Europe Adult Diaper Market Size, Share, Trends and Forecast by Type, Distribution Channel, and Country, 2026-2034

Europe Adult Diaper Market Size, Share, Trends & Forecast (2026-2034)

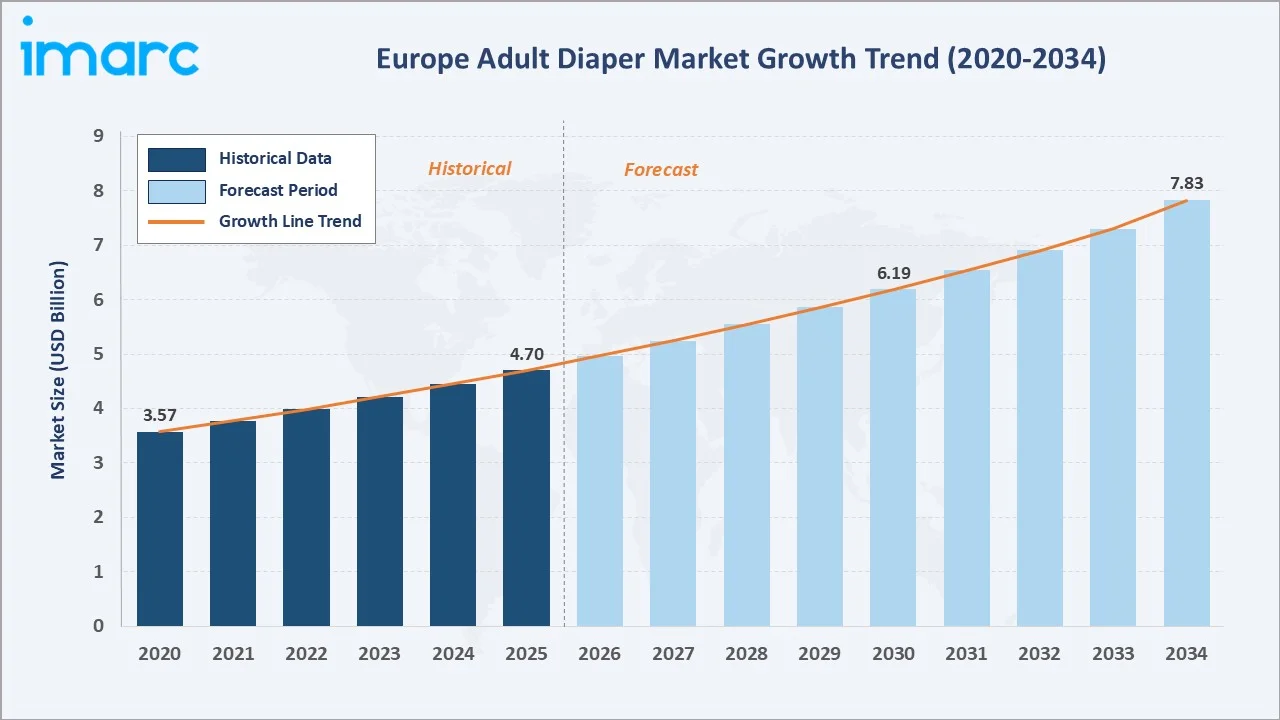

The Europe adult diaper market reached USD 4.70 Billion in 2025 and is projected to reach USD 7.83 Billion by 2034, growing at a CAGR of 5.65% during 2026-2034. Europe’s rapidly aging population, increasing clinical diagnosis and awareness of urinary and fecal incontinence, and the growing capacity of the institutional care sector are the primary forces driving sustained and predictable demand growth throughout the forecast period.

Market Snapshot

|

Metric |

Value |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Market Size (2025) |

USD 4.70 Billion |

|

Market Size (2034) |

USD 7.83 Billion |

|

CAGR (2026-2034) |

5.65% |

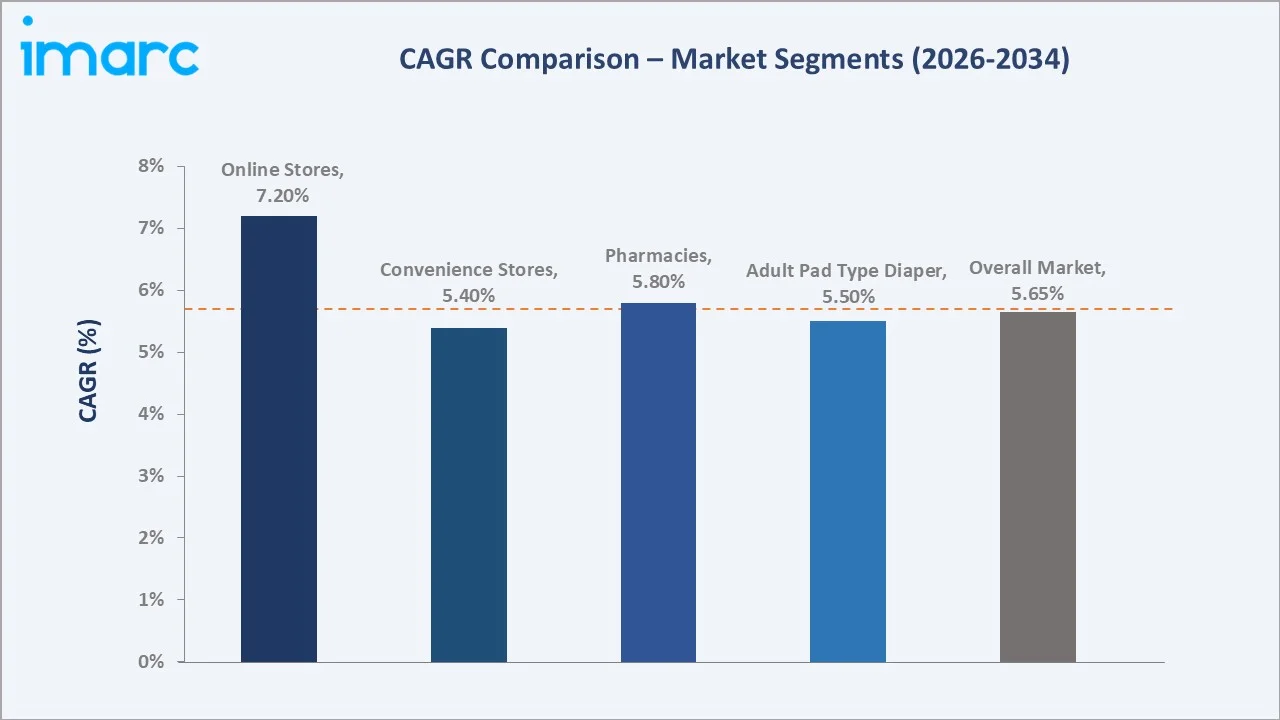

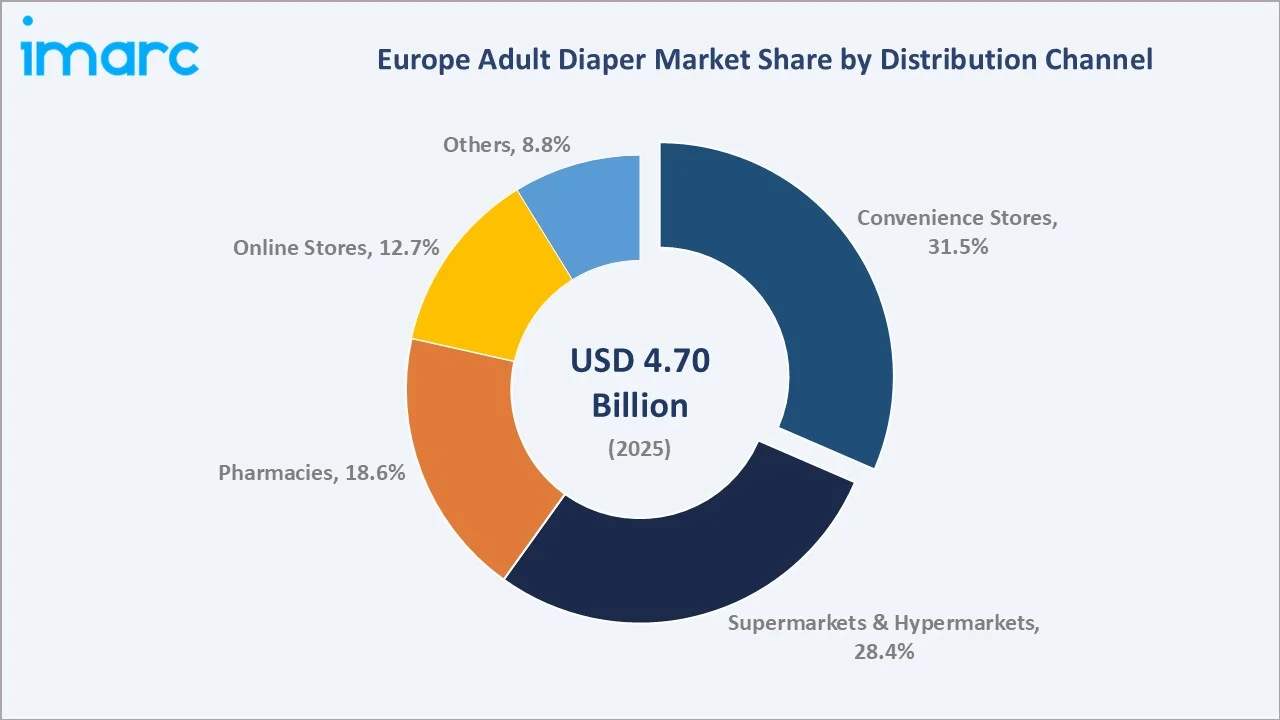

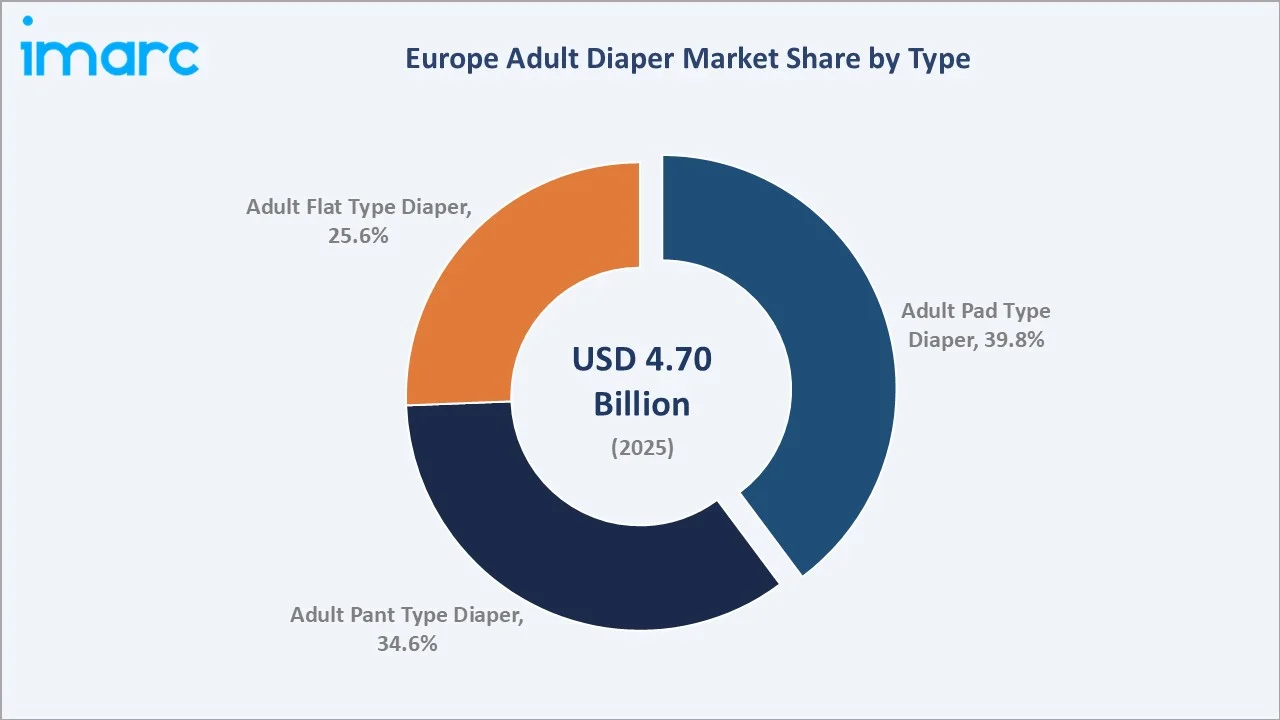

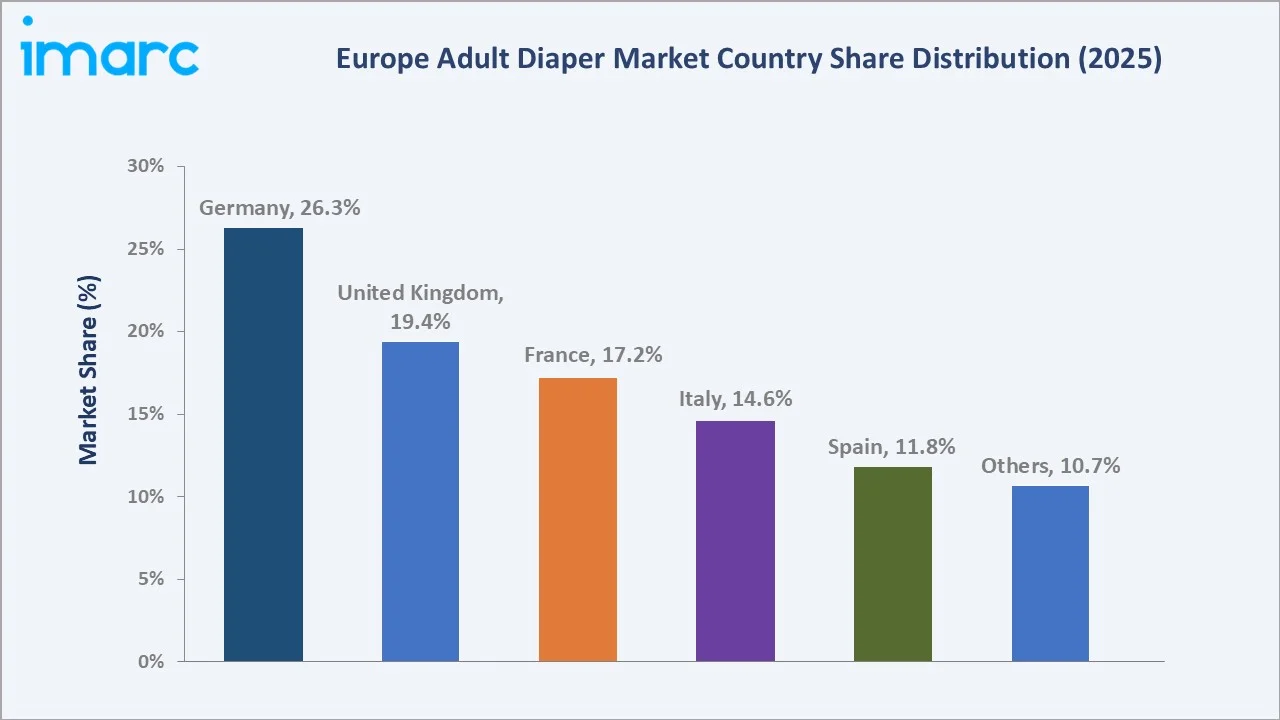

Germany leads regionally with a 26.3% market share in 2025, reflecting its position as Europe’s largest economy. Convenience stores command the largest distribution channel share at 31.5%, while online stores are the fastest-growing channel at ~7.2% CAGR. Adult pad type diaper dominates the product segment at 39.8%, while adult pant type diaper is the fastest-growing type, driven by premiumization and user preference for discreet, underwear-like designs.

To get more information on this market, Request Sample

The Europe adult diaper market grew from USD 3.57 Billion in 2020 to USD 4.70 Billion in 2025, an increase of USD 1.13 Billion over five years, driven by COVID-19-induced demand surge in home care and hospital settings, population aging across Germany, Italy, and Spain, and increasing caregiver and patient awareness of incontinence management products. The market is forecast to reach USD 7.83 Billion by 2034, reflecting the structural inevitability of demographic-driven demand and the expanding per-capita use of incontinence products as social stigma declines and product innovation drives uptake across a broader consumer age range.

Executive Summary

The Europe adult diaper market is a structurally defensive and demographically anchored category, characterized by non-discretionary purchase behavior, rising institutional procurement, and progressive product premiumization as consumer acceptance and clinical awareness continue to improve. The market stood at USD 4.70 Billion in 2025 and is forecast to reach USD 7.83 Billion by 2034 at a CAGR of 5.65%.

Convenience stores lead distribution with a 31.5% share in 2025, providing the discreet, accessible purchasing environment preferred by many incontinence sufferers who remain sensitive about product visibility and purchase occasion. Supermarkets and hypermarkets at 28.4% offer the price-competitive bulk purchasing format favored by caregivers and institutional procurement buyers.

Adult pad type diaper leads the product segment with a 39.8% share in 2025, serving the light-to-moderate incontinence segment where users can maintain their regular underwear while adding absorbent protection. Germany’s 26.3% share in 2025 is the largest adult diaper market, with 33 people of retirement age for every 100 people of working age in 2025 and projected to rise to 43 by 2070.

Key Market Insights

|

Insight |

Data |

|

Largest Distribution Channel |

Convenience Stores – 31.5% share (2025) |

|

Fastest Growing Distribution Channel |

Online Stores – ~7.2% CAGR (2026-2034) |

|

Largest Type |

Adult Pad Type Diaper – 39.8% share (2025) |

|

Fastest Growing Type |

Adult Pant Type Diaper – ~6.2% CAGR (2026-2034) |

|

Leading Country |

Germany – 26.3% share (2025) |

|

Top Companies |

Kimberly-Clark Corporation, Essity AB, Procter & Gamble, Ontex NV, and PAUL HARTMANN AG |

Key Analytical Observations Supporting The Above Data:

- Convenience stores at 31.5% (2025) serve as the primary retail purchase point as they offer the discretion, proximity, and product accessibility that many adult incontinence consumers prioritize, avoiding the perceived exposure of purchasing in supermarket settings where products are displayed in open, high-traffic aisles.

- Online stores at ~7.2% CAGR are growing fastest as the digital channel’s inherent discretion, home delivery in unmarked packaging, browser history that does not appear on shared devices, and subscription auto-delivery models that eliminate repeat purchase friction, address the most powerful barrier to adult diaper adoption: product purchase embarrassment.

- Adult pad type diaper at 39.8% (2025) dominates as it serves the largest addressable user segment: individuals with light-to-moderate incontinence who are ambulatory, cognitively intact, and want to manage their condition discreetly while maintaining normal daily activities.

- Germany’s 26.3% (2025) leadership reflects its status as Europe’s oldest and largest nation by GDP, combined with the German statutory health insurance (GKV) system’s coverage of incontinence aids under Hilfsmittelverzeichnis Category 15, ensuring that a significant proportion of adult diaper expenditure is reimbursed by statutory health insurers rather than paid out-of-pocket, creating a structurally supportive reimbursement environment for market expansion.

Europe Adult Diaper Market Overview

The Europe adult diaper market encompasses disposable and washable absorbent products for adults managing urinary and fecal incontinence, including adult pad type, pant type, and flat type diapers. The market serves community-dwelling individuals managing incontinence independently, institutionalized elderly and disabled patients in care homes and hospitals, and caregivers managing patient hygiene across the full spectrum of incontinence severity levels.

Europe’s adult diaper value chain is shaped by the dual commercial structure of consumer retail (where brand marketing and consumer psychology dominate purchase decisions) and institutional procurement (where product clinical performance, tender pricing, and EU Medical Device Regulation [EU MDR] compliance determine supplier selection). The growing online channel is adding a third structural layer in which DTC subscription economics and digital marketing are reshaping brand-consumer relationships in a category historically dominated by in-store purchasing.

Market Dynamics

To evaluate market opportunities, Request Sample

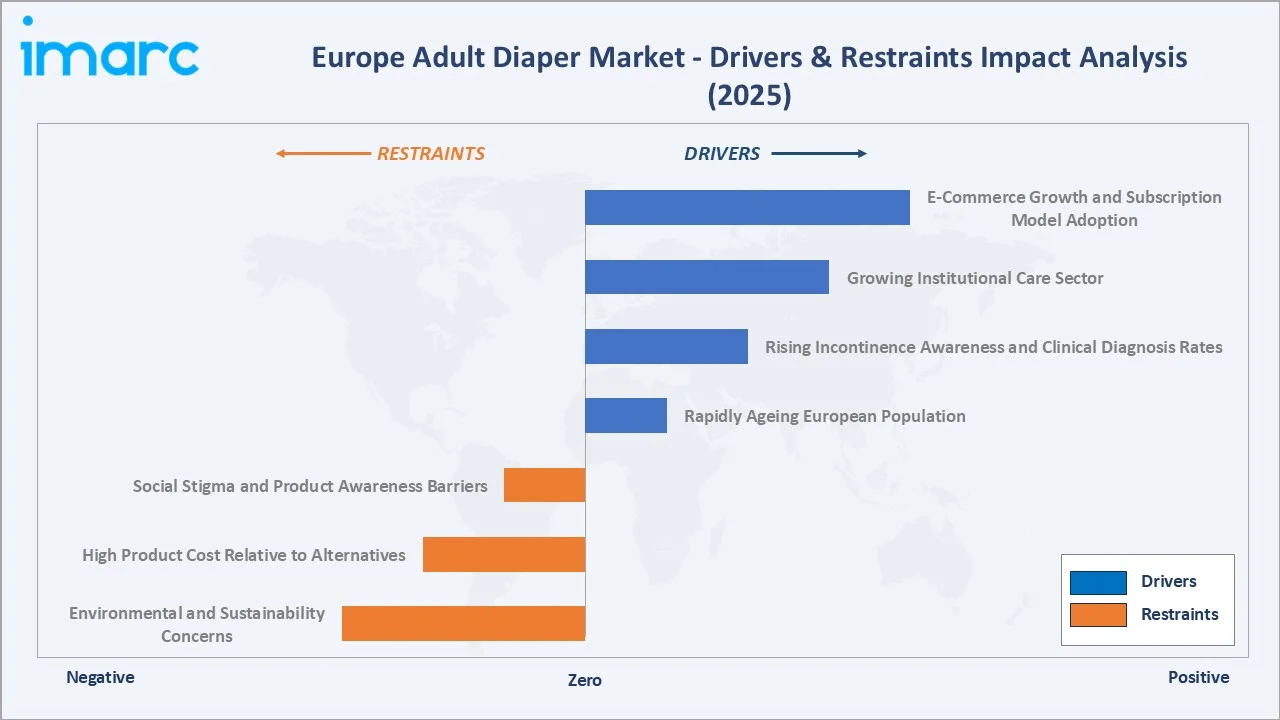

Market Drivers

- Rapidly Ageing European Population: As of January 1, 2025, the EU population was estimated at 450.6 million, with over one-fifth, or 22.0%, aged 65 years and above. Urinary incontinence (UI) is a widespread condition, affecting around 10% to 20% of people across Europe, creating a structurally expanding demand base that grows annually as the baby boomer cohort progresses through the 70–85 age band.

- Rising Incontinence Awareness and Clinical Diagnosis Rates: European healthcare systems and advocacy organizations, including the European Association of Urology (EAU) and the International Continence Society (ICS), are investing in primary care physician education and patient awareness campaigns that reduce the average time-to-diagnosis for incontinence from the current European median of 5–7 years to a target of under 2 years by 2030.

- Growing Institutional Care Sector: The care sector employs more than 3.3 million people across the EU’s social economy, with institutional care capacity expected to expand by 15–20% through 2034 as demographic aging outpaces family caregiver availability. Care homes, hospitals, and home care services are the primary institutional procurement channel for heavy-absorption flat-type and pant-type adult diapers, representing an estimated 40–45% of total European adult diaper market revenue.

- E-Commerce Growth and Subscription Model Adoption: The adult diaper category’s inherent privacy sensitivity makes e-commerce a structurally superior channel for a significant proportion of community-dwelling users. Home delivery in discreet packaging, subscription auto-delivery models that eliminate repeat purchase occasions, and access to a broader product range than available in local pharmacies or convenience stores collectively make online purchasing the preferred modality for a growing share of independent incontinence product users.

Market Restraints

- Social Stigma and Product Awareness Barriers: Incontinence remains a stigmatized condition in many European cultures, with studies indicating that 50–60% of European incontinence sufferers do not discuss the condition with their doctor and approximately 35–40% delay seeking treatment or product assistance for more than 3 years after symptom onset.

- High Product Cost Relative to Alternatives: Premium adult diapers retail at EUR 0.50–1.50 per unit in European markets, representing significant monthly recurring expenditure of EUR 30–120 for a typical community-dwelling user. Cost sensitivity is particularly acute in price-sensitive markets, including Spain, Portugal, and Eastern European markets, where consumer preference for lower-cost alternatives limits the addressable market for disposable product adoption.

- Environmental and Sustainability Concerns: Growing European consumer and regulatory focus on single-use plastics, landfill waste reduction, and circular economy principles is creating reputational risk for conventional disposable diaper manufacturers and driving investment in biodegradable, compostable, and washable alternatives that may partially substitute for conventional disposable volume in eco-conscious consumer segments.

Market Opportunities

- Men’s Incontinence Product Segment: Male urinary incontinence, affecting approximately 10–15% of European men aged 65+, is significantly underserved relative to the female incontinence market. Men’s incontinence products represent only approximately 15–18% of European adult incontinence product revenue despite accounting for approximately 35% of adult incontinence sufferers, reflecting the greater stigma and lower treatment-seeking behavior among men.

- Biodegradable and Eco-Friendly Adult Diapers: European consumers’ strong sustainability consciousness is creating genuine market demand for biodegradable and eco-certified adult incontinence products. Start-up brands are pioneering the sustainable incontinence category, commanding 20–40% price premiums over conventional products while addressing the environmental barrier to adult diaper adoption among environmentally motivated consumers.

Market Challenges

- Reimbursement Policy Heterogeneity Across European Markets: Germany’s GKV covers incontinence aids under Hilfsmittelverzeichnis Category 15; the UK’s NHS provides incontinence supplies through clinical prescription; France’s Assurance Maladie covers incontinence pads under certain diagnostic conditions. However, Spain, Italy, Portugal, and most Eastern European systems offer limited or no reimbursement, creating significant market heterogeneity in the effective demand level.

- Counterfeit and Low-Quality Product Competition: The adult diaper category’s high purchase frequency and price sensitivity attract the penetration of counterfeit and low-quality products, particularly through online marketplace channels and informal retail in Eastern European markets. Substandard products with inadequate absorption, skin irritation-inducing materials, or compromised sterility create negative user experiences that may discourage continued product adoption.

Emerging Market Trends

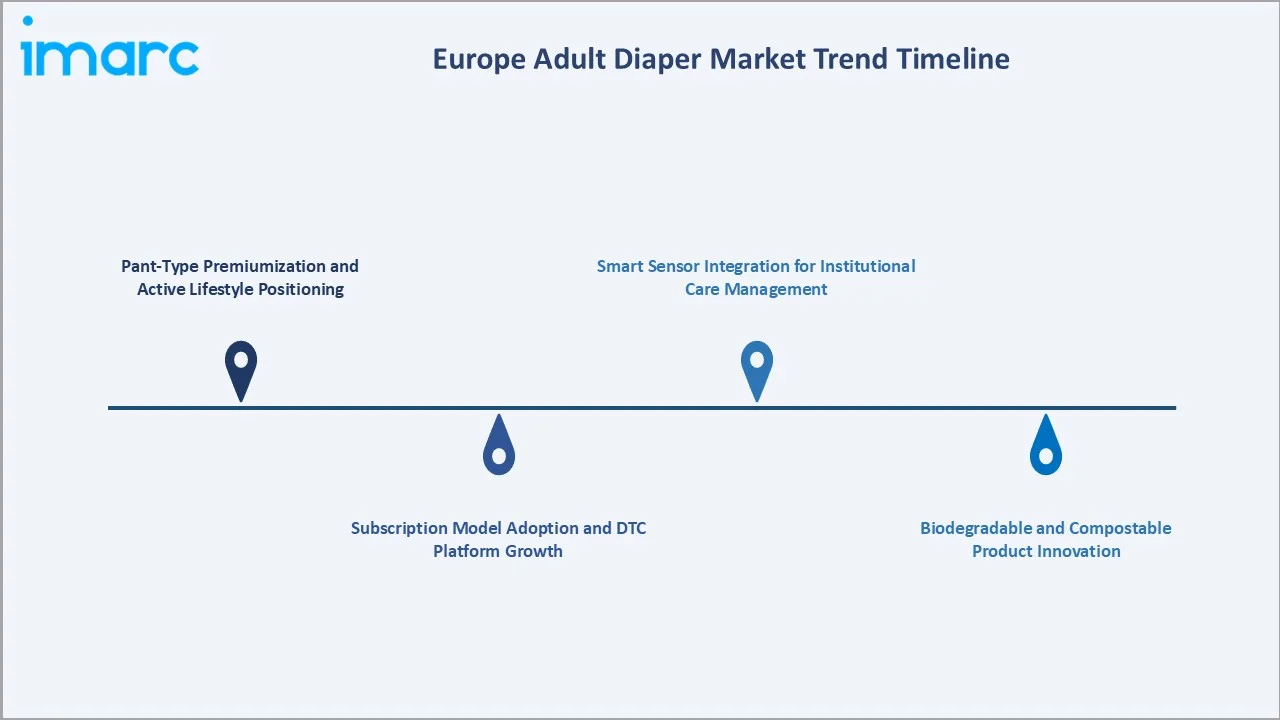

1. Pant-Type Premiumization and Active Lifestyle Positioning

Pant-type premiumization and active lifestyle positioning are emerging as important growth drivers in the European adult diaper market, as consumers increasingly prefer discreet, comfortable, and underwear-like products that support mobility and independence. Rising demand from elderly users, patients with mild-to-moderate incontinence, and active adults is encouraging manufacturers to develop thinner, highly absorbent, odor-control, and skin-friendly pant-style diapers.

2. Subscription Model Adoption and DTC Platform Growth

Subscription model adoption and DTC platform growth are strengthening the European adult diaper market by making incontinence products more accessible, discreet, and convenient for consumers. Online subscription services allow users and caregivers to receive regular deliveries based on usage needs, reducing the discomfort of repeated in-store purchases and ensuring uninterrupted product availability.

3. Biodegradable and Compostable Product Innovation

Biodegradable and compostable product innovation is gaining importance in the Europe adult diaper market as consumers, healthcare providers, and care facilities increasingly seek sustainable alternatives to conventional disposable hygiene products. Growing concerns over landfill waste, plastic use, and the environmental footprint of absorbent products are encouraging manufacturers to explore plant-based fibers, bio-based films, chlorine-free pulp, and compostable packaging.

4. Smart Sensor Integration for Institutional Care Management

Smart sensor integration is improving institutional care management by enabling real-time monitoring of diaper saturation levels, helping caregivers schedule timely changes and reduce discomfort, leakage, and skin-related issues. In Europe’s adult diaper market, these connected solutions support better hygiene management in hospitals, nursing homes, and long-term care facilities while improving staff efficiency and reducing unnecessary product usage.

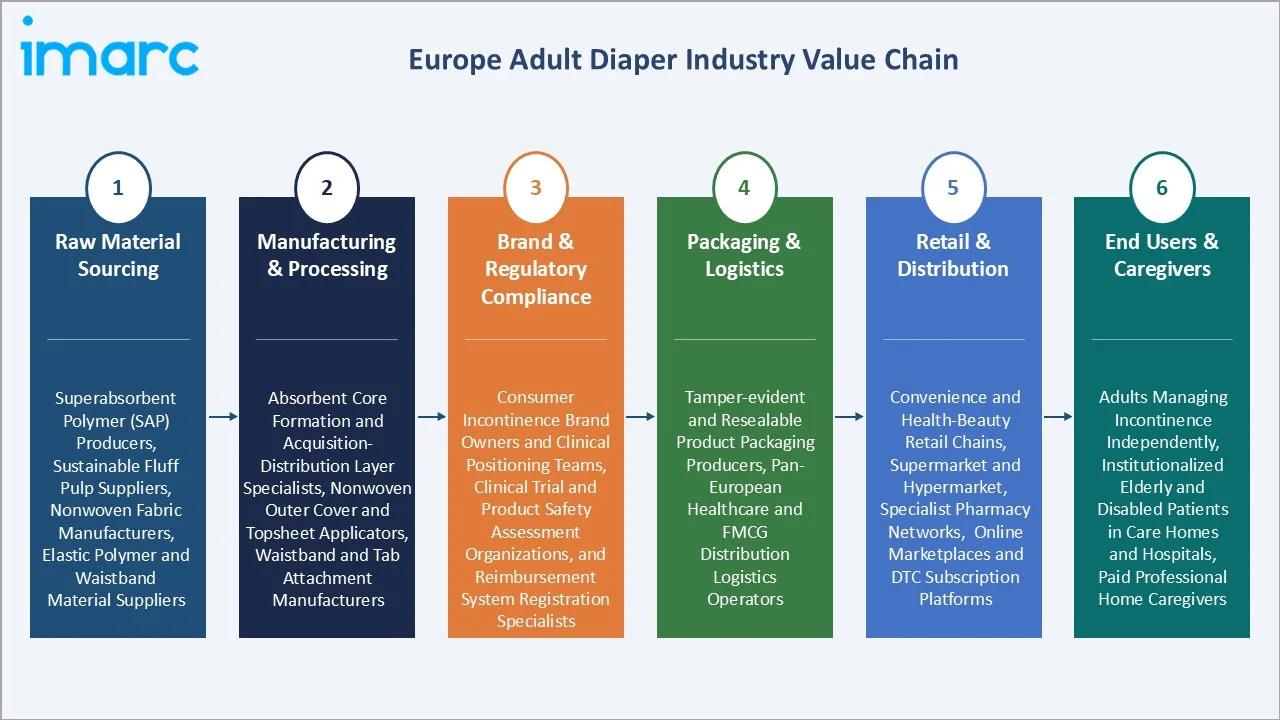

Industry Value Chain Analysis

Europe's adult diaper value chain is particularly influenced by EU Medical Device Regulation compliance requirements, national healthcare reimbursement system specifications, and the growing sustainability expectations of European consumers and regulatory authorities.

|

Stage |

Key Players |

|

Raw Material Sourcing |

Superabsorbent polymer (SAP) producers, sustainable fluff pulp suppliers, nonwoven fabric manufacturers, elastic polymer and waistband material suppliers |

|

Manufacturing & Processing |

Absorbent core formation and acquisition-distribution layer specialists, nonwoven outer cover and topsheet applicators, waistband and tab attachment manufacturers |

|

Brand & Regulatory Compliance |

Consumer incontinence brand owners and clinical positioning teams, clinical trial and product safety assessment organizations, and reimbursement system registration specialists |

|

Packaging & Logistics |

Tamper-evident and resealable product packaging producers, pan-European healthcare and FMCG distribution logistics operators |

|

Retail & Distribution |

Convenience and health-beauty retail chains, supermarket and hypermarket, specialist pharmacy networks, online marketplaces and DTC subscription platforms |

|

End Users & Caregivers |

Adults managing incontinence independently, institutionalized elderly and disabled patients in care homes and hospitals, paid professional home caregivers |

Technology Landscape in the Europe Adult Diaper Industry

Superabsorbent Polymer (SAP) and Core Technology Advancement

Modern European adult diapers incorporate superabsorbent polymer (SAP) at loading levels of 8–15 grams per product, enabling absorbency of 400–800 ml depending on product tier, while maintaining the thin profile required for modern pull-on pant designs.

Nonwoven Fabric and Skin-Contact Material Innovation

The skin-contact topsheet layer of adult diapers is undergoing significant material innovation as manufacturers respond to consumer demands for cotton-soft, breathable, and hypoallergenic surface materials. Cellulosic spunlace nonwovens, lyocell-based topsheets, and three-dimensional embossed nonwovens that minimize skin contact area while maintaining acquisition speed are being introduced across premium adult diaper ranges by Essity, Kimberly-Clark, and Hartmann.

Smart Sensor and Digital Health Integration

Wetness detection sensor systems, including printed conductive ink sensors embedded in diaper absorbent cores, ultrasonic sensor attachment systems, and RFID-enabled sensor tabs, are enabling real-time diaper saturation monitoring for institutional care applications.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Distribution Channel | Convenience Stores | 31.5% |

2025 |

| Type | Adult Pad Type Diaper | 39.8% |

2025 |

| Country | Germany | 26.3% |

2025 |

By Distribution Channel

Convenience stores lead with a 31.5% share in 2025. This segment provides the discretion, product range, and professional product advisory environment that many adult incontinence consumers require at the point of purchase. These formats enable the physically accessible, relatively private purchase occasion that distinguishes them from large hypermarket settings.

To access detailed market analysis, Request Sample

Supermarkets and hypermarkets at 28.4% serve the bulk purchase and household caregiver segment, offering multi-pack formats, promotional pricing, and private-label incontinence ranges that provide cost-effective alternatives to branded products. Online stores at 12.7% are the fastest-growing channel at ~7.2% CAGR, driven by subscription models, home delivery discretion, and the growing percentage of digitally confident senior consumers managing incontinence independently.

By Type

Adult pad type diaper dominates with a 39.8% share in 2025. Adult incontinence pads serve the light-to-moderate incontinence segment with the least disruption to the user’s habitual personal care routine. Pad type products are typically the first adult incontinence product adopted by newly diagnosed users, as they require no change in underwear type, are visually indistinguishable from conventional undergarments when worn, and carry the lowest perceived stigma of any incontinence product category.

Adult pant type diaper at 34.6% is the fastest-growing type at ~6.2% CAGR, reflecting consumer premiumization toward all-in-one pull-on designs that eliminate the two-step pad-and-underwear combination while delivering superior leak protection and body-conforming fit. Adult flat type diaper at 25.6% serves the heavy-to-severe incontinence segment primarily in institutional care settings, where caregiver-applied tab-style diapers remain the clinical standard.

Regional Market Insights

Germany’s market leadership (26.3%, 2025) is anchored by its combination of Europe’s largest elderly population and the most generous statutory health insurance reimbursement system for incontinence aids in the EU. The German GKV reimbursement system’s coverage of adult incontinence products under Hilfsmittelverzeichnis Category 15 creates a structurally expansive institutional demand base that insulates the market from economic cycles and sustains premium product adoption.

The United Kingdom, at 19.4%, benefits from the NHS’s systematic incontinence product prescribing through GP-referred Continence Clinics, which creates a structured clinical pathway from diagnosis to product prescription that systematically captures a large proportion of the eligible incontinence population into sustained product use.

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

26.3% |

Largest elderly population in the EU driving structural incontinence product demand; comprehensive statutory health insurance reimbursement for incontinence aids; strong domestic manufacturing base |

|

United Kingdom |

19.4% |

National health service incontinence supply program creating systematic product adoption pathways; growing digital and DTC subscription channel penetration; well-developed pharmacy retail infrastructure |

|

France |

17.2% |

Partial national health insurance reimbursement for incontinence products supporting institutional demand; strong pharmacy-led distribution culture; ageing baby boomer cohort |

|

Italy |

14.6% |

Europe's oldest median-age population creating large structural incontinence product demand; the strong institutional care home sector with significant procurement volumes |

|

Spain |

11.8% |

Rapidly ageing Mediterranean population driving growing incontinence product demand; expanding private care home sector; improving primary care incontinence diagnosis and referral rates |

|

Others |

10.7% |

A growing middle-class consumer base and improving living standards in Eastern European markets, progressively improving healthcare coverage for incontinence products |

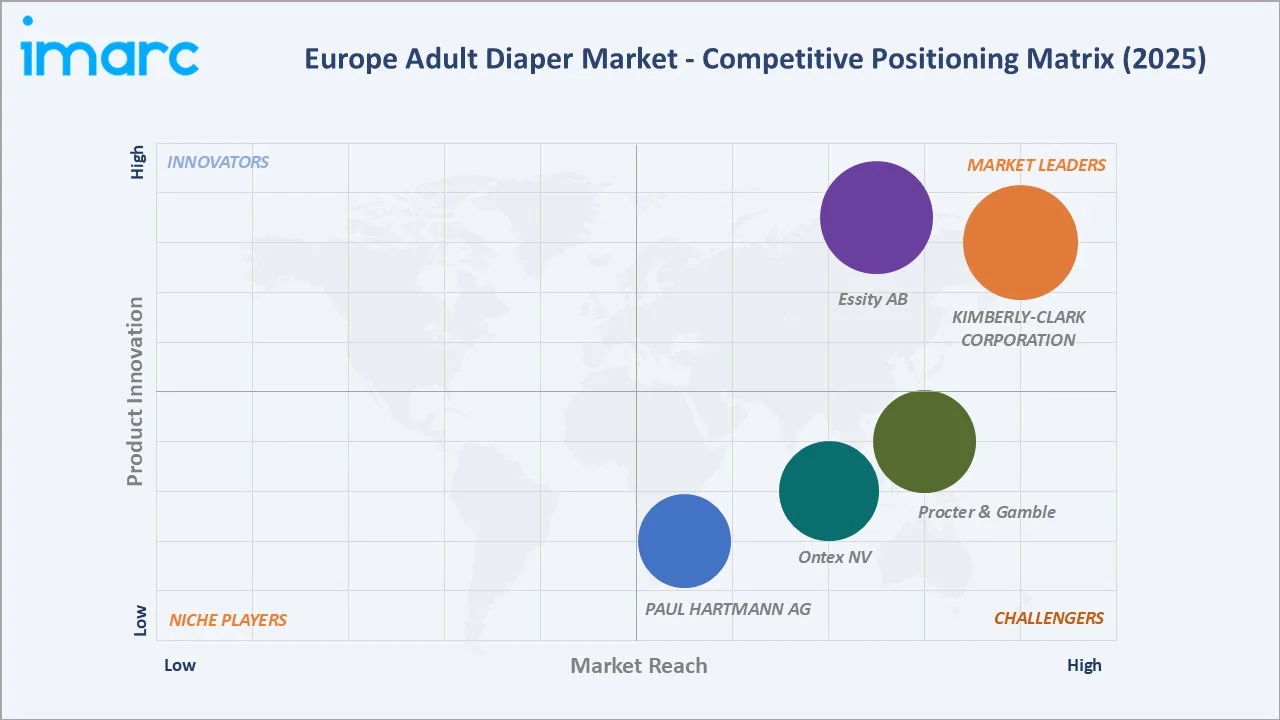

Competitive Landscape

Europe’s adult diaper market exhibits high concentration among five dominant multinational players, collectively estimated to control approximately 65–75% of the branded European adult diaper market revenue.

|

Company Name |

Key Brand(s) |

Market Position |

Core Strength |

|

KIMBERLY-CLARK CORPORATION |

Depend, Poise, Plenitud, Confidence |

Market Leader |

Global leader in adult incontinence; Depend brand European expansion; subscription DTC platform leadership |

|

Essity AB |

TENA |

Market Leader |

Europe’s dominant adult incontinence brand; TENA Silhouette premium pant innovation; TENA Smart Care institutional program |

|

Procter & Gamble |

Always Discreet |

Strong Challenger |

Always Discreet blends feminine care and incontinence positioning; strong European supermarket distribution through P&G retail partnerships |

|

Ontex NV |

iD, Serenity, Serenity Care, Lille Healthcare, Orizon, Kylie |

Strong Challenger |

European manufacturer with in-house nonwoven production; strong private-label supply for major retailers |

|

PAUL HARTMANN AG |

MoliCare |

Challenger |

Dominant in German and Central European institutional care market; Smart Care digital monitoring program; medical-grade product compliance expertise |

The competitive landscape is characterized by heavy investment in brand repositioning to destigmatize incontinence product use. Subscription model development and e-commerce platform investment are the primary competitive vectors among leading brands seeking to capture the growing online channel.

Key Company Profiles

KIMBERLY-CLARK CORPORATION

KIMBERLY-CLARK CORPORATION is one of the world’s largest personal care companies by revenue and the leading provider of Depend-branded adult incontinence products across European markets.

- Product Portfolio: Depend Real Fit, Depend Silhouette, Poise Microliners and Pads, and Depend Maximum Protection Briefs.

- Recent Developments: In January 2026, KIMBERLY-CLARK CORPORATION reported Q4 2025 net sales of USD 4.1 billion, with organic sales growth of 2.1% and adjusted EPS rising 24.0% to USD 1.86, supported by productivity gains and volume-led growth.

- Strategic Focus: Depend subscription D2C platform scaling across Europe; Smart Diaper Sensor institutional care program expansion; Re-think Depend destigmatisation marketing; Depend Eco partnership with European recycling infrastructure providers.

Essity AB

Essity AB is Europe’s largest health and hygiene company and one of the market leaders in European adult incontinence products through its TENA brand, the continent’s most recognized adult diaper brand by consumer awareness in all major markets.

- Product Portfolio: TENA Lady, TENA Men, TENA Pants, TENA Silhouette, TENA Slip, TENA Flex, TENA Smart Care.

- Recent Developments: In December 2025, Essity AB, BASF, and the Technical University of Vienna successfully piloted a recycling technology that converts used diapers and incontinence products into gasification. The pilot supports circularity in absorbent hygiene products by offering a scalable route to reduce landfill waste and recover value from complex used hygiene materials.

- Strategic Focus: TENA Silhouette premium pant-type expansion; TENA Smart Care institutional digitization program; European manufacturing sustainability investment; TENA Men brand growth through targeted male incontinence awareness campaigns.

Market Concentration Analysis

Europe’s adult diaper market exhibits high concentration in the branded consumer segment, with the top five players collectively accounting for approximately 65–75% of branded consumer revenue across the continent’s five largest markets. The institutional care segment is somewhat less concentrated, competing alongside regional institutional suppliers.

Market consolidation is a defining trend, driven by the scale advantages of pan-European retail distribution, the increasing cost of digital marketing and e-commerce platform investment, and the R&D investment required to develop smart sensors, biodegradable materials, and premium fabric innovations.

Private-label growth, estimated at approximately 20–25% of European adult diaper volume, creates ongoing pricing pressure on mid-market branded products, concentrating branded manufacturers’ investment in premium product tiers where private-label products cannot yet replicate the innovation premium.

Investment & Growth Opportunities

Fastest Growing Segments

Online Stores (~7.2% CAGR), adult pant type diaper (~6.2% CAGR), pharmacies channel (~5.8% CAGR), and men’s incontinence product sub-segment (estimated ~8–10% CAGR) represent the primary value-growth investment vectors through 2034. Smart sensor institutional diaper systems and biodegradable/eco-certified consumer products represent high-margin premium niches growing at double-digit rates from a small but rapidly expanding base.

Emerging Market Expansion

Eastern European markets, Poland, the Czech Republic, Hungary, and Romania, represent the fastest-growing geographic expansion opportunity, as middle-class income growth, improving primary care incontinence diagnosis rates, and e-commerce channel development collectively expand the addressable consumer base from a historically low penetration level.

Venture and Institutional Investment Trends

- In January 2026, Essity AB secured a EUR 400 million, seven-year loan from the European Investment Bank to support research, development, and innovation initiatives across all business areas. The funding will strengthen Essity’s hygiene and health innovation capabilities, while supporting sustainable product development, green transition goals, and circular economy initiatives.

- European venture capital investment in femtech and inclusive health platforms addressing incontinence awareness, pelvic floor health, and DTC product subscription has grown from approximately EUR 35 Million in 2022 to EUR 120 Million in 2025, supporting digital health brands that drive early product adoption and expand the addressable market among younger incontinence demographics.

Future Market Outlook (2026-2034)

Europe’s adult diaper market is positioned for sustained, demographically anchored growth through 2034. From a base of USD 4.70 Billion in 2025, the market is projected to reach USD 6.19 Billion by 2030 and USD 7.83 Billion by 2034 at a 5.65% CAGR. Germany will retain market leadership throughout the forecast period, while Spain and Italy, with Europe’s most rapidly growing elderly populations relative to their current market size, will grow at above-average rates, narrowing the gap with France and the UK.

The product mix will shift meaningfully toward adult pant type diaper by 2034, with the segment’s share growing from 34.6% to approximately 40–42% as premium pull-on designs penetrate the active lifestyle and younger incontinence demographics. The online channel’s share will expand from 12.7% to approximately 20–22% by 2034, driven by subscription model maturation, the generational shift of digitally native 65-year-olds into the primary incontinence product consumer cohort, and the continued normalization of online purchasing for sensitive personal care products.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 70 industry participants in 2024–2025, including incontinence product brand managers and marketing executives; pharmacy category buyers; NHS Continence Clinic nurses and incontinence specialist physicians; home care agency purchasing managers; and advocacy representatives from the European Association of Urology Patient Advocacy Group.

Secondary Research

Secondary research encompassed company annual reports and sustainability disclosures; European Association of Urology (EAU) incontinence prevalence and treatment guidelines; Eurostat demographic aging projections; national healthcare reimbursement policy documents for Germany (GKV Hilfsmittelverzeichnis), UK (NHS England Continence Products Commissioning Guide), and France (Assurance Maladie tariffication); and Statista and Euromonitor incontinence product market datasets.

Forecasting Models

Market size estimations were derived using bottom-up country-level demographic modelling, based on aged population growth, incontinence prevalence rates by age cohort, and per-capita product usage intensity, combined with pricing and channel mix trajectory analysis. A CAGR of 5.65% reflects consensus validated against EAU incontinence prevalence projections, GKV and NHS procurement growth trends, and IMARC’s primary expert panel review.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Adult Pad Type Diaper, Adult Flat Type Diaper, Adult Pant Type Diaper |

| Distribution Channels Covered | Pharmacies, Convenience Stores, Online Stores, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | KIMBERLY-CLARK CORPORATION, Essity AB, Procter & Gamble, Ontex NV, PAUL HARTMANN AG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Adult Diaper Market Report

The Europe adult diaper market reached USD 4.70 Billion in 2025 and is forecast to reach USD 7.83 Billion by 2034.

The market is expected to grow at a CAGR of 5.65% during 2026-2034, driven by rapidly ageing demographics, rising incontinence diagnosis rates, institutional care sector expansion, and online channel growth.

Germany leads with a 26.3% share in 2025, reflecting Europe’s largest elderly population, the GKV statutory insurance reimbursement for incontinence aids, and the strong domestic presence of international brands.

Convenience stores lead with a 31.5% share in 2025, driven by the discretion and professional product environment of health-beauty retail chains preferred by many adult incontinence consumers.

Adult pad type diaper leads with a 39.8% share in 2025, serving the light-to-moderate incontinence segment with minimum disruption to the user’s normal underwear habits and providing the lowest perceived stigma of any adult incontinence product format.

Some of the key players include Kimberly-Clark Corporation, Essity AB, Procter & Gamble, Ontex NV, and PAUL HARTMANN AG.

Online stores are growing at approximately 7.2% CAGR owing to home delivery in discreet packaging, subscription auto-delivery models, and access to a broader product range, which address the privacy sensitivity and repeat-purchase friction that are the primary behavioral barriers to adult diaper adoption.

Key challenges include persistent social stigma and delayed diagnosis, reducing effective demand relative to clinical incontinence prevalence, and high product costs relative to alternatives in price-sensitive southern and eastern European markets.

Men’s incontinence product segment development, biodegradable and eco-certified product innovation, smart sensor institutional diaper systems, online subscription platform investment, Eastern European market expansion, and pant-type premiumization represent the highest-growth investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)