Europe LED Lighting Market Size, Share, Trends and Forecast by Product Type, Installation, Application, and Country, 2026-2034

Europe LED Lighting Market Size, Share, Trends & Forecast (2026-2034)

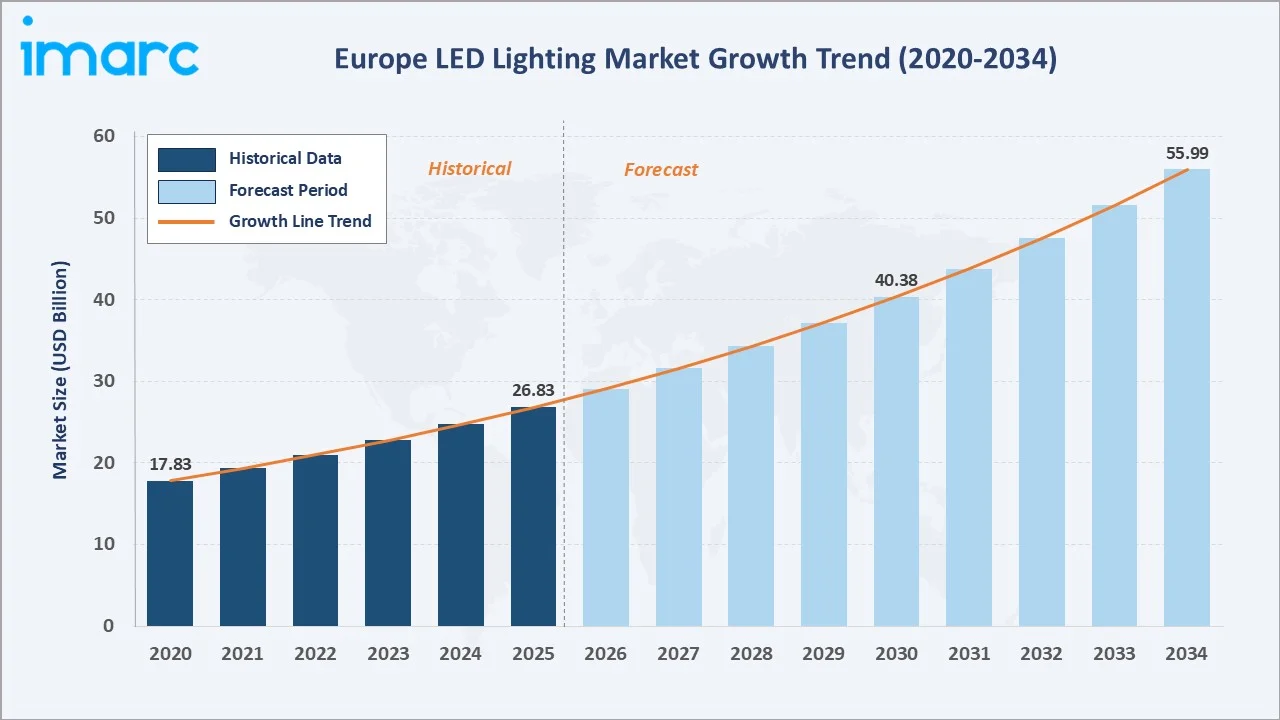

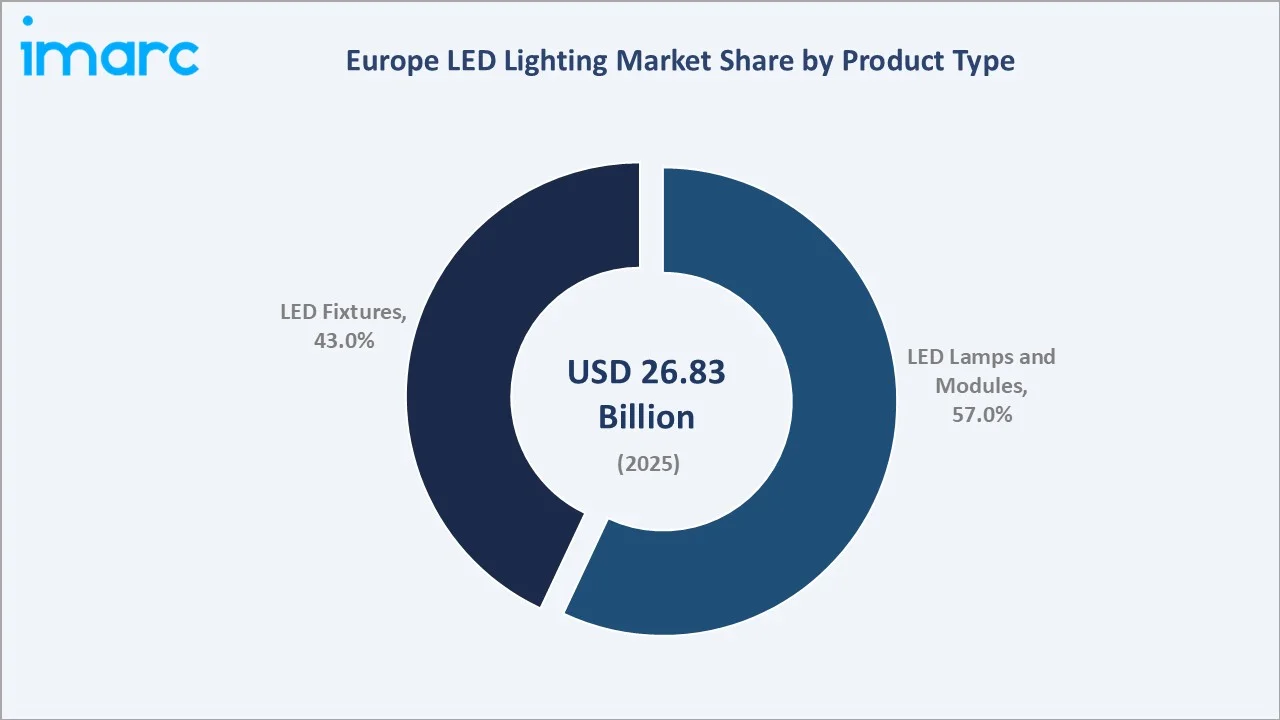

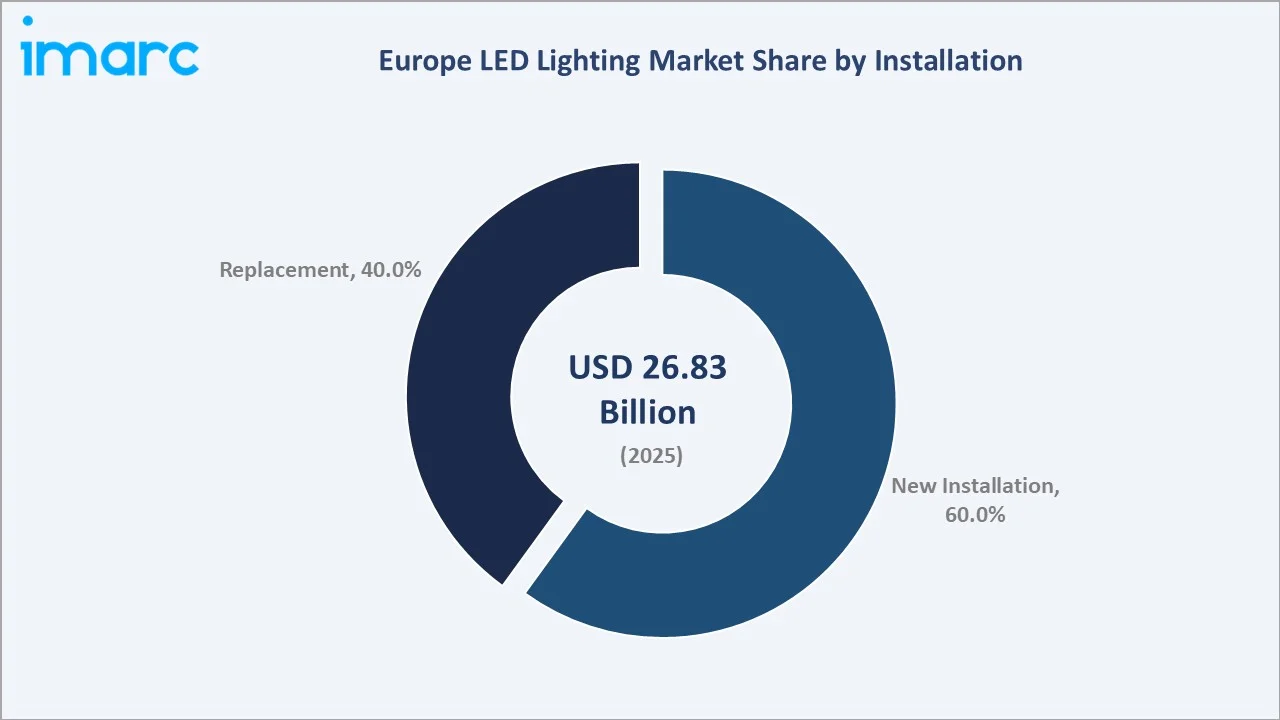

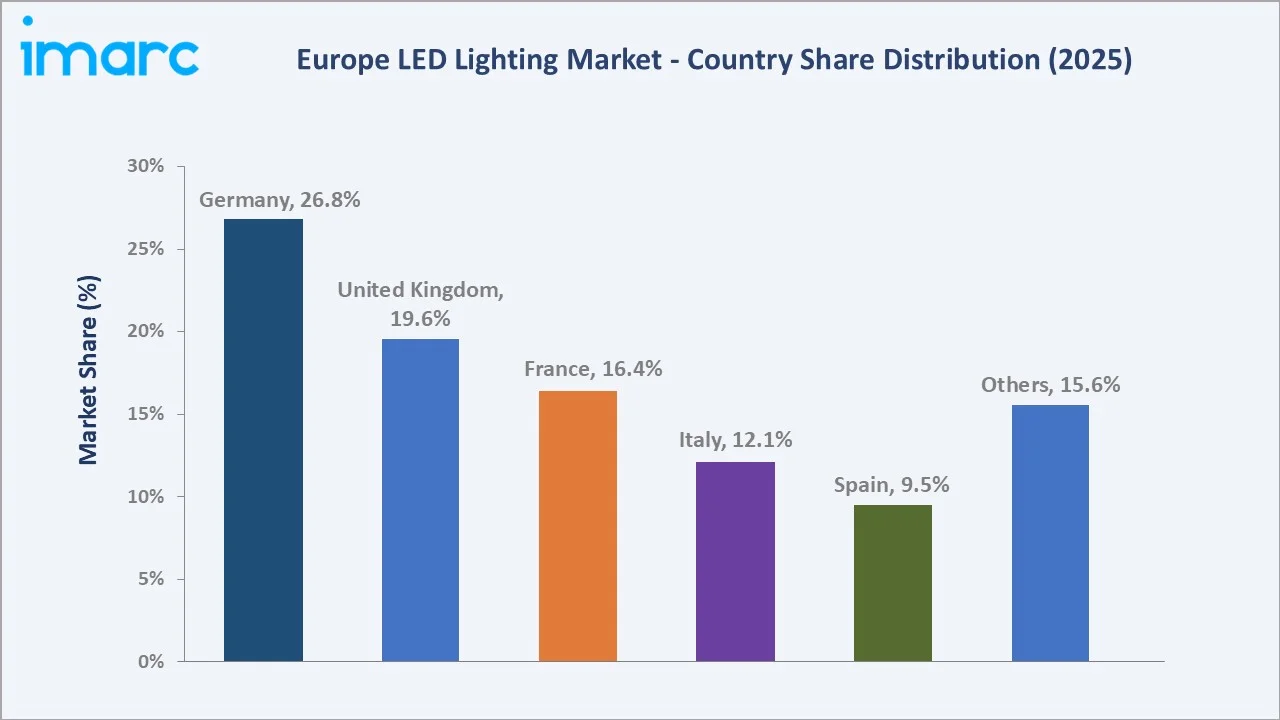

The Europe LED lighting market size was valued at USD 26.83 Billion in 2025 and is projected to reach USD 55.99 Billion by 2034, exhibiting a CAGR of 8.52% during the forecast period 2026-2034. EU energy efficiency regulations, urban infrastructure modernisation, rising adoption of smart and connected lighting, and retrofit demand across commercial and residential buildings are driving the Europe LED lighting market growth. LED Lamps and Modules lead the product type segment at 57.0% in 2025, while New Installation dominates the installation segment at 60.0%. Germany accounts for 26.8% of regional revenue in 2025, the largest national market in Europe for LED lighting.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 26.83 Billion |

|

Forecast Market Size (2034) |

USD 55.99 Billion |

|

CAGR (2026-2034) |

8.52% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (26.8% share, 2025) |

|

Fastest Growing Country |

Germany, supported by smart lighting uptake |

|

Leading Product Type |

LED Lamps and Modules (57.0%, 2025) |

|

Leading Installation |

New Installation (60.0%, 2025) |

The Europe LED lighting growth trajectory from 2020 through 2034 reflects steady historical expansion supported by EU-wide phase-out of inefficient lighting, and a forecast curve anchored by smart lighting integration, retrofit opportunities, and commercial infrastructure investment across leading European economies.

To get more information on this market, Request Sample

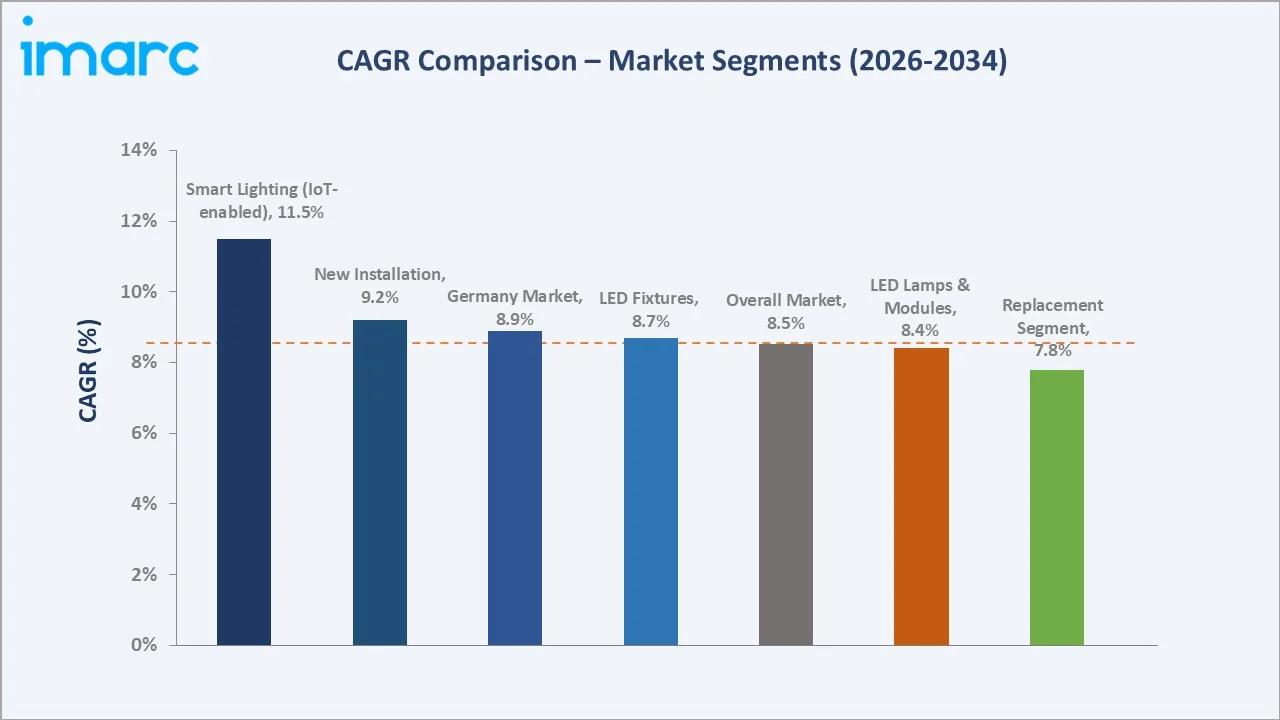

Segment-level CAGR comparison highlights smart lighting and new installation as the two fastest-growing sub-segments within the Europe LED lighting industry analysis through 2034, supported by IoT integration and large-scale EU infrastructure upgrades.

Executive Summary

The Europe LED lighting market is in a phase of accelerating expansion, shaped by the convergence of EU energy regulations, smart city deployments, and commercial retrofit cycles. Valued at USD 26.83 Billion in 2025, the market is forecast to reach USD 55.99 Billion by 2034 at a CAGR of 8.52%. The EU single-market framework harmonises energy efficiency rules, encouraging uniform LED adoption across member states.

LED Lamps and Modules command the dominant product type share at 57.0% in 2025, driven by widespread replacement demand and broad applicability across residential, commercial, and industrial end uses. LED Fixtures at 43.0% in 2025 serve integrated luminaire applications, with strong growth in office, retail, and hospitality fit-outs across Western Europe.

Germany leads with a 26.8% regional revenue share in 2025, supported by its large industrial base, robust green building activity, and early adoption of connected lighting platforms. The United Kingdom (19.6%) and France (16.4%) follow, with Italy, Spain, and others collectively rounding out the regional market, each contributing to a diversified European LED lighting landscape.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

LED Lamps and Modules - 57.0% share (2025) |

|

Largest Installation |

New Installation - 60.0% share (2025) |

|

Leading Country |

Germany - 26.8% revenue share (2025) |

|

Second Country |

United Kingdom - 19.6% revenue share (2025) |

|

Top Companies |

Signify Holding, ams-OSRAM AG, Zumtobel Group, TRILUX Lighting Ltd., Fagerhult Group, Glamox, Sylvania Group, and LEDVANCE GmbH |

Key Analytical Observations Supporting the Above Data:

- LED Lamps and Modules' 57.0% dominance in 2025 reflects broad residential and commercial adoption, supported by accessible price points, easy installation, and compatibility with legacy fixtures across the European building stock.

- New Installation share at 60.0% in 2025 reflects ongoing commercial real-estate development, large-scale infrastructure projects, and public sector building programmes where LED is specified as the default standard.

- Germany's 26.8% regional share in 2025 reflects its leading industrial and commercial building base, strong green-building certification uptake, and early adoption of smart and connected lighting platforms across public infrastructure.

Europe LED Lighting Market Overview

LED lighting in Europe is an integrated ecosystem combining component suppliers of chips, drivers, and optics; luminaire manufacturers delivering lamps, modules, and fixtures; smart-controls platform providers; and specialist distributors serving residential, commercial, industrial, and outdoor applications across the region.

Applications span commercial buildings, retail and hospitality, industrial facilities, street lighting, horticulture, and residential retrofits. Professional lighting specifiers, architects, and facility managers shape purchasing decisions, with growing emphasis on light quality, connectivity, and life-cycle carbon performance.

Macroeconomic enablers include EU Green Deal funding, building renovation programmes under the Energy Performance of Buildings Directive, post-pandemic commercial real-estate upgrades, and urban smart-city investments, which together underpin sustained LED lighting demand across all key European markets.

Market Dynamics

To evaluate market opportunities, Request Sample

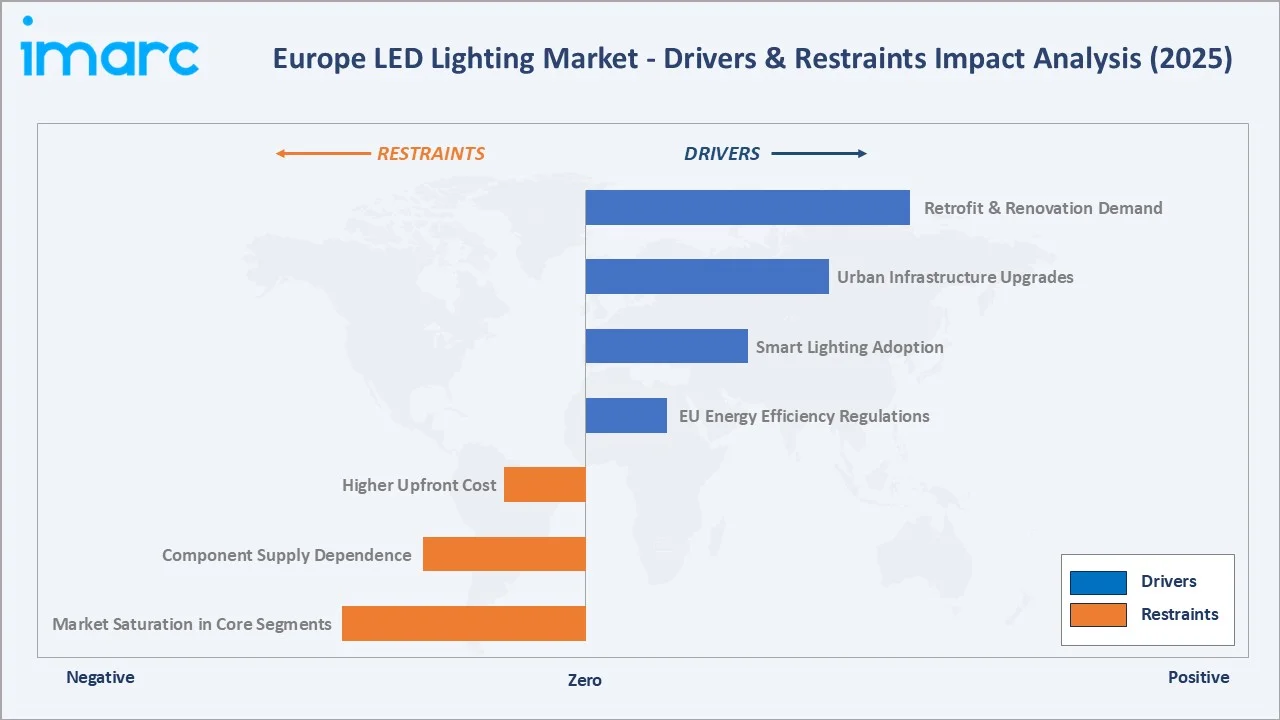

Market Drivers

- EU Energy Efficiency Regulations: The EU Ecodesign Directive and Single Lighting Regulation have progressively phased out inefficient lighting, mandating LED as the default option and anchoring structural demand across all member states.

- Smart Lighting Adoption: Growing deployment of IoT-enabled lighting, wireless controls, and daylight-harvesting systems is expanding premium product demand, particularly in German, Dutch, and UK commercial buildings. As of August 2025, Dortmund had 45,000 smart street lights fully operational, delivering over 70% energy savings and preventing more than 2,080 tonnes of CO₂ over six months through smart switching and dimming.

- Urban Infrastructure Upgrades: Municipal street-lighting conversion programmes, smart-city initiatives, and public transport modernisation projects are driving long-cycle demand for outdoor and industrial LED solutions. In November 2024, Itron announced a 10-year collaboration with Cielis, a consortium of Dalkia Electrotechnics and a subsidiary of Eiffage, to manage the City of Paris' nearly 200,000 smart streetlights using its CityEdge IoT portfolio, with the aim of reducing energy usage and improving sustainability.

- Retrofit and Renovation Demand: EU building renovation waves and energy-saving retrofits across commercial and residential stock are sustaining strong replacement-segment activity throughout the forecast period.

Market Restraints

- Higher Upfront Cost: Premium LED fixtures and connected systems carry higher initial costs versus legacy alternatives, slowing adoption in price-sensitive residential and small-commercial segments despite lifecycle savings.

- Component Supply Dependence: Europe's LED component supply chain remains substantially import-dependent, particularly from Asia, exposing manufacturers to currency fluctuations, shipping costs, and geopolitical supply risks.

- Market Saturation in Core Segments: Residential LED penetration has reached high levels across Western Europe, reducing replacement-cycle intensity in the basic lamp segment and pressuring average selling prices.

Market Opportunities

- Human-Centric and Circadian Lighting: Rising demand for wellbeing-focused lighting in offices, schools, and healthcare is opening a premium specification opportunity tied to tuneable-white and dynamic lighting solutions. For instance, Gagnef Municipality in Sweden installed human-centric lighting in two new schools opening in summer 2025, benefiting around 540 pupils aged 6–15 along with their teachers, with the municipality citing circadian rhythm support and pupil wellbeing as the primary rationale.

- Horticultural and Specialty LED: Growth in indoor and vertical farming, greenhouse cultivation, and aquaculture is creating a specialty LED market with high margins and strong technology differentiation.

- Li-Fi and Integrated Data Communications: Emerging light-based data transmission technologies offer early-stage commercial opportunities, particularly in secure environments where radio-frequency alternatives face constraints.

Market Challenges

- Product Commoditisation: Standard LED lamps face severe pricing pressure from low-cost Asian suppliers, squeezing margins and pushing European producers toward smart, connected, and specialty segments.

- End-of-Life and Recycling Compliance: Expanding WEEE obligations and circular-economy expectations require producers to invest in take-back, recycling, and eco-design capabilities, increasing compliance costs for mid-sized players.

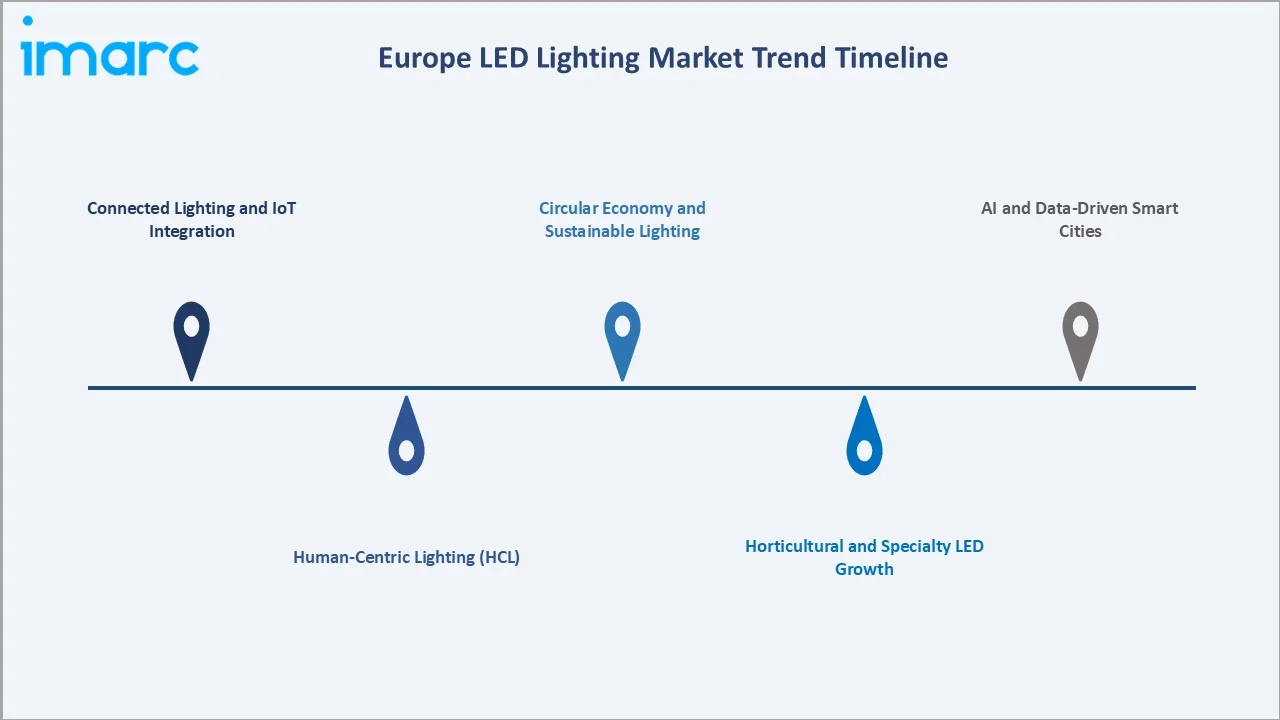

Emerging Market Trends

1. Connected Lighting and IoT Integration

Wireless mesh, Bluetooth, and Zigbee-based connected lighting platforms are moving from pilot deployments to standard specification in commercial buildings across Germany, the UK, and the Nordics. Integration with building management systems is enabling data-driven facility operations.

2. Human-Centric Lighting (HCL)

Tuneable-white and circadian-rhythm-aligned lighting solutions are gaining traction in offices, schools, healthcare, and senior-living facilities. Specifiers increasingly prioritise occupant wellbeing metrics alongside energy savings, particularly in Nordic and German markets.

3. Horticultural and Specialty LED Growth

Indoor farming, greenhouses, and vertical-agriculture installations are driving demand for specialty spectrum LEDs optimised for plant growth. The Netherlands, Germany, and the UK lead commercial-scale horticultural LED deployments. The Dutch Greenhouse Horticulture Energy Efficiency grant reopened in April 2025 with a €40 million budget, tightening LED conditions to require a minimum efficiency of photons per joule and mandatory dimmability for all qualifying installations.

4. Circular Economy and Sustainable Lighting

EU circular-economy policy and ecodesign rules are pushing manufacturers toward modular, serviceable, and recyclable LED products. Take-back schemes, repairable fixtures, and end-of-life recovery programmes are becoming competitive differentiators. For instance, German manufacturer TRILUX responded to the incoming ESPR framework by guaranteeing customers can purchase selected luminaires up to ten years after initial purchase, committing to repairability, long product service life, and long-term spare parts supply as core competitive differentiators.

5. AI and Data-Driven Smart Cities

European municipalities are deploying AI-optimised street lighting that adjusts output based on traffic, pedestrian presence, and weather. These platforms bundle lighting with broader smart-city sensors, creating long-term infrastructure opportunities.

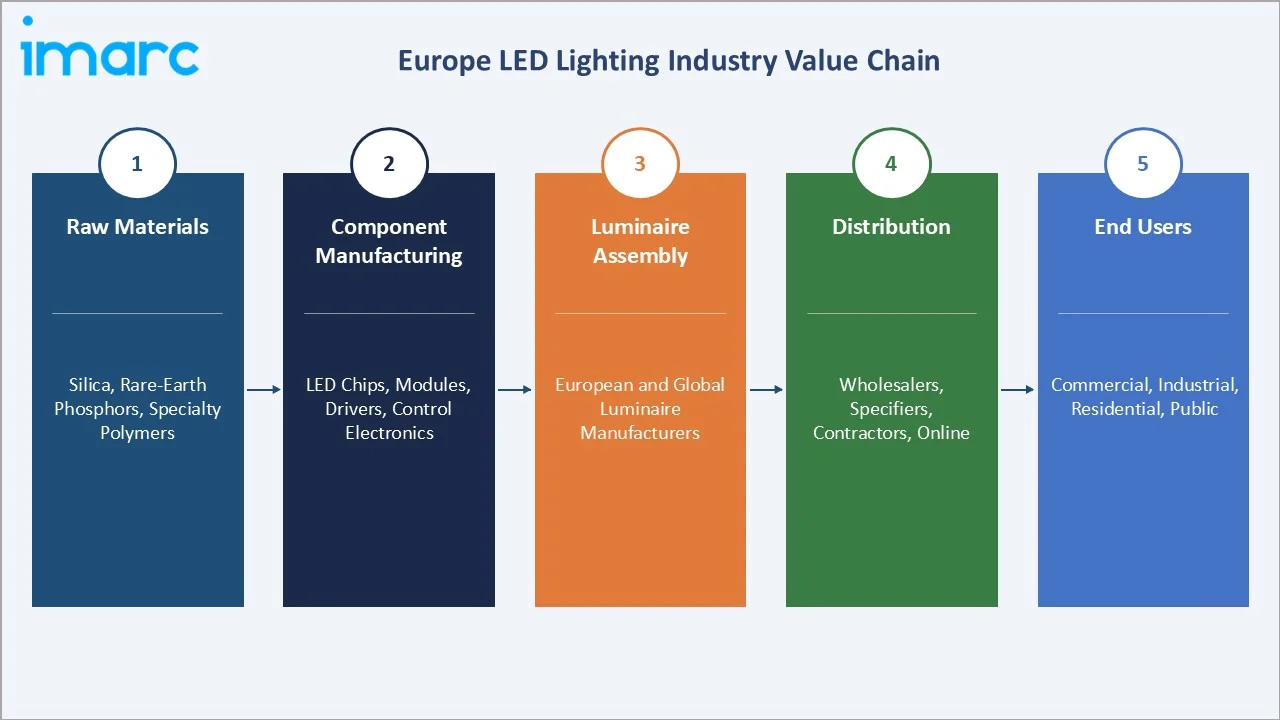

Industry Value Chain Analysis

The Europe LED lighting value chain spans five integrated stages from raw materials and semiconductor chip production through luminaire assembly, specification-led distribution, and installation services delivered to end-user sites across commercial, industrial, and residential segments.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Silica, rare-earth phosphors, and specialty polymers are sourced globally to produce the foundational inputs for LED chip fabrication and optical components. |

|

Component Manufacturing |

LED chips, modules, drivers, and control electronics are produced, primarily in Asia, and supplied to luminaire assemblers across Europe. |

|

Luminaire Assembly |

Components are engineered into finished lighting products by European and global manufacturers, with design, thermal management, and software integration adding value. |

|

Distribution |

Finished luminaires reach end users via electrical wholesalers, lighting specifiers, contractors, and retail channels, with specification-led routes dominant in commercial segments. |

|

End Users |

Lighting is installed and operated across commercial offices, industrial facilities, residential buildings, outdoor infrastructure, and horticultural environments. |

Luminaire manufacturers occupy the highest strategic-value position in the European LED lighting chain, combining optical design, driver electronics, industrial design, and smart-controls integration into turnkey solutions. Specification-led sales through architects, lighting designers, and facility managers dominate the professional segment, while consumer retail channels drive residential replacement volumes.

Technology Landscape in the Europe LED Lighting Industry

LED Chip and Luminaire Innovation

European specifiers increasingly demand higher-efficacy LED chips, improved colour rendering, and long-life fixtures with serviceable driver electronics supporting EU ecodesign repairability expectations. In April 2024, Signify launched the Philips PowerBalance UltraEfficient LED luminaire, delivering energy savings of up to 21.7% compared with other prevalent LED luminaires, alongside 3D-printed MyCreation luminaires using bio-circular materials, combining high-efficacy chip performance with circular design principles.

Smart Controls and Connectivity

Wireless mesh (Zigbee, Bluetooth Mesh, Thread), DALI-2 digital addressable lighting interfaces, and cloud-based lighting management platforms are becoming standard specifications in commercial buildings, enabling data-rich facility operations and integration with broader building management systems.

Human-Centric and Tuneable Lighting

Tuneable-white luminaires that adjust colour temperature and intensity to support circadian rhythms are scaling from premium offices into schools, healthcare, and senior-living facilities, particularly across Germany, the Nordics, and the Benelux markets.

Circular-Economy Design

Modular luminaire architectures with replaceable drivers and LED modules, standardised connectors, and recyclable aluminium housings are emerging as competitive differentiators as EU ecodesign rules expand repairability and end-of-life obligations.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | LED Lamps and Modules | 57.0% | 2025 |

| Installation | New Installation | 60.0% | 2025 |

| Application | Residential | 25.0% | 2025 |

| Country | Germany | 26.8% | 2025 |

By Product Type

LED Lamps and Modules command a 57.0% majority share in 2025, reflecting broad deployment across residential, commercial, and industrial applications where retrofit-compatible form factors allow straightforward replacement of legacy lighting. Price accessibility and DIY installation support high-volume adoption across European households and small-commercial sites.

To access detailed market analysis, Request Sample

LED Fixtures at 43.0% in 2025 serve integrated luminaire applications in professional settings, including offices, retail, hospitality, healthcare, and outdoor environments. Fixture-based specifications typically carry higher unit prices, smart-control integration, and longer warranty periods, driving a margin premium over standard lamps.

By Installation

New Installation applications dominate at 60.0% in 2025, driven by commercial real-estate development, public-sector infrastructure projects, and EU-funded renovation programmes where LED is specified as the default standard from the project outset.

Replacement applications at 40.0% in 2025 cover retrofit demand across existing building stock, with EU phase-out of inefficient lighting, retrofit incentives, and payback-driven building-owner decisions sustaining steady replacement-cycle activity across Germany, the UK, France, and southern European markets.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

26.8% |

Industrial base, green building adoption, smart lighting deployment |

|

United Kingdom |

19.6% |

Commercial retrofits, smart-city programmes, hospitality, and retail upgrades |

|

France |

16.4% |

Public infrastructure programmes, Paris regional renovation, retail modernisation |

|

Italy |

12.1% |

Tourism-led hospitality upgrades, industrial modernisation, and heritage lighting |

|

Spain |

9.5% |

Tourism sector, outdoor lighting upgrades, commercial real-estate renovation |

|

Others |

15.6% |

Nordics, Benelux, Poland, and other EU members are driving diverse demand |

Germany commands a 26.8% regional revenue share in 2025, the most dominant country position in the Europe LED lighting market. Germany combines the region's largest commercial and industrial building stock with early adoption of smart lighting platforms, strong green-building certification activity, and significant public infrastructure spending. The United Kingdom (19.6%) and France (16.4%) follow, anchored by commercial retrofit activity and public-sector modernisation programmes.

Italy holds 12.1% in 2025, supported by tourism-led hospitality upgrades and industrial modernisation. Spain (9.5%) benefits from outdoor lighting upgrades and tourism-sector investment. Other European markets (15.6%), including the Nordics, Benelux, and Poland, collectively drive meaningful demand through smart-city programmes and early adoption of human-centric and connected lighting platforms across public and commercial buildings.

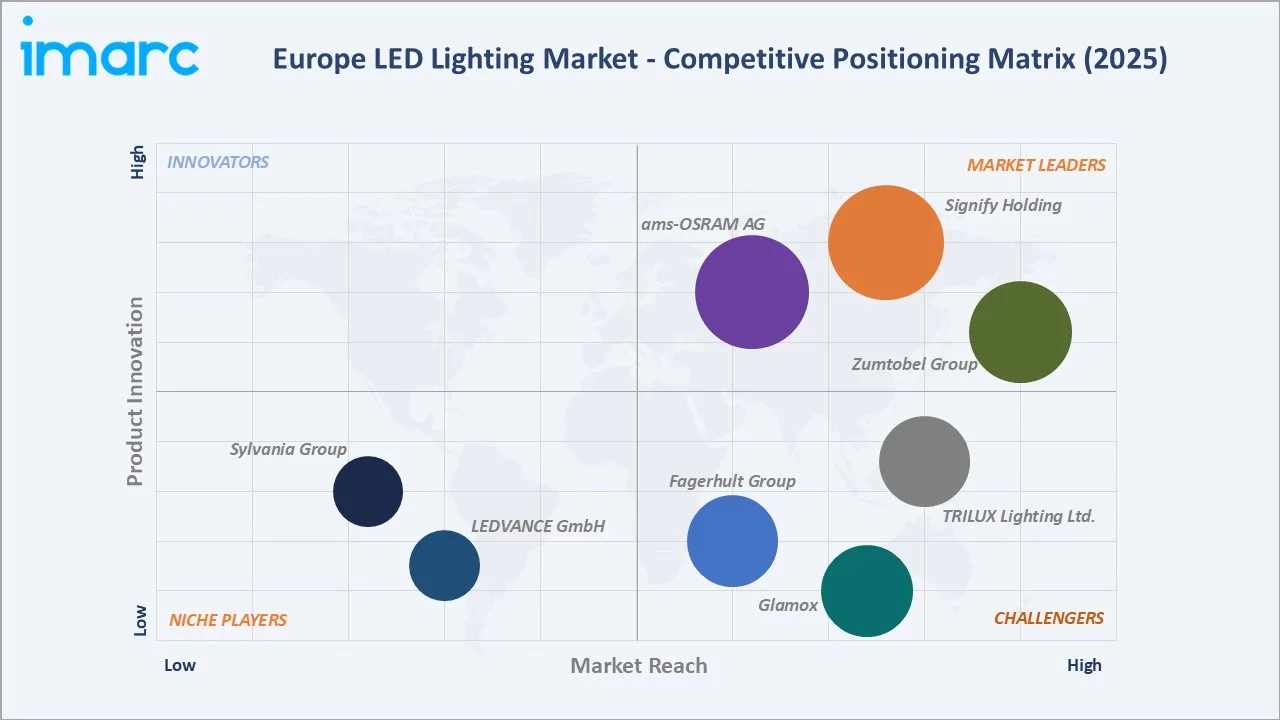

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Signify Holding |

Philips, Interact |

Leader |

Global scale, connected lighting platform, broad portfolio |

|

ams-OSRAM AG |

OSRAM, OSCONIQ |

Leader |

Component leadership, automotive, and specialty lighting |

|

Zumtobel Group |

Zumtobel, Thorn, Tridonic |

Leader |

Professional specification, architectural lighting |

|

TRILUX Lighting Ltd. |

LiveLink |

Challenger |

Mid-market professional, German commercial base |

|

Fagerhult Group |

Whitecroft, LED Linear |

Challenger |

Nordic design leadership, office and retail segments |

|

Glamox |

FX, COSMO APEX |

Challenger |

Marine, offshore, professional indoor applications |

|

Sylvania Group |

Sylvania PRO, START, SpeciaLITE |

Emerging |

Consumer and retail lighting, retrofit-focused |

|

LEDVANCE GmbH |

LED, Luminaires |

Emerging |

Consumer LED lamps, replacement market focus |

The Europe LED lighting competitive landscape is characterised by a handful of large integrated players commanding substantial professional and commercial specification share, alongside specialty and regional players with deep segment focus in architectural, outdoor, consumer, and marine markets. Market leaders differentiate through connected lighting platforms, specification-led sales organisations, and long-established relationships with architects and facility managers.

Key Company Profiles

Signify Holding

Signify, headquartered in Eindhoven, Netherlands, is the world leader in professional and consumer lighting, operating the Philips, Interact, and Color Kinetics brands across residential, commercial, industrial, and outdoor applications globally.

- Product & Platform Portfolio: Philips LED lamps and luminaires, Interact connected lighting platform, Color Kinetics architectural lighting, horticultural LEDs.

- Recent Developments: In September 2025, Signify launched the Philips Hue Bridge Pro alongside a redesigned range of LED strip lights and an entry-level product line, representing a major smart home lighting update supporting triple the device connections of the previous model and integrated AI-powered scene creation.

- Strategic Focus: Signify prioritises connected lighting leadership through its Interact platform, circular-economy differentiation, and strong specification-led sales across commercial, horticultural, and outdoor applications in Europe.

ams-OSRAM AG

ams OSRAM, formed through the merger of Austrian ams AG and German OSRAM Licht AG, is a global component and automotive lighting leader with significant European presence across specialty and professional segments.

- Product & Platform Portfolio: OSRAM LED chips and modules, automotive LED solutions, specialty and entertainment lighting, digital systems.

- Recent Developments: In December 2025, ams OSRAM expanded its NIGHT BREAKER LED portfolio with the launch of the NIGHT BREAKER LED C5W ECE, the first ECE R37-approved LED signal lamp for 12V vehicles, alongside four new NIGHT BREAKER LED SMART retrofit models, accelerating the automotive transition from halogen to LED signal lamps across European and ECE-regulated markets.

- Strategic Focus: ams OSRAM targets high-margin LED components and specialty applications, automotive lighting innovation, and selective portfolio restructuring, leveraging component leadership across European and global end markets.

Zumtobel Group

Zumtobel Group, headquartered in Dornbirn, Austria, is a leading European professional and architectural lighting group, operating Zumtobel (high-end architectural), Thorn (outdoor and industrial), and Tridonic (components) brands.

- Product & Platform Portfolio: Zumtobel architectural luminaires, Thorn outdoor and industrial fixtures, Tridonic drivers and LED modules.

- Recent Developments: In November 2025, Zumtobel Group and ams OSRAM jointly launched a paper-based alternative to plastic reels for transporting LED strips and components, reducing weight by over a third and CO2 emissions by 80%, reinforcing the Group's circular-economy positioning aligned with EU ecodesign rules.

- Strategic Focus: Zumtobel focuses on premium architectural specification, professional outdoor and industrial lighting through Thorn, and components leadership through Tridonic, combining design heritage with technical innovation for specifier-led markets.

Market Concentration Analysis

The Europe LED lighting market exhibits moderate concentration, with Signify, ams OSRAM, Zumtobel, Trilux, and Fagerhult collectively accounting for a substantial combined share of the professional and specification-led segments in 2025. The remaining market is distributed across specialty, regional, and consumer-focused players.

Segment-level concentration varies meaningfully. Professional and architectural specifications are more concentrated, as long-cycle projects favour established brands with comprehensive catalogues and specification support. The consumer lamp segment is more fragmented, with private-label and low-cost imports from Asia competing aggressively with branded European offerings.

Consolidation trends are expected to continue through 2030, driven by connected-lighting platform scale economics, ESG-linked financing, and the need for full European service coverage. Smaller specialty players with unique capabilities in horticultural, human-centric, or marine lighting remain attractive acquisition targets for larger groups seeking segment-specific differentiation.

Investment & Growth Opportunities

Fastest-Growing Segments

Smart and IoT-enabled lighting is the highest-growth sub-segment through 2034, driven by commercial building automation and EU smart-city initiatives. Germany and the UK lead regional growth, supported by the largest smart-building investment pipelines and strongest specification ecosystems.

Emerging Market Expansion

Horticultural LED, human-centric lighting, and Li-Fi data communications are the emerging premium sub-markets. Smart-city and circular-economy-aligned lighting platforms represent the highest-potential opportunity, offering both product-premium pricing and recurring service revenue through connected platform subscriptions.

Venture & Private Investment Trends

Notable transactions include continued strategic investment in connected lighting platforms, portfolio consolidation by listed groups such as Signify and Zumtobel, and private-equity interest in specialty and horticultural LED players. Start-ups in Li-Fi, tuneable-white, and modular-luminaire design are attracting European venture capital.

Future Market Outlook (2026-2034)

The Europe LED lighting market forecast projects sustained expansion from USD 26.83 Billion in 2025 to USD 55.99 Billion by 2034 at a CAGR of 8.52%, supported by EU decarbonisation policy, urban infrastructure investment, building renovation waves, and sustained commercial and public-sector demand for energy-efficient lighting.

Three technology discontinuities are most likely to reshape the European market through 2034. Connected lighting will shift from premium option to baseline specification in commercial buildings. Human-centric lighting will expand from office premium into schools, healthcare, and senior-living. Circular-economy product architectures will become a competitive requirement rather than a differentiator.

By 2034, the Europe LED lighting industry will have transitioned from a product-centric supply model toward integrated service and platform economics, where connected lighting data, building-management integration, and long-cycle service contracts drive competitive advantage. Leadership will consolidate around three strategic archetypes: integrated platform leaders (Signify, Zumtobel), specification specialists (Trilux, Fagerhult, Glamox), and component/specialty players.

Research Methodology

Primary Research

Primary research encompassed structured interviews with European lighting industry stakeholders, including product managers at leading luminaire manufacturers, facility managers, commercial lighting specifiers and architects, municipal smart-city leads, and European distribution specialists. Primary insights validated market sizing, segmentation, and competitive positioning.

Secondary Research

Secondary sources include European Commission energy efficiency publications, Eurostat statistics, LightingEurope industry reports, company annual reports from Signify, ams OSRAM, Zumtobel, and peer groups, trade publications, and European smart-building conference proceedings.

Forecasting Models

Market size estimations were derived using a combination of top-down and bottom-up models, incorporating European building stock data, renovation-rate assumptions, regulatory phase-out schedules, and historical evolution patterns. Scenario analysis (base, optimistic, conservative) was performed to account for regulatory and energy-cost variability.

Europe LED Lighting Market Report Coverage

|

Attribute |

Details |

|

Market Size (2025) |

USD 26.83 Billion |

|

Forecast Size (2034) |

USD 55.99 Billion |

|

CAGR (2026-2034) |

8.52% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Segmentation |

By Product Type (LED Lamps & Modules, LED Fixtures); By Installation (New, Replacement) |

|

Regional Analysis |

Germany, United Kingdom, France, Italy, Spain, and Others |

|

Key Companies |

Signify Holding, ams-OSRAM AG, Zumtobel Group, TRILUX Lighting Ltd., Fagerhult Group, Glamox, Sylvania Group, LEDVANCE GmbH, etc. |

|

Report Format |

PDF, Excel |

|

Customisation |

Available on request |

Frequently Asked Questions About the Europe LED Lighting Market Report

The Europe LED lighting market was valued at USD 26.83 Billion in 2025, driven by EU energy efficiency regulations, smart lighting adoption, urban infrastructure upgrades, and sustained retrofit demand across commercial and residential buildings.

The market is projected to reach USD 55.99 Billion by 2034, growing at a CAGR of 8.52% during 2026-2034, driven by connected lighting deployment, EU decarbonisation policy, and sustained commercial demand.

LED Lamps and Modules lead with a 57.0% share in 2025, driven by broad residential and commercial adoption, accessible pricing, and retrofit-compatible form factors across the European building stock.

New Installation dominates with a 60.0% share in 2025, driven by commercial real-estate development, public-sector infrastructure projects, and EU-funded renovation programmes across member states.

Germany leads with a 26.8% share in 2025, driven by its large industrial and commercial building stock, strong green-building certification uptake, and early adoption of smart and connected lighting platforms.

Key drivers include EU Ecodesign regulations, smart lighting and IoT adoption, urban infrastructure upgrades, building renovation programmes under the Energy Performance of Buildings Directive, and commercial retrofit activity.

Smart and IoT-enabled lighting is the fastest-growing sub-segment, driven by commercial building automation demand, EU smart-city initiatives, and premium specifications in offices, healthcare, and public buildings.

Leading companies include Signify Holding, ams-OSRAM AG, Zumtobel Group, TRILUX Lighting Ltd., Fagerhult Group, Glamox, Sylvania Group, and LEDVANCE GmbH across the European market.

EU Ecodesign and Single Lighting Regulation phase out inefficient lighting technologies, mandate LED efficiency thresholds, and push manufacturers toward repairability, recyclability, and circular-economy product architectures.

Human-Centric Lighting refers to tuneable-white and circadian-rhythm-aligned LED solutions that support occupant wellbeing and productivity, gaining traction in offices, schools, healthcare, and senior-living facilities across Europe.

Smart lighting with wireless controls and IoT integration enables data-driven building operations, occupancy-based dimming, and daylight harvesting, representing the fastest-growing premium sub-segment across commercial and public applications.

Replacement applications account for 40.0% of the market in 2025, driven by EU phase-out of inefficient lighting, retrofit incentives, and payback-driven upgrade decisions across commercial and residential building stock.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)