Europe Car Rental Market Size, Share, Trends and Forecast by Booking Type, Rental Length, Vehicle Type, Application, End-User, and Country, 2026-2034

Europe Car Rental Market Size, Share, Trends & Forecast (2026-2034)

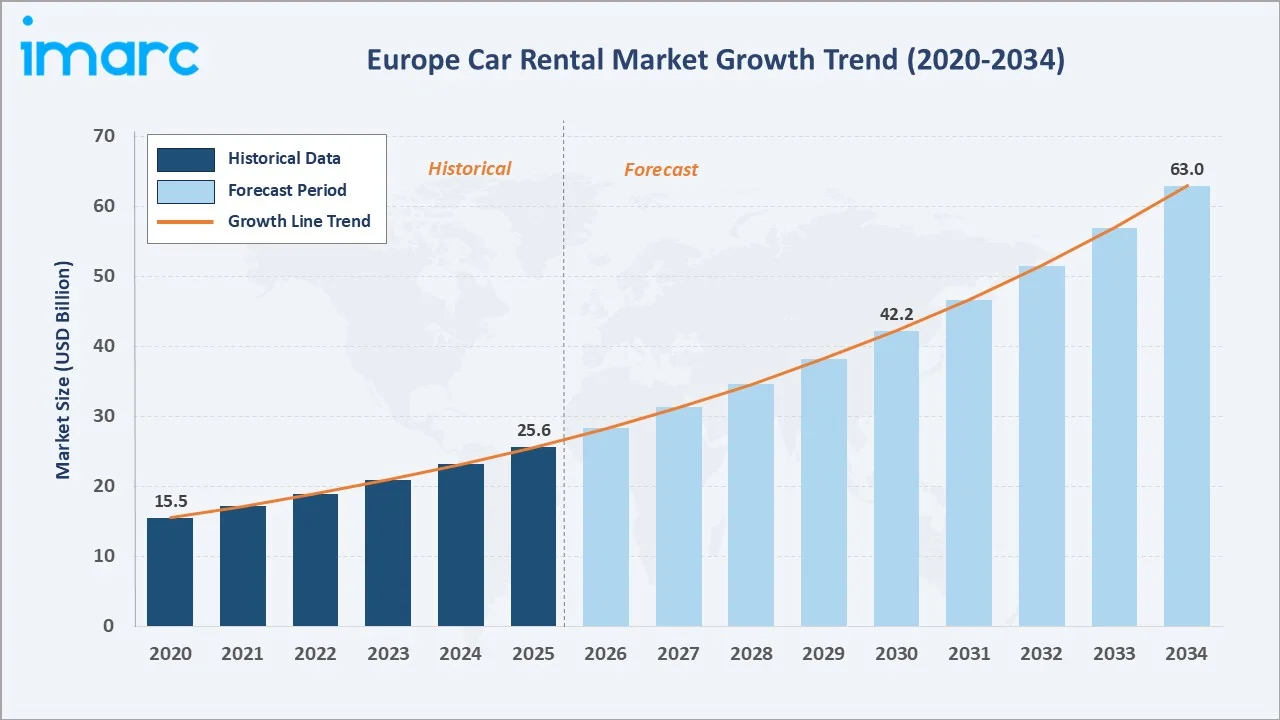

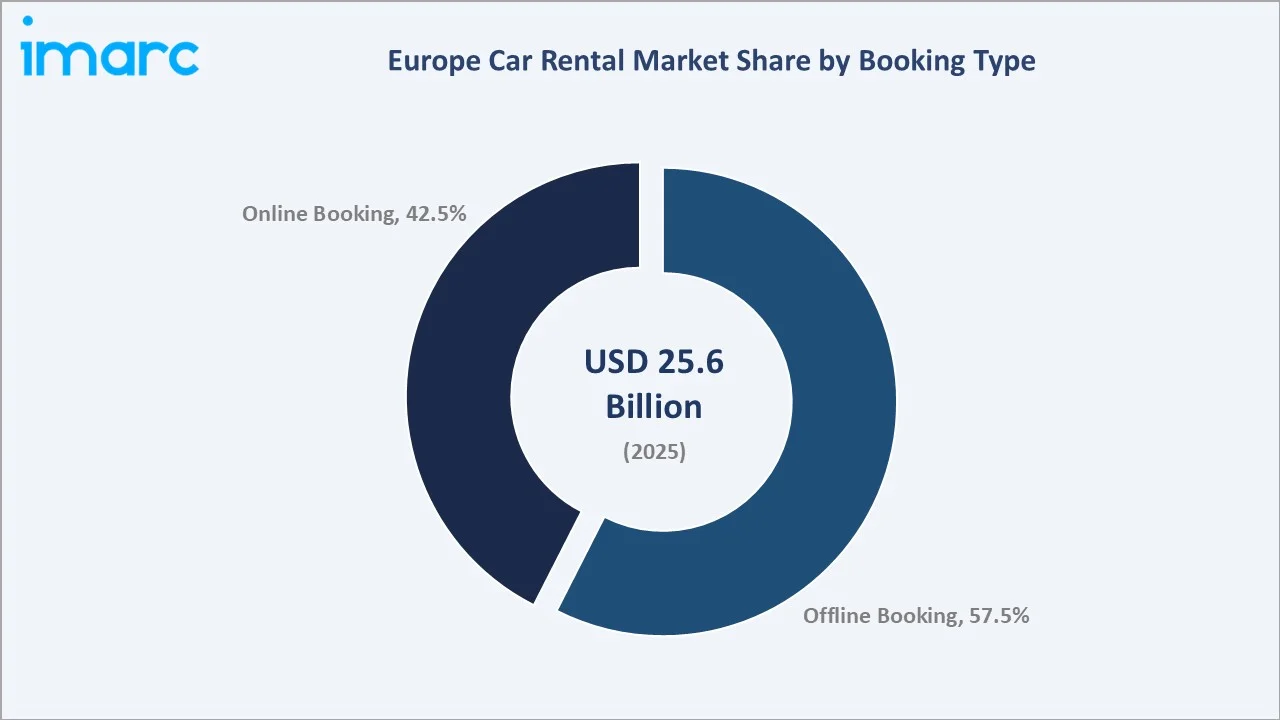

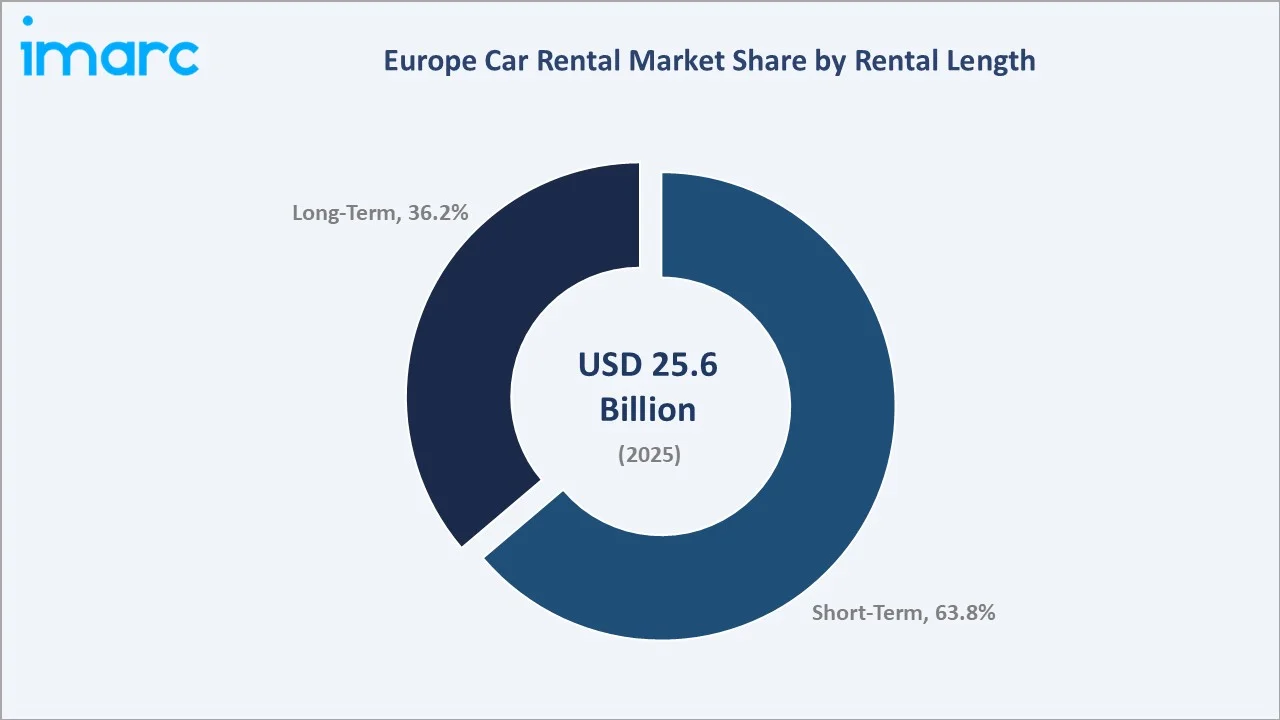

The Europe car rental market size was valued at USD 25.6 Billion in 2025 and is projected to reach USD 63.0 Billion by 2034, exhibiting a CAGR of 10.55% during the forecast period 2026-2034. Post-pandemic tourism recovery, mobile-first booking adoption, fleet electrification, and rising demand for short-term flexible mobility are driving the Europe car rental market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 25.6 Billion |

|

Forecast Market Size (2034) |

USD 63.0 Billion |

|

CAGR (2026-2034) |

10.55% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country Market |

Germany (24.5% share, 2025) |

|

Fastest Growing Segment |

Online Booking (~12.6% CAGR) |

|

Leading Booking Type |

Offline Booking (57.5%, 2025) |

|

Leading Rental Length |

Short Term (63.8%, 2025) |

The Europe car rental market growth trajectory from 2020 through 2034 contrasts historical pandemic-era recovery against a sustained forecast curve powered by inbound tourism, corporate mobility, and digital booking expansion across the region.

To get more information on this market, Request Sample

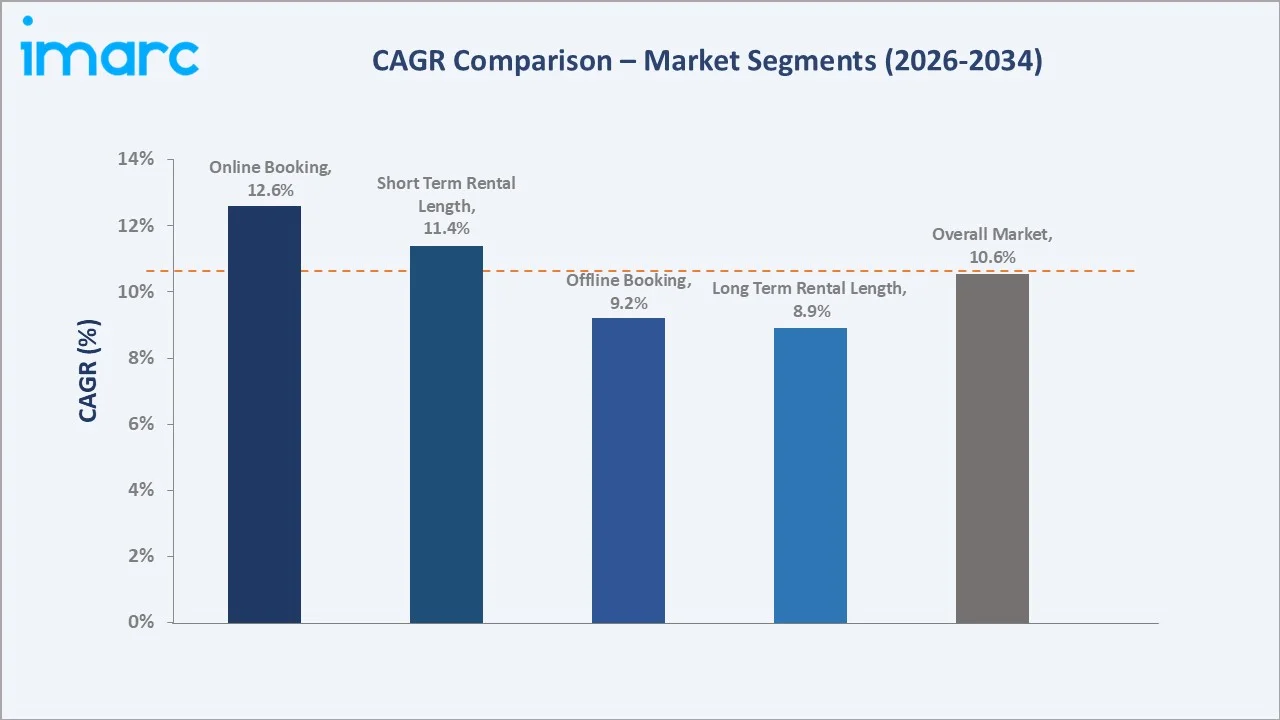

Segment-level CAGR comparisons highlight online booking and short-term rentals as the fastest-growing sub-categories within the Europe car rental market forecast through 2034.

Executive Summary

The Europe car rental market is undergoing a structural shift driven by digital booking platforms, fleet electrification mandates, and the rebound of inbound tourism. Valued at USD 25.6 Billion in 2025, the market is forecast to reach USD 63.0 Billion by 2034 at a CAGR of 10.55%.

Offline booking retains a 57.5% share in 2025, anchored by airport counters and corporate procurement. Online booking is the fastest-growing channel, expanding at an estimated CAGR of 12.6% through 2034 as mobile applications, OTAs, and direct-to-consumer portals capture leisure demand. Short-term rentals account for 63.8% of revenue, while long-term rentals gain traction among corporate fleets and subscription users.

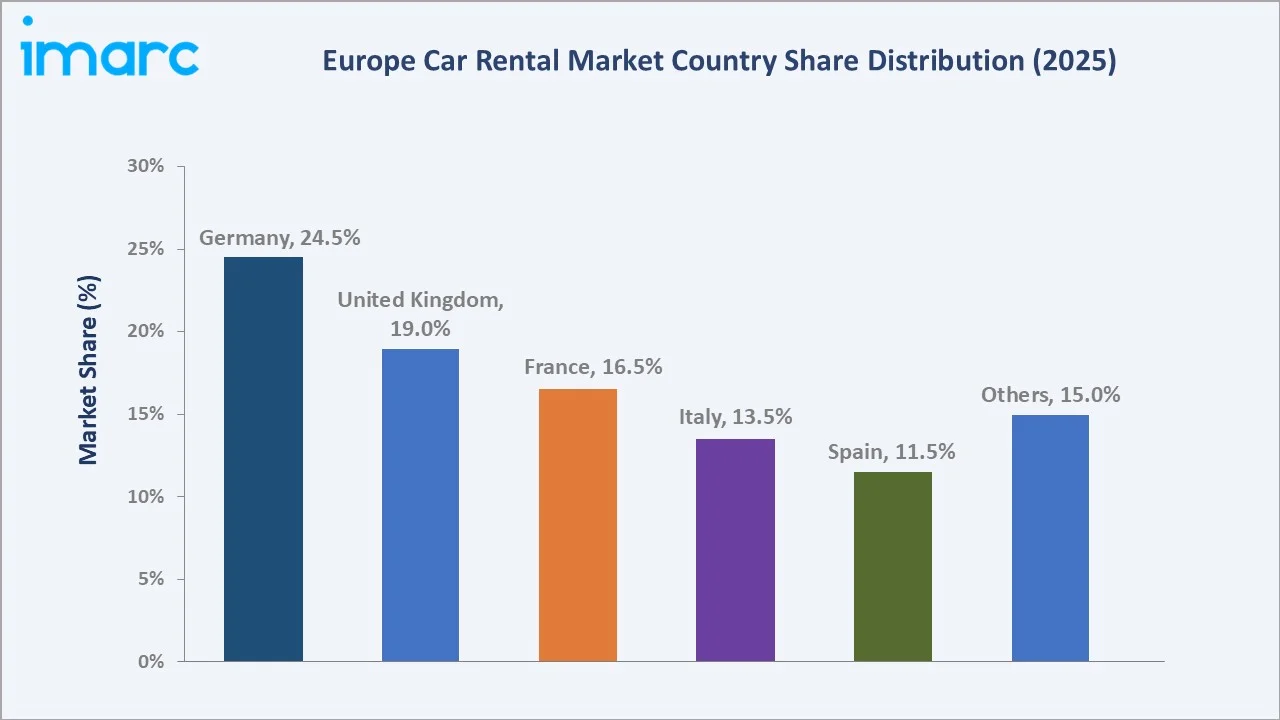

Germany leads the region with a 24.5% share in 2025, followed by the United Kingdom at 19.0% and France at 16.5%. The Europe car rental market outlook remains positive as EV integration, peer-to-peer platforms, and AI-led dynamic pricing converge across mature and emerging country markets.

Key Market Insights

|

Insight |

Data |

|

Largest Booking Type |

Offline Booking - 57.5% share (2025) |

|

Fastest Growing Booking Type |

Online Booking - ~12.6% CAGR (2026-2034) |

|

Largest Rental Length |

Short Term - 63.8% share (2025) |

|

Second Rental Length |

Long Term - 36.2% share (2025) |

|

Leading Country |

Germany - 24.5% revenue share (2025) |

|

Top Companies |

Volkswagen Group, Enterprise Holdings, Inc., Sixt, Hertz Global Holdings, Inc., Avis Budget Group, Inc., Localiza, Turo Inc. |

|

EV Fleet Adoption |

Over 8% of rental fleets in 2025 |

Key Analytical Observations Supporting the Above Data:

- Offline booking's 57.5% dominance in 2025 reflects the strength of airport desks and corporate rental contracts across Europe's major travel hubs, including Frankfurt, Heathrow, Charles de Gaulle, and Fiumicino airports.

- Online booking's 42.5% share is driven by mobile-first consumers and OTAs such as Booking.com and Skyscanner. Mobile bookings have become a significant portion of digital rental transactions in Western Europe, reflecting the growing preference for on-the-go and app-based reservation platforms.

- Short-term rentals' 63.8% majority is underpinned by leisure tourism and intra-European business travel. Eurostat recorded strong growth in nights spent in EU tourist accommodations, supporting sustained demand for short-term rental stays.

- Germany's 24.5% regional leadership reflects its role as Europe's largest automotive market and its dense airport and high-speed rail corridor network supporting business rentals across Frankfurt, Munich, and Berlin.

- EV and shared mobility adoption is accelerating, with a growing share of European rental fleets comprising electric vehicles, driven by EU CO₂ regulations and urban low-emission zones in Paris, London, and Amsterdam.

Europe Car Rental Market Overview

The Europe car rental market spans short-term leisure rentals, long-term corporate fleets, airport-based mobility, and emerging subscription and peer-to-peer models. Vehicles include economy, executive, luxury, SUV, and electric segments, served through operator-owned fleets, franchise networks, and digital aggregators. The ecosystem interfaces with OEMs, leasing companies, insurance providers, and digital booking platforms, creating a multi-stakeholder value chain.

Growth is supported by macroeconomic drivers such as tourism recovery, rising corporate travel budgets, cross-border mobility within the Schengen area, and urban mobility transformation. Regulatory tailwinds, including EU fleet emission standards and low-emission zone enforcement, are simultaneously reshaping vehicle mix and operator economics.

Market Dynamics

To evaluate market opportunities, Request Sample

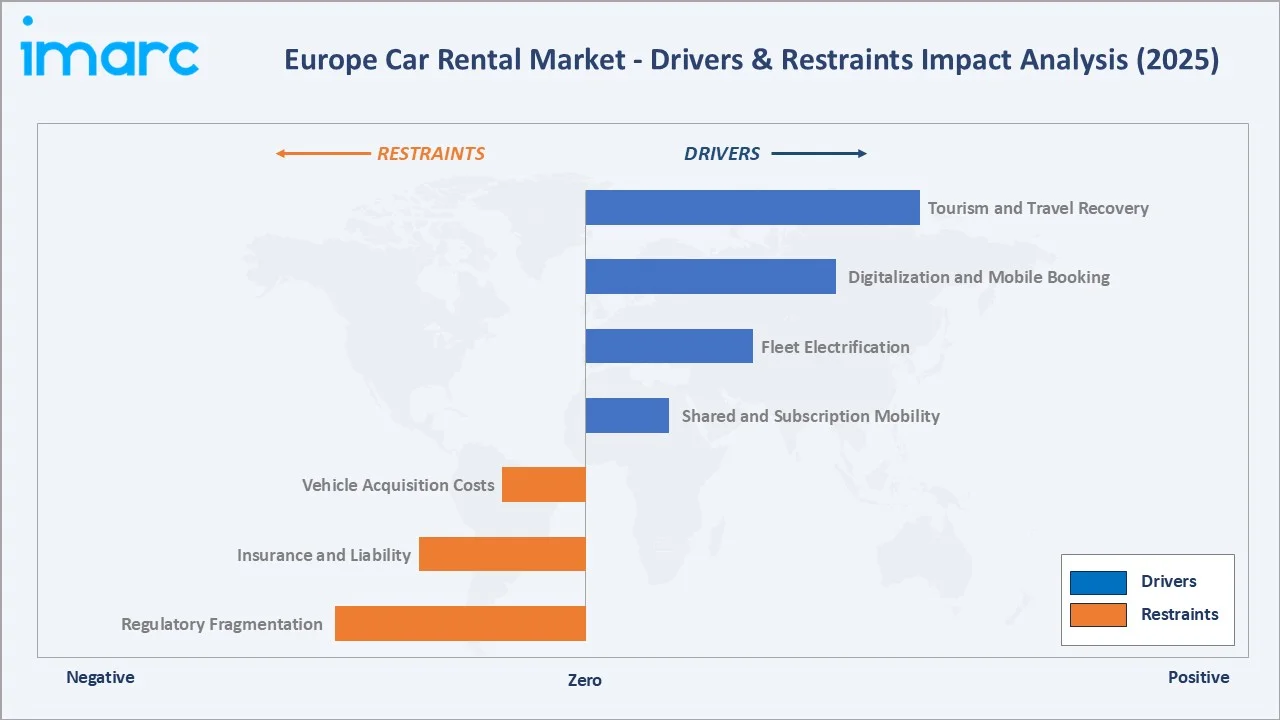

Market Drivers

- Tourism and Travel Recovery: International tourist arrivals in Europe reached 747 million in 2024 per UN Tourism data, exceeding pre-pandemic levels. Intra-EU travel, Mediterranean summer peaks, and city-break demand in Paris, Rome, and Barcelona continue to drive short-term rental volumes across leading airport hubs.

- Digitalization and Mobile Booking: Mobile and app-based bookings now account for a significant share of all digital rental transactions in Western Europe. Direct-to-consumer apps from Volkswagen Group, Enterprise Holdings, Inc., Sixt, along with aggregator platforms, are compressing booking times and enabling dynamic pricing strategies.

- Fleet Electrification: EU CO₂ regulations targeting significant emissions reduction by 2030 are pushing rental operators to electrify fleets. A growing share of European rental vehicles is now electric, with Sixt announcing a target of a largely electrified fleet by 2030 as part of its sustainability roadmap.

- Shared and Subscription Mobility: Subscription models and peer-to-peer platforms are expanding into the mainstream, with operators like Finn, Care by Volvo, and Turo capturing younger urban consumers. Monthly car subscriptions are forecast to grow at double-digit CAGR through 2030.

Market Restraints

- Vehicle Acquisition Costs: Rising new-vehicle prices, especially for EVs and premium segments, are inflating fleet capital expenditure for rental operators across the UK, Germany, and France.

- Insurance and Liability: Escalating insurance premiums and cross-border accident liability claims, particularly in Italy and Spain, are compressing operator margins and pushing up consumer-facing rental rates.

- Regulatory Fragmentation: Low-emission zones, divergent VAT rules, and country-specific driver licence requirements complicate pan-European fleet deployment and standardized digital onboarding.

Market Opportunities

- EV-Ready Rental Infrastructure: EU AFIR regulation mandates EV charging points every 60 km on core TEN-T corridors by 2025-2026. Rental operators partnering with Ionity, Fastned, and airport charging networks can capture premium EV rental demand across leisure and business segments.

- Corporate Mobility and Subscription Services: Large European corporates are shifting from vehicle ownership to flexible mobility-as-a-service. Long-term rental and monthly subscription offerings are creating a structured, recurring-revenue growth pipeline for market leaders through 2030.

Market Challenges

- Residual Value Volatility: EV residual values remain uncertain compared to internal combustion vehicles, creating fleet remarketing risk for operators rapidly transitioning their vehicle mix across Germany, France, and the Nordics.

- Labour and Operational Costs: Wage inflation across airport and city rental counters, combined with rising real estate costs in tourist hotspots, is pressuring operational margins for national and regional operators.

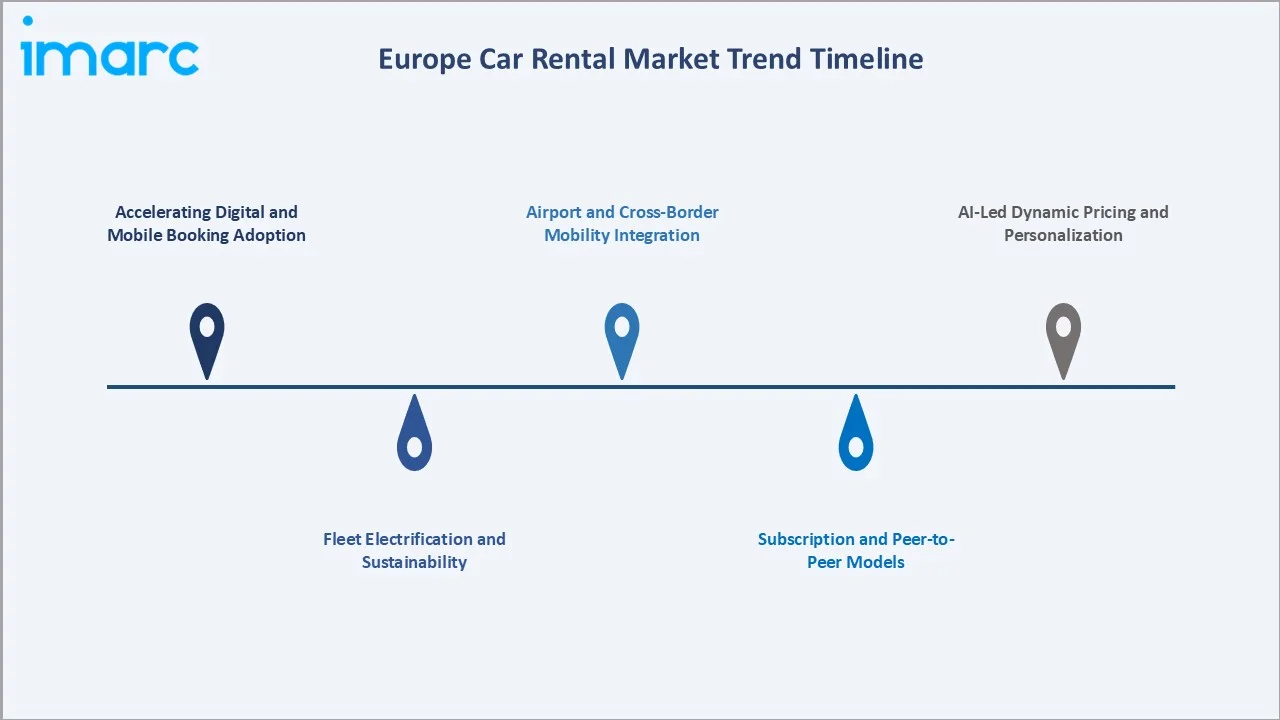

Emerging Market Trends

1. Accelerating Digital and Mobile Booking Adoption

Consumer preference for instant, contactless rental journeys is pushing operators to invest in mobile apps, keyless vehicle access, and AI-powered customer service. Digital channels are expected to dominate European rental bookings by 2030, reshaping counter-based operations and cost structures.

2. Fleet Electrification and Sustainability

Leading operators are aggressively electrifying their fleets to comply with EU CO2 regulations and meet ESG-linked procurement demand from corporate clients. Volkswagen Group, Enterprise Holdings, Inc., Sixt, Hertz Global Holdings, Inc have announced multi-billion-euro EV acquisition plans, partnering directly with OEMs including BMW, Stellantis, and BYD.

3. Subscription and Peer-to-Peer Models

Monthly subscriptions and peer-to-peer rental platforms are reshaping consumer expectations in urban centres. These asset-light, flexible offerings are gaining share among millennials and Gen Z consumers who prefer access over ownership, with Germany, the UK, and the Netherlands leading adoption.

4. Airport and Cross-Border Mobility Integration

Airport rental counters remain a core demand hub, supported by cross-border leisure and business travel within the Schengen area. Integrated rail-road-rental journeys, particularly through Deutsche Bahn and SNCF partnerships, are creating new multi-modal rental touchpoints.

5. AI-Led Dynamic Pricing and Personalization

Dynamic pricing engines powered by machine learning are enabling operators to optimize yield across seasonality, fleet utilization, and last-minute demand. Personalized upsell offers and loyalty-linked pricing are increasing average revenue per rental for digitally mature operators.

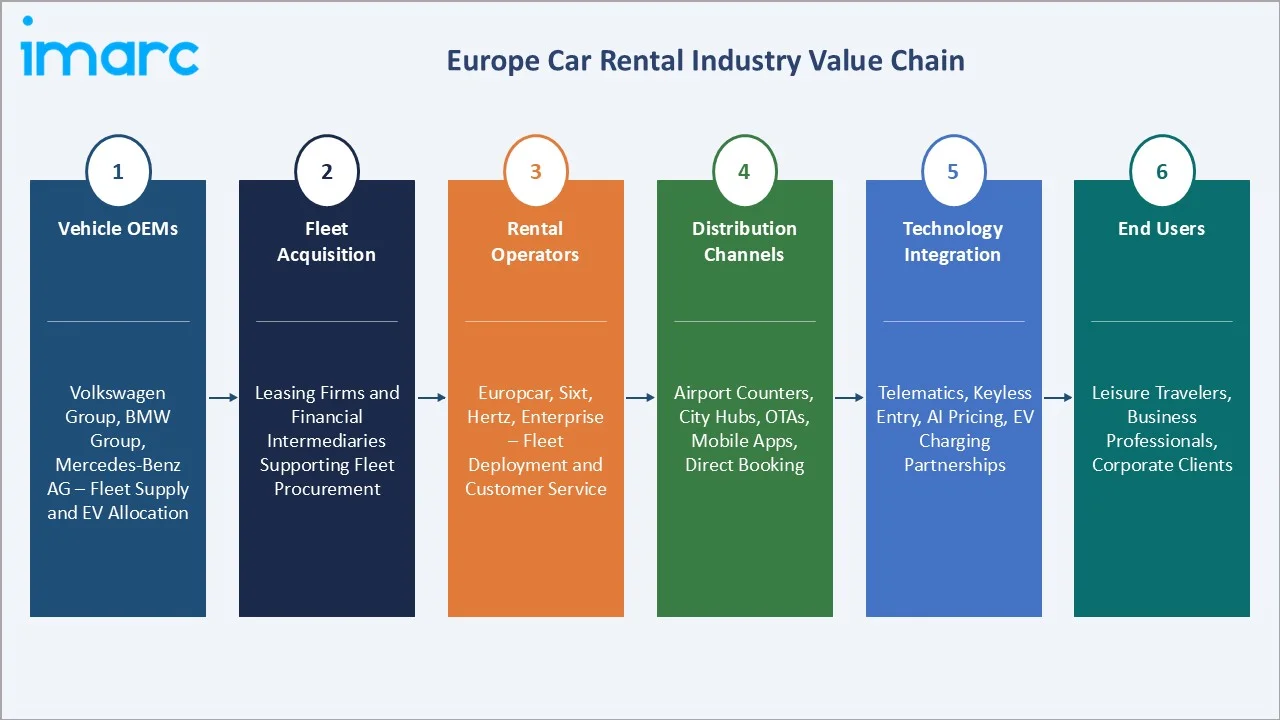

Industry Value Chain Analysis

The Europe car rental value chain spans five integrated stages from vehicle manufacturing through end-user rental. Each stage carries distinct margin profiles, capital intensity, and digital transformation priorities relevant to the overall Europe car rental market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Vehicle OEMs |

Automakers (Volkswagen, BMW Group, and Mercedes-Benz AG) supply vehicles through fleet partnerships, with increasing emphasis on electric vehicle allocation and tailored fleet specifications to meet rental operator requirements. |

|

Fleet Acquisition |

Leasing firms and financial intermediaries support fleet procurement through structured financing, leasing models, and buy-back arrangements to optimize asset lifecycle and cost efficiency. |

|

Rental Operators |

Fleet operators manage national and multi-country deployment, overseeing vehicle utilization, maintenance, pricing strategies, and customer service delivery. |

|

Distribution Channels |

Multi-channel access includes airport counters, city hubs, online travel platforms, direct booking websites, and mobile applications to enhance customer reach and convenience. |

|

Technology Integration |

Advanced technologies such as telematics, keyless entry systems, AI-driven pricing tools, and electric vehicle charging partnerships improve operational efficiency and user experience. |

|

End Users |

Demand is driven by leisure travelers, business professionals, local commuters, and corporate clients requiring flexible mobility solutions. |

Rental operators hold the highest strategic leverage by combining fleet scale, distribution reach, and digital customer experience. Meanwhile, OTAs and subscription platforms are reshaping the booking layer, enabling dynamic yield management and margin expansion.

Technology Landscape in the Car Rental Industry

Digital Booking and Mobile Platforms

Operators are consolidating bookings onto unified digital platforms offering mobile app reservations, contactless check-in, and in-app vehicle selection. Integration with Apple Pay, Google Pay, and biometric authentication is reducing counter times and improving customer NPS scores across leading markets.

Telematics and Connected Fleet Management

Connected vehicle telematics are enabling real-time fleet tracking, predictive maintenance, and fuel or energy optimization. Data-driven utilization analytics help operators reduce idle vehicle time, improve residual value management, and lower total cost of ownership across large European fleets.

EV Fleet and Charging Integration

Rental operators are partnering with Ionity, Fastned, Allego, and TotalEnergies to offer integrated charging solutions to EV renters. Smart routing, in-app charger availability, and bundled charging packages are becoming standard features across premium EV rental offerings in Germany, the Netherlands, and Scandinavia.

AI-Driven Pricing and Customer Intelligence

Machine learning-based dynamic pricing is optimizing yield across seasonality, location, and vehicle category. Customer segmentation engines are enabling personalized upsell, loyalty programmes, and targeted offers, supporting revenue growth even in flat-volume periods for mature Western European markets.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Booking Type | Offline Booking | 57.5% |

2025 |

| Rental Length | Short Term | 63.8% |

2025 |

| Vehicle Type | 🔒 | 🔒 |

2025 |

| Application | 🔒 | 🔒 |

2025 |

| End-User | 🔒 | 🔒 | 2025 |

| Country | Germany | 24.5% | 2025 |

By Booking Type

To access detailed market analysis, Request Sample

Offline booking leads the Europe car rental market with a 57.5% share in 2025. Demand is anchored by airport counter pickups, corporate rental contracts, and walk-in bookings at city-centre rental hubs. Business travellers in Germany, the UK, and France continue to rely on in-person bookings for flexibility, upgrades, and corporate billing arrangements.

By Rental Length

Short-term rentals are the dominant segment at 63.8% of Europe revenue in 2025. Demand is fuelled by leisure tourism, airport pickups, and business travel rentals typically under 10 days. Eurostat data shows EU residents took 1.16 billion tourism trips in 2024, supporting sustained short-term rental volumes across Mediterranean and Western European markets.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

24.5% |

Business travel, airport hubs, EV fleet mandates, Autobahn network |

|

United Kingdom |

19.0% |

Tourism recovery, luxury rental demand, Heathrow and Gatwick hubs |

|

France |

16.5% |

Paris 2024 Olympics legacy, leisure tourism, low-emission zones |

|

Italy |

13.5% |

Mediterranean tourism, cross-border rentals, airport concentration |

|

Spain |

11.5% |

Peak summer tourism, Canary and Balearic Islands demand |

|

Others |

15.0% |

Benelux, Nordics, Eastern Europe corporate and leisure growth |

Germany commands a 24.5% share of the Europe car rental market in 2025, making it the single largest national market. Strong business travel flows through Frankfurt, Munich, and Berlin, combined with a dense Autobahn network and a mature corporate fleet culture, underpin its leadership. Germany is also a frontrunner in EV fleet deployment, supported by government incentives and ambitious EU CO2 compliance targets.

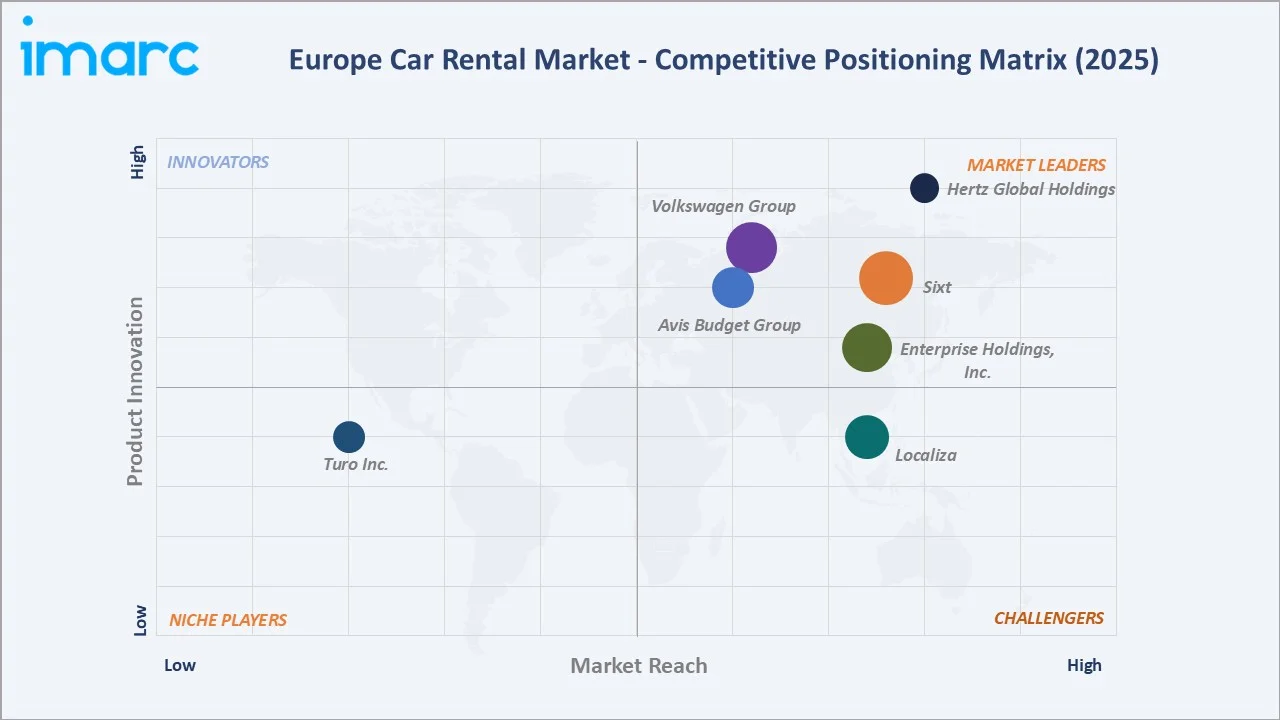

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Volkswagen Group |

Europcar, Goldcar, Euromobil |

Leader |

Pan-European scale, airport network, shared mobility |

|

Enterprise Holdings, Inc. |

National Car Rental, Alamo |

Leader |

Franchise depth, corporate contracts, US crossover travellers |

|

Sixt |

Sixt rent, Sixt+, Sixt share, Sixt ride |

Leader |

Premium fleet, digital-first strategy, EV leadership |

|

Hertz Global Holdings, Inc. |

Hertz, Dollar, Thrifty, Firefly |

Leader |

Airport dominance, EV partnerships, global loyalty programme |

|

Avis Budget Group, Inc. |

Avis, Budget, Zipcar |

Leader |

Multi-brand portfolio, car-sharing via Zipcar |

|

Localiza |

Localiza |

Challenger |

Value-tier positioning, growing European presence |

|

Turo Inc. |

Turo |

Emerging |

Peer-to-peer rentals, asset-light, Gen Z appeal |

The Europe car rental market's competitive landscape is moderately consolidated, with global leaders competing alongside regional specialists and emerging digital challengers. Leading operators compete on fleet scale, airport network coverage, EV transition pace, digital booking experience, and loyalty programme depth. Strategic moves include Europcar's acquisition by Volkswagen Group in 2022, enabling deeper OEM integration, fleet supply advantages, and mobility-as-a-service synergies.

Key Company Profiles

Volkswagen Group

Volkswagen Group is one of the world’s largest automotive manufacturers, headquartered in Wolfsburg, Germany. The company operates as a global leader in passenger cars, commercial vehicles, and mobility solutions.

- Product & Platform Portfolio: Volkswagen Group’s portfolio spans the Europcar, Goldcar, Euromobil brands, covering short-term rentals, low-cost leisure rentals, Mediterranean tourism, and round-trip car-sharing platforms across major European cities.

- Recent Developments: In 2022, A consortium led by Volkswagen Group secured a controlling stake in Volkswagen Group after acquiring 87.38% of its shares through a takeover bid. This gave the consortium effective control of the rental company, marking a major step in Volkswagen’s strategy to expand into mobility and rental services.

- Strategic Focus: Volkswagen Group’s strategy centers on pan-European digital platform consolidation, and expansion into subscription and shared mobility segments, particularly in Germany, France, and Southern Europe.

Sixt

Sixt is Germany's largest international vehicle rental company and one of Europe's premium mobility brands, headquartered in Pullach, Germany. Sixt operates in over 100 countries and has rapidly scaled in the United States while retaining European market leadership in premium rentals.

- Product & Platform Portfolio: Sixt's portfolio includes Sixt rent (short-term rental), Sixt+ (monthly flexible subscription), Sixt share (car-sharing), and Sixt ride (chauffeur and ride-hailing). The ONE app integrates all services into a single digital interface.

- Recent Developments: In 2026, Sixt has launched its new global loyalty programme Sixt One, expanding it into European markets after its initial rollout in the US. The programme replaces the earlier Advantage Circle scheme and introduces a two-tier points system: customers earn status points (to unlock higher membership tiers like Silver, Gold, Platinum and Diamond) and rental points, which can be redeemed for discounts on future bookings and other benefits.

- Strategic Focus: Sixt's strategy focuses on digital-first customer experience, premium and luxury vehicle positioning, fleet electrification, and continued international expansion, with particular emphasis on the US market and transatlantic business traveller flows.

Hertz Global Holdings, Inc.

Hertz Global Holdings, Inc. is a leading global car rental and mobility solutions provider headquartered in Estero, Florida, USA. The company is one of the largest vehicle rental operators worldwide, with a strong legacy in the mobility industry.

- Product & Platform Portfolio: Hertz's European portfolio covers premium airport rentals under the Hertz brand, value rentals under Dollar and Thrifty, and commercial fleet services. The Gold Plus Rewards programme integrates European operations with global loyalty benefits.

- Recent Developments: In 2026, Hertz announced its collaboration with Uber, wherein the ride-hailing company would rent 25,000 electric vehicles to its drivers in European capitals by 2025. The rollout of the rental deal will include models from Tesla and Polestar that were made available to Uber drivers in the London region, while the company is planning to add 10,000 more EVs by 2025.

- Strategic Focus: Hertz's European strategy centres on airport concession leadership, optimized EV-ICE fleet mix, premium leisure rentals, and transatlantic loyalty integration, leveraging US traveller demand flowing into European destinations.

Market Concentration Analysis

The Europe car rental market exhibits moderate-to-high consolidation. The top five players - Volkswagen Group, Enterprise Holdings, Inc., Sixt, Hertz Global Holdings, Inc., Avis Budget Group, Inc.- collectively account for approximately 60-68% of European revenue in 2025. The remaining share is distributed across regional specialists, low-cost Mediterranean operators, and emerging peer-to-peer and subscription platforms.

The market is undergoing a bifurcated dynamic. At the premium and corporate tier, consolidation is intensifying around OEM partnerships, fleet scale, and digital platform capability. Simultaneously, asset-light models such as peer-to-peer platforms and monthly subscriptions are creating new competitive pressure from digital-native challengers. This dual dynamic is expected to reshape the European rental competitive landscape through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Online booking is the highest-growth distribution channel at approximately 12.6% CAGR through 2034. Long-term rentals and subscription offerings are the fastest-growing rental length category among younger urban consumers. EV-specific rentals represent the premium technology growth opportunity.

Emerging Country Markets

Eastern Europe and the Nordics represent high-potential growth markets, supported by rising inbound tourism, corporate mobility transformation, and EV infrastructure investment. Poland, the Czech Republic, Sweden, and Norway collectively offer significant volume expansion opportunities for operators with localized digital capabilities and multi-brand fleet strategies.

Venture and Strategic Investment Trends

Strategic acquisitions are reshaping the European rental landscape. Volkswagen's acquisition of Europcar in 2022 created a vertically integrated mobility platform. Investments in EV charging partnerships, AI-led pricing engines, and subscription-model startups such as Finn Auto are the primary focus areas for venture and corporate capital through 2034.

Future Market Outlook (2026-2034)

The Europe car rental market forecast projects steady value expansion from USD 25.6 Billion in 2025 to USD 63.0 Billion by 2034 at a CAGR of 10.55%. Germany will retain country leadership while the UK and France sustain premium value growth through tourism recovery, corporate mobility transformation, and EV integration.

Three structural shifts will reshape the European rental market through the next decade. First, digital-first booking will dominate transactions, reducing reliance on counter-based operations.

Second, fleet electrification will expand significantly, driven by EU CO₂ mandates and urban low-emission zones. Third, subscription and peer-to-peer models will gain traction among younger urban consumers, creating a more diverse and competitive ecosystem across pricing tiers and service formats.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with Europe car rental industry stakeholders, including fleet directors at major rental operators, procurement managers at corporate mobility platforms, airport concession authorities, and institutional investors in mobility services. Primary insights validated market sizing, segmentation estimates, and EV adoption timelines.

Secondary Research

Secondary sources include Eurostat travel and tourism data, UN Tourism reports, European Automobile Manufacturers Association (ACEA) statistics, European Environment Agency (EEA) reports, company annual reports and investor presentations, trade publications such as BusinessCar and Fleet Europe, and country-level tourism and transport authority databases.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, tourist arrival data, business travel spend, fleet replacement cycles, and EV adoption trajectories. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic and regulatory uncertainty.

Europe Car Rental Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Booking Types Covered | Offline Booking, Online Booking |

| Rental Lengths Covered | Short Term, Long Term |

| Vehicle Types Covered | Luxury, Executive, Economy, SUVs, Others |

| Applications Covered | Leisure/Tourism, Business |

| End-Users Covered | Self-Driven, Chauffeur-Driven |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Volkswagen Group, Enterprise Holdings, Inc., Sixt, Hertz Global Holdings, Inc., Avis Budget Group, Inc., Localiza, Turo Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe car rental market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe car rental market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe car rental industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Car Rental Market Report

The Europe car rental market was valued at USD 25.6 Billion in 2025, driven by tourism recovery, digitalization of booking channels, and growing demand for flexible short-term mobility.

The market is projected to reach USD 63.0 Billion by 2034, growing at a CAGR of 10.55% during 2026-2034, supported by EV fleet integration, subscription mobility, and digital booking platforms.

Offline booking leads with a 57.5% share in 2025, driven by airport counter demand, corporate rental contracts, and walk-in bookings across Germany, the UK, and France.

Online booking is the fastest-growing channel, expanding at an estimated CAGR of 12.6% through 2034, driven by mobile apps, OTAs, and direct-to-consumer digital rental platforms.

Germany dominates with a 24.5% share in 2025, supported by strong business travel, dense airport network, mature corporate fleet culture, and EV adoption leadership.

Key drivers include post-pandemic tourism recovery, mobile-first booking adoption, EV fleet electrification under EU CO2 rules, subscription mobility models, and cross-border travel within Schengen.

Major players include Volkswagen Group, Enterprise Holdings, Inc., Sixt, Hertz Global Holdings, Inc., Avis Budget Group, Inc., Localiza, and Turo Inc.

Short-term rentals remain the largest segment at 63.8%, while long-term rentals and subscriptions are gaining traction fastest, particularly in Germany, the Netherlands, and the United Kingdom.

EVs accounted for over 8% of rental fleets in 2025 and are projected to exceed 25% by 2030, driven by EU CO2 regulations, low-emission zones, and operator electrification commitments.

Key opportunities include EV fleet expansion, charging network partnerships, subscription and peer-to-peer platforms, AI-led dynamic pricing, and Eastern European market expansion.

Short-term rentals dominate with a 63.8% share in 2025, supported by leisure tourism, airport pickups, and intra-European business travel across Germany, the UK, France, Italy, and Spain.

Digitalization is reshaping bookings, with mobile apps and OTAs driving over 38% of digital transactions and enabling contactless check-in, dynamic pricing, and AI-led personalization across operators.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)