Europe In Vitro Diagnostics Market Size, Share, Trends and Forecast by Test Type, Product, Usability, Application, End User, and Country, 2026-2034

Europe In Vitro Diagnostics Market Size, Share, Trends & Forecast (2026-2034)

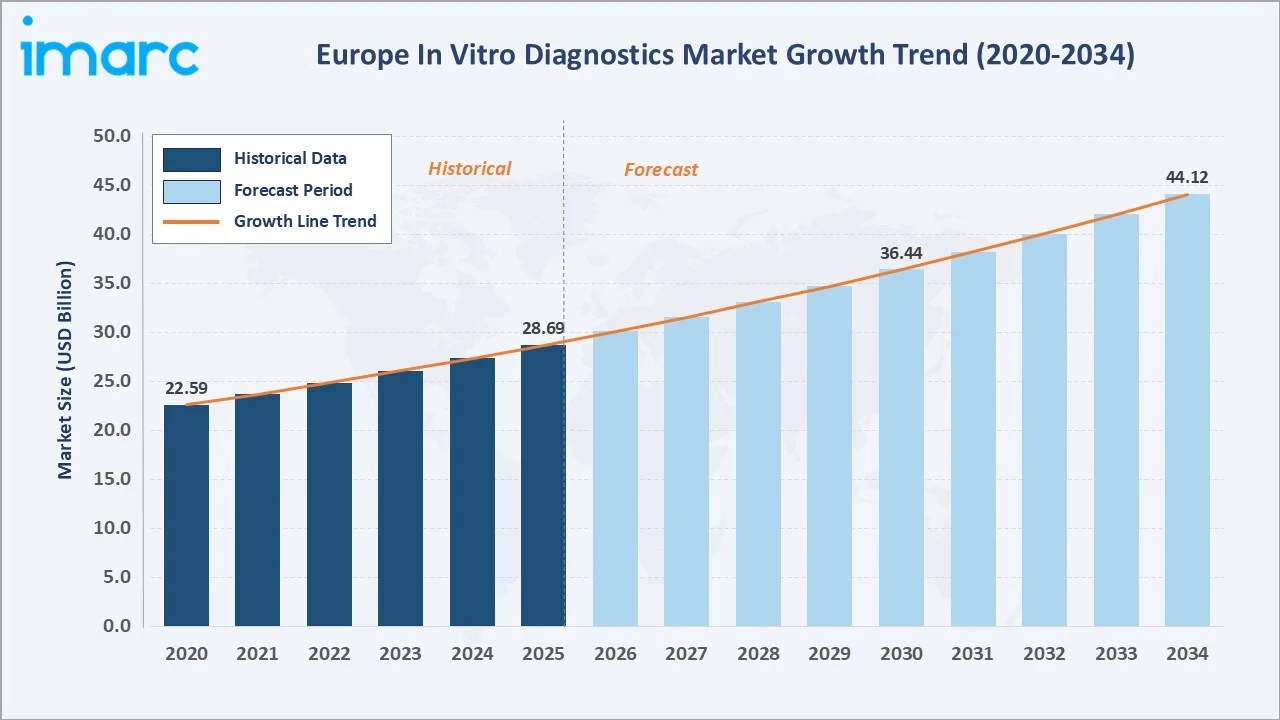

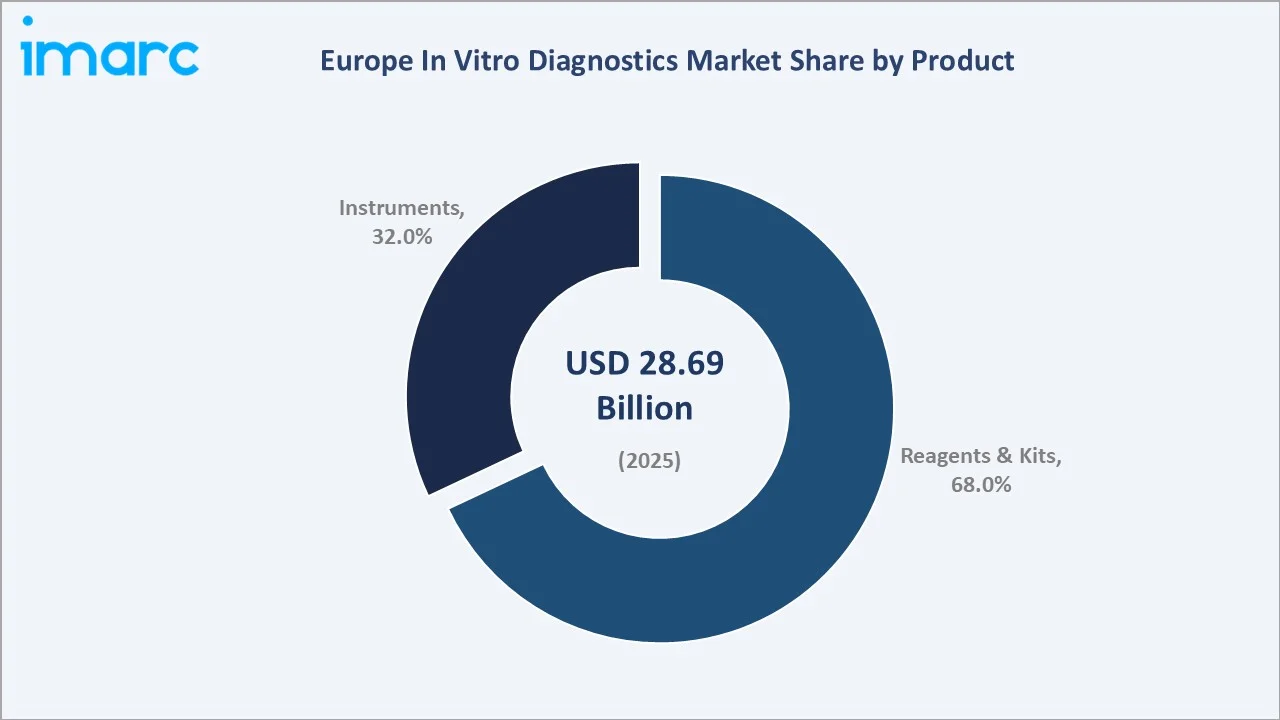

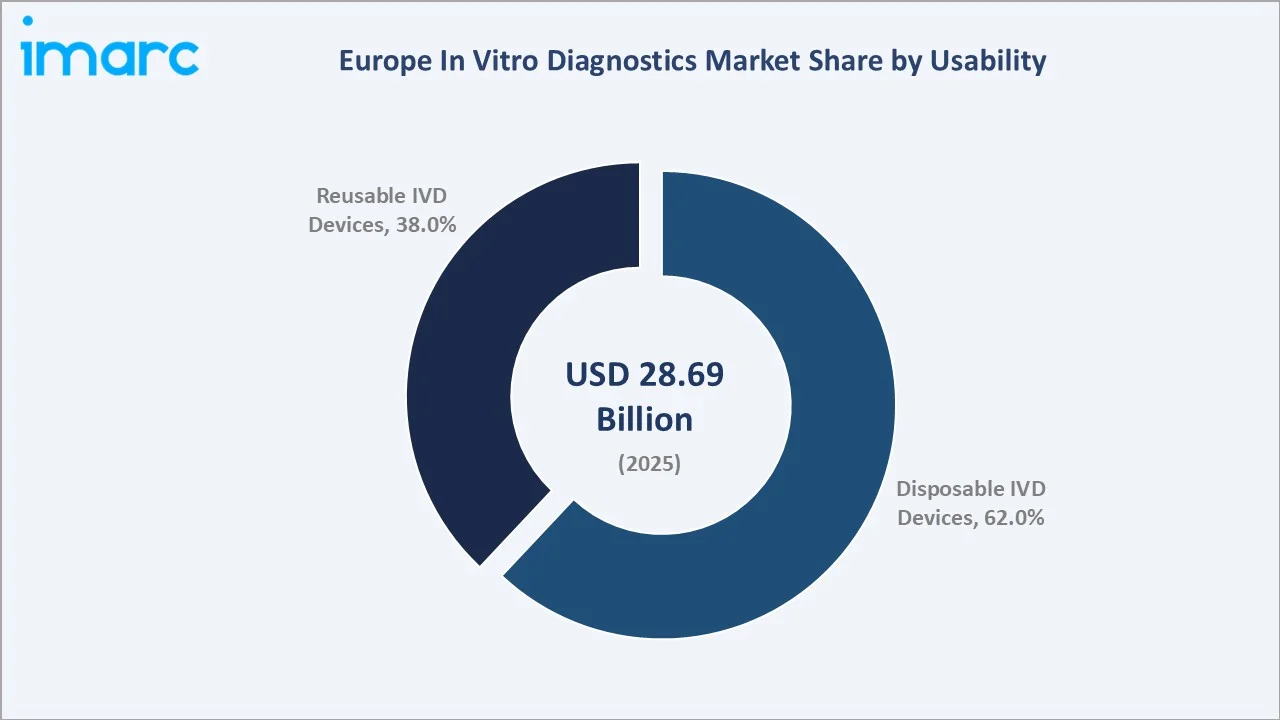

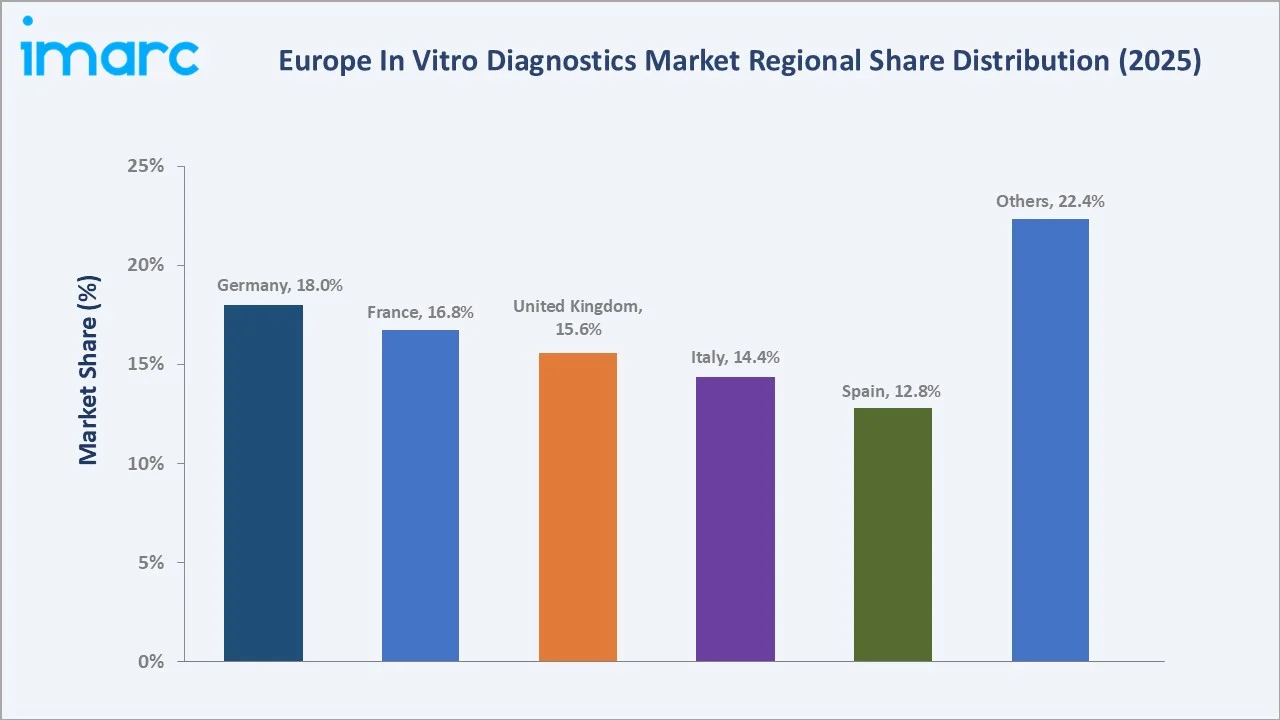

The Europe in vitro diagnostics market was valued at USD 28.69 Billion in 2025 and is projected to reach USD 44.12 Billion by 2034, expanding at a CAGR of 4.90% during the forecast period (2026-2034). Growth is driven by an ageing European population, rising chronic diseases, with over 50 million people having more than one chronic disease, the EU IVDR 2017/746 regulatory transition elevating product quality standards, precision medicine driving companion diagnostic demand, and the decentralization of testing through point-of-care platforms. Reagents and kits dominate at 68.0% product share, while disposable IVD devices lead usability at 62.0%. Germany holds the largest country share at 18.0%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 28.69 Billion |

|

Forecast Market Size (2034) |

USD 44.12 Billion |

|

CAGR (2026-2034) |

4.90% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (18.0%, 2025) |

|

Fastest Growing Country |

Spain (CAGR ~5.2%, 2026-2034) |

To get more information on this market, Request Sample

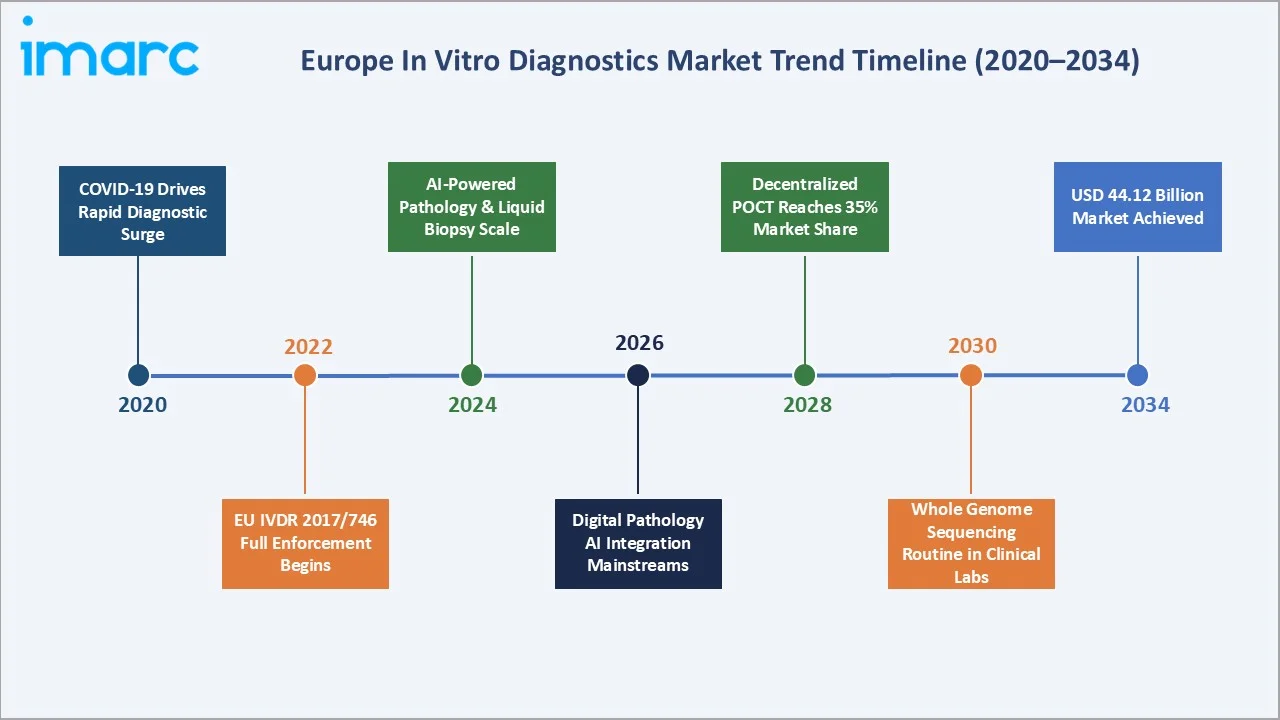

The Europe IVD market growth expanded from USD 22.59 Billion in 2020 to USD 28.69 Billion in 2025, driven by the COVID-19-era surge in rapid testing demand. Anchored at USD 36.44 Billion in 2030, the forecast is to USD 44.12 Billion by 2034, driven by IVDR compliance platform upgrades, molecular diagnostics expansion, and the proliferation of point-of-care testing across European healthcare systems.

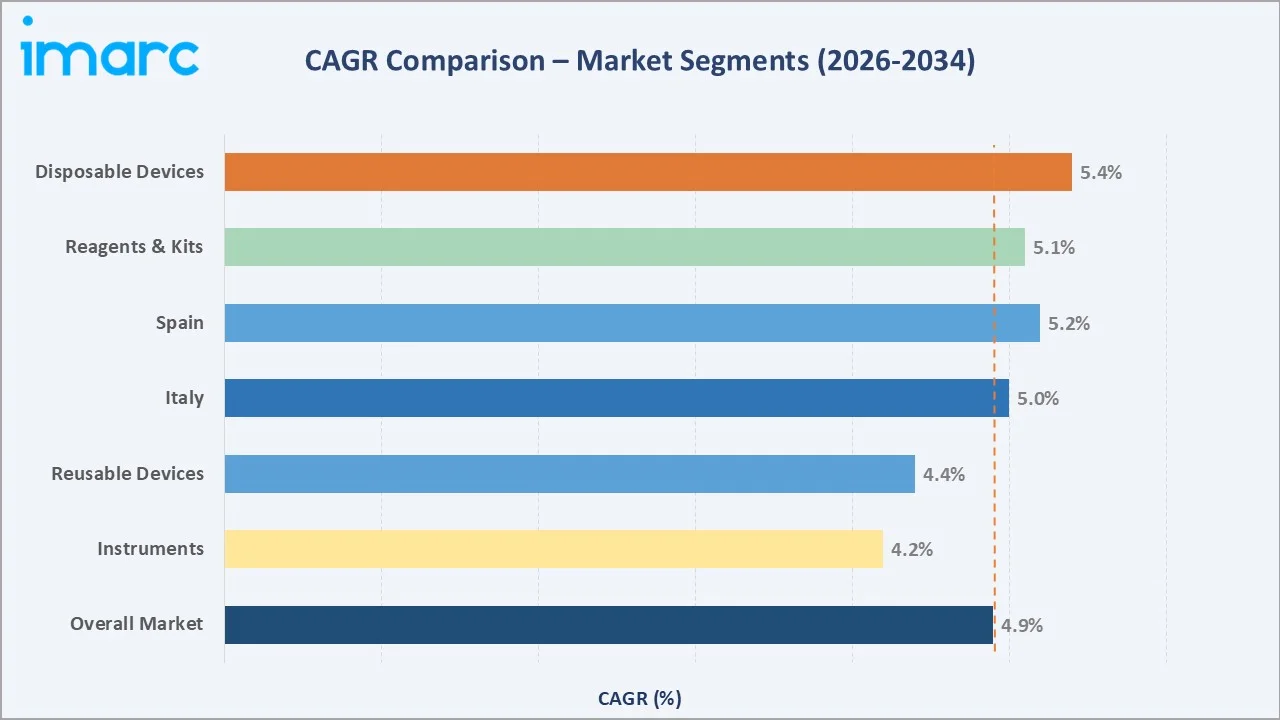

The CAGR across key segments with disposable IVD devices lead growth at ~5.4% CAGR, reflecting post-pandemic reinforcement of single-use device preferences and stringent infection control mandates across European hospital networks. Spain at ~5.2% CAGR is the fastest-growing major country market, driven by structural healthcare infrastructure investment and expanding private laboratory networks across the Iberian Peninsula.

Executive Summary

The Europe in vitro diagnostics market has grown from USD 22.59 Billion in 2020 to USD 28.69 Billion in 2025, achieved through the COVID-19 pandemic’s extraordinary surge in molecular diagnostic and rapid antigen test demand, followed by sustained structural growth driven by chronic disease prevalence, oncology companion diagnostics expansion, and the EU IVDR 2017/746 compliance cycle that is upgrading the quality of IVD products marketed across the European Union. The forecast trajectory to USD 44.12 Billion by 2034.

Reagents and kits at 68.0% market share (2025), reflecting the reagent-intensive nature of modern IVD workflows where automated analyzers consume reagent consumables at volumes 5–10× the value of the instruments themselves. Roche cobas reagents, Siemens Healthineers ADVIA chemistry reagents, and Abbott Alinity immunoassay kits form the backbone of European hospital laboratory reagent procurement. Disposable IVD devices at 62.0% encompass lateral flow rapid tests, single-use sample collection tubes, disposable cuvettes, and single-use POCT cartridges, a category that grew explosively during COVID-19 and has maintained elevated demand levels as POCT normalizes in European primary care settings.

Germany’s 18.0% leadership reflects both market size and the concentration of Europe’s most advanced diagnostic innovation infrastructure, hosting Siemens Healthineers, QIAGEN, and the Munich-based Helmholtz Zentrum research network. France at 16.8% is home to bioMérieux, the world’s leading clinical microbiology company, and benefits from Institut Pasteur’s infectious disease research excellence driving molecular diagnostic demand.

Key Market Insights

|

Insight |

Data |

|

Dominant Product |

Reagents & Kits – 68.0% revenue share (2025) |

|

Dominant Usability |

Disposable IVD Devices – 62.0% revenue share (2025) |

|

Leading Country |

Germany – 18.0% revenue share (2025) |

|

Fastest Growing Country |

Spain (CAGR ~5.2%, 2026-2034) |

Key Analytical Observations Supporting the Above Data:

- Reagents & Kits dominate at 68.0% (2025): The ongoing IVDR performance study requirements mandate substantially greater reagent use for new IVD product validation, further structurally expanding the reagent market as manufacturers conduct European conformity assessment studies across diverse patient populations.

- Disposable IVD devices lead at 62.0% (2025): The 8.9 million European patients acquire a HAI annually. Single-use blood collection devices, disposable lateral flow test cassettes, single-use point-of-care cartridges, and disposable molecular test cartridges collectively represent the disposable IVD device category growing above market average across all European markets.

- Germany leads at 18.0% (2025): Germany’s IVD market strength reflects the country’s laboratory testing spend, supported by the GKV-funded comprehensive test menu reimbursement system covering 450+ laboratory parameters.

Europe In Vitro Diagnostics Market Overview

In vitro diagnostics (IVD) encompasses laboratory tests, instruments, reagents, software, and accessories used to examine specimens derived from the human body such as blood, urine, tissue, and other biological materials, outside the human body (“in vitro”), with the purpose of diagnosing disease, monitoring treatment efficacy, guiding therapeutic decisions, and screening population health status. The European IVD ecosystem spans multinational manufacturers, European clinical laboratory networks, hospital laboratory departments, POCT platforms, and an evolving digital diagnostic software sector.

Applications span clinical chemistry (glucose, lipids, liver enzymes), molecular diagnostics (PCR, sequencing, FISH), immunodiagnostics (troponin, hormones, autoimmunity), hematology (CBC, coagulation), and microbiology (culture, rapid pathogen identification). Macroeconomic influences include European healthcare expenditure trends, the EU Horizon Europe research funding supporting IVD innovation, IVDR compliance investment creating capital expenditure cycles, and demographic ageing increasing chronic disease test volumes at compounding rates across all European national health systems.

Market Dynamics

To evaluate market opportunities, Request Sample

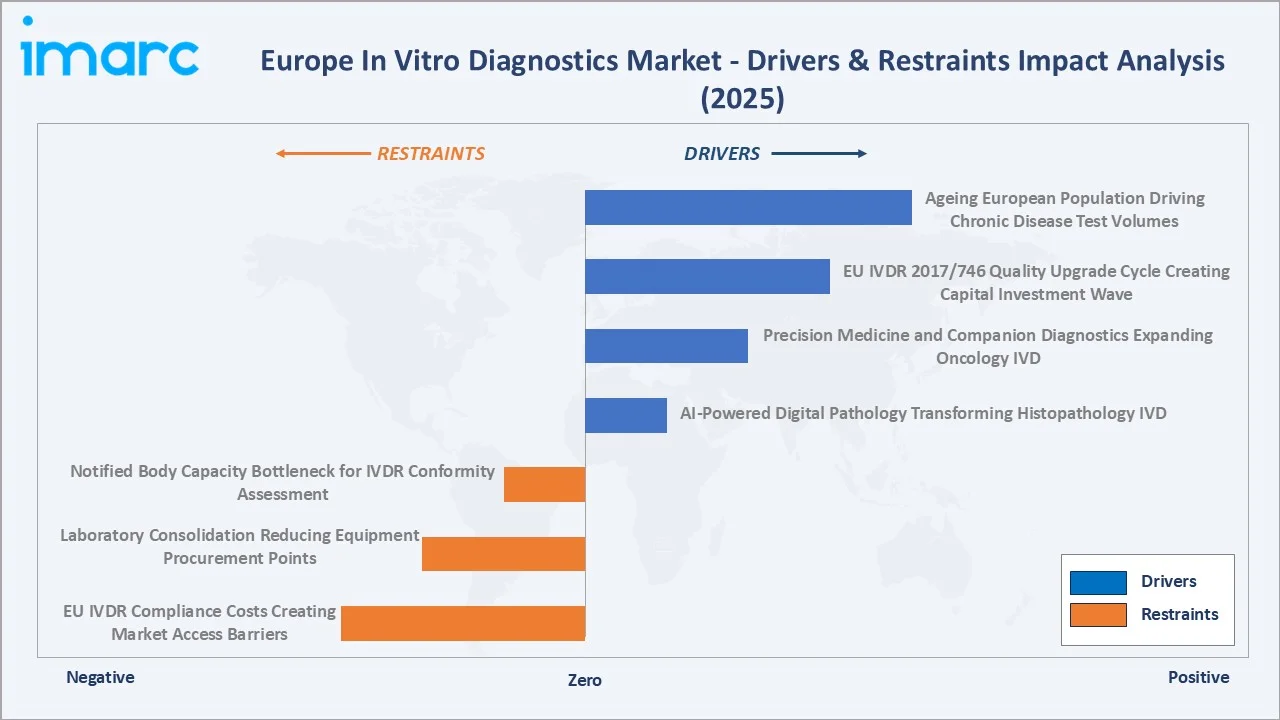

Market Drivers

- Ageing European Population Driving Chronic Disease Test Volumes: The number of individuals aged 60 and above in the WHO European Region is increasing significantly, rising from 215 million in 2021 to an estimated 247 million by 2030, and expected to exceed 300 million by 2050. This demographic reality directly translates to IVD market growth.

- EU IVDR 2017/746 Quality Upgrade Cycle Creating Capital Investment Wave: The EU In Vitro Diagnostic Regulation 2017/746, with reclassification transition deadlines across 2025–2028 for different risk classes, is forcing Europe’s 2,200+ registered IVD manufacturers to invest in clinical performance studies, Notified Body conformity assessments, and post-market surveillance systems.

- Precision Medicine and Companion Diagnostics Expanding Oncology IVD: In 2024, the European Medicines Agency (EMA) put forward 114 new medicines for human use, of which 48 featured completely new active substances, requiring a companion or complementary diagnostic test for patient selection.

Market Restraints

- EU IVDR Compliance Costs Creating Market Access Barriers: IVDR conformity assessment costs for Class C and D high-risk IVDs are estimated at EUR 500,000–3,000,000 per product, a cost burden that has driven more smaller European IVD manufacturers to withdraw products from the European market rather than sustain compliance investment.

- Laboratory Consolidation Reducing Equipment Procurement Points: European laboratory consolidation, where large laboratory networks acquire smaller independent laboratories and centralise testing onto standardized analyzers, is reducing the number of procurement decision-makers while increasing per-customer purchasing power.

Market Opportunities

- European Health Data Space Enabling Population-Scale Diagnostic Intelligence: The EU’s European Health Data Space (EHDS) regulation, adopted in February 2025, mandates interoperable electronic health records across all EU member states, creating the infrastructure for population-scale diagnostic data analysis that enables real-world evidence generation, predictive biomarker discovery, and diagnostic algorithm validation at European population scale.

- AI-Powered Digital Pathology Transforming Histopathology IVD: European digital pathology adoption accelerated dramatically, deploying whole slide imaging systems in European pathology departments.

Market Challenges

- Notified Body Capacity Bottleneck for IVDR Conformity Assessment: Only 12 Notified Bodies were designated under EU IVDR by 2025, creating a structural bottleneck where the assessment capacity for registered IVD products seeking IVDR conformity assessment is severely constrained.

- Cybersecurity and Data Privacy Requirements for Connected IVD Devices: The EU Medical Device Regulation’s cybersecurity requirements and GDPR’s stringent health data processing rules create complex compliance requirements for networked IVD instruments, POCT devices connected to hospital IT systems, and digital pathology platforms processing patient image data.

Emerging Market Trends

1. Syndromic POCT Panel Testing Replacing Sequential Single-Pathogen Tests

Multiplex syndromic panel tests, simultaneously detecting respiratory, gastrointestinal, meningitis, or blood culture pathogens from a single sample in under 60 minutes, are transforming European emergency departments and intensive care units' diagnostics.

2. AI-Assisted Diagnostic Decision Support Integration

Clinical AI algorithms are being integrated directly into laboratory information systems and IVD platforms to provide decision support at the point of result reporting, flagging critical values, suggesting differential diagnoses, identifying QC failures, and auto-approving normal results to reduce pathologist review burden.

3. Liquid Biopsy Entering Routine Oncology Practice

Cell-free DNA (cfDNA) liquid biopsy tests enabling non-invasive cancer detection, treatment monitoring, and minimal residual disease assessment through blood draw are transitioning from research settings to European clinical routine.

4. Continuous Glucose Monitoring Redefining Diabetes IVD

Abbott’s FreeStyle Libre continuous glucose monitoring (CGM) system is Europe’s most successful consumer IVD platform in EU member states. The transition from fingerstick glucose self-monitoring to CGM subscriptions represents a fundamental revenue model shift in diabetes IVD.

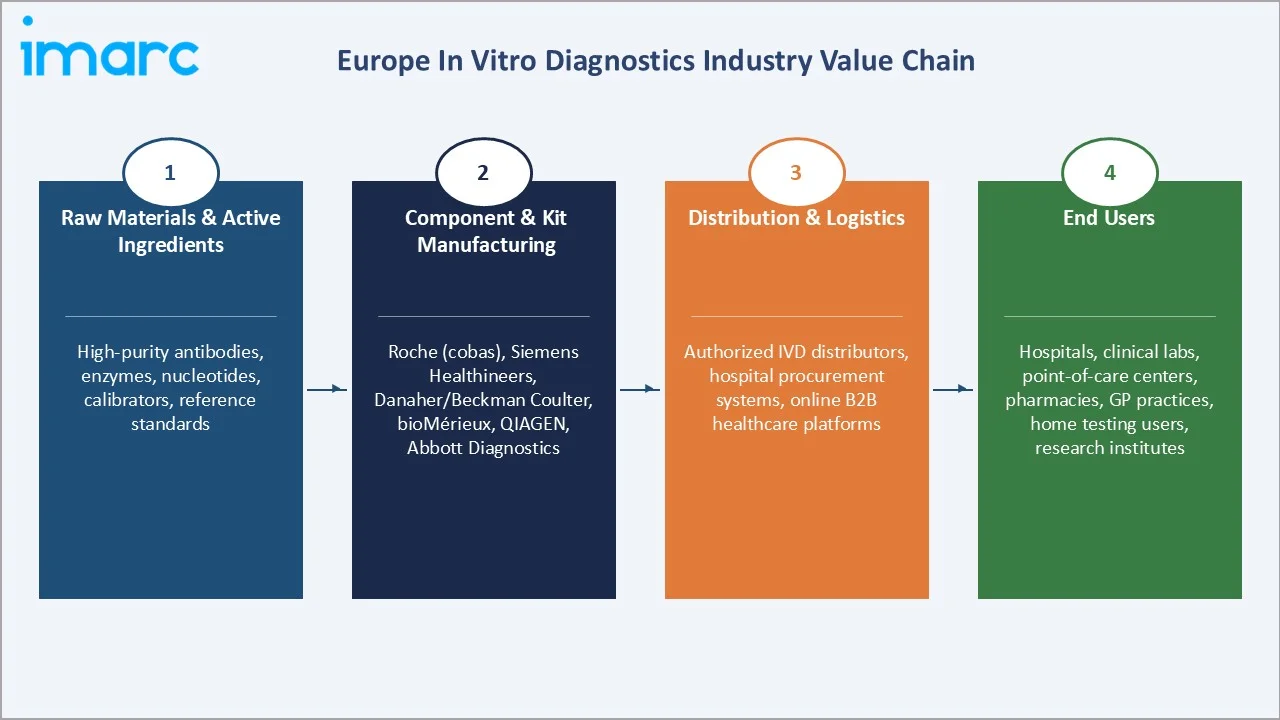

Industry Value Chain Analysis

The Europe IVD value chain spans raw material and active ingredient supply through diagnostic product manufacturing, software development, distribution, and clinical application across Europe’s diverse healthcare systems, from German university hospitals to Spanish community health centers.

|

Stage |

Key Participants |

|

Raw Materials & Active Ingredients |

High-purity antibodies, enzymes, nucleotides, calibrators, and reference standards for reagent manufacturing |

|

Component & Kit Manufacturing |

F. Hoffmann-La Roche (cobas reagents), Siemens Healthineers (ADVIA reagents), Danaher/Beckman Coulter, bioMérieux (VIDAS kits), QIAGEN (PCR kits), Abbott Diagnostics |

|

Distribution & Logistics |

local authorized IVD distributors, hospital procurement systems, online B2B healthcare platforms |

|

End Users |

Hospital laboratories, clinical reference laboratories, point-of-care testing centers (pharmacies, GP practices), patient self-testing (glucose, pregnancy, COVID-19 home tests), and academic and research institutes |

Reagent and kit manufacturing captures the highest revenue density in the IVD value chain, with Roche, Siemens, and Abbott each generating more in European reagent revenue from their installed analyzer base. The software and digital diagnostics tier is the highest-growth segment, with AI diagnostic software companies achieving 40–60% annual revenue growth from near-zero bases.

Technology Landscape in the Europe In Vitro Diagnostics Industry

Molecular Diagnostic Platforms: PCR, NGS, and CRISPR

Real-time PCR remains Europe’s workhorse molecular diagnostic technology, with Roche cobas 6800/8800 and QIAGEN QIAsymphony processing the majority of European molecular diagnostic tests. Next-generation sequencing (NGS) is entering clinical routine for cancer genomic profiling and rare disease diagnosis are the dominant European clinical NGS platforms.

Automated Immunoassay and Clinical Chemistry Platforms

Electrochemiluminescence (ECL) technology achieves the highest analytical sensitivity for troponin, thyroid hormones, and tumour markers, enabling earlier diagnosis of AMI (acute myocardial infarction) and improved cancer screening performance.

Digital Pathology and AI-Powered Image Analysis

Whole slide imaging (WSI) scanners convert glass microscopy slides into 40,000× digital images for AI-assisted diagnostic interpretation. The EU AI Act’s high-risk classification for diagnostic AI requires conformity assessment, creating compliance pathways that favour integrated platform providers over standalone AI software vendors.

Point-of-Care Testing Technology and Connectivity

Fifth-generation POCT platforms integrate analytical chemistry miniaturization, wireless connectivity, and cloud-based result management into handheld or benchtop devices deployable without laboratory infrastructure. EU IVDR’s new requirements for POCT near-patient testing are elevating performance standards while creating compliance investment requirements that benefit established POCT platform leaders over emerging competitors.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Test Type |

Clinical Chemistry |

32.0% |

2025 |

|

Product |

Reagent and Kits |

68.0% |

2025 |

|

Usability |

Disposable IVD Devices |

62.0% |

2025 |

|

Application |

Infectious Disease |

28.0% |

2025 |

|

End User |

Hospitals Laboratories |

44.0% |

2025 |

|

Country |

Germany |

18.0% |

2025 |

By Product

To access detailed market analysis, Request Sample

Reagents and kits lead at 68.0% market share (2025). This category encompasses immunoassay reagent systems, molecular diagnostic consumables, clinical chemistry calibrators and reagents, hematology reagents, and rapid test kits for POCT applications. The reagent category’s dominance reflects the IVD business model where analyzer placements generate multi-year reagent rental revenue streams.

Instruments at 32.0% encompass automated clinical analyzers, molecular diagnostic platforms (PCR, NGS, hybridization systems), hematology analyzers, digital pathology scanners, POCT devices, and laboratory automation systems. The instruments segment is driven by the EU IVDR-triggered replacement cycle, POCT platform expansion, and digital pathology WSI scanner investment.

By Usability

Disposable IVD devices lead at 62.0% (2025). This segment encompasses single-use lateral flow test strips, disposable PCR tubes and microfluidic cartridges, blood collection tubes, single-use cuvettes for biochemistry analyzers, disposable sample cups, and POCT single-use cassettes. Post-COVID-19, Europe’s POCT infrastructure investment has permanently elevated disposable IVD consumption levels, creating continuous high-volume demand for disposable test cartridges and lateral flow devices.

Reusable IVD devices at 38.0% cover automated laboratory analyzers (clinical chemistry, immunoassay, hematology, molecular platforms) and digital pathology scanners with multi-year service lifecycles. The reusable segment is growing as laboratory automation investment accelerates under EU IVDR compliance pressure and workforce shortage management requirements.

Country Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

18.0% |

World’s largest IVD market outside the U.S. and Japan, ageing population expanding chronic disease testing |

|

France |

16.8% |

French national cancer plan driving oncology IVD; HAS (Haute Autorité de Santé) precision medicine reimbursement expansion |

|

United Kingdom |

15.6% |

NHS Genomics Medicine Service (GMS) whole genome sequencing for 100,000+ patients annually, NHS Test and Trace COVID infrastructure legacy |

|

Italy |

14.4% |

Italian National Health Service (SSN) modernization driving lab automation investment, ISS (Istituto Superiore di Sanità) infectious disease surveillance |

|

Spain |

12.8% |

Spanish national oncology genomics strategy, post-COVID POCT infrastructure expansion in primary care |

|

Others |

22.4% |

Switzerland’s Roche and Tecan HQs; Netherlands’ QIAGEN European operations; Belgium’s clinical laboratory excellence; Sweden’s Karolinska genomics research driving molecular IVD demand; Poland’s rapid laboratory modernization under EU structural funds |

Germany’s 18.0% market dominance reflects the most comprehensive statutory health insurance (GKV) laboratory reimbursement system in Europe, covering 90%+ of the population without prior authorization requirements. Around 9 million laboratory results are produced every day in Germany, according to the BDL (Berufsverband Deutscher Laborärzte e.V.), the highest per-capita test volume in the EU.

France’s 16.8% share reflects a unique laboratory consolidation structure. This laboratory consolidation has driven systematic automation investment with French laboratory networks. On average, about 1.09 billion laboratory tests are conducted annually in France, with nearly 847.13 million (77.5%) performed in the private sector and 245.91 million (22.5%) in the public sector.

Competitive Landscape

The Europe IVD market is highly concentrated at the top tier, with F. Hoffmann-La Roche, Siemens, and Abbott Laboratories collectively commanding approximately 45–50% of European IVD market revenue.

|

Company Name |

Key Brand / Products |

Market Position |

Core Strength |

|

F. Hoffmann-La Roche Ltd. |

cobas DPX, cobas pure integrated solutions, Elecsys HIV Duo, Elecsys Syphilis, Elecsys Anti-HBc II, cobas WNV Test, cobas Babesia, cobas 5800 system, cobas 6800 system |

Dominant Market Leader |

Europe’s #1 IVD company; cobas automated analyzers dominate hospital central laboratory workflows; strongest companion diagnostics portfolio linked to Roche pharma pipeline |

|

Siemens Healthineers AG |

Atellica CI Analyzer, IMMULITE 2000 XPi System |

Market Leader |

Atellica Solution immunoassay analyzer is world’s most flexible high-throughput platform; ADVIA hematology systems in European hospital labs |

|

Abbott |

Alinity, AlinIQ, ARCHITECT, CELL-DYN, FreeStyle Libre CGM |

Market Leader |

Alinity family as a unified modular lab automation ecosystem, Freestyle Libre CGM as Europe’s #1 continuous glucose monitor |

|

bioMérieux |

ARGENE, BACT/ALERT, BIOFIRE (FilmArray), VIDAS, VITEK |

Strong Challenger |

BioFire FilmArray syndromic panel testing (respiratory, meningitis, blood culture identification) adopted in large French and European hospitals; VIDAS immunoassay as standard for bioMérieux’s infectious disease testing |

|

QIAGEN |

QIAcuityDx Digital PCR System, QIAamp DSP DNA Mini Kit, QIAcube Connect MDx, QIAsymphony DSP Circulating DNA Kits, QIAamp DSP DNA FFPE Tissue Kit, QIAamp DSP Virus Spin Kit, RNeasy DSP FFPE Kit, QIAamp DSP Virus Kit, PAXgene Blood DNA Tube (IVD) |

Strong Challenger |

QIAsymphony as Europe’s standard automated nucleic acid extraction platform; oncology companion diagnostics enabling precision medicine |

This high concentration reflects the platform economics of IVD, where installed analyzer base creates multi-year reagent lock-in, and the capital-intensive nature of clinical validation and EU IVDR regulatory compliance.

Key Company Profiles

F. Hoffmann-La Roche Ltd.

F. Hoffmann-La Roche is Europe’s dominant IVD company and the global diagnostics market leader.

- Product Portfolio: cobas DPX, cobas pure integrated solutions, Elecsys HIV Duo, Elecsys Syphilis, Elecsys Anti-HBc II, cobas WNV Test, cobas Babesia, cobas 5800 system, cobas HDV, cobas 6800 system.

- Recent Developments: In February 2026, Roche inaugurated its new Diagnostics Innovation Center in Penzberg, Germany.

- Strategic Focus: Integrated diagnostics-therapeutics ecosystem, every Roche pharma approval linked to a companion Roche IVD; navify digital health platform as recurring software revenue layer over installed instrument base; liquid biopsy and NGS clinical validation as next-generation oncology IVD platform; decentralized testing expansion through cobas Liat POCT in European primary care settings.

Siemens Healthineers AG

Siemens is Germany’s leading healthcare technology company and Europe’s second-largest IVD company. The company has Atellica Solution as the world’s most flexible high-throughput immunoassay platform deployed in European hospital central laboratories.

- Product Portfolio: Atellica CI Analyzer, IMMULITE 2000 XPi System, ADVIA Chemistry Systems, ADVIA Centaur Systems, Dimension Systems.

- Recent Developments: In January 2026, Siemens Healthineers inaugurated a new Immunoassay Instrument R&D Centre of Excellence in Swords, Ireland, backed by over €10 million in investment. The facility supports innovation in laboratory diagnostics for infectious diseases, cancer, and blood disorders.

- Strategic Focus: Varian oncology integration driving end-to-end cancer care diagnostics; Healthineers Digital Health as EUR 1B+ revenue target by 2028; laboratory automation leadership through Aptio TLA; European POCT market expansion through epoc and Xprecia Stride platforms; EU IVDR product transition as quality differentiation versus smaller competitors.

Abbott

Abbott is the world’s leading POCT diagnostics company and a strong competitor in European immunoassay and molecular diagnostics.

- Product Portfolio: Alinity, AlinIQ, ARCHITECT, CELL-DYN, FreeStyle Libre CGM.

- Recent Developments: BinaxNOW COVID-19 + Flu A&B test received CE-IVDR marking, first multiplex rapid test under IVDR.

- Strategic Focus: POCT market leadership through BinaxNOW platform extension beyond COVID-19 to influenza, RSV, strep, and cardiometabolic tests; Alinity central laboratory platform capturing Roche and Siemens menu consolidation opportunities; connected diagnostics ecosystem through Diagnostics Information Solutions linking POCT and central laboratory results.

bioMérieux

bioMérieux is France’s leading IVD company and the global pioneer in clinical microbiology diagnostics. The company’s singular focus on infectious disease diagnostics, spanning blood culture systems (BacT/ALERT), syndromic panels (BioFire), VITEK automated bacterial identification, and VIDAS immunoassay, established an unassailable clinical microbiology market leadership position in European hospital microbiology laboratories.

- Product Portfolio: ARGENE SOLUTION, BACT/ALERT Solutions, BIOFIRE Solutions, VIDAS Solutions, VITEK Solutions.

- Recent Developments: BioFire Blood Culture Identification Panel 2 (BCID2) received CE-IVDR marking detecting 33 organisms and 10 resistance markers.

- Strategic Focus: Infectious disease diagnostics specialization as defensible competitive moat against generalist IVD companies; antimicrobial stewardship – bioMérieux’s IVD enables targeted antibiotic therapy reducing inappropriate antibiotic use by 30–40% in European clinical trials; BIOFIRE Spot POCT expansion into primary care; AI-assisted AMR prediction as next-generation microbiology IVD platform; syndromic panel testing as replacement for sequential single-pathogen testing.

Market Concentration Analysis

The Europe IVD market is among the most concentrated in all of healthcare technology. Roche, Siemens, and Abbott collectively command approximately 45–50% of European IVD market revenue. The top five participants account for approximately 60–65% of total market value. This high concentration is structural rather than incidental, driven by platform economics (analyzer installation creates reagent lock-in), the capital intensity of EU IVDR clinical validation, and the customer relationship depth required to support 24/7 laboratory operations.

Market fragmentation exists in specialty diagnostic niches, autoimmunity testing, allergen testing, reproductive endocrinology, and esoteric reference laboratory testing, where specialty clinical expertise and established reference ranges create switching barriers that protect smaller specialist companies. The IVDR transition is paradoxically accelerating both consolidation and niche protection (large companies focused on high-volume mainstream tests, leaving specialty niches to dedicated smaller operators).

Investment & Growth Opportunities

Fastest Growing Segments

Molecular diagnostics (~7.2% CAGR), POCT (~8.5% CAGR), oncology/companion diagnostics (~9–12% CAGR), liquid biopsy (~25–35% CAGR), and digital pathology AI (~20–25% CAGR) represent the highest-growth investment vectors through 2034. The disposable POCT cartridge market represents the highest absolute volume growth opportunity, with 500M+ incremental test occasions anticipated from European POCT expansion in primary care by 2030.

Emerging Market Opportunities

CEE (Central and Eastern European) IVD markets, Poland, Czech Republic, Romania, Hungary, and Bulgaria are growing, as EU structural funds drive laboratory modernization and national health systems upgrade to Western European diagnostic standards.

Investment and Partnership Themes

European venture and institutional investment in IVD-adjacent technology, with diagnostic AI, liquid biopsy, and POCT platforms as primary investment themes.

- Key technology investment themes: CRISPR-based diagnostics, spatial transcriptomics for tissue diagnosis, federated AI learning across European laboratory networks, POCT miniaturization for home use, and wearable continuous biomarker monitoring beyond glucose.

- Corporate M&A pipeline: Roche and Danaher are all actively evaluating European molecular diagnostics and digital pathology acquisition targets in the EUR 100M–1B revenue range to fill platform gaps in their IVDR-compliant European product portfolios.

Future Market Outlook (2026-2034)

The Europe in vitro diagnostics market is positioned for consistent, structurally anchored growth through 2034. From USD 28.69 Billion in 2025, the market will reach USD 44.12 Billion by 2034, at a 4.90% CAGR. This growth trajectory reflects three irreversible structural forces: Europe’s demographic imperative generate compounding chronic disease test volume demands that no technology substitution can offset; the precision medicine revolution mandating molecular companion diagnostics for each of the 40–50 new oncology precision drugs expected to receive EMA approval annually through 2034; and the POCT decentralization movement permanently expanding diagnostic testing from European hospital and clinical laboratories to GP practices, pharmacies, and patient home environments that represent a structural expansion of the addressable testing occasion universe.

Research Methodology

Primary Research

Primary research included structured interviews with 140+ industry stakeholders in 2025, comprising clinical laboratory directors, IVD company commercial directors, hospital procurement managers, EU IVDR Notified Body consultants, EFLM (European Federation of Clinical Chemistry and Laboratory Medicine) representatives, and national health insurance reimbursement specialists. Geographic coverage spanned all six country segments analyzed in this report.

Secondary Research

Secondary research encompassed EFLM European laboratory testing statistics, EDMA (European Diagnostics Manufacturers Association) market data, EU IVDR EUDAMED database, EMA companion diagnostic approvals database, national laboratory billing data, company annual reports, Siemens Healthineers/Roche/Abbott/bioMérieux investor presentations, and peer-reviewed clinical laboratory literature. Over 260 secondary sources were reviewed.

Forecasting Models

Market size forecasts were developed using a bottom-up test-type country matrix validated against top-down. Key inputs include Eurostat demographic projections, European cancer incidence trends, IVDR compliance transition timelines, POCT adoption diffusion models by healthcare setting, and NGS/liquid biopsy clinical adoption S-curve projections.

Europe In Vitro Diagnostics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Test Types Covered | Clinical Chemistry, Molecular Diagnostics, Immunodiagnostics, Hematology, Others |

| Products Covered | Reagent and Kits, Instruments |

| Usabilities Covered | Disposable IVD Devices, Reusable IVD Devices |

| Applications Covered | Infectious Disease, Diabetes, Cancer/Oncology, Cardiology, Autoimmune Disease, Nephrology, Others |

| End Users Covered | Hospitals Laboratories, Clinical Laboratories, Point-of-care testing centers, Academic Institutes, Patients, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | F. Hoffmann-La Roche Ltd., Siemens Healthineers AG, Abbott, bioMérieux, QIAGEN, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe In Vitro Diagnostics Market Report

The Europe IVD market was valued at USD 28.69 Billion in 2025 and is projected to reach USD 44.12 Billion by 2034.

The Europe IVD market is forecast to grow at a CAGR of 4.90% during 2026-2034, driven by ageing demographics, EU IVDR compliance investment, precision medicine, and POCT decentralization.

Reagents and kits lead with 68.0% revenue share (2025), driven by the recurring consumable model of automated laboratory analyzers and expanding single-use POCT cartridge consumption.

Disposable IVD devices lead at 62.0% share (2025), driven by single-use lateral flow rapid tests, PCR cartridges, blood collection consumables, and POCT single-use cassettes.

Germany leads with 18.0% market share (2025), driven by GKV comprehensive reimbursement, Siemens Healthineers and QIAGEN domestic presence, and Europe’s most automated laboratory network.

Key market players include F. Hoffmann-La Roche Ltd., Siemens Healthineers AG, Abbott, bioMérieux, and QIAGEN.

Key drivers include ageing population chronic disease burden, EU IVDR quality upgrade investment, precision medicine companion diagnostics, POCT decentralisation, and NGS clinical routine adoption.

EU IVDR 2017/746 requires reclassification of 90%+ of CE-marked IVDs into higher-risk classes needing Notified Body assessment, generating EUR 5–8B compliance investment and concentrating market share among large compliant manufacturers.

Key trends include syndromic POCT panel testing, AI-assisted diagnostic decision support, liquid biopsy clinical adoption, continuous glucose monitoring expansion, and mobile diagnostic unit deployment.

Top opportunities include molecular POCT, liquid biopsy, AI digital pathology, NGS clinical sequencing, CEE market laboratory modernization, and EU Health Data Space-enabled diagnostic analytics platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)