Europe Craft Beer Market Size, Share, Trends and Forecast by Product Type, Age Group, Distribution Channel, and Country 2026-2034

Europe Craft Beer Market Size, Share, Trends & Forecast (2026-2034)

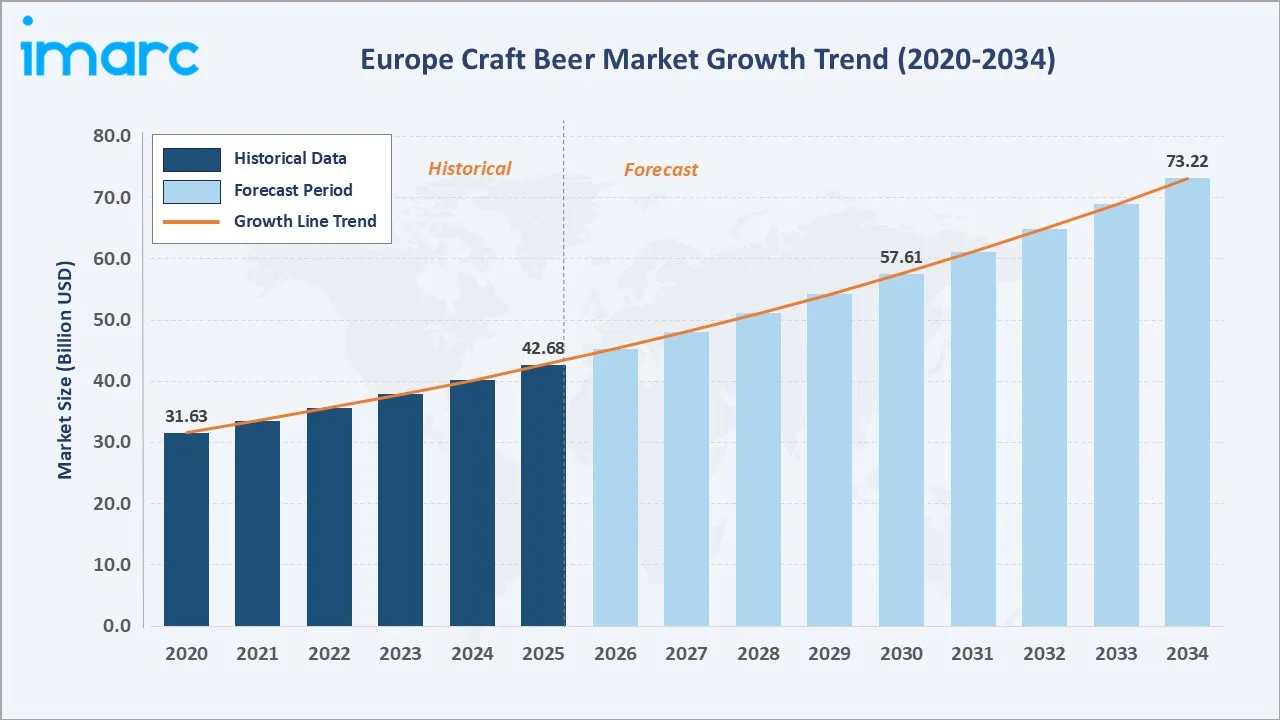

The Europe craft beer market size was valued at USD 42.7 Billion in 2025 and is projected to reach USD 73.2 Billion by 2034, exhibiting a CAGR of 6.18% during 2026-2034. Rising consumer preference for premium artisanal beverages, surging microbrewery proliferation across Germany, the UK, and France, and a sustained shift toward flavour diversity are the primary growth drivers. Ales dominate product type with a 58.4% share in 2025, while On-Trade channels account for 56.4% of revenue. Germany leads regional markets at 28.4%, followed by the United Kingdom at 22.6%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 42.7 Billion |

|

Forecast Market Size (2034) |

USD 73.2 Billion |

|

CAGR (2026-2034) |

6.18% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (28.4% share, 2025) |

|

Fastest Growing Country |

France (~8.2% CAGR, 2020-2025) |

|

Leading Product Type |

Ales (58.4%, 2025) |

|

Leading Distribution Channel |

On-Trade (56.4%, 2025) |

Figure 1 below illustrates the Europe craft beer market growth trend from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by microbrewery growth and premiumisation dynamics.

To get more information on this market, Request Sample

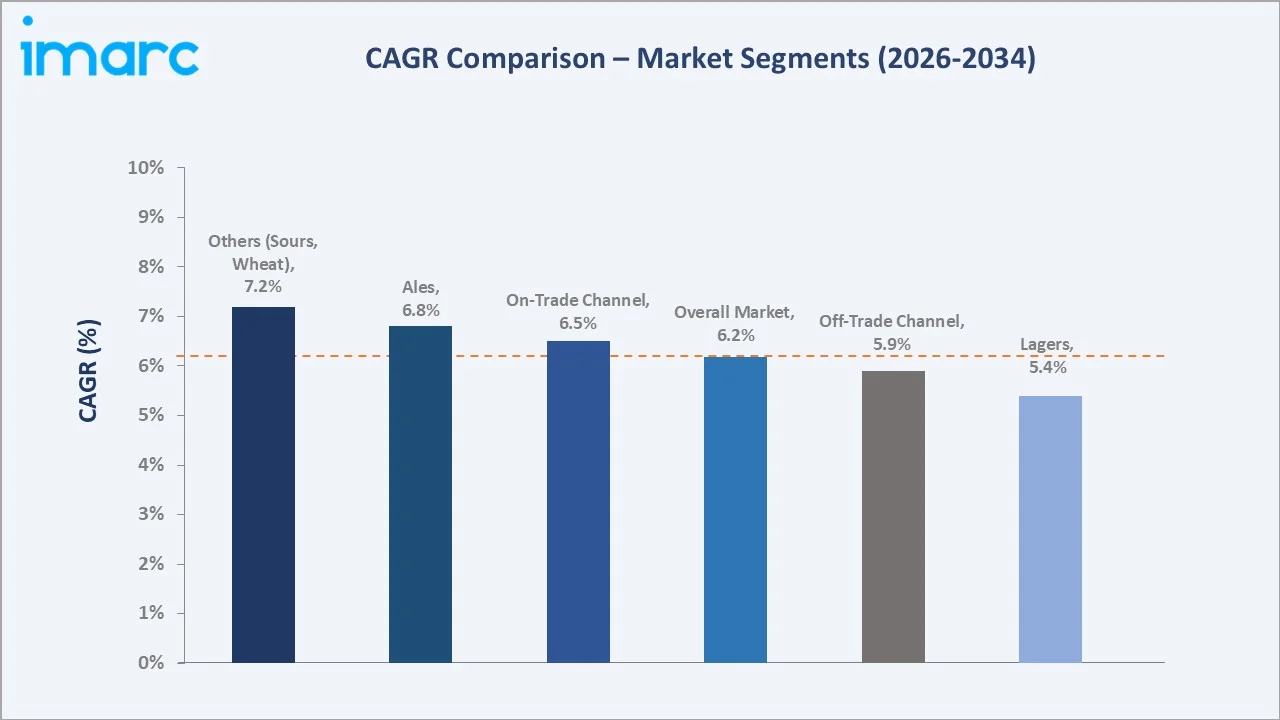

Figure 2 presents segment-level CAGR comparisons, with Others and On-Trade channels emerging as the two fastest-growing sub-categories within the Europe craft beer industry analysis through 2034.

Executive Summary

The Europe craft beer market is undergoing a structural transformation driven by premiumisation, localisation, and evolving distribution dynamics. Valued at USD 42.7 Billion in 2025, the market is forecast to reach USD 73.2 Billion by 2034 at a CAGR of 6.18%. The Brewers of Europe reported over 10,000 registered breweries on the continent as of 2024 - the highest concentration globally - underscoring the market's depth and competitive vitality.

Ales command a dominant 58.4% product type share in 2025, driven by consumer appetite for complex flavour profiles including IPAs, stouts, and sour ales, alongside growing interest in sessionable low-ABV variants. Lagers hold 30.3% in 2025 and are expanding through craft lager positioning in Germany and Central Europe. The On-Trade channel at 56.4% in 2025 remains primary, though Off-Trade is growing faster as e-commerce platforms and specialist retailers broaden consumer access.

Germany leads the regional landscape with a 28.4% share in 2025, supported by over 1,500 active breweries and deep brewing heritage. The United Kingdom holds 22.6%, with BrewDog's profile and London's vibrant taproom culture reinforcing growth. France at 18.3% and Italy at 14.2% are the fastest-rising markets, driven by a young consumer base and gastronomy-linked craft consumption.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type Segment |

Ales - 58.4% share (2025) |

|

Second Product Type Segment |

Lagers - 30.3% share (2025) |

|

Leading Distribution Channel |

On-Trade - 56.4% revenue share (2025) |

|

Largest Country |

Germany - 28.4% revenue share (2025) |

|

Second Country |

United Kingdom - 22.6% revenue share (2025) |

|

Top Companies |

AB InBev, Heineken, Carlsberg, BrewDog, Duvel Moortgat |

|

Market Opportunity |

Low-ABV craft variants; Eastern Europe expansion; DTC e-commerce |

Key Analytical Observations Supporting the Above Data:

- Ales' 58.4% dominance in 2025 reflects the industry-wide shift toward complex hop-forward styles - IPAs, pale ales, and stouts - as craft consumers demonstrate higher willingness to pay for distinctive flavour profiles.

- On-Trade channel's 56.4% share underscores the experiential nature of craft beer consumption; taprooms, craft pubs, and brewery bars continue to serve as primary trial and discovery venues across Europe.

- Germany's 28.4% leadership reflects its dual advantage of deep brewing tradition and active innovation - the country added over 80 new craft breweries between 2022 and 2024.

- France is Europe's fastest-growing craft beer market, with total craft volumes growing at approximately 8.2% CAGR (2020-2025), fuelled by gastronomy culture and a young urban consumer base.

- The Others segment (sours, wheat beers, experimental hybrids) at 11.3% in 2025 is projected to outperform all major segments through 2034 at a CAGR of approximately 7.2%.

- E-commerce penetration in off-trade craft beer sales reached approximately 14% across Europe in 2024, up from 6% in 2020, representing an accelerating structural channel shift.

Europe Craft Beer Market Overview

Craft beer refers to beer produced by independent, small-scale breweries that prioritise quality, flavour complexity, and traditional or innovative brewing techniques over mass production volume. The European craft beer ecosystem spans a rich continuum from centuries-old regional brewpubs to cutting-edge experimental microbreweries and contract-brewed premium labels targeting on-trade and e-commerce channels.

Applications span all on-trade hospitality environments and an expanding off-trade universe of supermarkets, specialist beer retailers, and e-commerce subscription platforms. Macroeconomic enablers include rising disposable incomes across Southern and Eastern Europe, a robust tourism-linked hospitality recovery post-2022, and strong EU regulatory support for origin-designated beer products - including German Reinheitsgebot heritage and Belgian beer UNESCO cultural heritage status.

Market Dynamics

To evaluate market opportunities, Request Sample

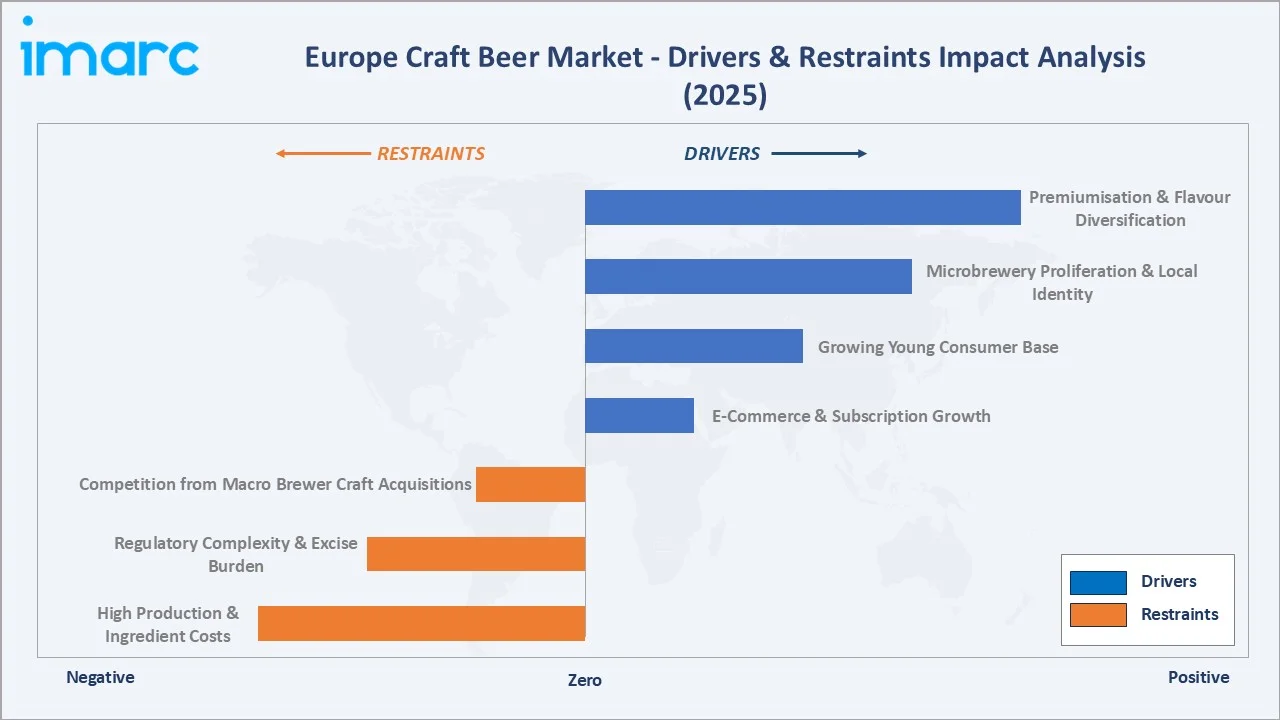

Market Drivers

- Premiumisation and Flavour Diversification: European consumers, particularly millennials aged 25-40, are actively trading up from standard lagers to premium craft variants. Euromonitor estimated that premium and super-premium beer volumes grew at 3x the rate of mainstream beer in Western Europe during 2021-2024, creating a structural demand upgrade cycle.

- Microbrewery Proliferation and Local Identity: The Brewers of Europe confirmed over 10,000 breweries across the continent in 2024. Germany, France, and the UK are among the top European nations for brewery counts, contributing significantly to the total, particularly when including the rapid rise of microbreweries, although precise percentages vary by source and year. Each new microbrewery generates distribution demand, local consumer loyalty, and regional identity.

- Growing Young Consumer Base: The 21-35 age cohort represents over 48% of European craft beer consumption by volume in 2025. In the UK, 63% of craft beer drinkers aged 18-34 reported consuming craft beer at least weekly in 2024 (YouGov), reflecting durable long-term structural demand.

- E-Commerce and Subscription Growth: Online beer sales in Europe grew at robust CAGR between 2020 and 2024. Beer52, Saveur Bière, and Beer Hawk are major players in the European craft beer market, offering subscription services and curated selections, materially expanding off-trade reach for small independent breweries.

Market Restraints

- High Production and Ingredient Costs: Based on recent industry data, European hop prices experienced notable volatility and an upward trend due to climate-linked yield disruption in Hallertau (Germany) and Saaz (Czech Republic) growing regions, compressing margins for smaller breweries.

- Regulatory Complexity and Excise Burden: European craft brewers navigate a fragmented regulatory landscape with differing excise duty structures across member states, raising cross-border distribution costs and limiting pan-European scaling for emerging brands.

- Competition from Macro Brewer Craft Acquisitions: AB InBev, Heineken, and Carlsberg have all made craft brewery acquisitions in Europe since 2018, deploying major-brewer distribution networks behind craft-positioned brands that intensify competitive pressure on independent operators.

Market Opportunities

- Low-ABV and No-ABV Craft Variants: Europe’s no-alcohol beer segment is set for steady growth through the forecast period, reflecting rising consumer interest in moderation and healthier drinking choices. Craft brewers are particularly well-positioned to capture this momentum, leveraging their strength in flavour innovation and small-batch experimentation

- Eastern European Market Expansion: Poland, Czech Republic, and Romania collectively represent an underpenetrated craft beer opportunity - craft beer accounts for a minimal share of total beer volumes in these markets in 2025, versus a significantly higher share in Western Europe.

- Festival and Tourism-Linked Demand: Europe’s craft beer festival economy generated substantial revenues in 2024, with events like and providing high-margin trial and brand-building channels.

Market Challenges

- Shelf Space Competition in Off-Trade: Supermarket and retail shelf space is dominated by macro-brewer SKUs, making consistent listings difficult for independent craft breweries facing slotting fees, volume thresholds, and frequent product rotations.

- Supply Chain Fragmentation: Many small breweries rely on spot purchasing for hops, malt, and packaging materials, creating vulnerability to ingredient price spikes and quality inconsistency that is compounded by limited cold-chain infrastructure in parts of Eastern Europe.

Emerging Market Trends

1. Sustainability and Green Brewing Practices

Sustainability has evolved from a marketing differentiator to a core operational requirement for European craft brewers. The EU Green Deal and ESG consumer expectations are driving rapid adoption of solar-powered brewhouses, water recycling systems, and circular economy grain models. BrewDog's Ellon facility - the world's first carbon-negative brewery - remains the benchmark, attracting thousands of visitors and reinforcing its premium brand equity through sustainability credentials.

2. Low-ABV and No-ABV Craft Innovation

Consumer health consciousness is catalysing rapid NPD in low-and-no-alcohol craft beer across Europe. The IWSR projected Europe's no-ABV beer segment at a steady CAGR through 2027. Craft brewers are innovating with vacuum distillation and arrested fermentation techniques to produce no-ABV variants maintaining the flavour complexity of full-strength craft products.

3. Hyperlocal Taproom-Centric Distribution Models

The taproom model - where breweries sell direct-to-consumer at on-site venues - is reshaping craft beer revenue structure. Taprooms capture 2-3x the margin of wholesale distribution and build direct consumer relationships.

4. Cross-Category Collaboration and Experimental Styles

European craft brewers increasingly collaborate with distilleries, wineries, coffee roasters, and food producers to create hybrid limited-edition products. Barrel-aged stouts finished in Scotch whisky casks, sour ales aged on Burgundy wine lees, and cold brew coffee-infused porters are driving media attention, collector behaviour, and premium price positioning at EUR 15-30 per 750ml bottle.

5. E-Commerce and Direct-to-Consumer Scaling

Post-pandemic DTC infrastructure for craft beer has matured significantly. Beer52 and Beerhawk now offer subscription models with 50,000+ aggregate European subscribers. DTC generates 25-40% higher net revenue per litre compared to wholesale channels while building proprietary consumer data assets unavailable through traditional distributor relationships.

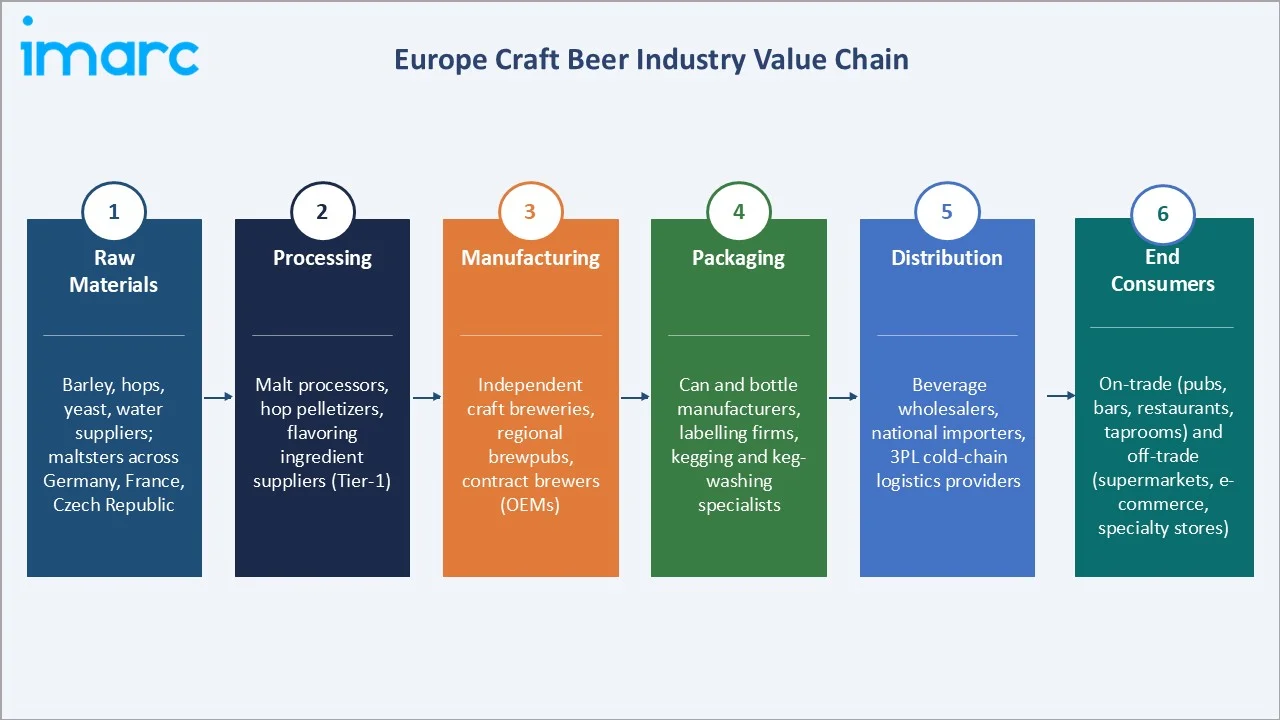

Industry Value Chain Analysis

The Europe craft beer value chain spans six integrated stages from raw ingredient supply through end-consumer access. Each stage presents distinct competitive dynamics, margin profiles, and sustainability investment requirements for both incumbents and new entrants.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Barley, hops, yeast, water suppliers; maltsters across Germany, France, Czech Republic |

|

Processing |

Malt processors, hop pelletisers, flavouring ingredient suppliers (Tier-1) |

|

Manufacturing |

Independent craft breweries, regional brewpubs, contract brewers (OEMs) |

|

Packaging |

Can and bottle manufacturers, labelling firms, kegging and keg-washing specialists |

|

Distribution |

Beverage wholesalers, national importers, 3PL cold-chain logistics providers |

|

End Consumers |

On-trade (pubs, bars, restaurants, taprooms) and off-trade (supermarkets, e-commerce, specialty stores) |

Independent craft breweries occupy the highest-value position within the chain, capturing premium margins through brand differentiation, recipe innovation, and taproom direct sales. Hop and malt procurement represents the most cost-sensitive stage, with ingredient costs accounting for 30-40% of craft beer's total cost of goods in 2025.

Technology Landscape in the Craft Beer Industry

Brewing Process Innovation

Advanced fermentation control systems - including programmable temperature-gradient fermenters and real-time dissolved oxygen monitoring - have reduced batch inconsistency rates by approximately 30-40% in modern craft installations. Automated brewing systems from Briggs of Burton (UK) and Kaspar Schulz (Germany) allow small-batch precision at competitive capital expenditure levels.

Sustainability and Energy Technology

Solar PV integration, heat recovery from fermentation and pasteurisation, and anaerobic digestion of spent grain are becoming standard practice among Europe's leading craft operators. BrewDog's Ellon facility achieves approximately 95% renewable energy supply - an increasingly cited benchmark among ESG-conscious investors and regulatory bodies.

Packaging and Quality Control

Canned craft beer accounts for a significant share of craft beer off-trade volume in the in 2024, marking a sharp increase from earlier years. High-speed small-batch canning lines from and have made canning economically viable for breweries operating at relatively small production scales.

Digital and E-Commerce Infrastructure

CRM and brewery management platforms including OrchestratedBEER and BreweryDB allow craft producers to manage taproom sales, e-commerce fulfilment, and distributor inventory from a unified digital interface.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Product Type | Ales | 58.4% |

2025 |

| Age Group | 🔒 | 🔒 |

2025 |

| Distribution Channel | On-Trade | 56.4% |

2025 |

| Country | Germany | 28.4% |

2025 |

By Product Type

Ales dominate the Europe craft beer market at 58.4% of total revenue in 2025. The segment encompasses IPAs, pale ales, stouts, porters, sour ales, and Belgian-style ales - providing continuous consumer novelty. IPAs alone represent the largest style sub-segment, growing at approximately 8% annually in the UK between 2020 and 2024. Ales are projected to maintain dominance through 2034 at a CAGR of approximately 6.8%.

To access detailed market analysis, Request Sample

Lagers hold 30.3% in 2025. Craft lager is gaining rapid traction in Germany and Czech Republic, where brewing heritage creates high consumer receptivity to premium lager positioning. Brands like Augustiner and Budvar have bridged craft quality with lager accessibility.

The chart above confirms ales' overwhelming market leadership at 58.4%, with lagers at 30.3% and the others segment at 11.3% reflecting growing appetite for style experimentation and flavour innovation.

By Distribution Channel

The On-Trade channel leads with a 56.4% revenue share in 2025. Pubs, bars, restaurants, brewery taprooms, and festival venues serve as the primary craft beer discovery and consumption environment across Europe. The UK's pub estate (~47,000 licensed premises in 2024), Germany's Biergarten culture, and Belgium's historic cafe tradition collectively underpin strong structural on-trade demand.

The Off-Trade channel at 43.6% in 2025 is the faster-growing segment, driven by supermarket craft beer shelf expansion and e-commerce subscription growth. UK supermarket chains including Waitrose, Marks & Spencer, and Tesco have substantially expanded craft ranges since 2022.

The distribution split reflects the enduring centrality of experiential on-trade consumption while demonstrating the structural expansion underway in off-trade and e-commerce - a dual-channel growth dynamic underpinning sustained market expansion through 2034.

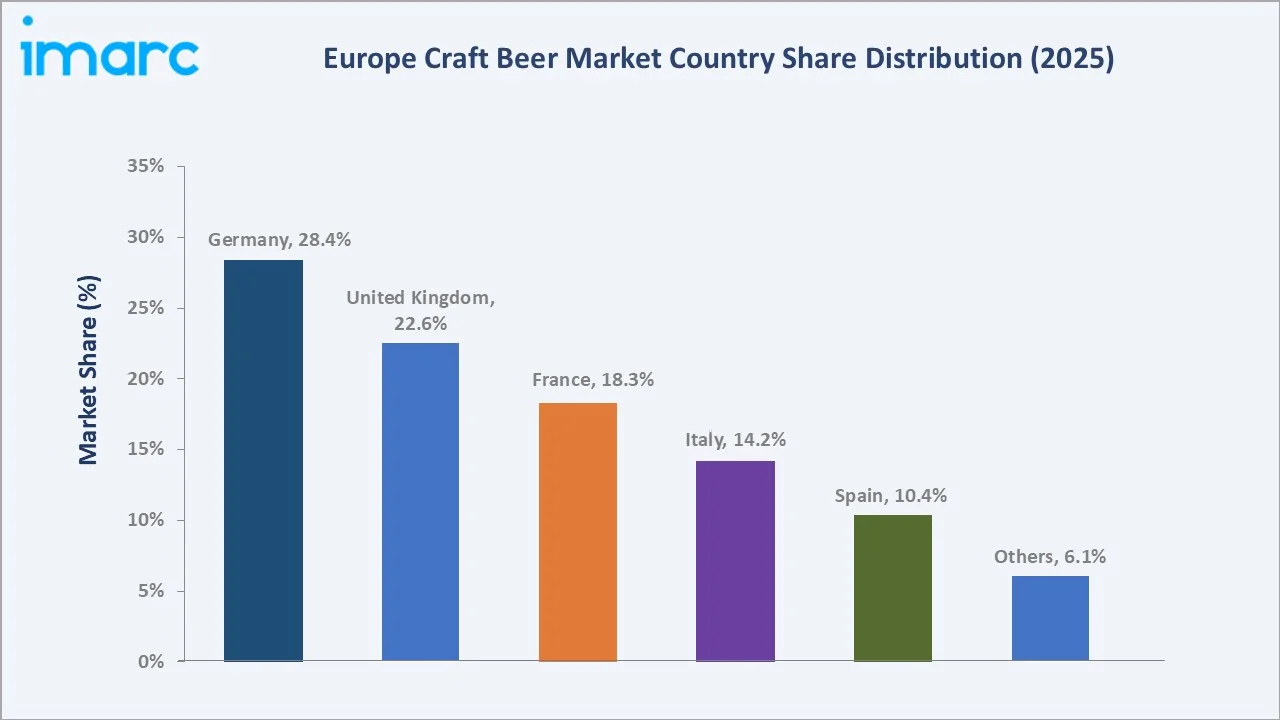

Regional Market Insights

Germany leads with a 28.4% revenue share in 2025. The country hosts over 1,500 craft breweries and benefits from the world's most codified beer culture including UNESCO-recognised brewing traditions. Germany's craft beer market is experiencing a significant shift toward premiumization and diverse, artisanal flavors, with notable growth observed in specialty, low-alcohol, and non-alcoholic segments

The United Kingdom accounts for 22.6% of Europe's craft beer market in 2025. BrewDog is Europe's largest craft brewery by volume. CAMRA drives on-trade demand while the UK's robust e-commerce infrastructure supports rapid off-trade growth. France holds 18.3% and is the continent's fastest-growing craft beer nation, expanding at approximately 8.2% CAGR (2020-2025) driven by gastronomy culture and a young urban consumer base in Paris, Lyon, and Bordeaux.

Italy at 14.2% represents Europe's most artisanal craft beer culture, with strong food-tourism linkage in Piedmont and Lombardy driving premium positioning. Spain holds 10.4%, with Barcelona and Madrid emerging as primary craft consumption hubs. The Others category (Belgium, Netherlands, Denmark, Poland, and remaining markets) collectively accounts for 6.1% but represents a high-growth frontier as Eastern European markets develop.

Competitive Landscape

The Europe craft beer competitive landscape is highly fragmented at its base, with over 11,000 breweries competing for market share, while the upper tier is consolidating as major international brewers acquire or partner with established craft brands to capture premiumisation momentum.

|

Company Name |

Brand Name |

Market Position |

|

AB InBev |

Goose Island |

Market Leader |

|

Heineken N.V. |

Lagunitas / Affligem |

Market Leader |

|

Carlsberg Group |

Jacobsen |

Major Challenger |

|

BrewDog PLC |

BrewDog / LostPunk |

Challenger |

|

Duvel Moortgat |

Duvel / Brasserie Chouffe |

Established Challenger |

|

Mikkeller |

Mikkeller / Baghaven |

Craft Innovator |

|

Cloudwater Brew Co. |

Cloudwater / Hazy Series |

Emerging Player |

|

Brasserie du Mont Blanc |

Mont Blanc / La Rousse |

Regional Player |

The competitive dynamics are characterised by a three-tier structure: global leaders with craft portfolio exposure through acquisitions; established independents with pan-European distribution; and a large base of hyper-local microbreweries and taproom-centric producers operating in geographically bounded markets.

Key Company Profiles

AB InBev (Goose Island)

AB InBev is the world's largest brewer by volume, with extensive European craft market exposure through Goose Island (distributed pan-Europe) and several regional craft label acquisitions since 2015. AB InBev mainstream beer portfolio represented approximately 50% of its FY24 revenue and delivered low-single digit revenue growth, with increases in 60% of its markets, including high-single digit growth in South Africa and Colombia.

Heineken N.V. (Lagunitas / Affligem)

Heineken holds a 28.9% global beer market share and has strategically diversified into craft through a Lagunitas (European distribution) and its Belgian abbey beer range. Over 2019-2024, the company has been able to increase market shares against some of its direct peers. According to Euromonitor, Heineken has a global market share within the beer category of about 12.4% (in terms of volume 2024), up from about 11% in 2019.

BrewDog PLC (BrewDog / LostPunk)

BrewDog is Europe's largest independent craft brewery by revenue with operations across the UK, Germany (DogTap Berlin), and 100+ licensed bars across Europe. The company was the first brewery globally to achieve carbon-negative status in 2020, with Punk IPA and Lost Lager as its highest-volume European products.

Carlsberg Group (Jacobsen)

Carlsberg holds a moderate share in European beer market share and competes in the craft segment through its Jacobsen Danish craft range and European Brooklyn Brewery distribution. Carlsberg Group is increasing investments in premium and alcohol-free segments as part of its growth strategy.

Duvel Moortgat (Duvel / Brasserie Chouffe)

Duvel Moortgat is Belgium's most respected independent craft operator, with brands including Duvel, Brasserie Chouffe, Vedett, and Firestone Walker (imported). Duvel Golden Strong Ale remains one of Europe's highest-rated craft beers on specialist review platforms.

Mikkeller (Mikkeller / Baghaven)

Mikkeller is Denmark's most internationally celebrated craft brewery, recognised for boundary-pushing experimental styles and global collaboration networks. The brewery operates 60+ Mikkeller Bar locations globally and generates significant premium margins through limited-release collector products, with its Baghaven facility representing the vanguard of European wild-fermentation craft.

Market Concentration Analysis

The Europe craft beer market exhibits a dual-layer concentration structure. At the macro level, AB InBev, Heineken, and Carlsberg collectively control approximately 55-60% of total European beer volumes in 2025 through combined mainstream and craft portfolios. Within the pure-play craft segment, the top five independent operators account for less than 18% of pure craft revenues, reflecting intense fragmentation at the artisanal production base.

The Herfindahl-Hirschman Index (HHI) for the pure craft segment in Europe is estimated below 500, characterising a highly competitive, low-concentration market. Consolidation is expected to accelerate from 2026-2030 as smaller breweries face rising ingredient costs and distribution challenges, attracting acquisition interest from mid-tier consolidators and private equity. Geographic concentration shows Germany and the UK jointly representing 51% of the total market in 2025.

Investment & Growth Opportunities

Fastest Growing Segments

The Others product segment (sours, wheat, experimental) at a projected 7.2% CAGR through 2034 represents the highest-growth sub-category. No-ABV and low-ABV craft variants within the ales segment also outpace the overall market by 150-200 basis points annually, supported by health-conscious consumer trends.

Emerging Market Expansion

Eastern European markets - Poland, Czech Republic, Hungary, and Romania - represent the highest-upside geographic opportunity. Craft beer penetration below 3% of total beer volumes, combined with rising millennial incomes and strong beer culture, positions these markets for sustained double-digit craft growth through 2030. Poland saw craft brewery count increase from 160 in 2018 to over 400 in 2024.

Private Equity and Venture Investment

The European craft beer sector attracted significant private equity and venture capital investment between 2021 and 2024. Key investment themes include direct-to-consumer e-commerce platforms, craft beer subscription services, brewery consolidation plays in the mid-sized revenue band, and sustainability technology for brewing operations.

Future Market Outlook (2026-2034)

The Europe craft beer market's growth through 2034 will be shaped by continued premiumisation, accelerating e-commerce penetration, and a growing sustainability imperative. Market revenues are projected to reach USD 73.2 Billion by 2034 from USD 42.7 Billion in 2025 at a CAGR of 6.18%. Geographic expansion into Eastern Europe, sustained innovation in low-ABV formats, and the maturation of France and Italy as primary growth markets will collectively drive performance.

Technological disruption in the form of AI-assisted recipe development, precision fermentation, and small-batch production robotics will progressively reduce the cost-premium of craft vs. mainstream beer - widening addressable consumer demographics and enabling craft breweries to compete more effectively on price in off-trade retail environments by the early 2030s.

Research Methodology

Primary Research

IMARC's primary research involved in-depth interviews with senior executives across the craft beer value chain, including independent brewery founders, distribution managers, retail category directors, and beverage-sector investment analysts. Primary interviews were conducted across Germany, UK, France, Italy, and Belgium during Q3-Q4 2025.

Secondary Research

Secondary sources included industry publications from the Brewers of Europe, CAMRA, Euromonitor International, IWSR Drinks Market Analysis, trade journals (The Grocer, Off Licence News, Brauwelt), company annual reports, government excise duty statistics, and IMARC's proprietary market intelligence databases across 50+ countries.

Forecasting Models

Market sizing applied a triangulated approach combining top-down macroeconomic modelling (GDP growth, per-capita alcohol expenditure, premiumisation elasticity) with bottom-up segment analysis (volume by style, distribution channel split, country-level CAGR differentiation). Historical data from 2020-2025 was validated against publicly disclosed brewer financial results and trade association volume statistics.

Europe Craft Beer Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Ales, Lagers, Others |

| Age Groups Covered | 21-35 Years Old, 40-54 Years Old, 55 Years and Above |

| Distribution Channels Covered | On-Trade, Off-Trade |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | AB InBev, Heineken N.V., Carlsberg Group, BrewDog PLC, Duvel Moortgat, Mikkeller, Cloudwater Brew Co., Brasserie du Mont Blanc, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe craft beer market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe craft beer market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe craft beer industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Craft Beer Market Report

The Europe craft beer market was valued at USD 42.7 Billion in 2025, driven by premiumisation, microbrewery growth, and rising consumer preference for artisanal flavour-forward beverages across Western and Eastern Europe.

The market is projected to reach USD 73.2 Billion by 2034 at a CAGR of 6.18% during 2026-2034, supported by DTC expansion, low-ABV innovation, and Eastern European market development.

Ales lead with a 58.4% revenue share in 2025, driven by IPA popularity, stout consumption, and continuous flavour innovation across the UK, Germany, and Belgium craft ecosystems.

The On-Trade channel holds 56.4% share in 2025. Pubs, bars, taprooms, and restaurants remain primary craft beer consumption and discovery environments across the continent.

Germany leads with a 28.4% revenue share in 2025, supported by over 1,500 active breweries, deep brewing heritage, and a strong on-trade Biergarten and festival economy.

France is growing at approximately 8.2% CAGR (2020-2025), the fastest among major European markets, driven by gastronomy culture and a young urban millennial consumer base.

Key drivers include premiumisation trends, microbrewery proliferation exceeding 11,000 breweries, growing 21-35 consumer cohort, e-commerce expansion at 22% CAGR (2020-2024), and low-ABV craft demand.

Leading companies include AB InBev, Heineken N.V., Carlsberg Group, BrewDog PLC, Duvel Moortgat, Mikkeller, Cloudwater Brew Co., and Brasserie du Mont Blanc, spanning market leaders, challengers, and emerging craft specialists.

Pure craft is highly fragmented with estimated HHI below 500. Top 5 independent brewers hold under 18% share. Consolidation is expected to accelerate from 2026 to 2030 driven by cost pressures.

Off-Trade at 43.6% in 2025 is the faster-growing channel. E-commerce within off-trade grew at approximately 22% CAGR (2020-2024) and is projected to reach 22% of off-trade volume by 2030.

Top opportunities include low-ABV innovation, Eastern European expansion (craft penetration below 3%), DTC e-commerce scaling, sustainability branding, and cross-category collaboration with food and spirits producers.

Major challenges include high ingredient costs (hops up 18-22% in 2021-2023), off-trade shelf competition, regulatory fragmentation across EU member states, and macro-brewer craft acquisition competition.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)