Mexico Freight and Logistics Market Size, Share, Trends and Forecast by Logistics Function, End Use Industry, and Region 2026-2034

Mexico Freight and Logistics Market Size, Share, Trends & Forecast (2026-2034)

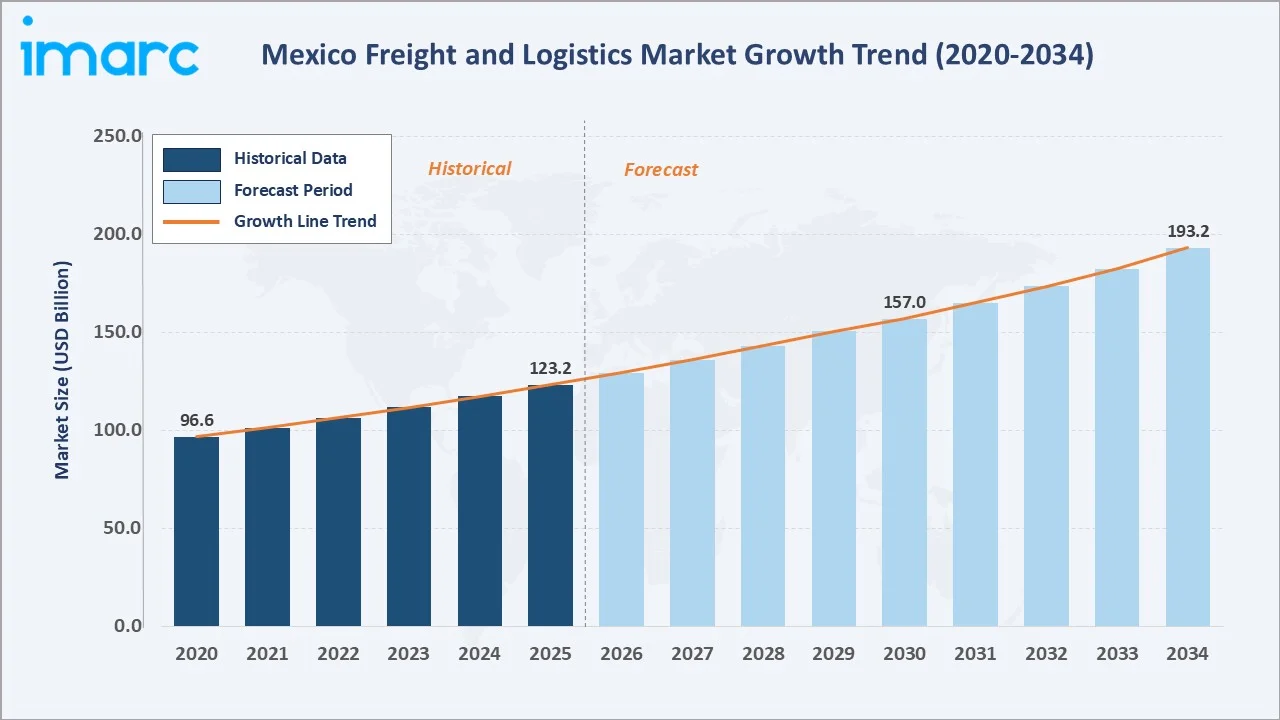

The Mexico freight and logistics market reached USD 123.2 Billion in 2025 and is projected to reach USD 193.2 Billion by 2034, growing at a CAGR of 4.98% during 2026-2034. The growth is driven by Mexico's strategic position as a key trade corridor connecting North and South America, expanding e-commerce activities, USMCA trade agreement benefits, and continuous infrastructure development initiatives.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 123.2 Billion |

|

Forecast Market Size (2034) |

USD 193.2 Billion |

|

CAGR (2026-2034) |

4.98% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Northern Mexico – 38.5% share (2025) |

|

Fastest Growing Segment |

E-commerce and Last-Mile Delivery |

To get more information on this market, Request Sample

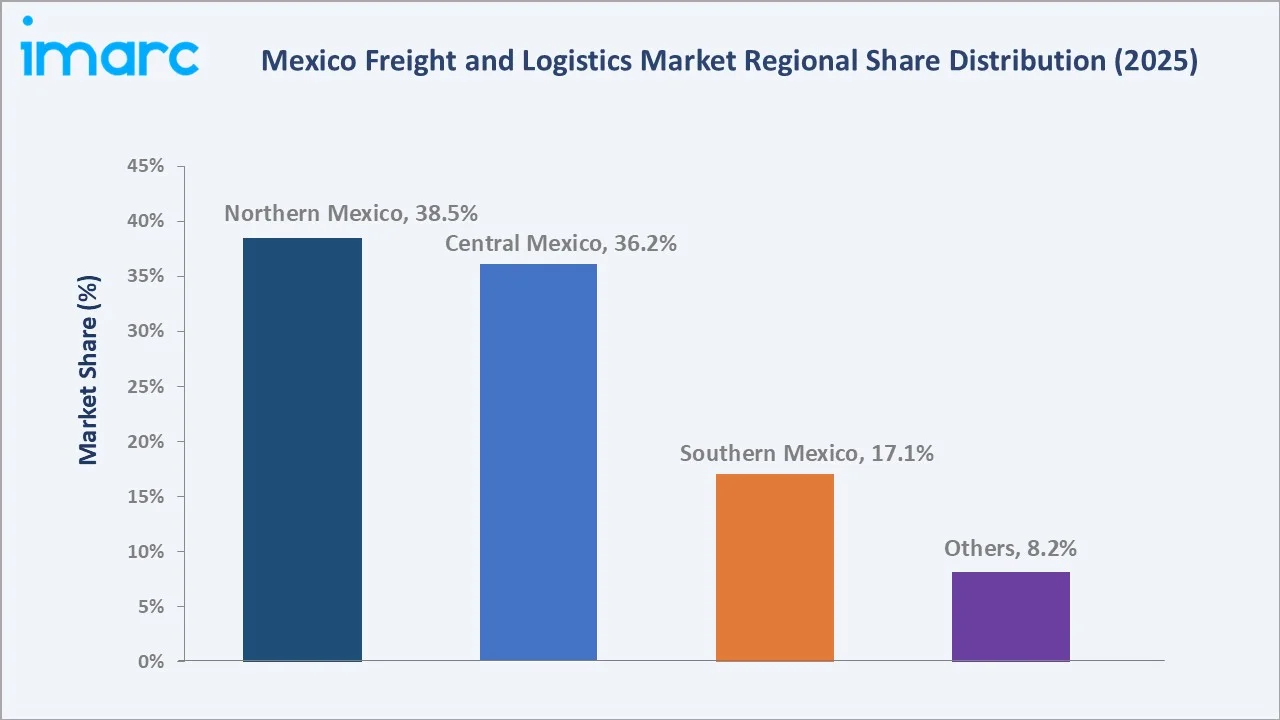

Northern Mexico dominates, holding a 38.5% share in 2025, driven by proximity to the U.S. border and extensive manufacturing activities. Freight transport accounts for 41.6% of the logistics function market, reflecting Mexico's position as a major transit corridor for international trade.

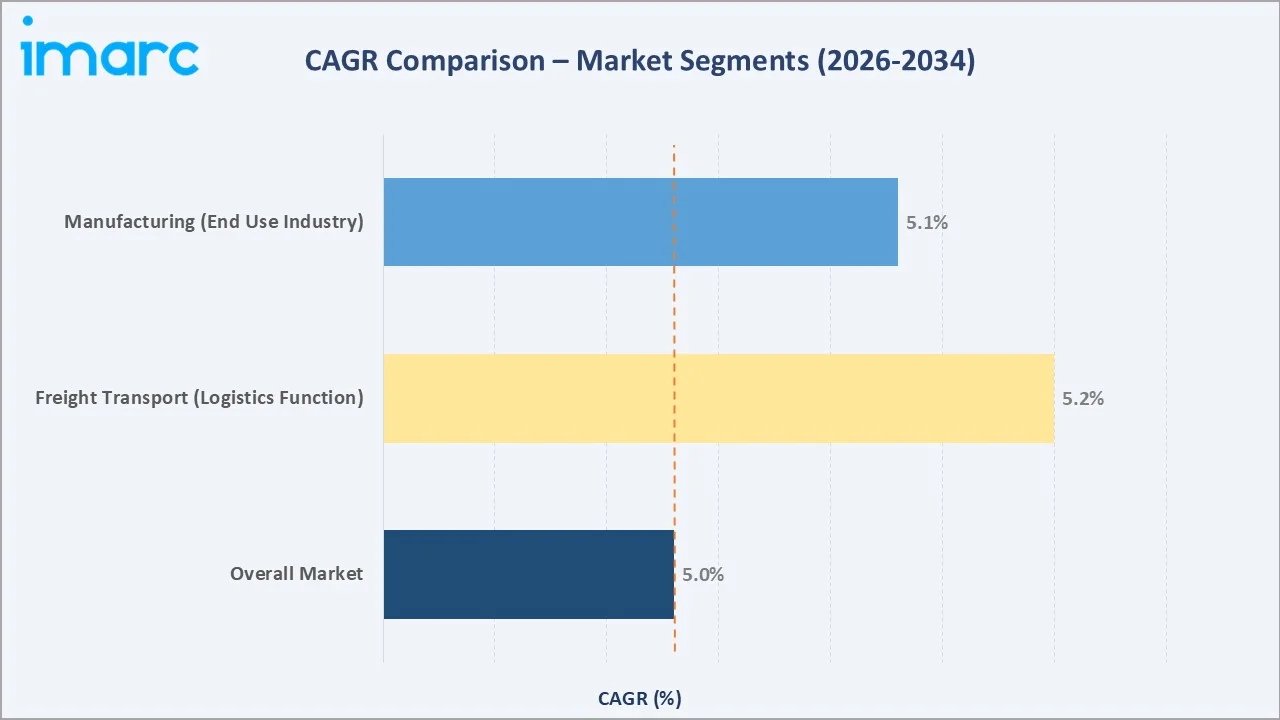

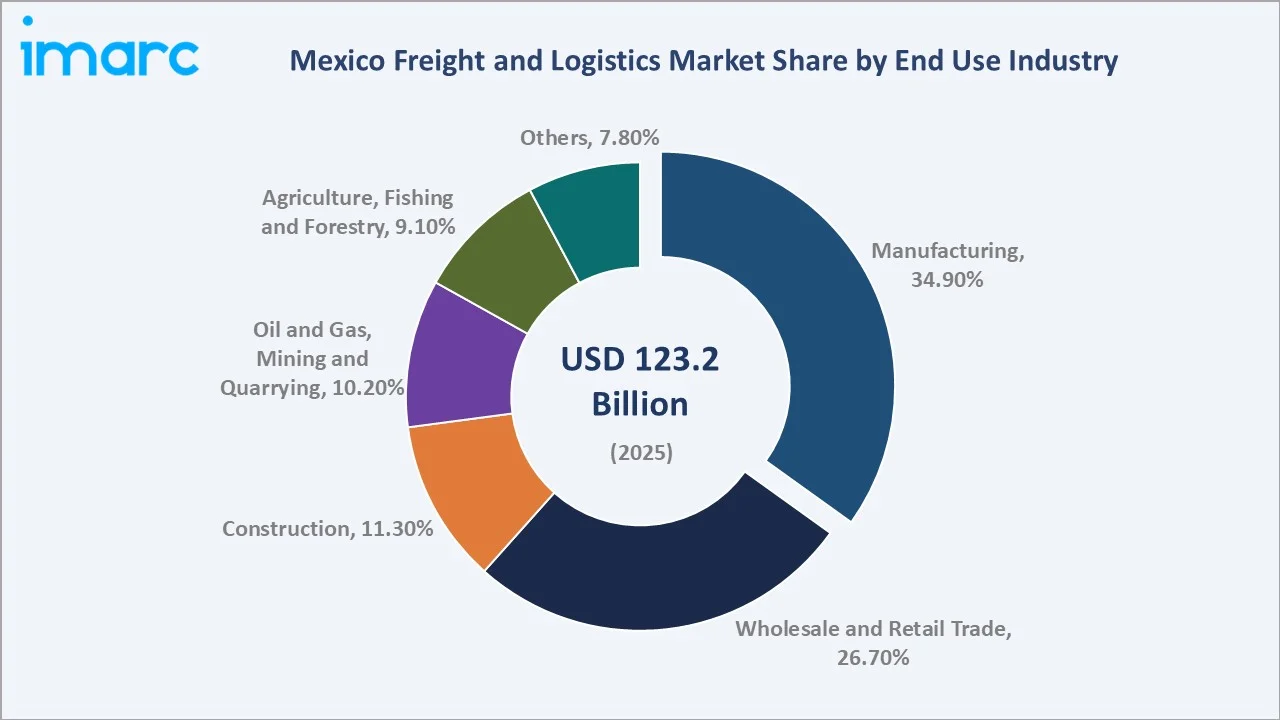

The market demonstrates strong growth momentum across all logistics functions, with freight transport leading at 41.6%, followed by warehousing and storage at 22.4% in 2025. Manufacturing represents the largest end-use industry segment at 34.9%, reflecting Mexico's robust industrial base and export-oriented economy.

Executive Summary

The Mexico freight and logistics market stands as one of Latin America's most dynamic and strategically important logistics hubs, driven by Mexico's unique geographical position, strong manufacturing base, and evolving trade relationships. The market reached USD 123.2 Billion in 2025 and is forecast to reach USD 193.2 Billion by 2034, reflecting a CAGR of 4.98% over the forecast period.

Northern Mexico leads geographically with 38.5% of the 2025 national market, benefiting from proximity to the U.S. border and concentration of maquiladora manufacturing facilities. Central Mexico follows with 36.2% market share, anchored by Mexico City as the primary distribution and commercial hub. Freight transport dominates the logistics function segment at 41.6%, supported by extensive road networks, cross-border trade volumes, and the country's role as a major transit corridor between North and South America.

Manufacturing leads end-use industry applications with 34.9% of the 2025 market, driven by automotive, electronics, and aerospace industries. The wholesale and retail trade segment follows at 26.7%, reflecting the growth of domestic consumption and e-commerce. Leading market participants include DHL International GmbH, FedEx, United Parcel Service of America, Inc., A.P. Moller - Maersk, C.H. Robinson Worldwide, Inc., alongside strong domestic players such as Estafeta Mexicana, S.A. DE C.V.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Logistics Function) |

Freight Transport – 41.6% share (2025) |

|

Largest Segment (End Use Industry) |

Manufacturing – 34.9% share (2025) |

|

Leading Region |

Northern Mexico – 38.5% revenue share (2025) |

|

Fastest Growing Trend |

E-commerce and Last-Mile Delivery Solutions |

|

Top Companies |

DHL International GmbH, FedEx, United Parcel Service of America, Inc., A.P. Moller - Maersk, C.H. Robinson Worldwide, Inc., and Estafeta Mexicana, S.A. DE C.V. |

|

Market Opportunity |

Cross-border trade facilitation and digital logistics platforms |

Key Analytical Observations Supporting The Above Data:

- Freight Transport dominates at 41.6% (2025), driven by Mexico's strategic position as a North-South America trade corridor, extensive cross-border commerce with the U.S., and the country's role in global supply chains for automotive and manufacturing industries.

- Manufacturing leads end-use applications at 34.9% (2025), reflecting Mexico's strong industrial base in automotive, electronics, aerospace, and textiles, supported by favorable trade agreements and competitive labor costs.

- Northern Mexico holds 38.5% of the national market (2025), anchored by border cities such as Tijuana, Ciudad Juárez, and Nuevo Laredo, which serve as critical trade gateways and manufacturing hubs.

- E-commerce growth is driving demand for last-mile delivery solutions, with companies investing in urban distribution centers, automated sorting facilities, and technology-enabled delivery platforms to meet consumer expectations.

- The USMCA trade agreement continues to strengthen Mexico's position as a preferred manufacturing and logistics destination, encouraging nearshoring trends and cross-border supply chain optimization.

Mexico Freight and Logistics Market Overview

The freight and logistics industry in Mexico encompasses the movement, storage, and management of goods across the country's diverse economic regions, serving both domestic consumption and international trade. The market includes freight transport (road, rail, air, and maritime), warehousing and storage, freight forwarding, and courier, express, and parcel services.

Market growth is supported by several structural advantages: proximity to the world's largest consumer market (U.S.), extensive bilateral trade relationships, competitive labor costs, and ongoing infrastructure development. The Mexico freight and logistics market forecast reflects positive trends in nearshoring, e-commerce expansion, digital transformation of logistics operations, and Mexico's integration into global value chains across automotive, electronics, aerospace, and consumer goods industries.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

- USMCA Trade Agreement Benefits: The United States-Mexico-Canada Agreement has strengthened trade relationships and reduced barriers, encouraging increased cross-border commerce. Mexico benefits from preferential access to North American markets, driving demand for logistics services supporting bilateral trade flows.

- E-commerce Growth Expansion: Mexico, with a 2024 e-commerce value of USD 97 billion, is the second-largest market in Latin America, following Brazil, according to PCMI proprietary data. This expansion requires sophisticated last-mile delivery networks, urban distribution centers, and technology-enabled logistics platforms.

- Manufacturing Sector Development: Foreign direct investment (FDI) in Mexico reached USD 40.9 billion in the third quarter of 2025, according to data from the Ministry of Economy, with manufacturing representing 37.1% of the total, highlighting its crucial role in the country’s economy.

- Infrastructure Investment Programs: Mexico's Infrastructure Investment Plan for 2026–2030 is set at MXN5.6 trillion (approximately USD325 billion), covering around 1,500 projects, with MXN722 billion allocated for 2026, poised to significantly enhance the country's freight and logistics market.

Market Restraints

- Regulatory Compliance Complexity: Complex and evolving regulatory frameworks for cross-border trade, customs procedures, and transportation safety create operational challenges and compliance costs for logistics providers, particularly affecting smaller companies with limited regulatory expertise.

- Security and Safety Concerns: Security issues in certain regions affect transportation routes and logistics operations, requiring additional security measures, route planning considerations, and insurance costs that can impact operational efficiency and profitability.

- Infrastructure Capacity Constraints: Despite ongoing investments, certain corridors and urban areas experience infrastructure bottlenecks, port congestion, and limited rail capacity that can restrict logistics efficiency and increase transportation costs.

Market Opportunities

- Digital Logistics Transformation: Technology adoption in transportation management, warehouse automation, and supply chain visibility creates opportunities for enhanced efficiency, cost reduction, and service quality improvements across the logistics value chain.

- Nearshoring and Reshoring Trends: Global supply chain diversification and nearshoring strategies position Mexico as a preferred manufacturing and logistics destination for companies seeking alternatives to Asian supply chains.

Market Challenges

- Skilled Workforce Development: In 2026, Mexico faces a structural talent gap, with 67% of employers finding it challenging to fill positions in logistics and technical roles. The industry requires continuous investment in workforce training and development to meet evolving technology requirements, regulatory compliance needs, and international service quality standards.

- Environmental Sustainability: Growing pressure for sustainable logistics operations requires investments in cleaner transportation technologies, energy-efficient warehouses, and carbon footprint reduction initiatives.

Emerging Market Trends

1. USMCA Implementation Driving Cross-Border Trade Optimization

North American trade surpassed USD 1.6 trillion, strengthening key sectors and enhancing labor conditions for millions of workers. Mexico’s exports rose by 4.3% in the first half of 2025. This has driven increased investment in border infrastructure, expedited customs processes, and integrated logistics platforms that facilitate seamless cross-border commerce. Logistics providers are developing specialized services for USMCA compliance, origin verification, and cross-border supply chain management.

2. Digital Transformation Accelerating Across Logistics Operations

Mexican logistics companies are rapidly adopting digital technologies, including transportation management systems (TMS), warehouse management systems (WMS), Internet of Things (IoT) tracking, and artificial intelligence for route optimization. This digital transformation is improving operational efficiency, enhancing customer visibility, and enabling data-driven decision-making.

3. Green Logistics and Sustainability Focus

Mexican electric mobility firm VEMO has unveiled an investment plan of over US$1.5 billion for the next five years, focused on expanding its public and private charging infrastructure, enhancing its operations, and growing its electric vehicle fleet. This strategic investment in electric mobility and infrastructure further strengthens Mexico's freight and logistics market, driving sustainability and efficiency in the transportation sector.

4. Automation and AI Integration Expansion

Warehouse automation, robotics, and artificial intelligence are gaining adoption in Mexico's logistics sector, particularly in high-volume facilities serving automotive, e-commerce, and manufacturing clients. Companies are implementing automated sorting systems, robotic picking solutions, and predictive analytics to enhance operational efficiency and service quality while addressing labor availability challenges in major metropolitan areas.

Industry Value Chain Analysis

The Mexico freight and logistics value chain encompasses raw materials sourcing through final delivery to end consumers, with each stage contributing to supply chain efficiency and economic value creation.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Agricultural products, manufactured goods, natural resources, import/export commodities |

|

Transportation Providers |

Freight carriers, shipping lines, railway companies, trucking fleets, air cargo operators |

|

Logistics Services |

DHL International GmbH, FedEx, United Parcel Service of America, Inc., A.P. Moller - Maersk, C.H. Robinson Worldwide, Inc., and Estafeta Mexicana, S.A. DE C.V. |

|

Infrastructure Facilities |

Ports (Veracruz, Manzanillo), airports, warehouses, distribution centers, cross-border facilities |

|

Technology & Systems |

TMS platforms, WMS systems, tracking solutions, customs software, digital platforms |

|

End Users |

Manufacturing, wholesale and retail trade, construction, oil and gas, agriculture and forestry |

Technology Landscape in Mexico Freight and Logistics Industry

Transportation Management Systems and Digital Platforms

Modern logistics operations in Mexico increasingly rely on sophisticated TMS platforms that optimize route planning, load matching, and fleet management. In September 2025, Freight Technologies strengthened its collaboration with Amazon Mexico by directly integrating its Fr8App platform with Amazon’s internal tracking system, enhancing real-time visibility and operational oversight for logistics operations.

Warehouse Automation and Robotics

In December 2025, DHL Supply Chain entered a five‑year strategic alliance with robotics firm Robust.AI to accelerate logistics automation in Mexico, beginning with the deployment of 15 collaborative Carter robots in its retail operations. These investments improve accuracy, reduce labor dependency, and increase throughput capacity.

IoT and Real-Time Tracking Technologies

Internet of Things sensors and GPS tracking systems provide comprehensive visibility across transportation networks, enabling real-time monitoring of shipment location, condition, and estimated arrival times. Advanced tracking solutions monitor temperature, humidity, and security for sensitive cargo, while providing predictive analytics for maintenance and route optimization.

Artificial Intelligence and Machine Learning Applications

According to a McKinsey survey, businesses experience a revenue boost of over 5% when incorporating AI into supply chain and inventory management. Mexican logistics companies are leveraging these technologies to improve operational efficiency, reduce costs, and enhance customer service through better demand planning and proactive issue resolution.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Logistics Function |

Freight Transport |

41.6% |

2025 |

|

End Use Industry |

Manufacturing |

34.9% |

2025 |

|

Region |

Northern Mexico |

38.5% |

2025 |

By Logistics Function

To access detailed market analysis, Request Sample

Freight transport dominates the Mexico freight and logistics market with a 41.6% share in 2025. This segment includes road transport (the largest component), rail transport, air cargo, and maritime shipping. Road transport leads due to Mexico's extensive highway network, flexibility for door-to-door delivery, and the country's role as a major cross-border trade corridor with the United States.

Warehousing and storage represents 22.4% of the market, valued at approximately USD 27.6 Billion, driven by e-commerce growth, manufacturing expansion, and the need for strategic inventory positioning. Freight forwarding accounts for 14.8% (USD 18.2 Billion), reflecting Mexico's international trade volumes and the complexity of cross-border logistics. Courier, express, and parcel services hold 13.2% (USD 16.3 Billion), growing rapidly due to e-commerce expansion and consumer expectations for fast delivery.

By End Use Industry

Manufacturing leads the Mexico freight and logistics market with a 34.9% share in 2025, representing approximately USD 43.0 Billion. This dominance reflects Mexico's strong industrial base in automotive, electronics, aerospace, textiles, and food processing. The manufacturing sector drives demand for inbound raw materials logistics, production support services, and outbound finished goods distribution to domestic and export markets.

Wholesale and retail trade commands 26.7% of the market, equivalent to approximately USD 32.9 Billion, driven by domestic consumption growth, retail expansion, and e-commerce development. Construction represents 11.3% (USD 13.9 Billion), supported by infrastructure development projects and urban growth. Oil and gas, mining, and quarrying account for 10.2% (USD 12.6 Billion), reflecting Mexico's energy sector and natural resource extraction activities.

Regional Market Insights

Northern Mexico's market leadership (38.5%, 2025) stems from its strategic location along the U.S.-Mexico border, concentration of maquiladora manufacturing facilities, and role as the primary gateway for bilateral trade. Key border cities, including Tijuana, Ciudad Juárez, Nuevo Laredo, and Reynosa, serve as critical logistics hubs with extensive cross-border infrastructure and specialized trade facilitation services.

|

Region |

Share (2025) |

Key Growth Drivers |

Primary Industries |

Growth Outlook |

|

Northern Mexico |

38.5% |

U.S. border proximity, maquiladora manufacturing, cross-border trade |

Automotive, electronics, aerospace |

Continued leadership |

|

Central Mexico |

36.2% |

Mexico City hub, domestic consumption, and distribution centers |

Manufacturing, retail, services |

Steady growth |

|

Southern Mexico |

17.1% |

Agricultural exports, tourism, and port infrastructure development |

Agriculture, tourism, energy |

Moderate expansion |

|

Others |

8.2% |

Regional manufacturing, resource extraction, and emerging markets |

Mining, agriculture, and local trade |

Gradual development |

Central Mexico, representing 36.2% of the 2025 national market, is anchored by Mexico City as the country's primary commercial and distribution hub. The region serves as the logistics nerve center for domestic consumption, with extensive warehouse networks, transportation infrastructure, and the largest concentration of consumers. Major distribution centers in the State of Mexico and surrounding areas serve both domestic retail and e-commerce markets.

Competitive Landscape

The leading companies command significant market presence through comprehensive service offerings, extensive infrastructure networks, and strategic partnerships. The competitive landscape is characterized by ongoing consolidation, technology investments, and expansion into emerging market segments such as e-commerce logistics and cross-border trade facilitation.

|

Company Name |

Key Services |

Market Position |

Core Strength |

|

DHL International GmbH |

Express, Supply Chain, Global Forwarding |

Market Leader |

Global network; technology leadership; comprehensive service portfolio |

|

FedEx |

Express, Freight, Supply Chain |

Strong Challenger |

Express delivery excellence; technology innovation; cross-border expertise |

|

United Parcel Service of America, Inc. |

Package, Freight, Supply Chain |

Major Player |

Integrated logistics solutions; ground network; supply chain capabilities |

|

A.P. Moller - Maersk |

Ocean, Logistics, Terminals |

Maritime Leader |

Ocean freight leadership; port operations; integrated logistics |

|

C.H. Robinson Worldwide, Inc. |

Transportation, Logistics |

Technology Leader |

Digital platform excellence; freight brokerage; supply chain optimization |

|

Estafeta Mexicana, S.A. de C.V.

|

Domestic Parcel, Logistics |

Domestic Leader |

Local market knowledge; domestic network; last-mile capabilities |

Key Company Profiles

DHL International GmbH

DHL International GmbH. maintains market leadership in Mexico's logistics sector through its comprehensive service portfolio spanning express delivery, supply chain solutions, and global forwarding. The company operates extensive infrastructure, including sortation facilities, distribution centers, and technology platforms that support both domestic and international logistics requirements.

- Service Portfolio: DHL Express for time-critical shipments; DHL Supply Chain for warehousing and distribution; DHL Global Forwarding for air and ocean freight.

- Recent Developments: In December 2024, DHL Express Mexico invested MXN 1.1 billion in fleet expansion and airport operation upgrades to enhance service capacity and efficiency.

- Strategic Focus: Technology leadership; sustainable logistics solutions; e-commerce and cross-border trade support; automation and digitalization of operations.

FedEx

FedEx operates as a major logistics provider in Mexico through its integrated network of express, freight, and supply chain services. The company leverages advanced technology platforms and extensive transportation infrastructure to serve diverse customer requirements across Mexico's key economic regions.

- Service Portfolio: FedEx Express for international and domestic express delivery; FedEx Freight for less-than-truckload services; FedEx Supply Chain for logistics solutions.

- Recent Developments: FedEx has expanded its Mexican operations with investments in technology-driven logistics solutions and enhanced customs compliance capabilities for cross-border trade.

- Strategic Focus: Express delivery leadership; technology innovation; cross-border trade facilitation; supply chain optimization for manufacturing clients.

A.P. Moller - Maersk

A.P. Moller - Maersk operates as a leading provider of ocean freight and integrated logistics services in Mexico, leveraging its global shipping network and local logistics infrastructure. The company serves Mexico's import/export trade flows and provides end-to-end supply chain solutions for manufacturing and retail clients.

- Service Portfolio: Ocean freight services; container shipping; port and terminal operations; inland transportation and logistics.

- Recent Developments: In March 2024, Maersk opened a new 30,000 m² warehouse in Tijuana, strategically located near the Otay border crossing to serve technology and retail clients.

- Strategic Focus: Ocean freight leadership; integrated logistics solutions; port and terminal operations; digital supply chain platforms.

Market Concentration Analysis

The Mexico freight and logistics market demonstrates moderate fragmentation, with the top five companies accounting for an estimated 35-45% of the formal market revenue in 2025. Market structure varies by segment, with express delivery and air freight showing higher concentration among global integrators, while ground transportation and warehousing remain more fragmented across numerous regional and local providers.

Competitive dynamics favor companies with strong technology platforms, comprehensive service portfolios, and a deep understanding of Mexican regulatory and operational requirements. The market continues to consolidate as companies seek scale economies, expanded geographic coverage, and enhanced service capabilities to meet evolving customer demands for integrated logistics solutions.

Investment & Growth Opportunities

High-Growth Market Segments

E-commerce and last-mile delivery (~8-12% CAGR), cross-border trade facilitation (~6-8% CAGR), and warehouse automation (~10-15% CAGR) represent the highest-growth investment opportunities through 2034. These segments address evolving consumer expectations, trade facilitation requirements, and operational efficiency demands, creating incremental revenue potential of approximately USD 25-35 Billion by 2034.

Geographic Expansion Opportunities

Secondary markets, including Puebla, Guadalajara, Querétaro, and Mérida, offer significant growth potential as manufacturing activities expand beyond traditional borders and central regions. Investment opportunities exist in developing regional distribution networks, specialized logistics facilities, and technology-enabled service platforms for emerging markets.

Technology and Innovation Investment

- Warehouse automation and robotics adoption present opportunities for operational efficiency improvements, particularly in high-volume e-commerce and manufacturing support facilities.

- Digital logistics platforms, artificial intelligence applications, and IoT integration offer competitive advantages through enhanced visibility, optimization, and customer service capabilities.

- Sustainable logistics technologies, including electric vehicles, renewable energy systems, and carbon management platforms, align with environmental regulations and customer sustainability requirements.

Future Market Outlook (2026-2034)

The Mexico freight and logistics market is forecast to reach USD 193.2 Billion by 2034 at a CAGR of 4.98%, positioning Mexico as one of the Western Hemisphere's most important logistics hubs. Growth will be driven by continued nearshoring trends, e-commerce expansion, infrastructure development, and Mexico's integration into North American and global value chains.

Market evolution will favor companies that successfully combine global reach with local expertise, invest in technology-enabled service platforms, and develop sustainable logistics operations. The integration of artificial intelligence, automation, and digital platforms will become essential for competitive differentiation, while environmental sustainability will emerge as a key customer requirement. The Mexico freight and logistics market growth trajectory reflects the country's strategic importance in global trade flows and its continued development as a preferred destination for manufacturing and logistics operations serving both domestic and international markets.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 120 industry participants in 2024–2025, including logistics service providers, freight forwarders, transportation companies, warehouse operators, technology vendors, and corporate logistics managers across Mexico's key economic regions.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, government trade statistics, industry association publications, logistics technology reports, and academic studies. Key sources include INEGI transportation data, Mexican logistics association reports, customs administration statistics, and international logistics industry publications. Over 200 secondary sources were reviewed and validated.

Forecasting Models

Market size estimations and growth projections employed econometric modeling incorporating macroeconomic indicators (GDP growth, trade volumes, industrial production), demographic factors (urbanization, e-commerce adoption), and industry-specific drivers (infrastructure investment, technology adoption). The base-case CAGR of 4.98% reflects Mexico's economic growth trajectory and logistics industry development trends.

Mexico Freight and Logistics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Logistics Functions Covered |

|

| End Use Industries Covered | Agriculture, Fishing and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, Others |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Companies Covered | DHL International GmbH, FedEx, United Parcel Service of America, Inc., A.P. Moller - Maersk, C.H. Robinson Worldwide, Inc. , Estafeta Mexicana, S.A. de C.V., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico freight and logistics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico freight and logistics market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico freight and logistics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mexico Freight and Logistics Market Report

The Mexico freight and logistics market reached USD 123.2 Billion in 2025, representing consistent expansion driven by trade growth, manufacturing development, infrastructure investment, and e-commerce expansion across Mexico's key economic regions.

The Mexico freight and logistics market is expected to grow at a CAGR of 4.98% during the forecast period from 2026 to 2034, supported by Mexico's strategic position in North American trade, continued manufacturing expansion, infrastructure development, and growing domestic consumption driven by e-commerce and retail growth.

The Mexico freight and logistics market is projected to reach USD 193.2 Billion by 2034, representing a 57% increase from the 2025 base. This growth reflects Mexico's continued integration into global value chains, nearshoring trends, infrastructure development, and the maturation of e-commerce and digital logistics platforms.

Northern Mexico leads the market with a 38.5% revenue share in 2025, driven by proximity to the U.S. border, concentration of maquiladora manufacturing facilities, and role as the primary gateway for bilateral trade. Key border cities, including Tijuana, Ciudad Juárez, and Nuevo Laredo, serve as critical logistics and trade facilitation hubs.

E-commerce and last-mile delivery represent the fastest-growing market segment, driven by Mexico's rapidly expanding digital commerce market, changing consumer expectations for delivery speed and convenience, and investments in urban distribution infrastructure and technology-enabled delivery platforms across major metropolitan areas.

Freight transport dominates with a 41.6% share of the logistics function market in 2025, valued at approximately USD 51.3 Billion. This dominance reflects Mexico's role as a major trade corridor, extensive road transportation networks, cross-border commerce volumes, and the country's position in North American supply chains.

The manufacturing sector holds the largest share at 34.9% in 2025 (approx. USD 43.0 Billion), driven by Mexico's strong industrial base in automotive, electronics, aerospace, textiles, and food processing. The sector benefits from favorable trade agreements, competitive costs, and strategic geographic positioning for serving both domestic and export markets.

Key players include DHL International GmbH, FedEx, United Parcel Service of America, Inc., A.P. Moller - Maersk, C.H. Robinson Worldwide, Inc., and Estafeta Mexicana, S.A. DE C.V. These companies compete through comprehensive service portfolios, technology platforms, and strategic infrastructure investments.

Major growth drivers include USMCA trade agreement benefits, enhancing cross-border commerce, rapid e-commerce expansion requiring sophisticated distribution networks, continued manufacturing sector development.

Significant opportunities exist in e-commerce and last-mile delivery infrastructure, cross-border trade facilitation services, warehouse automation and robotics, digital logistics platforms and technology solutions, sustainable transportation systems, and geographic expansion into secondary markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)