Luxury Fashion Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, End User, and Region, 2026-2034

Luxury Fashion Market Size, Share, Trends & Forecast (2026-2034)

The global luxury fashion market reached USD 261.0 Billion in 2025 and is projected to reach USD 341.0 Billion by 2034, growing at a CAGR of 3.02% during 2026-2034. The enduring desirability of luxury heritage brands, expanding high-net-worth individual (HNWI) populations in emerging economies, rising aspirational consumer demand, tourism-driven flagship retail spend, and the accelerating shift to digital and omni-channel luxury retail are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 261.0 Billion |

|

Forecast Market Size (2034) |

USD 341.0 Billion |

|

CAGR (2026-2034) |

3.02% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

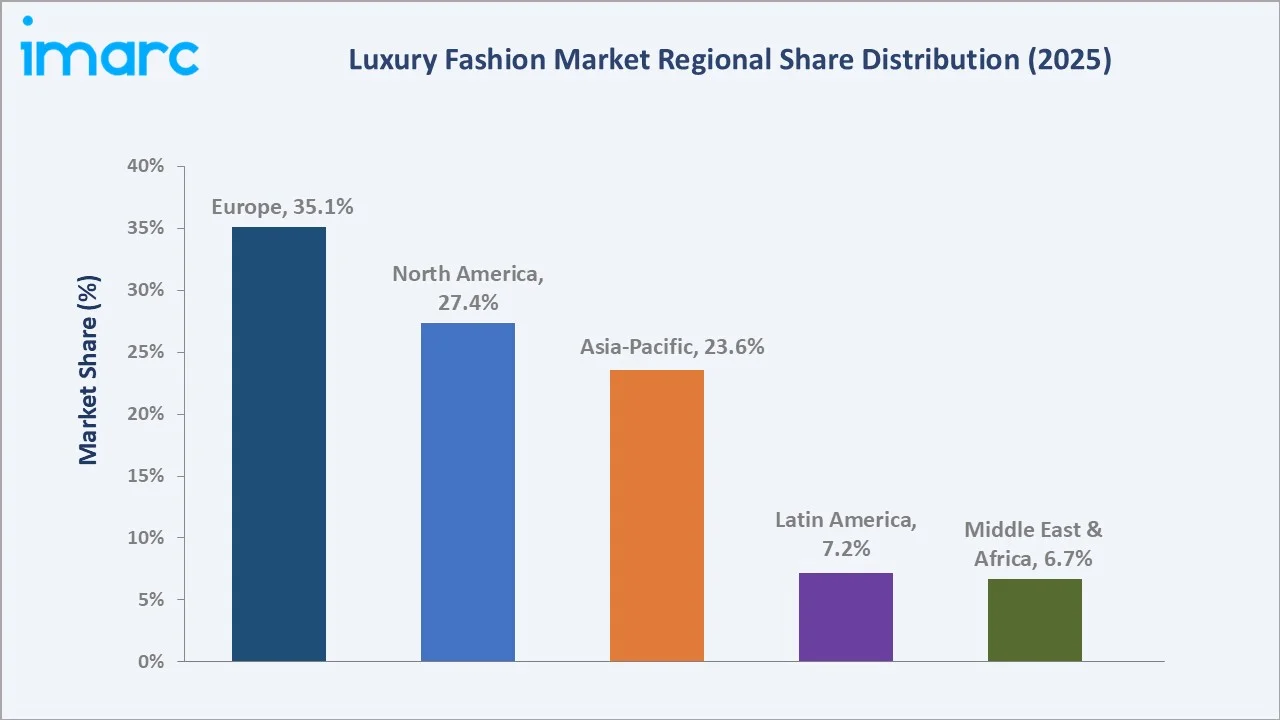

Europe leads regionally with a 35.1% share in 2025, anchored by France and Italy as the historic centers of luxury fashion creation and retail. Clothing and apparel dominate the product segment at 50.7%, while store-based distribution channels lead distribution at 74.6% despite accelerating online luxury penetration.

To get more information on this market, Request Sample

The global luxury fashion market is driven by three structural forces: the compound wealth accumulation of HNWI and ultra-high-net-worth individuals (UHNWIs) globally; the geographic expansion of luxury consumption beyond Europe and North America into Asia-Pacific, the Middle East, and Latin America; and the digital transformation of luxury retail from purely physical flagship experiences to omni-channel and direct-to-consumer digital models. These forces collectively sustain a 3.02% CAGR through 2034.

Executive Summary

The global luxury fashion market is navigating a period of selective growth characterized by polarization between resilient ultra-high-end demand and softening aspirational luxury consumption. The market reached USD 261.0 Billion in 2025 and is forecast to grow at a CAGR of 3.02% to reach USD 341.0 Billion by 2034. LVMH Moët Hennessy – Louis Vuitton, the world's largest luxury conglomerate with 75+ brands, maintained its market leadership, while Kering faced challenges from a structural reset at Gucci.

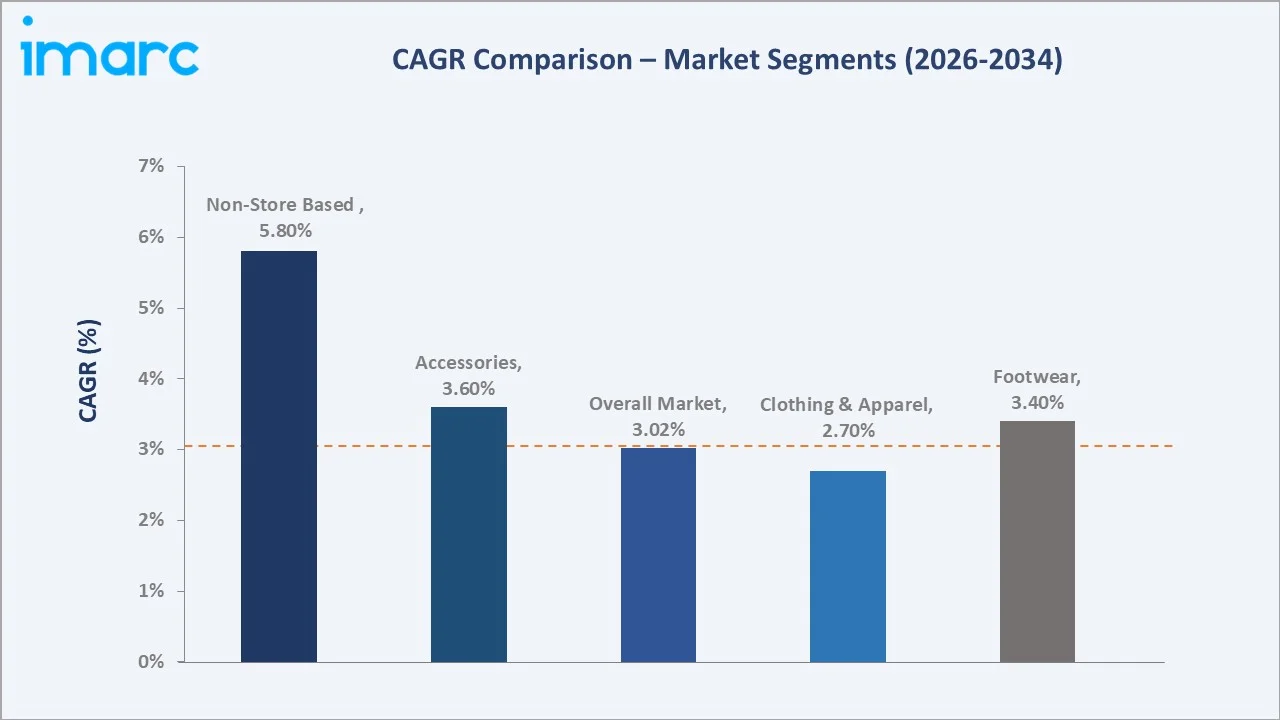

Clothing and apparel dominate at 50.7%, with ready-to-wear and couture from Louis Vuitton, Chanel, Dior, and Gucci anchoring the category. Accessories at 30.8% represent the highest-margin sub-segment, encompassing leather goods (handbags, small leather goods), jewelry, and watches that disproportionately drive revenue and brand desirability. Store-based 74.6% share, reflecting the luxury sector's commitment to flagship experiential retail, though non-store channels are growing at 5.8% CAGR as luxury e-commerce matures.

Europe commands 35.1% of global market share, anchored by France (home to Louis Vuitton, Chanel, Hermès) and Italy (Gucci, Prada, Armani, Valentino, Fendi). Key players include LVMH Moët Hennessy – Louis Vuitton, KERING, CHANEL, Prada S.p.A., and Burberry Group plc.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Clothing & Apparel – 50.7% share (2025) |

|

Fastest Growing Product |

Accessories – ~3.6% CAGR (2026-2034) |

|

Leading Distribution Channel |

Store-Based – 74.6% share (2025) |

|

Fastest Growing Channel |

Non-Store Based – ~5.8% CAGR (2026-2034) |

|

Leading Region |

Europe – 35.1% share (2025) |

|

Top Companies |

LVMH Moët Hennessy – Louis Vuitton, KERING, CHANEL, Prada S.p.A., and Burberry Group plc |

Key Analytical Observations Supporting the Above Data:

- Clothing & Apparel at 50.7% (2025) encompasses ready-to-wear, haute couture, knitwear, and outerwear from global luxury maisons. The segment benefits from the deepest brand heritage in luxury fashion and the strongest customer acquisition power through runway shows and media coverage. Louis Vuitton's ready-to-wear and Chanel's iconic tweed collection represent the category's most commercially successful franchise segments.

- Accessories at 30.8% (2025) and fastest growing (~3.6% CAGR) reflects accessories’ unique position as the entry-level luxury product category that attracts aspirational buyers while delivering the highest gross margins (60–75%) for luxury brands. Leather goods, including the Hermès Birkin, Louis Vuitton Speedy, and Chanel Flap Bag, have established asset-like value retention and waiting list exclusivity that sustains demand through economic cycles.

- Store-based retail at 74.6% (2025) reflects the irreplaceable role of luxury flagship boutiques in brand storytelling and the high-touch customer experience that commands luxury price premiums. Brands including Louis Vuitton, Chanel, and Hermès invest hundreds of millions in flagship retail architecture in Paris, Milan, New York, Tokyo, and Shanghai to reinforce brand equity and justify aspirational pricing.

- Non-store based growing at ~5.8% CAGR: represents the fastest structural shift in luxury retail. Direct brand e-commerce is growing at double-digit rates in North America and Asia-Pacific, driven by high-net-worth millennial and Gen Z consumers who prefer seamless digital purchasing for replenishment categories including leather accessories and shoes.

Luxury Fashion Market Overview

Luxury fashion encompasses high-end, prestigious clothing, accessories, and footwear designed and produced by heritage brands characterized by exceptional craftsmanship, scarcity, and strong brand identity. The global market spans ready-to-wear, haute couture, premium leather goods and accessories, and luxury footwear. Luxury fashion brands maintain their prestige through controlled distribution, artisanal manufacturing (primarily in France, Italy, and Switzerland), brand heritage storytelling, and celebrity and media-driven aspirational positioning.

The market is shaped by a dual-tier consumption structure: ultra-high-net-worth buyers (UHNWI: wealth >USD 30M) who purchase across all price tiers without economic constraint, and aspirational luxury buyers (income USD 100,000–500,000 annually) whose purchasing behavior is more cyclically sensitive. The Bain & Company Altagamma Luxury Study estimates the global luxury consumer population at 330 million in 2025, with Asia-Pacific Gen Z and Millennial consumers representing the most significant incremental cohort.

Market Dynamics

To evaluate market opportunities, Request Sample

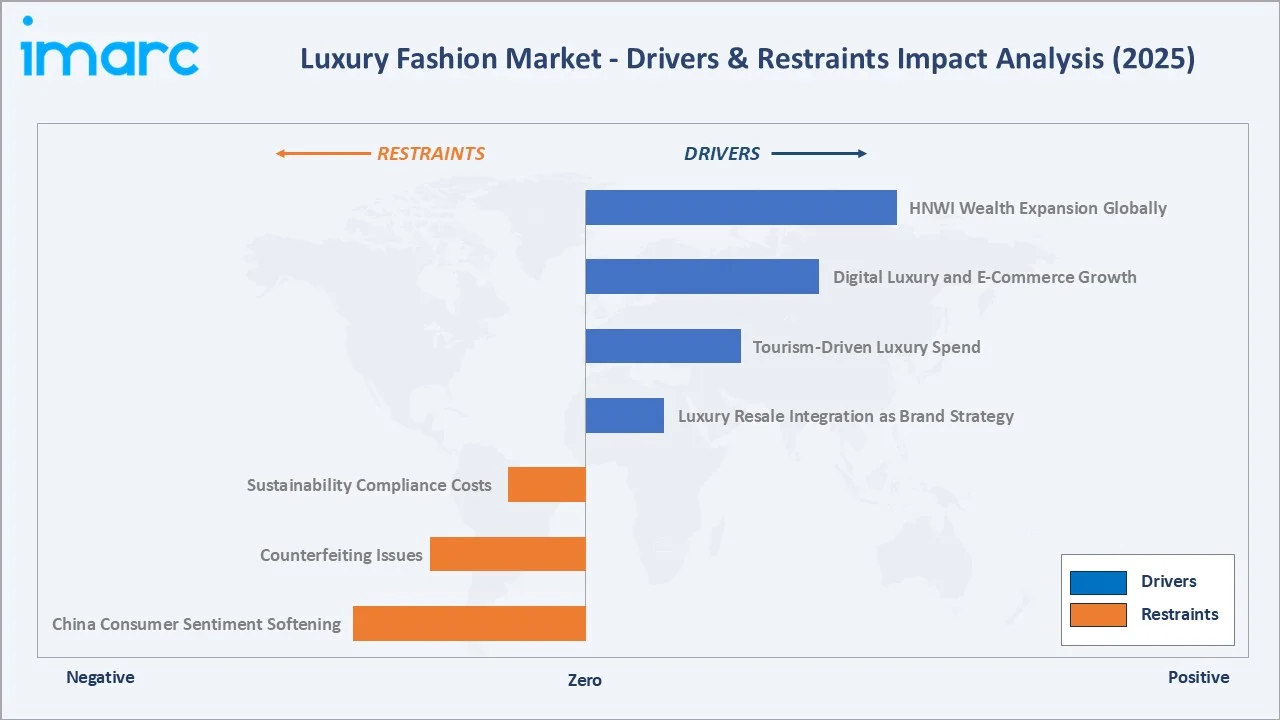

Market Drivers

- Rising HNWI Population Growth: By the end of June 2025, the global population of high-net-worth (HNW) individuals, each holding wealth exceeding USD 1 million, was estimated at approximately 41.3 million, creating a structurally expanding base of luxury fashion buyers.

- Tourism-Driven Luxury Spend: The recovery of Chinese outbound tourism to Europe and the US post-2023, combined with the structural growth of Middle Eastern and Indian tourist spending in Paris, Milan, and London, has been a key revenue driver. Tourist spending by US visitors in Europe grew around 5% in 2025.

- Digital Luxury and E-Commerce Growth: Direct-brand e-commerce and luxury multi-brand online platforms are growing at 12–18% annually in key markets. In August 2024, CHANEL launched its e-commerce platform in India to expand access to its luxury products, serving 27,000 postcodes and addressing the limited physical retail presence.

Market Restraints

- China Consumer Sentiment Softening: China's luxury market contracted by an estimated 20–22% in 2024 as consumer confidence weakened, property sector deleveraging reduced perceived wealth, and anti-ostentation social trends dampened conspicuous luxury spending.

- Counterfeiting Issues: The global secondhand luxury goods market size was valued at USD 40.4 Billion in 2025, partly cannibalizing new luxury purchases in price-sensitive segments. Advanced counterfeiting techniques, particularly for leather goods and accessories, continue to undermine brand value and erode consumer trust in secondary market authenticity.

- Sustainability Compliance Costs: EU Digital Product Passport (DPP) regulations mandating material traceability by 2025–2026, combined with rising carbon border adjustment mechanisms, are imposing compliance costs of 2–5% of revenue for luxury brands with complex multi-country supply chains.

Market Opportunities

- India as the Next Luxury Frontier: India's luxury fashion market is growing at 8–10% annually, driven by a billionaire population that exceeded China's in 2024, a growing upper-middle class, and increasing fashion-forward urban consumption in Mumbai, Delhi, Bangalore, and Hyderabad. Brands including Louis Vuitton, Gucci, Chanel, and Hermès are accelerating store expansion, while Chanel's August 2024 India e-commerce launch signals a systematic digital market entry strategy.

- Luxury Resale Integration as Brand Strategy: Certified pre-owned programs from LVMH Moët Hennessy – Louis Vuitton and KERING portfolio brands are transforming the resale channel from a competitive threat into a brand equity tool. Aura Blockchain Consortium (founded by LVMH Moët Hennessy – Louis Vuitton, Prada S.p.A., and Cartier, part of Richemont) has issued 40+ million digital provenance certificates, enabling first-sale brand engagement with pre-owned buyers and creating authenticated circular economy infrastructure.

Market Challenges

- Generational Brand Relevance: The luxury fashion industry faces a structural challenge in maintaining desirability among Gen Z consumers who are more price-value conscious, sustainability-oriented, and resistant to traditional prestige signaling than prior generations.

- Macroeconomic Sensitivity of Aspirational Luxury: Around 35% of aspirational luxury consumers, typically spending below $6,000 (€5,000) annually on luxury goods, have reduced discretionary luxury purchases and redirected their spending toward savings, investments, wellness, second-hand luxury products, and more affordable fashion alternatives.

Emerging Market Trends

1. Burberry Group plc’s Supply Chain Vertical Integration

In March 2023, Burberry Group plc announced the acquisition of Pattern, an Italian luxury outerwear supplier it had partnered with for nearly two decades, strengthening its vertical integration in its quilted and down outerwear category. This strategic move to own manufacturing capabilities directly at the craftsmanship source reflects the broader luxury industry trend of vertical integration in heritage product categories to protect quality standards, ensure supply chain resilience, and improve margins on high-value outerwear lines.

2. Prada S.p.A.’s Luxury Beauty Expansion into Skincare

In 2023, Prada S.p.A. announced its venture into skincare and color cosmetics, joining Chanel, Hermès, Dior, and Giorgio Armani in expanding luxury fashion brand equity into the high-margin beauty category. This adjacency strategy reflects luxury brands’ recognition that beauty represents a lower price-point entry vehicle for aspirational consumers and a high-frequency repurchase category that deepens brand engagement beyond infrequent fashion purchases.

3. CHANEL’s India E-Commerce Launch

In August 2024, CHANEL launched its e-commerce platform in India, expanding access to its luxury products including fragrances, beauty, and eyewear across 27,000 postcodes and directly addressing the limited physical retail infrastructure in a country where e-commerce is projected to represent 40%+ of luxury sales by 2030. This digital expansion strategy signals CHANEL's recognition of India as a tier-1 luxury growth market requiring dedicated digital investment.

4. Aura Blockchain Consortium for Luxury Authenticity

Aura Blockchain Consortium, which by 2024 had issued over 40 million digital certificates providing immutable provenance and ownership histories for luxury goods. This blockchain infrastructure directly addresses luxury counterfeiting, supports certified pre-owned program authentication, and creates a digital ownership record that enhances resale value transparency and brand trust in secondary markets.

Industry Value Chain Analysis

The luxury fashion value chain is distinguished by the primacy of craftsmanship and brand narrative at every stage, from raw material provenance to post-purchase relationship management, with geographic concentration in France, Italy, and Switzerland for heritage production.

|

Stage |

Key Players / Activities |

|

Raw Materials & Craftsmanship |

Premium textile mills, tanneries, silk weavers, leather suppliers, and precious metal artisans providing certified luxury-grade inputs |

|

Creative Design & Ateliers |

In-house design teams, Creative Directors, and specialist ateliers for haute couture pattern-making and prototyping |

|

Manufacturing & Quality Control |

Made-in-France and Made-in-Italy workshops, ISO-certified luxury goods manufacturers, artisan training programs, and heritage craft preservation initiatives |

|

Brand Marketing & Fashion Shows |

Paris, Milan, London, and New York Fashion Week runway shows; celebrity partnerships; magazine editorials; and influencer luxury placement programs. |

|

Flagship & Digital Retail |

Architect-designed flagship boutiques, multi-brand luxury department stores, brand direct e-commerce, and luxury e-tailers |

|

After-Sales & Loyalty CX |

Repair and restoration ateliers, private client advisors, loyalty gifting, and certified pre-owned authentication programs |

Technology Landscape in the Luxury Fashion Industry

Clothing and Apparel – Ready-to-Wear and Haute Couture

Luxury clothing & apparel encompasses ready-to-wear (prêt-à-porter) and haute couture, with the 50.7% market share reflecting clothing's role as the foundational product category of luxury fashion. RTW collections from Louis Vuitton, Dior, Gucci, and Chanel drive seasonal brand momentum through runway shows and fashion media, while their commercial volumes are sustained by the breadth of silhouette, color, and style offerings that generate repeat purchase from loyal wardrobing clients.

Luxury Accessories – Leather Goods and Jewelry

Accessories at 30.8% represent the luxury industry's highest-margin category, with iconic leather goods such as the Birkin (Hermès), Neverfull (Louis Vuitton), and Classic Flap (Chanel) commanding three-year waiting lists and auction premiums of 50–100% over retail. Jewelry from Cartier and Tiffany & Co. represents the cross-category expansion of fashion houses into hard luxury.

Luxury Footwear – Design and Craftsmanship

Luxury footwear at 18.5% is anchored by Italian heritage cobbling traditions and fashion-forward luxury shoe design from Christian Louboutin, Jimmy Choo (Capri Holdings), Manolo Blahnik, and luxury fashion house shoe lines (Prada, Gucci, Louis Vuitton). Athletic luxury crossover, including Gucci x adidas and Louis Vuitton trainers, has expanded the footwear addressable market to include younger Gen Z buyers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Clothing & Apparel |

50.7% |

2025 |

|

Distribution Channel |

Store-Based |

74.6% |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Europe |

35.1% |

2025 |

By Product Type

Clothing and apparel dominates the product type segment with a 50.7% share in 2025. This encompasses all luxury ready-to-wear, couture, sportswear, outerwear, and knitwear from global luxury maisons and independent heritage brands. The segment's dominance reflects the fashion industry's seasonal collection-driven business model that generates consistent new product volume through spring/summer and autumn/winter runway collections.

To access detailed market analysis, Request Sample

Accessories at 30.8%, driven by the asset-like appreciation of iconic luxury handbags, growing jewelry demand from aspirational consumers, and expanding luxury accessory product ranges that offer lower absolute price points than apparel for new luxury consumer acquisition. Footwear at 18.5% benefits from luxury brand expansion into sneaker and casual shoe categories.

By Distribution Channel

Store-based distribution channel with a 74.6% share in 2025, reflecting the primacy of physical flagship retail in luxury brand equity creation. Luxury brands invest in architecturally distinctive flagship boutiques as brand identity assets that command tourist pilgrimages and media coverage exceeding their direct revenue contribution.

Non-store based distribution channels at 25.4%, driven by the maturation of luxury e-commerce in North America and Europe, the rapid expansion of luxury digital retail in Southeast Asia and India, and Gen Z and Millennial luxury consumers’ preference for seamless online purchasing. Major luxury brand direct e-commerce platforms are increasingly offering exclusive digital-first drops and personalization services unavailable in physical retail.

Regional Market Insights

Europe's 35.1% market share in 2025 reflects its irreplaceable position as both the production heartland and the most prestigious retail destination of global luxury fashion. France and Italy house the world's most iconic luxury fashion maisons, including Louis Vuitton, Hermès, Chanel (France); Prada, Giorgio Armani, Valentino, Fendi (Italy).

North America at 27.4% represents the world's largest single-country luxury consumer base, with the United States generating approximately USD 65–70 Billion in luxury fashion retail annually. The US luxury market is characterized by a large, geographically distributed affluent consumer base in metropolitan areas, strong luxury e-commerce penetration, and a growing secondhand luxury ecosystem that sustains brand desirability across income brackets.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe |

35.1% |

Home to LVMH Moët Hennessy – Louis Vuitton, KERING, CHANEL, and Prada S.p.A.; Paris and Milan as luxury retail pilgrimages; strong inbound tourist luxury spend |

|

North America |

27.4% |

US as the world's largest single luxury consumer market; growing luxury e-commerce; employer-driven affluent consumer base |

|

Asia-Pacific |

23.6% |

India as fast-growing frontier; Southeast Asia luxury hub development in Singapore and Thailand |

|

Latin America |

7.2% |

Brazil and Mexico as primary luxury consumer markets; growing middle-class luxury entry; duty-free luxury retail expansion in major airports and tourist destinations |

|

Middle East & Africa |

6.7% |

UAE and Saudi Arabia as high-per-capita luxury markets; Vision 2030 retail investments; growing HNWI population in Gulf states |

Competitive Landscape

The global luxury fashion market is concentrated at the conglomerate level, with LVMH Moët Hennessy – Louis Vuitton, KERING, and Burberry Group plc, and the privately held CHANEL collectively commanding approximately 40–45% of global luxury fashion revenue.

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

LVMH Moët Hennessy – Louis Vuitton |

Louis Vuitton, Christian Dior, Celine, Fendi, Givenchy, Marc Jacobs, Tiffany & Co., Hublot, Bvlgari, among others |

Market Leader |

World's largest luxury conglomerate; 75+ brands; Louis Vuitton is one of the world’s largest global luxury brands |

|

KERING |

Gucci, Saint Laurent, Bottega Veneta, Balenciaga, Alexander McQueen, Brioni, Boucheron, Pomellato, DoDo, Qeelin, among others |

Market Leader |

Fashion-forward positioning; structural Gucci reset challenge in 2024–2025 |

|

CHANEL |

Chanel |

Strong Challenger |

Iconic No.5 fragrance and Tweed suit heritage; disciplined global price harmonization |

|

Prada S.p.A. |

Prada, Miu Miu, Church’s, Versace, Car Shoe, Luna Rossa |

Strong Challenger |

Beauty expansion; Aura Blockchain Consortium founding member; Italy's most valuable fashion group |

|

Burberry Group plc |

Burberry |

Challenger |

British heritage trenchcoat leadership; Pattern acquisition for vertical integration |

Independent houses including Hermès International, Prada S.p.A., and Giorgio Armani S.p.A. maintain leading positions through deliberate independence from conglomerate ownership.

Key Company Profiles

LVMH Moët Hennessy – Louis Vuitton

LVMH Moët Hennessy – Louis Vuitton is the world's largest luxury conglomerate. Founded and controlled by Bernard Arnault, the company operates 75+ prestigious brands across fashion, leather goods, jewelry, wines, and hospitality, with Louis Vuitton as the world's most valuable luxury brand.

- Product Portfolio: Louis Vuitton (ready-to-wear, leather goods, accessories), Christian Dior, Céline, Fendi, Givenchy, Loewe, Loro Piana, Marc Jacobs, TAG Heuer, and other additional brands across luxury fashion, jewelry, and lifestyle.

- Recent Developments: In June 2024, LVMH Moët Hennessy – Louis Vuitton strengthened its watches division through the acquisition of L’Epée 1839, a Swiss luxury clock manufacturer, enhancing its expertise in high-end horology and mechanical “objets d’art.”

- Strategic Focus: Sephora beauty retail global expansion; India and Southeast Asia luxury retail footprint scaling; digital clienteling platform investment.

KERING

KERING is one of the global luxury conglomerates, managing a portfolio of numerous luxury houses across fashion, leather goods, jewelry, and eyewear.

- Product Portfolio: Gucci (apparel, leather goods, accessories), Saint Laurent (ready-to-wear, bags), Bottega Veneta (leather goods), Balenciaga (fashion, footwear), Alexander McQueen, Brioni, Pomellato, Boucheron, and Kering Eyewear, among others.

- Recent Developments: In April 2026, KERING formed a strategic partnership with ICCF and acquired a minority stake in the group to support the international expansion of ICCF's flagship luxury fashion brand, ICICLE.

- Strategic Focus: Kering Beauté fragrance portfolio expansion; Saint Laurent and Bottega Veneta sustaining above-group-average growth; digital clienteling platform development.

Prada S.p.A.

Prada S.p.A. is one of Italy's most internationally recognized luxury groups, operating the Prada, Miu Miu, Versace, and Church's brands across ready-to-wear, leather goods, accessories, and footwear.

- Product Portfolio: Prada (apparel, bags, shoes, accessories, fragrances), Miu Miu (ready-to-wear, accessories), Church's (luxury English footwear), Car Shoe, and Luna Rossa (sailing and sportswear).

- Recent Developments: In December 2025, Prada S.p.A. completed the acquisition of Versace from Capri Holdings. The deal expanded Prada Group’s brand portfolio by integrating the iconic Italian fashion house alongside Prada and Miu Miu to enhance long-term growth and global market competitiveness.

- Strategic Focus: Miu Miu brand acceleration for Gen Z audience; Prada beauty launch with L'Oréal partnership; Aura Blockchain Consortium digital authentication scale-up.

Market Concentration Analysis

The global luxury fashion market is moderately concentrated at the conglomerate level, with LVMH Moët Hennessy – Louis Vuitton, KERING, Prada S.p.A., and Burberry Group plc, and the privately held CHANEL collectively commanding approximately 40–45% of global luxury fashion revenue.

Market consolidation has been driven primarily by LVMH Moët Hennessy – Louis Vuitton’s serial acquisitions (Tiffany & Co., Off-White, and Loro Piana) rather than KERING or Richemont. The luxury market's future concentration is expected to be influenced by family ownership structures (Hermès remains 66% controlled by the Hermès family), which protect several major houses from conglomerate consolidation.

Investment & Growth Opportunities

Fastest Growing Segments

Non-store based distribution channel (~5.8% CAGR), Accessories product type (~3.6% CAGR), and Middle East & Africa region (~8.0% CAGR) represent the highest-growth investment vectors through 2034. Luxury e-commerce, in particular, represents a USD 50–60 Billion addressable market increment by 2034 as digital channel penetration increases from 25.4% to an estimated 35% of total luxury fashion revenue.

India as Emerging Luxury Frontier

India's luxury fashion market is estimated at USD 8–10 Billion in 2025 and growing at 8–10% annually. With a billionaire count exceeding China's in 2024, a rapidly expanding upper-middle class in metropolitan cities, and a young, fashion-forward consumer demographic, India is the luxury industry's most significant near-term growth market. Brands building early digital and physical retail infrastructure in India are positioned to capture first-mover advantages in the next decade's most important luxury consumer market.

Investment Trends

- Private equity investment in luxury fashion grew significantly in 2024–2025, with LVMH Moët Hennessy – Louis Vuitton’s investment arm L Catterton and KERING's investment platform actively co-investing in emerging luxury fashion brands in the USD 50–200 Million revenue range that can be scaled through conglomerate distribution and marketing infrastructure.

- The global luxury resale market, estimated at USD 50–60 Billion, represents a structural investment opportunity as certified pre-owned programs, blockchain authentication platforms, and luxury recommerce specialists scale.

Future Market Outlook (2026-2034)

The global luxury fashion market is positioned for steady, profitable growth through 2034. From USD 261.0 Billion in 2025, the market is projected to reach USD 341.0 Billion by 2034 at a CAGR of 3.02%. This trajectory reflects a market that has absorbed its post-pandemic normalization and China demand correction and is returning to its structural long-term growth rate, sustained by the compound expansion of the global HNWI population and the geographic diversification of luxury demand toward India, the Middle East, Southeast Asia, and Latin America.

The 2026–2034 period will be defined by the completion of digital luxury infrastructure, the integration of circular economy principles through certified pre-owned and upcycling programs, and the generational transition of luxury brand custodianship to creative directors who understand Gen Z and Millennial luxury values of authenticity, sustainability, and cultural relevance over pure status signaling.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 90 industry participants in 2024–2025, including luxury brand executives, retail buyers, consumer insights specialists, investment analysts covering luxury equities, and HNWI consumer panels across Europe, North America, Asia-Pacific, and the Middle East.

Secondary Research

Secondary research encompassed LVMH Moët Hennessy – Louis Vuitton, KERING, Prada S.p.A., and Burberry Group plc annual reports; Bain & Company Altagamma Luxury Study; McKinsey State of Fashion reports; Business of Fashion global fashion monitor; and industry publications including Vogue Business, WWD, and The Financial Times luxury sector coverage.

Forecasting Models

Market size estimations used top-down and bottom-up modelling incorporating global HNWI population growth projections, per-capita luxury spend trajectories by region, brand revenue disclosures, and tourism-driven demand multipliers. A base-case CAGR of 3.02% reflects consensus luxury market growth estimates validated against Bain-Altagamma forecasts and leading conglomerate guidance.

Luxury Fashion Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered |

|

| Distribution Channels Covered | Store-Based, Non-Store Based |

| End Users Covered | Men, Women, Unisex |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | LVMH Moët Hennessy – Louis Vuitton, KERING, CHANEL, Prada S.p.A., Burberry Group plc, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the luxury fashion market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global luxury fashion market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the luxury fashion industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Luxury Fashion Market Report

The global luxury fashion market reached USD 261.0 Billion in 2025 and is projected to reach USD 341.0 Billion by 2034.

The market is expected to grow at a CAGR of 3.02% during the forecast period of 2026-2034.

Clothing and apparel dominate with a 50.7% market share in 2025, reflecting the fashion industry's seasonal collection-driven business model that generates consistent new product volume.

Store-based distribution channels dominate with a 74.6% market share in 2025, driven by luxury retail store expansions in North America, Europe, and Asia-Pacific.

Europe leads with a 35.1% regional share in 2025, anchored by France and Italy as the home markets of the world's most iconic luxury fashion maisons.

Key players include LVMH Moët Hennessy – Louis Vuitton, KERING, CHANEL, Prada S.p.A., and Burberry Group plc.

Primary drivers include HNWI population expansion globally, tourism-driven luxury spend recovery, digital luxury e-commerce growth, India and Middle East market development, and the integration of Accessories as the highest-growth product category.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)