Adult Diaper Market Size, Share, Trends and Forecast by Type, Distribution Channel, and Region, 2026-2034

Adult Diaper Market Size, Share, Trends & Forecast (2026-2034)

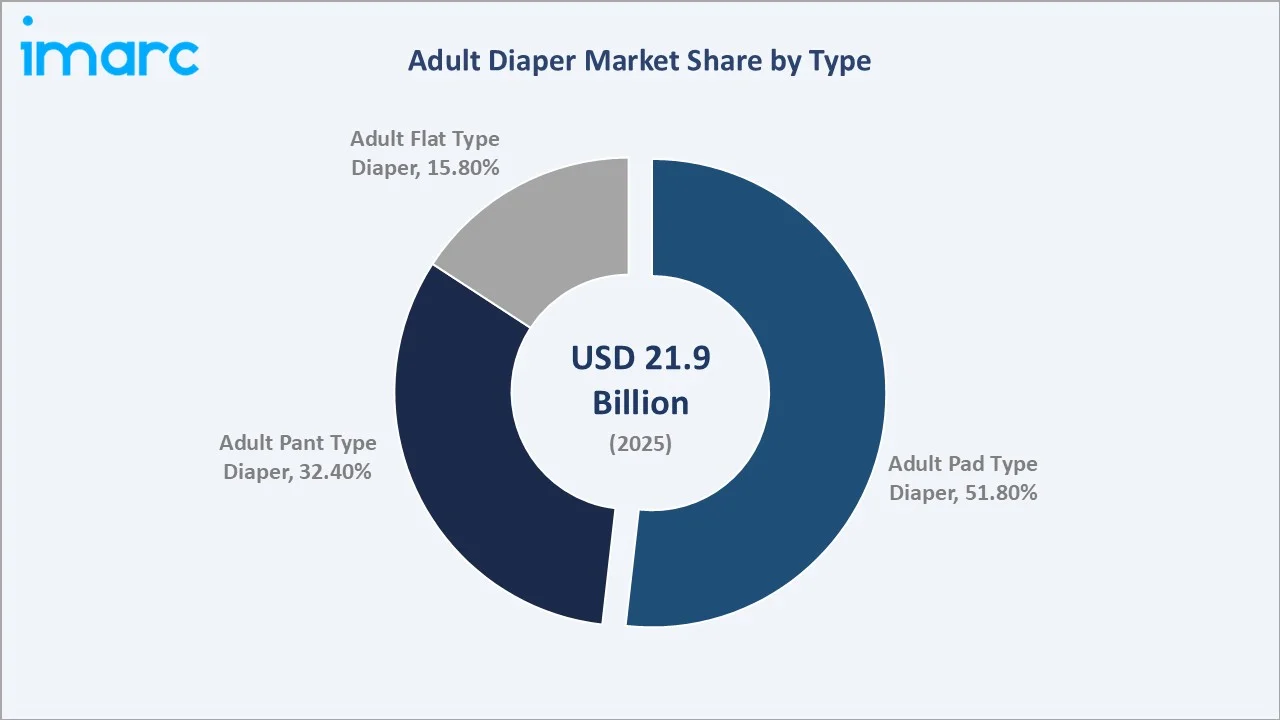

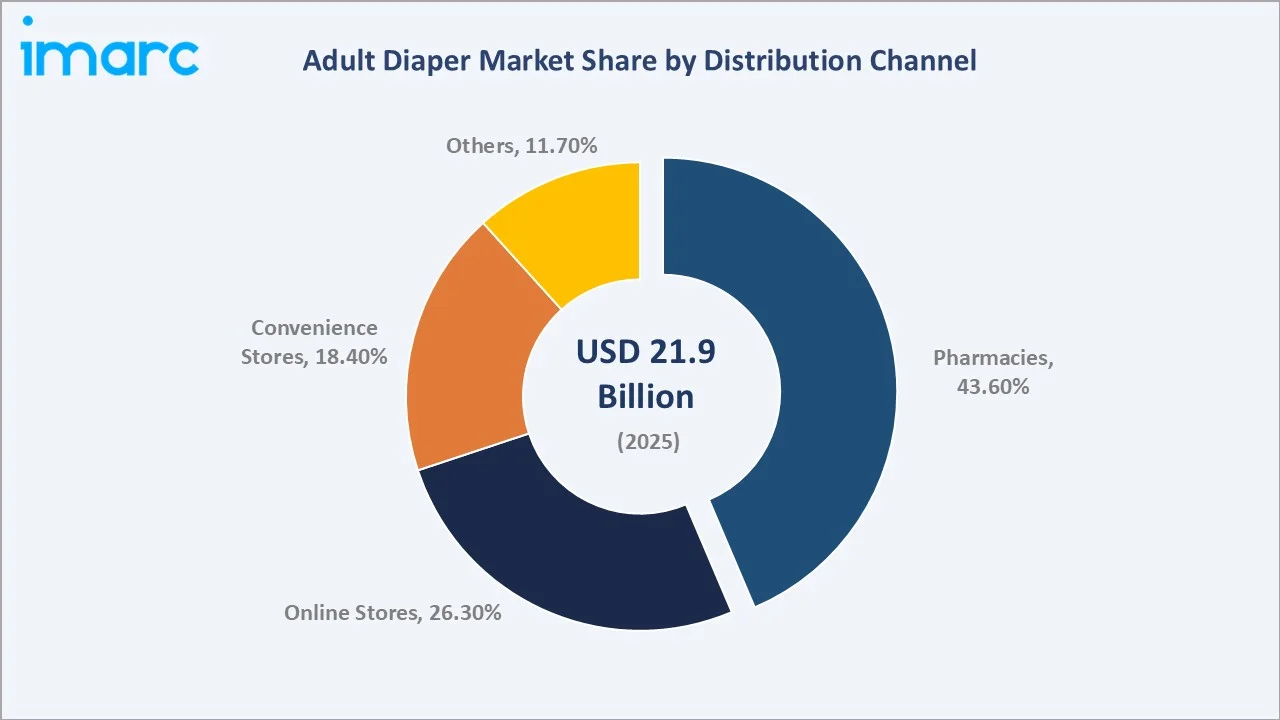

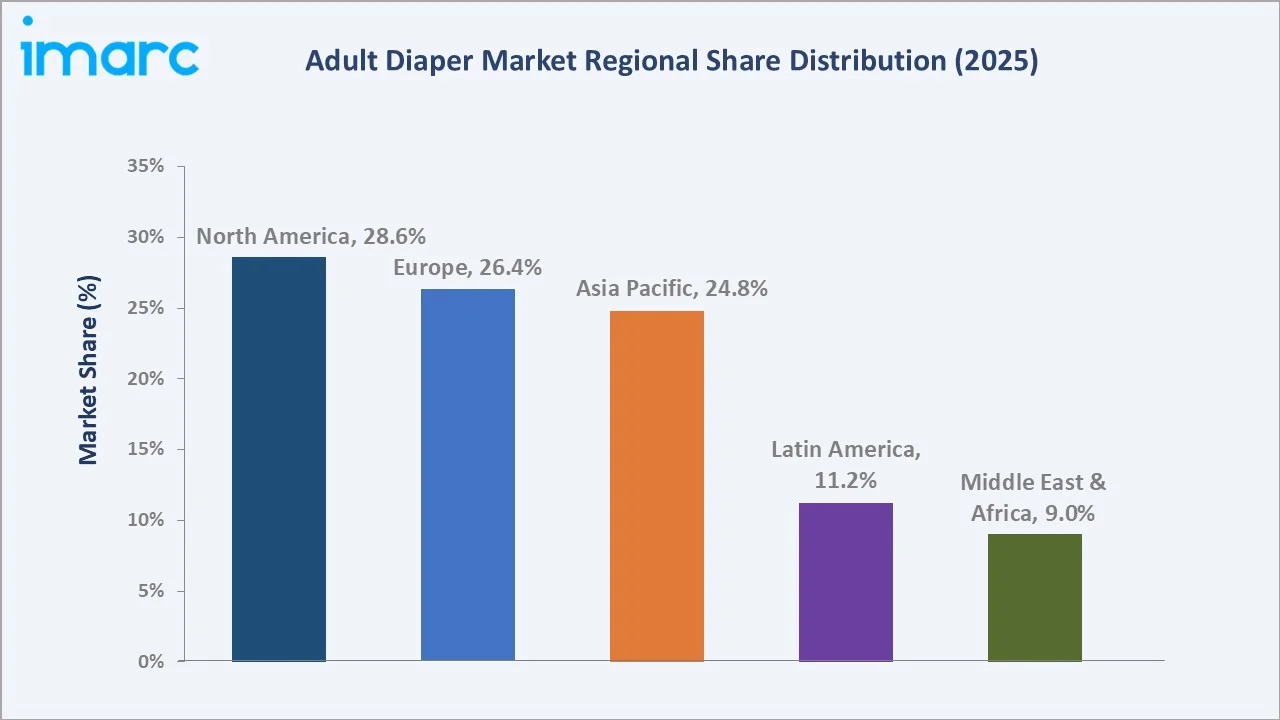

The global adult diaper market size was valued at USD 21.9 Billion in 2025 and is projected to reach USD 37.4 Billion by 2034, exhibiting a CAGR of 5.80% during 2026-2034. Growth is primarily driven by an accelerating global geriatric population, the Population Reference Bureau (PRB) reports that 10% of the global population is currently aged 65 and older, rising incontinence prevalence, advancements in product technology, and expanding retail accessibility through online and pharmacy channels. Adult Pad Type Diapers lead the type segment at 51.8% in 2025, while Pharmacies dominate distribution at 43.6%. North America holds the largest regional share at 28.6%, underpinned by a large aging demographic and robust home healthcare infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 21.9 Billion |

|

Forecast Market Size (2034) |

USD 37.4 Billion |

|

CAGR (2026-2034) |

5.80% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (28.6% share, 2025) |

|

Fastest Growing Channel |

Online Stores (CAGR ~9.3%, 2026-2034) |

|

Leading Type |

Adult Pad Type Diaper (51.8%, 2025) |

|

Leading Distribution Channel |

Pharmacies (43.6%, 2025) |

To get more information on this market, Request Sample

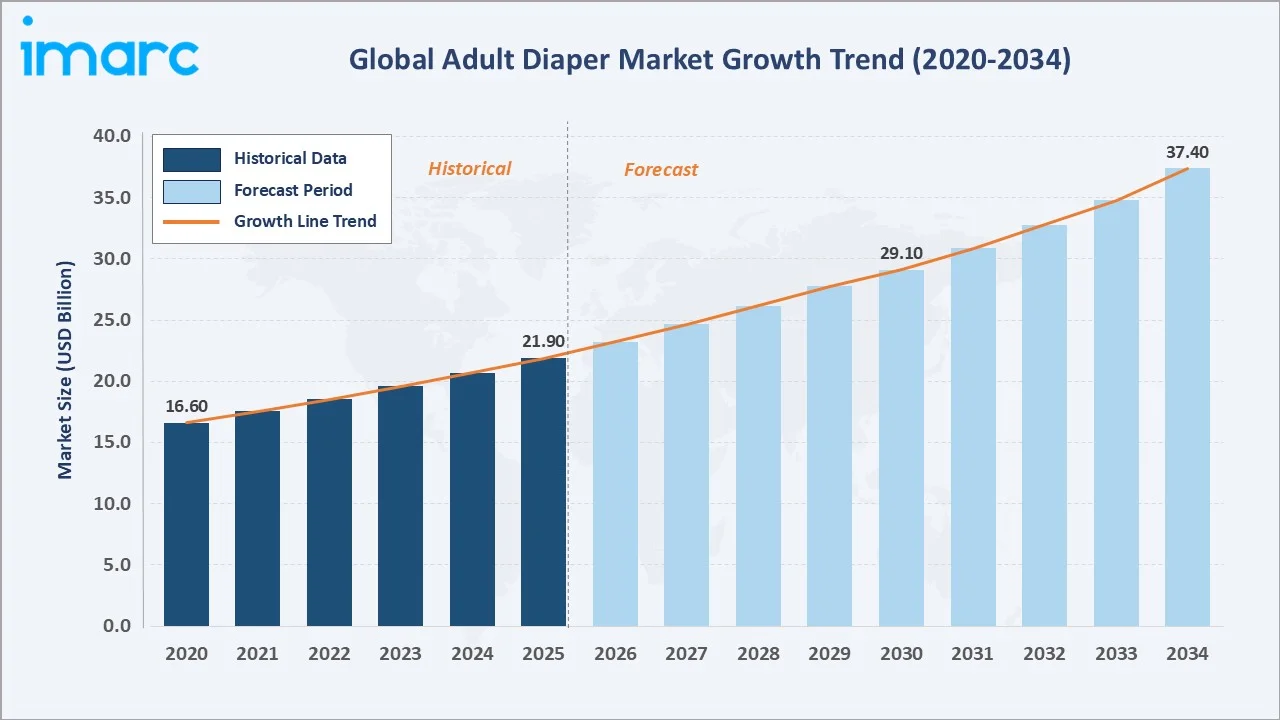

Figure 1 shows steady market growth from USD 16.6 Billion in 2020 to USD 37.4 Billion by 2034, with CAGR 5.80%, driven by rising institutional adoption, innovation, and global aging trends.

Executive Summary

The global adult diaper market is expanding due to aging demographics, evolving healthcare systems, and product innovation, growing from USD 21.9 Billion in 2025 to USD 37.4 Billion by 2034 at 5.80% CAGR. According to the Population Reference Bureau (PRB), roughly 10% of the global population, approximately 800 million individuals, is aged 65 and above, creating a structurally large and growing consumer base for incontinence management products.

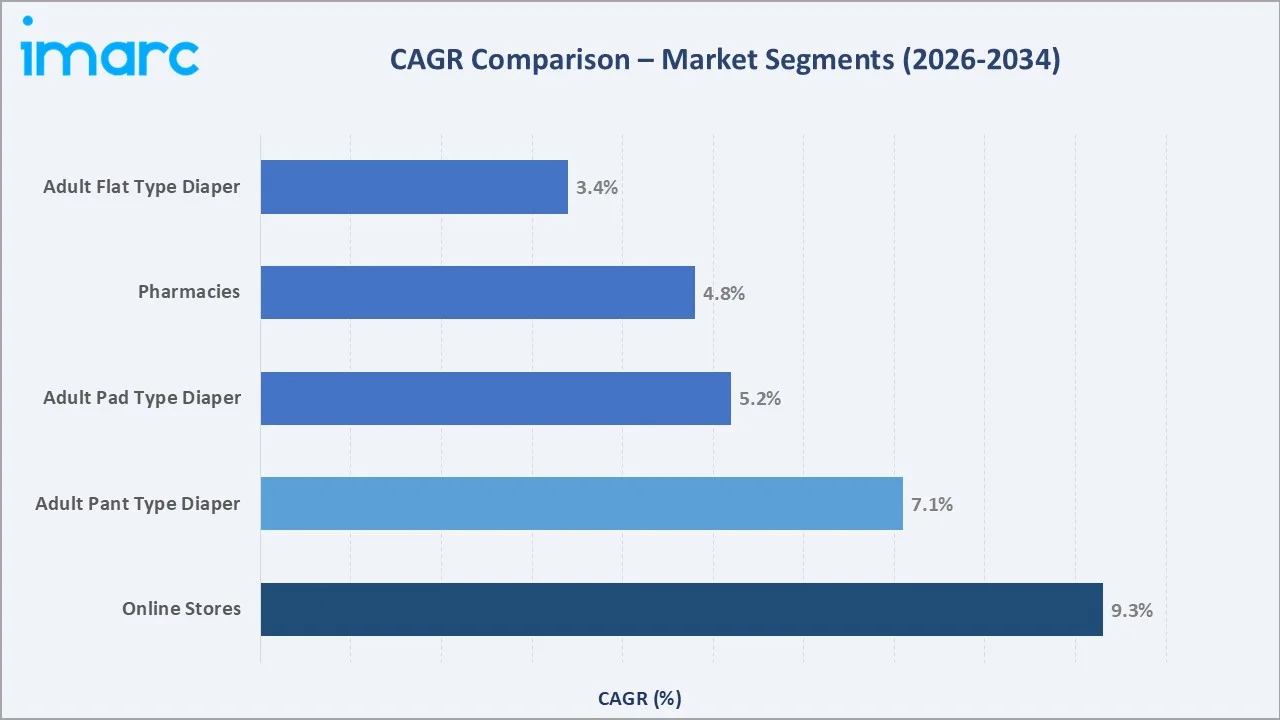

Adult pad type diapers lead with 51.8% in 2025, while pant type grows fastest at ~7.1% CAGR. Pharmacies hold 43.6%, and Online Stores expand at ~9.3% CAGR. North America accounts for 28.6% of global revenue in 2025, led by the United States were number of Americans ages 65 and older is projected to increase from 58 million in 2022 to 82 million by 2050 (a 42% increase). Europe follows at 26.4%, driven by aging populations in Germany, France, and Italy. Asia Pacific holds 24.8%, with Japan, where citizens aged 65+ already exceed 29% of the population, and China as the primary growth engines.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

Adult Pad Type Diaper - 51.8% share (2025) |

|

Fastest Growing Type Segment |

Adult Pant Type Diaper - CAGR ~7.1% (2026-2034) |

|

Leading Distribution Channel |

Pharmacies - 43.6% share (2025) |

|

Fastest Growing Channel |

Online Stores - CAGR ~9.3% (2026-2034) |

|

Leading Region |

North America - 28.6% revenue share (2025) |

|

Top Companies |

Unicharm, Kimberly-Clark, P&G, Essity, Ontex |

|

Key Market Driver |

Aging population (10% of world aged 65+, PRB data) |

|

Market Opportunity |

Online distribution + smart diaper technology integration |

The Following Analytical Observations Expand Upon the Structured Data Above:

- Adult Pad Type Diapers hold 51.8% share in 2025, reflecting strong institutional demand from nursing homes, hospitals, and homecare settings where moderate-to-heavy absorbency products are preferred for bedridden patients.

- Adult Pant Type Diapers, at 32.4% in 2025, are the fastest-growing type at ~7.1% CAGR (2026-2034), as pull-up designs cater to mobile users and reduce stigma through underwear-like aesthetics.

- Pharmacies control 43.6% of distribution in 2025, benefiting from trusted healthcare advisor positioning, immediate product availability, and insurance claim processing capabilities.

- Online Stores at 26.3% (2025) represent the fastest-growing channel at ~9.3% CAGR, leveraging subscription models, discreet home delivery, and competitive pricing for privacy-conscious consumers.

- North America accounts for 28.6% in 2025, driven by the aging population, with Americans aged 65+ rising from 58 million in 2022 to 82 million by 2050

Global Adult Diaper Market Overview

Adult diapers, or adult incontinence products, are absorbent solutions for managing urinary and fecal incontinence, available in pad, pant, and flat/tape types, and used across homecare, hospitals, and long-term care settings.

Macroeconomic enablers include rising global life expectancy now averaging 73.4 years globally (WHO, 2024), escalating chronic disease burden (537 million adults (10.5%) aged 20–79 years were living with diabetes in 2021), increasing healthcare expenditure, and a growing middle class in emerging economies with heightened awareness of hygiene product benefits. The proliferation of e-commerce, Global B2C ecommerce revenue is expected to grow to USD$5.5 trillion by 2027 at a steady 14.4% compound annual growth rate, will substantially improve product accessibility in previously underserved geographies.

Market Dynamics

To evaluate market opportunities, Request Sample

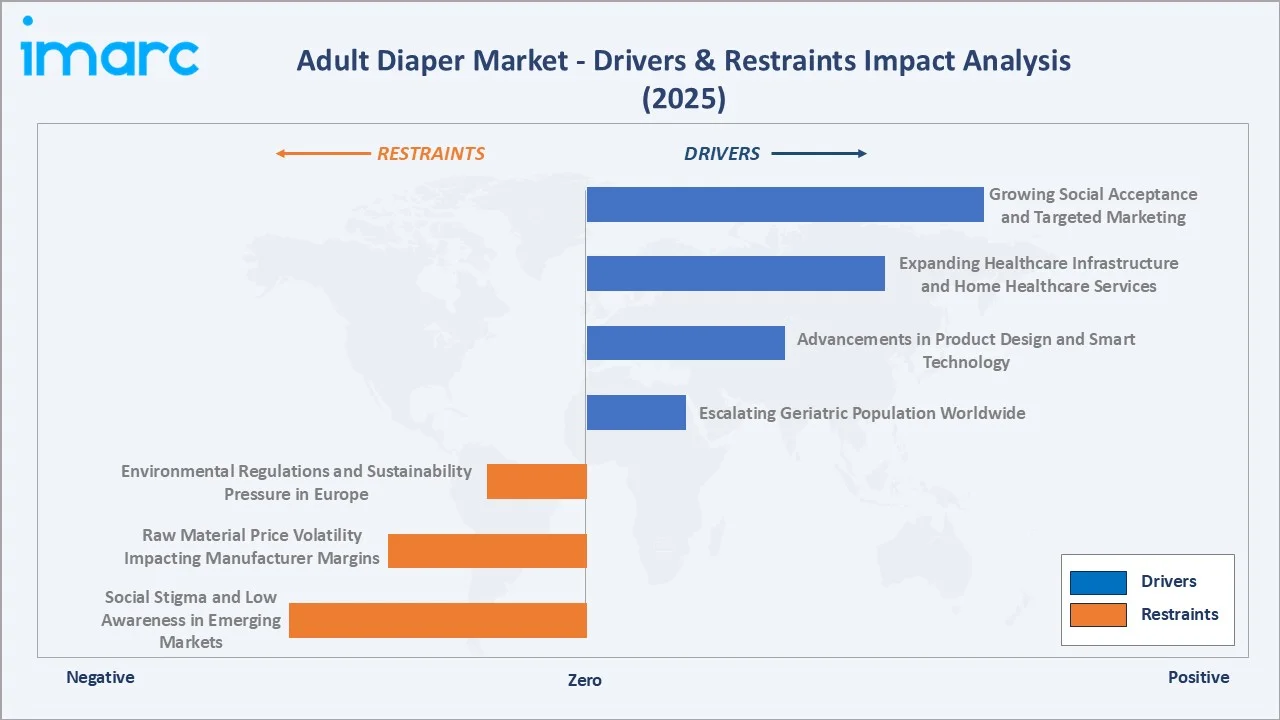

Market Drivers

- Escalating Geriatric Population Worldwide: The growing elderly population is a key driver for adult incontinence products, with individuals aged 65+ representing around 10% of the global population. PRB projects 82 million Americans aged 65+ by 2050 (23% of the population), while Japan reported 29.1% elderly in 2023–2024. Additionally, diabetes cases are expected to rise from 537 million in 2021 to 853 million by 2050, further increasing incontinence-related demand.

- Advancements in Product Design and Smart Technology: Continuous innovation in absorbent hygiene products, including ultra-thin cores, advanced SAP, odor control, and breathable materials, is expanding adoption. Smart adult diapers with IoT-based moisture sensors are gaining traction in hospitals and long-term care facilities, improving monitoring and outcomes. Additionally, homecare expansion and discreet product formats supporting active lifestyles continue to drive market growth and investment.

- Expanding Healthcare Infrastructure and Home Healthcare Services: Home-based healthcare expansion is boosting adult incontinence demand among elderly and post-hospitalization patients, with caregiver recommendations, trained staff availability, and remote monitoring supporting adoption and sustained market growth.

- Growing Social Acceptance and Targeted Marketing: Rising awareness and reduced stigma are expanding adoption across age groups, with healthcare campaigns and targeted marketing normalizing adult diaper use, including younger consumers during post-partum and post-surgical recovery.

Market Restraints

- Social Stigma and Low Awareness in Emerging Markets: Persistent social stigma surrounding adult incontinence and limited awareness in developing economies continue to restrict product adoption, particularly among lower-income consumers in sub-Saharan Africa, South Asia, and rural Latin America. Cultural discomfort, lack of education about incontinence management, and affordability constraints significantly reduce market penetration in price-sensitive regions, slowing adoption of adult diaper products in emerging markets.

- Raw Material Price Volatility Impacting Manufacturer Margins: Volatility in key raw materials — including superabsorbent polymers (SAP), fluff pulp, and polypropylene nonwoven fabrics — continues to pressure manufacturer margins. Fluctuations in wood pulp and polymer feedstock prices directly influence diaper production costs, while supply chain disruptions and crude-oil-linked polymer price swings further complicate cost forecasting and pricing strategies for hygiene product manufacturers.

- Environmental Regulations and Sustainability Pressure in Europe: Growing environmental concerns and regulatory pressure, particularly under the EU Single-Use Plastics Directive (EU 2019/904), are increasing compliance costs for diaper manufacturers. These regulations aim to reduce plastic waste, enforce labeling requirements, and promote sustainable alternatives, prompting manufacturers to reformulate products and invest in biodegradable and recyclable materials.

Market Opportunities

- Growing Demand for Biodegradable and Eco-Friendly Adult Diapers: Biodegradable adult diapers present strong growth opportunities, driven by sustainability awareness in Europe and North America. Plant-based, low-plastic products enable premium pricing and differentiation in mature markets.

- Expansion of Online Subscription and Direct-to-Consumer Models: Online subscription models drive recurring revenue and retention, while DTC channels enable automatic reordering and discreet purchasing. Rising e-commerce penetration further supports long-term subscription-based growth.

- Rising Healthcare Spending in Underpenetrated Asia Pacific Markets: Underpenetrated healthcare systems across Asia Pacific, particularly rural China, India, Indonesia, and the Philippines, present strong volume-growth opportunities. Rising per-capita healthcare expenditure, expanding elderly populations, and improving healthcare infrastructure are increasing awareness and accessibility of adult incontinence products, supporting market expansion in emerging economies.

Market Challenges

- Concentrated Raw Material Supply and Pricing Risks: The adult diaper industry faces supply chain concentration risks, particularly for superabsorbent polymers (SAP), which are produced by a limited number of global suppliers. Dependence on major chemical manufacturers increases vulnerability to price fluctuations, production disruptions, and availability constraints, creating cost uncertainty across the global hygiene product manufacturing base.

- Rising Competition from Private-Label and Regional Manufacturers: Intense price competition from private-label brands and regional manufacturers, particularly in Asia Pacific and Latin America, continues to compress margins for established brands. Retailers are expanding store-brand incontinence products at competitive price points, while local manufacturers offer lower-cost alternatives, increasing pricing pressure and limiting premium product growth.

- Complex Regulatory Compliance Across Multiple Markets: Regulatory compliance across the EU, U.S., and Asia creates challenges, as varying standards for safety, absorbency, and labeling increase certification costs, reformulation needs, and time-to-market complexity.

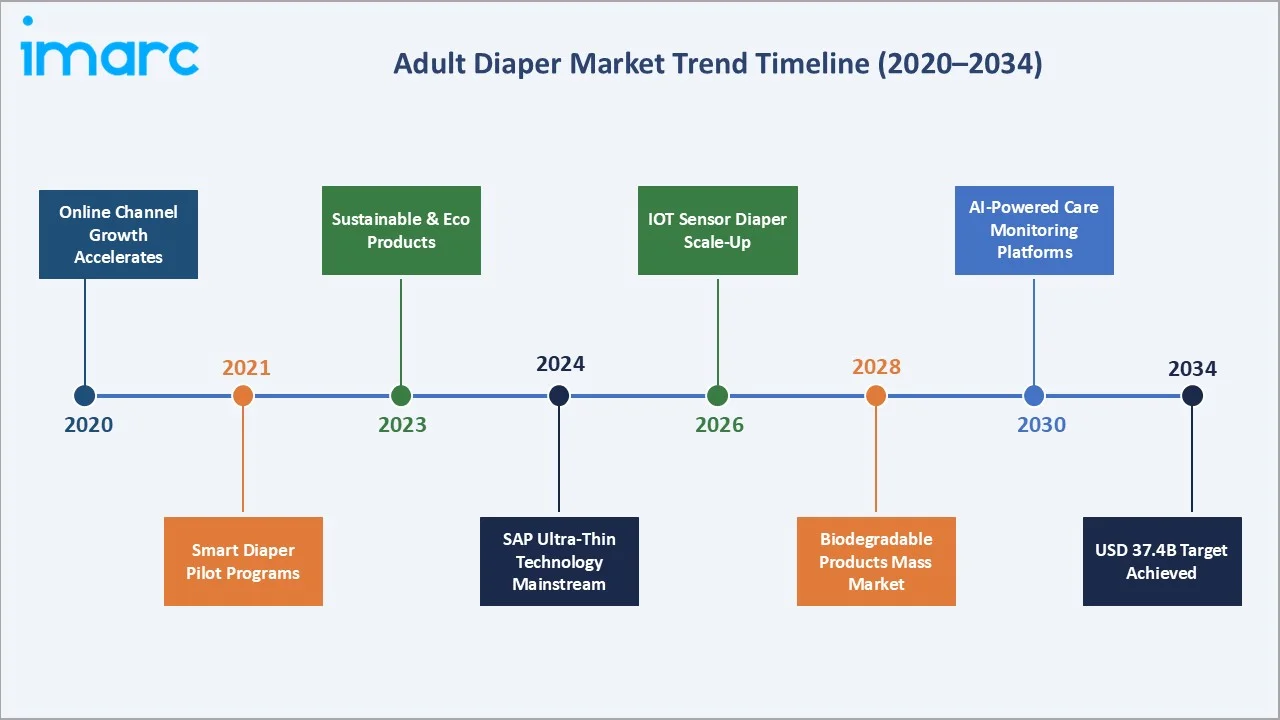

Emerging Market Trends

Figure 5 maps the transformative milestones shaping adult diaper market evolution, from the 2020 acceleration of online channel growth through the projected 2034 attainment of the USD 37.4 Billion market target, driven by smart technology, sustainable materials, and AI-powered care platforms.

1. Smart Diaper Technology and IoT Integration

Sensor-enabled smart diapers, deployed from pilots in Japan and Europe, reduce caregiver workload and improve monitoring. Companies like Ontex and Panasonic are expanding adoption in hospitals and nursing homes.

2. Biodegradable and Sustainable Product Development

Rising demand for eco-friendly hygiene products and EU sustainability regulations are driving biodegradable innovations. Companies like Essity and Kimberly-Clark are expanding sustainable adult incontinence portfolios.

3. Online Subscription Models Reshaping Distribution

E-commerce and subscription models are transforming adult diaper distribution, with platforms like Amazon Subscribe & Save and Walmart+ driving recurring purchases, convenience, discounts, and rapid online channel growth globally.

4. Premiumization and Lifestyle-Oriented Product Design

Growing demand from active adults experiencing light-to-moderate incontinence is encouraging manufacturers to develop thinner, discreet, and body-contoured products. Premium offerings emphasizing comfort, odor control, and lifestyle integration are gaining traction, particularly in North America and Europe. This shift toward premium products is supporting higher average selling prices and stronger margins for manufacturers.

5. Institutional Channel Growth in Asia Pacific

Rapid aging and government-backed eldercare programs in Japan, China, and South Korea are increasing institutional demand, with hospitals and nursing homes driving stable procurement across Asia Pacific.

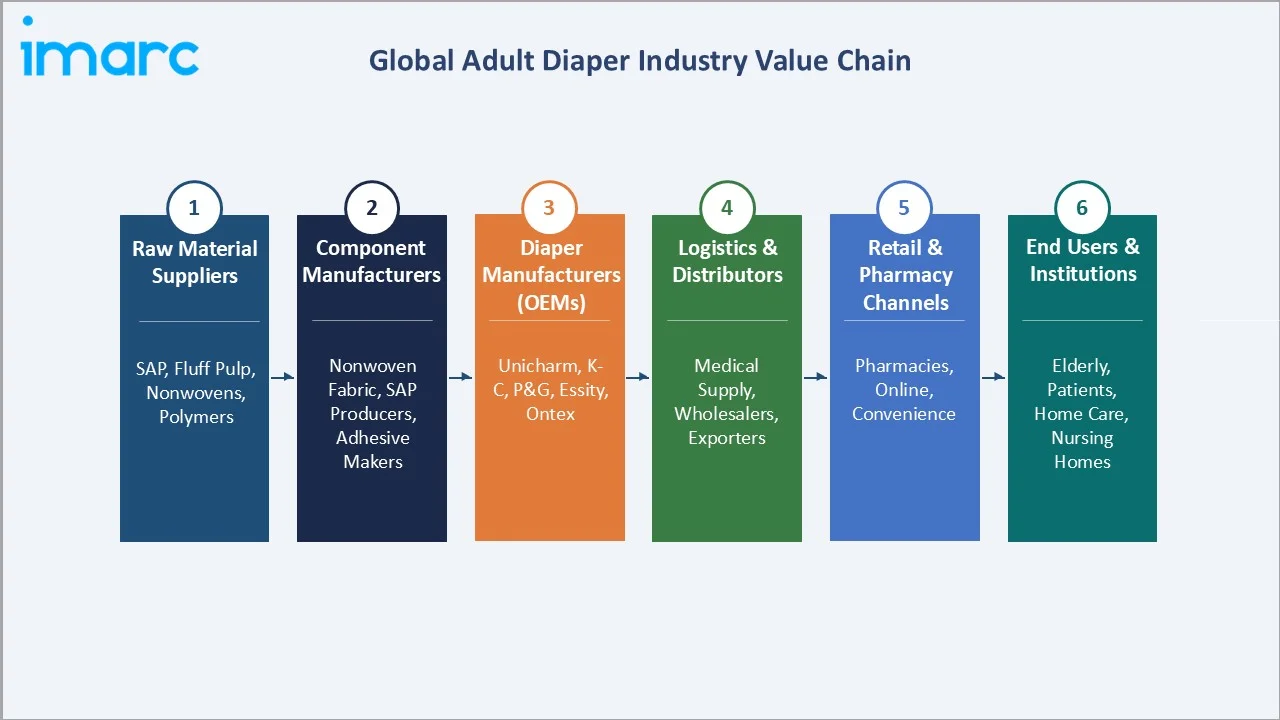

Industry Value Chain Analysis

The adult diaper value chain spans six stages, with superabsorbent polymer (SAP) as a critical input. Concentrated SAP production among global chemical companies creates upstream supply risk. Diaper manufacturing is capital-intensive and automated, with world-scale production lines capable of manufacturing 600–1,000 diapers per minute.

|

Stage |

Key Players / Examples |

|

Raw Material Suppliers |

SAP (Superabsorbent Polymers), Fluff Pulp Producers, Nonwoven Fabric Manufacturers, Polymers & Film Suppliers (BASF, Evonik, Weyerhaeuser) |

|

Component Manufacturers |

Nonwoven Fabric Makers, SAP Producers, Adhesive Makers, Elastic & Closure Component Suppliers (Berry Global, Avgol Nonwovens, Fitesa) |

|

Diaper Manufacturers (OEMs) |

Unicharm Corporation, Kimberly-Clark (K-C), Procter & Gamble (P&G), Essity, Ontex Group, Domtar, Chiaus (Fujian) |

|

Logistics & Distributors |

Medical Supply Chains, Wholesalers, Exporters & Import Agents, Third-Party Logistics Providers (3PLs), Regional Warehousing Networks |

|

Retail & Pharmacy Channels |

Pharmacies (43.6% share), Online Retail/E-Commerce (26.3%), Convenience & Grocery Stores (18.4%), Hospital & Institutional Supply Chains |

|

End Users & Institutions |

Elderly Individuals, Post-Surgical Patients, Home Care Recipients, Nursing Homes & Long-Term Care Facilities, Hospitals & Rehabilitation Centers |

Figure 6 presents the six-stage value chain from raw material suppliers to end users, with distribution facing disruption. Online channels hold 26.3% share in 2025, growing at ~9.3% CAGR, challenging pharmacies at 43.6%, as Unicharm and Kimberly-Clark expand DTC platforms.

Technology Landscape in the Adult Diaper Industry

Superabsorbent Polymer (SAP) Innovation

Superabsorbent polymer (SAP) technology continues advancing toward thinner, high-capacity designs. SAP materials absorb 300 to 1000 times their weight, with some expanding up to 500 times, enabling ultra-thin cores that enhance comfort, discretion, and longer wear duration.

Smart Connectivity and IoT Sensor Integration

Moisture-sensing smart diaper technologies with embedded sensors are moving toward commercial deployment. Clinical studies show accurate detection and improved monitoring, reducing unnecessary changes and enhancing caregiver efficiency, with growing adoption in elderly care settings.

Sustainable Materials Innovation

Sustainability innovation in adult diapers is accelerating, with biodegradable polymers, cellulose absorbent layers, and bamboo-based materials gaining focus. Studies highlight growing development of compostable components to reduce landfill waste, driven by regulatory pressure and sustainability commitments across Europe and developed markets.

Automation and Manufacturing Efficiency

Manufacturers are adopting AI-based computer vision, predictive maintenance, and automated production lines to boost efficiency. Modern lines operate at 800–1,200 diapers per minute, while AI-enabled inspection detects defects in real time, supporting Industry 4.0-driven operational improvements.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Adult Pad Type Diaper |

51.8% |

2025 |

|

Distribution Channel |

Pharmacies |

43.6% |

2025 |

|

Region |

North America |

28.6% |

2025 |

By Type

- Adult Pad Type Diaper (51.8%, 2025): Pad-type products lead the market with a majority 51.8% share in 2025. They are designed to be worn inside regular underwear, offering flexibility and discretion for mild-to-moderate incontinence users . Institutional adoption, nursing homes, hospitals, rehabilitation centers, provides a stable, recurring demand foundation. Pad types benefit from the lowest per-unit cost structure among the three formats.

- Adult Pant Type Diaper (32.4%, 2025): Pant-type adult diapers are growing at ~7.1% CAGR (2026-2034), driven by pull-on designs, 360-degree elastic waistbands, breathable materials, and increasing adoption among active elderly and post-surgical patients.

- Adult Flat Type Diaper (15.8%, 2025): Flat (tape-type) diapers remain critical for bedridden and hospital patients, offering high absorbency and coverage. The segment is expected to grow at ~3.4% CAGR as care shifts toward pant-type products.

To access detailed market analysis, Request Sample

The chart highlights adult pad type Diapers leading with 51.8% share in 2025, driven by institutional demand, while Adult Pant Type holds 32.4% and is projected to grow at ~7.1% CAGR through 2034.

By Distribution Channel

- Pharmacies (43.6%, 2025): Pharmacies lead distribution, supported by healthcare proximity, insurance processing, and trusted guidance. Pharmacist recommendations strongly influence first-time buyers, improving product selection, satisfaction, and continued adoption.

- Online Stores (26.3%, 2025): The fastest-growing channel at ~9.3% CAGR (2026-2034). E-commerce platforms provide discreet purchasing, competitive pricing (15–25% savings vs. pharmacy retail), subscription auto-delivery models, and consumer review-driven product discovery. Global B2C ecommerce revenue is expected to grow to USD$5.5 trillion by 2027 at a steady 14.4% compound annual growth rate.

- Convenience Stores (18.4%, 2025): Convenience and mass retail channels drive value-tier demand, with supermarkets playing key roles in Asia Pacific and Latin America.

- Others (11.7%, 2025): Institutional procurement through medical distributors, hospitals, and government tenders accounts for the remaining share, supported by stable demand from healthcare system procurement budgets.

Pharmacies hold a 43.6% share but are expected to decline as faster-growing online channels expand, with e-commerce projected to exceed 35% of total distribution by 2034.

Regional Market Insights

The adult diaper market varies by demographics, healthcare systems, and income levels. North America leads at 28.6% (2025), followed by Europe 26.4%, Asia Pacific 24.8%, Latin America 11.2%, and MEA 9.0%.

The regional chart shows North America leading at 28.6%, followed by Europe at 26.4% and Asia Pacific at 24.8%. Similar aging trends drive convergence, with Asia Pacific expected to surpass both as China’s population ages and eldercare infrastructure strengthens.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

Major Companies |

|

North America |

28.6% |

82M Americans aged 65+ by 2025 (PRB) and strong home healthcare growth (USD 424B in 2024). |

FDA 21 CFR; CMS coverage expansion for incontinence products. |

Kimberly-Clark, P&G, First Quality, Domtar |

|

Europe |

26.4% |

Aging populations and strong public healthcare support in Germany, France, and Italy. |

EU Single-Use Plastics Directive; CE marking requirements. |

Essity (TENA), Ontex, Paul Hartmann AG |

|

Asia Pacific |

24.8% |

China and Japan lead elderly populations, with Japan 65+ above 29% (2024) and rising incomes. |

Japan LTCI System; China eldercare government policy. |

Unicharm Corp., Hengan International, Kao Corporation |

|

Latin America |

11.2% |

Growing middle class and healthcare awareness in Brazil and Mexico. |

ANVISA (Brazil); COFEPRIS (Mexico) regulatory frameworks. |

Kimberly-Clark LatAm, Ontex, local manufacturers |

|

Middle East & Africa |

9.0% |

Growing institutional care adoption; expanding pharmacy retail in UAE, Saudi Arabia, South Africa. |

GCC-GSO compliance requirements; national health ministry standards. |

Essity, Unicharm, regional private-label manufacturers |

Competitive Landscape

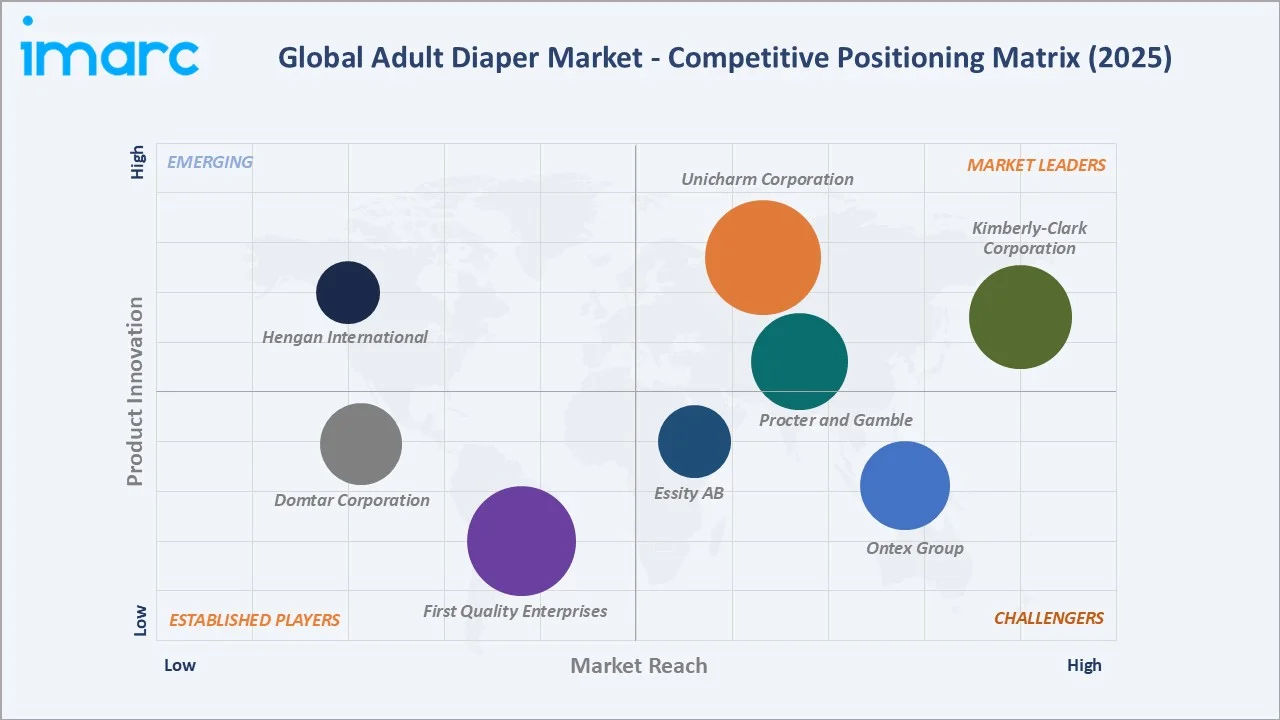

The global adult diaper market is moderately consolidated, with Unicharm, Kimberly-Clark, P&G, Essity, and Ontex holding about 62% share in 2025, while regional players expand in emerging markets.

|

Company |

Brand Name |

Market Position |

Est. Market Share (2025) |

|

Unicharm Corporation |

Lifree |

Market Leader |

~18% |

|

Kimberly-Clark Corporation |

Depend / Poise |

Market Leader |

~17% |

|

Procter & Gamble |

Always Discreet |

Market Leader |

~15% |

|

Essity AB |

TENA |

Challenger |

~14% |

|

Ontex Group |

Ontex / iD Expert |

Challenger |

~8% |

|

First Quality Enterprises |

Prevail |

Established Player |

~6% |

|

Domtar Corporation |

Attends |

Established Player |

~5% |

|

Hengan International |

Anerkang / Elderjoy |

Emerging |

~4% |

The competitive matrix maps players by market share and innovation, with Procter & Gamble leading innovation, while Unicharm and Kimberly-Clark combine strong share with investments in smart and sustainable technologies.

Key Company Profiles

Unicharm Corporation

- Overview: Unicharm is a Japanese personal care corporation headquartered in Tokyo, and one of the world's largest manufacturers of adult diapers, baby diapers, and feminine hygiene products. Annual revenues exceed JPY 950 Billion (~USD 6.5 Billion) in FY2024.

- Key Brands: MamyPoko (baby),Lifree (adult incontinence), Moony.

- Adult Diaper Portfolio: The Lifree portfolio includes pants, pads, and tape-type adult diapers across multiple absorbency levels. The company is also developing smart diaper monitoring solutions and institutional-care focused products for aging populations.

- Strategic Focus: Asia Pacific expansion (China, India, ASEAN), smart diaper R&D commercialization, sustainable material integration, and direct-to-institutional sales capability enhancement.

Kimberly-Clark Corporation

- Overview: Kimberly-Clark is a US-based global personal care company operating in over 175 countries, with annual net sales of approximately USD 20 Billion. The company is a major global leader in adult incontinence and personal hygiene products.

- Key Brands: Depend (adult diapers/pants), Poise (bladder leak protection), Kotex.

- Adult Diaper Portfolio: Depend Real Fit, Depend Fresh Protection, and Depend Night Defense provide light-to-heavy incontinence protection across pad, underwear, and brief formats.

- Strategic Focus: E-commerce channel expansion, sustainable packaging initiatives, growth in gender-specific incontinence solutions, and premium product innovation through absorbency technology improvements.

Procter & Gamble

- Overview: Procter & Gamble is a global consumer goods leader with approximately USD 84.0 Billion in net sales for FY2024. The company entered the adult incontinence category with Always Discreet and has expanded the brand globally.

- Key Brand: Always Discreet premium adult incontinence protection targeted toward active women.

- Strategic Focus: Premium product innovation using advanced absorbent core technology, subscription-based commerce growth, digital marketing expansion, and leveraging feminine hygiene distribution networks in emerging markets.

Essity AB

- Overview: Essity is a Swedish hygiene and health company spun off from SCA in 2017. The company reported net sales of approximately SEK 146 Billion (~USD 13.8-14 Billion) in 2024, with strong performance in incontinence products. TENA remains one of the most recognized adult incontinence brands globally.

- Key Brand: TENA , available in over 90 countries globally, offering pants, pads, briefs, and institutional healthcare solutions for both retail and professional healthcare settings.

- Strategic Focus: Sustainable product innovation (TENA ProSkin), digital health-enabled incontinence management, professional healthcare channel expansion, and circular economy initiatives.

Market Concentration Analysis

The adult diaper market is moderately concentrated, with Unicharm, Kimberly-Clark, P&G, Essity, and Ontex accounting for ~62% of global revenue in 2025. The top three - Unicharm, Kimberly-Clark, and P&G - hold about 50% share, supported by scale, strong brand equity, and extensive retail distribution.

Market fragmentation remains high in Asia Pacific and Latin America, with regional and private-label players competing on price. Essity acquisitions and Ontex expansion highlight consolidation, while rising online private-label penetration increases competitive pressure on premium brands.

Investment & Growth Opportunities

Fastest-Growing Segments

- Adult Pant Type Diapers (~7.1% CAGR, 2026-2034): Pull-on format innovation catering to active, independent users is the highest-growth product investment opportunity within the type segmentation.

- Online Distribution (~9.3% CAGR, 2026-2034): Investment in direct-to-consumer e-commerce platforms, healthcare subscription services, and digital marketing capabilities represents the highest-CAGR channel opportunity.

Emerging Market Opportunities

- Asia Pacific Rural Markets: China's government-funded community eldercare expansion and India's growing middle class present multi-billion-dollar underpenetrated market opportunities for both branded and value-tier adult diaper products.

- Middle East & Africa: GCC government healthcare spending increases and a growing professional population are creating demand for premium adult incontinence products in UAE, Saudi Arabia, and Qatar.

Technology Investment Opportunities

- Smart diaper sensor technology commercialization: IoT-enabled incontinence monitoring systems targeting nursing home chains and home healthcare providers represent a high-margin adjacency opportunity for technology-enabled manufacturers.

- Biodegradable and eco-certified product lines: Premium-priced sustainable adult diapers targeting environmentally conscious consumers in North America and Europe offer attractive margin expansion potential.

- Digital incontinence management platforms: Apps integrating product recommendations, pelvic floor exercise programs, and telemedicine incontinence consultations are attracting healthcare technology venture capital.

Future Market Outlook (2026-2034)

The global adult diaper market is expected to grow at a 5.80% CAGR, reaching USD 37.4 Billion by 2034. Growth will be driven by aging populations, product innovation, and online distribution expansion. Online channels may exceed 35% share by 2034 from 26.3% in 2025, while pant-type diapers approach parity with pad-type products.

Asia Pacific is projected to emerge as the world's largest regional market by approximately 2031–2032, driven by China's rapid institutional eldercare infrastructure development and the aging of its post-1960 baby boom cohort. Smart diaper technology, currently at pilot stage in Japan and select. Late-decade commercial scale deployment (late 2020s) instead of 2028–2030 confirmed timeline.

Research Methodology

Primary Research

IMARC Group conducts primary interviews with executives, healthcare professionals, and distributors across the United States, Germany, Japan, China, and Brazil, with primary research contributing 35–40% of total data inputs.

Secondary Research

Secondary sources include FDA, EMA, MHLW, NHS databases, EDANA publications, company annual reports, regulatory filings, trade publications, and peer-reviewed literature on incontinence prevalence and management.

Forecasting Models

Market estimates use bottom-up and top-down approaches, validated with historical data, primary research, and demographic projections from UN, WHO, and national agencies, with CAGR scenario-tested.

Adult Diaper Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Adult Pad Type Diaper, Adult Flat Type Diaper, Adult Pant Type Diaper |

| Distribution Channels Covered | Pharmacies, Convenience Stores, Online Stores, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Unicharm Corporation, Kimberly-Clark Corporation, Procter & Gamble, Essity AB, Ontex Group, First Quality Enterprises, Domtar Corporation, Hengan International |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the adult diaper market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global adult diaper market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the adult diaper industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Adult Diaper Market Report

The global adult diaper market was valued at USD 21.9 Billion in 2025 and is projected to reach USD 37.4 Billion by 2034at a CAGR of 5.80%.

The adult diaper market is projected to grow at a CAGR of 5.80% during 2026-2034, driven by demographic aging, product innovation, and expanding healthcare services.

North America dominates with 28.6% of global revenue in 2025, supported by 82 million Americans aged 65+ and a robust home healthcare sector valued at USD 424.0 Billion.

Adult pad type diaper holds the largest share at 51.8% in 2025, favored for institutional use in hospitals, nursing homes, and homecare settings.

Online stores is the fastest-growing distribution channel at ~9.3% CAGR (2026-2034), while Adult Pant Type Diapers lead type-segment growth at ~7.1% CAGR.

Key drivers include a growing global geriatric population, rising incontinence prevalence, product design advancements, expanding homecare services, and increasing e-commerce penetration worldwide.

Leading companies include Unicharm Corporation, Kimberly-Clark Corporation, Procter & Gamble, Essity AB, Ontex Group, First Quality Enterprises, Domtar Corporation, and Hengan International.

Online stores hold 26.3% share in 2025 and are growing at ~9.3% CAGR, offering discreet purchasing, subscription delivery models, and competitive pricing versus pharmacy retail.

Adult Pant Type Diapers account for 32.4% of the global adult diaper market in 2025and are growing fastest among type segments at approximately 7.1% CAGR through 2034.

The adult diaper market is forecast to reach USD 37.4 Billion by 2034, up from USD 21.9 Billion in 2025, reflecting consistent 5.80% annual compound growth driven by global aging and innovation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)