Active Pharmaceutical Ingredients (API) Market Size, Share, Trends and Forecast by Drug Type, Type of Manufacturer, Type of Synthesis, Therapeutic Application, and Region, 2026-2034

Global Active Pharmaceutical Ingredients (API) Market Size, Share, Trends & Forecast (2026-2034)

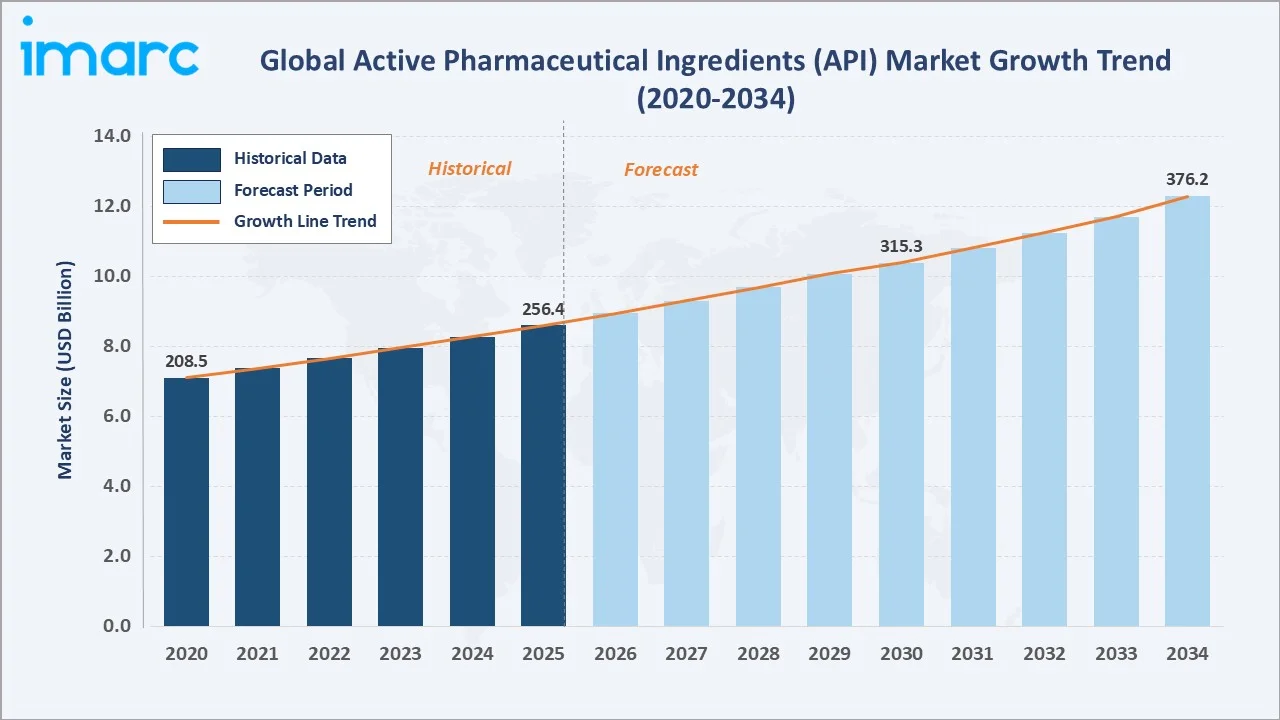

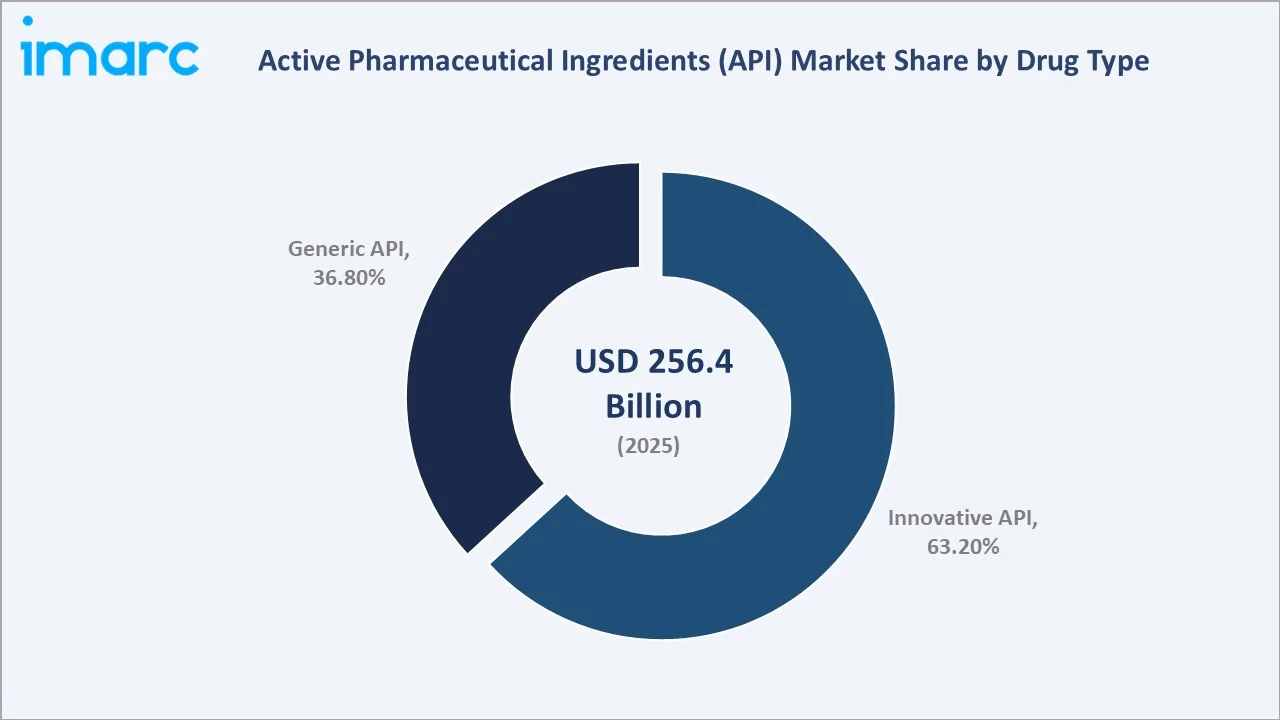

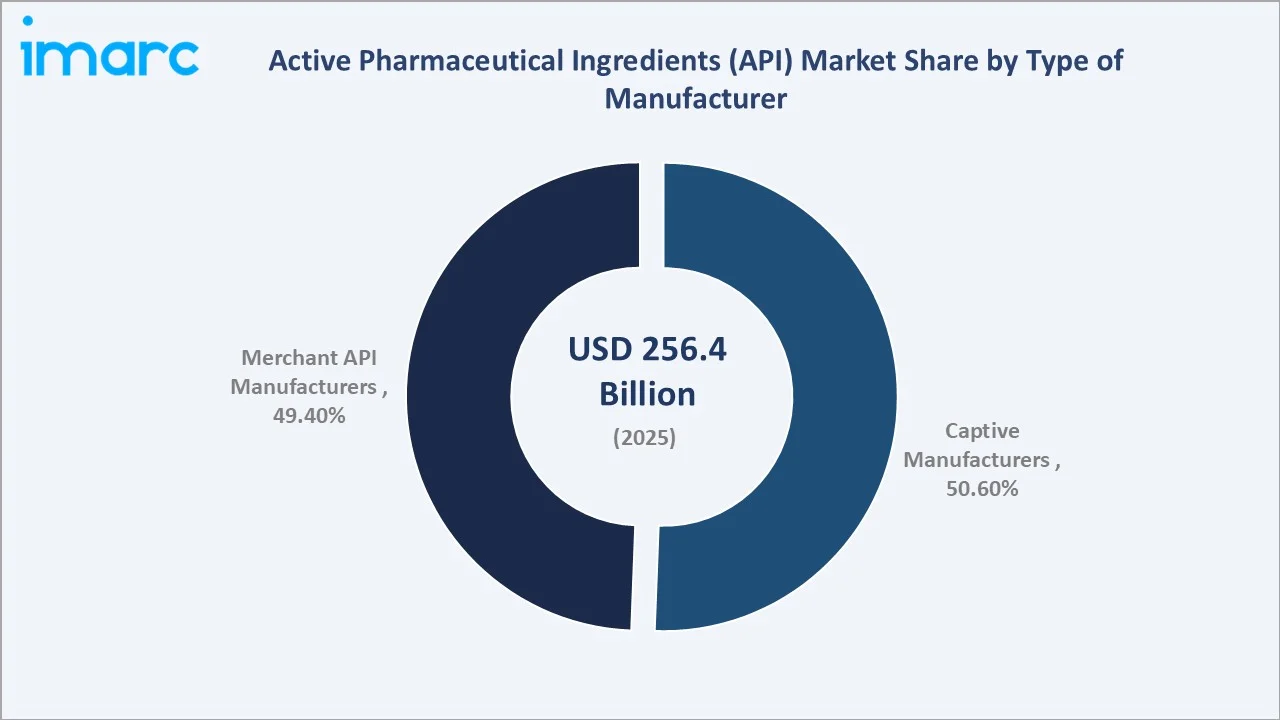

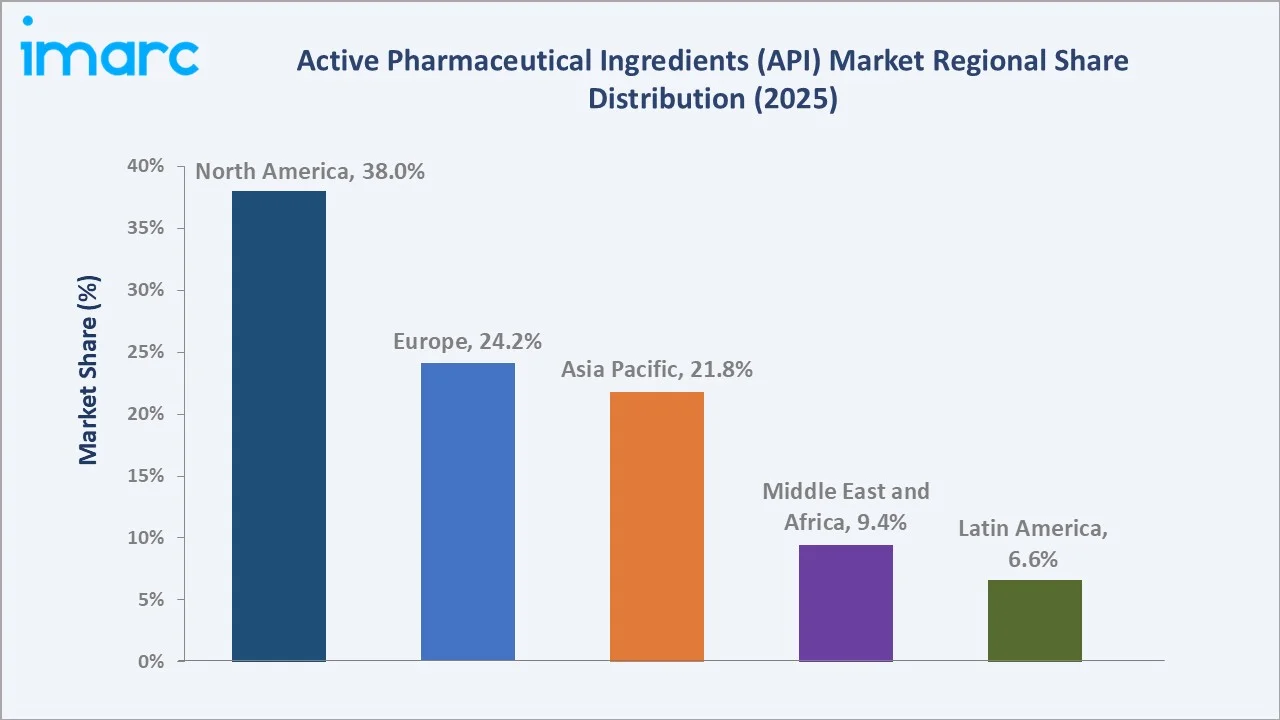

The global active pharmaceutical ingredients (API) market reached USD 256.4 Billion in 2025 and is projected to reach USD 376.2 Billion by 2034, exhibiting a CAGR of 4.22% during 2026-2034. Growth is driven by rising chronic disease prevalence, accelerating demand for biosimilars and generics, expansion of contract manufacturing organizations (CMOs/CDMOs), and significant R&D investment in targeted biopharmaceutical therapies. North America leads with a 38.0% market share (2025), supported by advanced pharmaceutical infrastructure, high R&D intensity, and supportive FDA regulatory frameworks. Innovative APIs dominate at 63.2%, while captive API manufacturers hold a 50.6% share of the manufacturer landscape.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 256.4 Billion |

|

Forecast Market Size (2034) |

USD 376.2 Billion |

|

CAGR (2026-2034) |

4.22% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Region |

North America (38.0%, 2025) |

|

Fastest Growing Region |

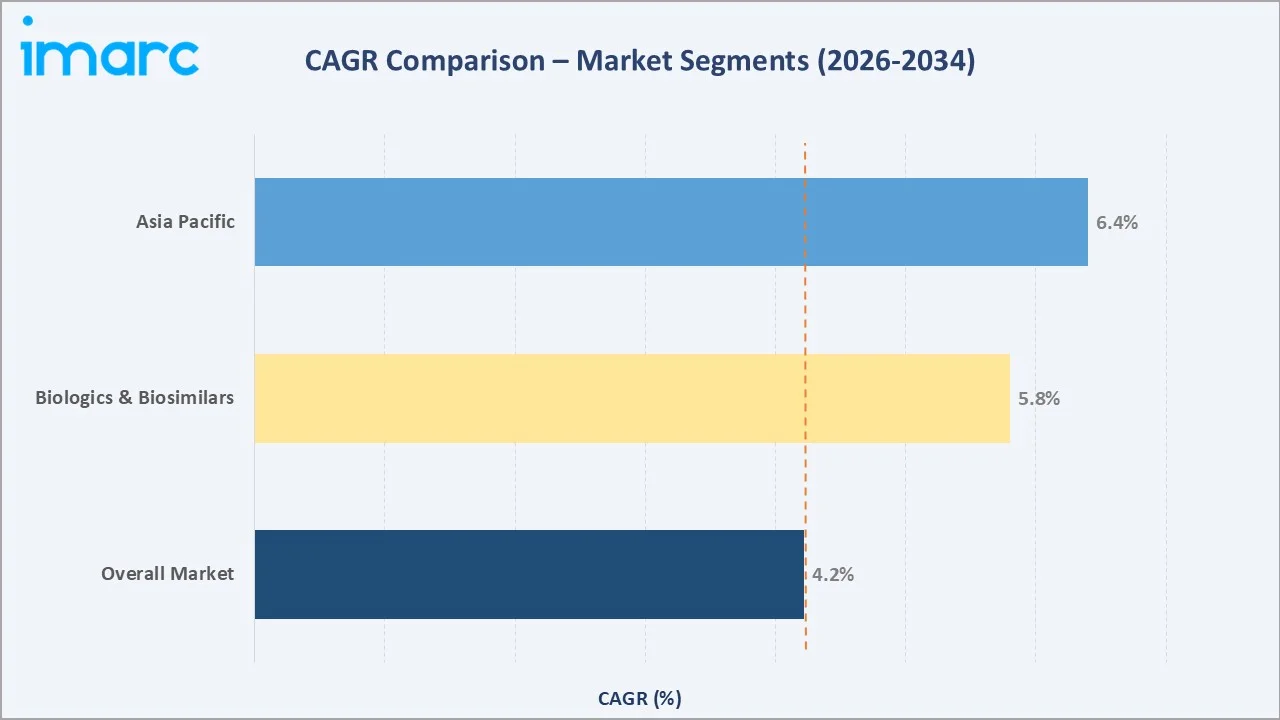

Asia Pacific (~6.4% CAGR) |

|

Dominant Drug Type |

Innovative API (63.2%, 2025) |

|

Leading Manufacturer Type |

Captive API Mfrs. (50.6%, 2025) |

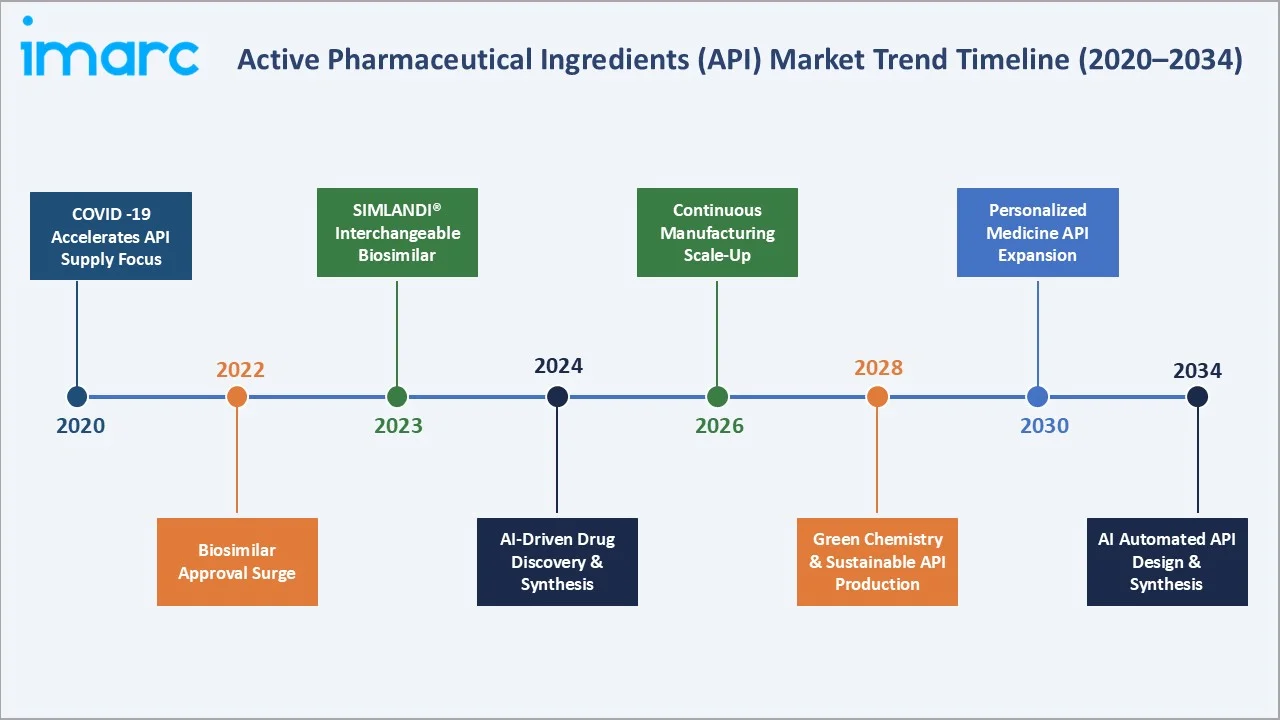

From 2020 to 2025, the market grew at a consistent pace driven by post-COVID supply chain restructuring, biosimilar approvals, including the FDA's February 2024 clearance of SIMLANDI® (adalimumab-ryvk) as the first high-concentration, citrate-free interchangeable biosimilar to Humira®, and the continued genericization of blockbuster drug franchises globally. The forecast addition of USD 119.8 Billion through 2034 represents a 46.7% value expansion from the 2025 base.

To get more information on this market, Request Sample

The 4.22% CAGR reflects a market expanding on multiple structural fronts simultaneously biologics driving innovation API demand, generic API volumes rising through patent expiry waves, and CMO/CDMO outsourcing growth creating scalable third-party manufacturing capacity across India, China, and Europe.

Executive Summary

The global active pharmaceutical ingredients (API) market encompasses the biologically active components in pharmaceutical formulations including small molecule chemical entities, biotechnology-derived proteins, and complex biologics, produced for use in branded innovative drugs, generic medicines, and biosimilar products. The market's USD 256.4 Billion scale in 2025 reflects its position as a foundational layer of the global pharmaceutical supply chain, serving drug product manufacturers across all therapeutic areas and geographies.

Innovative APIs account for 63.2% of total market revenues (2025), driven by strong R&D investment in biologics, monoclonal antibodies, ADCs (antibody-drug conjugates), and gene therapy vectors. Generic APIs at 36.8% continue to serve global healthcare cost-containment objectives. Captive API manufacturers (producing APIs exclusively for internal drug product use) represent 50.6% of the market, while merchant manufacturers selling APIs to external pharmaceutical clients account for 49.4%. North America (38.0%), Europe (24.2%), and Asia Pacific (21.8%) collectively account for 84.0% of global active pharmaceutical ingredients (API) market value in 2025.

Key strategic themes for 2026–2034 include: biologics and biosimilar API capacity expansion; supply chain diversification away from China concentration; green and continuous manufacturing adoption; and personalized medicine's demand for smaller-batch, high-complexity specialty APIs.

Key Market Insights

|

Insight |

Data |

|

Market Size (2025) |

USD 256.4 Billion |

|

Market Forecast (2034) |

USD 376.2 Billion |

|

CAGR (2026-2034) |

4.22% |

|

Dominant Drug Type |

Innovative API – 63.2% (2025) |

|

Leading Manufacturer Type |

Captive API Manufacturers – 50.6% (2025) |

|

Leading Region |

North America – 38.0% (2025) |

|

Fastest Growing Region |

Asia Pacific (~6.4% CAGR) |

|

Top Therapeutic Application |

Oncology – 22.4% (2025) |

|

Key Market Opportunity |

Biosimilar & biologic API – ~USD 80B+ addressable by 2034 |

|

Top Companies |

Pfizer, Teva, Dr. Reddy's, Sun Pharma, Lonza, Cipla, Aurobindo |

Key Analytical Observations:

- Innovative APIs’ 63.2% dominance (2025) is underpinned by the biopharmaceutical industry’s robust R&D pipeline, with biologics representing the majority of late-stage drug candidates, driving sustained demand for novel API synthesis and manufacturing capabilities.

- Captive API manufacturers’ 50.6% share reflects large integrated pharmaceutical companies’ strategic preference to maintain control over proprietary API synthesis, quality, and supply security for their branded and biosimilar portfolios.

- North America's 38.0% share reflects both high domestic pharmaceutical consumption and the concentration of global innovator biopharmaceutical R&D. The U.S. holds approximately 90.8% of North American active pharmaceutical ingredients (API) market value (2025).

- Oncology API is the largest therapeutic segment at 22.4%, driven by the proliferation of targeted cancer therapies, ADCs, and immuno-oncology monoclonal antibodies requiring highly complex, high-value API synthesis.

- Asia Pacific's ~6.4% CAGR – the highest among all regions – reflects India and China's expanding generic API manufacturing capacity, growing domestic pharmaceutical markets, and increasing biosimilar manufacturing investment in South Korea and China.

Global Active Pharmaceutical Ingredients (API) Market Overview

Active pharmaceutical ingredients are the biologically or pharmacologically active components within a drug product responsible for its therapeutic effect. The global API ecosystem spans raw chemical and biological precursor supply, synthesis and fermentation manufacturing, analytical quality control, regulatory submission (Drug Master Files), and distribution to formulation manufacturers globally. As of 2025, the market encompasses thousands of commercially significant API molecules across seven major therapeutic categories, manufactured at scales ranging from multi-ton commodity APIs (aspirin, metformin, paracetamol) to microgram-scale specialty oncology ADC payloads.

Market Dynamics

To evaluate market opportunities, Request Sample

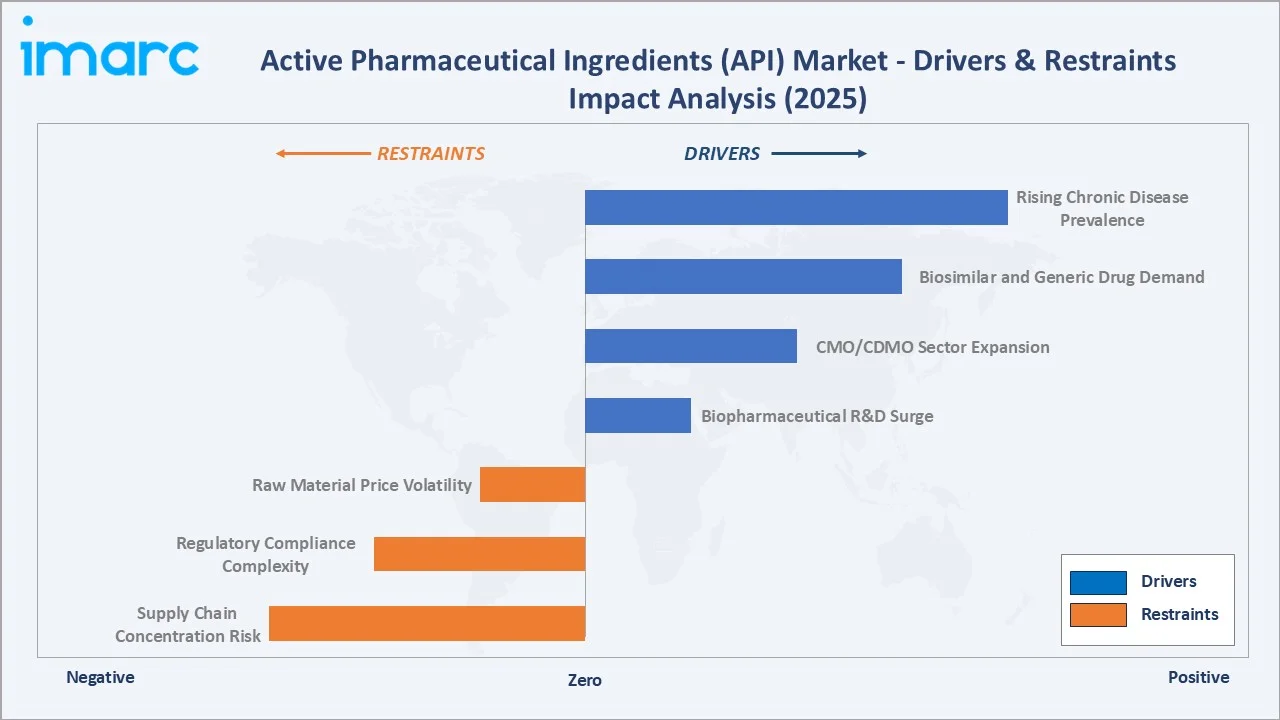

Market Drivers

- Rising Chronic Disease Prevalence: Cardiovascular diseases, diabetes, oncology, and CNS disorders collectively account for significant portion of global disease burden. Expanding patient populations across all geographies create sustained pharmaceutical demand, directly driving API procurement volumes. Global diabetes cases are projected to reach 783 million by 2045, representing an enormous API demand engine.

- Biosimilar and Generic Drug Demand: The FDA's February 2024 approval of SIMLANDI® as an interchangeable biosimilar to Humira exemplifies the accelerating biosimilar approval wave. Patent expirations on biologics worth USD 200+ Billion in annual revenues are creating large-scale biosimilar API manufacturing opportunities. Generic market volume growth in emerging economies sustains chemical API demand.

- CMO/CDMO Sector Expansion: The global CDMO market has grown significantly with India CDMO market growing at 7% annually, absorbing API manufacturing outsourcing from both innovators and generic manufacturers. CDMOs provide variable cost manufacturing, specialized synthesis capabilities, and regulatory expertise that internal manufacturing cannot cost-effectively replicate at small batch scales.

- Biopharmaceutical R&D Surge: The global pharmaceutical pipeline contained over 8,000 drugs in clinical development as of 2024, with biologics representing approximately half of all late-stage drug candidates. Each IND-to-approval cycle creates sustained demand for development-stage and commercial-scale innovative API manufacturing.

Market Restraints

- Supply Chain Concentration Risk: Approximately 70–80% of global active pharmaceutical ingredient production for U.S. drug products originates from India and China. This geographic concentration creates significant supply vulnerability, illustrated by COVID-19 disruptions and subsequent regulatory focus on supply chain resilience.

- Regulatory Compliance Complexity: APIs must comply with FDA Current Good Manufacturing Practices (cGMP), ICH Q7 guidelines, EMA GMP requirements, and country-specific pharmacopoeial standards. Warning letters, import alerts, and facility shutdowns for GMP non-compliance create significant business continuity risks for API manufacturers.

- Raw Material Price Volatility: API synthesis requires specialty chemical intermediates, solvents, and catalysts subject to commodity price volatility. Solvent and energy cost increased significantly during 2022–2023 significantly compressed API manufacturer margins.

Market Opportunities

- Biologics and Biosimilar Capacity: The global biologics active pharmaceutical ingredients (API) market is projected to reach USD 370+ Billion by 2034. Investments in bioreactor capacity, upstream/downstream bioprocessing, and cold chain logistics for biologic APIs represent the highest-value growth opportunity in the API industry over the forecast period.

- Nearshoring and Supply Diversification: U.S. and EU initiatives to reduce API import dependency are creating investment opportunities for domestic and friendly-nation API manufacturing capacity. The BIOSECURE Act and EU Pharmaceutical Strategy are directing subsidies and procurement preferences toward non-China API sources.

- Continuous Manufacturing Adoption: Continuous manufacturing (CM) technologies for API synthesis are achieving 30–50% reduction in manufacturing footprint, 20–40% cost reduction, and improved quality consistency versus batch manufacturing. FDA actively encourages CM adoption through expedited review pathways.

Market Challenges

- Intellectual Property and Generic Entry Timing: Complex biologic patent defense strategies (patent thickets, manufacturing trade secrets) create uncertainty in biosimilar active pharmaceutical ingredients (API) market entry timelines. Litigation risk around secondary patents delays market entry for generic and biosimilar API manufacturers.

- Environmental and Sustainability Compliance: Pharmaceutical manufacturing is among the most polluting industrial sectors per unit output. Zero liquid discharge requirements, effluent treatment standards, and carbon emissions reporting obligations are creating compliance cost headwinds particularly for high-volume Indian and Chinese API producers.

Emerging Market Trends

Five converging trends are reshaping API manufacturing competitiveness, R&D investment priorities, and supply chain strategy through 2034.)

1. Biologic and ADC API Complexity Surge

Antibody-drug conjugates (ADCs), combining a monoclonal antibody with a cytotoxic small molecule payload represent the fastest-growing API complexity category, with over 400 ADCs in clinical development as of 2025. Each ADC requires both biologic (antibody) and highly potent small molecule (payload) API manufacturing capabilities, driving significant investment in dedicated containment and bioconjugation facilities.

2. AI-Accelerated Drug Discovery and API Synthesis

Generative AI platforms including AlphaFold, Insilico Medicine, and Recursion Pharmaceuticals are identifying novel molecular targets and optimizing synthesis routes faster than traditional computational methods. AI-designed APIs with optimized molecular properties are accelerating the pipeline to clinical synthesis, reducing time from target identification to API GMP batch by 30–40%.

3. Supply Chain Reshoring and China+1 Strategy

The U.S. BIOSECURE Act's provisions targeting Chinese CDMOs, combined with EU supply chain resilience mandates, are accelerating API sourcing diversification. India, South Korea, Ireland, and Singapore are primary beneficiaries of this geographic diversification, with many companies looking to invest. For instance, Eli Lilly and Company announcing that it plans to build a $5 billion manufacturing facility just west of Richmond, Virginia, in Goochland County.

4. Green Chemistry and Sustainable API Production

The pharmaceutical industry's sustainability commitments are reshaping API synthesis preferences. Biocatalysis, flow chemistry, solvent-free reactions, and enzymatic synthesis are replacing multi-step chemical processes with lower E-factor (waste-per-product) equivalents. AstraZeneca and Pfizer have both committed to green chemistry API synthesis adoption targets tied to carbon neutrality goals.

5. Personalized Medicine and Small-Batch Specialty APIs

Cell and gene therapies, RNA therapeutics, and personalized cancer vaccines require API manufacturing paradigms radically different from commodity chemical synthesis, small batch sizes, patient-specific production, complex biomolecular synthesis, and ultra-cold chain management.

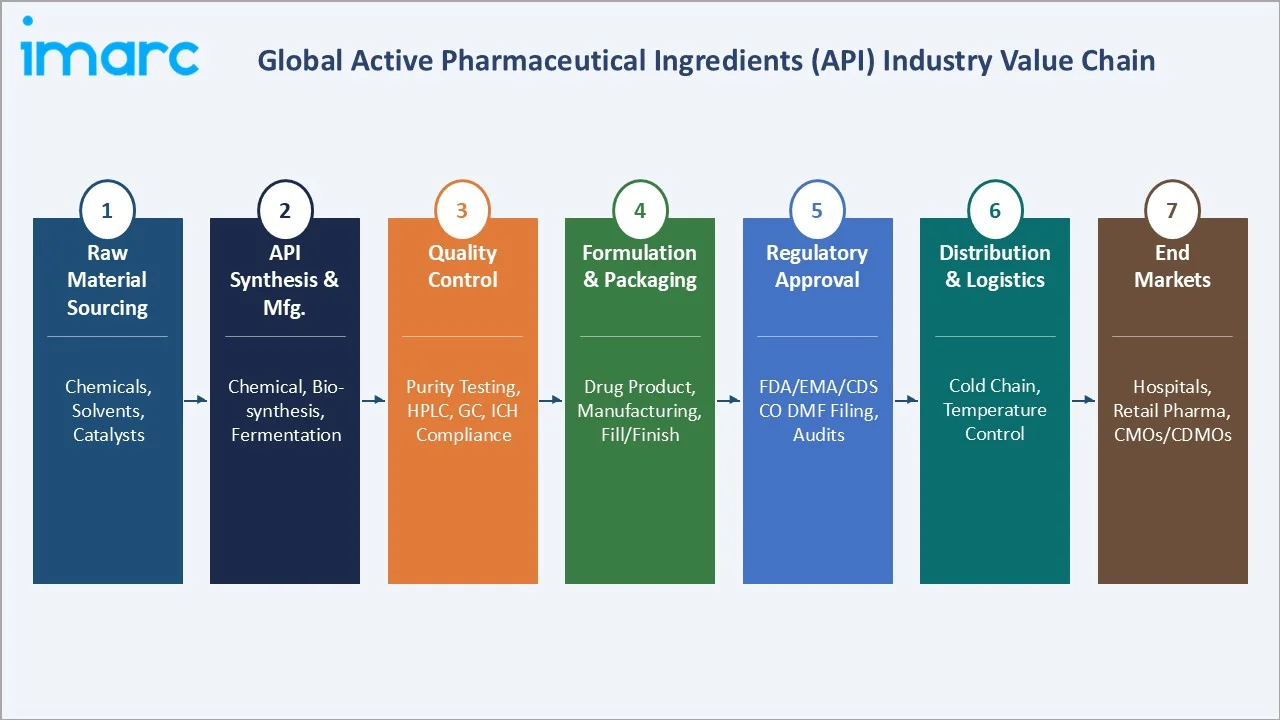

Industry Value Chain Analysis

The API value chain spans seven stages from precursor chemistry through to end pharmaceutical market delivery.

|

Stage |

Key Activities |

Representative Players |

|

Raw Material Sourcing |

Chemical precursors, solvents, biologics media, catalyst supply |

BASF, Sigma-Aldrich (Merck KGaA), Thermo Fisher, Divi's (intermediates) |

|

API Synthesis & Manufacturing |

Chemical synthesis, fermentation, bioprocessing, purification |

Aurobindo, Teva API, WuXi AppTec, Lonza, Samsung Biologics |

|

Quality Control & Testing |

HPLC, GC, microbial testing, ICH stability, pharmacopoeial release |

Eurofins Pharma, Charles River, SGS Life Sciences |

|

Formulation & Drug Product |

Tablet, capsule, injectable, parenteral fill-finish manufacturing |

Pfizer CentreOne, Recipharm, Piramal Pharma |

|

Regulatory Filing |

DMF submission, CEP application, ANDA/NDA support, GMP audits |

Regulatory affairs consultancies, in-house regulatory teams |

|

Distribution & Logistics |

Temperature-controlled API shipping, customs clearance, cold chain |

DHL Life Sciences, Marken, World Courier |

|

End Markets |

Branded pharma, generics, biosimilar drug product manufacturers |

Pfizer, Novartis, Abbott, Dr. Reddy's, Cipla, Mylan |

Technology Landscape

Continuous Manufacturing (CM)

FDA-endorsed continuous manufacturing platforms for API synthesis are delivering significant footprint reduction and significant quality consistency improvements over batch equivalents. Eli Lilly, Pfizer, and Vertex have commercially deployed CM for small molecule APIs, with adoption accelerating for high-volume generic APIs.

Bioreactor and Bioprocessing Innovation

Single-use bioreactor systems, intensified upstream perfusion culture, and continuous downstream processing are enabling biologics API manufacturers to achieve significant productivity improvements per manufacturing suite. These advances are reducing the capital intensity of biologic API scale-up, enabling smaller CDMOs to compete in the biologics outsourcing market.

Flow Chemistry and Microreactor Technology

Flow chemistry enables precise control of reaction parameters, enabling safer synthesis of energetic intermediates and significantly reducing API synthesis time from days to hours. High-potent API (HPAPI) synthesis in contained flow systems is enabling oncology ADC payload production at commercial scale with superior containment versus conventional batch synthesis.

AI and Machine Learning in Process Optimization

Machine learning models applied to API crystallization, purification, and particle engineering are reducing development time for solid-state API forms from months to weeks. Digital twin simulations of API manufacturing processes are enabling real-time release testing and reducing QC cycle time by nearly half.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Drug Type |

Innovative Active Pharmaceutical Ingredients |

63.2% |

2025 |

|

Type of Manufacturer |

Captive Manufacturer |

50.6% |

2025 |

|

Type of Synthesis |

Synthetic Active Pharmaceutical Ingredients (API) |

71.8% |

2025 |

|

Therapeutic Application |

Oncology |

21.2% |

2025 |

|

Region |

North America |

38.0% |

2025 |

By Drug Type

To access detailed market analysis, Request Sample

Innovative APIs lead at 63.2% (2025) versus generic APIs at 36.8%, reflecting the pharmaceutical industry’s accelerating investment in biologics, targeted therapies, and advanced molecular entities across global drug pipelines.

By Type of Manufacturer

Captive API manufacturers (50.6%) produce APIs solely for internal drug product use within the same organization. Merchant manufacturers (49.4%) sell APIs externally to pharmaceutical manufacturers, including through CDMO models.

Regional Market Insights

North America dominates the global active pharmaceutical ingredients (API) market, while Asia Pacific is the highest-growth region driven by manufacturing scale in India and China and rising domestic pharmaceutical demand.

Asia Pacific's ~6.4% CAGR significantly above the global average reflects India's position as the world's largest generic drug exporter, China's continued expansion despite supply chain diversification pressures, and South Korea's rapidly growing biosimilar API manufacturing ecosystem led by Samsung Biologics and Celltrion.

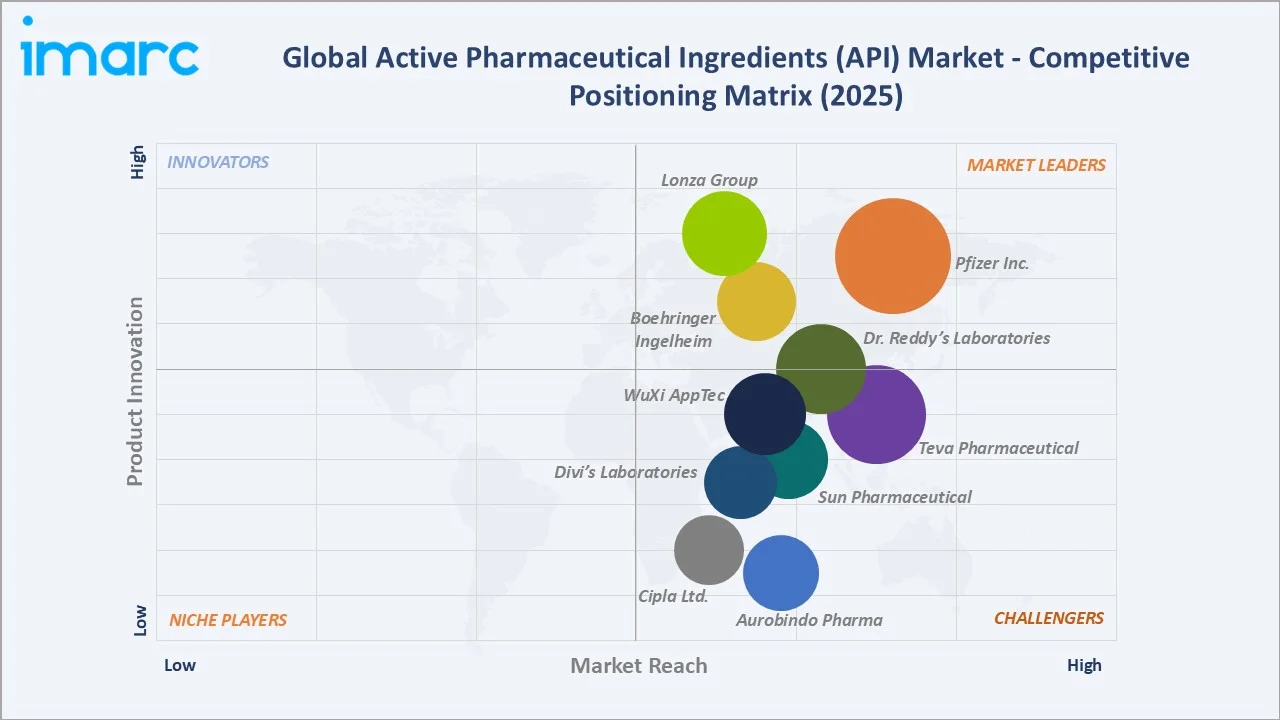

Competitive Landscape

The global active pharmaceutical ingredients (API) market is moderately fragmented, combining large vertically integrated pharmaceutical companies operating captive API facilities with specialized merchant API manufacturers and CDMOs. No single company controls more than 5–6% of global API revenues, reflecting the market's breadth across hundreds of distinct molecules and therapeutic areas.

|

Company |

HQ |

Position |

Strategy |

|

Pfizer Inc. |

New York, USA |

Leader – Innovative & Generic |

Biologic API captive production, generic API divestiture strategy, mRNA API investment |

|

Teva Pharmaceutical |

Tel Aviv, Israel |

Leader – Generic API |

World's largest generic manufacturer, API vertical integration, biosimilar pipeline |

|

Dr. Reddy's Laboratories |

Hyderabad, India |

Leader – Merchant API |

Global generic API supply, PSAI (API) division, biosimilar API development |

|

Sun Pharmaceutical |

Mumbai, India |

Leader – Specialty API |

Specialty API, complex generics, U.S. and EU market focus, dermatology/CNS |

|

Lonza Group |

Basel, Switzerland |

Leader – CDMO/Biologics |

Mammalian cell culture API, HPAPI containment, gene therapy vectors, CMC support |

|

Aurobindo Pharma |

Hyderabad, India |

Established – Generic API |

High-volume generic API for global markets, cephalosporin specialist, EU/US supply |

|

Divi's Laboratories |

Hyderabad, India |

Established – Merchant API |

Custom synthesis, nutraceuticals, carotenoids, high-purity API intermediates |

|

Boehringer Ingelheim |

Ingelheim, Germany |

Challenger – Biologic CDMO |

Biopharmaceutical CDMO, mammalian and microbial API, viral vector manufacturing |

|

Cipla Ltd. |

Mumbai, India |

Established – Generic API |

Respiratory API specialty, anti-retroviral global supply, U.S. generic market |

|

WuXi AppTec |

Shanghai, China |

Challenger – CDMO |

End-to-end CDMO, small molecule + biologic API, BIOSECURE Act risk exposure |

Indian API manufacturers (Dr. Reddy's, Aurobindo, Sun Pharma, Divi's, Cipla) collectively dominate merchant generic API supply globally, leveraging cost structures significantly below Western equivalents and deep chemistry capabilities. However, the BIOSECURE Act's potential restrictions on Chinese CDMOs (WuXi AppTec, Zhejiang Huahai) are creating a structural realignment opportunity for Indian and European CDMO capacity.

Key Company Profiles

Pfizer Inc.

Pfizer's API operations span captive manufacturing for its branded portfolio and global supply agreements for generic API, under its unit-Pfizer CentreOne). Post-COVID, Pfizer has invested heavily in mRNA API manufacturing capabilities (nucleoside synthesis, lipid nanoparticle components) representing next-generation biologic API infrastructure.

- Recent: mRNA API manufacturing scale-up; COVID antiviral (Paxlovid) API commercial production; partnerships with biosimilar API manufacturers for Humira® follow-on biologics supply.

- Strategy: mRNA platform API diversification; oncology ADC API pipeline build; manufacturing network optimization through site consolidation.

Dr. Reddy's Laboratories

Dr. Reddy's is India's largest API exporter, with its Pharmaceutical Services & Active Ingredients (PSAI) division. With eight USFDA-inspected cGMP facilities that adhere to ICH Q7 criteria and are routinely assessed by international regulators, Dr. Reddy's produces more than 250 APIs throughout India, Mexico, and the UK. The company has significant oncology API and biosimilar API capabilities.

- Recent: Expanded API manufacturing for biosimilar adalimumab; launched dedicated oncology HPAPI facility in Hyderabad; filed multiple COS/DMF submissions across EU/FDA in 2023–2024.

- Strategy: Biosimilar API capacity expansion; oncology HPAPI investment; complex API synthesis differentiation for regulated Western markets.

Lonza Group

Lonza is the world's premier independent biologics CDMO. Its mammalian cell culture, microbial fermentation, gene therapy vector, and HPAPI capabilities make it the preferred partner for innovative biologic API outsourcing globally.

- Recent: Expanded Ibex® Solutions large-scale mammalian cell culture in Switzerland; launched viral vector manufacturing facility in Houston, Texas; won multiple cell/gene therapy CDMO contracts.

- Strategy: Biologics CDMO leadership, cell and gene therapy API manufacturing scale-up, HPAPI containment capabilities expansion.

Aurobindo Pharma

Aurobindo is one of the world's largest generic pharmaceutical and API manufacturers, with dedicated API manufacturing at 10+ facilities in Andhra Pradesh and Telangana, India. It is a leading supplier of cephalosporin, ARV, and penicillin APIs globally.

- Recent: Expanded European API supply for U.S./EU generic manufacturers; received FDA approval for multiple new API synthesis routes; progressed biosimilar API development pipeline.

- Strategy: API volume leadership, European market API supply expansion, biosimilar API entry.

Market Concentration Analysis

The global active pharmaceutical ingredients (API) market is structurally fragmented. The top ten API companies account for approximately 20–25% of global API revenues, with the remainder distributed across hundreds of specialty and regional manufacturers. Generic API manufacturing is highly competitive in commodity molecules, with Indian and Chinese producers commanding the highest volume shares through cost leadership. The biologic API segment is more concentrated, with a smaller number of capable CDMOs (Lonza, Samsung Biologics, WuXi Biologics) controlling significant market share due to the high capital and expertise barriers to biologics API manufacturing.

Consolidation is accelerating in the CDMO sector. Thermo Fisher's acquisition of Patheon, Catalent's acquisition by Novo Holdings (2024), and multiple CDMO mergers reflect the strategic value of integrated API manufacturing and drug product capabilities.

Investment & Growth Opportunities

Biologics and Biosimilar API

Investment in mammalian cell culture capacity, single-use bioprocessing, and cold chain logistics for biologic APIs represents the highest absolute value opportunity. Biosimilar API manufacturing for adalimumab, trastuzumab, bevacizumab, and rituximab biosimilars constitutes an addressable market.

HPAPI and Oncology Specialty

High-potent API (HPAPI) manufacturing for ADCs, oncology targeted therapies, and hormone antagonists is growing at approximately 8% annually. HPAPI requires dedicated containment infrastructure (OEB4/OEB5 grade) that limits market entry, creating durable pricing power for certified HPAPI manufacturers.

Supply Chain Diversification Investment

- U.S. BIOSECURE Act provisions are creating redirected demand for non-Chinese API CDMOs, benefiting Indian (Divi's, Aurobindo, Cipla), European (Lonza, Cambrex, Albany Molecular), and Korean (Samsung) manufacturers.

- EU Pharma Strategy's goal of reducing strategic API dependency is driving public investment in European API manufacturing capacity, including Critical Medicines Act provisions supporting domestic production incentives.

- India's Production-Linked Incentive (PLI) scheme for bulk drugs and APIs has committed INR 6,940 crore to incentivize domestic API production, covering 41 priority pharmaceutical products.

Future Market Outlook (2026-2034)

The global active pharmaceutical ingredients (API) market is set for sustained structural expansion through 2034, anchored by the biopharmaceutical industry's innovation pipeline, patent-driven generic API demand waves, and the continued growth of pharmaceutical consumption in emerging markets. From USD 256.4 Billion in 2025, the market is forecast to reach USD 376.2 Billion by 2034 at a 4.22% CAGR, an incremental addition of USD 119.8 Billion over nine years.

Biologic APIs will be the primary value growth driver. The transition of multiple large-molecule drugs from exclusivity to biosimilar competition, a pattern established with Humira and Enbrel now extending to Keytruda, Opdivo, and Eylea, will sustain both innovative biologic API demand and create biosimilar active pharmaceutical ingredients (API) market entry opportunities through 2034. Simultaneously, AI-driven drug discovery is expected to accelerate the flow of novel API candidates from computational design to clinical synthesis, maintaining innovative API R&D investment momentum.

Geographically, Asia Pacific will gain market share through 2034, with India expanding beyond generic API to biosimilar and specialty API capabilities, and South Korea's Samsung Biologics and Celltrion cementing global top-tier biologic CDMO positions. North America's share will moderate slightly as nearshoring-eligible nations absorb new investment, but its dominance in high-value innovative API will sustain a leading regional position through the forecast decade.

Research Methodology

Primary Research

Structured interviews with over 140 industry participants in 2024–2025, comprising API manufacturers, pharmaceutical procurement managers, CDMO executives, regulatory consultants, and investment analysts across North America, Europe, India, and Asia Pacific.

Secondary Research

Review of FDA Drug Master File databases, EMA API certification records, company annual reports, trade publications (Pharmaceutical Technology, Chemical & Engineering News, Generic Drug Bulletin), and industry databases (Evaluate Pharma, IQVIA). Over 280 sources reviewed and triangulated.

Forecasting Models

Market size projections derived from bottom-up API molecule demand modeling incorporating patent expiry schedules, new drug approval forecasts, biosimilar approval pipelines, and regional pharmaceutical consumption growth data. Scenario analysis across base, optimistic, and conservative cases.

Active Pharmaceutical Ingredients (API) Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Drug Types Covered |

|

| Types of Manufacturers Covered |

|

| Types of Synthesis Covered | Synthetic Active Pharmaceutical Ingredients (API), Biotech Active Pharmaceutical Ingredients (API) |

| Therapeutic Applications Covered | Oncology, Cardiovascular and Respiratory, Diabetes, Central Nervous System Disorders, Neurological Disorders, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia |

| Companies Covered | Pfizer Inc., Teva Pharmaceutical, Dr. Reddy's Laboratories, Sun Pharmaceutical, Lonza Group, Aurobindo Pharma, Divi's Laboratories, Boehringer Ingelheim, Cipla Ltd., WuXi AppTec, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the active pharmaceutical ingredients (API) market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global active pharmaceutical ingredients (API) market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the active pharmaceutical ingredients (API) industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Active Pharmaceutical Ingredients (API) Market Report

The global active pharmaceutical ingredients (API) market was valued at USD 256.4 Billion in 2025 and is projected to reach USD 376.2 Billion by 2034.

The market is forecast to grow at a CAGR of 4.22% during 2026-2034, driven by biosimilar demand, chronic disease prevalence, CMO/CDMO expansion, and biopharmaceutical R&D investment.

North America dominates with a 38.0% share in 2025, backed by advanced pharmaceutical R&D, high biopharmaceutical consumption, and strong regulatory infrastructure.

Innovative APIs lead with a 63.2% share in 2025, driven by strong biopharmaceutical R&D investment, expanding biologics pipelines, and growing demand for novel targeted therapies including monoclonal antibodies, ADCs, and gene therapy vectors.

Captive manufacturers produce APIs exclusively for internal drug product use within the same organization. Merchant manufacturers sell APIs externally to third-party pharmaceutical companies, including through CDMO models.

Patent expiries on biologic blockbusters (adalimumab, trastuzumab, bevacizumab), FDA/EMA interchangeability pathways, and healthcare payer demand for biologic cost reduction are collectively driving biosimilar API demand growth at above-market-average rates.

Leading companies include Pfizer, Teva Pharmaceutical, Dr. Reddy's Laboratories, Sun Pharmaceutical, Lonza Group, Aurobindo Pharma, Divi's Laboratories, Boehringer Ingelheim, Cipla, and WuXi AppTec.

Primary opportunities include biologics API CDMO capacity, HPAPI manufacturing for oncology ADCs, API supply chain diversification away from China, and green/continuous manufacturing technology adoption for cost-competitive API production.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade