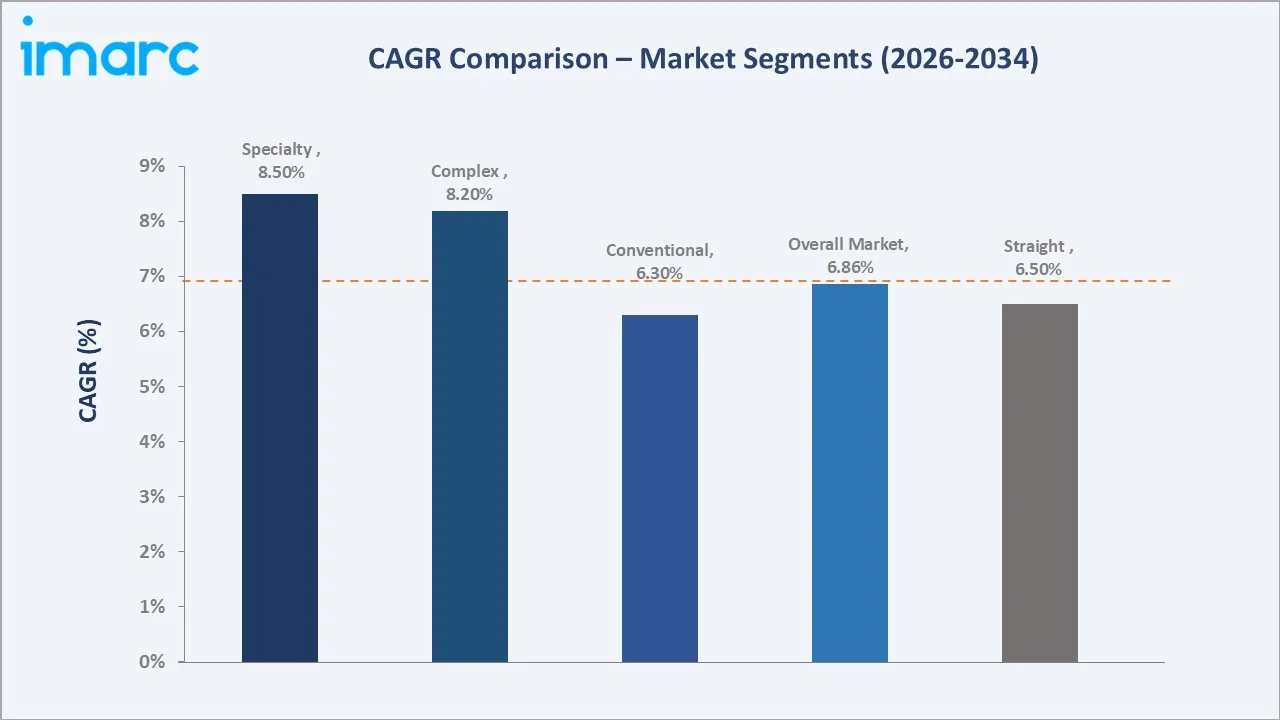

Straight fertilizers dominate with a 95.4% share in 2025, reflecting the dominance of single-nutrient nitrogen, phosphate, and potash applications across Brazil's large-scale commodity farming operations. However, complex fertilizers at 4.6% are growing at the fastest rate (~8.2% CAGR), driven by precision nutrition demand from high-value and export-oriented farmers.

On the form front, conventional fertilizers lead at 84.7%, while specialty fertilizers at 15.3% are the fastest-growing form (~8.5% CAGR), driven by controlled-release and water-soluble product adoption in the horticulture, sugarcane, and premium export crop segments. The Brazil fertilizers market outlook remains strongly positive through 2034, reinforced by agricultural frontier expansion and domestic production development.

Key Market Insights

|

Insight |

Data |

|

Largest Fertilizer Type |

Straight – 95.4% share (2025) |

|

Fastest Growing Type |

Complex (~8.2% CAGR, 2026-2034) |

|

Largest Form |

Conventional – 84.7% share (2025) |

|

Fastest Growing Form |

Specialty (~8.5% CAGR, 2026-2034) |

|

Leading Region |

Central-West – 36.5% share (2025) |

|

Top Companies |

Yara, Mosaic, Haifa Group, and K+S Aktiengesellschaft |

Key Analytical Observations Supporting the Above Data:

- Straight fertilizers at 95.4% dominate due to their affordability, established supply chains, and straightforward application compatibility with large-scale soybean, corn, and sugarcane operations.

- Complex fertilizers at 4.6% are growing fastest at ~8.2% CAGR as precision farming adoption in the Cerrado and São Paulo corridors drives demand for multi-nutrient blends tailored to specific soil profiles.

- Specialty form at 15.3% is growing at ~8.5% CAGR, the fastest among all form segments, driven by controlled-release fertilizer adoption (CRF) in water-stressed and labor-constrained farming environments.

- Central-West at 36.5% reflects the concentration of Brazil's soybean and grain production in Goiás state, which accounts for an average yield of 4.12 mt/ha in MY 2024/25. These states also exhibit the highest fertilizer application intensity, making them the critical demand engine for the national market.

Brazil Fertilizers Market Overview

Fertilizers in Brazil encompass all nitrogen, phosphate, potash, and micronutrient inputs, whether straight, complex, conventional, or specialty, applied across the country's cultivated agricultural land. Brazil is simultaneously the world's largest soybean exporter, third-largest corn producer, and largest sugarcane producer, creating structural and persistent demand for high-volume fertilizer inputs. The market reached USD 3.31 Billion in 2025, growing from USD 2.38 Billion in 2020.

Brazil's fertilizer market is uniquely characterized by 77% and 85% import dependency for its NPK inputs; the country lacks domestic potash production at scale and depends on Russia, Canada, and Belarus for potash, Morocco and Jordan for phosphate, and Russia and the Middle East for nitrogen feedstocks. This dependency creates supply security imperatives that are shaping government investment in domestic production expansion, particularly through Petrobras's plans to restart dormant urea and ammonia plants by 2029.

According to the Brazilian Association of Plant Nutrition Technology (Abisolo), revenues from specialty fertilizers in Brazil reached BRL 26.9 Billion in 2024, marking an 18.9% year-over-year increase, reflecting the broader market's dynamism. The Brazil fertilizers market size is projected to grow to USD 4.61 Billion by 2030 and USD 6.02 Billion by 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

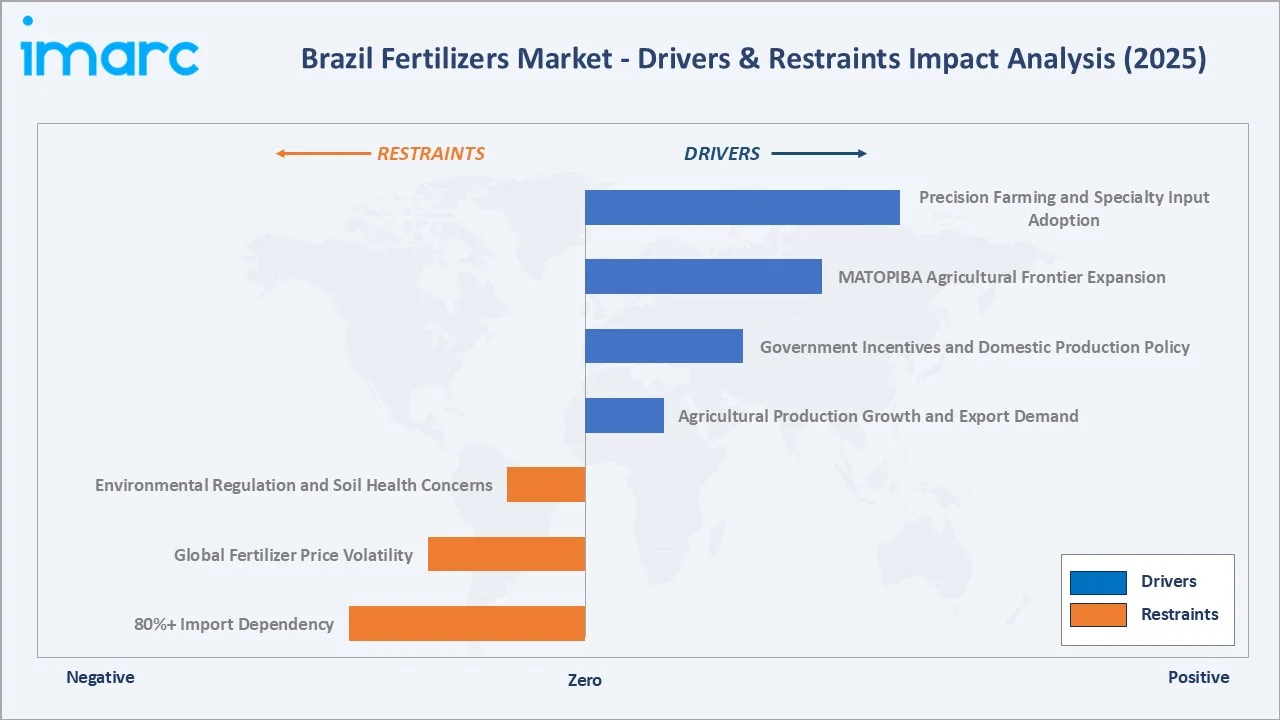

Market Drivers

- Agricultural Production Growth and Export Demand: Brazil's commodity agriculture sector, producing over 160 million tons of soybeans and corn annually, is the primary demand engine for fertilizers. Record soybean harvests and expanding corn double-cropping across the Cerrado create sustained, high-volume NPK demand.

- Government Incentives and Domestic Production Policy: Brazil's National Fertilizer Plan (Plano Nacional de Fertilizantes, PNF), launched in 2022, targets reducing import dependency from 85% to 45% by 2050 through domestic production capacity expansion, regulatory simplification, and infrastructure investment.

- MATOPIBA Agricultural Frontier Expansion: The MATOPIBA region (Maranhão, Tocantins, Piauí, and Bahia) represents Brazil's most rapidly expanding agricultural frontier, with soybean cultivation growing at 8–12% annually in some municipalities. As new land is converted from Cerrado savanna to commodity farmland, first-time fertilizer application requirements create incremental demand volumes that directly contribute to the market's above-GDP growth rate.

- Precision Farming and Specialty Input Adoption: Growing availability of soil mapping technology, variable-rate application equipment, and agronomic data services is enabling Brazilian farmers to optimize fertilizer placement and timing, driving the shift from bulk straight applications toward premium controlled-release and water-soluble specialty formulations.

Market Restraints

- 80%+ Import Dependency: Brazil's structural dependence on imported potash (predominantly from Russia, Canada, and Belarus), imported phosphate rock, and imported nitrogen feedstocks creates exposure to geopolitical supply disruptions.

- Global Fertilizer Price Volatility: Fertilizer prices in Brazil are highly sensitive to global commodity market movements, natural gas pricing (which drives urea production costs), and shipping freight rates. Price volatility creates procurement uncertainty for farmers, incentivizes bulk purchasing and stock-building behaviors that distort demand signals.

- Environmental Regulation and Soil Health Concerns: Growing regulatory and public scrutiny around fertilizer runoff, soil acidification, and water quality impacts in Brazil's agricultural watersheds is creating pressure for more sustainable application practices. Stricter nutrient management regulations at the state level and EU deforestation and environmental due diligence import regulations for Brazilian commodities are indirectly raising compliance costs for fertilizer-intensive production systems.

Market Opportunities

- Domestic Production Capacity Development: In January 2026, Petrobras announced that it is close to fully restarting fertilizer production at its Bahia and Sergipe plants, which together could supply about 12% of Brazil’s urea demand.

- Controlled-Release and Biostimulant Fertilizers: The specialty fertilizer segment, including controlled-release (CRF), slow-release (SRF), water-soluble, and biostimulant-enhanced formulations, is growing at 8.5% CAGR, nearly double the overall market rate. Investment in CRF production capacity (as demonstrated by Haifa Group's Uberlândia plant launch in February 2025) and biostimulant-fertilizer combinations targeting Brazil's high-value horticulture and export crop segments offer premium margin opportunities.

Market Challenges

- Infrastructure Bottlenecks and Logistics Costs: Brazil's challenging logistical inefficiencies, inadequate rail coverage, poor road conditions in interior agricultural states, and port congestion at Santos and Paranaguá add 15–25% to fertilizer delivered cost compared to peer agricultural exporters.

- Currency and Macroeconomic Volatility: Brazil's Real (BRL) has experienced significant volatility relative to the USD, materially impacting the import cost of fertilizers priced in USD. Currency depreciation episodes directly increase the BRL cost of fertilizer procurement for farmers, compressing margins and occasionally triggering demand contraction in price-sensitive commodity crop segments.

Emerging Market Trends

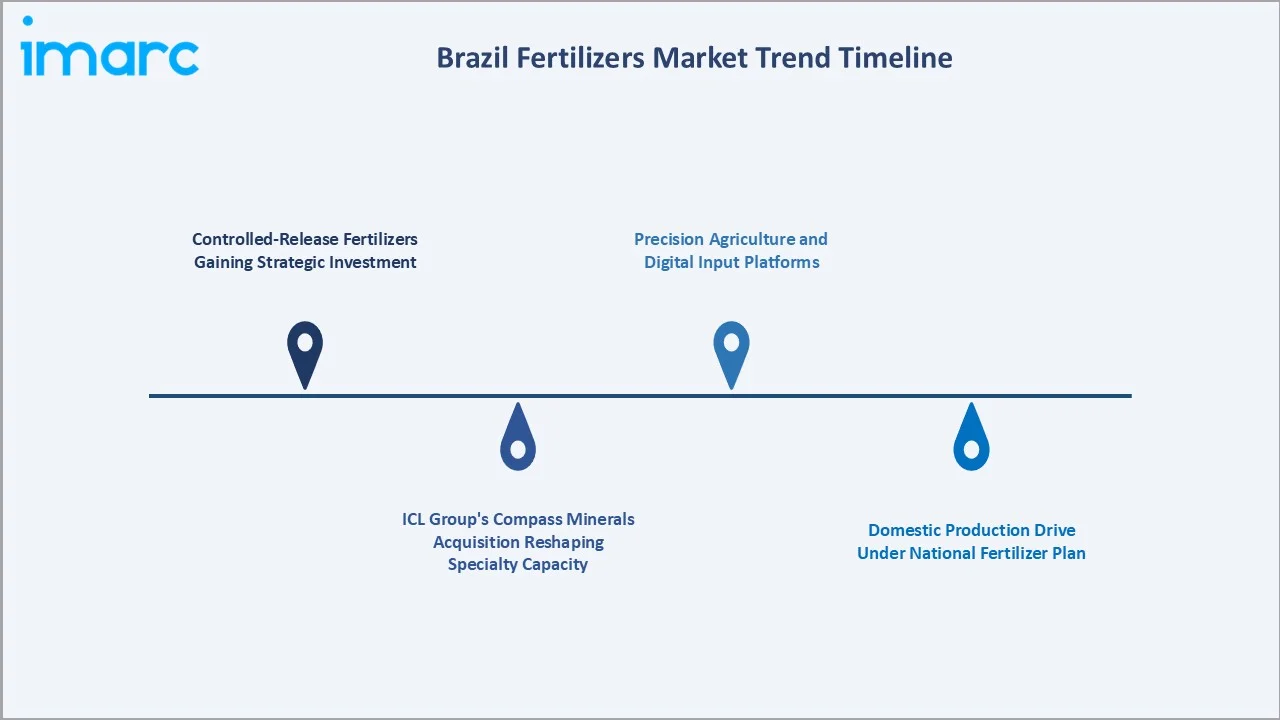

1. Controlled-Release Fertilizers Gaining Strategic Investment

In March 2025, Haifa Group received investment approval to expand production of its biodegradable coating technology for controlled-release fertilizers, supporting compliance with upcoming European environmental regulations. The investment aims to accelerate large-scale commercialization of sustainable fertilizer solutions while strengthening Haifa’s position in specialty plant nutrition.

2. ICL Group's Compass Minerals Acquisition Reshaping Specialty Capacity

ICL Group completed the USD 420 million acquisition of Compass Minerals' South American plant nutrition business, instantly doubling ICL's specialty fertilizer capacity in Brazil. This deal signals institutional confidence in Brazil's specialty segment trajectory and reshapes the competitive landscape by creating a more formidable third-force challenger to Yara and Mosaic's dominant positions.

3. Domestic Production Drive Under National Fertilizer Plan

Brazil's National Fertilizer Plan (PNF) is catalyzing domestic production investment across the nitrogen, phosphate, and potash sub-chains. In May 2025, Yara debuted YaraBasa TURBO at the 30th Agrishow in São Paulo, a fertilizer specifically formulated for Brazilian crop and soil requirements, reflecting the localization of product development for Brazil's unique Cerrado and tropical soil chemistry.

4. Precision Agriculture and Digital Input Platforms

In December 2025, Nissan Chemical Corporation acquired a stake in Brazilian biotech firm Innova Agrotecnologia to expand its biological crop protection business across Latin America. The partnership focuses on advanced biological technologies, including microbial-based crop protection and bio-input solutions designed to improve agricultural productivity sustainably.

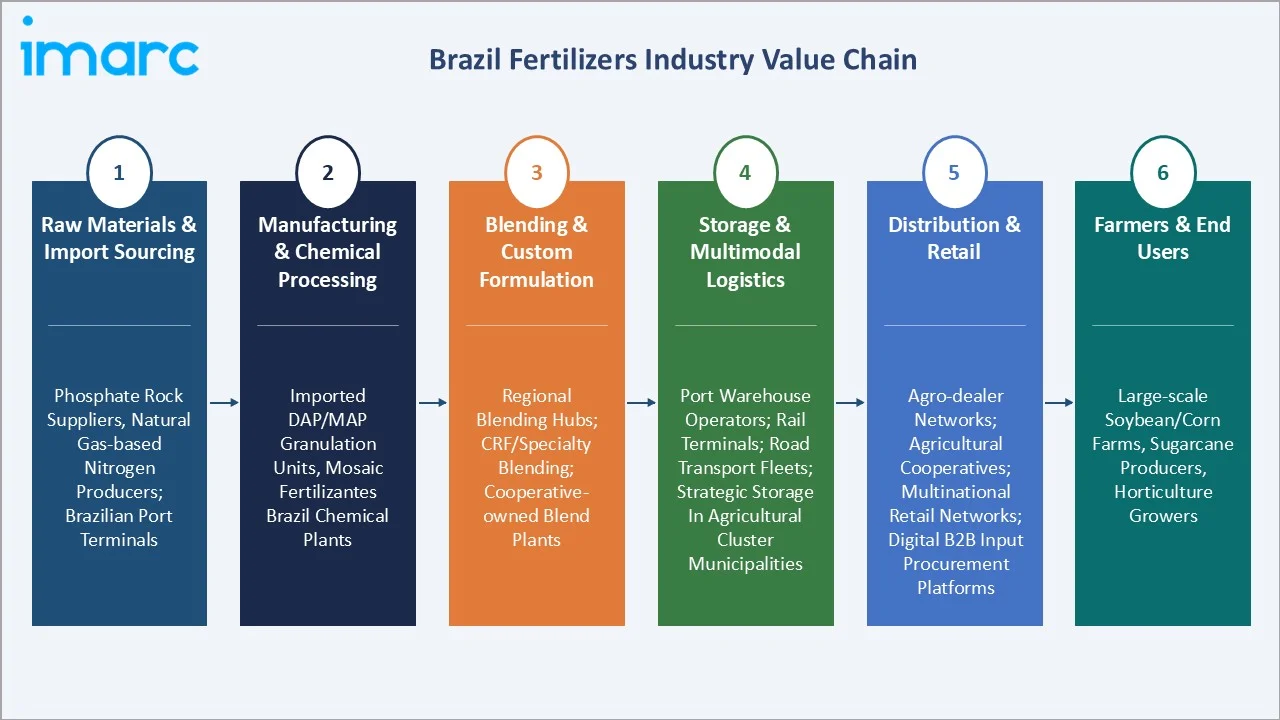

Industry Value Chain Analysis

Brazil's fertilizer value chain spans from raw material extraction and international sourcing through manufacturing, blending, and multi-modal distribution to farm-level application. Brazil's unusual combination of massive scale, remote agricultural geography, and import-dependent supply structure creates a distinctively complex and logistics-intensive value chain.

|

Stage |

Key Players / Examples |

|

Raw Materials & Import Sourcing |

Phosphate rock suppliers, natural gas-based nitrogen producers; Brazilian port terminals |

|

Manufacturing & Chemical Processing |

Imported DAP/MAP granulation units; Mosaic Fertilizantes Brazil chemical plants |

|

Blending & Custom Formulation |

Regional blending hubs; specialized CRF/specialty blending; cooperative-owned blend plants |

|

Storage & Multimodal Logistics |

Port warehouse operators; rail terminals; road transport fleets; strategic storage in agricultural cluster municipalities |

|

Distribution & Retail |

Agro-dealer networks; agricultural cooperatives; multinational retail networks; digital B2B input procurement platforms |

|

Farmers & End Users |

Large-scale soybean/corn farms, sugarcane producers, horticulture growers |

Technology Landscape in the Brazil Fertilizers Industry

Controlled-Release Fertilizer (CRF) Technology

Polymer-coated granule technology, in which a semi-permeable membrane regulates nutrient release in response to soil temperature and moisture, can reduce nitrogen loss through leaching and volatilization by up to 50% compared to conventional urea, directly improving fertilizer use efficiency and reducing environmental impact in Brazil's tropical, high-rainfall farming environments.

Precision Agriculture and Variable-Rate Application Technology

Variable-rate technology (VRT) systems, combining GPS-guided application equipment, georeferenced soil sampling grids, and digital prescription maps, are enabling Brazil's large-scale Cerrado farming operations to apply fertilizers at spatially optimized rates that match soil nutrient variability across individual farm paddocks. Precision application equipment can achieve application rate accuracy within 2–3% of prescription targets, reducing input waste and improving yield response homogeneity across variable soil profiles.

Soil Mapping, Remote Sensing and Data Analytics

Brazil's agricultural sector has embraced satellite and drone-based remote sensing as foundational technologies for soil nutrient mapping and fertilizer prescription optimization. The convergence of high-resolution soil data, real-time crop monitoring, and AI-based recommendation engines is enabling Brazilian agronomists to move from reactive to predictive fertilizer management, progressively closing the yield gap between actual and potential farm productivity.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Straight |

95.4% |

2025 |

|

Form |

Conventional |

84.7% |

2025 |

|

Application Mode |

🔒 |

🔒 |

2025 |

|

Crop Type |

🔒 |

🔒 |

2025 |

|

Region |

Central-West |

36.5% |

2025 |

By Type

Straight fertilizers dominate with a commanding 95.4% share in 2025. This segment encompasses single-nutrient inputs, urea (N), MAP/DAP (P), and KCl/K2SO4 (K), which form the primary nutrition inputs for Brazil's cultivated land. Their dominance reflects the scale economics of bulk NPK procurement for commodity farming, the compatibility of straight fertilizers with Brazil's cooperative blending infrastructure, and their established integration into credit financing programs for commodity crop production.

To access detailed market analysis, Request Sample

Complex fertilizers hold 4.6% of the market in 2025 but are growing at the fastest rate (~8.2% CAGR). This segment includes NPK blends, multi-nutrient compound formulations, and specialty complex products targeted at specific crop requirements and soil nutrient deficiencies. As Brazilian farmers increasingly access soil mapping data and agronomic consulting services, demand for customized complex blend prescriptions is growing rapidly across the Cerrado's iron-rich, acidic Oxisol soils.

By Form

Conventional fertilizers command a dominant 84.7% share in 2025. This form encompasses standard granular, prilled, and liquid fertilizers applied through broadcast spreading, incorporation, and basic fertigation systems. Conventional form dominance reflects the cost-sensitivity and scale of Brazil's commodity crop farming sector, where bulk application economics and established cooperative procurement systems favor standardized conventional product formats over premium specialty alternatives.

Specialty fertilizers at 15.3% are growing at the fastest rate (~8.5% CAGR), outpacing the overall market growth of 6.86%. This form encompasses controlled-release fertilizers (CRF), slow-release fertilizers (SRF), water-soluble fertilizers for fertigation, and biostimulant-enhanced specialty formulations. Haifa Group's Uberlândia Multicote blending/mixing unit launch in February 2025 signals a structural supply-side investment cycle in Brazil's specialty form segment.

Regional Market Insights

The Central-West region commands 36.5% of the national market in 2025, reflecting the concentration of Brazil's most intensive commodity grain production in Mato Grosso, Goiás, and Mato Grosso do Sul states. This region hosts the Cerrado's most productive agricultural lands, with Mato Grosso producing 85.7 million tons of soybeans during the 2023/2024 harvest season alone, and consequently representing the single largest sub-national fertilizer demand cluster in South America.

The Southeast at 24.7% is anchored by São Paulo's massive sugarcane belt and citrus production, combined with Brazil's most advanced precision agriculture adoption. The South at 18.6% encompasses Paraná and Rio Grande do Sul's strong cooperative-driven soybean, wheat, and tobacco production systems.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Central-West |

36.5% |

Brazil's leading soybean and corn belt; highest fertilizer intensity per hectare; major port terminal access. |

|

Southeast |

24.7% |

High sugarcane and citrus production; advanced precision farming adoption; largest fertilizer blending and distribution; Domestic fertilizer production base. |

|

South |

18.6% |

Soybean, wheat, and tobacco production; high cooperative-driven input procurement; strong specialty and controlled-release fertilizer adoption. |

|

Northeast |

12.1% |

MATOPIBA expansion driving rapid agricultural frontier growth; increasing irrigation-based agriculture; growing demand for targeted nutrient management. |

|

North |

8.1% |

Early-stage agricultural development; Amazon watershed expansion; government programs supporting smallholder and medium-scale farming with subsidized input access and extension services. |

The Northeast at 12.1% is the fastest-growing region driven by MATOPIBA agricultural frontier expansion. The North at 8.1% represents early-stage agricultural development with significant long-term potential as infrastructure investment and environmental governance frameworks mature.

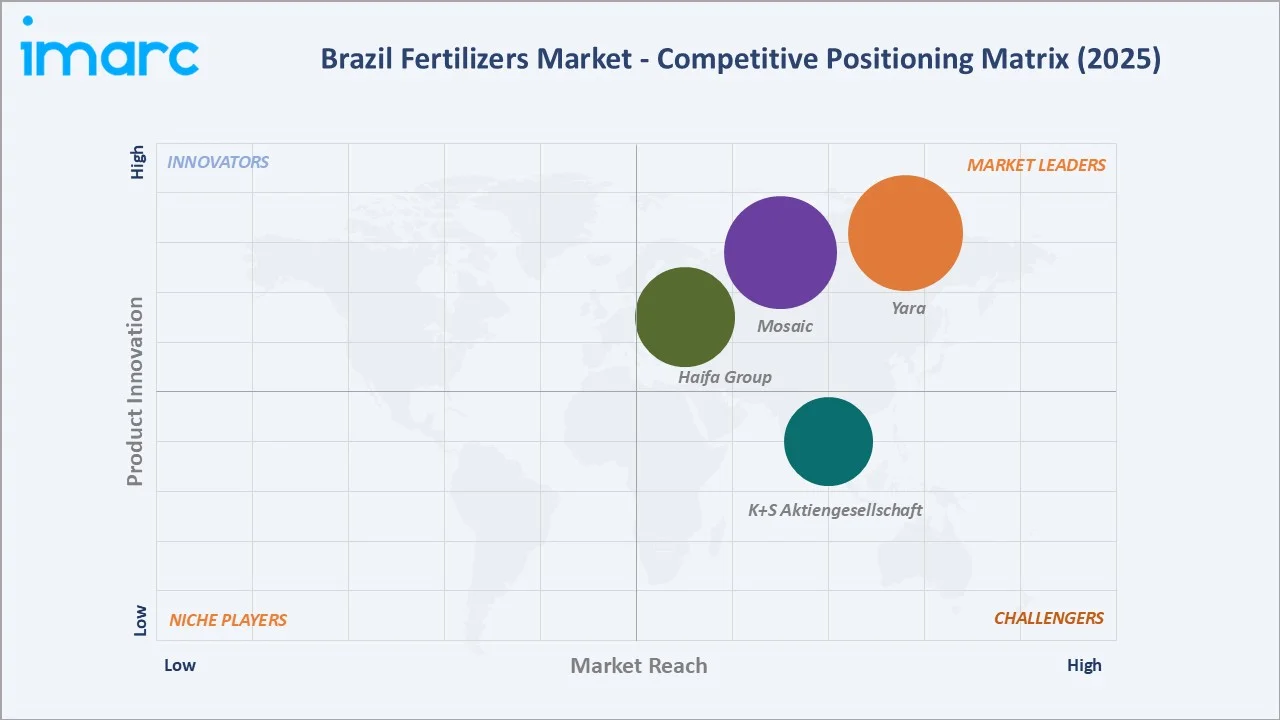

Competitive Landscape

Brazil's fertilizer market is moderately fragmented at the distribution tier but concentrated at the import, manufacturing, and specialty product tiers. According to Mordor Intelligence, the top companies, Yara, Mosaic, Haifa Group, and K+S Aktiengesellschaft, collectively hold approximately 30% of total market share in 2025, with the remaining 70% distributed among regional distributors, cooperatives, and smaller blending operations.

|

Company |

Brands |

Position |

Core Strength |

|

Yara |

YaraMila, YaraLiva, YaraVita, YaraRega, YaraTera, YaraBasa TURBO, YaraBela |

Market Leader |

Global nitrogen leader; broad distribution; crop nutrition agronomy services. |

|

Mosaic |

MicroEssentials, Pegasus, Aspire, Mosaic |

Market Leader |

One of the world's largest potash/phosphate producers; Mosaic Fertilizantes Brazil operations; Cerrado farming relationships. |

|

Haifa Group |

Fertigation / Nutrigation, Foliar Fertilizer, Haifa Micro, Haifa Turbo-K, Multicote |

Specialist Leader |

Launched Brazil's first foreign Multicote blending/mixing unit in Uberlândia; Multicote technology; high-value crop focus. |

|

K+S Aktiengesellschaft |

KALISOIL, KALISOLU |

Regional Challenger |

Chloride-free K specialty products; EU-export crop compliance solutions; water-soluble fertigation lines. |

Consolidation is accelerating through acquisition activity: ICL's Compass Minerals deal, Ihara's planned acquisition of Innova (March 2025), and Adufértil's acquisition of Fass Agro (September 2025) all reflect an intensifying M&A cycle reshaping Brazil's specialty fertilizer competitive structure. The Brazil fertilizers market share at the premium specialty tier is consolidating rapidly.

Key Company Profiles

Yara

Yara, headquartered in Oslo, Norway, is the world's leading nitrogen fertilizer company and one of Brazil's most significant fertilizer market participants. Yara Brazil operates an extensive distribution and blending network across all major Brazilian agricultural regions, offering both commodity nitrogen inputs and premium specialty crop nutrition solutions.

- Product Portfolio: YaraMila (NPK blends), YaraVita (foliar micronutrients), YaraBasa TURBO, YaraLiva, YaraRega, YaraTera, and YaraBela.

- Recent Developments: In November 2024, Yara delivered Brazil’s first batch of lower-carbon nitrogen fertilizer to Cooxupé, a major coffee cooperative in Minas Gerais, with up to 90% lower carbon footprint than fossil gas-based fertilizer.

- Strategic Focus: Brazil-specific product localization; digital precision agriculture integration; specialty crop nutrition growth in horticulture and sugarcane; sustainability and carbon footprint reduction programs aligned with Brazilian agri-export ESG requirements.

Mosaic

Mosaic, headquartered in Tampa, Florida, USA, is the world's largest producer of potash and phosphate fertilizers and operates Mosaic Fertilizantes do Brasil as its primary Brazilian market vehicle, the country's largest integrated fertilizer producer and distributor.

- Product Portfolio: MicroEssentials (premium phosphate micronutrient), Pegasus, Aspire, Mosaic, and agronomic consulting services.

- Recent Developments: In July 2025, Mosaic opened a new USD 84 million blending, storage, and distribution facility in Palmeirante, Tocantins, Brazil, with capacity to process 1 million tons of fertilizer annually.

- Strategic Focus: Vertical integration of Brazilian phosphate mining-to-distribution value chain; MicroEssentials premium penetration in yield-focused farming operations; digital agronomy service expansion through Mosaic Crop Nutrition advisory platform.

Market Concentration Analysis

Brazil's fertilizer market exhibits a bimodal concentration structure: the import, manufacturing, and port logistics tiers are dominated by a small number of multinational players controlling critical supply infrastructure, while the blending, distribution, and retail tiers are fragmented across hundreds of regional operators and agricultural cooperatives.

The top five companies collectively hold approximately 30% of total market revenue, leaving a highly competitive mid-market structure that sustains price competition in commodity segments while allowing specialty segment entrants to command premium positioning.

Consolidation is accelerating in 2024–2025 through a wave of M&A activity targeting specialty capacity: ICL's USD 420 million Compass Minerals acquisition and Adufértil's acquisition of Fass Agro's liquid fertilizer capabilities all reflect a strategic pivot toward capturing the higher-margin specialty segment before price competition intensifies.

Investment & Growth Opportunities

Fastest Growing Segments

Specialty fertilizers (~8.5% CAGR), complex fertilizer types (~8.2% CAGR), controlled-release formulations (~7.1% CAGR), and biostimulant-fertilizer combinations represent the highest-growth investment vectors through 2034. MATOPIBA agricultural frontier expansion offers greenfield fertilizer distribution and blending opportunities in underserved northeastern Cerrado municipalities.

Emerging Investment Themes

- Domestic Production Import Substitution: Government-supported investment in domestic nitrogen (urea/ammonia), phosphate, and potash production infrastructure offers strategic first-mover advantages for producers willing to commit capital ahead of the PNF's long-term trajectory.

- Precision Nutrition Service Platforms: Digital agronomy platforms integrating soil data, prescription fertilizer recommendations, and input financing are transforming fertilizer distribution from commodity supply toward high-value service businesses with recurring revenue streams.

- CRF and Specialty Capacity Investment: CRF production capacity expansion in Brazil, following Haifa's Uberlândia plant model, offers strong risk-adjusted returns in a segment growing at 8.5% CAGR with significant pricing premiums over commodity alternatives.

Future Market Outlook (2026-2034)

Brazil's fertilizer market is positioned for sustained, above-average growth through 2034, driven by structural agricultural expansion, specialty input premiumization, and domestic production development. From a base of USD 3.31 Billion in 2025, the market is projected to reach USD 6.02 Billion by 2034, representing total incremental value creation of USD 2.71 Billion at a CAGR of 6.86%.

The market's composition will evolve meaningfully. Straight fertilizer dominance (95.4%) will moderate as complex fertilizer share grows toward 8–10% by 2034. Specialty form fertilizers will expand from 15.3% to approximately 22–25% of total market value as premium input adoption accelerates. Central-West region will capture disproportionate growth as agricultural frontier expansion and irrigation investment mature.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 75 industry stakeholders in 2024–2025, including fertilizer distributors, agricultural cooperative procurement managers, large-scale farm operators, agronomists, government policy officials, and institutional investors across Mato Grosso, São Paulo, Paraná, and MATOPIBA states. Expert input validated market sizing, regional demand dynamics, and specialty fertilizer adoption trends.

Secondary Research

Secondary research encompassed Abisolo (Brazilian Association of Plant Nutrition Technology) annual reports, ANDA (National Association of Fertilizer Distributors) statistical databases, MAPA (Ministry of Agriculture) agricultural census data, Brazil Customs trade statistics, company annual reports (Yara, Mosaic, ICL), and trade publications (AgroEsfera, AgroLink, Canal Rural).

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating agricultural area expansion data, crop-specific fertilizer application rates, specialty segment premiumization trends, and domestic production development timelines. A base-case CAGR of 6.86% reflects consensus estimates validated against MAPA agricultural projections and fertilizer import-export trade data from 2020 to 2025.

Brazil Fertilizers Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

| Forms Covered |

|

| Application Modes Covered | Fertigation, Foliar, Soil |

| Crop Types Covered | Field Crops, Horticultural Crops, Turf and Ornamental |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | Yara, Mosaic, Haifa Group, K+S Aktiengesellschaft, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil fertilizers market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Brazil fertilizers market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil fertilizers industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Brazil Fertilizers Market Report

The Brazil fertilizers market reached USD 3.31 Billion in 2025, up from USD 2.38 Billion in 2020.

The market is projected to exhibit a CAGR of 6.86% during 2026-2034, reaching USD 6.02 Billion by 2034, supported by agricultural frontier expansion, specialty input adoption, and domestic production development under Brazil's National Fertilizer Plan.

The straight type dominates the Brazil fertilizers market with a share of 95.4% in 2025.

The conventional form dominates the Brazil fertilizers market with a share of 84.7% in 2025.

Growing agricultural production for soybean, corn, and sugarcane export, government incentives under the National Fertilizer Plan (PNF), precision farming adoption driving specialty input demand, and domestic production capacity development under import substitution policy are the primary growth drivers.

The Central-West region dominates the Brazil fertilizers market with a share of 36.5% in 2025. Its leadership reflects the concentration of Brazil's most intensive soybean and grain production in Mato Grosso, Goiás, and Mato Grosso do Sul.

The major players include Yara, Mosaic, Haifa Group, and K+S Aktiengesellschaft.

Complex fertilizers are the fastest-growing type at ~8.2% CAGR during 2026–2034. Growth is driven by precision nutrition adoption, soil-specific multi-nutrient blend demand in Cerrado agriculture, and increasing farmer awareness of micronutrient deficiencies in Brazil's iron-rich, acidic Oxisol soils.

Specialty fertilizers are driven by controlled-release product adoption in water-constrained and labor-constrained farming environments, precision soil mapping enabling prescription nutrition programs, and high-value horticulture and export crop segment demand.

Key challenges include Brazil's structural 80%+ fertilizer import dependency creating supply security and price volatility exposure, significant logistics cost burdens from inadequate rail and road infrastructure in interior agricultural states, and currency (BRL/USD) volatility.

Key investment opportunities include CRF and specialty fertilizer production expansion to capture the specialty segment growth, digital precision nutrition service platforms integrating data, and cooperative-aligned distributors as consolidation accelerates across Brazil's fragmented mid-market fertilizer supply chain.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)