India Machine Vision Market Size, Share, Trends and Forecast by Product, Component, Application, Industry, and Region, 2026-2034

India Machine Vision Market Size, Share, Trends & Forecast (2026-2034)

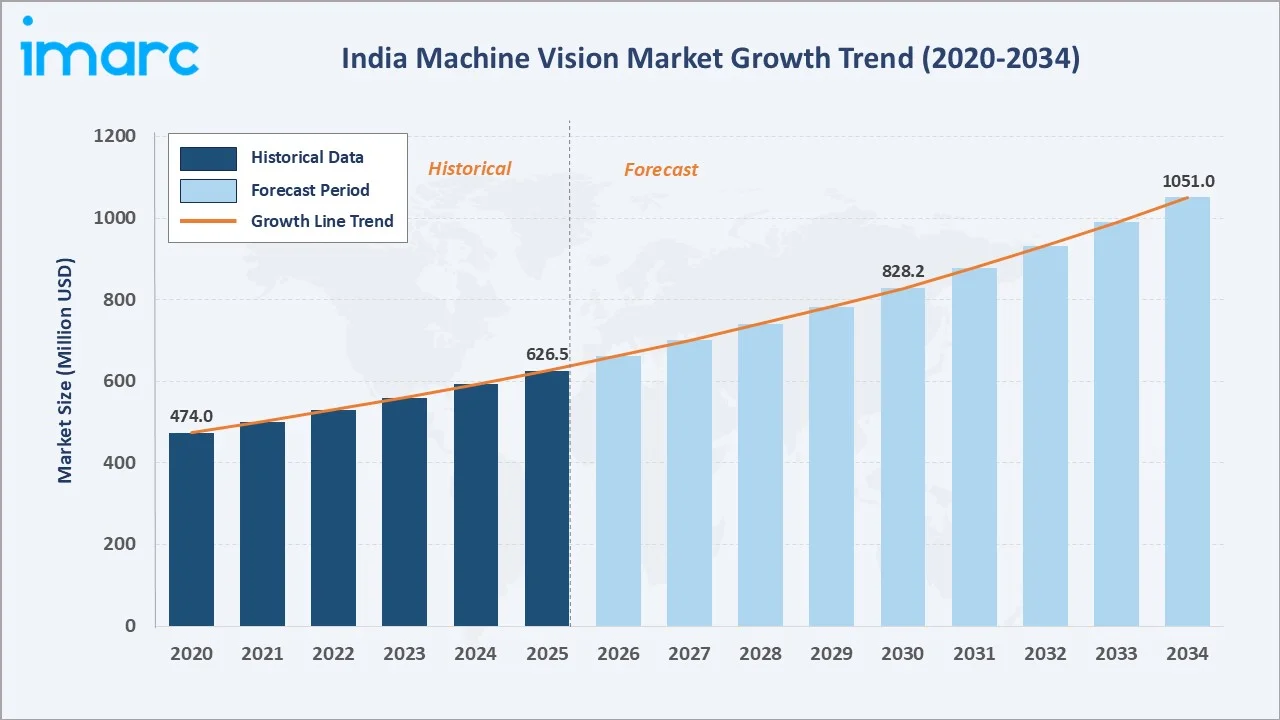

The India machine vision market was valued at USD 626.5 Million in 2025 and is projected to reach USD 1,051.0 Million by 2034, exhibiting a CAGR of 5.74% during 2026-2034. Rising automation across automotive, electronics, and pharmaceutical manufacturing is the primary force shaping this growth. India's electronics production reached INR 11.3 Lakh Crore during 2024-25, reinforcing demand for automated quality inspection and defect detection on high-volume production lines.

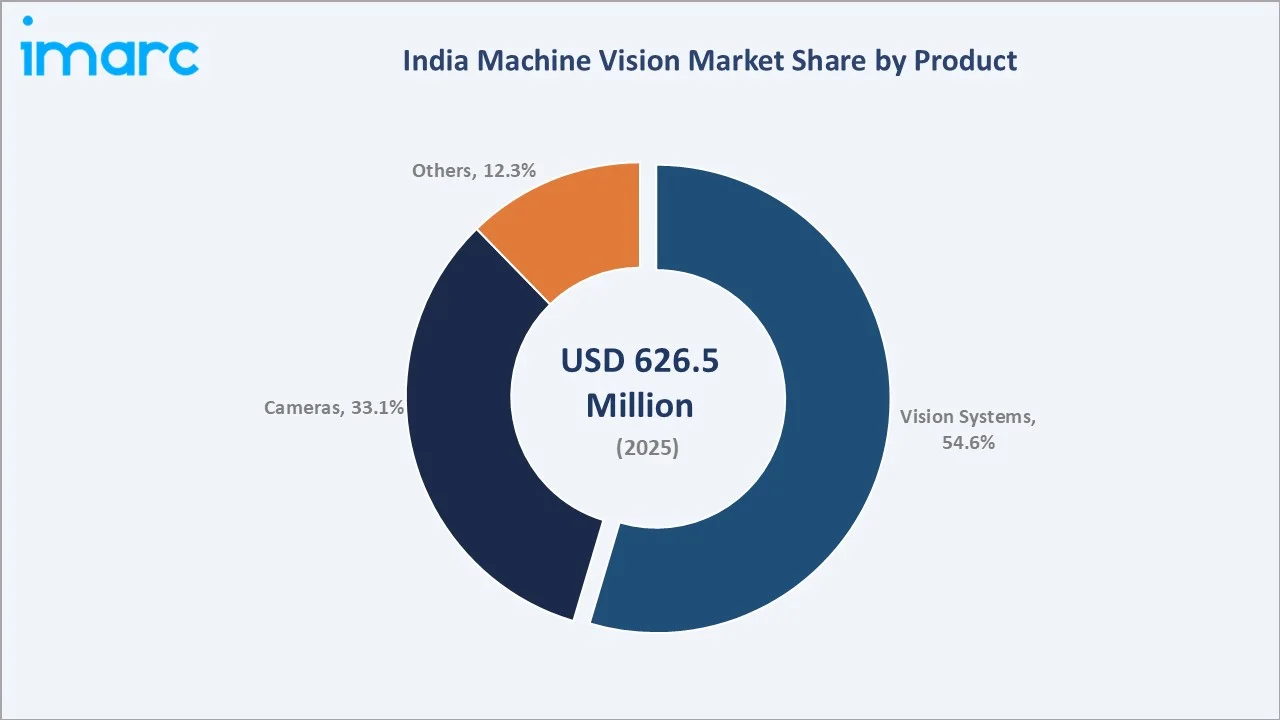

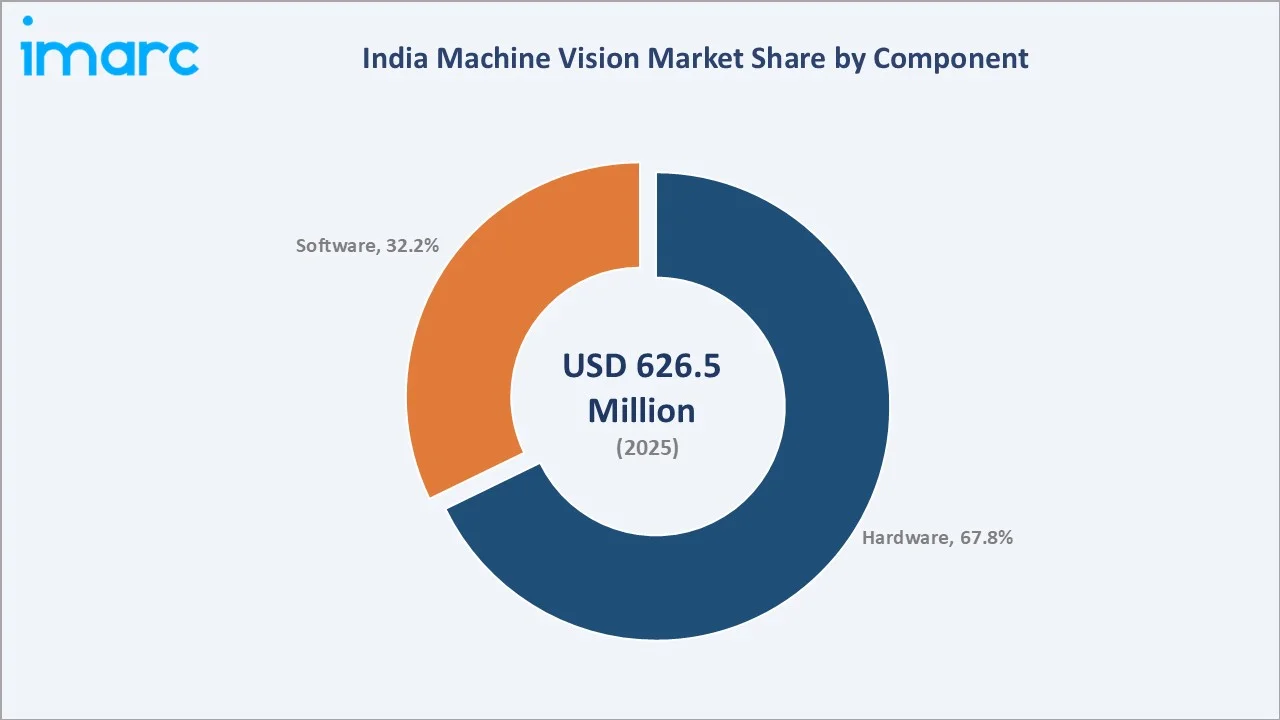

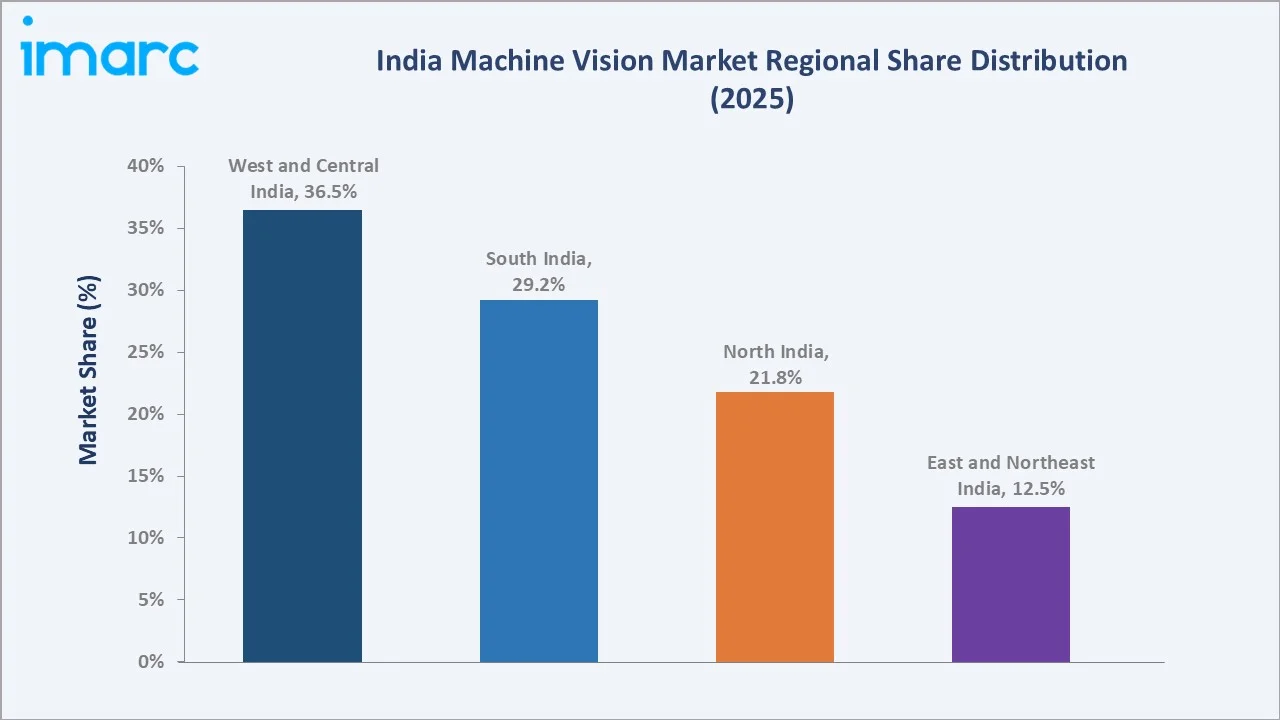

Vision systems lead the product segment at 54.6%, hardware dominates the component segment at 67.8%, and West and Central India commands 36.5% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 626.5 Million |

|

Forecast Market Size (2034) |

USD 1,051.0 Million |

|

CAGR (2026-2034) |

5.74% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West and Central India (36.5%, 2025) |

|

Second Largest Region |

South India (29.2%, 2025) |

|

Leading Product |

Vision Systems (54.6%, 2025) |

|

Leading Component |

Hardware (67.8%, 2025) |

The India machine vision market expanded from USD 474.0 Million in 2020 to USD 626.5 Million in 2025, supported by early automation adoption on automotive and electronics assembly lines. Anchored at USD 828.2 Million in 2030, the forecast to USD 1051.0 Million by 2034 is driven by expanding semiconductor fabrication capacity, broader deployment of 3D and embedded vision, and rising integration of AI-based defect detection.

To get more information on this market, Request Sample

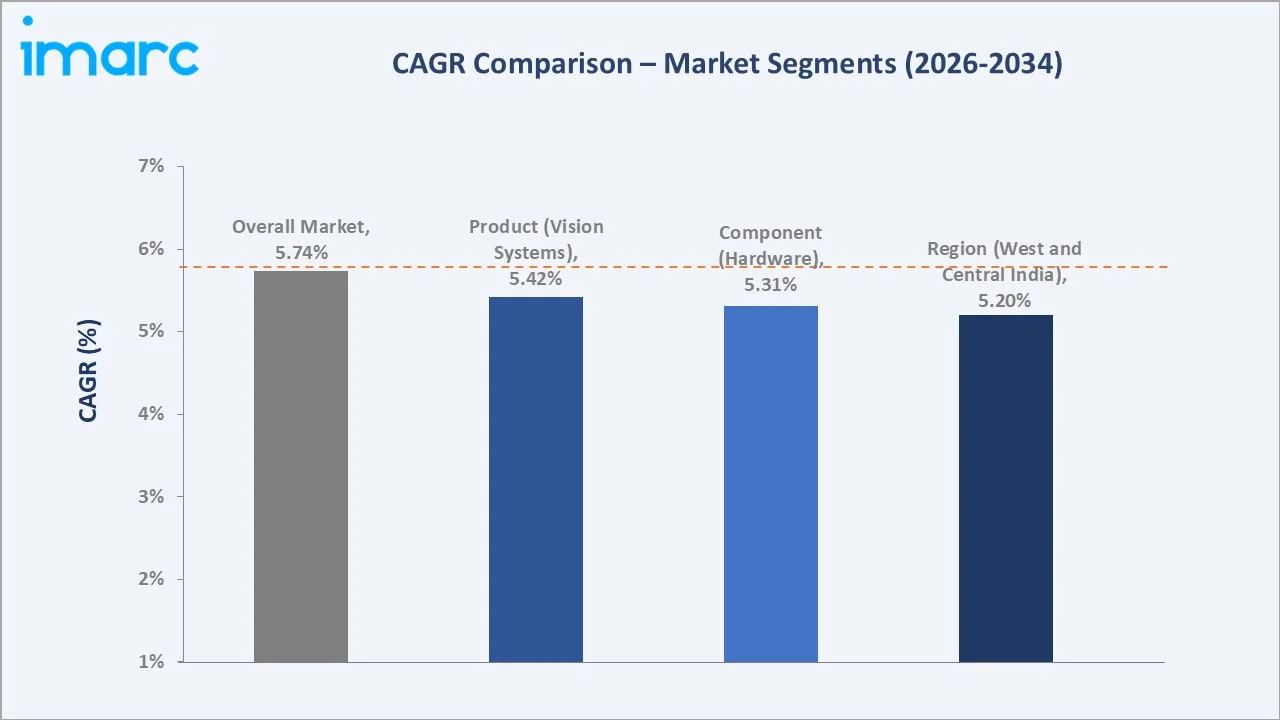

CAGR trajectories across product, component, and regional sub-segments show software and South India expanding faster than the overall 5.74% market CAGR, driven by rising demand for AI-based analytics, cloud-connected inspection platforms, and accelerating electronics and semiconductor manufacturing outside the traditional West and Central India base.

Executive Summary

The India machine vision market is on a steady growth path from USD 474.0 Million in 2020 to USD 1051.0 Million by 2034. Adoption has shifted from manual visual inspection toward automated, camera-driven quality control across automotive, electronics, food and beverage, and pharmaceutical manufacturing. Falling camera and sensor costs, along with growing awareness of deep learning-based inspection, are encouraging manufacturers to integrate vision-guided automation into production lines.

Vision systems lead the product segment at 54.6% in 2025, supported by widespread use in defect detection, dimensional measurement, and robotic guidance applications. Based on component, hardware dominates with a 67.8% share, reflecting continued investment in cameras, sensors, and optics. West and Central India commands 36.5% of the regional share, led by dense automotive and engineering manufacturing clusters.

Key Market Insights

|

Insight |

Data |

|

Leading Product |

Vision Systems - 54.6% share (2025) |

|

Second Largest Product |

Cameras - 33.1% share (2025) |

|

Leading Component |

Hardware - 67.8% share (2025) |

|

Second Largest Component |

Software - 32.2% share (2025) |

|

Leading Region |

West and Central India - 36.5% share (2025) |

|

Second Largest Region |

South India - 29.2% share (2025) |

|

Top Companies |

Cognex, Keyence Corporation, Omron Corporation, Basler AG, SICK AG |

Key Analytical Observations Expanding On The Data Above:

- Vision systems dominance at 54.6% is supported by widespread deployment across defect detection, dimensional measurement, and robotic guidance in automotive and electronics assembly.

- Cameras at 33.1% remain essential as standalone imaging hardware, particularly among cost-sensitive small and mid-sized manufacturers across tier-2 industrial clusters.

- Hardware leadership at 67.8% reflects continued capital investment in cameras, sensors, lighting, and optics as manufacturers upgrade legacy production lines.

- Software share at 32.2% is expanding steadily as manufacturers increasingly adopt AI-enabled image processing, deep learning-based inspection, and analytics platforms to improve defect detection accuracy, production efficiency, and real-time quality monitoring across automated manufacturing environments.

- West and Central India at 36.5% dominates regional share, anchored by Maharashtra and Gujarat's dense automotive, engineering, and chemical manufacturing base.

India Machine Vision Market Overview

Machine vision refers to the use of cameras, sensors, and computer algorithms that enable industrial equipment to capture, analyze, and interpret visual information for automated inspection, measurement, identification, and robotic guidance. The market spans vision systems, cameras, and other supporting products.

The India machine vision ecosystem integrates camera and sensor manufacturers, optics and lighting suppliers, software and algorithm developers, system integrators, distributors, and end-use industries, including automotive, electronics, food and beverage, and pharmaceuticals. Together, these participants enable automated visual inspection across increasingly complex, high-speed manufacturing environments.

Market Dynamics

To evaluate market opportunities, Request Sample

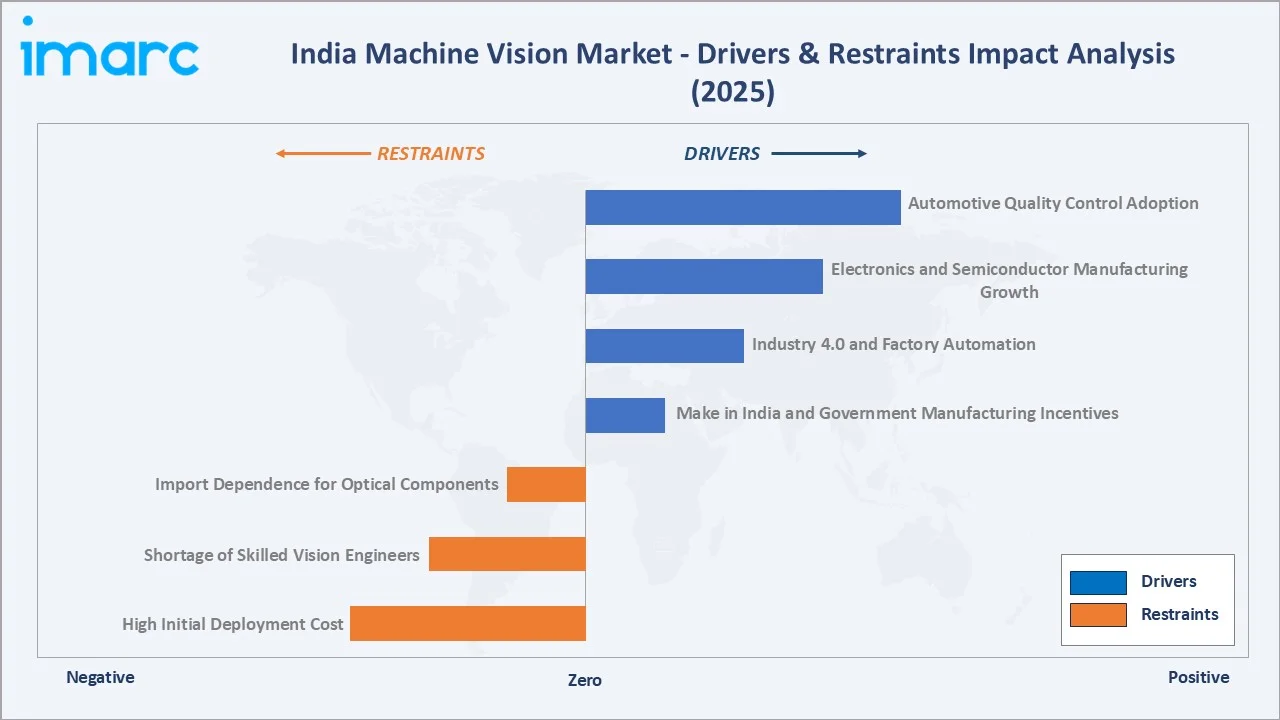

Market Drivers

- Automotive Quality Control Adoption: India's expanding automotive and auto-component manufacturing base is increasingly deploying vision-guided inspection to meet tightening quality and safety standards across engine, body, and electronics assembly lines. In January 2026, in India, the overall production of passenger vehicles, three wheelers, two wheelers, and quadricycle reached approximately 2.9 Million units.

- Electronics and Semiconductor Manufacturing Growth: Expanding domestic electronics assembly and emerging semiconductor fabrication and packaging facilities are driving demand for high-precision optical inspection of components, wafers, and printed circuit boards.

- Industry 4.0 and Factory Automation: As per IMARC Group, the India Industry 4.0 market size reached USD 6.3 Billion in 2025. Rising integration of robotics, IoT-enabled sensors, and connected production lines is increasing reliance on machine vision for real-time quality monitoring and process control.

- Make in India and Government Manufacturing Incentives: Cumulative committed investment under India's Production Linked Incentive (PLI) scheme crossed INR 1.76 Lakh Crore by 2025 across the electronics, automotive, and allied sectors, reinforcing capital deployment toward automated, vision-enabled production capacity.

Market Restraints

- High Initial Deployment Cost: Advanced vision systems, particularly 3D and multi-camera configurations, require significant upfront capital, which continues to limit adoption among small and mid-sized manufacturers.

- Shortage of Skilled Vision Engineers: Limited availability of engineers trained in vision system integration, calibration, and AI model training constrains the pace of deployment across smaller industrial clusters.

- Import Dependence for Optical Components: India continues to rely on imported semiconductors, cameras, sensors, and optical components, increasing procurement costs and extending lead times for domestic machine vision system integrators and manufacturers.

Market Opportunities

- AI-Enabled Predictive Quality Analytics: Growing interest in combining machine vision with AI-based predictive analytics presents opportunities for value-added software offerings beyond traditional pass or fail inspection.

- Expansion into Food, Beverage, and Pharmaceutical Packaging: Rising regulatory emphasis on traceability and packaging quality is opening new application areas for vision-based inspection beyond core automotive and electronics use cases.

Market Challenges

- Integration Complexity with Legacy Production Lines: Retrofitting vision systems onto older manufacturing equipment often requires custom engineering, extending deployment timelines and raising project costs.

- Data Security and Connectivity Constraints: Cloud-connected vision platforms raise concerns around data security and require reliable connectivity, which remains inconsistent across some industrial clusters.

Emerging Market Trends

1. AI-Enabled Deep Learning Vision

Manufacturers are increasingly replacing rule-based inspection algorithms with deep learning models capable of detecting subtle, previously unclassified defects. This shift is improving inspection accuracy on complex parts with variable surface textures and irregular geometries.

2. Edge Computing and 5G-Integrated Vision

On-device processing and expanding 5G connectivity are enabling vision systems to analyze images locally with minimal latency, supporting real-time defect rejection on high-speed production lines without dependence on centralized servers.

3. Autonomous Quality Inspection Ecosystems

Vision-guided robotics is increasingly combined with automated material handling to create closed-loop inspection and correction systems, reducing manual intervention across high-volume automotive and electronics manufacturing.

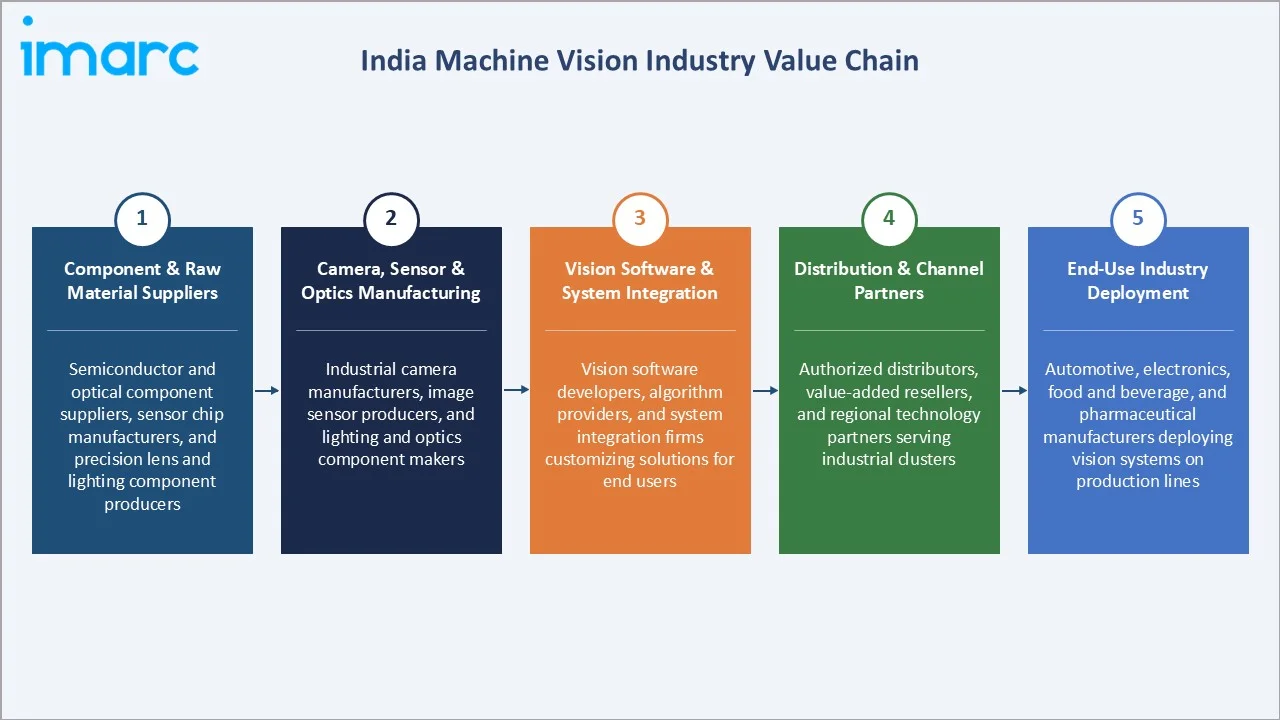

Industry Value Chain Analysis

The India machine vision value chain spans five stages, from component and raw material supply through end-use industry deployment. Camera and sensor manufacturing, along with vision software and system integration, capture the highest value-add, while distribution and channel partnerships increasingly determine market reach across India's fragmented industrial base.

|

Stage |

Key Players / Examples |

|

Component & Raw Material Suppliers |

Semiconductor and optical component suppliers, sensor chip manufacturers, and precision lens and lighting component producers |

|

Camera, Sensor & Optics Manufacturing |

Industrial camera manufacturers, image sensor producers, and lighting and optics component makers |

|

Vision Software & System Integration |

Vision software developers, algorithm providers, and system integration firms customizing solutions for end users |

|

Distribution & Channel Partners |

Authorized distributors, value-added resellers, and regional technology partners serving industrial clusters |

|

End-Use Industry Deployment |

Automotive, electronics, food and beverage, and pharmaceutical manufacturers deploying vision systems on production lines |

Vertically integrated suppliers offering combined hardware and software capabilities are increasingly positioned to capture greater value than partners reliant on third-party components, particularly as customers seek single-vendor accountability for complex inspection systems.

Technology Landscape in the India Machine Vision Industry

AI and Deep Learning Algorithms

Convolutional neural network-based inspection models are increasingly deployed for defect classification, optical character recognition, and anomaly detection, reducing reliance on manually programmed rule sets and improving accuracy on complex, variable products.

3D and Embedded Vision

Structured light, time-of-flight, and stereo vision technologies are enabling volumetric measurement and robotic bin picking, while embedded vision modules are being integrated directly into machinery for compact, cost-efficient inspection.

Edge Computing and Connectivity

On-device processing is reducing latency for real-time inspection decisions, while growing 5G and industrial Ethernet connectivity supports centralized monitoring across distributed production lines.

Robotics and Automation Integration

Vision-guided robotic arms are increasingly used for pick-and-place, assembly verification, and automated material handling, tightening the link between inspection and corrective action on the factory floor.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Vision Systems |

54.6% |

2025 |

|

Component |

Hardware |

67.8% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Industry |

🔒 |

🔒 |

2025 |

|

Region |

West and Central India |

36.5% |

2025 |

By Product

Vision systems command a 54.6% majority share in 2025, driven by widespread deployment in defect detection, dimensional measurement, and robotic guidance across automotive and electronics assembly lines. The segment benefits from continuous improvement in processing speed and integration with AI-based software.

To access detailed market analysis, Request Sample

Cameras at 33.1% in 2025 continue to serve as standalone imaging hardware for simpler inspection tasks, particularly among small and mid-sized manufacturers seeking cost-efficient entry points into automated visual inspection.

By Component

Hardware dominates with 67.8% share in 2025, reflecting sustained capital investment in cameras, sensors, lighting, and optics as the foundation of any vision deployment. The segment remains the default entry point as manufacturers begin automating inspection processes.

Software at 32.2% is expanding as AI-based analytics, no-code configuration tools, and cloud-connected inspection platforms gain adoption, allowing manufacturers to extract greater value from existing camera and sensor investments.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

West and Central India |

36.5% |

Established automotive and engineering manufacturing base, dense industrial clusters, and strong presence of component suppliers and system integrators |

|

South India |

29.2% |

Expanding electronics, semiconductor, and EV manufacturing clusters, rising R&D investment, and growing presence of global technology companies |

|

North India |

21.8% |

Growing automotive and consumer electronics manufacturing, expanding industrial corridors, and increasing government-backed manufacturing incentives |

|

East and Northeast India |

12.5% |

Emerging industrial development, expanding logistics and manufacturing infrastructure, and rising government focus on regional industrial growth |

West and Central India at 36.5% in 2025 leads the regional landscape, anchored by Maharashtra and Gujarat. Dense automotive and engineering manufacturing clusters, along with an established base of component suppliers and system integrators, support sustained regional leadership.

South India at 29.2% is the fastest growing region. Expanding electronics, semiconductor, and EV manufacturing clusters around Bengaluru, Chennai, and Hyderabad are accelerating regional growth through 2034.

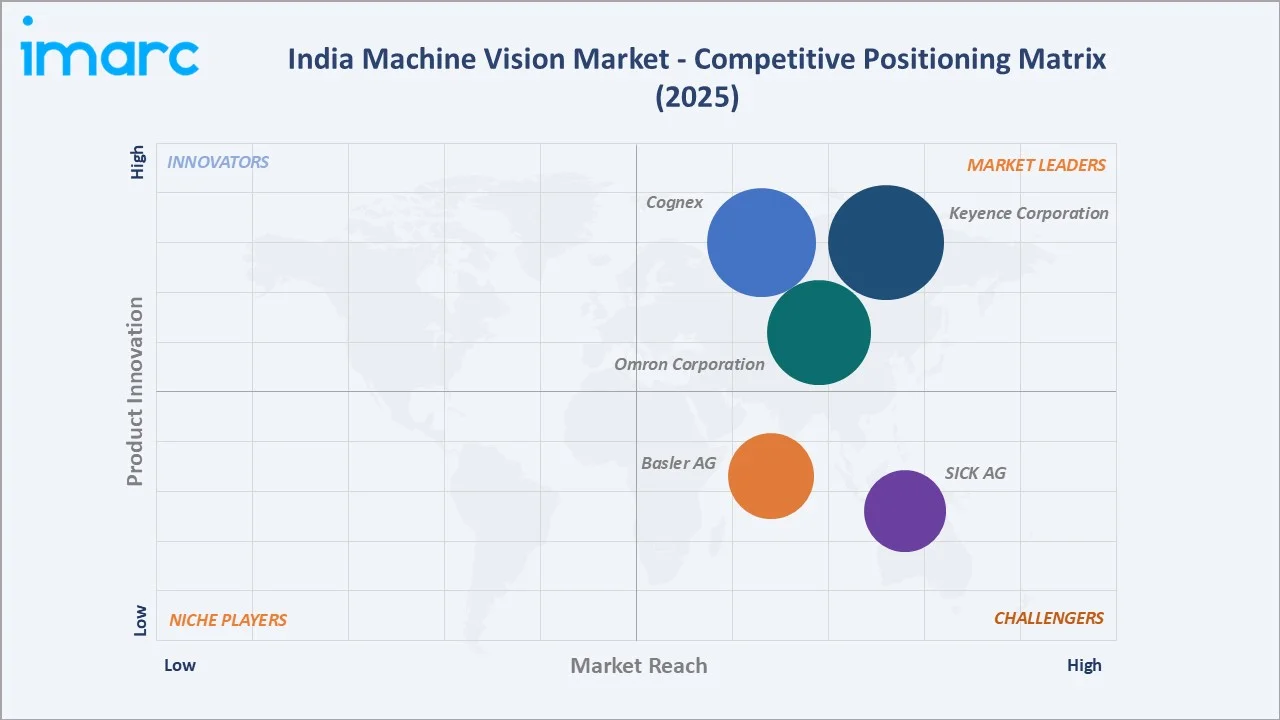

Competitive Landscape

The India machine vision market is moderately fragmented, with established global technology providers competing alongside regional system integrators. Product breadth, AI capability, local support infrastructure, and pricing flexibility form the key competitive differentiators across automotive, electronics, and general manufacturing applications.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Cognex |

Machine Vision Systems |

Leader |

Broad-based machine vision provider emphasizing AI-enabled inspection and barcode reading across manufacturing and logistics |

|

Keyence Corporation |

Intuitive Vision System - CV-X Series |

Leader |

Direct sales-driven vision and sensor provider emphasizing rapid customer support and continuous product innovation |

|

Omron Corporation |

FH Series Vision System |

Leader |

Integrated automation provider combining vision, robotics, and controllers for smart factory applications |

|

Basler AG |

ace 2 Cameras |

Challenger |

Imaging component specialist offering a broad camera and hardware portfolio for system integrators |

|

SICK AG |

Inspector Vision Sensors |

Challenger |

Sensor-focused provider combining vision with broader factory and logistics automation solutions |

Key players include Cognex, Keyence Corporation, Omron Corporation, Basler AG, and SICK AG, among others.

Key Company Profiles

Cognex

Cognex is an American machine vision company headquartered in Natick, Massachusetts. The company designs cameras, sensors, and software that enable industrial equipment to inspect, identify, and guide manufacturing processes, serving customers across automotive, electronics, and logistics industries, including a growing base in India.

- Product Portfolio: In-Sight 7000; OCR readers used for inspection, identification, and robotic guidance.

- Recent Developments: Cognex has expanded its AI-enabled machine vision portfolio with enhanced deep learning inspection capabilities and strengthened its industrial automation partnerships to support advanced manufacturing applications.

- Strategic Focus: Broadening AI-based inspection capability, deepening presence across India's automotive and electronics manufacturing clusters, and expanding barcode and traceability solutions.

Keyence Corporation

Keyence Corporation is a Japanese factory automation company headquartered in Osaka. The company develops sensors, measuring instruments, and vision systems through a direct sales model, supporting manufacturers across electronics, automotive, and general industrial applications in India.

- Product Portfolio: Intuitive Vision System - CV-X Series, along with a broad range of sensors and measurement instruments used for inspection and quality control.

- Recent Developments: Keyence Corporation continues to expand its direct sales and technical support network across India, supporting on-site application testing and faster product deployment for manufacturers.

- Strategic Focus: Strengthening direct customer engagement through on-site technical support, expanding vision system capability, and broadening its sensor and measurement portfolio for Indian manufacturers.

Omron Corporation

Omron Corporation is a Japanese industrial automation company headquartered in Kyoto. The company integrates vision systems with robotics and controllers, offering combined automation solutions to manufacturers across automotive, electronics, and consumer goods industries in India.

- Product Portfolio: FH series vision systems integrated with automation controllers and robotics for combined inspection and material handling solutions.

- Recent Developments: Omron Corporation continues to expand its integrated automation offerings in India, combining vision, robotics, and controls to support smart factory initiatives among domestic manufacturers.

- Strategic Focus: Deepening integration between vision, robotics, and controls, and expanding smart factory solutions across India's automotive and electronics manufacturing base.

Market Concentration Analysis

The India machine vision market is moderately fragmented, with global technology providers such as Cognex, Keyence Corporation, and Omron Corporation accounting for a meaningful share of high-end vision system deployment, while numerous regional system integrators serve cost-sensitive small and mid-sized manufacturers.

Barriers to entry include the need for deep application engineering expertise, established distribution and technical support networks, and the ability to combine hardware with AI-enabled software. These factors favor established global players with broad product portfolios and local service infrastructure.

Consolidation is gradually increasing as larger technology providers acquire specialized software and imaging component firms to broaden their capabilities. Strategic partnerships with system integrators and distributors are further shaping competitive positioning across India's fragmented industrial base.

Investment & Growth Opportunities

Fastest-Growing Segments

Software is expanding the fastest among component segments, driven by rising adoption of AI-based analytics, cloud-connected inspection platforms, and no-code vision configuration tools. Cameras and others are also gaining share as embedded vision modules proliferate across compact production equipment.

Emerging Markets

South India is the fastest growing region, anchored by expanding electronics, semiconductor, and EV manufacturing clusters. The region represents significant opportunity for vendors able to combine strong local technical support with AI-enabled inspection capability.

Venture & Investment Trends

Investment is increasingly directed toward AI-based inspection software, embedded vision modules, and system integration capability. Capital is also flowing into domestic component manufacturing as India's broader electronics and semiconductor investment push encourages localization of camera, sensor, and optics production.

Future Market Outlook (2026-2034)

The India machine vision market is forecast to expand from USD 626.5 Million in 2025 to USD 1051.0 Million by 2034 at a CAGR of 5.74%, adding roughly USD 424.5 Million in incremental market value over the forecast period.

Three forces will shape the market through 2034: deepening integration of AI-based deep learning inspection, expanding semiconductor and electronics manufacturing capacity, and rising adoption of vision-guided robotics across automotive and general manufacturing.

By 2034, the India machine vision market is expected to be defined by AI-native inspection platforms, tighter integration between vision and robotics, and a broader base of domestic component manufacturing supporting more cost-efficient deployment across small and mid-sized manufacturers.

Research Methodology

Primary Research

Primary research included structured interviews with vision system integrators, automotive and electronics manufacturing executives, component suppliers, and industry association representatives, validating market sizing, segment mix, and regional demand patterns.

Secondary Research

Secondary sources included Ministry of Electronics and Information Technology publications, India Semiconductor Mission communications, Society of Indian Automobile Manufacturers data, company annual reports, and industry association publications.

Forecasting Models

Market forecasts used top-down and bottom-up models combining manufacturing output trends, automation adoption rates, component pricing trends, and macroeconomic variables. Scenario analysis addressed semiconductor investment pace and manufacturing capital expenditure cycles.

India Machine Vision Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Vision Systems, Cameras, Others |

| Components Covered | Hardware, Software |

| Applications Covered | Positioning, Identification, Verification, Measurement, Flaw Detection, Others |

| Industries Covered | Electronics and Semiconductor, Automotive, Medical and Pharmaceutical, Food, Packaging and Printing, Security and Surveillance, Intelligent Traffic System, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Cognex, Keyence Corporation, Omron Corporation, Basler AG, SICK AG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India machine vision market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India machine vision market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India machine vision industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Machine Vision Market Report

The India machine vision market was valued at USD 626.5 Million in 2025, driven by rising automation across automotive, electronics, and pharmaceutical manufacturing industries.

The market is projected to grow at a CAGR of 5.74% from 2026-2034, reaching USD 1,051.0 Million, supported by expanding semiconductor and electronics manufacturing.

Vision systems lead at 54.6% in 2025, driven by widespread use in defect detection and robotic guidance. Their integrated capabilities support higher inspection accuracy and production efficiency across manufacturing industries.

Hardware dominates at 67.8% in 2025, reflecting continued investment in cameras and sensors. Ongoing factory automation and production line upgrades continue to support demand for these components.

West and Central India commands 36.5% in 2025, led by dense automotive and engineering manufacturing clusters across Maharashtra and Gujarat.

South India, with 29.2% share in 2025, is the fastest growing region, supported by expanding electronics, semiconductor, and EV manufacturing clusters.

Leading players include Cognex, Keyence Corporation, Omron Corporation, Basler AG, and SICK AG, among others.

AI-based deep learning models are improving defect detection accuracy on complex parts, enabling manufacturers to move beyond traditional rule-based inspection algorithms.

High initial deployment costs, a shortage of skilled vision engineers, and dependence on imported optical components remain key restraints for smaller manufacturers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)