Europe Industrial Gases Market Size, Share, Trends and Forecast by Type, Application, Supply Mode, and Country, 2026-2034

Europe Industrial Gases Market Size, Share, Trends & Forecast (2026-2034)

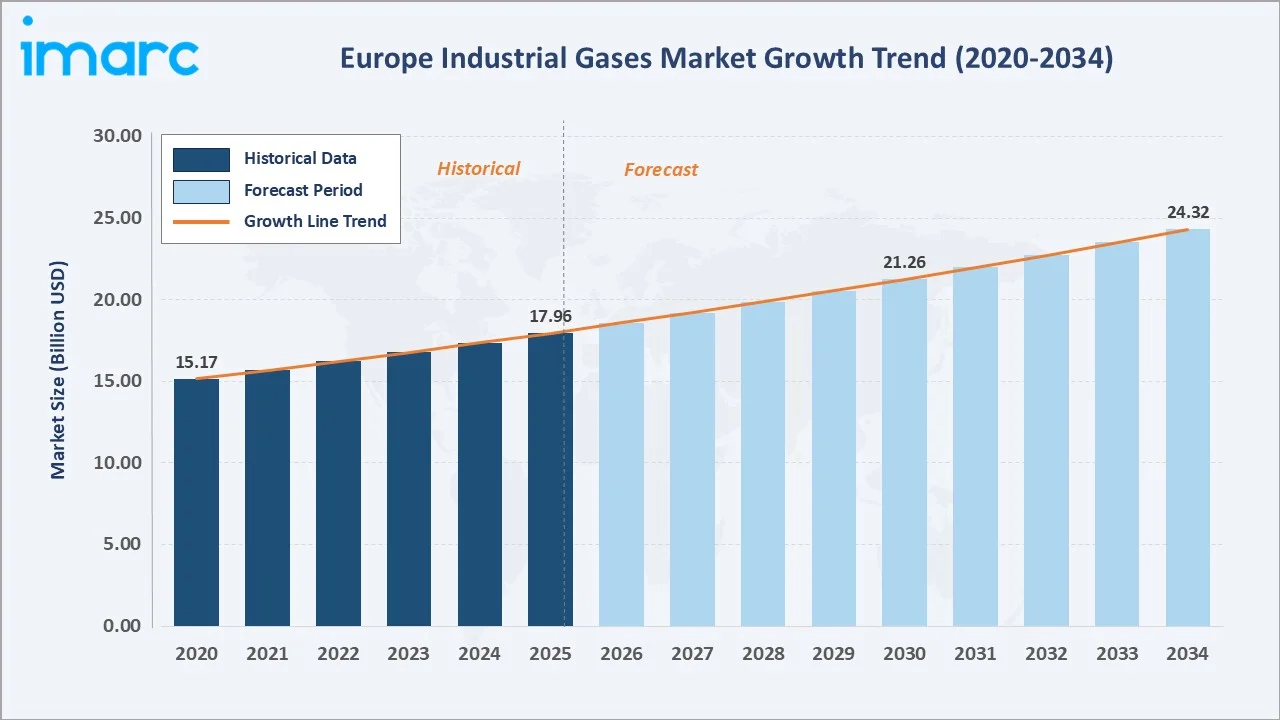

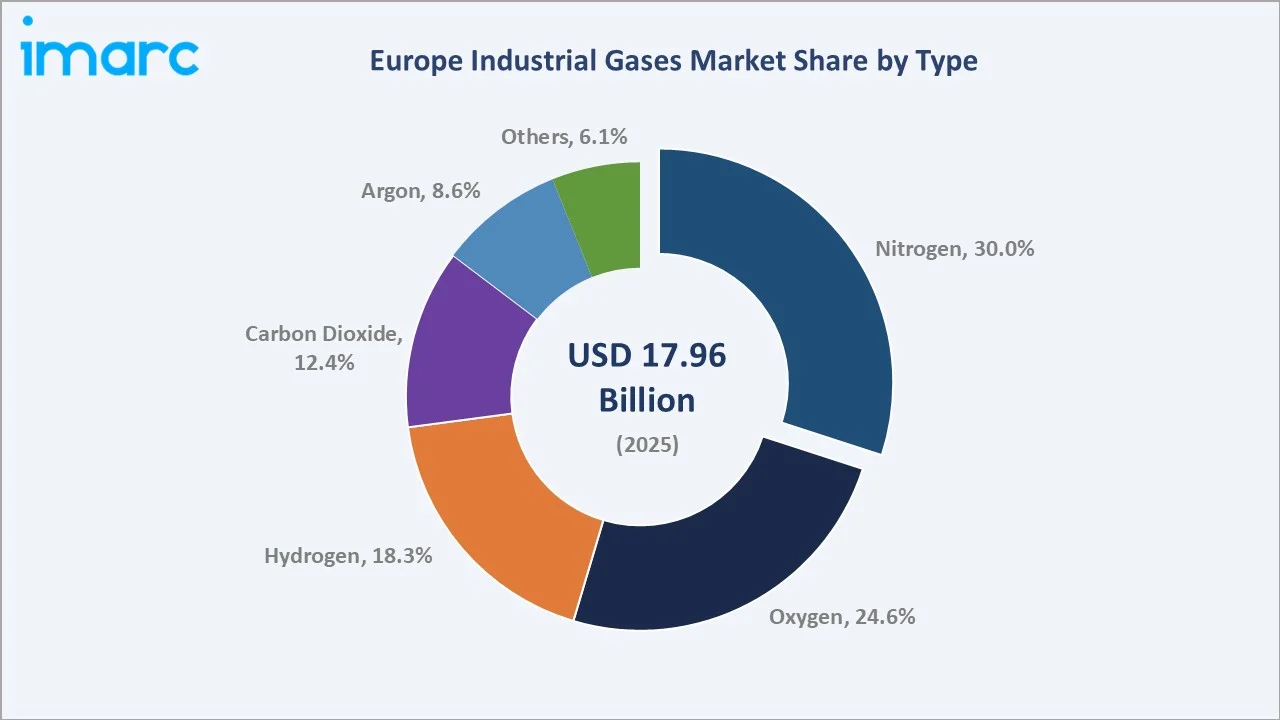

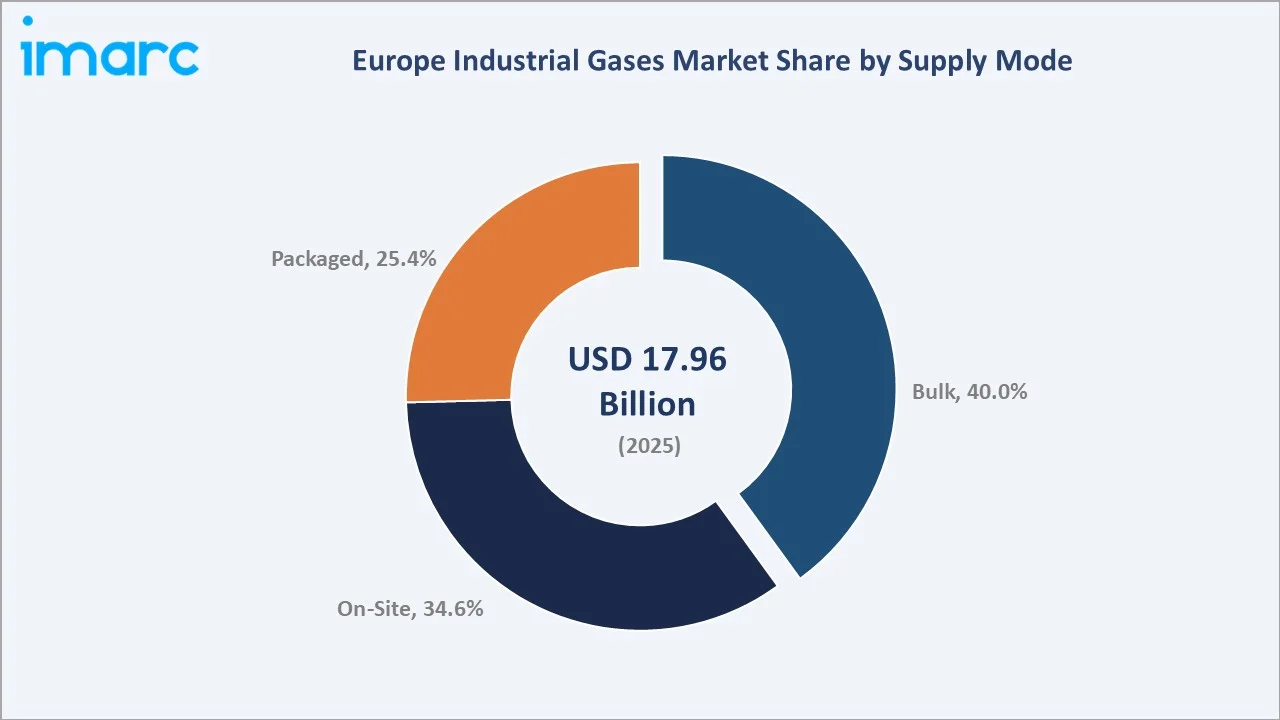

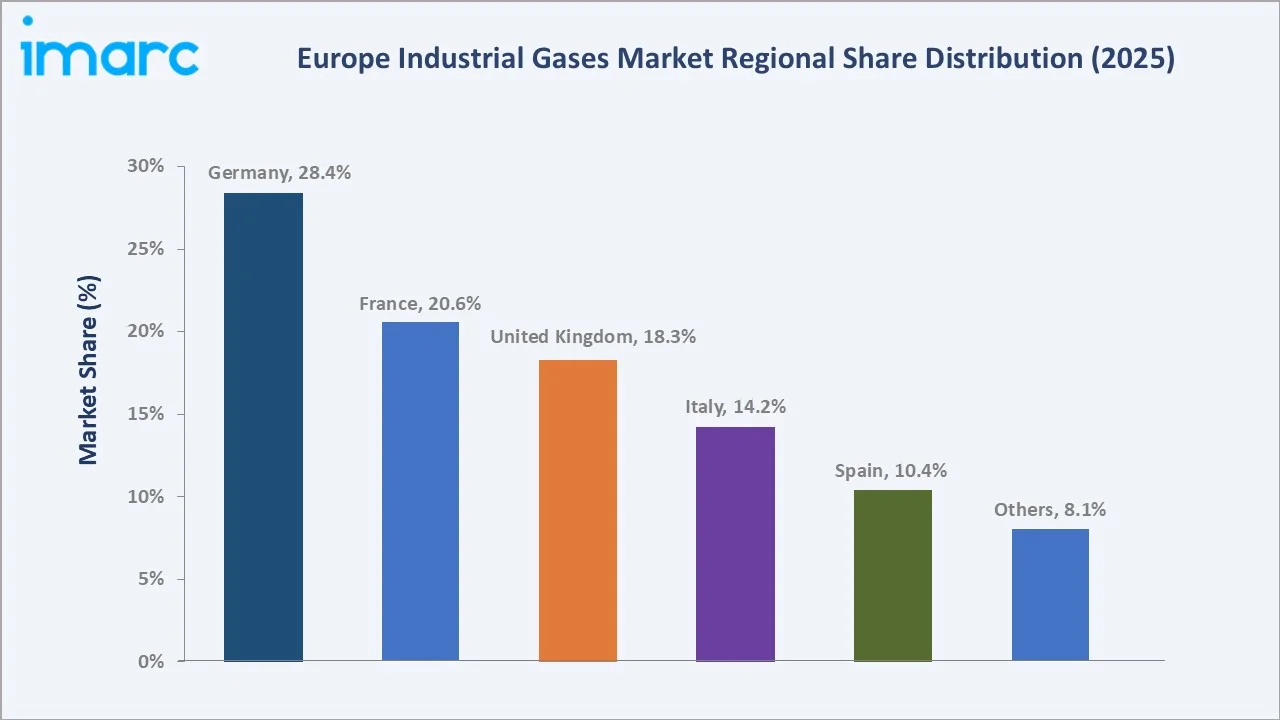

The Europe industrial gases market was valued at USD 17.96 Billion in 2025 and is projected to reach USD 24.32 Billion by 2034, exhibiting a CAGR of 3.43% during the forecast period 2026-2034. The market is primarily driven by the accelerating green hydrogen transition under the EU Hydrogen Strategy, expanding medical oxygen demand from an ageing European population, and robust consumption in steel, food processing, and electronics manufacturing. Nitrogen leads gas-type segmentation at 30.0% in 2025, while bulk supply mode commands 40.0% of delivery-channel revenues. Germany anchors regional demand with a 28.4% country-level share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 17.96 Billion |

|

Forecast Market Size (2034) |

USD 24.32 Billion |

|

CAGR (2026-2034) |

3.43% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (28.4%) |

|

Largest Gas Type |

Nitrogen (30.0%) |

|

Dominant Supply Mode |

Bulk (40.0%) |

The Europe industrial gases market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by green hydrogen investment, healthcare sector demand, and industrial decarbonisation commitments.

To get more information on this market, Request Sample

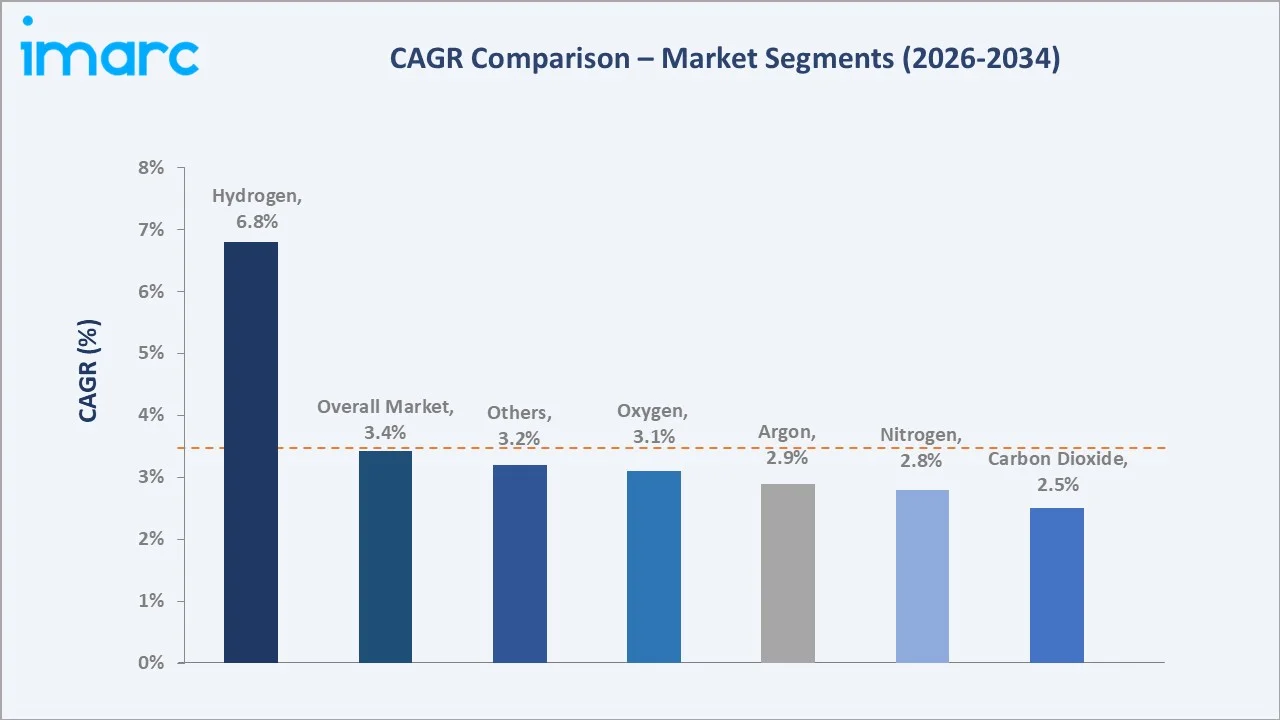

Segment-level CAGR comparisons highlighting hydrogen as the fastest-growing gas type at approximately 6.8% CAGR through 2034, significantly outpacing the overall market average of 3.43%, reflecting structural demand from EU green energy mandates.

Executive Summary

The Europe industrial gases market is undergoing a structural evolution driven by the continent's dual imperatives of industrial decarbonisation and energy security. From USD 15.17 Billion in 2020, the market expanded steadily to USD 17.96 Billion in 2025, reflecting consistent demand from manufacturing, healthcare, and food processing sectors, alongside a notable acceleration in hydrogen-related investment following the EU Green Deal and REPowerEU strategy. The market is projected to reach USD 24.32 Billion by 2034 at a CAGR of 3.43%.

Nitrogen commands the dominant gas-type share at 30.0% in 2025, supported by its versatility across food preservation, electronics, and pharmaceutical packaging. Bulk delivery at 40.0% remains the primary supply mode, though on-site generation at 34.6% is gaining momentum among energy-intensive industries seeking supply security and lower unit costs.

Germany dominates country-level demand at 28.4% in 2025, driven by Europe's largest chemical cluster, dense automotive manufacturing, and the continent's most ambitious national hydrogen strategy. France at 20.6% and the United Kingdom at 18.3% round out the top three. The competitive landscape is highly concentrated – Air Liquide, Linde PLC, and Air Products and Chemicals, Inc. collectively account for an estimated 65–70% of European industrial gas revenues, competing on infrastructure depth, long-term customer contracts, and green gas credentials.

Key Market Insights

|

Insight |

Data |

|

Largest Gas Type Segment |

Nitrogen – 30.0% share in 2025 |

|

Fastest-Growing Gas Type |

Hydrogen – ~6.8% CAGR (2026-2034) |

|

Leading Supply Mode |

Bulk – 40.0% share in 2025 |

|

Leading Country |

Germany – 28.4% share in 2025 |

|

Top Market Players |

Air Liquide, Linde PLC, Air Products and Chemicals, Inc., Messer SE & Co. KGaA |

Key Analytical Observations Supporting The Above Data:

- Nitrogen's 30.0% leadership in 2025 reflects its near-universal industrial applicability – from food packaging and semiconductor inerting to pharmaceutical manufacturing and pipeline purging – making it Europe's highest-volume industrial gas by value.

- Hydrogen at 18.3% in 2025 masks its disproportionate strategic importance. EU electrolyser capacity targets of 40 GW by 2030 and Germany's EUR 9 Billion national hydrogen commitment are creating structural demand inflections that will expand hydrogen's share significantly through 2034.

- Germany's 28.4% country share reflects the world's third-largest chemical sector, Europe's most intensive steel production base, and a dense automotive manufacturing cluster – all high-volume consumers of nitrogen, oxygen, argon, and hydrogen.

- Bulk supply mode at 40.0% signals industrial maturity. Large petrochemical complexes, refineries, and steel mills typically operate on long-term bulk contracts providing revenue predictability for leading gas producers.

- On-site generation at 34.6% is growing above the market average, driven by semiconductor fabs in Germany and the Netherlands, glass manufacturers, and steelmakers transitioning to direct-reduced iron (DRI) processes using hydrogen.

Europe Industrial Gases Market Overview

Industrial gases—nitrogen, oxygen, argon, hydrogen, CO₂, acetylene, helium, and specialty blends—are produced via cryogenic distillation, PSA, membranes, and electrolysis, serving as critical inputs across Europe’s manufacturing and services sectors.

The market is highly consolidated, supported by integrated infrastructure (ASUs, liquefaction plants, pipelines, and cryogenic logistics) and long-term supply contracts in key industrial hubs such as Rhine-Ruhr, Seine corridor, and Thames Estuary. Demand tracks core industries—metals, automotive, pharmaceuticals, food, and semiconductors—while growth is driven by the EU Green Deal, Hydrogen Strategy, Chips Act, and healthcare investment.

Market Dynamics

To evaluate market opportunities, Request Sample

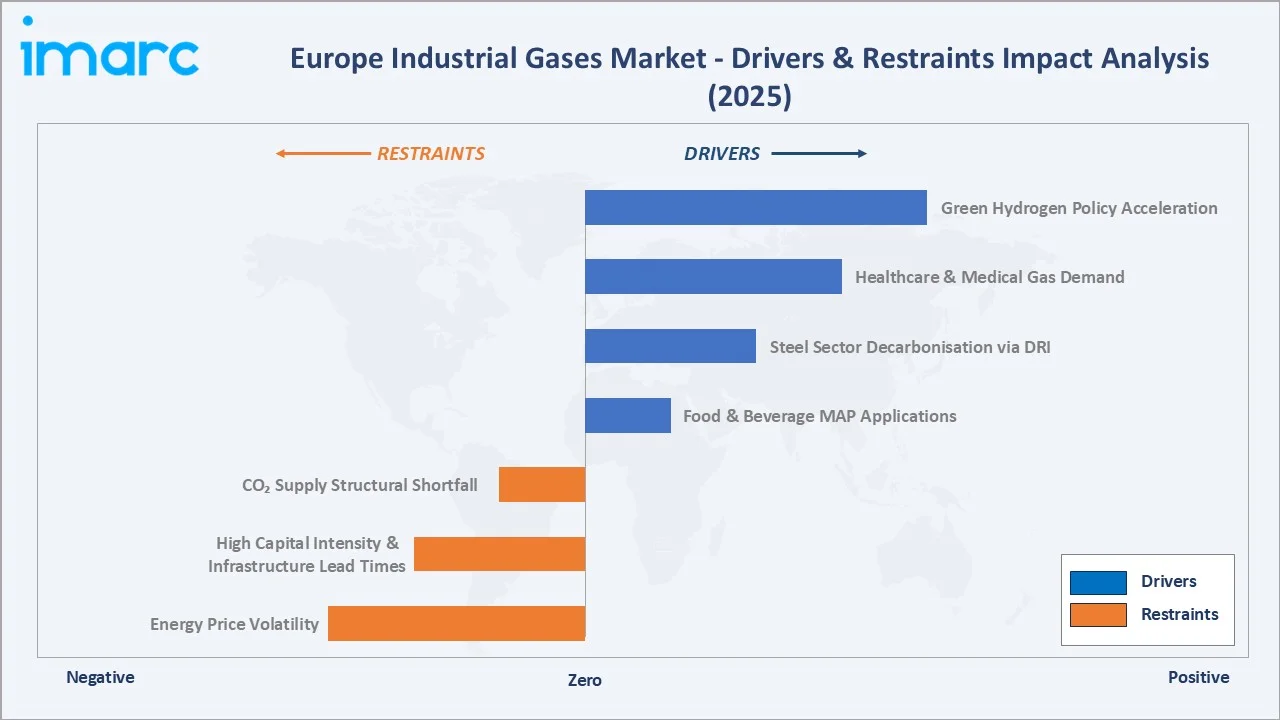

Market Drivers

- Green Hydrogen Policy Acceleration: EU targets ~10 Mt domestic renewable hydrogen by 2030 (EU Hydrogen Strategy, REPowerEU), driving investment in electrolysers, pipelines, and oxygen co-product streams; supported by national funding (e.g., Germany) and long-term industrial offtake (steel, refining).

- Healthcare and Medical Gas Demand: Ageing population (20%+ aged 65+, Eurostat) sustains demand for medical oxygen, nitrous oxide, and pharma-grade gases across hospitals and biopharma.

- Steel Sector Decarbonisation via DRI: ThyssenKrupp's tkH2Steel project, SSAB's HYBRIT initiative, and ArcelorMittal's DRI expansion programmes collectively represent a multi-billion euro demand signal for industrial hydrogen, displacing coking coal and requiring large-scale on-site gas supply partnerships.

- Food and Beverage Modified Atmosphere Packaging: Rising use of nitrogen and CO₂ in modified atmosphere packaging supports steady growth in food-grade gases.

Market Restraints

- Energy Price Volatility: Energy-intensive production (notably ASUs) makes margins highly sensitive to electricity price volatility, as seen during the 2022 EU energy crisis.

- High Capital Intensity and Infrastructure Lead Times: ASUs (EUR 50–200M; ~2–3 years) and hydrogen infrastructure require long build cycles, limiting supply responsiveness.

- CO₂ Supply Structural Shortfall: Reduced ammonia output in Europe has structurally constrained CO₂ availability for food and industrial use.

Market Opportunities

- Semiconductor Expansion Under EU Chips Act: EU Chips Act (~EUR 43B) and new fabs (e.g., Germany) are boosting demand for ultra-high-purity and specialty gases.

- Carbon Capture and Utilisation (CCU) for CO₂ Supply: Capture from biogas, industrial emissions, and DAC is emerging as an alternative CO₂ source and revenue stream.

- Specialty Gas Premiumisation: Growth in biopharma, labs, and electronics is increasing demand for high-purity/custom gases with significantly higher margins.

Market Challenges

- Regulatory Compliance Complexity: REACH, F-gas rules, and national safety standards increase compliance burden across multi-country operations.

- Supply Chain Resilience Post-Energy Crisis: Post-2022 disruptions highlighted vulnerabilities in energy supply, production continuity, and logistics, elevating supply security concerns.

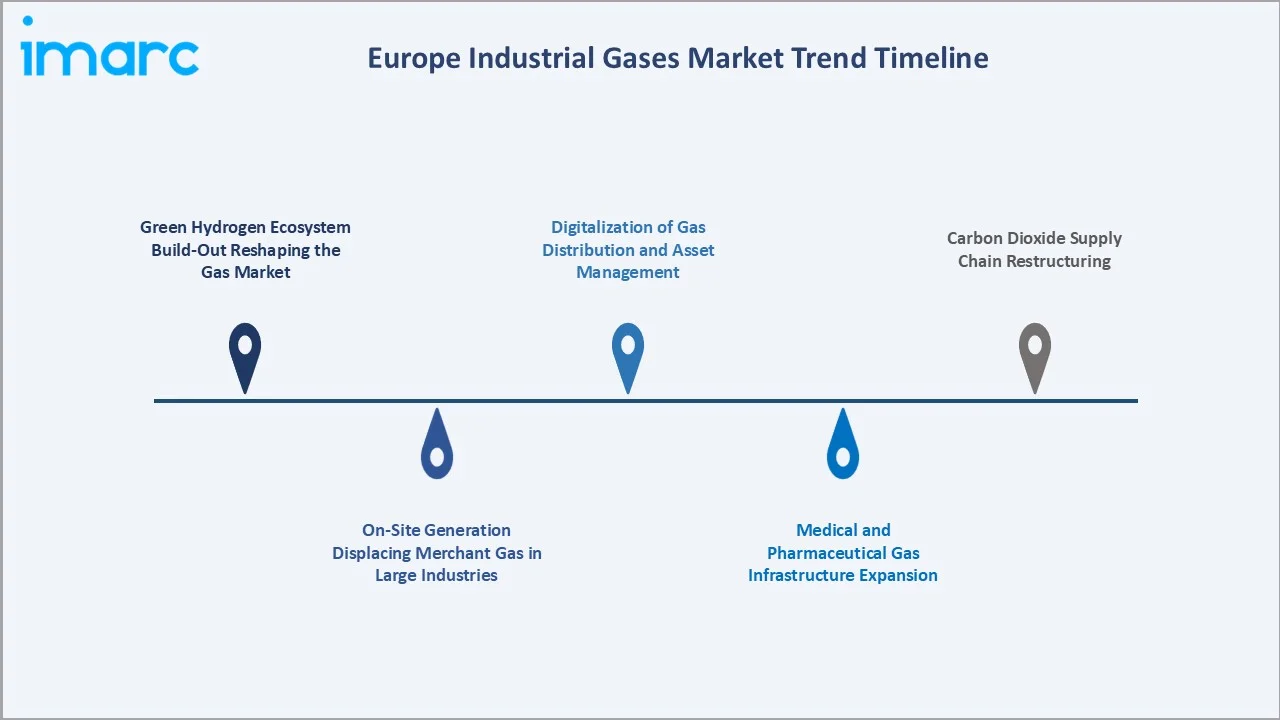

Emerging Market Trends

1. Green Hydrogen Ecosystem Build-Out Reshaping the Gas Market

Europe is a global hub for green hydrogen, with a multi-GW electrolyser pipeline across Germany, France, Spain, the Netherlands, and the UK (EU Hydrogen Strategy, REPowerEU). Capacity expansions by players such as ITM Power, Nel, and Linde signal large-scale capital deployment, with green/low-carbon hydrogen expected to steadily displace grey SMR supply over the next decade.

2. On-Site Generation Displacing Merchant Gas in Large Industries

Post-2022 energy disruptions are accelerating the adoption of captive on-site supply models (BOO). Large users—semiconductors, glass, and DRI steel—are prioritising supply security, with on-site generation expected to gain share from merchant gas over the medium term.

3. Digitalisation of Gas Distribution and Asset Management

Industrial gas majors are integrating IoT, telemetry, and AI into distribution networks. Smart cylinders, connected storage tanks, and route optimisation platforms (e.g., Air Liquide, Linde PLC) are enabling predictive replenishment, lowering logistics costs, and improving reliability—especially in packaged gas segments.

4. Medical and Pharmaceutical Gas Infrastructure Expansion

Healthcare investments post-COVID have strengthened piped gas infrastructure and redundancy across major EU markets. Demand is further supported by ageing demographics, home care oxygen usage, and biopharma growth requiring liquid nitrogen for advanced therapies.

5. Carbon Dioxide Supply Chain Restructuring

Structural CO₂ shortages—linked to reduced ammonia production—are driving diversification toward bio-based and captured CO₂ (fermentation, biogas, industrial emissions, DAC). This is shifting CO₂ from a by-product to a strategically managed supply stream.

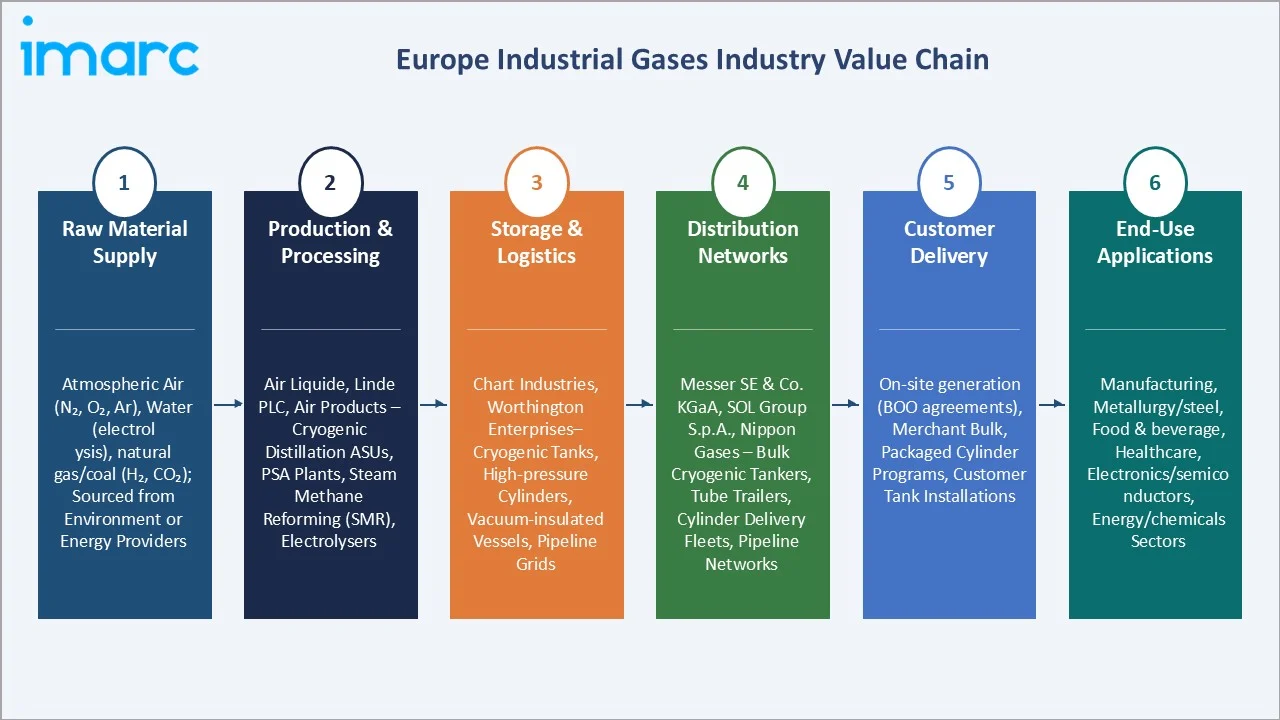

Industry Value Chain Analysis

The Europe industrial gases value chain spans six integrated stages from raw material sourcing through end-user delivery. Each stage exhibits distinct competitive dynamics, capital requirements, and margin profiles, with gas producers spanning multiple stages through vertical integration strategies.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Atmospheric air (N₂, O₂, Ar), water (electrolysis), natural gas/coal (H₂, CO₂); sourced from environment or energy providers |

|

Production & Processing |

Air Liquide, Linde PLC, Air Products – cryogenic distillation ASUs, PSA plants, steam methane reforming (SMR), electrolysers |

|

Storage & Logistics |

Chart Industries, Worthington Enterprises– cryogenic tanks, high-pressure cylinders, vacuum-insulated vessels, pipeline grids |

|

Distribution Networks |

Messer SE & Co. KGaA, SOL Group S.p.A., Nippon Gases – bulk cryogenic tankers, tube trailers, cylinder delivery fleets, pipeline networks |

|

Customer Delivery |

On-site generation (BOO agreements), merchant bulk, packaged cylinder programmes, customer tank installations |

|

End-Use Applications |

Manufacturing, metallurgy/steel, food & beverage, healthcare, electronics/semiconductors, energy/chemicals sectors |

Linde PLC and Air Liquide hold commanding vertical positions across production, logistics, and distribution, leveraging captive air separation units, cryogenic tanker fleets, and dedicated pipeline networks spanning thousands of kilometres. Mid-tier producers (Messer SE & Co. KGaA, SOL Group S.p.A.) compete on regional distribution excellence and service quality. Specialty gas blenders occupy high-margin niche positions serving calibration, pharmaceutical, and electronics applications.

Technology Landscape in the European Industrial Gases Industry

Cryogenic Air Separation and Liquefaction Technology

Cryogenic distillation remains the dominant large-scale technology for nitrogen, oxygen, and argon, delivering ultra-high purities (>99.999%). Modern air separation units (ASUs) achieve ~0.28–0.35 kWh/Nm³ (oxygen basis) through advanced turbine expanders, structured packing, and heat integration. Leading designs from Linde and Air Products set current efficiency benchmarks in Europe.

Electrolysis and Green Hydrogen Production

Alkaline and PEM electrolysis are the primary commercial pathways for green hydrogen. Alkaline systems (e.g., ThyssenKrupp Nucera) offer lower capex at scale, while PEM (e.g., ITM Power, Nel, Siemens Energy) provides operational flexibility for variable renewables. Solid oxide electrolysis (SOEC), operating at ~700–900°C, is emerging as a high-efficiency next-generation solution, with pilots underway in Europe.

Pressure-Swing Adsorption and Membrane Separation

PSA enables on-site nitrogen/oxygen production for small-to-mid scale users (~10–500 Nm³/hr), reducing reliance on delivered gases. Membrane systems provide lower-purity nitrogen (≈95–99.5%) with compact, low-maintenance setups suited for food packaging, inerting, and industrial applications. Both are gaining traction as industries prioritise cost control and supply security.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Nitrogen |

30.0% |

2025 |

|

Application |

Manufacturing |

26.0% |

2025 |

|

Supply Mode |

Bulk |

40.0% |

2025 |

|

Country |

Germany |

28.4% |

2025 |

By Type

Nitrogen leads Europe's industrial gas market with a 30.0% share in 2025, reflecting its broad application base across food and beverage, electronics, chemicals, and general manufacturing. Oxygen at 24.6% serves dual industrial and healthcare markets, while hydrogen's 18.3% share masks its structural importance as the fastest-growing gas type underpinned by EU decarbonisation mandates.

To access detailed market analysis, Request Sample

Nitrogen's 30.0% leadership reflects unmatched versatility. Applications range from modified atmosphere packaging (MAP) for food preservation – where nitrogen displaces oxygen to extend shelf life by 3–5x – to semiconductor clean-room inerting environments requiring purities of 99.9999% (6N). Nitrogen is also essential for pharmaceutical filling lines, chemical reactor blanketing, and cryogenic freezing in food processing. Oxygen at 24.6% supports oxygen-enriched combustion in glass furnaces, electric arc furnace steelmaking, and as medical oxygen for an estimated 120 million European patients requiring respiratory support annually.

Hydrogen at 18.3% in 2025 is the market's strategic growth engine. Current demand originates from petroleum refining, hydrocracking, ammonia synthesis for fertilisers, and specialty chemical processes. However, the green hydrogen transition is creating entirely new demand pools: fuel cell electric vehicles (FCEVs), industrial decarbonisation (steel, cement, glass), and power-to-gas energy storage. Carbon dioxide at 12.4% underpins food and beverage carbonation, dry ice production, and welding applications. Argon at 8.6% serves high-value precision welding and semiconductor manufacturing, commanding premium pricing versus commodity gas types.

By Supply Mode

Bulk liquid delivery commands the largest supply mode share at 40.0% in 2025, primarily serving large industrial customers through scheduled cryogenic tanker deliveries and customer-owned vacuum-insulated storage. On-site generation at 34.6% is strategically growing as majors sign BOO agreements with semiconductor fabs, steel plants, and energy transition projects. Packaged cylinders at 25.4% serve SMEs, healthcare, and laboratory segments.

Bulk supply's 40.0% dominance reflects the cost efficiency advantages of cryogenic liquid delivery for customers consuming above 200 tonnes per month. Scheduled delivery through a dedicated tanker fleet – typically on 2–7 day intervals – provides a reliable, cost-optimised supply solution for petrochemical complexes, large food processors, and hospitals. On-site generation at 34.6% eliminates logistics risk and can reduce per-unit gas costs by 15–25% at an industrial scale, making it compelling for semiconductor manufacturers, glass producers, and DRI steelmakers. The on-site model also enables the supply of ultra-high-purity grades that would be difficult to transport cryogenically at the required specifications. Packaged gases (cylinders, tube bundles) at 25.4% serve the diverse long-tail of SME, laboratory, and portable welding applications where consumption volumes preclude bulk or on-site economics.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

28.4% |

Largest chemical cluster (BASF, Evonik), EU's most intensive steel production, National Hydrogen Strategy (EUR 9B), automotive manufacturing |

|

France |

20.6% |

Air Liquide headquarters, nuclear power enables competitive electrolysis, aerospace (Airbus, Safran), biopharmaceutical, and food processing sectors. |

|

United Kingdom |

18.3% |

North Sea oil & gas operations, large biopharmaceutical sector (AstraZeneca, GSK), food & beverage processing, and hydrogen mobility programmes |

|

Italy |

14.2% |

Metal fabrication and welding (world's 6th largest steel producer), food processing, automotive (Stellantis, Ferrari), packaged gas strength |

|

Spain |

10.4% |

Growing renewables integration (green H₂ corridors H2Med), steel and chemicals, agri-food sector, expanding cleantech manufacturing base |

|

Others |

8.1% |

Benelux semiconductor demand (ASML, IMEC), Poland's industrial expansion, Nordic clean energy, and maritime H₂ applications |

Germany commands a 28.4% share – equivalent to approximately USD 5.1 billion in 2025 – anchored by the world's third-largest chemical industry, including BASF's Ludwigshafen Verbund (the world's largest integrated chemical complex), and Europe's most productive steel sector. Automotive manufacturing demands large volumes of nitrogen, CO₂, and argon in body fabrication, painting, and airbag propellant production.

France, at 20.6%, benefits from Air Liquide's deep domestic infrastructure and a nuclear-powered electricity grid that reduces green hydrogen production costs relative to European peers. Aerospace and defence applications (Airbus, Safran, Dassault) drive specialty gas consumption. The United Kingdom, at 18.3%, maintains significant demand despite post-Brexit manufacturing headwinds, driven by North Sea energy operations, a large biopharmaceutical manufacturing base, and active hydrogen mobility programmes including HyDeploy and the H100 Fife network. Italy (14.2%) and Spain (10.4%) generate demand from metal fabrication, automotive components, agrifood processing, and emerging cleantech clusters, respectively.

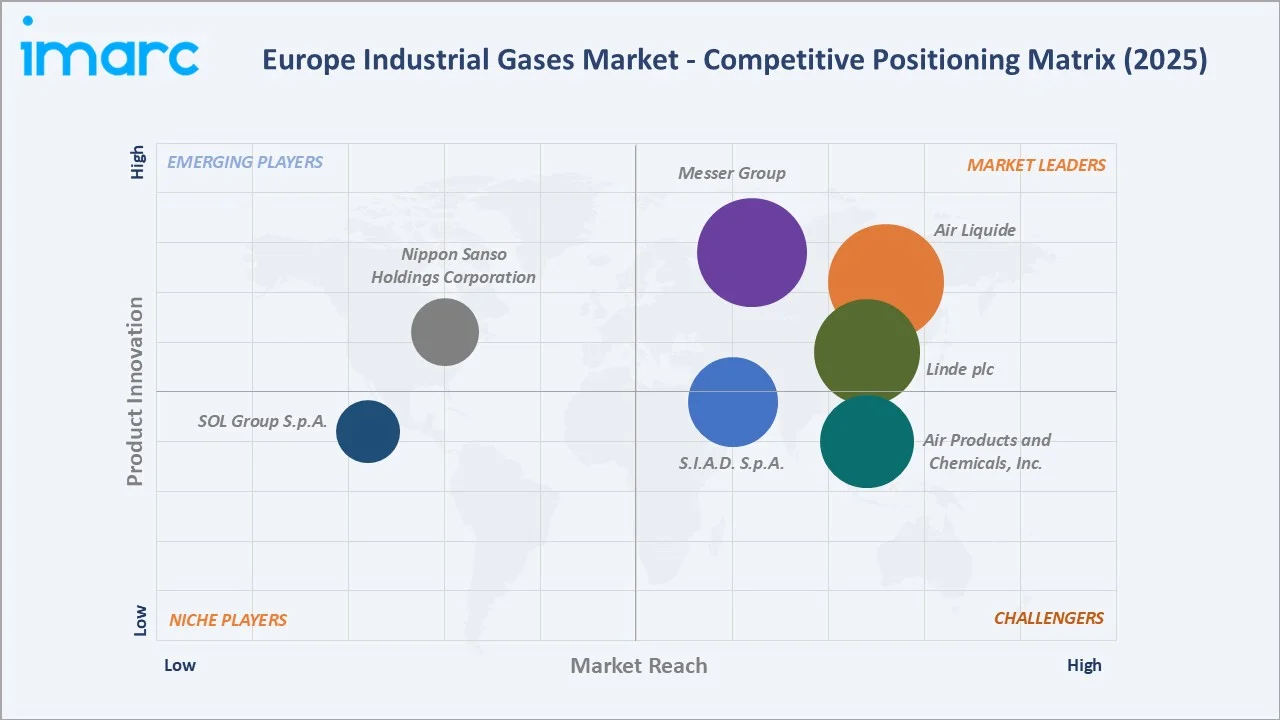

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Air Liquide |

Air Liquide |

Market Leader |

Infrastructure depth, green H₂, digital distribution |

|

Linde PLC |

Linde / AGA / BOC |

Market Leader |

Cryogenic engineering, HyCO, on-site plants |

|

Air Products and Chemicals, Inc. |

Air Products / PRISM |

Key Challenger |

Hydrogen infrastructure, BOO on-site, Americas crossover |

|

Messer SE & Co. KGaA |

Messer |

Regional Leader |

Central/Eastern Europe, specialty gases, SME reach |

|

SOL Group S.p.A. |

SOL / Vivisol |

Niche Specialist |

Southern Europe, healthcare gases, lab blends |

|

Nippon Sanso Holdings Corporation |

Nippon Gases |

Emerging Player |

Electronics/semiconductor purity gases, M&A expansion |

|

S.I.A.D. S.p.A. |

SIAD / Istrabenz Plini |

Regional Player |

Italy & SE Europe industrial/medical gases, integrated engineering (ASU, LNG, CO₂ plants), LPG & natural gas distribution; 16 European countries |

The Europe industrial gases competitive landscape is characterised by a small number of global producers commanding dominant positions, supplemented by regional specialists with strong country-level franchises. Air Liquide and Linde collectively account for an estimated 55–60% of European industrial gas revenues, forming a near-duopoly in large-scale atmospheric and process gas supply. Their competitive moats rest on proprietary pipeline infrastructure, long-term customer contracts (often 10–20 year durations for on-site plants), and first-mover advantages in green hydrogen.

Key Company Profiles

Air Liquide

Air Liquide is the world's largest industrial gas company by revenue, headquartered in Paris, France. In Europe, it operates more than 250 air separation units and a hydrogen production network spanning France, Germany, Belgium, the Netherlands, and the UK – making it the leading supplier to the continent's chemical, steel, food, healthcare, and electronics sectors.

- Product & Platform Portfolio: Atmospheric gases (N₂, O₂, Ar), hydrogen, CO₂, specialty and rare gases, ALTIS digital gas management platform, on-site cryogenic plants, gas equipment and services.

- Recent Developments: In February 2021, Siemens Energy and Air Liquide announced a large-scale electrolyzer partnership for sustainable hydrogen production.

- Strategic Focus: Targeting 30% of revenues from low-carbon gases by 2030 under the ADVANCE strategic plan. Investing EUR 8 Billion in green hydrogen infrastructure by 2035, with major European hydrogen backbone participation, including the European Hydrogen Backbone initiative.

Linde PLC

Linde PLC, formed through the 2018 merger of Linde AG and Praxair, is Europe's second-largest industrial gas supplier and a global engineering powerhouse in cryogenic process technology. European operations are anchored in Germany with extensive Rhine-Ruhr pipeline infrastructure, UK industrial gas networks, and North Sea energy service contracts.

- Product & Platform Portfolio: Cryogenic atmospheric gases, hydrogen and syngas (HyCO), helium, specialty gases, on-site gas plants, SUALOX oxygen enrichment systems, gas cylinders and equipment, cryogenic engineering services.

- Recent Developments: In May 2024, Linde signed a long-term agreement with H2 Green Steel for the supply of industrial gases to the world’s first large-scale green steel production plant.

- Strategic Focus: Accelerating hydrogen value chain investment across production, distribution, and end-use applications. Digitalising operations through predictive asset maintenance and smart distribution to reduce costs and improve reliability. Targeting above-market growth in semiconductor and life sciences specialty gas segments.

Air Products and Chemicals, Inc.

Air Products operates a substantial European industrial gas business centred on hydrogen energy infrastructure, on-site generation, and industrial bulk supply. Its European footprint spans the UK, Belgium, the Netherlands, Germany, and Spain, with particular strength in hydrogen refuelling infrastructure and large-scale industrial hydrogen supply.

- Product & Platform Portfolio: Industrial hydrogen, nitrogen, oxygen, argon, liquefied gases, PRISM membrane separators, on-site gas generation plants (BOO model), LNG equipment, cryogenic technology licensing.

- Recent Developments: In April 2026, Air Products announced a significant construction milestone on its new liquid hydrogen facility in the Port of Rotterdam. The facility, now at an advanced stage of construction and over 65% complete, reflects a major step in reinforcing and modernizing Air Products' current hydrogen footprint in the Netherlands.

- Strategic Focus: Hydrogen-first strategy aligned with European Green Deal targets; aggressive BOO on-site model deployment for large industrial customers; targeting hydrogen refuelling station (HRS) partnerships for FCEV fleet operators across Germany, France, and the Netherlands.

Market Concentration Analysis

The European industrial gases market is highly concentrated, with Air Liquide, Linde PLC, and Air Products and Chemicals, Inc. collectively holding ~55–60% share (2025). This reflects high capex barriers, long-term contracts, and strong switching costs driven by dedicated pipeline networks.

The market shows a bifurcated structure: large industrial customers are increasingly tied into long-term BOO on-site agreements (10–20 years), reinforcing consolidation, while the packaged and specialty segment remains more fragmented, with players like Messer SE & Co. KGaA, SOL Group S.p.A., Nippon Sanso Holdings Corporation, and S.I.A.D. S.p.A are competing on service, specialty capabilities, and regional reach.

The landscape is evolving with new entrants in hydrogen, including utilities and electrolyser firms. Incumbents are responding via partnerships, vertical integration, and long-term green hydrogen contracts, while selective M&A—particularly in specialty gases and Eastern Europe—continues.

Investment & Growth Opportunities

Fastest-Growing Segments

Hydrogen is the fastest-growing segment (~6–7% CAGR to 2034), supported by EU decarbonisation policy, industrial demand (steel, refining), and mobility use cases. In parallel, on-site supply for semiconductor fabs—driven by the ~EUR 43B EU Chips Act—is a high-value niche, with ultra-high-purity gas contracts commanding significant pricing premiums over bulk supply.

Emerging Market Expansion

Eastern Europe (Poland, Czech Republic, Hungary, Romania) is seeing strong industrial growth driven by EU funding and nearshoring, creating opportunities in atmospheric and specialty gases. Southern Europe—especially Spain and Portugal—is emerging as a green hydrogen hub (e.g., H2Med corridor), supporting demand for electrolysis-linked oxygen and hydrogen infrastructure.

Venture & Private Investment Trends

Private equity is actively targeting specialty gas distributors and blenders, creating bolt-on acquisition opportunities for majors. At the same time, capital is flowing into electrolyser developers (e.g., Nel, ITM Power, Sunfire, Enapter), backed by infrastructure funds and sovereign investors, as hydrogen scales toward commercial deployment.

Future Market Outlook (2026-2034)

The Europe industrial gases market forecast projects steady value expansion from USD 17.96 Billion in 2025 to USD 24.32 Billion by 2034 at a CAGR of 3.43% – a cumulative growth of 31% over the outlook period, reflecting durable structural demand from legacy industrial sectors complemented by emerging growth drivers in clean energy and semiconductors.

Three structural shifts will reshape Europe’s industrial gases market through 2034: the rise of green hydrogen as a large-scale energy carrier, semiconductor expansion under the EU Chips Act driving ultra-high-purity gas demand, and industrial decarbonisation under EU ETS increasing demand for hydrogen, oxygen, and CO₂ services. As a result, the industry will evolve beyond its traditional commodity role into a dual function as both an industrial input supplier and a clean energy infrastructure enabler, with competitiveness defined by hydrogen infrastructure scale, specialty gas capabilities, and digital supply chain sophistication.

Research Methodology

Primary Research

Primary research included interviews with key industry stakeholders—procurement heads, plant operators, specialty gas distributors, and policy advisors—used to validate market sizing, supply chain dynamics, and competitive positioning.

Secondary Research

Secondary sources include European Industrial Gases Association (EIGA) statistical publications, Eurostat industrial production indices, IEA Global Hydrogen Review, European Hydrogen Backbone reports, EU Chips Act implementation documents, Bloomberg NEF electrolyser database, company annual reports and investor presentations (Air Liquide, Linde, Air Products, Messer SE & Co. KGaA), and trade publications including Gasworld, Industrial Minerals, and Chemical Week.

Forecasting Models

Market size estimations and forecasts were derived using a combination of bottom-up and top-down forecasting models incorporating end-use industry output projections, per-unit gas intensity coefficients, supply mode shift assumptions, and green hydrogen production capacity ramp curves. CAGR calculations are based on 2025 base year values and 2034 terminal year projections. All values are presented in USD Billion at 2025 constant exchange rates unless otherwise stated.

Europe Industrial Gases Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Nitrogen, Oxygen, Carbon Dioxide, Argon, Hydrogen, Others |

| Applications Covered | Manufacturing, Metallurgy, Energy, Chemicals, Healthcare, Others |

| Supply Modes Covered | Packaged, Bulk, On-Site |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Air Liquide, Linde PLC , Air Products and Chemicals, Inc., Messer SE & Co. KGaA, SOL Group S.p.A., Nippon Sanso Holdings Corporation, S.I.A.D. S.p.A., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Industrial Gases Market Report

The Europe industrial gases market was valued at USD 17.96 Billion in 2025, driven by nitrogen demand in manufacturing and food processing, oxygen in steel and healthcare, and accelerating hydrogen consumption in energy transition applications.

The market is projected to reach USD 24.32 Billion by 2034, growing at a CAGR of 3.43% during 2026 to 2034, supported by green hydrogen investment, semiconductor manufacturing expansion under the EU Chips Act, and healthcare sector demand.

Nitrogen leads with a 30.0% share in 2025, driven by its versatile applications in food preservation, electronics manufacturing, pharmaceutical packaging, and chemical process inerting across all major European industrial economies.

Hydrogen is the fastest-growing gas type at approximately 6.8% CAGR through 2034, underpinned by the EU Hydrogen Strategy's 10 million tonne domestic production target by 2030, DRI-based steel decarbonisation programmes, and emerging hydrogen mobility applications.

Bulk delivery commands 40.0% share in 2025, serving large industrial customers through cryogenic tanker scheduled delivery. On-site generation at 34.6% is the fastest-growing supply mode, driven by semiconductor fabs and DRI steelmakers seeking supply security.

Germany leads with 28.4% of European market revenues in 2025, anchored by the world's third-largest chemical industry, Europe's most productive steel sector, and a EUR 9 Billion National Hydrogen Strategy creating forward demand for electrolytic hydrogen.

Key drivers include the EU Hydrogen Strategy and REPowerEU mandates, ageing population, healthcare gas demand, steel and cement sector decarbonisation via DRI processes, semiconductor manufacturing expansion under the EU Chips Act, and food processing MAP applications.

Leading companies include Air Liquide, Linde PLC, Air Products and Chemicals, Inc., Messer SE & Co. KGaA, SOL Group S.p.A., Nippon Sanso Holdings Corporation, S.I.A.D. S.p.A and others.

Green hydrogen electrolysis produces ~8 kg of oxygen per kg of hydrogen, creating an additional merchant oxygen supply. At the same time, hydrogen demand is expanding beyond traditional refinery and chemical uses into steel, energy, and mobility, reshaping the industry’s revenue mix and investment focus through 2034.

In 2025, bulk delivery represented approximately USD 7.2 Billion (40.0%), on-site generation approximately USD 6.2 Billion (34.6%), and packaged gases approximately USD 4.6 Billion (25.4%) of the total USD 17.96 Billion European industrial gases market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)