Food Service Market Size, Share, Trends and Forecast by Sector, Systems, Types Of Restaurants, and Region, 2026-2034

Global Food Service Market Size, Share, Trends & Forecast (2026-2034)

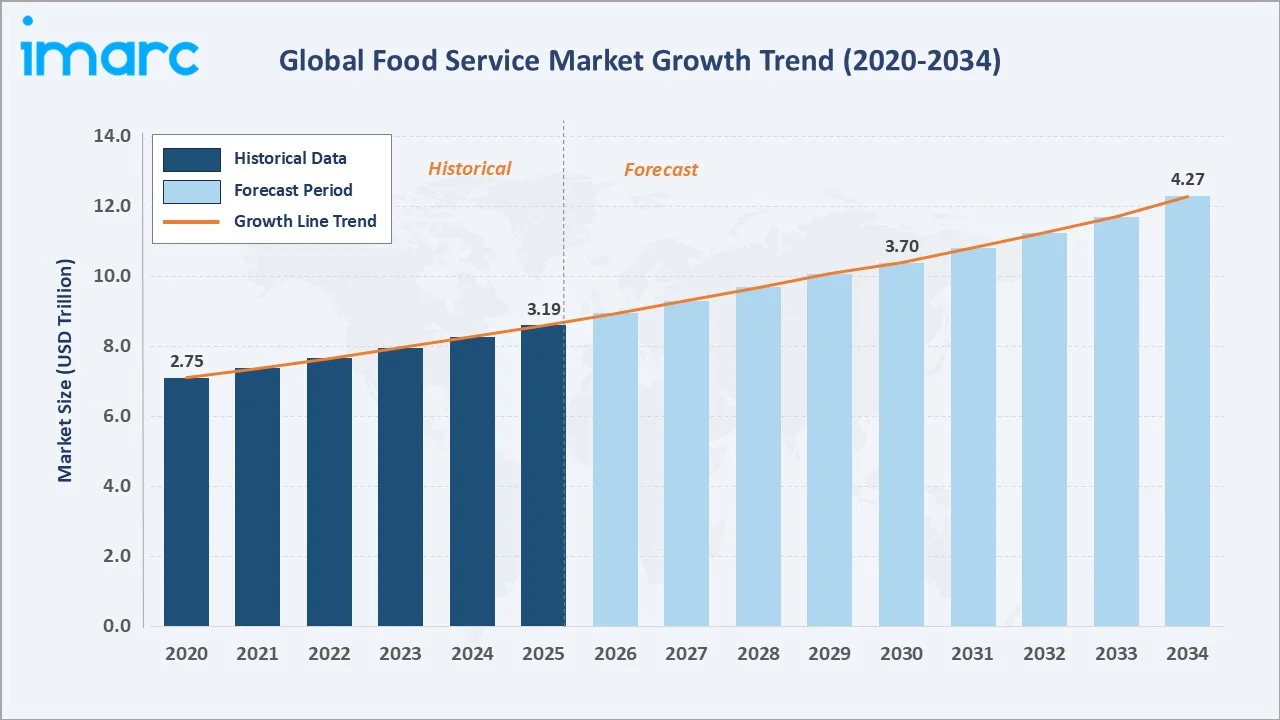

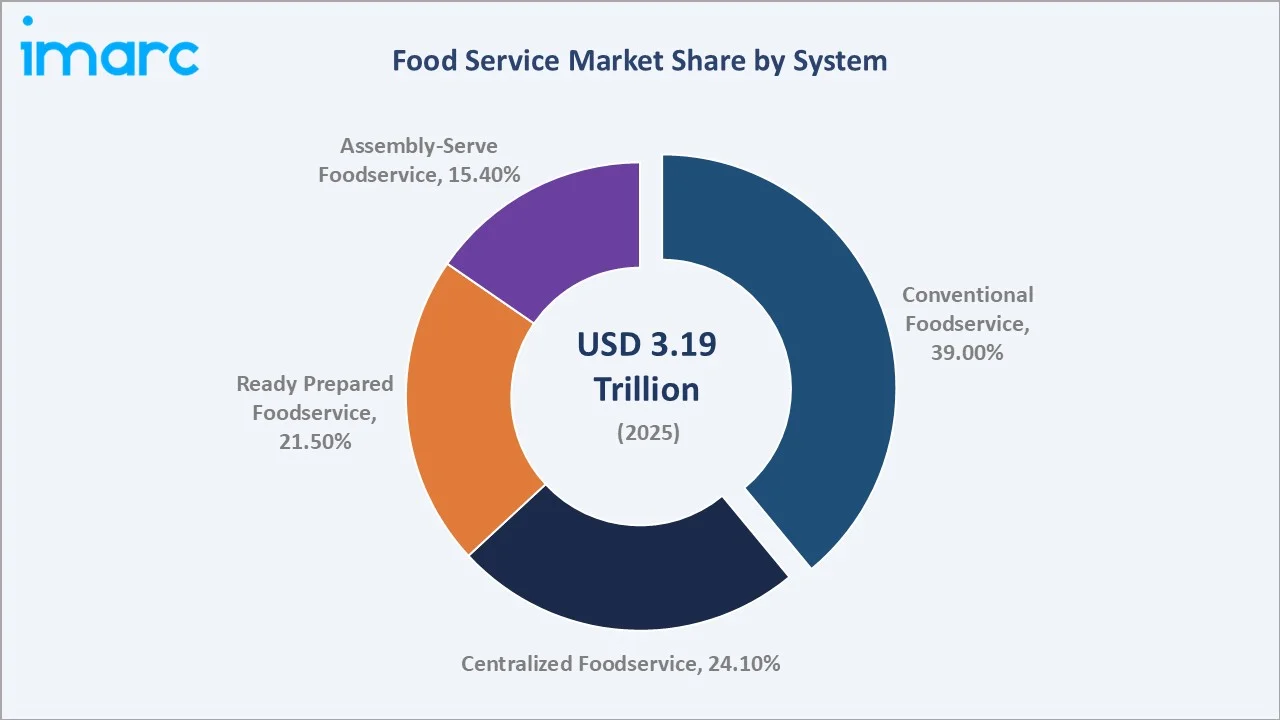

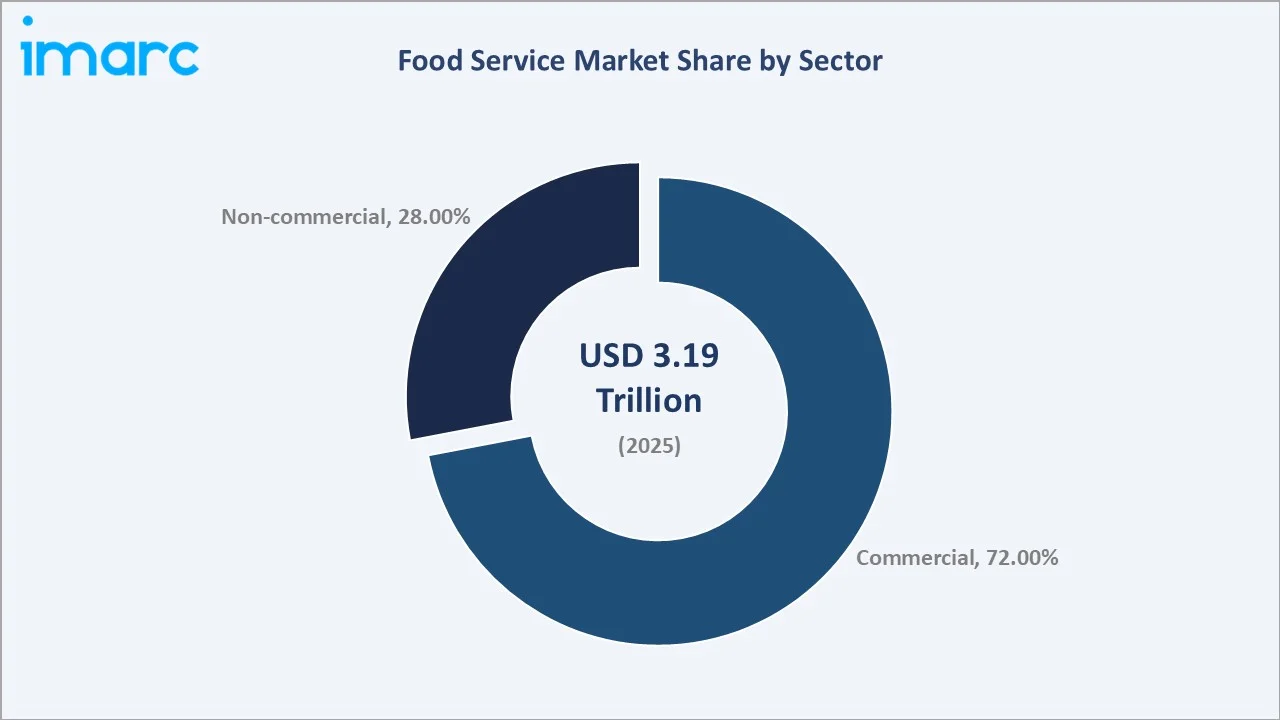

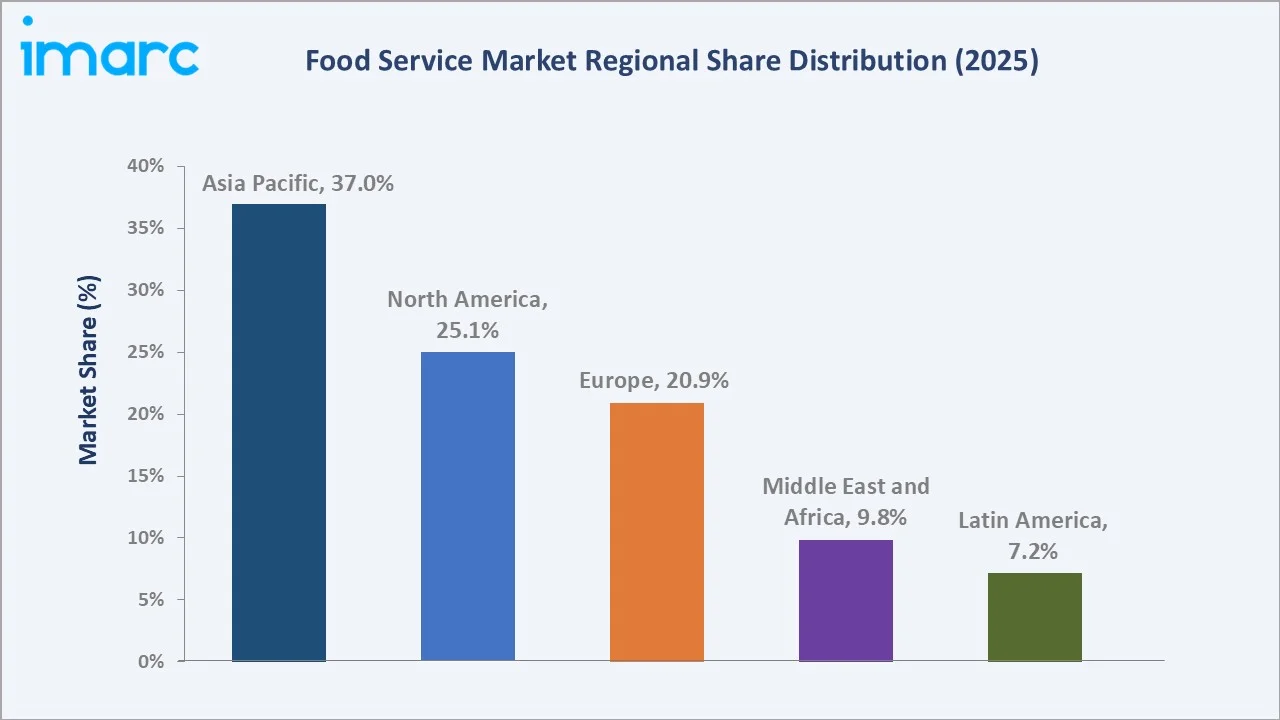

The global food service market reached a value of USD 3.19 Trillion in 2025 and is projected to reach USD 4.27 Trillion by 2034, exhibiting a CAGR of 3.02% during the forecast period (2026-2034). Market expansion is driven by accelerating urbanization, rising disposable incomes across emerging economies, and a structural shift toward digital ordering and off-premises dining. Asia Pacific dominates with a 37.0% revenue share in 2025, underpinned by rapid urbanization in China, India, and Southeast Asia. The commercial sector leads at 72.0% (2025), and the conventional foodservice system holds the largest operational model share at 39.0%. Key players include McDonald's, Starbucks, Yum! Brands, Domino's Pizza, and Restaurant Brands International.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.19 Trillion |

|

Forecast Market Size (2034) |

USD 4.27 Trillion |

|

CAGR (2026-2034) |

3.02% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (37.0%, 2025) |

|

Fastest Growing Region |

Asia Pacific |

The incremental revenue addition of approximately USD 1.08 Trillion over the forecast decade underlines the sustained structural opportunity across all food service formats and geographies.

To get more information on this market, Request Sample

The divergence between the historical period (2020–2025) and the forecast trajectory highlights the post-pandemic recovery acceleration. From a constrained base of USD 2.75 Trillion in 2020, the market returned to growth driven by digital infrastructure investment, emerging-market QSR expansion, and the normalization of delivery-first consumer behavior.

Executive Summary

The global food service market stood at USD 3.19 Trillion in 2025, supported by the convergence of demographic momentum, digital transformation, and evolving consumer lifestyles. The market is forecast to reach USD 4.27 Trillion by 2034 at a CAGR of 3.02%, reflecting steady long-term demand across quick-service restaurants, full-service establishments, institutional dining, and delivery-centric formats. Rising urbanization rates, particularly in Asia Pacific, which commands a 37.0% share, and the proliferation of digital ordering platforms are primary catalysts reshaping market structure.

Key growth drivers include an expanding middle-class consumer base in developing nations, a behavioral shift toward convenience-driven and off-premises dining, and broad-based technology adoption across restaurant operations. The commercial sector dominates at 72.0% of total revenues in 2025. Among operational systems, the conventional foodservice system leads with 38.6%, followed by centralized (24.1%), ready-prepared (21.5%), and assembly-serve (15.4%) formats.

North America (25.1%), Europe (20.9%), the Middle East and Africa (9.8%), and Latin America (7.2%) complete the global regional picture. Investment in digital infrastructure, sustainability-oriented menu innovation, and ghost kitchen proliferation are the critical strategic themes shaping competitive positioning through 2034.

Key Market Insights

|

Insight |

Data |

|

Market Size (2025) |

USD 3.19 Trillion |

|

Market Forecast (2034) |

USD 4.27 Trillion |

|

CAGR (2026-2034) |

3.02% |

|

Largest System Segment |

Conventional Foodservice System- 39.0% (2025) |

|

Largest Sector Segment |

Commercial - 72.0% (2025) |

|

Leading Region |

Asia Pacific – 37.0% (2025) |

|

Second-Largest Region |

North America – 25.1% (2025) |

|

Fastest Growing Segment |

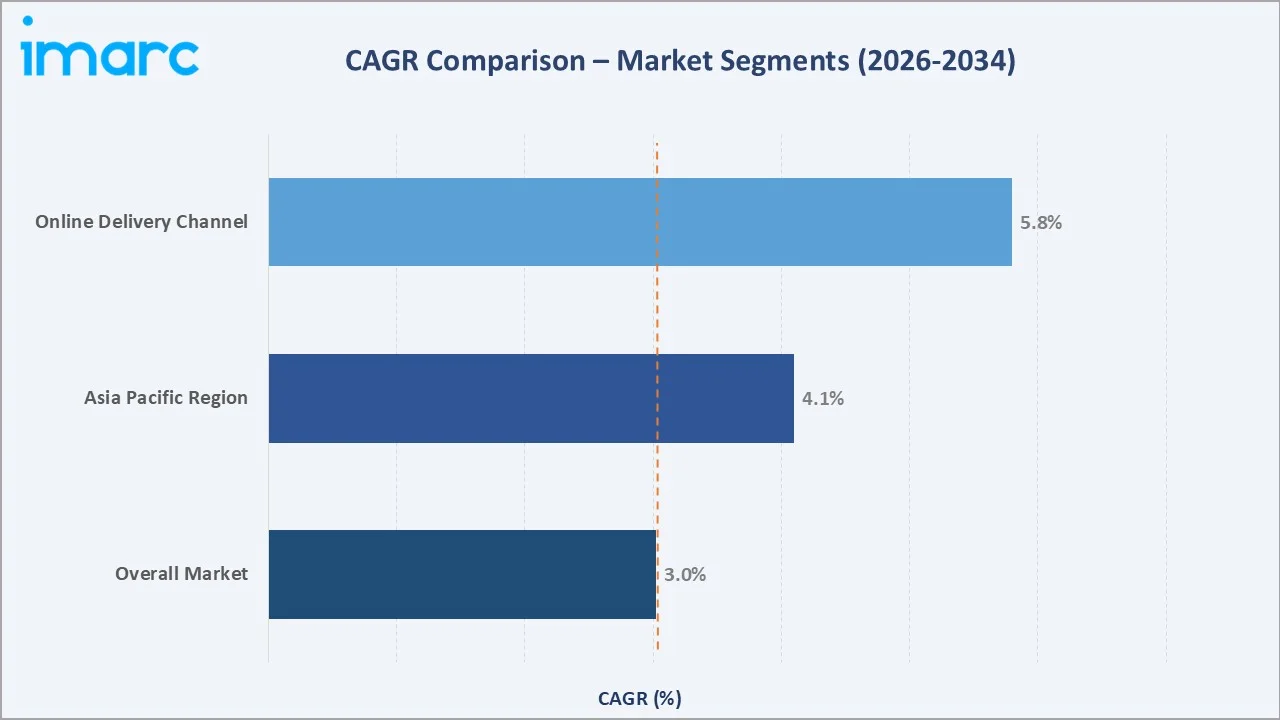

Online Delivery & Assembly-Serve Formats |

|

Top Companies |

McDonald's, Starbucks, Yum! Brands, Domino's, RBI |

|

Key Market Opportunity |

Online delivery channel – projected USD 1.2 Trillion+ by 2034 |

Key Analytical Observations Supporting the Above Data Points:

- The commercial sector's 72.0% share (2025) underscores the dominance of QSR, casual dining, and café formats globally, with consumers prioritizing convenience, speed, and dining variety.

- Conventional foodservice systems lead with 39.0% of system-based revenues (2025), reflecting the continued prominence of on-site meal preparation in hotels, schools, healthcare facilities, and restaurant chains.

- Asia Pacific's 37.0% share (2025) is driven by rapid urbanization in China, India, and Southeast Asia, a youthful consumer demographic, and the exponential adoption of food delivery aggregators.

- North America, holding 25.1% (2025), benefits from deeply embedded QSR culture, strong franchising infrastructure, and leading-edge digital ordering adoption, with off-premises traffic accounting for nearly 75% of U.S. restaurant transactions.

- Plant-based and sustainable menu innovation is emerging as a critical revenue lever, with operators including Starbucks and McDonald's expanding allergen-friendly and dairy-alternative offerings to serve health-conscious consumers.

Global Food Service Market Overview

The food service industry encompasses all businesses and institutions engaged in preparing meals, snacks, and beverages for consumption outside the home, spanning QSRs, full-service restaurants, institutional catering, street food vendors, cloud kitchens, and food delivery aggregators. As of 2025, the market is valued at USD 3.19 Trillion and constitutes one of the world's largest employer sectors. The ecosystem integrates raw material suppliers, food processors, packaging providers, technology platforms, logistics networks, and end consumers into a complex, high-velocity value chain. Macroeconomic tailwinds including urbanization, income growth, and demographic expansion are sustaining structural demand, positioning the food service market for USD 1.08 Trillion in incremental value through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

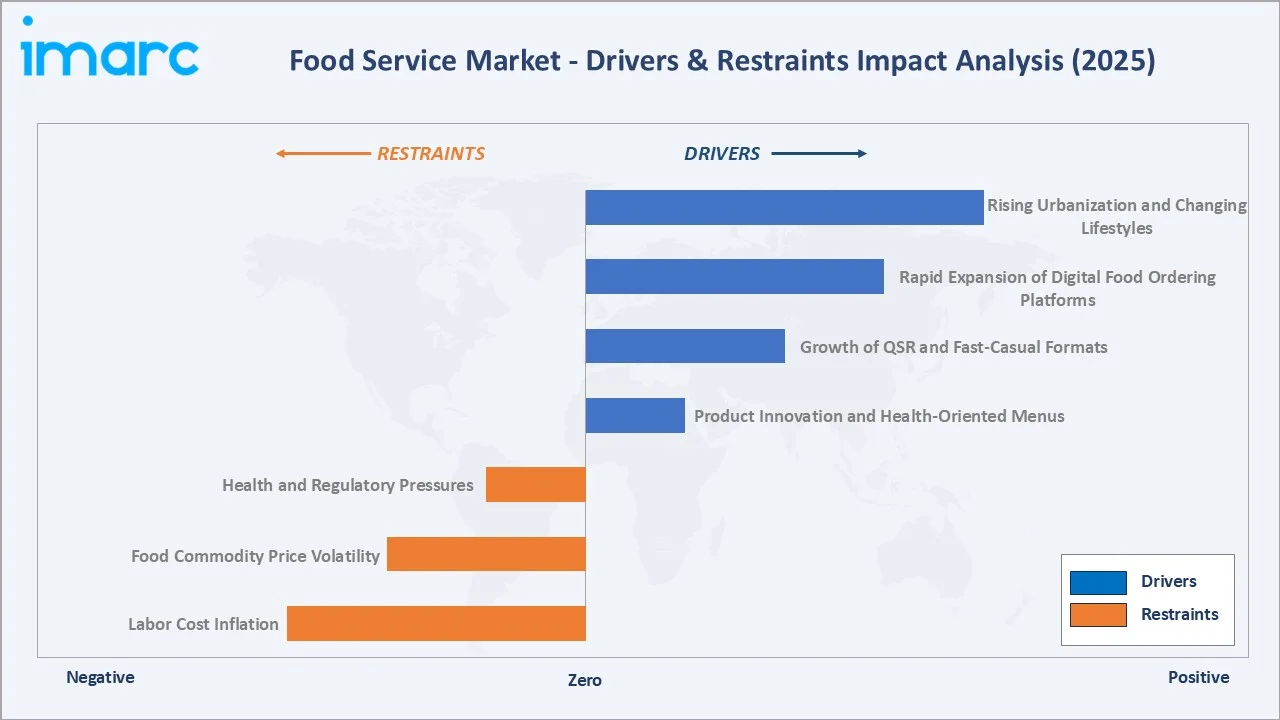

Market Drivers

- Rising Urbanization and Changing Lifestyles: Over 55% of the global population resides in urban areas, projected to reach 68% by 2050. Urbanization concentrates demand for external food services, reducing home-cooking frequency and increasing dining-out occasions across income brackets.

- Rapid Expansion of Digital Food Ordering Platforms: Digital ordering channels, including mobile apps, self-service kiosks, and third-party aggregators, are transforming consumer engagement. In 2024, Amazon integrated Grubhub food delivery directly into its platform for U.S. consumers, reflecting accelerating platform consolidation.

- Growth of QSR and Fast-Casual Formats: Global fast food and QSR industry revenues exceeded USD 276.2 billion in 2025. Pizza chains, burger formats, and coffee QSRs represent a substantial share of total commercial foodservice revenues, with franchise expansion into Asia Pacific and MEA accelerating.

- Product Innovation and Health-Oriented Menus: Starbucks eliminated extra charges for plant-based milk alternatives across North America in November 2024, reflecting the commercial mainstreaming of sustainable menu options and health-led consumer demand.

Market Restraints

- Labor Cost Inflation: Persistent labor shortages and minimum wage increases across North America and Europe are compressing restaurant operating margins. Food service businesses experienced significantly higher staff turnover rates post-2020.

- Food Commodity Price Volatility: Fluctuations in key raw material costs, including proteins, grains, and packaging, directly impact menu pricing strategies and profitability, particularly for small and mid-size operators with limited hedging capability.

- Health and Regulatory Pressures: Evolving nutritional labeling requirements and calorie disclosure mandates in the EU and North America are increasing reformulation and compliance costs, adding operational complexity for QSR and fast-casual chains.

Market Opportunities

- Ghost Kitchen and Cloud Kitchen Expansion: Ghost kitchens in the US numbered over 1,500 units in 2023. These asset-light models reduce overhead by 40-50% versus traditional dine-in formats, enabling scalable brand expansion in dense urban markets.

- Emerging Market Penetration: Asia Pacific, Middle East and Africa, and Latin America collectively represent an incremental addressable market, driven by rising middle-class populations and increasing smartphone penetration.

- Technology-Driven Personalization: AI-powered recommendation engines and loyalty programs are generating measurable revenue uplifts. Domino's processed over 70% of U.S. orders digitally in 2024, with AI personalization boosting average order values by rising significantly and customer satisfaction rising by 15%.

Market Challenges

- Cold Chain and Logistics Complexity: Rising cold chain logistics costs, went up significantly between 2021 and 2024, are impacting margin structures for operators dependent on centralized commissaries and ready-prepared formats.

- Intensifying Market Competition: Saturation of QSR delivery markets in North America and Western Europe, combined with low-overhead digital-native concepts, is intensifying pricing pressure on established restaurant groups.

- Consumer Retention and Loyalty: Shifting consumer preferences and app-based platform switching are making long-term customer retention increasingly difficult and expensive, requiring sustained investment in loyalty ecosystems.

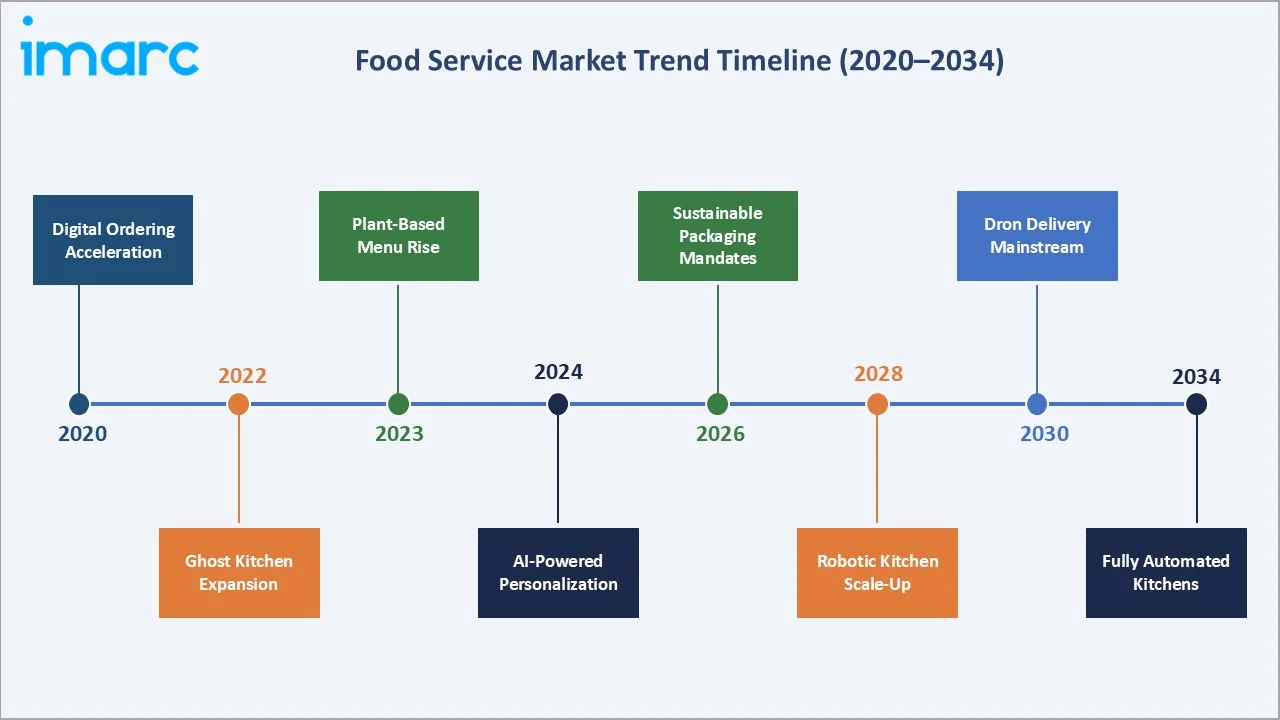

Emerging Market Trends

The global food service market is undergoing rapid structural transformation, shaped by five converging trends that are redefining competitive dynamics across all formats and regions.

1. Digital Integration and AI-Powered Operations

Point-of-sale systems, AI-driven inventory management, kitchen display technology, and contactless payment platforms are becoming standard. Starbucks' partnership with Bank of America in February 2024, enabling 45 million cardholders to link accounts and earn loyalty rewards, illustrates how integrated digital ecosystems are driving customer engagement and repeat visit frequency.

2. Plant-Based and Sustainable Menu Transformation

Health, environmental sustainability, and animal welfare awareness are driving significant menu reformulation. The global plant-based food market is forecast to reach USD 32.2 Billion by 2034, creating substantial crossover opportunity for food service operators expanding plant-forward menus at scale.

3. Off-Premise and Delivery-Centric Format Growth

Nearly 75% of all U.S. restaurant traffic now occurs off-premises (National Restaurant Association, 2024). This behavioral shift has catalysed cloud kitchen proliferation and third-party platform expansion, fundamentally reshaping the food service cost and revenue model globally.

4. Franchise Expansion into Emerging Markets

Leading QSR operators are aggressively expanding franchise networks across Asia Pacific, MEA, and Latin America. Asia Pacific's is the fastest among all regions, reflects the structural demand momentum in these expansion markets through 2034.

5. Sustainable Packaging and ESG-Aligned Operations

Major operators are committing to 100% recyclable or compostable packaging targets by 2030. ESG-aligned investors and consumer advocacy groups are accelerating this transition, reshaping procurement, supply chain, and branding strategies across the global industry.

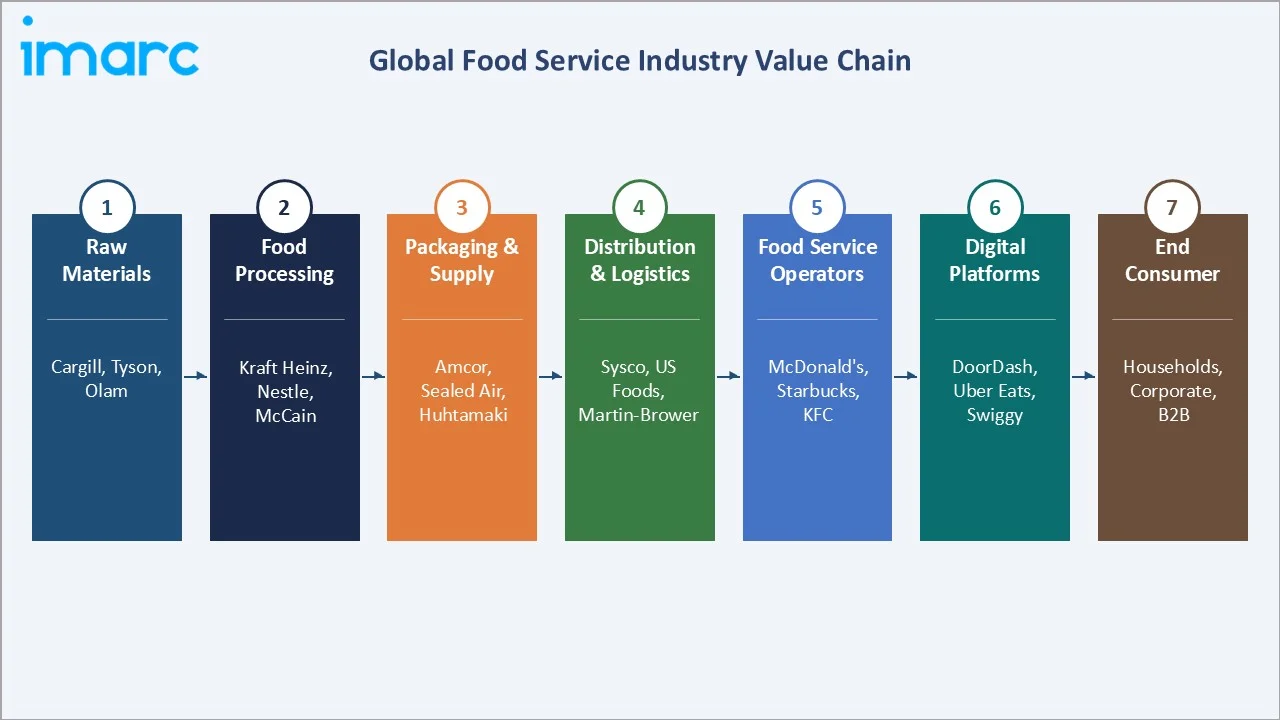

Industry Value Chain Analysis

The food service industry value chain spans six interconnected stages. Each stage is populated by specialized operators whose efficiency directly influences product quality, cost competitiveness, and market responsiveness.

|

Stage |

Key Activities |

Representative Players |

|

Raw Material Procurement |

Agricultural sourcing, livestock supply, beverage inputs |

Cargill, Tyson Foods, Olam International |

|

Food Processing |

Ingredient processing, sauce production, frozen meal manufacturing |

Kraft Heinz, Conagra Brands, Nestlé, McCain |

|

Packaging & Supply |

Food-grade containers, compostable packaging, cold chain materials |

Sealed Air, Amcor, Huhtamaki, Berry Global |

|

Distribution & Logistics |

Cold chain logistics, last-mile delivery, warehouse management |

Sysco, US Foods, Martin-Brower, DHL |

|

Food Service Operators |

Meal preparation, service, delivery-only formats |

McDonald's, Starbucks, Domino's, Chipotle |

|

End Consumers |

Dine-in, delivery, takeout, institutional (B2B) consumption |

Households, corporates, schools, hospitals |

The distribution and logistics stage is increasingly critical as off-premises volumes grow. Cold chain infrastructure investment is rising at approximately 8-10% annually in different regions, reflecting the growing share of delivered and ready-to-consume food service formats. Technology platforms, including demand forecasting AI and automated kitchen systems, are creating efficiency gains across the operator stage.

Technology Landscape in the Food Service Industry

Digital Ordering and POS Systems

Cloud-based point-of-sale platforms, mobile ordering applications, and self-service kiosks are now standard across QSR and fast-casual formats. Third-party aggregators including DoorDash, Uber Eats, and Deliveroo collectively are growing rapidly in this space. Multiple acquisitions took place in this space in 2025 leading to Just Eat being sold to Prosus, Deliveroo sold to DoorDash, and Grubhub being sold at a 90% discount on its 2021 value to Wonder Foods.

AI and Data Analytics

AI-driven demand forecasting, menu engineering analytics, and customer behavior modelling enable operators to reduce food waste, optimize labor scheduling, and personalize promotions. Predictive analytics adoption among top-tier restaurant operators grew by over 30% between 2022 and 2024.

Kitchen Automation and Robotics

Robotic food preparation systems are moving from pilot programs to commercial deployment. Picnic, the food automation startup behind the pizza-making robot, has raised $5 million in funding and gained the support of Unlock Venture Partners, reflecting growing investor appetite for kitchen automation within food service.

Sustainable and Smart Packaging

Active packaging technologies using biodegradable materials, moisture control, and temperature-indicator labels are gaining commercial traction. At least 65% of all packaging waste must be recycled by weight by the end of 2025, and at least 70% of all packaging trash must be recycled by the end of 2030.

Market Segmentation Analysis

By System

To access detailed market analysis, Request Sample

The food service market is segmented into four operational systems, each with distinct revenue contribution and growth characteristics as of 2025, the conventional system's 39.0% share reflects its enduring applicability across restaurant, hotel, and institutional formats. The assembly-serve system is gaining momentum as operators seek capital-efficient models that scale rapidly across delivery-first markets.

By Sector

The commercial sector dominates with a 72.0% revenue share in 2025, encompassing QSRs, full-service restaurants, cafes, bars, hotels, and event catering. Non-commercial foodservice, at 28.0%, includes institutional settings such as healthcare, education, military, and corporate dining. Non-commercial catering is experiencing growing outsourcing to specialist contract catering firms. Major operators such as Compass Group and Sodexo are expanding their institutional footprint, particularly in healthcare and education.

Regional Market Insights

The global food service market exhibits meaningful regional differentiation in growth drivers, competitive dynamics, and consumer behavior. Asia Pacific leads in revenue share, while North America and Europe anchor mature but innovation-driven markets. Asia Pacific’s 37.0% share (2025) is underpinned by China's huge foodservice ecosystem, India's rapidly expanding QSR sector growing at approximately 10-12% annually, and Southeast Asia's booming digital delivery market. North America’s 25.1% reflects a market where digital transformation and off-premises consumption are structural norms rather than emerging trends.

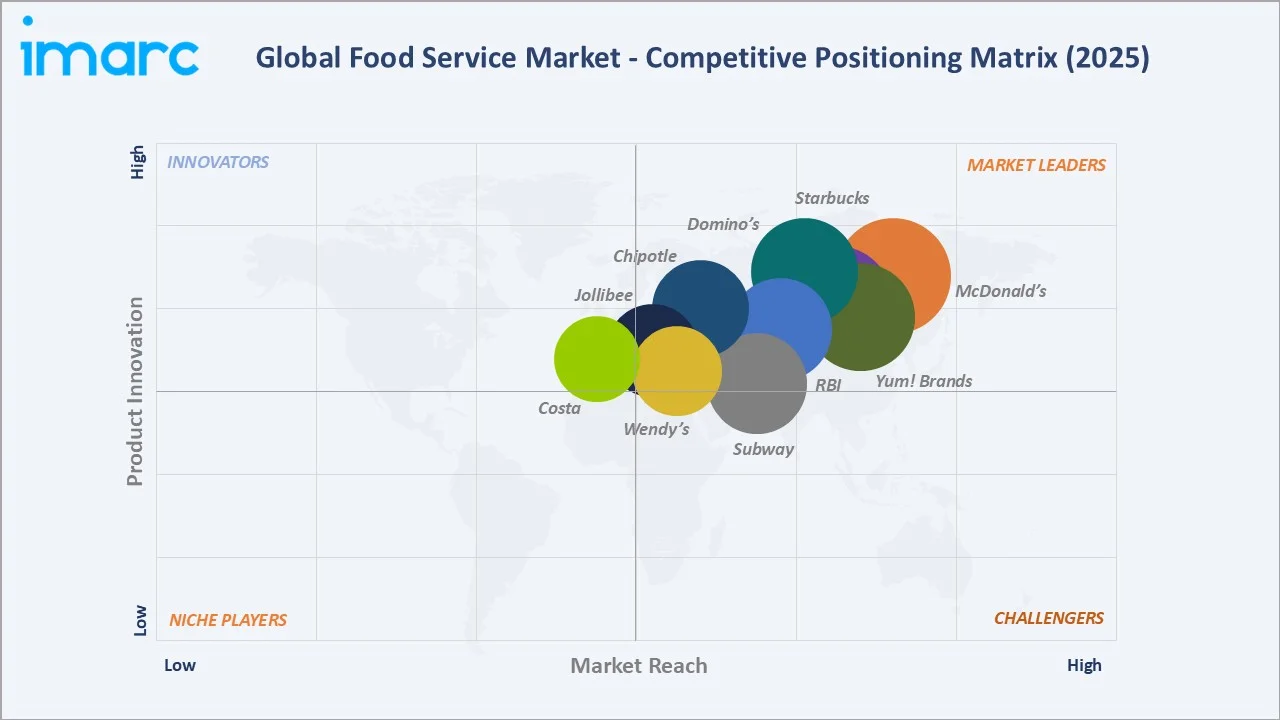

Competitive Landscape

The global food service competitive landscape is characterized by a small group of dominant multinationals QSR and food service corporations, a mid-tier of regional chains, and a highly fragmented long tail of independent operators. The top five operators collectively account for approximately 18–20% of global food service revenues in 2025.

|

Company Name |

Key Brand(s) |

Market Position |

Primary Strategy |

|

McDonald's Corporation |

McDonald's |

Market Leader – QSR Global |

Digital ordering, loyalty programs, menu innovation |

|

Starbucks Corporation |

Starbucks |

Leader – Coffee/Café |

Digital loyalty ecosystem, plant-based menus |

|

Yum! Brands Inc. |

KFC, Pizza Hut, Taco Bell |

Leader – Multi-brand QSR |

Emerging market franchising, digital ordering |

|

Restaurant Brands International |

Burger King, Tim Hortons, Popeyes |

Leader – Multi-brand QSR |

Refranchising, international expansion |

|

Domino's Pizza Inc. |

Domino's |

Leader – Pizza Delivery |

AI-powered delivery, digital-first ordering |

|

Chipotle Mexican Grill |

Chipotle |

Challenger – Fast Casual |

Digital ordering, Chipotlane expansion |

|

Jollibee Foods Corporation |

Jollibee, Smashburger |

Challenger – Asia-Pacific |

Global M&A, culturally adapted menus |

|

Subway IP LLC |

Subway |

Established – QSR Global |

Franchise restructuring, menu refresh |

|

Costa Limited |

Costa Coffee |

Challenger – Coffee QSR |

UK/Europe/Asia expansion, loyalty app |

|

Wendy's International LLC |

Wendy's |

Established – QSR |

Breakfast expansion, digital loyalty |

Competitive differentiation is increasingly driven by digital platform investment, loyalty program depth, and speed of emerging-market franchise expansion. Operators that combine robust digital ordering infrastructure with health and sustainability-aligned menu innovation are demonstrating the strongest revenue growth profiles.

Key Company Profiles

McDonald's Corporation

McDonald's is the world's largest QSR operator by system sales, with over 44,000 locations across 100+ countries as of 2025. The company generated global system-wide sales exceeding USD 100 Billion in 2023.

- Product Portfolio: Big Mac, McFlurry, McCafé beverages, plant-based McPlant options, breakfast items, and regional menu adaptations.

- Recent Developments: Introduced CosMc's beverage concept in 2023; continued AI-powered drive-thru ordering trials; deepened delivery platform collaboration across Asia Pacific and Europe.

- Strategic Focus: Digital-first ordering ecosystem (MyMcDonald's Rewards), international franchise growth, and net-zero packaging sustainability commitments.

Starbucks Corporation

Starbucks operates over 41,000 stores globally and plans over 2,000 net new stores across the global company in fiscal 2026, maintaining leadership in the premium coffee and café segment globally.

- Product Portfolio: Handcrafted beverages, cold brew and ready-to-drink formats, food items, and Starbucks Reserve premium range.

- Recent Developments: Partnership with Bank of America (February 2024) to expand digital loyalty; elimination of plant-based milk surcharges in November 2024 across North America.

- Strategic Focus: Digital loyalty ecosystem deepening, plant-based and sustainable menu expansion, and international café format scaling.

Yum! Brands Inc.

Yum! Brands operates KFC, Pizza Hut, Taco Bell, and The Habit Burger Grill, collectively comprising over 55,000 restaurants across 155 countries as of 2025.

- Product Portfolio: Fried chicken (KFC), pan and delivery pizza (Pizza Hut), Mexican-inspired QSR (Taco Bell), and premium burger formats (The Habit).

- Recent Developments: Accelerated KFC franchise expansion in Africa and Southeast Asia in 2023–2024; Pizza Hut expanded plant-based menu options across European markets.

- Strategic Focus: Digital ordering investment, emerging market franchise penetration, menu diversification, and franchisee profitability improvement.

Domino's Pizza Inc.

Domino's is the world's largest pizza company by global retail sales, operating over 20,000 stores across 90+ countries as of 2024. Global retail sales reached approximately USD 18.6 Billion in 2023.

- Product Portfolio: Traditional, specialty, and artisan pizzas; pasta, sandwiches, sides, and beverages across dine-in, carryout, and delivery formats.

- Recent Developments: Partnership with Uber Eats launched in 2023; AI-powered delivery routing reduced average delivery times by 2.4 minutes per order.

- Strategic Focus: Technology-first ordering infrastructure, AI-driven operational efficiency, and international franchise expansion.

Jollibee Foods Corporation

Jollibee is Southeast Asia's largest food service company, with over 1,800 stores across 17 countries. The group operates Jollibee, Smashburger, Tim Ho Wan, and Highlands Coffee, among other brands.

- Product Portfolio: Fried chicken, burgers, pasta, and localized Asian menu adaptations through Jollibee; premium smash burgers via Smashburger.

- Recent Developments: Continued international expansion in North America and Europe; invested in digital ordering capabilities and loyalty programs across key markets in 2024.

- Strategic Focus: Global M&A-driven brand portfolio expansion, Asian-market food culture leverage, and franchise scaling.

Market Concentration Analysis

The global food service market is structurally fragmented, with the top five operators collectively holding approximately 18–20% of total global revenues in 2025. This moderate top-end concentration coexists with a highly fragmented base of over 15 million independent operators globally, particularly in Asia Pacific, Europe, and Latin America.

The QSR and fast-casual sub-segments exhibit higher concentration. McDonald's, Yum! Brands, and Restaurant Brands International are mammoth players in the market. The full-service and institutional catering segments remain significantly more fragmented. Contract catering consolidation continues, with Compass Group, Sodexo, and Aramark commanding significant institutional positions.

Consolidation activity has accelerated since 2020. The market is expected to see 10–15 significant M&A transactions annually through 2034, primarily targeting regional franchise groups and delivery-native food service brands. Private equity interest in multi-unit franchise roll-ups, particularly in Asia Pacific, MEA, and Latin America, remains elevated.

Investment & Growth Opportunities

Fastest Growing Segments

Online delivery and ghost kitchen formats (CAGR approximately 8–10%), plant-based food service menus (CAGR approximately 9%), and premium/artisan restaurant formats (CAGR approximately 5–6%) represent the highest-growth investment vectors through 2034.

Emerging Market Expansion

Asia Pacific and Latin America present the most compelling geographic investment opportunities. India's food service sector is expected to grow at over 13% CAGR through 2034. Brazil represents an incremental opportunity in the region of Latin America. Entry via franchise partnerships, joint ventures, and digital delivery platform investments are the preferred strategies.

Technology and Venture Investment Trends

- Venture capital investment in food-tech and delivery infrastructure remained robust in 2023–2024, with key themes including AI-powered kitchen automation and digital loyalty ecosystems.

- Kitchen robotics companies including Picnic Works (USD 5 Million raised, 2024) are attracting significant institutional investment as labor cost pressures intensify.

- ESG-aligned investors are targeting sustainable packaging, ethical sourcing, and low-emission supply chain initiatives within the food service ecosystem.

- Digital ordering platform consolidation, exemplified by Amazon's 2024 integration of Grubhub, is creating large-scale aggregation opportunities, particularly in North America and Asia Pacific.

Future Market Outlook (2026-2034)

The global food service market is poised for sustained, broad-based growth through 2034, anchored by digital transformation, geographic expansion into high-growth emerging markets, and structural shifts in consumer dining behavior. From USD 3.19 Trillion in 2025, the market is forecast to reach USD 4.27 Trillion by 2034, representing absolute incremental value of approximately USD 1,082.2 Billion over the forecast decade.

Technological disruptions including AI-driven demand forecasting, robotic kitchen automation, drone delivery pilots, and blockchain-enabled supply chain traceability, are expected to reshape operational economics across the value chain by 2028–2030. Operators achieving 20–30% cost efficiency improvements through automation will secure decisive competitive advantages in high-volume delivery markets.

Health, sustainability, and personalization will transition from niche differentiators to baseline consumer requirements. Brands that embed these values into core product strategy will sustain and grow market share. Gen-Z consumers will be the primary arbiter of brand relevance across both commercial and digital food service formats.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys conducted with over 200 industry participants in 2024–2025, comprising food service chain executives, franchise operators, digital platform managers, procurement leaders, and end consumers across North America, Europe, Asia Pacific, and MEA.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, regulatory filings, trade publications (Nation's Restaurant News, Food Business News, QSR Magazine), industry databases (Euromonitor, Mintel, USDA Food Data), and publicly available financial data. Over 400 secondary sources were reviewed and cross-referenced.

Forecasting Models

Market size estimations and growth projections were derived using a combination of bottom-up and top-down forecasting models, incorporating GDP growth rates, urbanization indices, consumer expenditure data, digital ordering penetration rates, and historical market evolution patterns. Scenario analysis across base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty.

Food Service Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Trillion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Sectors Covered | Commercial, Non-Commercial |

| Systems Covered | Conventional Foodservice System, Centralized Foodservice System, Ready Prepared Foodservice System, Assembly-Serve Foodservice System |

| Types of Restaurants Covered | Fast Food Restaurants, Full-Service Restaurants, Limited Service Restaurants, Special Food Services Restaurants |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | McDonald's Corporation, Starbucks Corporation, Yum! Brands Inc., Restaurant Brands International, Domino's Pizza Inc., Chipotle Mexican Grill, Jollibee Foods Corporation, Subway IP LLC, Costa Limited, Wendy's International LLC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the food service market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global food service market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the food service industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Food Service Market Report

The global food service market was valued at USD 3.19 Trillion in 2025 and is projected to reach USD 4.27 Trillion by 2034, growing at a CAGR of 3.02%.

The market is forecast to grow at a CAGR of 3.02% during 2026-2034, driven by urbanization, digital ordering adoption, and emerging-market expansion.

Asia Pacific is the leading region with a 37.0% share in 2025. Rapid urbanization and strong digital food ordering adoption in China, India, and Southeast Asia are key contributors.

Asia Pacific is also the fastest-growing region, with a CAGR of approximately 4.1%, fueled by QSR chain expansion and rising middle-class populations.

Key drivers include rising urbanization, expanding digital food ordering platforms, QSR format proliferation, product premiumization, and the structural shift toward off-premises dining.

The conventional foodservice system is the largest at 39.0% in 2025, due to its broad applicability across restaurant, hotel, and institutional food service formats.

Key trends include digital AI-powered operations, plant-based menu transformation, off-premises dining dominance, ghost kitchen proliferation, and emerging-market franchise expansion.

Leading companies include McDonald's, Starbucks, Yum! Brands, Restaurant Brands International, Domino's Pizza, Chipotle, Jollibee, Subway, Costa Limited, and Wendy’s International.

The commercial sector accounts for 72.0% of global food service revenues in 2025, encompassing QSRs, cafes, hotels, casual dining, and event catering.

Digital technologies, including AI-driven POS, mobile ordering apps, and loyalty ecosystems, are transforming consumer engagement. Domino's processed over 70% of U.S. orders digitally in 2024.

High-growth opportunities exist in ghost kitchen infrastructure, plant-based formats, emerging market franchise expansion (India, Brazil, GCC), kitchen robotics, and AI-powered personalization platforms.

Key challenges include labor cost inflation, commodity price volatility, cold chain logistics complexity, intense digital delivery platform competition, and evolving nutritional regulations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)