A2 Milk Market Size, Share, Trends and Forecast by End-Use, Distribution Channel, and Region, 2026-2034

Global A2 Milk Market Size, Share, Trends & Forecast (2026-2034)

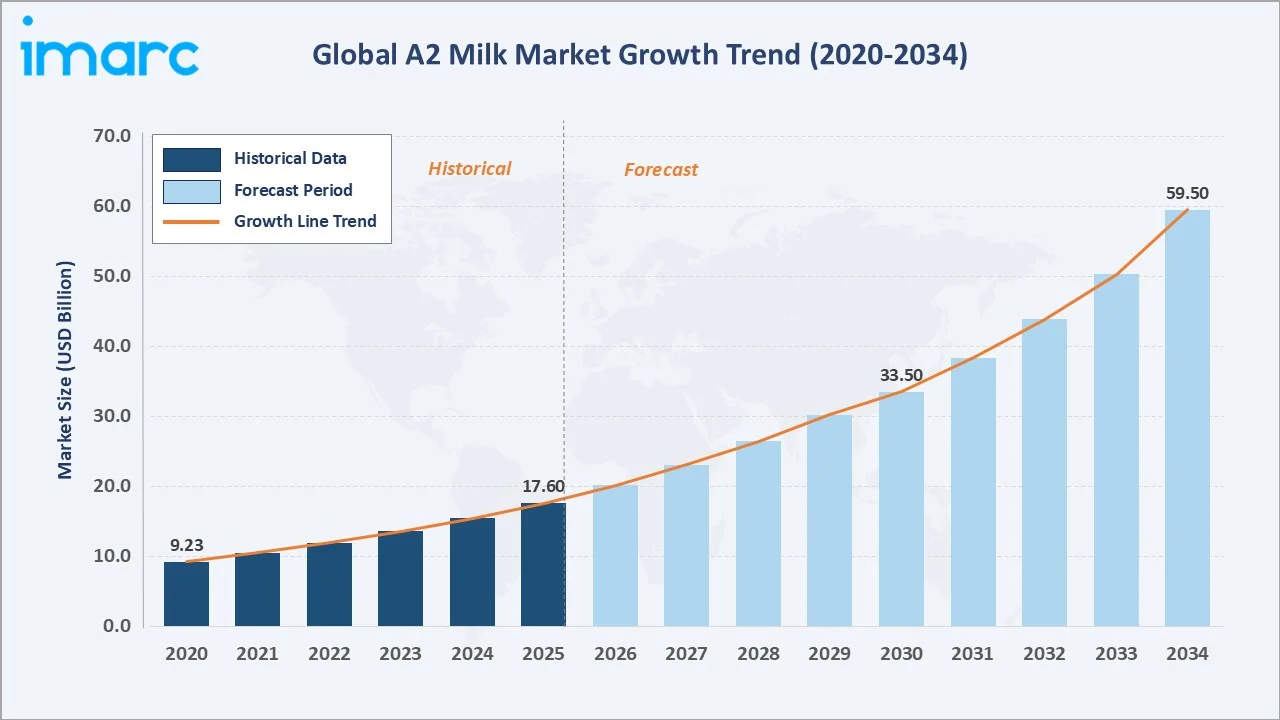

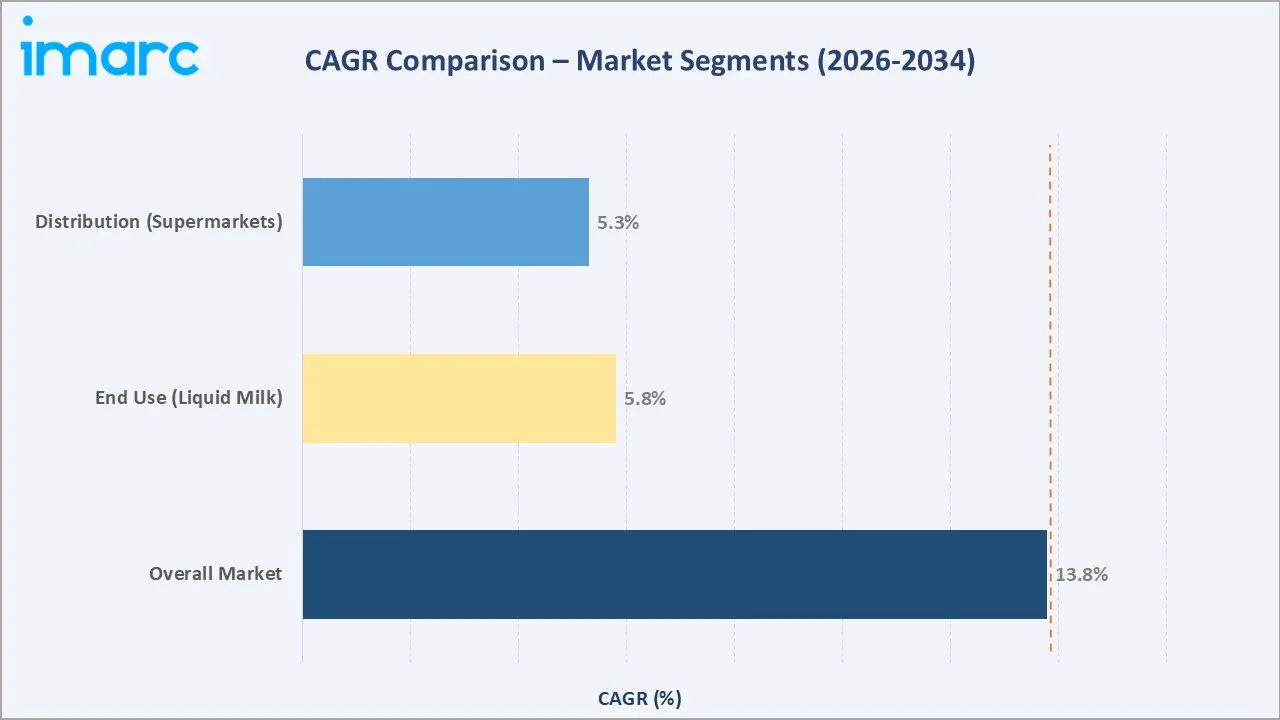

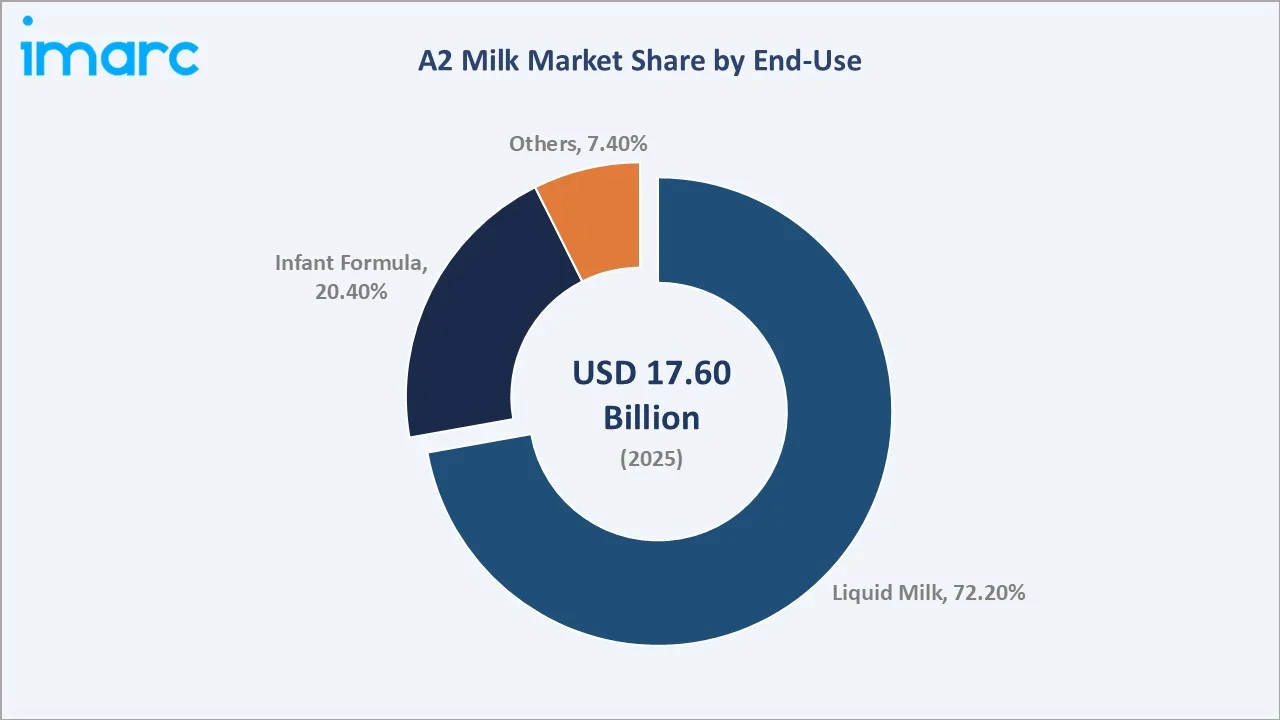

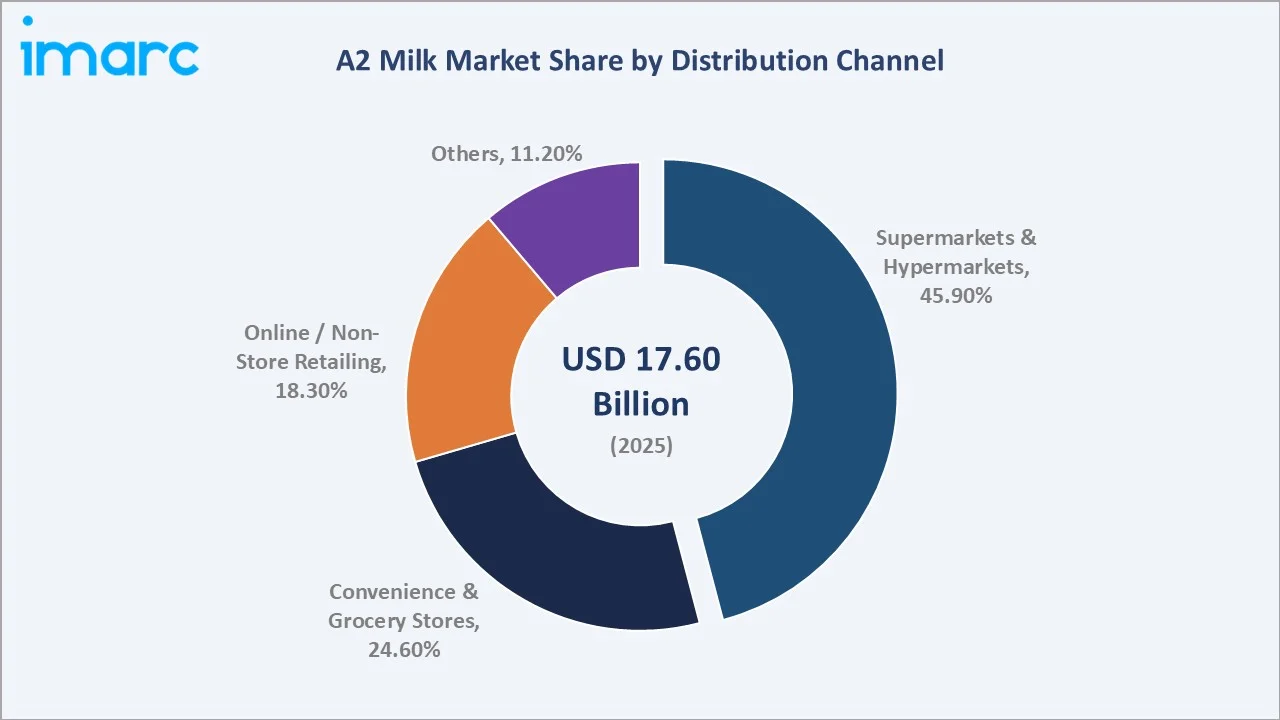

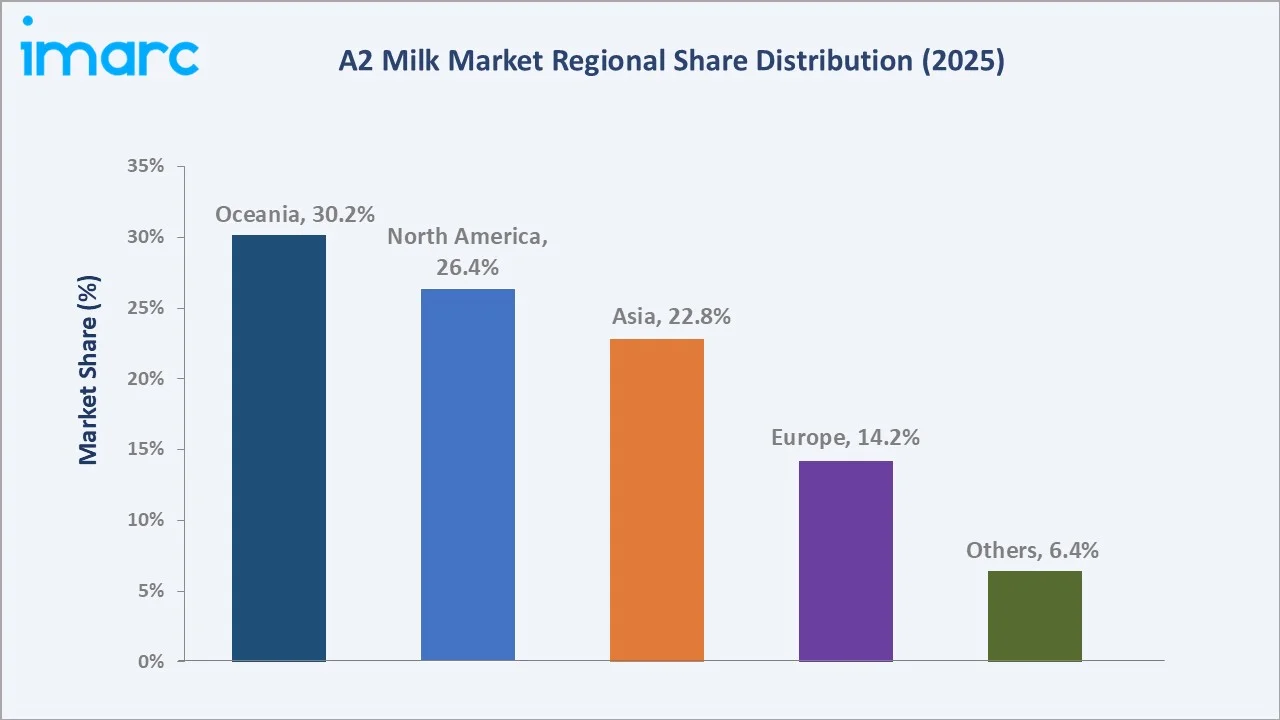

The global A2 milk market was valued at USD 17.6 Billion in 2025. It is projected to reach USD 59.5 Billion by 2034, expanding at a CAGR of 13.77% during the forecast period (2026-2034). Rising consumer awareness about digestive health, growing prevalence of lifestyle diseases, and rapid expansion into new dairy categories are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 17.6 Billion |

|

Forecast Market Size (2034) |

USD 59.5 Billion |

|

CAGR (2026-2034) |

13.77% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Oceania (30.2% share, 2025) |

|

Fastest Growing Region |

Asia (est. CAGR ~15.8%, 2026-2034) |

A2 milk is derived from cows that produce only the A2 beta-casein protein, as opposed to the more common A1 protein found in conventional milk. This difference has led to claims that A2 milk is easier to digest and less likely to cause digestive discomfort, making it appealing to individuals with lactose intolerance or sensitivity to A1 protein.

To get more information on this market, Request Sample

Oceania leads all regions with a 30.2% share (2025), while liquid milk dominates the end-use mix at 72.2%. Post-pandemic shifts toward health-conscious consumption and heightened awareness of digestive wellness significantly accelerated A2 milk adoption in mainstream retail channels worldwide.

The A2 milk market has witnessed steady growth due to increasing consumer awareness of its potential health benefits over regular milk. A2 milk, which contains only the A2 beta-casein protein, is believed to be easier to digest and less likely to cause digestive discomfort compared to the more common A1 protein found in conventional milk. This has made A2 milk a popular alternative, particularly for individuals with lactose intolerance or sensitivity to A1 protein.

Executive Summary

The global A2 milk market is in a high-growth phase, underpinned by converging trends in functional food demand, gut health awareness, and premium dairy adoption. The market registered USD 9.23 Billion in 2020 and accelerated to USD 17.6 Billion by 2025, reflecting a near-doubling of value within five years. The market is forecast to reach USD 59.5 Billion by 2034, adding over USD 42 Billion in incremental market value during the forecast period.

Liquid milk dominates end-use with a 72.2% share (2025), driven by everyday household consumption and its role in beverages across cafes and foodservice. Infant formula commands 20.4%, supported by parental preference for A2 beta-casein's gentler protein profile. Supermarkets and hypermarkets lead distribution channel at 45.9% (2025), enabled by dedicated specialty dairy sections and in-store promotional activity.

Oceania leads regionally with a 30.2% revenue share (2025), anchored by advanced A2 breeding programs and efficient export supply chains. North America holds 26.4%, supported by strong functional dairy demand, while Asia at 22.8% is the fastest-growing region owing to China and India's expanding premium dairy consumption base.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (End-Use) |

Liquid Milk - 72.2% share (2025) |

|

Second Segment (End-Use) |

Infant Formula - 20.4% share (2025) |

|

Largest Distribution Channel |

Supermarkets & Hypermarkets - 45.9% share (2025) |

|

Fastest Growing Channel |

Online/Non-store Retailing - est. CAGR ~18.2% (2026-2034) |

|

Leading Region |

Oceania - 30.2% revenue share (2025) |

|

Fastest Growing Region |

Asia - est. CAGR ~15.8% (2026-2034) |

|

Top Companies |

The a2 Milk Company Limited, Bega Dairy & Drinks, Lactalis Group, Gujarat Cooperative Milk Marketing Federation (Amul), Noumi Limited, Organic Valley, and Provilac Dairy Farms |

Key Analytical Observations Supporting The Above Data:

- Liquid milk holds 72.2% (2025) as the dominant end-use segment, driven by its universal household appeal, ready-to-consume format, and accelerating adoption among lactose-sensitive consumers seeking easier-to-digest dairy alternatives.

- Infant formula captures 20.4% (2025), with A2-based formulas commanding premium pricing of 20-35% above conventional alternatives. Parental demand for clean-label, digestive-friendly infant nutrition is the primary demand driver.

- Supermarkets and hypermarkets lead distribution channel at 45.9% (2025), leveraging dedicated specialty dairy aisles, sampling events, and shelf-prominence strategies to build consumer trials and repeat purchase frequency.

- Oceania's 30.2% regional share (2025) is anchored by New Zealand and Australia's long-established A2 dairy infrastructure, where approximately 10% of the national dairy herd is certified A2-only as of 2024.

- Asia's 22.8% share is projected to surpass North America's by 2030, with China's liquid milk imports totaling 437,800 tons, marking a 4.2% decrease compared to the previous year. The import value reached 994 million U.S. dollars, reflecting a 5.7% year-on-year increase.

Global A2 Milk Market Overview

A2 milk is a distinct category of cow's milk that contains only A2 beta-casein protein, unlike conventional milk, which contains both A1 and A2 variants. The A1 protein is associated with digestive discomfort in some consumers, making A2 milk a preferred alternative for those with milk sensitivities.

The A2 milk category has transitioned from a niche health product to a mainstream premium dairy segment within a decade. The growing lactose intolerance market, valued at USD 11.37 Billion in 2024 and projected to reach USD 22.18 Billion by 2035 (CAGR 6.27%, 2025-2035), creates a structural demand base for A2 milk as a perceived digestive solution.

Approximately 68% of the global adult population experiences some degree of lactose malabsorption, according to the National Institutes of Health (2024). A2 milk brands are strategically positioning their products at the intersection of clean-label, nutritional density, and digestive wellness, three of the fastest-growing consumer purchase drivers in the post-pandemic food landscape.

Market Dynamics

To evaluate market opportunities, Request Sample

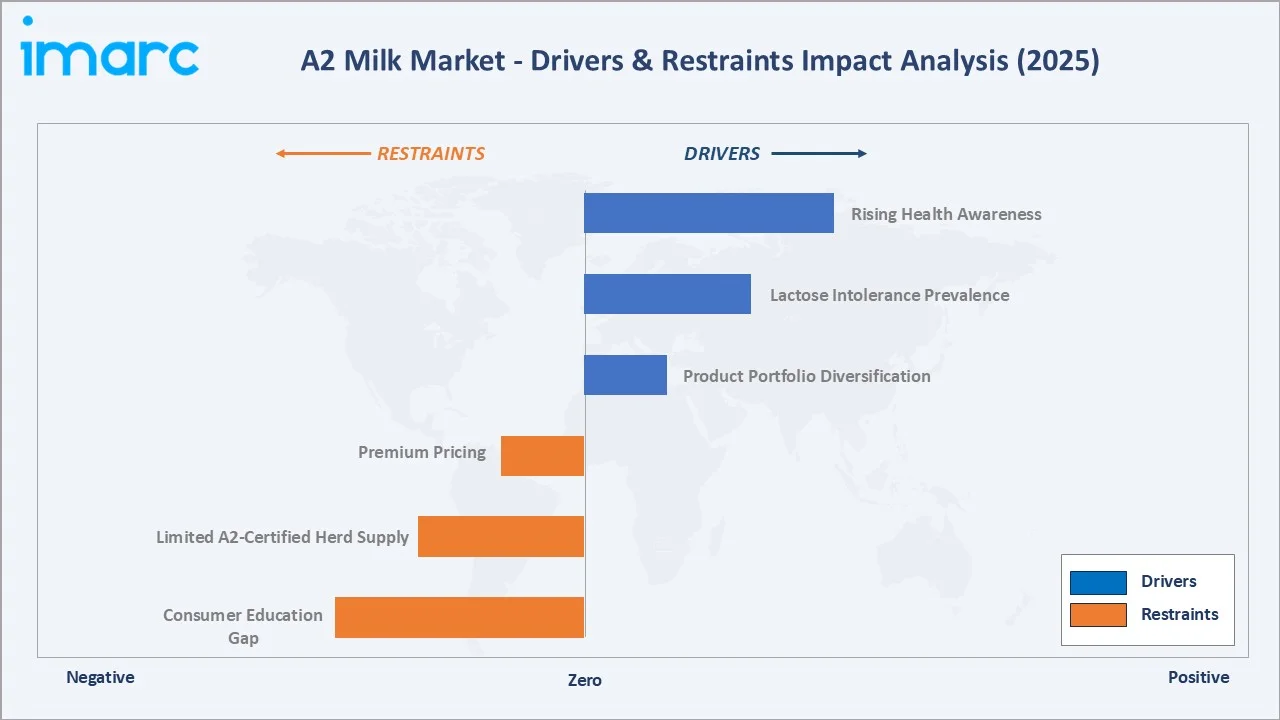

Market Drivers

- Rising Health Awareness: An analysis of A2 milk consumption patterns in Bengaluru, Karnataka, reveals moderate awareness of its health benefits, with 57.5% of respondents demonstrating a medium level of awareness.

- Lactose Intolerance Prevalence: Lactose intolerance is notably more common, affecting 50% to 80% of South Americans, 60% to 80% of Ashkenazi Jews and Western Africans, and nearly 100% of American Indians and certain East Asian populations. A2 milk's positioning as an easier-to-digest dairy alternative is generating rapid category switching from conventional milk.

- Product Portfolio Diversification: Expansion of A2 milk beyond liquid formats into infant formula, yogurt, cheese, and butter increases the addressable market by 40-50%. New SKU launches in A2-based functional dairy grew 28% globally in 2023.

These drivers collectively reinforce a sustained growth trajectory. Health awareness catalyzes initial trial, retail expansion drives accessibility, and product diversification builds loyalty across multiple consumption occasions throughout the day.

Market Restraints

- Premium Pricing: A2 milk products typically command a 20-50% price premium over conventional milk. In price-sensitive markets across Southeast Asia and Latin America, this premium restricts mass-market penetration and limits growth velocity.

- Limited A2-Certified Herd Supply: Specialized A2 dairy breeding programs require significant capital investment. Certifying a dairy herd as A2-only takes up to 10 years, creating meaningful supply constraints during peak demand periods.

- Consumer Education Gap: A common misconception is that A2 milk is lactose-free, but it actually contains the same amount of lactose as regular milk. The difference lies in the protein content, not the sugar. A2 milk contains A2 beta-casein protein, which is easier to digest compared to A1 protein.

Market Opportunities

- Emerging Market Expansion: Asia-Pacific and the Middle East represent an incremental addressable market of approximately USD 24 Billion by 2034. India's A2 milk segment is expected to grow at 19.2% CAGR (2026-2034), driven by indigenous A2 cow breed awareness.

- A2 Infant Formula Growth: The global infant formula market is projected to reach USD 103 Billion by 2030. A2-based infant formulas represent a high-growth sub-segment, with premium positioning and clinical claims supporting significant market share capture.

Market Challenges

- Regulatory Heterogeneity: Regulatory frameworks for A2 protein claims vary significantly across markets. The US FDA, EU EFSA, and FSSAI (India) have differing requirements for health claims on A2 milk packaging, increasing compliance complexity.

- Cold Chain Logistics Costs: Maintaining cold chain integrity across extended international export routes, particularly from Oceania to Asia, adds 10-15% to distribution costs versus domestic dairy logistics, pressuring margin structures.

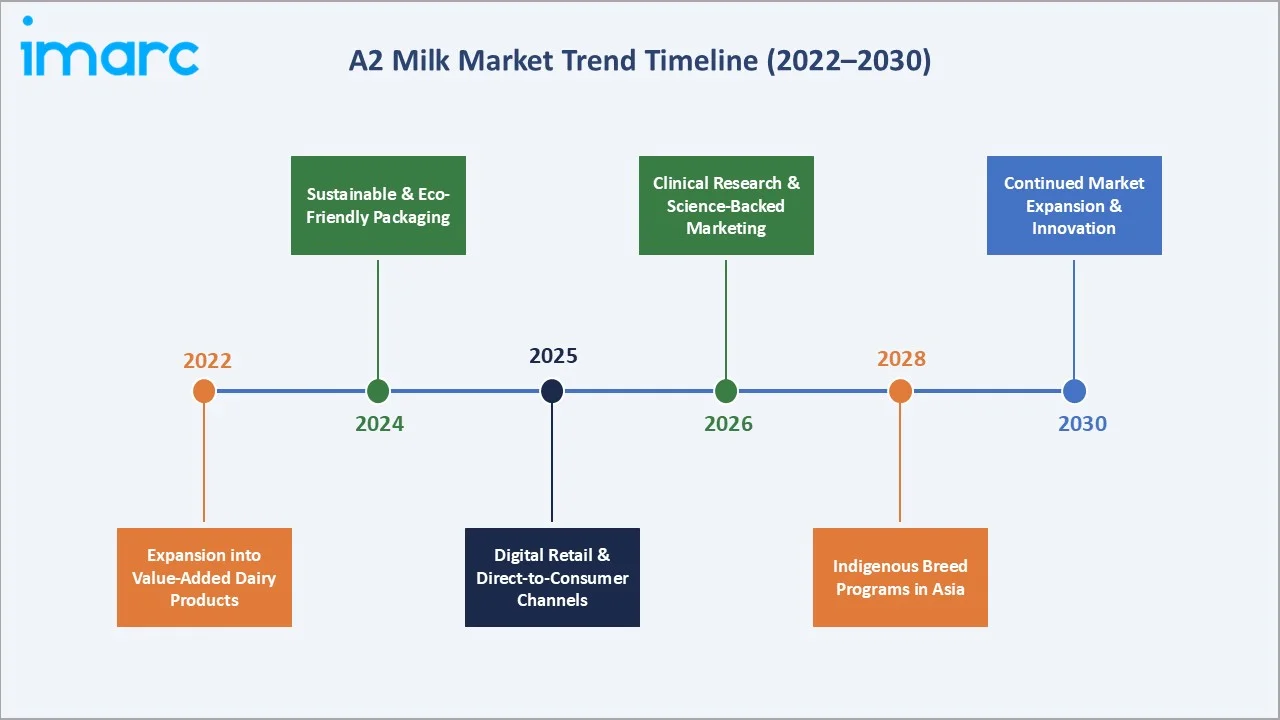

Emerging Market Trends

1. Expansion into Value-Added Dairy Products

A2 milk producers are extending their portfolios beyond liquid milk. A2-based infant formula is the fastest-growing sub-category, registering a CAGR of approximately 15.8% (2026-2034). Products such as A2 ghee, yogurt, and cheese are experiencing high annual growth in specialty retail across North America and Europe.

2. Sustainable and Eco-Friendly Packaging

Sustainability is becoming a key competitive differentiator. In 2024, Farmery launched A2 cow milk in eco-friendly glass bottles, sourced from indigenous breeds and delivered fresh within 12 hours of milking.

3. Digital Retail and Direct-to-Consumer Channels

Online/non-store retailing is the fastest-growing distribution channel at an estimated CAGR of 18.2% (2026-2034). Subscription-based A2 milk delivery models are gaining traction in the US, UK, Australia, and China, with average order values 28% higher than single-purchase transactions.

4. Clinical Research and Science-Backed Marketing

Increasing investment in peer-reviewed clinical trials is enabling A2 brands to substantiate digestive comfort claims with scientific evidence. Over 42 clinical studies on A2 beta-casein were published between 2022 and 2024, supporting regulatory approval for health claims in Australia, New Zealand, and South Korea.

5. Indigenous Breed Programs in Asia

India's emphasis on indigenous A2 cow breeds such as Gir and Sahiwal has created a unique domestic A2 supply chain. The Department of Animal Husbandry and Dairying, Government of India, realigned a budget of Rs. 1,790 crore in July 2021, divided into two components: improving milk testing and chilling infrastructure (Component A) and upgrading dairy facilities through cooperatives (Component B).

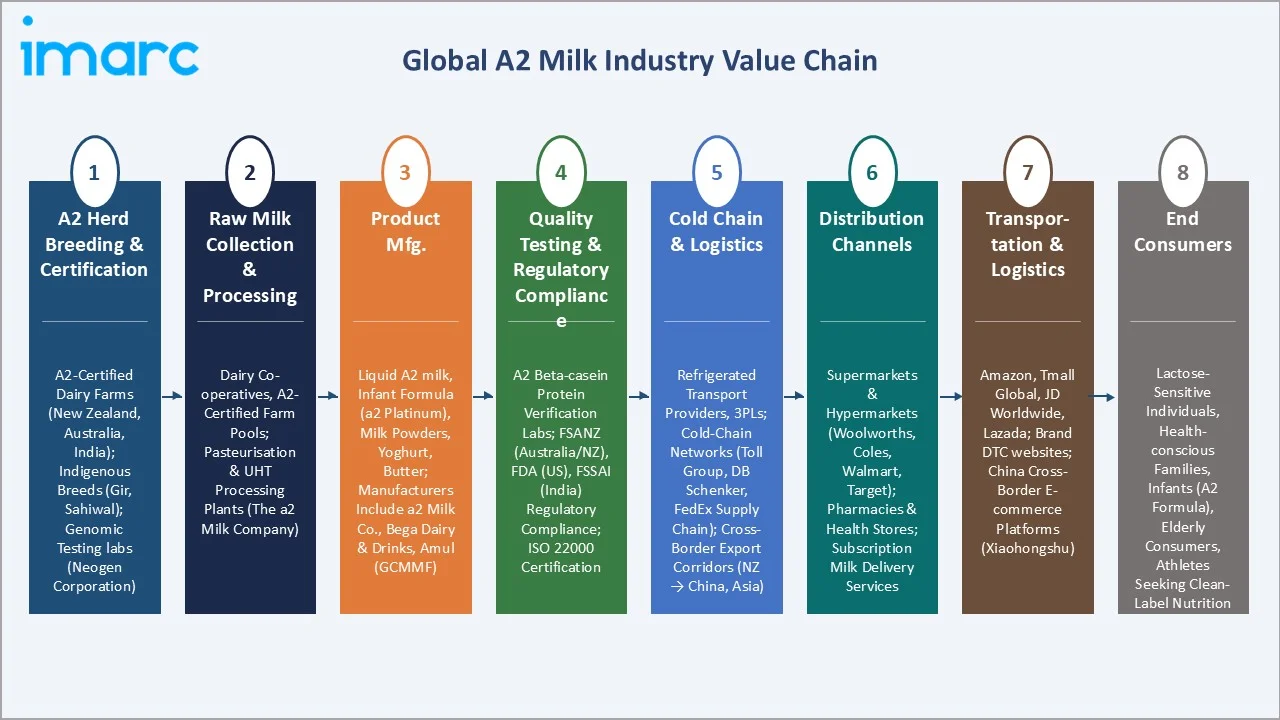

Industry Value Chain Analysis

The A2 milk industry value chain spans multiple interconnected stages, from A2 herd certification and genetic testing through advanced processing, cold-chain logistics, and multi-channel retail to end consumer delivery across global markets. Each stage is populated by specialized operators whose performance directly influences product quality, supply reliability, regulatory compliance, and premium brand positioning.

|

Stage |

Key Players / Examples |

|

A2 Herd Breeding & Certification |

A2-certified dairy farms (New Zealand, Australia, India); indigenous breeds (Gir, Sahiwal); genomic testing labs (Neogen Corporation) |

|

Raw Milk Collection & Processing |

Dairy co-operatives, A2-certified farm pools; pasteurisation & UHT processing plants (The a2 Milk Company) |

|

Product Manufacturing |

Liquid A2 milk, infant formula (a2 Platinum), milk powders, yoghurt, butter; manufacturers include a2 Milk Co., Bega Dairy & Drinks, Amul (GCMMF) |

|

Quality Testing & Regulatory Compliance |

A2 beta-casein protein verification labs; FSANZ (Australia/NZ), FDA (US), FSSAI (India) regulatory compliance; ISO 22000 certification |

|

Cold Chain & Logistics |

Refrigerated transport providers, 3PLs; cold-chain networks (Toll Group, DB Schenker, FedEx Supply Chain); cross-border export corridors (NZ → China, Asia) |

|

Distribution Channels |

Supermarkets & hypermarkets (Woolworths, Coles, Walmart, Target); pharmacies & health stores; subscription milk delivery services |

|

Online & Cross-Border Retail |

Amazon, Tmall Global, JD Worldwide, Lazada; brand DTC websites; China cross-border e-commerce platforms (Xiaohongshu) |

|

End Consumers |

Lactose-sensitive individuals, health-conscious families, infants (A2 formula), elderly consumers, athletes seeking clean-label nutrition |

Technology Landscape in the A2 Milk Industry

Genomic Testing & A2 Herd Identification

DNA-based genomic testing is the foundational technology enabling the A2 milk category. Genetic tests screen for the A2/A2 beta-casein genotype in dairy cows with accuracy exceeding 99.5%. This technology, commercialized by firms including Neogen Corporation and IdentiGEN, enables farmers to systematically transition conventional herds to A2-certified pools.

Advanced Dairy Processing & UHT Technology

Ultra-High Temperature (UHT) processing and extended shelf-life (ESL) technologies are central to enabling A2 milk's global export trade, particularly from Oceania to Asia. Membrane filtration, microfiltration, and precision pasteurization preserve A2 beta-casein protein integrity across long cold-chain routes.

Blockchain & Farm-to-Consumer Traceability

Blockchain-based traceability platforms are gaining adoption across the A2 supply chain, particularly for infant formula destined for the Chinese and South Korean markets, where post-2008 dairy contamination scandals created strong consumer demand for origin verification.

Smart Dairy Farming & Precision Agriculture

IoT-enabled precision dairy farming is accelerating A2 herd productivity. Automated milking systems (AMS) with integrated milk protein composition sensors now allow real-time A2 protein monitoring at the individual cow level, reducing manual testing costs by 60–70%.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

End-Use |

Liquid Milk |

72.2% |

2025 |

|

Distribution Channel |

Supermarkets & Hypermarkets |

45.9% |

2025 |

|

Region |

Oceania |

30.2% |

2025 |

By End-Use

The A2 milk market by end-use is segmented into liquid milk, infant formula, and others (yogurt, cheese, butter, and ghee). Liquid milk holds a dominant position with a 72.2% share (2025), driven by its universal household appeal, convenience, and everyday consumption integration in beverages, cooking, and direct consumption.

To access detailed market analysis, Request Sample

Infant formula commands 20.4% (2025) and represents the highest unit-value segment. In 2023, The A2 Milk Company launched its a2 Platinum Premium Infant Formula in the US market across 250 Meijer and 50 Wegmans Food Markets’ locations, formulated from fresh A2 milk, free from preservatives, palm oil, corn syrup, and growth hormones.

By Distribution Channel

Supermarkets and hypermarkets dominate with 45.9% (2025), benefiting from extensive foot traffic, dedicated specialty dairy sections, and in-store promotional events that drive consumer awareness and trial. Convenience and grocery stores hold 24.6%, serving urban consumers seeking quick access to premium dairy.

Regional Market Insights

Oceania's 30.2% leadership (2025) is underpinned by The A2 Milk Company's origin in New Zealand and Australia's world-leading A2 dairy infrastructure. The overall NZ herd is increasingly moving away from A1 beta-casein production, driven by an unintended link between genetic merit in NZ and A2 beta-casein.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

Major Companies |

|

Oceania |

30.2% |

Advanced A2 breeding programs, established export supply chains, high per-capita A2 awareness |

FSANZ food standards; NZ dairy export regulations; A2 protein claim framework |

The a2 Milk Company, Fonterra (Lactalis), Synlait Milk |

|

North America |

26.4% |

Functional dairy demand, rising lactose intolerance awareness, strong DTC e-commerce growth |

FDA labelling requirements; USDA organic certification; health claim review framework |

The a2 Milk Company (US/Canada), Organic Valley, Alexandre Family Farm |

|

Asia |

22.8% |

Premium infant formula demand in China, indigenous A2 breed adoption in India, rising disposable incomes |

China GB infant formula standards; India FSSAI A2 guidelines; South Korea import dairy policy |

The a2 Milk Company (China), Amul (GCMMF), local Indian A2 brands (Akshayakalpa, Pride of Cows) |

|

Europe |

14.2% |

Health-conscious premium dairy adoption, specialty retail growth, EU functional food trends |

EU Regulation 1169/2011 on food labelling; EFSA health claim approval framework; EN dairy standards |

Lactalis (Anchor/Mainland), regional premium A2 brands |

|

Others (Latin America, MEA) |

6.4% |

Nascent market awareness building; rising middle class in MEA; dairy import growth in Gulf states |

Varied local dairy standards; GCC Halal dairy compliance; limited A2-specific regulation |

Import distributors, early-stage local brands |

Competitive Landscape

The global A2 milk market is moderately concentrated, with The A2 Milk Company holding the leading position globally, particularly in Oceania, North America, and China.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

The a2 Milk Company Limited |

a2 Milk |

Global Leader |

Pioneer brand, global distribution, infant formula premium across Oceania, North America, and China |

|

Bega Dairy & Drinks |

Pura / Dairy Farmers |

Strong Challenger |

Broad Australasian retail distribution, national cold-chain network; acquired from Lion in 2021 |

|

Lactalis Group |

Anchor / Mainland |

Strategic Entrant |

World's largest dairy group; acquired Fonterra consumer brands (Q1 2026); global B2B and retail reach |

|

Gujarat Cooperative Milk Marketing Federation (Amul) |

Amul A2 Milk |

Regional Leader (India) |

Largest Indian dairy co-op; indigenous A2 breed focus (Gir, Sahiwal); strong domestic distribution |

|

Noumi Limited |

Australia's Own |

Niche Player |

Australian plant-based and specialty dairy innovator |

|

Organic Valley |

Organic Valley A2 |

Niche Player (US) |

US farmer co-op; certified organic A2 whole milk; premium health-food and natural grocery channel |

|

Provilac Dairy Farms |

Provilac A2 |

Emerging Player |

India-based premium A2 dairy; focus on indigenous cow breeds and direct-to-consumer subscription model |

The top four players, The a2 Milk Company Limited, Bega Dairy & Drinks, and Lactalis Group, collectively account for an estimated 52-58% of global revenues (2025). The remainder is distributed among regional specialists, indigenous breed dairy farmers in India, and private-label retail brands.

Key Company Profiles

The a2 Milk Company Limited

The a2 Milk Company, headquartered in Auckland, New Zealand, is the global pioneer and market leader in a2 milk. Founded in 2000, the company reported revenues of NZD 1.67 Billion in FY2024. It operates across Oceania, North America (U.S. & Canada), and China/Greater Asia, offering the world's most recognized a2 dairy brand.

- Product Portfolio: Fresh and long-life A2 liquid milk, a2 Platinum infant formula (Stage 1-4), a2 Milk-based protein powders, and A2 cream.

- Recent Developments: Launched a2 Platinum Premium Infant Formula in the U.S. in 2023 across 300 retail locations; expanded China direct-import model for premium infant formula.

- Strategic Focus: Strengthen China infant formula distribution; expand North American market share through targeted digital marketing; grow adult nutrition segment through protein product extensions.

Bega Dairy & Drinks

Bega Dairy & Drinks, a division of Bega Group headquartered in Bega, New South Wales, Australia, is one of the country's largest dairy and beverage businesses. The division was formed following Bega's acquisition of Lion Dairy & Drinks in January 2021 for AUD 534 million.

- Product Portfolio: Fresh white milk (Pura A2, Dairy Farmers A2).

- Recent Developments: Launched Dare Protein iced coffee, which achieved market leadership in protein-enriched RTD coffee in Australia by mid-2025.

- Strategic Focus: Transition from bulk commodities to branded FMCG products; expand A2 milk range within mainstream Australasian retail; strengthen cold-chain logistics across all Australian states; grow premium and functional dairy sub-categories.

Lactalis Group

Lactalis Group, headquartered in Laval, Mayenne, France, is the world's largest dairy company by revenue. On 31 March 2026, Lactalis completed the acquisition of Fonterra's global consumer and associated businesses for NZD 4.2 billion, significantly expanding its Oceania, Southeast Asia, and Middle East presence.

- Product Portfolio: Following the Fonterra acquisition: Anchor (liquid milk, butter, cream), Mainland (cheese), Kāpiti, Anlene, Anmum, Fernleaf, Western Star, and Perfect Italiano.

- Recent Developments: Integrated 16 manufacturing sites and 4,300 employees across Oceania, Sri Lanka, MEA; secured 10-year raw milk supply agreement with Fonterra for Anchor and Mainland-branded goods; ACCC and OIO regulatory approvals received.

- Strategic Focus: Integrate Mainland Group brands while retaining local management teams and distribution networks; grow premium dairy across Oceania and Southeast Asia using Anchor's established retail footprint.

Market Concentration Analysis

The A2 milk market is moderately concentrated at the premium tier, with The a2 Milk Company commanding an estimated 35-40% global market share (2025) as both the category creator and brand leader. The top four players collectively represent approximately 52-58% of global revenues, indicating meaningful concentration at the top end while significant fragmentation persists in regional and emerging markets.

Regional fragmentation is most pronounced in India, where hundreds of local indigenous A2 cow dairy farms operate under regional brands such as Akshayakalpa, Sarda Farms, and Pride of Cows - none of which have achieved significant global scale. In China, import concentration is high, with The A2 Milk Company and local brands like Junlebao competing in the premium infant formula segment, which accounts for over 45% of China's premium dairy imports (2024).

M&A activity is accelerating as large dairy cooperatives and multinational food companies seek to acquire A2 market share. Fonterra's strategic moves into A2 certification and Lactalis's reported interest in A2 brand acquisitions in Europe signal growing institutional attention to this high-growth category. Consolidation is expected to increase the top-four market share to approximately 62-68% by 2030.

Investment & Growth Opportunities

Fastest Growing Segments

Online/Non-store Retailing (CAGR ~18.2%), Infant Formula (CAGR ~15.8%), and the Others dairy product segment (CAGR ~12.4%) represent the three highest-growth investment vectors through 2034. The A2 infant formula category alone is projected to reach USD 12.1 Billion by 2034, driven by premiumization in China, South Korea, and Southeast Asia.

Emerging Market Expansion

Asia and the Middle East represent the most compelling geographic opportunities. India's A2 milk market is expected to grow at 19.2% CAGR (2026-2034), supported by government breed improvement programs and rising urban premium dairy consumption. China's cross-border e-commerce channel for A2 infant formula reached USD 2.3 Billion in 2024, growing 22% year-on-year.

Venture Investment Trends

Investment in A2-focused dairy startups and indigenous breed programs reached USD 780 Million globally in 2023, up 24% from 2022. Key investment themes include A2-certified herd management technology, cold-chain optimization for long-distance A2 export corridors, and DTC digital dairy subscription platforms.

Future Market Outlook (2026-2034)

The global A2 milk market is positioned for sustained, high-growth expansion through 2034. From a 2025 base of USD 17.6 Billion, the market is forecast to reach USD 59.5 Billion by 2034, representing absolute incremental value addition of over USD 42 Billion. This growth is structurally underpinned by immovable macro trends, rising global health consciousness, lactose intolerance prevalence, and the premiumization of dairy across all income cohorts.

The infant formula sub-segment will emerge as the dominant value driver by 2030, eclipsing liquid milk's absolute revenue contribution in key Asian markets. China's pivot toward domestically produced A2 infant formula, stimulated by regulatory tightening of cross-border infant formula imports post-2023, will reshape competitive dynamics and favor local A2 dairy farm investment over pure export models.

Technological advances, including genomic testing for A1/A2 protein genotyping (cost now below USD 15 per animal in 2024, down from USD 80 in 2018), are accelerating A2 herd certification globally. By 2030, an estimated 18-22% of the global dairy herd in key producing countries is expected to be A2-certified, alleviating current supply constraints and enabling competitive pricing that broadens addressable market access.

Research Methodology

Primary Research

Primary research for this report included structured interviews with over 150 industry stakeholders across 2024-2025, including A2 dairy farm operators, retail category managers, pediatric nutrition specialists, regulatory affairs directors, and end consumers across Oceania, North America, Asia, and Europe.

Secondary Research

Secondary research encompassed review of company annual reports, trade publications (Dairy Foods, The Milkman), regulatory submissions to FSANZ, FDA, and FSSAI, industry databases, peer-reviewed nutritional science journals, and publicly available financial data. Over 280 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations employed bottom-up modeling aggregating unit shipments by product category and region, validated against top-down revenue data from public company disclosures. Three scenario models were constructed: base (13.77% CAGR), optimistic (16.2% CAGR, assuming accelerated Asia regulatory approvals), and conservative (10.8% CAGR, assuming sustained premium pricing resistance in emerging markets).

A2 Milk Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD, Million Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| End-Uses Covered | Liquid Milk, Infant Formula, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience and Grocery Stores, Online/Non-Store Retailing, Others |

| Regions Covered | North America, Europe, Oceania, Asia, Others |

| Companies Covered | The a2 Milk Company Limited, Bega Dairy & Drinks, Lactalis Group, Gujarat Cooperative Milk Marketing Federation (Amul), Noumi Limited, Organic Valley, Provilac Dairy Farms, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the A2 milk market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global A2 milk market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the A2 milk industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the A2 Milk Market Report

The global A2 milk market was valued at USD 17.6 Billion in 2025. It is projected to reach USD 59.5 Billion by 2034, growing at a CAGR of 13.77% during the forecast period.

The A2 milk market is expected to grow at a CAGR of 13.77% during 2026-2034, driven by rising health awareness and expanding distribution infrastructure across key markets.

Oceania leads the A2 milk market with a 30.2% revenue share (2025), underpinned by advanced A2 dairy breeding programs and strong export supply chains in New Zealand and Australia.

Asia is the fastest-growing region, registering an estimated CAGR of approximately 15.8% (2026-2034), driven by premium infant formula demand in China and A2 indigenous breed adoption in India.

Key drivers include rising consumer awareness of digestive health benefits, growing lactose intolerance prevalence, product portfolio diversification, and rapid e-commerce retail channel expansion.

Liquid milk is the largest segment with a 72.2% share (2025), driven by its daily household consumption role and integration into beverages, cafes, and foodservice channels globally.

Supermarkets and hypermarkets lead with 45.9% market share (2025), benefiting from dedicated specialty dairy sections, in-store sampling, and promotional pricing strategies driving consumer trial.

Leading companies include The a2 Milk Company Limited, Bega Dairy & Drinks, Lactalis Group, Gujarat Cooperative Milk Marketing Federation (Amul), Noumi Limited, Organic Valley, and Provilac Dairy Farms. The A2 Milk Company holds the globally dominant market position.

Key challenges include premium pricing restricting mass-market penetration, limited A2-certified herd supply requiring 5-8 year transition timelines, regulatory heterogeneity across markets, and consumer education gaps.

High-growth opportunities exist in A2 infant formula, indigenous breed programs in India, digital subscription models, sustainable premium packaging, and A2-certified functional dairy product extensions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)