Adipic Acid Market Size, Share, Trends and Forecast by End Product, Application, End User, and Region, 2026-2034

Adipic Acid Market Size and Share:

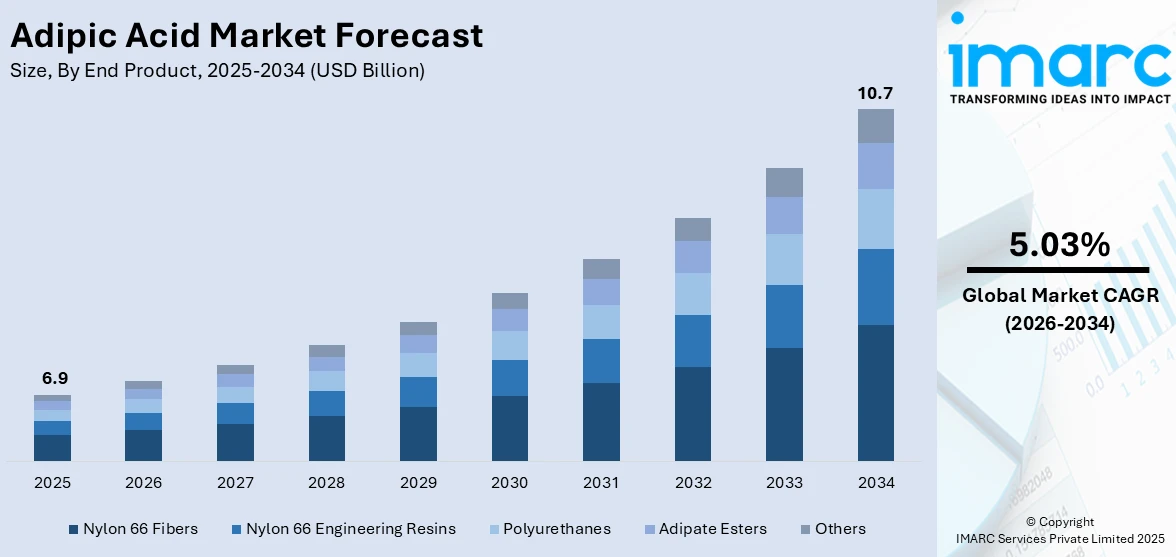

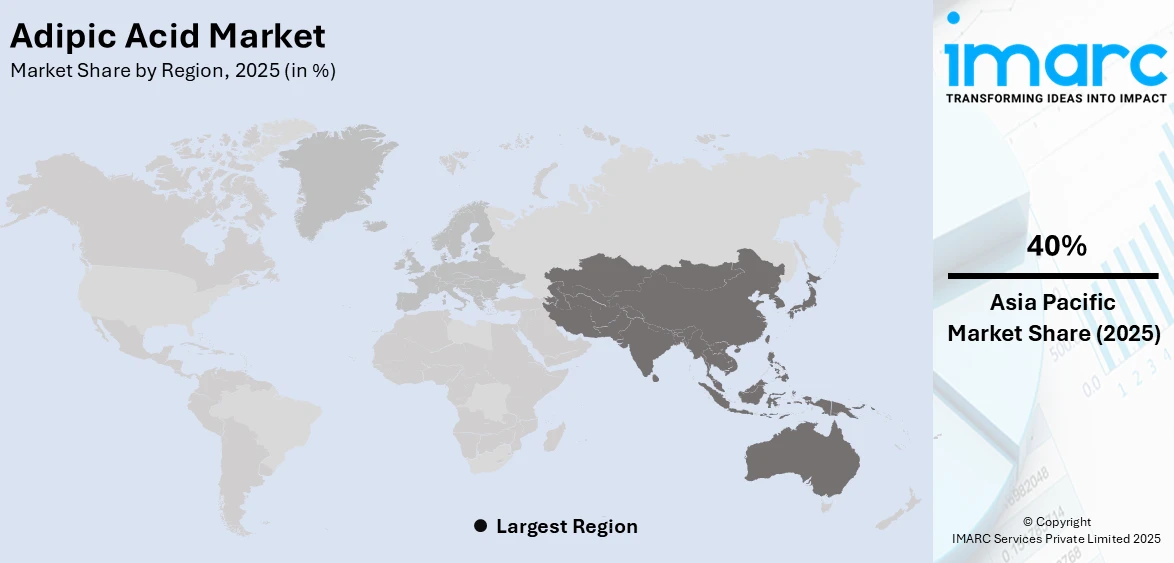

The global adipic acid market size was valued at USD 6.9 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 10.73 Billion by 2034, exhibiting a CAGR of 5.03% from 2026-2034. Asia-Pacific currently dominates the market, holding a market share of 40% in 2025. The region benefits from extensive chemical manufacturing infrastructure, robust demand from the automotive and textile industries, and favorable government initiatives promoting industrial expansion and polyamide production, contributing to the adipic acid market share.

The growing demand for nylon 66 across the automotive, textile, and electrical sectors represents a primary driver of the adipic acid market. Adipic acid serves as a critical precursor in the production of polyamide 66, which is widely utilized in engineering plastics for lightweight vehicle components, industrial fibers, and electronic connectors. The increasing emphasis on vehicle weight reduction to meet stringent emission regulations is further accelerating the adoption of nylon 66-based materials. Additionally, the expanding polyurethane industry is propelling demand for adipic acid as a key ingredient in flexible and semi-rigid foams used in furniture, insulation, and footwear applications. The adipic acid market growth is bolstered by the rising consumption of the chemical as a plasticizer component in flexible polyvinyl chloride (PVC) products for construction, healthcare, and packaging applications.

The United States has emerged as a major region in the adipic acid market owing to many factors. The country’s well-established automotive and aerospace sectors drive significant demand for nylon 66-based engineering plastics and fibers used in airbags, seat belts, tire cords, and under-hood components. In December 2024, the production of motor vehicles in the United States was recorded at 10,562,188.000 units, according to the International Organization of Motor Vehicle Manufacturers, sustaining strong demand for nylon 66 engineering plastics across the automotive supply chain. The growing adoption of electric vehicles (EVs) is further fueling demand for lightweight polymer materials derived from adipic acid. Moreover, the increasing focus on sustainable manufacturing practices and the development of bio-circular production pathways are creating new growth avenues for adipic acid producers in the country.

To get more information on this market Request Sample

Adipic Acid Market Trends:

Growing Demand for Lightweight Automotive Materials

The escalating demand for lightweight materials in the automotive industry is significantly driving adipic acid consumption globally. Nylon 66, produced using adipic acid, is increasingly replacing traditional metals in vehicle components, such as engine covers, air intake manifolds, radiator end tanks, and structural under-hood parts due to its superior strength-to-weight ratio, thermal resistance, and durability. As automakers intensify efforts to reduce vehicle weight for improved fuel efficiency and compliance with stringent carbon emission standards, the utilization of engineering plastics derived from adipic acid continues to expand. Global car production reached over 92.5 Million units in 2024, sustaining robust demand for nylon 66-based engineering plastics. The transition toward EVs is further amplifying this trend, as lighter vehicles require less energy for propulsion, extending battery range and reducing overall energy consumption. Additionally, the growing adoption of nylon 66 in airbag fabrics, tire reinforcement cords, and brake components is enhancing vehicle safety and performance standards worldwide.

Rising Focus on Sustainable Bio-Based Production

Increasing emphasis on environmental sustainability is transforming the adipic acid market outlook and competitive dynamics. Conventional adipic acid manufacturing through cyclohexane oxidation generates significant nitrous oxide emissions. This has prompted industry participants to invest in alternative production routes, including microbial fermentation using renewable feedstocks and catalytic conversion of biomass-derived compounds. Through the European Green Deal, the European Union has established a target to reduce greenhouse gas emissions by at least 55% by 2030, encouraging manufacturers across the chemical sector to transition towards bio-based and recycled chemical products. The adoption of mass-balance approaches for producing bio-circular nylon 66 from sustainable feedstocks is gaining traction among leading manufacturers. Furthermore, regulatory frameworks mandating lower emissions from chemical plants are accelerating investment in advanced abatement technologies and greener production pathways, positioning sustainability as a core driver of long-term market evolution.

Expanding Polyurethane and Plasticizer Applications

The growing utilization of adipic acid in polyurethane and plasticizer manufacturing is creating significant demand expansion beyond traditional nylon applications. Adipic acid-based polyester polyols are essential components in producing flexible and semi-rigid polyurethane foams widely used in furniture cushioning, insulation materials, and footwear. The escalating construction activity and rising consumer spending on home furnishings are driving polyurethane foam consumption globally. Moreover, adipate esters derived from adipic acid are gaining prominence as non-phthalate plasticizers in flexible PVC products, benefiting from regulatory shifts away from traditional phthalate-based formulations. The increasing demand for flexible packaging materials, medical tubing, wire insulation, and flooring products is reinforcing the adipic acid market forecast over the coming years.

Adipic Acid Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global adipic acid market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on end product, application, and end user.

Analysis by End Product:

- Nylon 66 Fibers

- Nylon 66 Engineering Resins

- Polyurethanes

- Adipate Esters

- Others

Nylon 66 fibers hold 33% of the market share, serving as the foundational material for a wide range of industrial and consumer textile products. In order to manufacture these fibers, adipic acid and hexamethylenediamine are polycondensed, producing a polymer with remarkable tensile strength, abrasion resistance, and thermal stability. Nylon 66 fibers are mostly used in the automotive sector to make seat belt webbing, tire reinforcing cords, airbag materials, and under-hood textiles that need to withstand high temperatures. In addition to automobiles, nylon 66 fibers are widely utilized in industrial filtration materials, carpeting, clothing, ropes, and conveyor belts. The steady demand from the consumer and industrial sectors guarantees the continuous use of adipic acid through nylon 66 fiber production channels worldwide.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

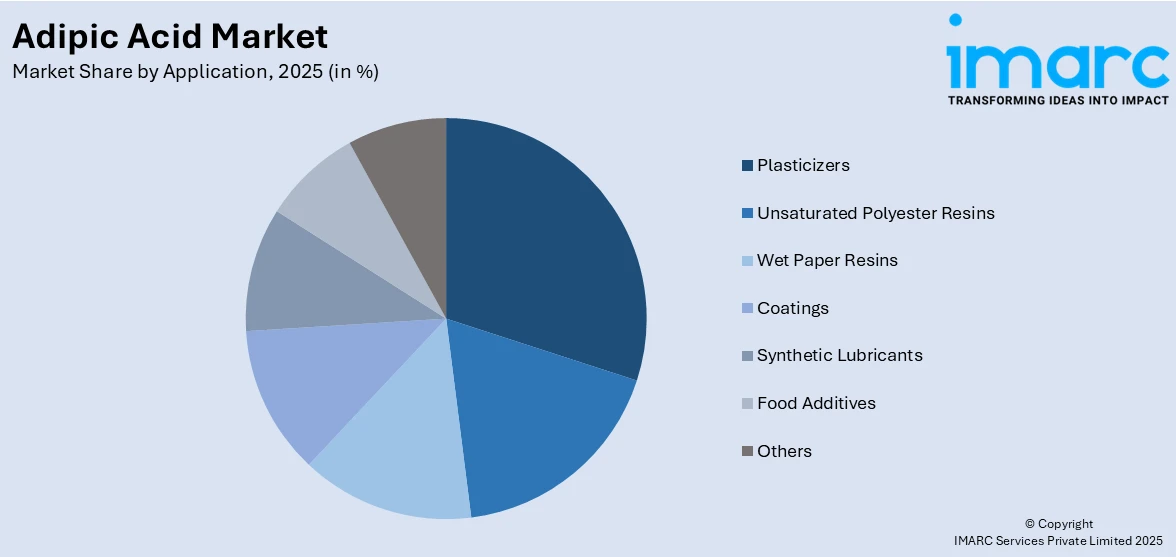

- Plasticizers

- Unsaturated Polyester Resins

- Wet Paper Resins

- Coatings

- Synthetic Lubricants

- Food Additives

- Others

Plasticizers lead the market with a share of 26%. Plasticizers based on adipic acid, especially adipate esters like dioctyl and diisononyl adipate, are crucial ingredients in flexible PVC formulations used in a variety of industrial applications. These plasticizers are preferred over conventional phthalate-based substitutes due to their exceptional resistance to extraction, lower volatility, and better low-temperature performance. Adipate-based formulations are becoming increasingly popular as a result of regulatory changes in regions like Europe and North America, which favor non-phthalate plasticizers. Consumer products, medical tubing, food packaging films, construction floors, and automobile cable insulation are some of the main applications. Consumption of adipic acid-based plasticizers is also being driven by the growing construction sector in emerging economies and the rising need for flexible, environment-friendly packaging materials. Worldwide, this application segment is growing steadily, owing to strict environmental rules that favor safer plasticizer formulas.

Analysis by End User:

- Automotive

- Electrical and Electronics

- Textiles

- Food and Beverage

- Personal Care

- Pharmaceuticals

- Others

Automotive dominates the market, with a share of 32%, spurred by the widespread use of nylon 66 engineered plastics and fibers in the production of automobiles. Lightweight yet robust parts, such as engine covers, radiator end tanks, cylinder head covers, air intake manifolds, fuel system components, and electrical connectors, are made from polyamide 66, which is derived from adipic acid. The use of engineering plastics, in place of conventional metal components, has increased due to the surging need to reduce vehicle weight, in order to increase fuel economy and lower carbon emissions. This trend is further reinforced by the rapid adoption of EVs, which require lightweight materials to enhance battery efficiency and extend driving range. According to the International Energy Agency (IEA), electric car sales exceeded 17 Million globally in 2024, driving substantial demand for lightweight nylon 66 components.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia-Pacific, accounting for 40% of the share, enjoys the leading position in the market. The region’s dominance is underpinned by the presence of large-scale chemical manufacturing facilities, rapidly growing automotive and textile industries, and substantial government support for industrial expansion. China serves as one of the largest manufacturers and consumers of adipic acid, with a comprehensive production infrastructure spanning the entire nylon 66 value chain from upstream raw materials to downstream polymer processing. India is emerging as a high-growth market, driven by expanding automotive manufacturing, rising textile consumption, and increasing adoption of polyurethane-based products in construction and packaging applications. As per IMARC Group, the India textile market size was valued at USD 152.40 Billion in 2025. Japan and South Korea contribute through advanced engineering plastics production and strong automotive sector demand. The region’s competitive cost structure, abundant raw material availability, and favorable trade dynamics continue to reinforce Asia-Pacific’s leading position in the market.

Key Regional Takeaways:

North America Adipic Acid Market Analysis

North America represents a significant market for adipic acid, supported by a mature chemical manufacturing sector, strong automotive production base, and well-established demand from the nylon 66 and polyurethane industries. The region benefits from the presence of world-scale adipic acid production facilities, particularly in the United States, which house some of the largest integrated nylon 66 value chain operations globally. The automotive industry remains the primary demand driver, with nylon 66 engineering plastics extensively used in manufacturing lightweight structural components, electrical connectors, and under-hood applications. The region’s increasing focus on sustainability is also shaping market dynamics, with manufacturers investing in bio-circular and mass-balance production pathways to reduce the carbon footprint of nylon 66 and related products. The polyurethane sector contributes additional demand through applications in furniture cushioning, automotive seating, building insulation, and footwear manufacturing. Furthermore, regulatory developments surrounding emission standards and environmental compliance are encouraging innovation in production technologies and supporting the adoption of greener chemical processes across the adipic acid supply chain in North America.

United States Adipic Acid Market Analysis

The United States represents one of the most established markets for adipic acid, anchored by the presence of world-class production facilities and a diversified downstream industrial base. The country’s automotive sector drives substantial demand for nylon 66 engineering plastics used in engine components, structural parts, airbag fabrics, and electrical connectors, supporting sustained adipic acid consumption. The growing EV segment is creating incremental demand for lightweight nylon-based materials to improve energy efficiency and extend driving range. As per IMARC Group, the United States electric car market size was valued at USD 102.6 Billion in 2025, creating incremental demand for lightweight adipic acid-derived polymer materials. The aerospace and defense sectors provide additional consumption channels for high-performance nylon 66 fibers and resins. The food and beverage (F&B) industry also utilizes adipic acid as a regulated food additive for acidulation and flavoring in processed products. The country’s robust research and development (R&D) ecosystem is fostering innovation in sustainable production technologies, including bio-based and bio-circular adipic acid manufacturing pathways, positioning the United States as a leader in the transition towards greener chemical production methods.

Europe Adipic Acid Market Analysis

Europe is a significant market for adipic acid, driven by a strong automotive manufacturing base, stringent sustainability regulations, and growing demand for bio-based chemical products. Germany, France, and the United Kingdom are key contributors, with well-established polyamide and polyurethane production infrastructures supporting diversified industrial applications. The European Union’s regulatory framework is accelerating the transition towards sustainable and bio-based adipic acid production methods. The automotive industry continues to drive demand for nylon 66 engineering plastics in vehicle lightweighting applications. Additionally, the expanding adoption of non-phthalate adipate-based plasticizers in construction, healthcare, and packaging is creating sustained growth opportunities across the European market. Furthermore, increasing investments in circular economy initiatives and recycling-compatible polymer solutions are reinforcing long-term demand for adipic acid derivatives across multiple end-use sectors.

Asia-Pacific Adipic Acid Market Analysis

Asia-Pacific leads the global adipic acid market, driven by the region’s rapidly expanding automotive and textile sectors, extensive chemical manufacturing capabilities, and favorable government industrial policies. China is among the top producers and consumers, featuring an extensive manufacturing infrastructure that encompasses the entire polyamide value chain. As of November 2024, China’s production of new energy vehicles (NEVs) exceeded 10 Million units for the first time in 2024, according to CAAM, driving substantial demand for lightweight nylon 66 automotive components derived from adipic acid. Additionally, strong growth in textile manufacturing and rising consumption of synthetic fibers for apparel and industrial applications are among the major adipic acid market trends across the Asia-Pacific region.

Latin America Adipic Acid Market Analysis

Latin America represents a growing market for adipic acid, supported by expanding automotive manufacturing, construction activity, and increasing adoption of polyamide-based industrial products. Brazil and Mexico serve as the primary demand centers, driven by their established automotive production bases and growing textile sector. The packaging industry is emerging as a supplementary demand driver, with rising consumption of flexible PVC products and polyurethane materials. Government infrastructure development programs are further supporting steady consumption growth across the region.

Middle East and Africa Adipic Acid Market Analysis

The Middle East and Africa region represents an emerging market for adipic acid, driven by increasing industrialization, growing construction activity, and expanding manufacturing sectors. The UAE and South Africa serve as the primary demand hubs, supported by infrastructure development projects and rising adoption of polymer-based construction materials. For instance, the total value of construction contracts awarded in the UAE increased by 14% year-on-year in 2024, totaling USD 121 Billion, driving demand for polyurethane-based insulation materials and polymer-based construction products derived from adipic acid. The automotive sector is contributing incremental demand as vehicle assembly operations expand across the region.

Competitive Landscape:

The global adipic acid market features a consolidated competitive landscape, with leading manufacturers investing in capacity optimization, sustainable production methods, and strategic asset realignment. Key industry participants are focusing on backward integration across the nylon 66 value chain to ensure supply reliability and cost efficiency. Several producers have shifted production from high-cost European sites to more competitive facilities in Asia-Pacific, reflecting broader trends in global chemical manufacturing. The pursuit of bio-based adipic acid through fermentation and catalytic pathways is emerging as a critical competitive differentiator. Major players are committing resources to reduce greenhouse gas emissions, particularly nitrous oxide, and align with evolving environmental regulations, while exploring strategic partnerships and acquisitions to strengthen their market positions. These strategies are collectively enhancing operational resilience and reinforcing long-term competitiveness in the global adipic acid market.

The report provides a comprehensive analysis of the competitive landscape in the adipic acid market with detailed profiles of all major companies, including:

- Asahi Kasei Corporation

- Ascend Performance Materials

- BASF SE

- Domo Chemicals

- Invista (Koch Industries)

- Lanxess AG

- Radici Partecipazioni SpA

- Solvay S.A.

- Sumitomo Chemical Co. Ltd.

- Tangshan Zhonghao Chemical Co. Ltd.

- TCI Chemicals (India) Pvt. Ltd.

- Tian Li High & New Tech Co. Ltd.

Latest News and Developments:

- In July 2025, BASF completed the acquisition of DOMO Chemicals' 49% stake in the Alsachimie joint venture, resulting in BASF becoming the exclusive owner of the production facility for key polyamide 6.6 precursors, such as KA-oil, adipic acid, and hexamethylenediamine adipate in Chalampe, France. The purchase bolstered BASF’s operational presence at its European center for PA 6.6 manufacturing, improving backward integration and supply dependability throughout the value chain.

Adipic Acid Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| End Products Covered | Nylon 66 Fibers, Nylon 66 Engineering Resins, Polyurethanes, Adipate Esters, Others |

| Applications Covered | Plasticizers, Unsaturated Polyester Resins, Wet Paper Resins, Coatings, Synthetic Lubricants, Food Additives, Others |

| End Users Covered | Automotive, Electrical and Electronics, Textiles, Food and Beverage, Personal Care, Pharmaceuticals, Others |

| Region Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Asahi Kasei Corporation, Ascend Performance Materials, BASF SE, Domo Chemicals, Invista (Koch Industries), Lanxess AG, Radici Partecipazioni SpA, Solvay S.A., Sumitomo Chemical Co. Ltd., Tangshan Zhonghao Chemical Co. Ltd., TCI Chemicals (India) Pvt. Ltd., Tian Li High & New Tech Co. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the adipic acid market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global adipic acid market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter’s Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the adipic acid industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Adipic Acid Market Report

The adipic acid market was valued at USD 6.9 Billion in 2025.

The adipic acid market is projected to exhibit a CAGR of 5.03% during 2026-2034, reaching a value of USD 10.73 Billion by 2034.

The key factors driving the adipic acid market include the rising demand for nylon 66 in the automotive and textile sectors, the growing adoption of lightweight engineering plastics for vehicle manufacturing, expanding polyurethane applications in construction and furniture, and the increasing shift towards non-phthalate adipate-based plasticizers across the healthcare, packaging, and consumer goods industries.

Asia-Pacific currently dominates the adipic acid market, accounting for a share of 40%. The region benefits from extensive chemical manufacturing infrastructure, robust demand from the automotive and textile sectors, and the presence of major producers driving consumption across polyamide and polyurethane applications.

Some of the major players in the adipic acid market include Asahi Kasei Corporation, Ascend Performance Materials, BASF SE, Domo Chemicals, Invista (Koch Industries), Lanxess AG, Radici Partecipazioni SpA, Solvay S.A., Sumitomo Chemical Co. Ltd., Tangshan Zhonghao Chemical Co. Ltd., TCI Chemicals (India) Pvt. Ltd., Tian Li High & New Tech Co. Ltd., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade