Europe Real Estate Market Size, Share, Trends and Forecast by Property, Business, Mode, and Country, 2026-2034

Europe Real Estate Market Size, Share, Trends & Forecast (2026-2034)

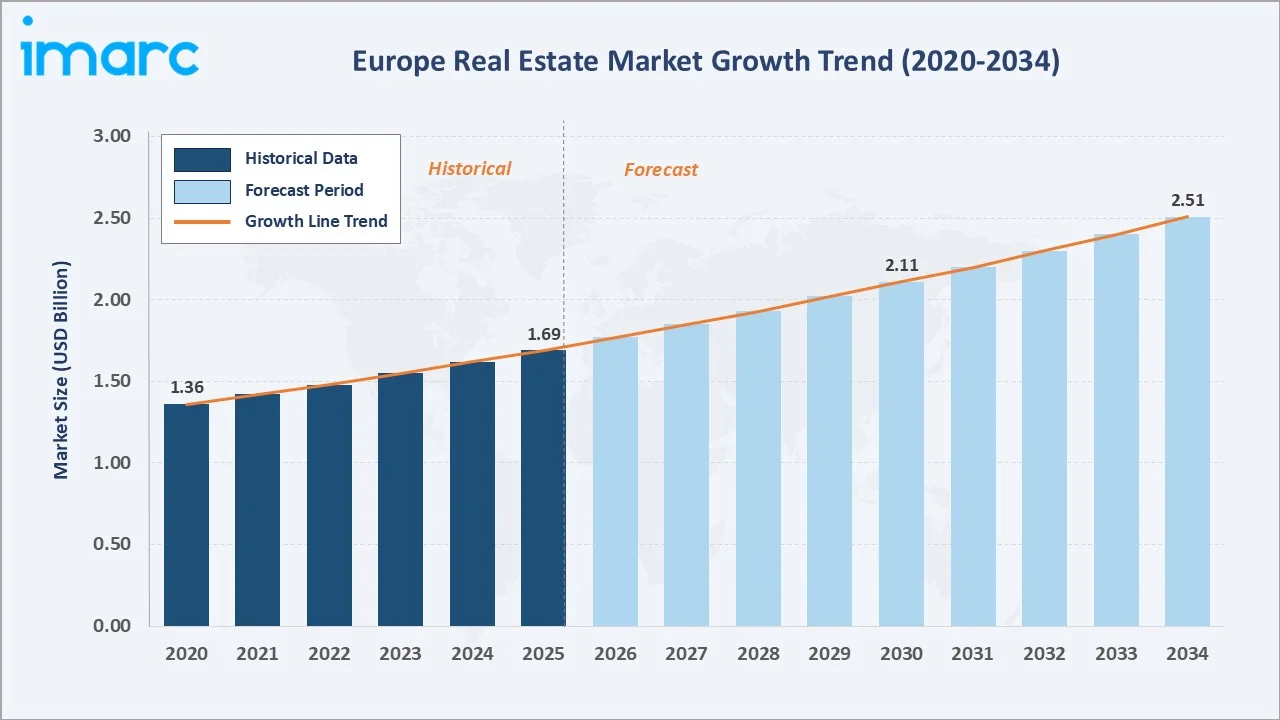

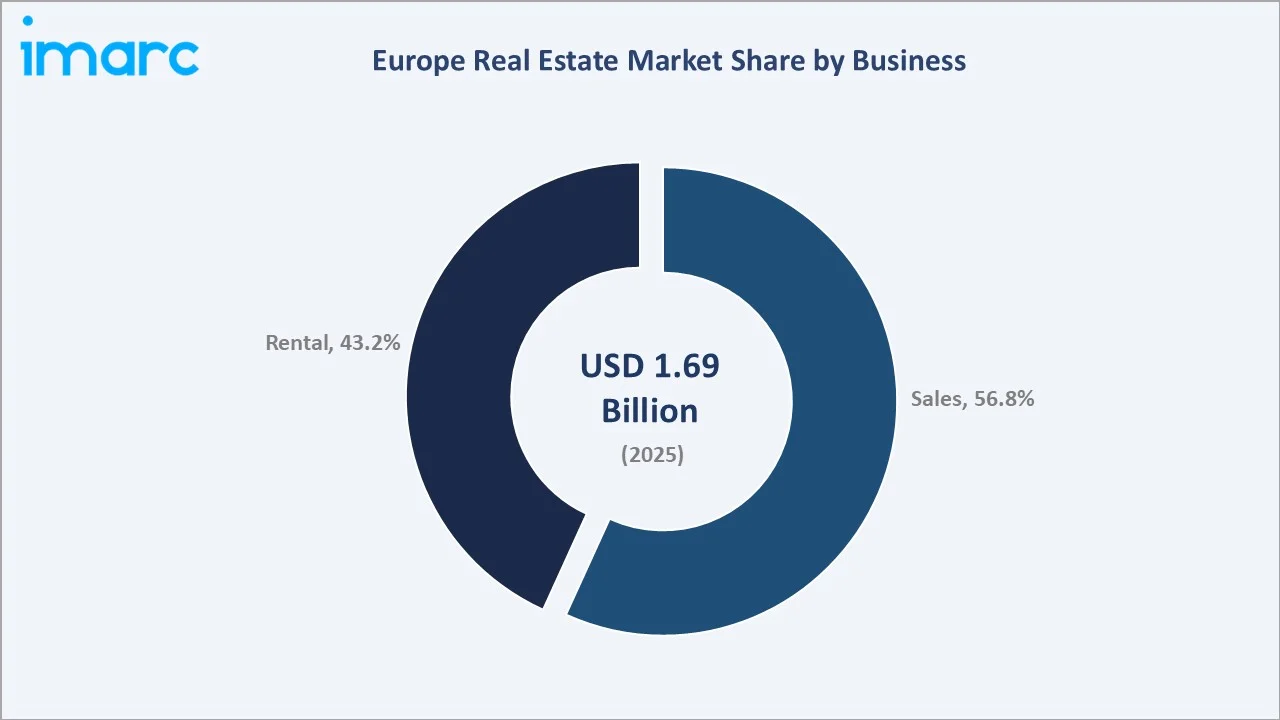

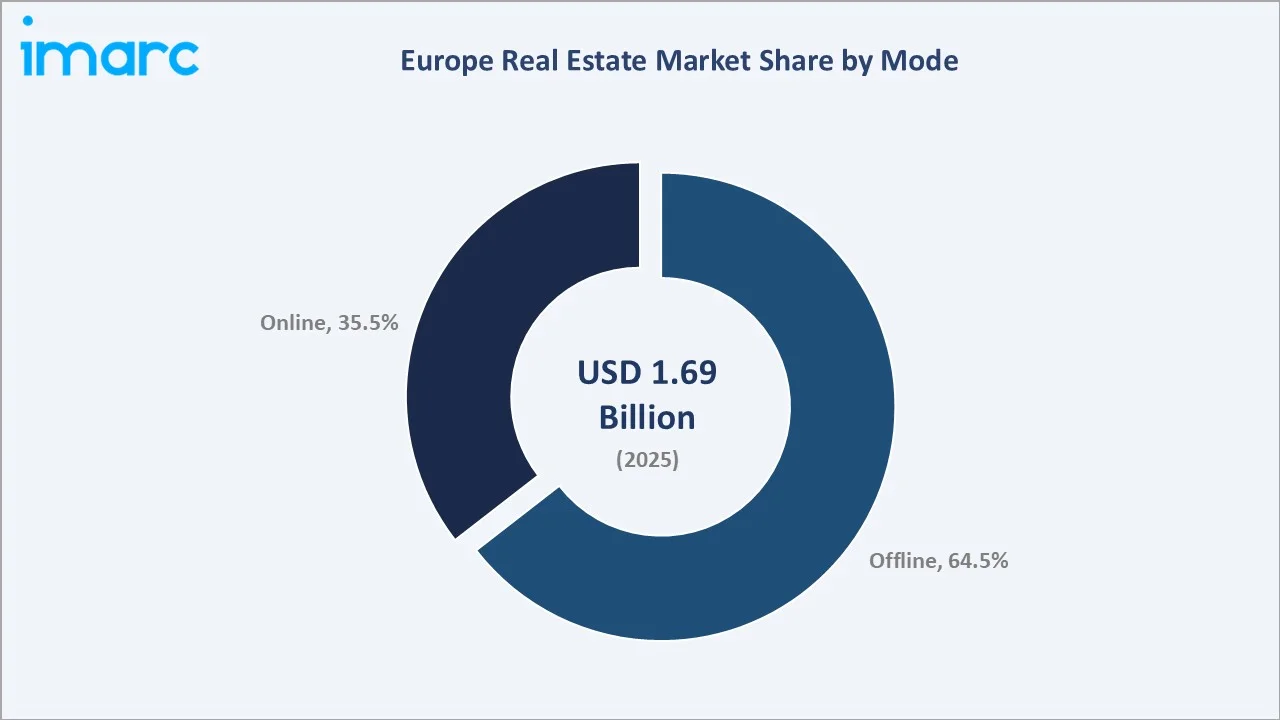

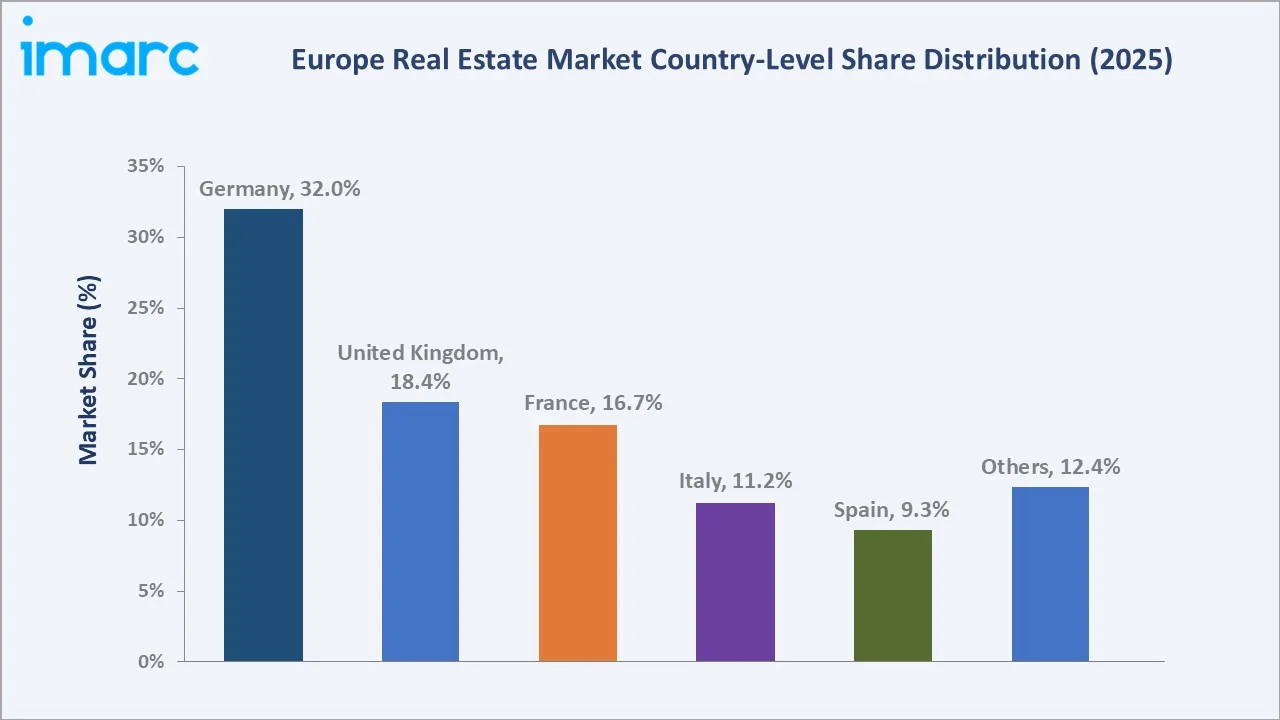

The Europe real estate market size was valued at USD 1.69 Billion in 2025 and is projected to reach USD 2.51 Billion by 2034, exhibiting a CAGR of 4.46% during the forecast period 2026-2034. Rising urban population, sustained cross-border institutional capital inflows, post-pandemic office repositioning, and rapid digitalisation of property workflows are driving the Europe real estate market growth. Sales leads the business segment at 56.8% in 2025, while Offline dominates the mode segment at 64.5%. Germany accounts for 32.0% of regional revenue in 2025, the largest country-level market, powered by its deep institutional investor base and resilient residential demand.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.69 Billion |

|

Forecast Market Size (2034) |

USD 2.51 Billion |

|

CAGR (2026-2034) |

4.46% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country Market |

Germany (32.0% share, 2025) |

|

Fastest Growing Country Market |

Spain (CAGR ~5.4%) |

|

Leading Business Segment |

Sales (56.8%, 2025) |

|

Leading Mode Segment |

Offline (64.5%, 2025) |

The Europe real estate market growth trajectory from 2020 through 2034 reflects steady historical expansion through pandemic recovery, extending into a sustained forecast curve powered by residential modernisation, logistics, and data-centre expansion, and cross-border institutional capital.

To get more information on this market, Request Sample

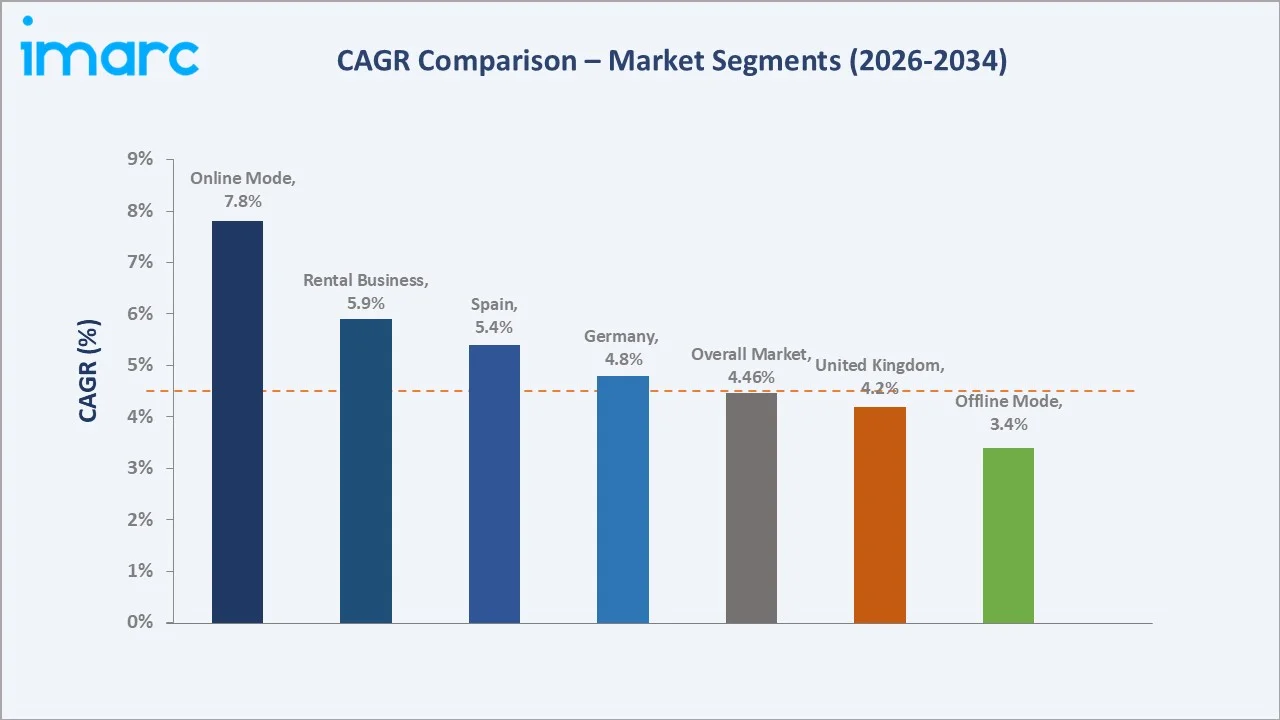

Segment-level CAGR comparisons highlight Online Mode and Rental Business as the fastest-growing sub-segments through 2034, driven by platform-based property discovery and the shift toward institutional build-to-rent housing.

Executive Summary

The Europe real estate market is undergoing a structural transformation driven by urban housing deficits, evolving workplace models, and digital transaction platforms. Valued at USD 1.69 Billion in 2025, the market is forecast to reach USD 2.51 billion by 2034 at a CAGR of 4.46%. Eurostat reported roughly 75% of Europe's population lives in urban areas in 2024, creating housing demand that outpaces supply in core metros.

Sales commands the dominant business share at 56.8% in 2025, underpinned by Southern European homeownership culture and institutional deals in logistics and multifamily assets. Rental at 43.2% is the fastest-growing mode, supported by affordability pressures and BTR expansion across Germany, the UK, and the Netherlands.

Germany dominates with a 32.0% regional share in 2025, led by 43+ million dwellings and a safe-haven status for cross-border capital. The UK holds 18.4% and France 16.7%, characterised by mature institutional frameworks and premium commercial concentration in London and Paris.

Key Market Insights

|

Insight |

Data |

|

Leading Business Segment |

Sales - 56.8% share (2025) |

|

Leading Mode Segment |

Offline - 64.5% share (2025) |

|

Leading Country Market |

Germany - 32.0% revenue share (2025) |

|

Second Country Market |

United Kingdom - 18.4% share (2025) |

|

Top Companies |

Vonovia SE, CBRE, Jones Lang LaSalle IP, Inc., Savills plc, UNIBAIL-RODAMCO-WESTFIELD |

Key Analytical Observations Supporting the Above Data:

- Sales's 56.8% dominance reflects Europe's homeownership culture, where Romania, Hungary, and Spain report ownership rates above 75%, combined with institutional deal flow in income-producing assets.

- The offline channel leads at 64.5% in 2025, supported by advisory-intensive high-ticket transactions, entrenched notary systems, and preference for in-person due diligence in commercial deals above EUR 10 million.

- Germany's 32.0% dominance reflects its dual role as Europe's largest housing market and deepest institutional real estate capital pool, holding over EUR 600 billion in managed assets.

- Online mode is the fastest-growing sub-segment at ~7.8% CAGR through 2034, driven by portal consolidation and rapid digital mortgage and e-conveyancing adoption.

- Pan-European logistics yields reached 5.1% weighted average in 2024 per CBRE, reflecting rerating as e-commerce penetration above 18% pulls warehouse absorption.

- Spain leads country-level growth at ~5.4% CAGR, supported by tourism-linked residential demand, Madrid office repricing, and Iberian logistics exposure.

Europe Real Estate Market Overview

Europe real estate encompasses land and built-asset ownership, leasing, and investment across residential, commercial, industrial, and land categories. The ecosystem integrates developers, institutional owners, retail investors, brokerage networks, property managers, digital listing platforms, mortgage lenders, and public REITs across the EU-27, UK, Switzerland, and Norway.

Applications span primary housing, rental dwellings, offices, shopping centres, logistics parks, data centres, hotels, healthcare real estate, and development land.

Market Dynamics

To evaluate market opportunities, Request Sample

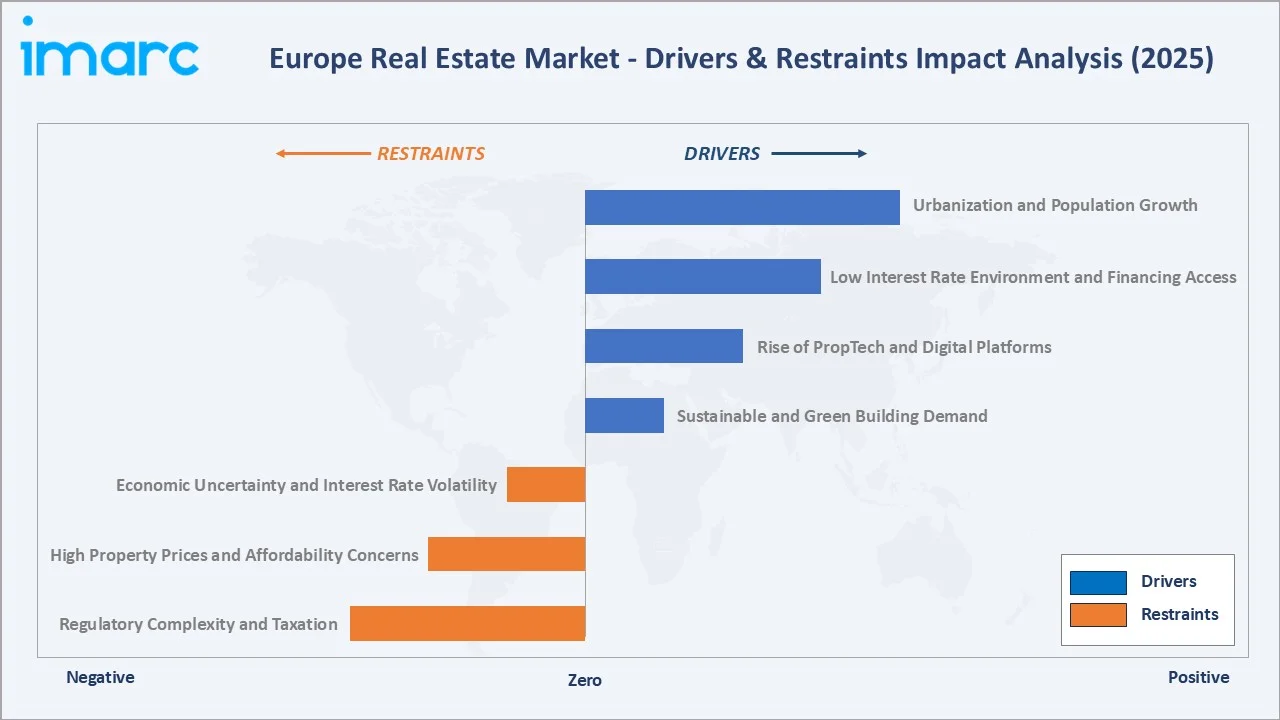

Market Drivers

- Structural Housing Deficit & Urbanisation: Europe continues to face a significant housing shortfall of ~5 million units, particularly concentrated in high-demand urban centres such as Amsterdam, Berlin, and Dublin. Persistent under-supply relative to household formation is sustaining upward pressure on residential prices.

- Logistics & Alternative Asset Expansion: Investment into logistics, data centres, and life sciences assets exceeded EUR 85 billion in 2024. Rising e-commerce penetration (~18.4%) is directly translating into strong logistics absorption and demand for last-mile infrastructure.

- Interest Rate Normalisation: The refinancing rate stabilised at ~2.15% by Q4 2025, following a peak cycle. This has improved financing visibility, revived cross-border capital flows, and driven a >20% YoY rebound in transaction volumes.

- ESG-Driven Building Modernisation: Regulatory momentum around sustainability and net-zero targets is accelerating a large-scale retrofit cycle across Europe’s ageing building stock, creating substantial capital deployment opportunities through 2030.

Market Restraints

- Regulatory Uncertainty & Rent Controls: Policy interventions such as rent caps and freezes across key markets are limiting rental yield growth and reducing investor confidence, particularly in the build-to-rent (BTR) segment.

- Construction Cost Inflation: Elevated construction costs (up ~18–22% since 2021) continue to compress developer margins, leading to project delays and reduced pipeline viability in marginal developments.

- Office Market Repricing: Post-pandemic demand shifts have driven vacancy rates above 12% in select Tier-2 cities. Older Grade-B office assets face structural obsolescence, resulting in a bifurcated (“two-speed”) office market.

Market Opportunities

- Build-to-Rent & Living Sector Growth: Institutional capital is increasingly targeting rental housing, with over EUR 22 billion invested in BTR and private rented sector platforms. The segment remains under-penetrated compared to more mature markets, offering long-term scalability.

- Data Centres & Digital Infrastructure: Data centre investment surpassed EUR 8 billion in 2024, with major hubs accounting for the majority of capacity additions. Demand is being driven by hyperscale cloud adoption and AI-related workloads.

- Demographic-Led Alternative Assets: Rising demand for senior living, healthcare infrastructure, and student housing is supported by long-term demographic trends, including a rapidly ageing population base.

Market Challenges

- Energy Transition Capex Burden: Compliance with evolving energy-efficiency standards is expected to require substantial retrofit investment, placing financial strain on smaller and fragmented property owners.

- Market Fragmentation Across Jurisdictions: Europe’s multi-country landscape, with diverse regulatory frameworks, legal systems, and data standards, continues to create complexity in cross-border transactions and limits scalability for investors and PropTech platforms.

Emerging Market Trends

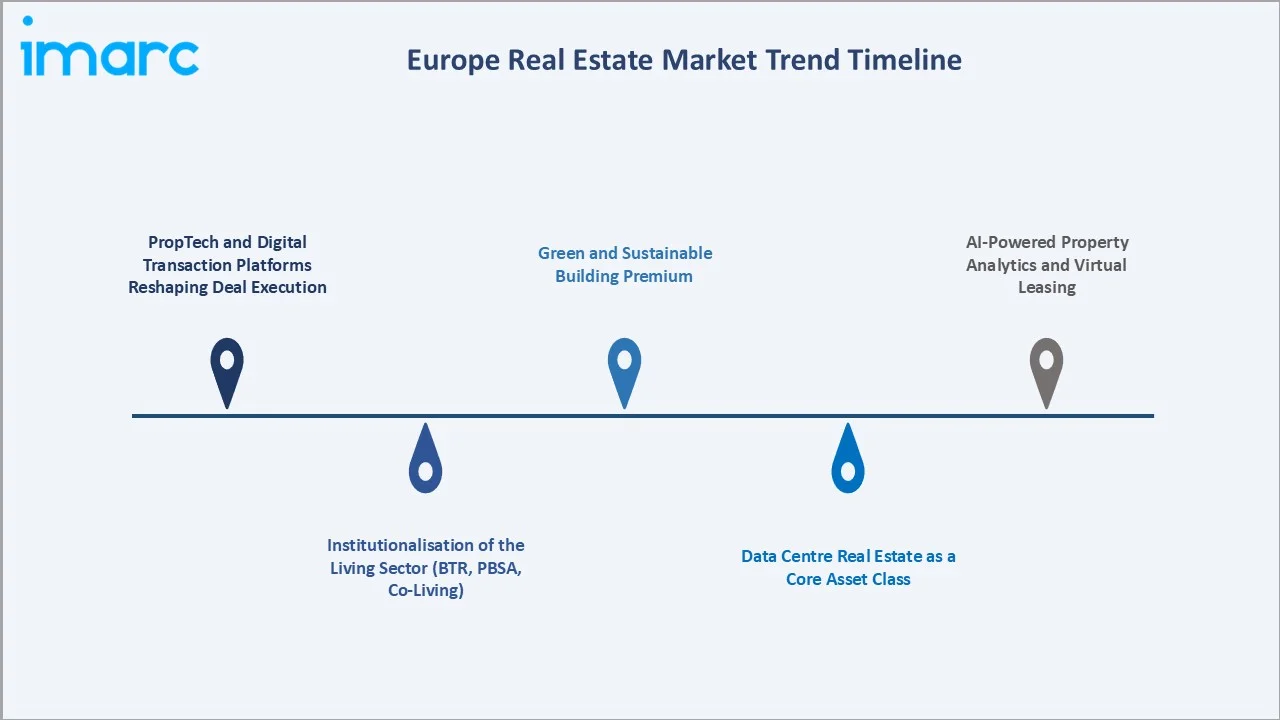

1. PropTech and Digital Transaction Platforms Reshaping Deal Execution

European PropTech funding reached EUR 3.6 billion in 2024, per CREtech, focused on digital underwriting, fractional ownership, and ESG data. IMMO Capital, Habyt, and Seaya are industrialising residential transactions. E-conveyancing in the UK and Germany is compressing transaction times from months to weeks.

2. Institutionalisation of the Living Sector (BTR, PBSA, Co-Living)

Living-sector capital rose to 22% of European transactions in 2024, up from 14% in 2019 per MSCI. Blackstone, Greystar, and Heimstaden are building multi-billion-euro portfolios in Berlin, Madrid, and Copenhagen.

3. Green and Sustainable Building Premium

BREEAM Outstanding and LEED Platinum offices commanded a 10-12% rent premium and 5-7% capital uplift in 2024 per JLL. Green-leased space represents 38% of prime central London office stock.

4. Data Centre Real Estate as a Core Asset Class

European data-centre additions reached 1.1 GW in 2024 per Cushman & Wakefield, with Amazon, Microsoft, and Google anchoring long-dated leases. Dublin, Frankfurt, and London remain primary hubs while Madrid, Milan, and Warsaw emerge as Tier-2 targets.

5. AI-Powered Property Analytics and Virtual Leasing

Generative AI embedded in CoStar, Idealista, and Rightmove is transforming property search and valuation. AI-driven AVMs now cover over 60% of European urban residential stock, enabling instant-offer capabilities used by iBuyers such as Casavo.

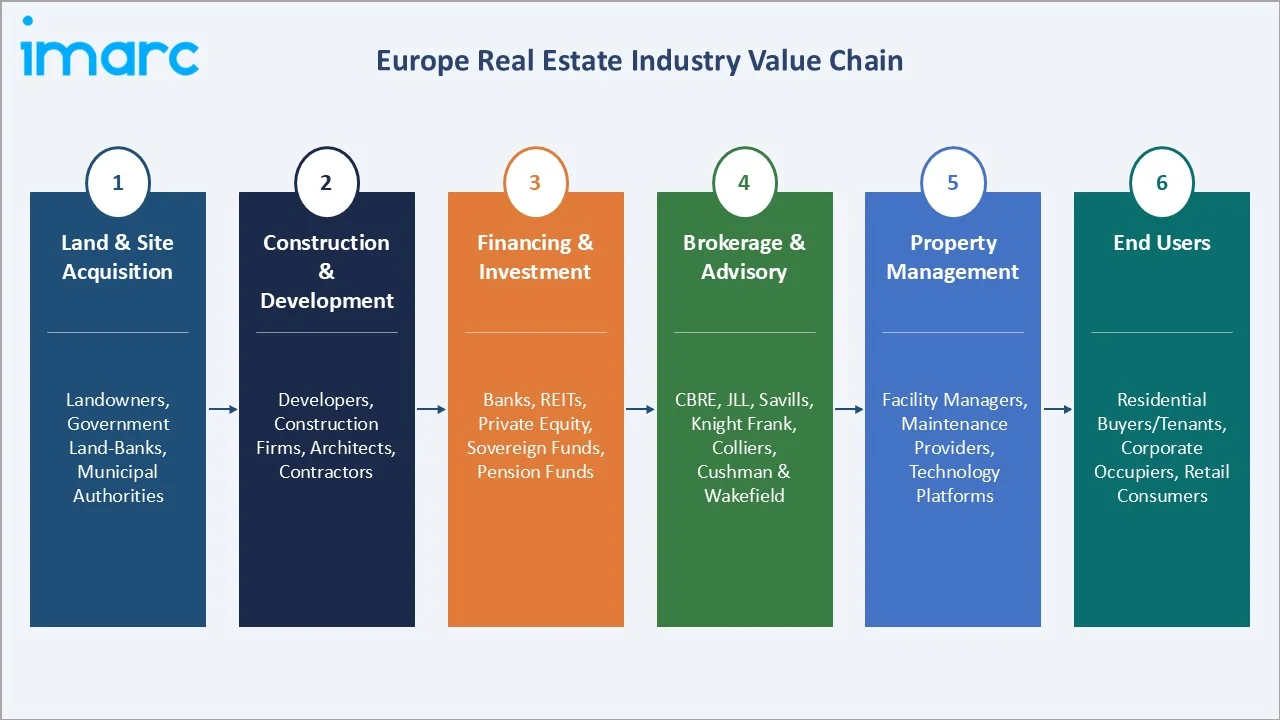

Industry Value Chain Analysis

The Europe real estate value chain spans six integrated stages from land assembly through end-user occupancy, each with distinct competitive dynamics and margin profiles.

|

Stage |

Key Players / Activities |

|

Land & Development |

Covers land acquisition, planning, and new property delivery — shaped by Europe's persistent housing shortages and tightening EU green building mandates. |

|

Construction & Contractors |

Physical delivery of buildings from structure to fit-out, facing headwinds from rising material costs, labour shortages, and mandatory sustainability compliance. |

|

Asset Owners / Investors |

digital platforms modernising property search and transactions through AI-driven price intelligence, virtual tours, and end-to-end digital deal management. |

|

Brokerage & Advisory |

CBRE, JLL, Savills, Knight Frank, Colliers, Cushman & Wakefield |

|

Listing & PropTech Platforms |

Rightmove, Scout24, SeLoger, Idealista, Habyt, IMMO Capital |

|

End Occupiers |

Ultimate demand drivers — households, corporates, retailers, and logistics operators — whose evolving space needs shape demand across all property segments. |

Global advisory firms occupy the highest-value position, combining brokerage with capital markets, valuation, and asset management across cross-border portfolios. Their dominance is challenged by PropTech platforms industrialising mid-market and residential transactions.

Technology Landscape in the Europe Real Estate Industry

Digital Listing and Marketplace Platforms

Europe's listing platforms have consolidated: Rightmove in the UK (60%+ share), Scout24 in Germany, Idealista in Iberia, and SeLoger in France. The segment combined for EUR 2.2 Billion in revenue in 2024, with AI search, virtual tours, and mortgage pre-qualification as core features.

AI-Driven Automated Valuation Models

AVMs covering European residential stock achieve mean absolute errors below 6% in dense urban markets. PriceHubble, Houseful, and CoreLogic Europe are embedding these into lender workflows, cutting underwriting from 7 days to under 24 hours.

Smart Building and IoT Infrastructure

Connected-building platforms from Siemens, Schneider Electric, and Johnson Controls are deployed in over 40% of new prime office completions in 2024. Real-time energy, occupancy, and air-quality analytics are standard in BREEAM Outstanding certifications.

Digital Conveyancing and Tokenisation

Distributed-ledger registries in Liechtenstein, Sweden, and the UK have pilot-tested tokenisation. Over EUR 500 million of European property was fractionalised on-chain in 2024 via Bricklane, BrickMark, and RealT.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Property | Residential | 45.8% | 2025 |

| Business | Sales | 56.8% | 2025 |

| Mode | Offline | 64.5% | 2025 |

| Country | Germany | 32.0% | 2025 |

By Business

Sales commands 56.8% in 2025, reflecting Europe's homeownership culture in Southern and Eastern Europe, institutional deal flow in multifamily and logistics, and pent-up demand unlocked by stabilising rates. Ownership rates above 75% in Romania, Hungary, and Slovakia contribute to volume, while Germany's 49% rate is offset by large-ticket institutional deals.

To access detailed market analysis, Request Sample

Rental at 43.2% is the fastest-growing mode, supported by affordability pressures, migration inflows, and institutional BTR. Institutional rental is under-penetrated at below 5% versus 15% in the US. UK BTR deliveries surpassed 25,000 units in 2024, per the BPF.

By Mode

Offline dominates at 64.5% in 2025, benefitting from advisory-intensive transactions, entrenched notary systems in France, Germany, and Italy, and in-person due diligence in deals above EUR 10 million. CBRE, JLL, and Savills control the large-ticket commercial segment.

Online at 35.5% in 2025 is the fastest-growing segment at ~7.8% CAGR through 2034, powered by Rightmove, Scout24, and Idealista, digital mortgage tools, and iBuyers. The UK Land Registry processes over 35% of England and Wales transactions digitally. Online share is expected to exceed 45% by 2034.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

32.0% |

Largest housing stock, deep institutional capital, safe-haven status, logistics hub |

|

United Kingdom |

18.4% |

London premium offices, BTR leadership, PropTech adoption, REIT ecosystem |

|

France |

16.7% |

Paris core offices, Grand Paris project, logistics corridor, SCPI investor market |

|

Italy |

11.2% |

Tourism-linked residential, Milan office recovery, retail repositioning |

|

Spain |

9.3% |

Madrid/Barcelona growth, Iberian logistics, BTR emergence, tourism demand |

|

Others |

12.4% |

Benelux logistics, Nordic living sector, CEE yield compression |

Germany commands 32.0% in 2025, the most dominant single-country position. The German residential sector, with 43+ million dwellings and leaders Vonovia and LEG Immobilien, anchors weight. Bundesbank data showed German prices rebounded 1.2% in 2024 after the 2022-2023 correction. Frankfurt, Munich, and Hamburg absorbed over EUR 11 billion of logistics investment in 2024.

The UK, at 18.4% in 2025, is anchored by London's global financial-centre office market, the most institutionalised BTR pipeline, and the deepest European REIT ecosystem led by Segro, Landsec, and British Land.

France at 16.7% in 2025 is powered by Paris as Continental Europe's largest office market, the Grand Paris Express infrastructure cycle, and a mature SCPI ecosystem channeling over EUR 7 billion annually into commercial property. Unibail-Rodamco-Westfield and Klépierre anchor retail real estate.

Italy at 11.2% and Spain at 9.3% represent Southern Europe's recovery. Milan's prime office yields are compressed to 4.0% by mid-2025 per Cushman & Wakefield. Spain's Madrid and Barcelona logistics delivered double-digit rental growth in 2024. Others at 12.4% captures the Netherlands, Benelux, Nordics, Poland, and CEE.

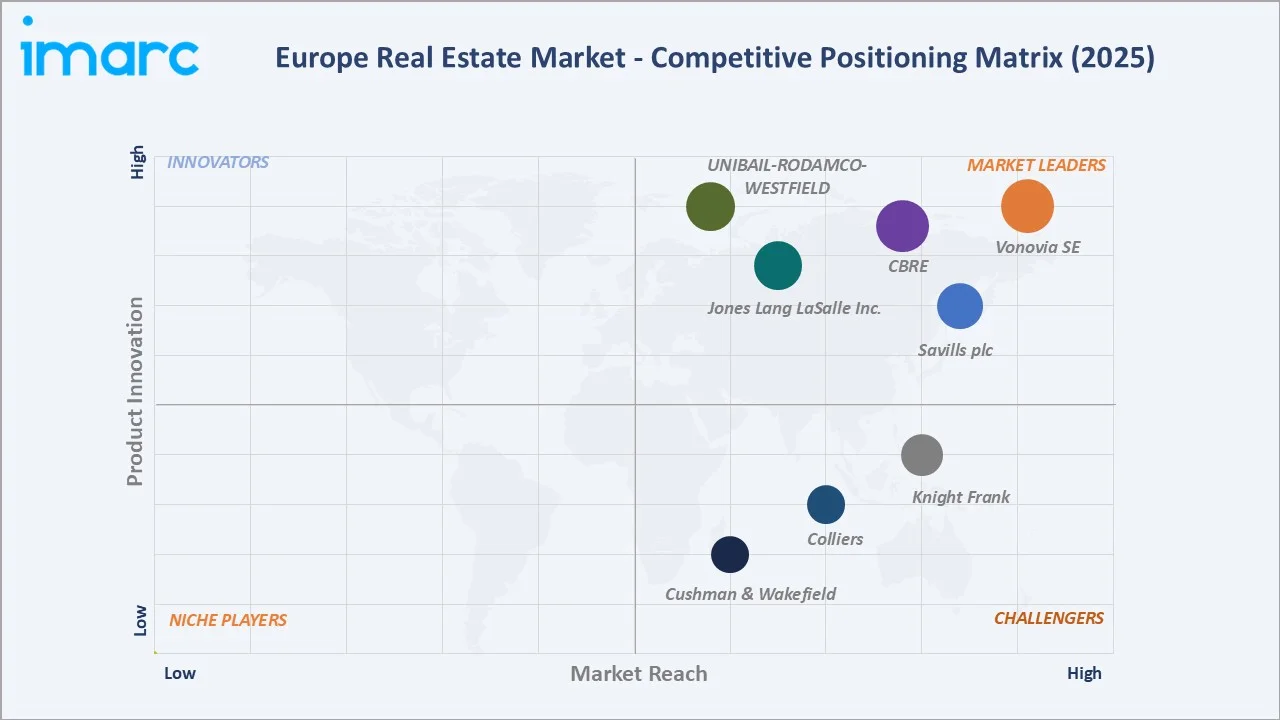

Competitive Landscape

|

Company Name |

Brand / Platform |

Market Position |

Core Strength |

|

Vonovia SE |

Vonovia |

Leader |

Germany's largest residential landlord, 548,000+ units |

|

CBRE |

CBRE |

Leader |

Global advisory scale, capital markets, valuation |

|

Jones Lang LaSalle IP, Inc. |

JLL |

Leader |

Integrated brokerage, PropTech stack, capital flows |

|

Savills plc |

Savills |

Leader |

UK premium, cross-border residential and commercial |

|

UNIBAIL-RODAMCO-WESTFIELD |

Unibail-Rodamco-Westfield |

Leader |

Prime European shopping centres, retail real estate |

|

Knight Frank |

Knight Frank |

Challenger |

Prime residential, wealth-oriented advisory |

|

Colliers |

Colliers |

Challenger |

Mid-market advisory, investment management |

|

Cushman & Wakefield |

Cushman & Wakefield |

Challenger |

Advisory, capital markets, corporate services |

The Europe real estate competitive landscape combines global advisory giants, listed REITs in Germany and the UK, pan-European asset managers, and national residential champions. The top-five advisory firms account for over 55% of pan-European brokerage fees in 2024, and the listed REIT universe represents roughly EUR 200 Billion of market cap.

Key Company Profiles

Vonovia SE

Vonovia SE is Europe's largest residential real estate company, headquartered in Bochum, Germany, with a portfolio of approximately 548,000 residential units across Germany, Austria, and Sweden as of 2024.

- Product & Platform Portfolio: Residential leasing, property management, energy retrofits, modular new construction, and tenant services across Central Europe.

- Recent Developments: In November 2025, Vonovia turned to Apollo on three occasions to date for bespoke equity financing solutions totaling approximately €3 billion.

- Strategic Focus: Vonovia's strategy centres on portfolio optimisation, ESG-led energy retrofits aligned with EU EPBD 2030 targets, and digital tenant-service platforms. The company targets operational excellence and disciplined capital deployment across its core German footprint.

CBRE

CBRE is the world's largest commercial real estate services firm, with a deep European franchise spanning advisory, capital markets, valuation, property management, and investment management across major EU markets and the UK.

- Product & Platform Portfolio: Transaction advisory, capital markets, valuation, property and facilities management, and CBRE Investment Management with over EUR 145 Billion AUM globally.

- Recent Developments: In May 2023, CBRE announced that its property management group has formed a global strategic partnership with Deepki that will bring Deepki Ready, one of the world’s most extensive landlord-focused real estate sustainability data-intelligence platforms, to the commercial properties CBRE manages for investors around the world.

- Strategic Focus: CBRE's European strategy prioritises integrated occupier and investor service delivery, expansion of recurring-revenue property management mandates, and vertical leadership in data centres, life sciences, and logistics advisory.

Savills plc

Savills is a London-headquartered global real estate services advisor with a deep European residential and commercial presence, operating in over 70 countries with pronounced strength in UK premium housing and Continental European capital markets.

- Product & Platform Portfolio: Residential and commercial agency, capital markets, consultancy, property management, and Savills Investment Management with over GBP 27 Billion AUM.

- Recent Developments: In January 2024, Savills expanded its EMEA data centre advisory team with the appointment of Rupert Duckworth, who joins as an associate director at the firm’s Margaret Street head office.

- Strategic Focus: Savills targets prime residential and commercial advisory leadership, expansion of recurring-revenue investment management, and vertical specialisation in living, logistics, and digital infrastructure sectors across Europe.

Market Concentration Analysis

The Europe real estate market is moderately fragmented at the asset-ownership level but more concentrated in advisory and listed residential. The top-five advisory firms - Vonovia SE, CBRE, Jones Lang LaSalle IP, Inc., Savills plc, and UNIBAIL-RODAMCO-WESTFIELD- collectively commanded ~55% of pan-European brokerage revenue in 2024.

Asset ownership is fragmented: the top 25 institutional investors hold ~12-14% of Europe's investable stock. In the German listed residential sub-segment, Vonovia and LEG Immobilien jointly control ~28% of the listed housing stock.

The market continues to consolidate. Blackstone, Brookfield, Apollo, and KKR deployed over EUR 30 Billion into European real estate platforms in 2024, focused on logistics, student accommodation, senior living, and data centres.

Investment & Growth Opportunities

Fastest-Growing Segments

Online is the highest-growth sub-segment at ~7.8% CAGR through 2034, driven by portal consolidation, AVM-backed underwriting, and e-conveyancing in the UK, Germany, and Nordics. Rental grows at ~5.9% CAGR, anchored by BTR deployment and affordability-driven tenure shift.

Emerging Market Expansion

Data-centre real estate is the highest-priority alternative class, with European colocation capacity expected to double from 10.8 GW in 2025 to over 22 GW by 2034 per CBRE. Student accommodation, senior living, and life sciences represent a EUR 40-60 Billion annual opportunity by 2030.

Venture & Private Investment Trends

European PropTech venture funding reached EUR 3.6 Billion in 2024, led by IMMO Capital, Habyt, and PriceHubble. Private equity dry powder for European deployment stood at EUR 120 Billion at end-2024 per Preqin. Green retrofit financing vehicles from AXA IM Alts and Patrizia attract EUR 5-7 Billion annually.

Future Market Outlook (2026-2034)

The Europe real estate market forecast projects steady expansion from USD 1.69 Billion in 2025 to USD 2.51 Billion by 2034 at a CAGR of 4.46%, a near-50% increase underpinned by residential modernisation, logistics and data-centre buildouts, and institutionalisation of the living sector.

Three structural shifts will reshape the industry through 2034. First, ESG-driven retrofit capex will create a EUR 275 Billion obligation under the EPBD recast. Second, the living sector is projected to rise from 22% to over 30% of annual transaction volume by 2030. Third, data-centre real estate grows from ~3% to over 8% of annual European CRE investment by 2034.

By 2034, the Europe real estate industry will have shifted toward digitally intermediated, ESG-aligned, and institutionally owned models. The competitive landscape will be shaped by global advisory platforms (CBRE, JLL), pan-European institutional asset managers (Blackstone, Brookfield, Patrizia), and digitally native residential platforms.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews in 2024-2025 with European real estate stakeholders, including heads of capital markets at Tier-1 firms, institutional investor MDs, REIT executives, PropTech founders, and officials at BPF (UK), ZIA (Germany), and FPI (France). Insights validated sizing, segmentation, and positioning.

Secondary Research

Secondary sources include Eurostat housing statistics, ECB Financial Stability Review, MSCI Real Capital Analytics, INREV surveys, Housing Europe, CBRE Research, JLL EMEA, Cushman & Wakefield Marketbeat, Savills European research, company annual reports, and press such as EuroProperty, React News, and PropertyEU.

Forecasting Models

Market size estimates and growth projections were derived using top-down and bottom-up forecasting, integrating GDP, household formation, ECB rate trajectories, and historical evolution patterns. Scenario analysis (base, optimistic, conservative) accounts for macroeconomic uncertainty through 2034.

Europe Real Estate Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Properties Covered | Residential, Commercial, Industrial, Land |

| Businesses Covered | Sales, Rental |

| Modes Covered | Online, Offline |

| Countries Covered | Germany, France, the United Kingdom, Italy, Spain, Others |

| Companies Covered | Vonovia SE, CBRE, Jones Lang LaSalle IP, Inc., Savills plc, UNIBAIL-RODAMCO-WESTFIELD, Knight Frank, Colliers, Cushman & Wakefield, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe real estate market from 2020-2034.

- The Europe real estate market research report provides the latest information on the market drivers, challenges, and opportunities in the regional market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within the region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe real estate industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the European Real Estate Market Report

The Europe real estate market was valued at USD 1.69 Billion in 2025, supported by sustained residential demand, logistics expansion, and stabilising policy rates across the Eurozone and the UK.

The market is projected to reach USD 2.51 Billion by 2034 at a CAGR of 4.46% during 2026-2034, driven by ESG retrofits, BTR scaling, and data-centre real estate buildouts.

Sales leads with a 56.8% share in 2025, reflecting Europe's homeownership culture, institutional multifamily transactions, and rebound in commercial capital markets after rate stabilisation.

Offline mode leads at 64.5% in 2025, driven by advisory-intensive transactions, entrenched notary systems across France, Germany, and Italy, and in-person due diligence in big-ticket deals.

Germany leads with a 32.0% share in 2025, underpinned by its residential stock of over 43 million dwellings, institutional capital depth, and safe-haven status for cross-border investors.

Key drivers include a 5-million-unit housing deficit, logistics and data-centre demand, interest-rate normalisation at 2.15% ECB level, and ESG-led EPBD retrofits creating multi-year capex cycles.

Online mode is the fastest-growing sub-segment at approximately 7.8% CAGR through 2034, powered by portal consolidation, AI-based valuations, and rising e-conveyancing adoption.

Leading companies include Vonovia SE, CBRE, Jones Lang LaSalle IP, Inc., Savills plc, UNIBAIL-RODAMCO-WESTFIELD, Knight Frank, Colliers, and Cushman & Wakefield.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)